Chapter 22

What's Your Number?

“Nature does not hurry, yet everything is accomplished.”

—Lao Tzu

Everyone has a number and that number for many people, including the advisor, can control one's ability to live a balanced life. In this case, I'm referring to your client's number. What's your number? Wall Street spends hundreds of millions of dollars helping clients answer that question. Fintech firms with retirement‐planning software can produce a document informing clients how much money they will need for retirement or what their shortfall may be. All these financial tools are terrific, except these plans are stagnant, and life is anything but. Life happens and circumstances change. The right plan needs to be developed with the advisor navigating the journey and with the client's complete collaboration.

The best way to answer the question, “What's your number?,” is to look back at some of the great thinkers like Plato, Aristotle, and Seneca. Some advisors say the first step starts with a financial plan, but that's really the second step in the process. The first step is to follow this simple formula: Be + Do = Have. The first time I heard this was in 1989 when I attended a two‐day workshop on growing my business. As a young advisor, everything that came out of Bob Dunwoody's mouth I made sure to write down. Bob's workshop was by far the most impactful workshop in my life. We became friends and he went on to mentor me. So, the first step is to answer the question: Whom do you want to be? In other words, what's your vision? Who are you? What's your destination? Once you know the answer to these questions, you can start doing the activities that will make you whom you want to be. These actions will result in having what you want.

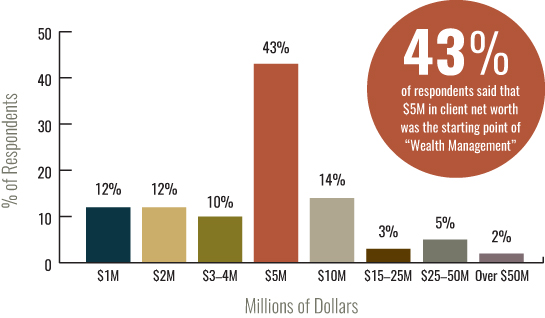

What do people need in order to feel that they are wealthy? By far, as the graph shows, most people believe $5 million is necessary in order to truly feel as if they are wealthy.

Starting Point of Wealth Management

Source: Barron's

It makes perfect sense when you think about it. Before people reach their goals they have to create a vision. So, if you're an advisor who wants to double your business, you first have to start with being that $2 million producer now, and follow it up with the actions and tactics of what it takes to be a $2 million producer. Then you will have the success you are seeking. In the case of the client, helping them with the number is helping them understand where they are in terms of their financial goals (Be) and what adjustments they need to make today to move in the directions of their goals (Do) in order to achieve their intended goal (Have). This simple philosophy has been around over 2,300 years. Socrates said, “To do is to be”; Plato said, “To be is to do”; Descartes said, “I think, therefore I am”; and the Christian Bible states, “As a man thinketh, so shall he be.” Each of these great philosophers arrived at the same conclusion. When we think of wealth management, we primarily think about the future, but I suggest looking at the past as well. Ultimately, it's about determining the client's number based on knowing who they are (be). Everything starts with the vision.

Comfortable means something different to every client. That's why the number of what you will need is very different from one person to another. People are never all the same. As advisors creating the right balance of communication, the number is very important. Let's say, for example, a client's target retirement number has a $2 million shortfall. Advisors who focus solely on that number create more anxiety for the client. They may offer suggestions to work longer, save more, or get more aggressive in the market. But if we are truly holistic, we have to look at the other side of the balance sheet. Do you really need a house that big? Do you need to live where you're living? Do you need three cars? Do you need the second home? You get the picture. The conversation should not be centered around the actual number; rather it should be about helping your clients discover what's truly important and helping them find meaning and purpose. Helping clients get to the core of what brings them happiness in their lives is what will differentiate you from every other advisor.

A comfortable retirement for some is being able to travel the world on a regular basis. To someone else, it's being able to travel in first class and staying at the finest accommodations. To others, it's being able to do all that with the luxury of their own private plane. For some, it's having a $100,000 cash flow while for others it may be $1 million. As I said, according to Barron's, $5 million is where 43 percent of high‐net‐worth individuals feel rich. For others, $2 million will be just fine, and for others $25 million will not be enough. Many high‐net‐worth individuals have made a conscious effort to retire. They are staying active much longer and are enjoying the journey.

