Chapter 14

Business Development

Introductions

“Everyone wants to live on top of the mountain, but all the happiness and growth occurs while you're climbing it.”

—Andy Rooney

Let me start with the good news, of the 300,000 advisors in the United States, the majority are not actively prospecting. A small percentage have a business development process, and even a smaller percentage are rainmakers that can produce significant asset growth on a consistent basis. The bad news is the fact that clients have many more choices and access to any information at their fingertips. Therefore being casual about business development is a waste of time and will only lead to frustration. Become committed to the art and science of growing the business, but only if that's truly what you are committed to. The most important aspect of developing your business in an efficient and effective way is asking for introductions. But before you start to initiate a referral campaign, get your house in order. Because if your clients are not satisfied it will only result in disappointment. On the other hand it could serve as a wakeup call. It doesn't matter if you're just starting out or a 30‐year industry veteran. About 60 percent of new business comes from referrals. That's an average; for some advisors it's 95 percent, for some it's 10 percent, and for others it's zero. I firmly believe introductions need to be a key component of business strategy, part of your culture and part of who you are. Based on my research, the following are the top five ways to focus on business development: introductions, strategic alliances, COIs and networking, target marketing programs, and client events.

Here is the myth of business development: if I'm really smart and provide great service, my business will grow naturally. As you know by now, I have met thousands of advisors over the years and that's simply not true. This business doesn't reward you for just being smart; there are lots of very smart people on Wall Street. The business or clients for that matter don't care how smart you are until you turn that body of knowledge into action. I have hired PhDs who failed quickly because they tried to outsmart the process of building a business. Business development rewards people who can execute, who are doers, and who are masters at networking. It rewards those that take some risks by trying new methods of growing their book. Most of all they persevere.

If you're thinking as an owner, you're always thinking about growing the business, not just managing the business. Growing the business means a commitment of time and resources.

There are a number of high‐payoff activities you can facilitate to strengthen your client base and keep growing your business. These include:

- Hosting client events

- Arranging introductions

- Strategic networking

- Talking to clients/prospects

- Meeting with partners frequently

- Holding face‐to‐face reviews with clients/prospects

The following nine attributes make a rainmaker:

- Self‐confidence. A champion fails, but gets back up.

- Great communicator and collaborator. Rainmakers ask great questions.

- Lives in the world of possibilities, not limitations. They have a purpose and are motivated.

- Takes full responsibility versus being a victim. They set business goals and activities and track progress.

- High likability index. Humility attracts people.

- They are competitive, they like to win. They are always prospering and networking.

- They know what they don't know.

- Relentless about details and follow‐up. They have a sense of urgency. They know how to manage their time effectively and they don't get caught up in the noise.

- They are passionate and curious of the world around them. They are lifelong learners.

Step One: Self‐Confidence

If you believe that by asking for introductions you will diminish your brand, or that it somehow makes you come across desperate, all I can do is urge you to reconsider your position. Is your hesitancy to ask for introductions truly for those reasons, or is it more of a matter of feeling shy and uncomfortable at the thought of doing it? If so, ask yourself whether you have the desire to grow your business, the vision, and the model to offer success to potential clients. If the answer is yes, you can't provide those services by waiting for clients to come to you. If you have confidence in your abilities, it should not be hard to ask for an introduction. With a healthy sense of confidence, it doesn't matter as much when you get rejected—because there will be rejection—it matters more that you have built the appropriate mental momentum that nothing gets in the way. Plus, top advisors don't take rejection personally.

Just as I used to talk to myself before a football game, I do so now before I go on stage for a presentation as a way to build up my confidence. Everything starts and ends with confidence. In our business we become masters of hiding and compartmentalizing our feelings; therefore, it is harder to notice when someone lacks confidence. We don't ask for introductions because we lack confidence, not because it's hard work. It's a simple concept, but it's not always easy to execute. You just have to embrace the motto, “Sometimes you win; sometimes you lose.” But if you don't play the game, I guarantee you will never win.

Step Two: Get Your House in Order

Introductions happen naturally when your house is in order, when you have the right people in the right roles delivering a fantastic client experience. This creates loyal and happy clients. In turn, you feel comfortable asking these clients for introductions and, even better, they are more likely to make an introduction without asking. How do you know your clients are happy? The most obvious way is when they transfer more assets to you. People vote with their feet.

