Execute the following steps to implement the CAPM in Python.

- Import the libraries:

import pandas as pd

import yfinance as yf

import statsmodels.api as sm

- Specify the risky asset and the time horizon:

RISKY_ASSET = 'AMZN'

MARKET_BENCHMARK = '^GSPC'

START_DATE = '2014-01-01'

END_DATE = '2018-12-31'

- Download the necessary data from Yahoo Finance:

df = yf.download([RISKY_ASSET, MARKET_BENCHMARK],

start=START_DATE,

end=END_DATE,

adjusted=True,

progress=False)

- Resample to monthly data and calculate the simple returns:

X = df['Adj Close'].rename(columns={RISKY_ASSET: 'asset',

MARKET_BENCHMARK: 'market'})

.resample('M')

.last()

.pct_change()

.dropna()

- Calculate beta using the covariance approach:

covariance = X.cov().iloc[0,1]

benchmark_variance = X.market.var()

beta = covariance / benchmark_variance

The result of the code is beta = 1.6709.

- Prepare the input and estimate the CAPM as a linear regression:

y = X.pop('asset')

X = sm.add_constant(X)

capm_model = sm.OLS(y, X).fit()

print(capm_model.summary())

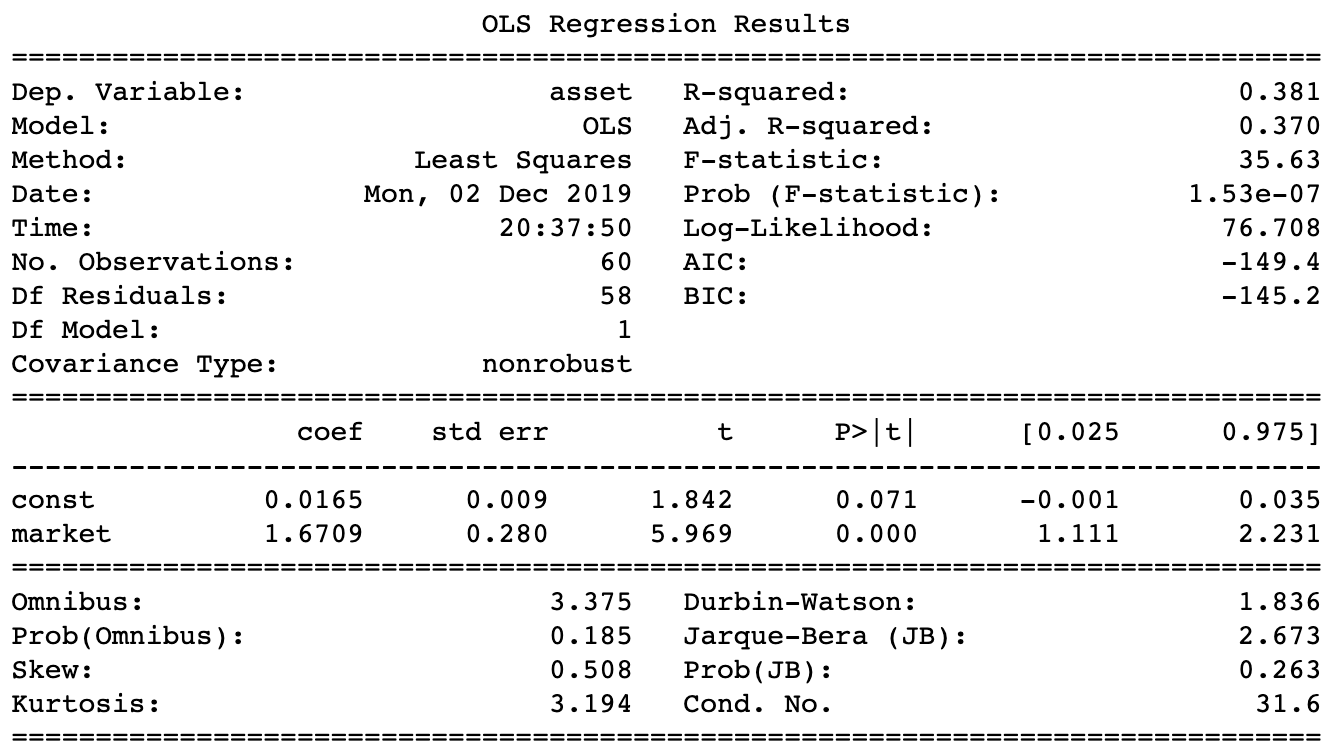

The following image shows the results of estimating the CAPM model:

These results indicate that the beta (denoted as market here) is equal to 1.67, which means that Amazon's returns are 67% more volatile than the market (proxied by S&P 500). The value of the intercept is relatively small and statistically insignificant at the 5% significance level.