For most high‐net‐worth individuals, having a trusted advisor is invaluable. If you are a high‐net‐worth person and have a trusted advisor, hold onto him or her because she will provide peace of mind. If you're not sure, you may want to look for someone else. As a client, you should never settle when it comes to your future. Look for the right fit for you and your family. Look for someone who can look at your entire financial picture. Your trusted advisor should work with you in a very collaborative way, not dictating what you need. Ultimately, you are the leader and the advisor's job is to inform you, empower you, and help you get to your destination.

High‐net‐worth clients want:

- Fee transparency

- Good advice (investment performance based on achieving their goals)

- Understanding of concerns and needs (risk)

- Quick and effective resolution of service‐related issues

Regardless of what your client's number is, a top advisor will help a high‐net‐worth individual focus on the four most important areas and deal with the challenges that come with them: market volatility, spending behaviors, taxes and inflation, and longevity.

Market Volatility

Why is it so important to discuss market volatility? People in general are highly emotional about their money. A client's belief system about the market can have a major impact on how she invests and how she reacts to market cycles. Volatility can be heart wrenching; I have seen my share of volatility over the past 34 years. But more importantly, I have seen how clients and advisors react in the middle of the storm. Helping clients deal with volatility does two things: one is to ride out the storm versus jumping out for cover like some people did during the financial crisis of 2007–2009 when the S&P 500 lost approximately 50 percent of its value. The second result in helping clients weather volatility is being appropriately allocated in equities in order for the portfolio to maintain purchasing power. The prolific and highly respected Jeremy Siegel, a professor at the Wharton School of Business, has always been a bull. I've had the opportunity to hear him speak on many occasions, and his enthusiasm about the market and his convictions are very powerful. His famous book, Stocks for the Long Run, was first released in 1994, and the fifth edition was released in 2014. In the book, covering a span of more than two centuries, he shows that the total real return of stocks after inflation is 6.7 percent compared to U.S. government bonds' return of 3.6 percent or gold's return of 0.6 percent. Having history as our guide, we have 200 years of volatility and meltdowns, but for the long‐term investor, being invested in stocks with a well‐diversified portfolio serves them well. The financial collapse that took place in 2008 was more of an aberration than the norm, but history had shown us what can happen when you have irrational exuberance. The Internet has made it easy for individuals, many of whom lack the proper knowledge and expertise, to buy and sell stocks. With a handheld smartphone you can execute a trade in seconds. Investing is a serious and long‐term disciplined process. It's not about hunches, entertainment, or gambling. That's why a trusted advisor can make all the difference and provide a customize roadmap for each relationship.

Spending Behaviors

Let's be honest, many of us are materialistic; it's just a matter of to what degree. All we need to do is look in our closets, what percentage of our clothes do we really use? By definition this means being excessively concerned with physical comforts or the acquisition of wealth and material possessions, rather than with spiritual, intellectual, or cultural values. In the past, I saw books only on creating wealth as the key to happiness. Now I'm seeing books, information, and documentaries that focus more on flexibility, thrift, and a life balance and abundance. I hope this means a growing number of the next generation may have more perspective on balance. But, we are still attracted to things we don't need. We all know we own too much stuff. According to the LA Times, there are 300,000 items in the average American home. That's hard to believe, but even if it's a quarter of that, it's still a lot. The Telegraph reported on a British research study that found that the average 10‐year‐old owns 238 toys but plays with just 12 daily. Clients always tell us that they want to simplify their lives. They want to be organized and have more free time. Helping them reach a more satisfying state is a definite value add in my book. Because at the end it doesn't matter how much people have accumulated; if they don't have a well‐thought‐out comprehensive plan that addresses what a reasonable budget is, they will find themselves struggling in retirement. Managing cash flow should be as important as managing a portfolio. A trusted advisor helps them make better decisions. Align your values, mission, and purpose to the net worth you're working with. Excess can clutter our minds, and it can irritate our purpose. Help your clients find the right balance for them.