But we also can't operate under the old adage, “No news is good news.” We can't rest on our laurels and assume that because a client hasn't expressed dissatisfaction they are happy with your services. It's essential to ask your clients at least once a year how you can better serve them. You want to know what you're doing right, what you're doing wrong, and what you and your team can do better. Most people use a one‐page survey, and that can have some benefit, but I recommend a face‐to‐face meeting with your best clients so that you can ask them directly. Have a meaningful conversation and take notes. You need to make sure that your clients value your services before you just start asking for introductions. Nothing could be worse than asking a client to make an introduction only to be told no because the client hasn't been happy with what you've been doing and is considering changing advisors.

Success breeds more success. In other words, stack the deck in your favor right out of the gate. The foundation is simple: you don't have the right to ask for anything unless you have made enough emotional deposits and you're meeting or exceeding the client's expectations. Ultimately, only a small percentage of your clients will go out of their way to introduce you to their friends and family unsolicited. Most clients will not initiate an introduction for a number of reasons:

- The client may think you're too busy to take on more clients.

- Clients may think if they make an introduction, they will lose their privacy.

- The client may not know how to properly introduce you and all the services you provide.

Research I have seen over the last 30 years indicates that 80 percent of clients are never asked for an introduction. They also go on to say that if they were asked, 77 percent would give one. A great way to start getting your business on the right track is to create a client advisory board, made up of 8 to 10 clients who meet over dinner twice a year. Their job is to provide open feedback on ways to improve your services.

Step Three: Reciprocity

Reciprocity has been around since the beginning of time, yet people in our business can't seem to employ it effectively in the interest of creating the best outcome for you and the client. Every deal needs to be a win‐win and the person with the best leverage has the upper hand. In the end, I want my client to say, “You are irreplaceable.” I want clients to be so happy with our relationship that when I do ask for an introduction, it will not feel like I'm “asking,” but rather I'm “offering.” That's a big difference. Asking can come across like it's only a deal for you and that it's all about you and the growth of your business. When you have the mindset that you're offering to help one of their friends, it feels different. If you believe in your value so strongly, you naturally offer your services because you believe others will be in better hands by working with you.

Teach your clients how to introduce you. They are busy and they don't need another thing to do, so make it easy for them. Once you know they are willing to introduce you, give them a very short one‐pager that tells them:

- Who you are

- What you do

- What makes you different

Plant the seed from the very start, at the initial discovery meeting. Part of that meeting should include time for you to share how you built the business and how your business continues to grow. It can end with a statement about always being grateful for referrals. For example, you might say, “Robert and Mary, it's been a pleasure meeting you today and we feel confident that we can meet your expectations. Our goal, however, is to exceed your expectations because our business is built on referrals. We always welcome an introduction if our services meet and exceed your expectations, and our goal is to do that every day, it's not to push product.”

Of course, say it in your own way, but stating something like this does a few key things. First, it lets clients know that you and your team are motivated to do a great job for them because that's how your business grows; second, you're informing the client that you encourage and appreciate an introduction; and third, you are being completely transparent about your business. Remember, it only feels like begging if you're not adding value to the client's experience. In return, when you feel confident that you're delivering an outstanding client experience, you feel like a champion.

Step Four: Motivation

Why would someone go out of her way to help you? Well, maybe your client is going out of her way to help a friend. The client is convinced that her friend would be better off in your hands or she is trying to do a favor for someone she cares about. It's your job to understand and get into your client's head to see what motivates them. Needs and recognition can be a powerful motivator. If someone makes an introduction, you had better make a really big deal of it. Most people will call the client and say thank you. That's not a big deal. It's the very least you can do. It's important to make the client who made the introduction feel like a super VIP:

- Absolutely call and say thank you. And remind the client again that you honor privacy and never discuss other people's matters with anyone.

- Send the client a small gift (under $30) of thanks with a handwritten note.

- Take the client out to lunch or dinner.

- Thank the client again a few weeks or months later and tell him or her how much you appreciated the introduction and how much you enjoy working with the new clients.

- Never discuss the confidentiality with one client to another.

