Module 23: Professional and Legal Responsibilities

Overview

This module covers the general standards of care and ethics that must be followed by CPAs. CPAs are authorized to practice by the various state boards of accountancy. They must follow the rules of these bodies which generally follow the AICPA Code of Professional Conduct. The AICPA and the state societies cooperate on enforcing the ethics of the profession.

A. Regulation of the Profession

B. Disciplinary Systems of the Profession and Regulatory Bodies

C. Accountant’s Legal Liabilities

D. Legal Considerations Affecting the Accountant’s Responsibility

E. Criminal Liability

F. Responsibilities of Auditors under Private Securities Litigation Reform Act

G. Responsibilities under Sarbanes-Oxley Act

H. Additional Statutory Liability Against Accountants

I. Responsibilities of Tax Return Preparers

Key Terms

Multiple-Choice Questions

Multiple-Choice Answers and Explanations

Simulations

Simulation Solutions

Accountants’ civil liability arises primarily from contract law, the law of negligence, fraud, the Securities Act of 1933, and the Securities Exchange Act of 1934. The first three are common law and largely judge-made law, whereas the latter two are federal statutory law.

The agreement between an accountant and his/her client is generally set out in a carefully drafted engagement letter. Additionally, the accountant has a duty to conduct his/her work with the same reasonable care as an average accountant. This duty defines the standard used in a negligence case. It is important to understand

CPAs also have specific rules and regulations that affect their practice as tax preparers which are covered in this module. Before beginning the reading you should review the key terms at the end of the module.

A. Regulation of the Profession

Permits to practice for CPA firms and licenses to practice for individual CPAs are granted by the boards of accountancy in the various states and other jurisdictions. These boards also regulate the profession and may suspend or revoke a CPA or a CPA firm’s right to practice. While all boards require successful completion of the CPA examination, the requirements for education and experience vary.

B. Disciplinary Systems of the Profession and Regulatory Bodies

C. Accountant’s Legal Liabilities

- Defenses available to auditors:

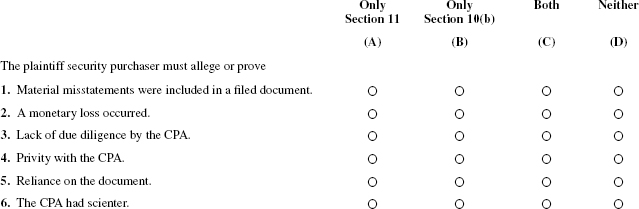

1934 Act 1933 Act 1. Audit was performed with due care Yes Yes 2. Misstatement was immaterial Yes Yes 3. Plaintiff had prior knowledge of misstatement Yes Yes 4. Plaintiff did not rely on information Yes No 5. Misstatement was not cause of loss Yes Yes Prepared by Debra R. Hopkins, Northern Illinois University

- Due diligence is a defense for the 1933 Act only (Do not use for liability under the 1934 Act)

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 31 THROUGH 34

D. Legal Considerations Affecting the Accountant’s Responsibility

E. Criminal Liability

F. Responsibilities of Auditors under Private Securities Litigation Reform Act

G. Responsibilities under Sarbanes-Oxley Act

H. Additional Statutory Liability Against Accountants

I. Responsibilities of Tax Return Preparers

KEY TERMS

Common Law. Law that has historically been established by judicial precedents. Much common law has now been codified in state statutes. This law is the source of liability to clients and third parties (not covered by securities laws).

Constructive fraud. Failure to even use slight care. Constructive fraud is often referred to as gross negligence.

Contributory negligence. Negligence on the part of the plaintiff that contributed to that party’s losses. Contributory negligence will typically mitigate some or all of the defendant’s damages.

Due diligence. The standard of care required under filings under the Securities Act of 1933. To establish “due diligence” an accountant must have made a reasonable investigation, and must have had reasonable grounds to believe and did believe that that the registration statement (including the financial statements) were not misleading.

Fraud. A misrepresentation intended to mislead another party or a representation made with a reckless disregard for its truth.

Joint and several liability. A concept of liability that is similar to joint liability except that if all of the judgment is recovered from one defendant that party may attempt to collect from other defendants their proportionate shares of the judgment. As an example, assume a bank files suit against both the CPA firm and management for misleading financial statements, and the CPA firm is found to be 30% liable and management is found to be 70% liable. The bank may recover 100% of the judgment from the CPA firm and it is up to the CPA firm to collect from management its share of the judgment.

Joint Ethics Enforcement Program (JEEP). A joint program of the American Institute of Certified Public Accountants (AICPA) and state CPA societies to jointly investigate ethics violations.

Joint liability. A liability concept in which any joint defendant may be forced to pay the entire amount of a judgment. As an example, if a bank files suit against both the CPA firm and management for misleading financial statements, the bank may recover the entire amount from management or the CPA firm.

Negligence. Failure to perform with the level of skill and judgment possessed by a typical professional. Negligence is often referred to as ordinary negligence.

Primary beneficiary. A party other than the client who primarily benefits from the contracted services provided by the CPA. As an example, if the CPA is aware that an audit is being performed at the request of the client’s bank, the bank is a primary beneficiary of the contract between the CPA and the client. Under common law a primary beneficiary has the same rights as the client.

