Execute the following steps to estimate the CCC-GARCH model in Python.

- Import the libraries:

import pandas as pd

import yfinance as yf

from arch import arch_model

- Specify the risky assets and the time horizon:

RISKY_ASSETS = ['GOOG', 'MSFT', 'AAPL']

N = len(RISKY_ASSETS)

START_DATE = '2015-01-01'

END_DATE = '2018-12-31'

- Download data from Yahoo Finance:

df = yf.download(RISKY_ASSETS,

start=START_DATE,

end=END_DATE,

adjusted=True)

- Calculate daily returns:

returns = 100 * df['Adj Close'].pct_change().dropna()

returns.plot(subplots=True,

title=f'Stock returns: {START_DATE} - {END_DATE}');

This results in the plot shown below:

- Define lists for storing objects:

coeffs = []

cond_vol = []

std_resids = []

models = []

- Estimate the univariate GARCH models:

for asset in returns.columns:

model = arch_model(returns[asset], mean='Constant',

vol='GARCH', p=1, o=0,

q=1).fit(update_freq=0, disp='off')

coeffs.append(model.params)

cond_vol.append(model.conditional_volatility)

std_resids.append(model.resid / model.conditional_volatility)

models.append(model)

- Store the results in DataFrames:

coeffs_df = pd.DataFrame(coeffs, index=returns.columns)

cond_vol_df = pd.DataFrame(cond_vol).transpose()

.set_axis(returns.columns,

axis='columns',

inplace=False)

std_resids_df = pd.DataFrame(std_resids).transpose()

.set_axis(returns.columns,

axis='columns',

inplace=False)

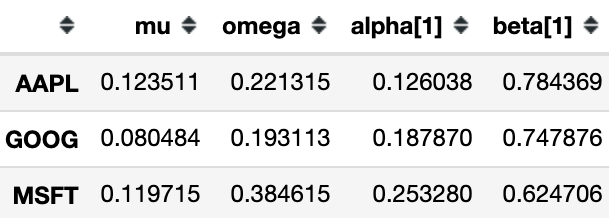

The following image shows a table containing the estimated coefficients for each series:

- Calculate the constant conditional correlation matrix (R):

R = std_resids_df.transpose()

.dot(std_resids_df)

.div(len(std_resids_df))

- Calculate the one-step-ahead forecast of the conditional covariance matrix:

diag = []

D = np.zeros((N, N))

for model in models:

diag.append(model.forecast(horizon=1).variance.values[-1][0])

diag = np.sqrt(np.array(diag))

np.fill_diagonal(D, diag)

H = np.matmul(np.matmul(D, R.values), D)

The end result is:

array([[6.98457361, 3.26885359, 3.73865239],

[3.26885359, 6.15816116, 4.47315426],

[3.73865239, 4.47315426, 7.51632679]])

We can compare this matrix to the one obtained using a more complex DCC-GARCH model, which we cover in the next recipe.