How to Ask for Introductions

How did you learn to ride a bike? It took practice and persistence most likely. Learn how to ask for introductions by starting to ask for introductions. It may feel awkward in the beginning and you may hear “no,” but the more you ask, the more you learn, the better you get, and the more yeses you begin to hear. Finessing the way you ask takes practice. If you do it like most—wing it—it shows. Develop a style that speaks to your brand. Remember, it's how you frame the request. Choose your words carefully. But, most importantly, keep it simple. Being yourself is key. Be transparent.

“John, you told me how much you enjoy working with our team and how you are very satisfied with the level of services. Do you still feel that way?” Once John responds with “Yes,” you continue. “First, I want to say thank you for placing your trust in us. It's a pleasure working with you and we all appreciate your business. We know we have to earn your trust every day. The reason I asked the first question is because I would like to continue to grow my business with more people like you. Can I help you think of some people who may want a second opinion about their portfolio?”

In the end, growing your business with a focus on introductions is the most efficient and effective tool in your box.

Developing Advocates

In addition to becoming a trusted advisor to your clients, it's beneficial to cultivate a special group of clients for yourself, ones I call advocates. Developing advocates is based on the approach that it is better to have fewer accounts of higher quality with more assets than a large number of lower quality accounts with fewer assets. About one hundred relationships is the right number for many advisors.

Client advocates are ones who trust and believe strongly enough in you that they go out of their way to refer business to you. They can give you access to a network of people with significant assets to invest.

Obviously, developing advocates means building relationships. Those relationships have to be genuine, which is not so easy because it takes time. These clients have to genuinely like you and you have to genuinely like them. There has to be chemistry and trust. You can find people who want to help you grow your business, but only if they truly value what you are all about—your whole makeup. At some point, it becomes hard to separate advocates from friends.

Your baseline for developing advocates is making sure you are serving them to the best of your ability and that you are competent in their eyes. While you should survey all your clients, your advocate development campaign will be based on selecting good clients whose opinions and judgment you respect.

The second part of the process is more personal: spending quality time with clients outside the office and getting to know them on a more personal level. I do it by going to dinner, to a sporting event, and so forth.

Some clients will turn into advocates on their own, without prodding. With others, you have to ask. “Bob, I know you have placed trust in our team to manage all of your wealth management needs. That level of trust means a lot to me. You're an influential person with friends who could probably use our services and if there's any way you could help, I would appreciate it.”

Since advocates are clients, you must continue to maintain high levels of communication with them. Ask them to be candid with you: “If you think I'm doing something that's not consistent with what I'm trying to achieve, I would hope that you would tell me—not just when I ask, but any time. Pick up the phone and let me know, ‘Your sales assistant has dropped the ball,’ or ‘Your firm is doing something I don't like.’ ” Five to ten advocates with major spheres of influence can have a major impact on your business.

Community Engagement and Networking

Community involvement can be another form of networking—a very effective one—but it has to be done even more unselfishly than networking as community service and charity work is about doing something from the heart, for the good of your community.

I believe many people don't get involved because the world's problems seem too big for a single person to have an effect. You don't have to change the world; you only have to change one person as the saying goes. Try devoting four or five hours a week to charity. Find something you enjoy and that allows you to make a difference. It will enrich your life more than any material object can.

It's also an opportunity to make business contacts, although it's the least important reason to do it. If you volunteer at a nonprofit for your own business purposes, it won't happen and you will waste your time. Think with your heart when you are thinking about an organization you might want to be involved with. Over time, you will find yourself developing long‐term win‐win relationships with other volunteers. You will also find yourself surrounded by good people—people who actually do good as opposed to people who just talk about doing good.

You can get involved with cultural organizations, fundraising activities, the Chamber of Commerce, athletic associations, colleges, your local high school, homeowners' associations, sporting events, art shows, hospitals, and more. The list is endless. You will learn how other people live, experience new environments, and pick up useful new skills. Depending on the organization to which you offer your time, even some of your professional skills may be useful to the organization. Ultimately, you will gain new insights into yourself, which only increases your self‐awareness.

In terms of making community involvement work for your business, the key is to get active and be visible immediately. While not everyone in each area of exposure is a prospect, you can quickly build a sphere of influence that can be expanded over time.

As I've said before, you can't hide your character, so it is important to get involved for the right reasons. Give back without looking for paybacks.