Privileged communication. Communication that is not subject to disclosure in court or administrative proceedings. Privilege must be established by law, and generally the communication between an accountant and a client is not privileged.

Privity. A mutual relationship established between parties typically established by a contract. The client and third-party beneficiaries are in privity with the CPA in a contract to provide services.

Public Company Accounting Oversight Board (PCAOB). A nonprofit organization created by the Sarbanes-Oxley Act to oversee the audits of public companies (issuers).

Public Company Accounting Reform and Investor Protection (Sarbanes-Oxley) Act. An act that set a new set of enhanced standards for public company boards, management, and public accounting firms. The Act established the Public Company Accounting Oversight Board (PCAOB).

Racketeer Influenced and Corrupt Organization (RICO) Act. An act designed to allow prosecution of organized criminals. However, the Act has been used to pursue CPA firms who engage in multiple instances (a pattern) of wrongful acts. Civil actions under the Act can result in recovery of treble damages.

Securities Act of 1933. A federal securities act that covers the initial registration of securities.

Securities Exchange Act of 1934. A federal securities act that covers the secondary purchase and sale of securities.

Several liability. A concept of liability in which joint defendants are responsible for only their proportionate share of the judgment. As an example, assume that a bank files suit against both the CPA firm and management for misleading financial statements, and the CPA firm is found to be 30% liable and management is found to be 70% liable. The bank may recover only 30% of the judgment from the CPA firm. The remaining amount must be recovered by the bank from management.

State boards of accountancy. State boards that regulate the practice of public accountancy in a state or jurisdiction. All individual CPAs and CPA firms must be licensed to practice in the states where they practice.

Statements on Standards for Tax Services. AICPA standards for CPAs that perform tax services for clients.

Treasury Department Circular 230. Regulatory requirements regarding the authority to practice before the Internal Revenue Service.

US Securities and Exchange Commission (SEC). A federal agency with primary responsibility for enforcing the federal securities laws and regulating the securities industry.

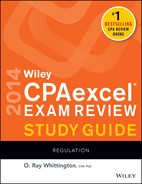

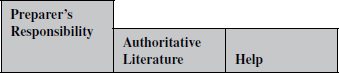

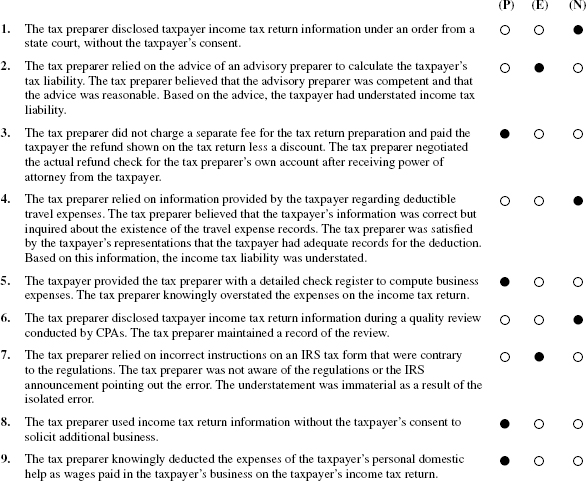

Multiple-Choice Questions (1–79)

A. Regulation of the Profession

1. Which of the following bodies issue permits to practice for CPAs?

a. The AICPA.

b. The SEC.

c. The state boards of accountancy.

d. The PCAOB.

2. Which of the following is not an accurate statement about the requirements of the AICPA Uniform Accountancy Act (UAA)?

a. The UAA requires all accountants to be licensed.

b. The UAA contains requirements for the issuance of CPA certificates.

c. The UAA contains a substantial equivalency provision to allow for movement between states.

d. The UAA contains provisions for continuing education.

B. Disciplinary Systems of the Profession and Regulatory Bodies

3. Which of the following is not a possible result of an AICPA investigation of a member for an ethics violation?

a. Revocation of right to prepare tax returns.

b. Admonishment.

c. Corrective action.

d. Expulsion.

4. Which of the following may not result in automatic expulsion from the AICPA?

a. Revocation of CPA certificate by an authorized body.

b. Filing a fraudulent tax return.

c. Failure to file a required tax return.

d. Conviction for a felony or a misdemeanor.

5. A member of the AICPA is convicted of filing a fraudulent tax return. What is the likely consequence of this action?

a. The CPA will likely be expelled or suspended from membership in the AICPA.

b. The CPA will likely be admonished by the AICPA.

c. The CPA will likely have his or her permit to practice revoked by the AICPA.

d. The AICPA will take no action because the court has already taken sufficient action.

C.1. Common Law Liability to Clients

6. Cable Corp. orally engaged Drake & Co., CPAs, to audit its financial statements. Cable’s management informed Drake that it suspected the accounts receivable were materially overstated. Though the financial statements Drake audited included a materially overstated accounts receivable balance, Drake issued an unqualified opinion. Cable used the financial statements to obtain a loan to expand its operations. Cable defaulted on the loan and incurred a substantial loss.

If Cable sues Drake for negligence in failing to discover the overstatement, Drake’s best defense would be that Drake did not

a. Have privity of contract with Cable.

b. Sign an engagement letter.

c. Perform the audit recklessly or with an intent to deceive.

d. Violate generally accepted auditing standards in performing the audit.