Generally, the most expensive stage of retirement is the early years, 60 to 70 years old. This makes perfect sense as it's when retirees are most active. A good advisor helps new retirees with their spending. It's about getting inside their heads to understand what's important to them, what brings joy and fulfillment, and what needs to be eliminated from their lives. Helping people connect the dots of what truly brings them satisfaction or helping them discover a new passion could be worth much more than just trying to figure out how to pick up a few more basis points on the portfolio.

Taxes and Inflation

Maintaining purchasing power in a low‐interest‐rate environment will be key. As life expectancies increase, your clients could easily enjoy 30 or 40 years in retirement and, therefore, those assets need to work for the client and they need to last. After health issues, running out of money is the greatest fear for many. Your clients' portfolios have to be reexamined once they retire. Many are underexposed in equities. Holding onto bonds or other fixed‐income investments is a common error because after inflation and taxes they're likely losing money every year. Let the power of compounding work for your clients.

In terms of taxes, take advantage of all the retirement plans available to the client in order to maximize all the benefits. Clients may want to consider moving to a tax‐friendly state, selecting alternative investments, or choosing tax‐efficient investments and tax‐advantage accounts. Estate planning for wealthy individuals is a necessity in order to establish a legal foundation to execute the most effective benefits to their heirs.

Longevity

Average life expectancy in the United States is 78.7 years. A good, long life requires resilience, mental fitness, emotional wellness, physical health, and future planning. Develop and implement an asset protection strategy based on the client's goals and objectives. Utilize insurance in the wealth management process to help mitigate catastrophic losses: life insurance, disability insurance, and long‐term care. Develop a business succession plan if the client is an entrepreneur. Security is the cornerstone of wealth management.

This close client–advisor relationship needs to be a consultative process with customized solutions. The questions below should serve as a reminder to both the advisor and the client of a relationship built on trust and transparency.

Every prospective client should ask the advisor the following questions:

- Please tell me about your experience in dealing with a client similar to me.

- Please explain your service model and what can I expect from you and your team.

- How do you charge for the services?

- Can I see a sample financial plan?

- What services do you specialize in?

- What's your investment process and philosophy?

- What makes the client experience unique?

- Are you acting in a fiduciary capacity?

- What questions should I have asked that I didn't ask?

Because a client or prospect will most likely not be reading this book, I would suggest you answer these questions for the client. As a successful and effective advisor, you have to uncover what wealth means to your client. Wealth to me is discretionary time and meaningful relationships. It's freedom. Most importantly, it's not a certain number of dollars. I have been servicing and been around high‐net‐worth clients for three decades and I have learned an awful lot about money, life, success, and accomplishments. These people worked very hard for what they have with countless sacrifices. Unfortunately, too many feel they never have enough wealth. Just like sea water, the more you drink the thirsty or you become.

A confident and competent advisor can help a family deal with their relationship with wealth, help determine what amount of money is enough, and help clients live the life they want and leave a legacy that's significant to them. As Warren Buffett wisely said, “Risk is not knowing what you're doing.”

The next generation of investors will have the same ultimate goals of a comfortable retirement, but the way they will connect and communicate with a firm and advisor may be different. After the Great Recession, generations X and Y have become even more cynical and less trusting. They still value their relationship with a trusted advisor, but they require complete transparency and will be more demanding to see value in the relationship.

Retirement means something very different to me than it did for my parents or past generations. And it will mean something different for my children. Bain's Global Wealth Management group profiled 20 companies that make up roughly 10 percent of global assets under management; they augmented that analysis with interviews with more than 100 senior executives in the industry. The analysis confirms a formidable challenge: while clients are more inclined than ever to seek professional wealth management, they are less trusting and more skeptical now.

That puts a premium on building durable, trusting client relationships. A strong client experience creates high levels of customer loyalty, which is vital to increasing profitability. Bain research shows that loyal customers give their financial service providers a larger share of their business, recommend them to friends and colleagues, and cost less to serve.

Therefore helping the client hit the number is not just advising them on investment management; that's only part of the equation. It’s helping them make the best life choices about all aspects of their financial life. Helping clients live more fully and with greater peace of mind is not something a robot is likely solve in this century.