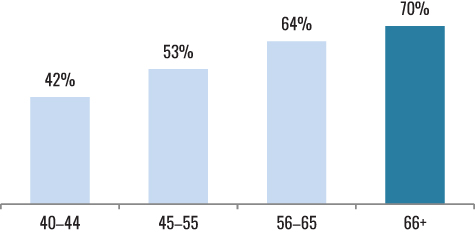

Percentage Willing to Refer by Age Group

Source: McKinsey

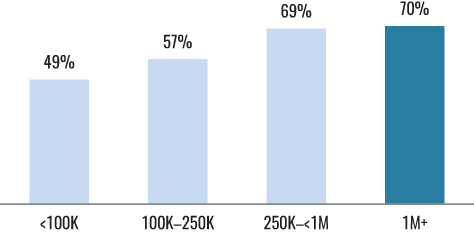

Percentage Willing to Refer by Affluence

Source: McKinsey

Present a Successful Seminar

Leading or presenting in professional seminars can be an effective way to attract clients and grow your business. But, it takes a lot of hard work, a solid process, and you can't just do one and done. Hold a seminar once every month and focus on quality of attendees, not quantity. Having 20 people attend is fine if they know that for them to be a client they need at least $1 million of investable assets. Also, if public speaking is not your strength, bring in an outside speaker. Think about a partnership with an accounting firm or a group that gets together already and you become a guest speaker. I talked about my tips on public speaking in Part One of the book. Here are my tips for creating a successful seminar.

- Make sure your presentation works before you use it on a crowd. Ask a friend—one who will be honest with you—to critique you.

- Rehearsing is very important. Recite your entire presentation at least three times before the day of the seminar. Don't wing it.

- Carefully target your invitations.

- Make the seminar short, direct, and easy to understand.

- Remember that it's not just what you say, it's how you say it. (Be a crowd pleaser.) If you speak technical industry jargon in a monotone voice, your prospects will drift away.

- The most important thing is to connect with the audience. Pick out individuals and make eye contact with them for three to four seconds at a time. Make sure to do this for every person in attendance.

- Get immediate feedback by asking attendees to fill out a confidential questionnaire. The only way to get better is to ask how you did!

- Follow up. Send out notes thanking them for attending and invite them to call you if they have any questions or want to discuss their situations. Put them on your mailing list for newsletters.

If you are truly committed to business development, focus on buying assets. Buying a book can take a long time to find the right fit and valuation.

Social Media

Although the financial industry has been late to adopt it, the value of social media is finally starting to sink in. From RIA firms to the larger wirehouses, financial institutions are looking to harness the power of social media now more than ever. They are becoming more and more comfortable with the regulations and starting to really get the concept of social media and how it can be used for business.

Courtney McQuade is an expert in financial technology and social media, with a specific focus on marketing and sales strategy. Over the past 18 years, she has worked at startups, hedge funds, private equity firms, and several of Wall Street's largest banks. I met Courtney in New York City about 15 years ago while we were both working at Prudential Securities. We reconnected a few years ago on—where else—LinkedIn. I recently caught up with her and asked about some of the trends she's seeing and why it's so important for advisors to include social media in their strategy.

Rick: Social media, to a lot of people, still seems like just a platform for fun. How can it actually tie into an advisor's business strategy?

Courtney: That's a very common question I get, Rick. You've heard the old cliché, “life is sales.” You could be an amazing attorney, personal trainer, and so on, but if you don't know how to market yourself, to sell yourself, no one is ever going to know how good you are and want your services. Social media is the perfect place to prove yourself as a thought leader in your industry. Post content your clients and prospects want to know about, want to learn, breaking down the latest news in the market in a way they can easily digest and understand. Show that you have a real finger on the pulse of what's happening and how it applies it to their needs.

In a joint study by Cognet Research and LinkedIn, “Nearly two in five of the mass affluent use social media for discovery or consideration of financial companies, products, policies, or accounts (36%); among mass affluent who use social media for both purposes, nearly two in three (63%) take action as a result of what they learn.”

It's also the perfect platform to build your personal brand and connect with people; not just to show that you know what you're doing, but to show the kind of person you are, what interests you have, humanizing yourself. I always tell my clients, “People like to do business with people, not companies—show them who you are as a person.” If you like to cook, travel, sew, volunteer, whatever you're passionate about, share some of this on social media. Your clients and potential clients will enjoy seeing the human side of you—the mother, the father, the artist, the philanthropist, someone who might have something in common with them. Social media is the perfect place to form bonds with clients and prospects.