7. Which of the following statements best describes whether a CPA has met the required standard of care in conducting an audit of a client’s financial statements?

a. The client’s expectations with regard to the accuracy of audited financial statements.

b. The accuracy of the financial statements and whether the statements conform to generally accepted accounting principles.

c. Whether the CPA conducted the audit with the same skill and care expected of an ordinarily prudent CPA under the circumstances.

d. Whether the audit was conducted to investigate and discover all acts of fraud.

8. Ford & Co., CPAs, issued an unqualified opinion on Owens Corp.’s financial statements. Relying on these financial statements, Century Bank lent Owens $750,000. Ford was unaware that Century would receive a copy of the financial statements or that Owens would use them to obtain a loan. Owens defaulted on the loan.

To succeed in a common law fraud action against Ford, Century must prove, in addition to other elements, that Century was

a. Free from contributory negligence.

b. In privity of contract with Ford.

c. Justified in relying on the financial statements.

d. In privity of contract with Owens.

9. When performing an audit, a CPA

a. Must exercise the level of care, skill, and judgment expected of a reasonably prudent CPA under the circumstances.

b. Must strictly adhere to generally accepted accounting principles.

c. Is strictly liable for failing to discover client fraud.

d. Is not liable unless the CPA commits gross negligence or intentionally disregards generally accepted auditing standards.

10. When performing an audit, a CPA will most likely be considered negligent when the CPA fails to

a. Detect all of a client’s fraudulent activities.

b. Include a negligence disclaimer in the client engagement letter.

c. Warn a client of known internal control weaknesses.

d. Warn a client’s customers of embezzlement by the client’s employees.

Items 11 through 14 are based on the following:

Edgar, CPA, reviewed the financial statements of Yoke Company (a nonissuer company). In performing the review Edgar failed to discover that a supplier had been overbilling Yoke for purchases for a number of years. Yoke filed a lawsuit against Edgar for negligence in performing the review.

11. Under which of the following sources of law would this lawsuit likely be filed?

a. The Securities Act of 1933.

b. The Securities Exchange Act of 1934.

c. Common law.

d. State securities law.

12. What would be essential to proving Yoke’s case against Edgar?

a. Failure to adhere to generally accepted auditing standards.

b. Reckless disregard for professional standards.

c. Ordinary negligence in the performance of the review.

d. Gross negligence in the performance of the review.

13. Which of the following would not likely be part of Edgar’s defense in this lawsuit?

a. Contributory negligence.

b. Performance of the engagement in accordance with Statement for Accounting and Review Services.

c. A review cannot be relied upon to detect fraud.

d. Misrepresentations by management.

14. Assuming that Yoke prevails in proving negligence by Edgar in this case, which of the following is the most accurate statement about the damages that would be awarded? Assume that no other party, including Yoke, was found to be partially responsible for the losses.

a. Edgar would be responsible for all of the overbillings that occurred.

b. Edgar would be responsible for overbillings occurring since the date he should have detected the scheme.

c. Edgar would be responsible only for returning the fees for the engagement.

d. Edgar would not be held responsible for any damages unless he is also found to be in violation of some criminal law.

15. A CPA’s duty of due care to a client most likely will be breached when a CPA

a. Gives a client an oral instead of written report.

b. Gives a client incorrect advice based on an honest error of judgment.

c. Fails to give tax advice that saves the client money.

d. Fails to follow generally accepted auditing standards.

16. Which of the following elements, if present, would support a finding of constructive fraud on the part of a CPA?

a. Gross negligence in applying generally accepted auditing standards.

b. Ordinary negligence in applying generally accepted accounting principles.

c. Identified third-party users.

d. Scienter.

C.2. Common Law Liability to Third Parties (Nonclients)

17. If a CPA recklessly departs from the standards of due care when conducting an audit, the CPA will be liable to third parties who are unknown to the CPA based on

a. Negligence.

b. Gross negligence.

c. Strict liability.

d. Criminal deceit.

18. In a common law action against an accountant, lack of privity is a viable defense if the plaintiff

a. Is the client’s creditor who sues the accountant for negligence.

b. Can prove the presence of gross negligence that amounts to a reckless disregard for the truth.

c. Is the accountant’s client.

d. Bases the action upon fraud.

19. A CPA audited the financial statements of Shelly Company. The CPA was negligent in the audit. Sanco, a supplier of Shelly, is upset because Sanco had extended Shelly a high credit limit based on the financial statements which were incorrect. Which of the following statements is the most correct?

a. In most states, both Shelly and Sanco can recover from the CPA for damages due to the negligence.

b. States that use the Ultramares decision will allow both Shelly and Sanco to recover.

c. In most states, Sanco cannot recover as a mere foreseeable third party.

d. Generally, Sanco can recover but Shelly cannot.

20. Under the Ultramares rule, to which of the following parties will an accountant be liable for negligence?

| Parties in privity | Foreseen parties | |

| a. | Yes | Yes |

| b. | Yes | No |

| c. | No | Yes |

| d. | No | No |

Items 21 and 22 are based on the following:

While conducting an audit, Larson Associates, CPAs, failed to detect material misstatements included in its client’s financial statements. Larson’s unqualified opinion was included with the financial statements in a registration statement and prospectus for a public offering of securities made by the client. Larson knew that its opinion and the financial statements would be used for this purpose.

21. In a suit by a purchaser against Larson for common law negligence, Larson’s best defense would be that the

a. Audit was conducted in accordance with generally accepted auditing standards.

b. Client was aware of the misstatements.

c. Purchaser was not in privity of contract with Larson.

d. Identity of the purchaser was not known to Larson at the time of the audit.

22. In a suit by a purchaser against Larson for common law fraud, Larson’s best defense would be that

a. Larson did not have actual or constructive knowledge of the misstatements.

b. Larson’s client knew or should have known of the misstatements.

c. Larson did not have actual knowledge that the purchaser was an intended beneficiary of the audit.

d. Larson was not in privity of contract with its client.

C.3. Statutory Liability to Third Parties—Securities Act of 1933

23. Quincy bought Teal Corp. common stock in an offering registered under the Securities Act of 1933. Worth & Co., CPAs, gave an unqualified opinion on Teal’s financial statements that were included in the registration statement filed with the SEC. Quincy sued Worth under the provisions of the 1933 Act that deal with omission of facts required to be in the registration statement. Quincy must prove that

a. There was fraudulent activity by Worth.

b. There was a material misstatement in the financial statements.

c. Quincy relied on Worth’s opinion.

d. Quincy was in privity with Worth.

24. Beckler & Associates, CPAs, audited and gave an unqualified opinion on the financial statements of Queen Co. The financial statements contained misstatements that resulted in a material overstatement of Queen’s net worth. Queen provided the audited financial statements to Mac Bank in connection with a loan made by Mac to Queen. Beckler knew that the financial statements would be provided to Mac. Queen defaulted on the loan. Mac sued Beckler to recover for its losses associated with Queen’s default. Which of the following must Mac prove in order to recover?

I. Beckler was negligent in conducting the audit.

II. Mac relied on the financial statements.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

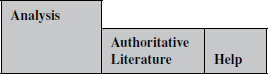

Items 25 and 26 are based on the following:

Dart Corp. engaged Jay Associates, CPAs, to assist in a public stock offering. Jay audited Dart’s financial statements and gave an unqualified opinion, despite knowing that the financial statements contained misstatements. Jay’s opinion was included in Dart’s registration statement. Larson purchased shares in the offering and suffered a loss when the stock declined in value after the misstatements became known.

25. In a suit against Jay and Dart under the Section 11 liability provisions of the Securities Act of 1933, Larson must prove that

a. Jay knew of the misstatements.

b. Jay was negligent.

c. The misstatements contained in Dart’s financial statements were material.

d. The unqualified opinion contained in the registration statement was relied on by Larson.

26. If Larson succeeds in the Section 11 suit against Dart, Larson would be entitled to

a. Damages of three times the original public offering price.

b. Rescind the transaction.

c. Monetary damages only.

d. Damages, but only if the shares were resold before the suit was started.

Items 27 and 28 are based on the following:

Under the liability provisions of Section 11 of the Securities Act of 1933, a CPA may be liable to any purchaser of a security for certifying materially misstated financial statements that are included in the security’s registration statement.

27. Under Section 11, a CPA usually will not be liable to the purchaser

a. If the purchaser is contributorily negligent.

b. If the CPA can prove due diligence.

c. Unless the purchaser can prove privity with the CPA.

d. Unless the purchaser can prove scienter on the part of the CPA.

28. Under Section 11, which of the following must be proven by a purchaser of the security?

| Reliance on the financial statements | Fraud by the CPA | |

| a. | Yes | Yes |

| b. | Yes | No |

| c. | No | Yes |

| d. | No | No |

29. Ocean and Associates, CPAs, audited the financial statements of Drain Corporation. As a result of Ocean’s negligence in conducting the audit, the financial statements included material misstatements. Ocean was unaware of this fact. The financial statements and Ocean’s unqualified opin-ion were included in a registration statement and prospectus for an original public offering of stock by Drain. Sharp purchased shares in the offering. Sharp received a copy of the prospectus prior to the purchase but did not read it. The shares declined in value as a result of the misstatements in Drain’s financial statements becoming known. Under which of the following Acts is Sharp most likely to prevail in a lawsuit against Ocean?

| Securities Exchange Act of 1934, Section 10(b), Rule 10b-5 | Securities Act of 1933, Section 11 | |

| a. | Yes | Yes |

| b. | Yes | No |

| c. | No | Yes |

| d. | No | No |

30. Danvy, a CPA, performed an audit for Lank Corporation. Danvy also performed an S-1 review to review events subsequent to the balance sheet date. If Danvy fails to further investigate suspicious facts, under which of these can he be found negligent?

a. The audit but not the review.

b. The review but not the audit.

c. Neither the audit nor the review.

d. Both the audit and the review.

C.4. Statutory Liability to Third Parties—Securities Exchange Act of 1934

31. Dart Corp. engaged Jay Associates, CPAs, to assist in a public stock offering. Jay audited Dart’s financial statements and gave an unqualified opinion, despite knowing that the financial statements contained misstatements. Jay’s opinion was included in Dart’s registration statement. Larson purchased shares in the offering and suffered a loss when the stock declined in value after the misstatements became known.