Rick: Quite a few advisors seem to feel uncomfortable posting things about themselves, even if it's purely professional; is this something you see as well?

Courtney: For sure. Different generations have different feelings related to posting things about themselves on social media—some tend to feel like it's bragging and I totally understand that. To the millennial generation it's normal to post your life experiences and/or knowledge online, to share your personal thoughts and feelings. But to the baby boomer generation, and even the generations in between, it might feel weird, awkward, invasive, or like bragging.

But we now live in an information age. One thing I think we all can agree on is that people now do all their research online. (Although I still enjoy a paper copy of Barron’s in my hands on Sundays.) It can definitely take some getting used to, so I always tell my advisors to start small with just one or two LinkedIn posts a week, to start getting comfortable with it. Follow other companies and thought leaders in our industry on LinkedIn and try to incorporate just 10 to 15 minutes a day, reading through your LinkedIn Home feed, the same way you'd read through the Wall Street Journal or Bloomberg newsfeed.

A lot of advisors already are getting comfortable with it. An internal study done last year at Morgan Stanley showed that 46% of its advisors who use social media used it to connect with their clients' children and grandchildren. And 57% reported bringing in new assets through their social media engagement.

Rick: So, basically, if an advisor is not currently using LinkedIn, he might be losing out to the advisors who are.

Courtney: That's exactly right, Rick. Every day you're not active on LinkedIn is a missed opportunity to connect with prospects, reinforce your value to clients, and build your credibility as a forward‐looking investment expert. You may also be losing mindshare to competitors who have invested the time and thought that it takes to establish a strong social media presence. Social media is now one of the leading forms of communication. It is how we connect with one another, and it is how we research the companies we are considering doing business with. No longer is a company's website enough to gain credibility; people want to see what advisors have to say and how much they know. Now, businesses are translating this knowledge through social media.

Not to mention, by default, a LinkedIn profile is your professional online identity. If a potential client Googles you, it will most likely be their first stop to learn more about you.

Rick: LinkedIn seems like the obvious platform all advisors should be using, but what about Facebook?

Courtney: I hear a lot of advisors now talking about taking a “holistic approach” to investment planning with their clients, which means not just taking their net worth and allocating it into the appropriate investment vehicles; it means taking into account their lifestyle, their passions, specific family dynamics, and more. A few years ago, Facebook would not have been recommended as a good business platform for our industry. But now advisors are starting to connect with their clients through Facebook and although they may not be posting industry knowledge or opinions on the platform, they are using it to keep that personal relationship by sharing family photos and major life events. And in turn they can see when their clients are posting vacation photos, retirement party photos, and other life events. They can use Facebook as talking points in client meetings and/or as indicators for the time to contact their clients.

Now, as an advisor, if you do choose to use your personal Facebook to connect with clients, because historically it has been so very personal, you might want to tone down some of your posts and potentially go back in your Timeline and clean up a little, depending on your past posting style.

“Success consists of going from failure to failure without loss of enthusiasm.”

—Winston Churchill

Think Like an Owner and Invest in Your Business

Successful advisors believe so strongly in their own future that they are willing to ante up now. They know every dollar put back into their business will produce sustainable growth in the future. This principle doesn't just apply to larger practices with staffs of 10 or more, but to a solo practitioner who recognizes that having his or her own assistant, for instance, would create tremendous advantages. This is about taking personal responsibility for the rate of growth one chooses and then making it happen. Proven strategies of investing back into the business are the following; human capital, technology, business development, marketing, or buying assets.

Investing back into the business means different things to different advisors. It could mean a comprehensive targeted marketing campaign or buying another wealth manager's book of business. If you aren't reinvesting in your business, then you are underestimating, undervaluing, and underrating your business, your team, your firm, and, of course, yourself. Are you a growth stock? Would you invest in your stock?

Of course, investing back into your business for the wirehouse advisor will come with a different set of priorities than those for the RIA advisor. For the RIA, it's about creating scale; for many, it's breaking the $1 billion mark while for others it's $10 billion. Therefore, investing back into the business is all based on where you are now. The larger RIAs or IBDs focus on providing the best technology possible and they focus on acquisitions, marketing, and the right level of client support to achieve an outstanding client experience. Business development is one area where allocation of resources will be paramount.