In a suit against Jay under the antifraud provisions of Section 10(b) and Rule 10b-5 of the Securities Exchange Act of 1934, Larson must prove all of the following except

a. Larson was an intended user of the false registration statement.

b. Larson relied on the false registration statement.

c. The transaction involved some form of interstate commerce.

d. Jay acted with intentional disregard of the truth.

32. Under the antifraud provisions of Section 10(b) of the Securities Exchange Act of 1934, a CPA may be liable if the CPA acted

a. Negligently.

b. With independence.

c. Without due diligence.

d. Without good faith.

33. Under Section 11 of the Securities Act of 1933, which of the following standards may a CPA use as a defense?

| Generally accepted accounting principles | Generally accepted fraud detection standards | |

| a. | Yes | Yes |

| b. | Yes | No |

| c. | No | Yes |

| d. | No | No |

34. Dart Corp. engaged Jay Associates, CPAs, to assist in a public stock offering. Jay audited Dart’s financial statements and gave an unqualified opinion, despite knowing that the financial statements contained misstatements. Jay’s opinion was included in Dart’s registration statement. Larson purchased shares in the offering and suffered a loss when the stock declined in value after the misstatements became known.

If Larson succeeds in the Section 10(b) and Rule 10b-5 suit, Larson would be entitled to

a. Only recover the original public offering price.

b. Only rescind the transaction.

c. The amount of any loss caused by the fraud.

d. Punitive damages.

D.1. Accountant’s Working Papers

35. Which of the following statements is correct with respect to ownership, possession, or access to a CPA firm’s audit working papers?

a. Working papers may never be obtained by third parties unless the client consents.

b. Working papers are not transferable to a purchaser of a CPA practice unless the client consents.

c. Working papers are subject to the privileged communication rule which, in most jurisdictions, prevents any third-party access to the working papers.

d. Working papers are the client’s exclusive property.

36. Which of the following statements is correct regarding a CPA’s working papers? The working papers must be

a. Transferred to another accountant purchasing the CPA’s practice even if the client hasn’t given permission.

b. Transferred permanently to the client if demanded.

c. Turned over to any government agency that requests them.

d. Turned over pursuant to a valid federal court subpoena.

37. To which of the following parties may a CPA partnership provide its working papers, without being lawfully subpoenaed or without the client’s consent?

a. The IRS.

b. The FASB.

c. Any surviving partner(s) on the death of a partner.

d. A CPA before purchasing a partnership interest in the firm.

38. To which of the following parties may a CPA partnership provide its working papers without either the client’s consent or a lawful subpoena?

| The IRS | The FASB | |

| a. | Yes | Yes |

| b. | Yes | No |

| c. | No | Yes |

| d. | No | No |

D.2. Privileged Communications between Accountant and Client

39. A CPA is permitted to disclose confidential client information without the consent of the client to

I. Another CPA who has purchased the CPA’s tax practice.

II. Another CPA firm if the information concerns suspected tax return irregularities.

III. A state CPA society voluntary quality control review board.

a. I and III only.

b. II and III only.

c. II only.

d. III only.

40. Thorp, CPA, was engaged to audit Ivor Co.’s financial statements. During the audit, Thorp discovered that Ivor’s inventory contained stolen goods. Ivor was indicted and Thorp was subpoenaed to testify at the criminal trial. Ivor claimed accountant-client privilege to prevent Thorp from testifying. Which of the following statements is correct regarding Ivor’s claim?

a. Ivor can claim an accountant-client privilege only in states that have enacted a statute creating such a privilege.

b. Ivor can claim an accountant-client privilege only in federal courts.

c. The accountant-client privilege can be claimed only in civil suits.

d. The accountant-client privilege can be claimed only to limit testimony to audit subject matter.

41. A violation of the profession’s ethical standards most likely would have occurred when a CPA

a. Issued an unqualified opinion on the 2002 financial statements when fees for the 2001 audit were unpaid.

b. Recommended a controller’s position description with candidate specifications to an audit client.

c. Purchased a CPA firm’s practice of monthly write-ups for a percentage of fees to be received over a three-year period.

d. Made arrangements with a financial institution to collect notes issued by a client in payment of fees due for the current year’s audit.

42. Which of the following statements concerning an accountant’s disclosure of confidential client data is generally correct?

a. Disclosure may be made to any state agency without subpoena.

b. Disclosure may be made to any party on consent of the client.

c. Disclosure may be made to comply with an IRS audit request.

d. Disclosure may be made to comply with generally accepted accounting principles.

E. Criminal Liability

43. A CPA may be held criminally liable under any of the following, except:

a. The Securities Act of 1933.

b. Common law.

c. The Racketeer Influenced and Corrupt Organizations Act.

d. Federal tax laws.

44. Which of the following acts allows civil suits with the potential recovery of treble damages?

a. The Racketeer Influenced and Corrupt Organizations Act.

b. The Securities Act of 1933.

c. The Securities Exchange Act of 1934.

d. Federal tax acts.

F. Responsibilities of Auditors under Private Securities Litigation Reform Act

45. McGee is auditing Nevus Corporation and detects probable criminal activity by one of the employees. McGee believes this will have a material impact on the financial statements. The financial statements of Nevus Corporation are under the Securities Exchange Act of 1934. Which of the following is correct?

a. McGee should report this to the Securities Exchange Commission.

b. McGee should report this to the Justice Department.

c. McGee should report this to Nevus Corporation’s audit committee or board of directors.

d. McGee will discharge his duty by requiring that a note of this be included in the financial statements.

46. Which of the following is an auditor not required to establish procedures for under the Private Securities Litigation Reform Act?

a. To develop a comprehensive internal control system.

b. To evaluate the ability of the firm to continue as a going concern.

c. To detect material illegal acts.

d. To identify material related-party transactions.

47. Which of the following is an auditor required to do under the Private Securities Litigation Reform Act concerning audits under the Federal Securities Exchange Act of 1934?

I. Establish procedures to detect material illegal acts of the client being audited.

II. Evaluate the ability of the firm being audited to continue as a going concern.

a. Neither I nor II.

b. I only.

c. II only.

d. Both I and II.

48. Lin, CPA, is auditing the financial statements of Exchange Corporation under the Federal Securities Exchange Act of 1934. He detects what he believes are probable material illegal acts. What is his duty under the Private Securities Litigation Reform Act?

a. He must inform the principal shareholders within ten days.

b. He must inform the audit committee or the board of directors.

c. He need not inform anyone, beyond requiring that the financial statements are presented fairly.

d. He should not inform anyone since he owes a duty of confidentiality to the client.

49. The Private Securities Litigation Reform Act

a. Applies only to securities not purchased from a stock exchange.

b. Does not apply to common stock of a publicly held corporation.

c. Amends the Federal Securities Act of 1933 and the Federal Securities Exchange Act of 1934.

d. Does not apply to preferred stock of a publicly held corporation.

50. Bran, CPA, audited Frank Corporation. The shareholders sued both Frank and Bran for securities fraud under the Federal Securities Exchange Act of 1934. The court determined that there was securities fraud and that Frank was 80% at fault and Bran was 20% at fault due to her negligence in the audit. Both Frank and Bran are solvent and the damages were determined to be $1 million. What is the maximum liability of Bran?

a. $0

b. $ 200,000

c. $ 500,000

d. $1,000,000

G. Responsibilities under Sarbanes-Oxley Act

51. Which of the following nonattest services are auditors allowed to perform for a public company?

a. Bookkeeping services.

b. Appraisal services.

c. Tax services.

d. Internal audit services.

52. Which of the following Boards has the responsibility to regulate CPA firms that audit public companies?

a. Auditing Standards Board.

b. Public Oversight Board.

c. Public Company Accounting Oversight Board.

d. Accounting Standards Board.

53. The Sarbanes-Oxley Act includes all of the following provisions, except:

a. Penalties for failure to retain audit workpapers.

b. Requirement for registration of CPA firms to audit public companies.

c. Requirement for inspection of public-company audits.

d. Requirement for a minimum level of experience for audit partners.

54. Under the Sarbanes-Oxley Act, which of the following individuals are required personally to certify to the accuracy of financial statements filed with the SEC?

a. The chief financial officer and the chief executive officer.

b. The chief financial officer, the chief executive officer, and the controller.

c. The audit partner and the chief executive officer.

d. The chairman of the board, the chief executive officer, and the chief financial officer.

55. Generally a Form 8-K must be filed with the SEC

a. Annually.

b. Quarterly.

c. Within four days of the occurrence of a triggering event.

d. Within 10 days of the occurrence of a triggering event.

56. The Sarbanes-Oxley Act of 2002 requires rotation of the audit partner on a public company audit at least every

a. 3 years.

b. 5 years.

c. 7 years.

d. 10 years.

I. Responsibilities of Tax Return Preparers

57. Which of the following acts constitute(s) grounds for a tax preparer penalty?

I. Without the taxpayer’s consent, the tax preparer disclosed taxpayer income tax return information under an order from a state court.

II. At the taxpayer’s suggestion, the tax preparer deducted the expenses of the taxpayers’ personal domestic help as a business expense on the taxpayer’s individual tax return.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

58. Vee Corp. retained Water, CPA, to prepare its 2013 income tax return. During the engagement, Water discovered that Vee had failed to file its 2008 income tax return. What is Water’s professional responsibility regarding Vee’s unfiled 2008 income tax return?

a. Prepare Vee’s 2008 income tax return and submit it to the IRS.

b. Advise Vee that the 2008 income tax return has not been filed and recommend that Vee ignore filing its 2008 return since the statute of limitations has passed.

c. Advise the IRS that Vee’s 2008 income tax return has not been filed.

d. Consider withdrawing from preparation of Vee’s 2013 income tax return until the error is corrected.

59. To avoid tax return preparer penalties for a return’s understated tax liability due to an intentional disregard of the regulations, which of the following actions must a tax preparer take?

a. Audit the taxpayer’s corresponding business operations.

b. Review the accuracy of the taxpayer’s books and records.

c. Make reasonable inquiries if the taxpayer’s information is incomplete.

d. Examine the taxpayer’s supporting documents.

60. Kopel was engaged to prepare Raff’s 2012 federal income tax return. During the tax preparation interview, Raff told Kopel that he paid $3,000 in property taxes in 2012. Actually, Raff’s property taxes amounted to only $600. Based on Raff’s word, Kopel deducted the $3,000 on Raff’s return, resulting in an understatement of Raff’s tax liability. Kopel had no reason to believe that the information was incorrect. Kopel did not request underlying documentation and was reasonably satisfied by Raff’s representation that Raff had adequate records to support the deduction. Which of the following statements is correct?

a. To avoid the preparer penalty for willful understatement of tax liability, Kopel was obligated to examine the underlying documentation for the deduction.

b. To avoid the preparer penalty for willful understatement of tax liability, Kopel would be required to obtain Raff’s representation in writing.

c. Kopel is not subject to the preparer penalty for willful understatement of tax liability because the deduction that was claimed was more than 25% of the actual amount that should have been deducted.

d. Kopel is not subject to the preparer penalty for willful understatement of tax liability because Kopel was justified in relying on Raff’s representation.

61. A penalty for understated corporate tax liability can be imposed on a tax preparer who fails to

a. Audit the corporate records.

b. Examine business operations.

c. Copy all underlying documents.

d. Make reasonable inquiries when taxpayer information appears incorrect.

62. A tax return preparer is subject to a penalty for knowingly or recklessly disclosing corporate tax return information, if the disclosure is made

a. To enable a third party to solicit business from the taxpayer.

b. To enable the tax processor to electronically compute the taxpayer’s liability.

c. For peer review.

d. Under an administrative order by a state agency that registers tax return preparers.

63. A tax return preparer may disclose or use tax return information without the taxpayer’s consent to

a. Facilitate a supplier’s or lender’s credit evaluation of the taxpayer.

b. Accommodate the request of a financial institution that needs to determine the amount of taxpayer’s debt to it, to be forgiven.

c. Be evaluated by a quality or peer review.

d. Solicit additional nontax business.

64. Which, if any, of the following could result in penalties against an income tax return preparer?

I. Knowing or reckless disclosure or use of tax information obtained in preparing a return.

II. A willful attempt to understate any client’s tax liability on a return or claim for refund.

a. Neither I nor II.

b. I only.

c. II only.

d. Both I and II.

65. Clark, a professional tax return preparer, prepared and signed a client’s 2012 federal income tax return that resulted in a $600 refund. Which one of the following statements is correct with regard to an Internal Revenue Code penalty Clark may be subject to for endorsing and cashing the client’s refund check?

a. Clark will be subject to the penalty if Clark endorses and cashes the check.

b. Clark may endorse and cash the check, without penalty, if Clark is enrolled to practice before the Internal Revenue Service.

c. Clark may endorse and cash the check, without penalty, because the check is for less than $1,000.

d. Clark may endorse and cash the check, without penalty, if the amount does not exceed Clark’s fee for preparation of the return.

66. A CPA who prepares clients’ federal income tax returns for a fee must

a. File certain required notices and powers of attorney with the IRS before preparing any returns.

b. Keep a completed copy of each return for a specified period of time.

c. Receive client documentation supporting all travel and entertainment expenses deducted on the return.

d. Indicate the CPA’s federal identification number on a tax return only if the return reflects tax due from the taxpayer.

67. A CPA owes a duty to

a. Provide for a successor CPA in the event death or disability prevents completion of an audit.

b. Advise a client of errors contained in a previously filed tax return.

c. Disclose client fraud to third parties.

d. Perform an audit according to GAAP so that fraud will be uncovered.

68. In general, if the IRS issues a 30-day letter to an individual taxpayer who wishes to dispute the assessment, the taxpayer

a. May, without paying any tax, immediately file a petition that would properly commence an action in Tax Court.

b. May ignore the 30-day letter and wait to receive a 90-day letter.

c. Must file a written protest within 10 days of receiving the letter.

d. Must pay the taxes and then commence an action in federal district court.

69. A CPA will be liable to a tax client for damages resulting from all of the following actions except

a. Failing to timely file a client’s return.

b. Failing to advise a client of certain tax elections.

c. Refusing to sign a client’s request for a filing extension.

d. Neglecting to evaluate the option of preparing joint or separate returns that would have resulted in a substantial tax savings for a married client.

70. According to the AICPA Statement on Standards for Tax Services, which of the following statements is correct regarding the standards a CPA should follow when recommending tax return positions and preparing tax returns?

a. A CPA may recommend a position that the CPA concludes is frivolous as long as the position is adequately disclosed on the return.

b. A CPA may recommend a position in which the CPA has a good faith belief that the position has a realistic possibility of being sustained if challenged.

c. A CPA will usually not advise the client of the potential penalty consequences of the recommended tax return position.

d. A CPA may sign a tax return as preparer knowing that the return takes a position that will not be sustained if challenged.

71. According to the standards of the profession, which of the following statements is(are) correct regarding the action to be taken by a CPA who discovers an error in a client’s previously filed tax return?

I. Advise the client of the error and recommend the measures to be taken.

II. Withdraw from the professional relationship regardless of whether or not the client corrects the error.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

72. According to the profession’s ethical standards, a CPA preparing a client’s tax return may rely on unsupported information furnished by the client, without examining underlying information, unless the information

a. Is derived from a pass-through entity.

b. Appears to be incomplete on its face.

c. Concerns dividends received.

d. Lists charitable contributions.

73. Which of the following acts by a CPA will not result in a CPA incurring an IRS penalty?

a. Failing, without reasonable cause, to provide the client with a copy of an income tax return.

b. Failing, without reasonable cause, to sign a client’s tax return as preparer.

c. Understating a client’s tax liability as a result of an error in calculation.

d. Negotiating a client’s tax refund check when the CPA prepared the tax return.

74. According to the standards of the profession, which of the following sources of information should a CPA consider before signing a client’s tax return?

I. Information actually known to the CPA from the tax return of another client.

II. Information provided by the client that appears to be correct based on the client’s returns from prior years.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

75. According to Treasury Department Circular 230, a practitioner may

a. Charge a contingent fee for preparing a client’s original tax return.

b. Charge any amount of fixed fee for tax work.

c. Retain a client’s records for nonpayment of fees.

d. Charge a contingent fee for representing a client in connection with a judicial proceeding.

76. Circular 230 limits practice before the Internal Revenue Service to

a. Certified Public Accountants.

b. Attorneys.

c. Registered tax return preparers.

d. All of the above may practice before the IRS.

77. A practitioner is in violation of Circular 230 if the practitioner

a. Publishes the availability of a written schedule of fees containing hourly rates.

b. Charges a contingent fee for filing an original tax return.

c. Informs a client of the possible penalties that may apply to a position taken on a tax return.

d. Relies, without verification, upon information furnished by the client.

78. Circular 230 defines practice before the Internal Revenue Service to include

a. Preparing and filing documents with the IRS.

b. Corresponding and communicating with the IRS.

c. Representing a client during an examination at IRS offices.

d. All of the above are considered practice before the IRS.

79. According to Circular 230, practitioners must not sign a tax return if the return takes a position that does not have

a. A more-likely-than-not probability of being sustained.

b. Substantial authority.

c. A realistic possibility of being sustained.

d. A reasonable basis.

Multiple-Choice Answers and Explanations

Answers

Explanations

1. (c) The requirement is to identify the body that issues permits to practice. Answer (c) is correct because only state boards of accountancy (or similar authorities) may issue permits to practice. The other organizations do not.

2. (a) The UAA only requires accountants who perform attest services or compilations of financial statements to be licensed. Answers (b), (c), and (d) are incorrect because they are all requirements of the UAA.

3. (a) The requirement is to identify the item that is not a possible result of an AICPA ethics investigation. Answer (a) is correct because the AICPA cannot revoke the right to prepare a tax return.

4. (d) The requirement is to identify the item that may not result in automatic expulsion from the AICPA. Answer (d) is correct because conviction for a misdemeanor would not result in automatic expulsion.

5. (a) The requirement is to identify the likely result of a member of the AICPA being convicted of filing a fraudulent tax return. Answer (a) is correct because this is one of the situations that can result in suspension or expulsion without a hearing.

6. (d) A CPA is not automatically liable for failure to discover a materially overstated account. The CPA can be liable if the failure to discover was due to the CPA’s own negligence. Although performing an audit in accordance with GAAS does not guarantee that there is no negligence, it is normally a good defense against negligence. Answer (a) is incorrect because there was privity of contract with Cable. There was an oral agreement constituting a contractual relationship, therefore this would not be a good defense. Answer (b) is incorrect because an oral contract for an audit is still enforceable without a signed engagement letter. Answer (c) is incorrect because a CPA does not have to perform an audit recklessly or with an intent to deceive to be liable for negligence. Negligence simply means that a CPA failed to exercise due care owed of the average reasonable accountant in performing an audit.

7. (c) In order to meet the required standard of due care in conducting an audit of a client’s financial statements, a CPA has the duty to perform with the same degree of skill and judgment expected of an ordinarily prudent CPA under the circumstances. Answer (a) is incorrect because the client’s expectations do not guide the standard of due care. Rather, the standard of due care is guided by state and federal statute, court decisions, the contract with the client, GAAS and GAAP, and customs of the profession. Answer (b) is incorrect because it is generally the client’s responsibility to prepare its financial statements in accordance with generally accepted accounting principles. Answer (d) is incorrect because a CPA is not normally liable for failure to detect fraud or irregularities unless (1) a “normal” audit would have detected it, (2) the accountant by agreement has undertaken greater responsibility, or (3) the wording of the audit report indicates greater responsibility.

8. (c) The following elements are needed to establish fraud against an accountant: (1) misrepresentation of the accountant’s expert opinion, (2) scienter shown by either the accountant’s knowledge of falsity or reckless disregard of the truth, (3) reasonable reliance by injured party, and (4) actual damages. Answer (a) is incorrect because contributory negligence of a third party is not a defense available for the accountant in cases of fraud. Answers (b) and (d) are incorrect because privity of contract is not a requirement for an accountant to be held liable for fraud.

9. (a) In the performance of an audit, a CPA has the duty to exercise the level of care, skill, and judgment expected of a reasonably prudent CPA under the circumstances. Answer (b) is incorrect because a CPA performing an audit must adhere to generally accepted auditing standards. It is the client’s responsibility to prepare its financial statements in accordance with generally accepted accounting principles. Answer (c) is incorrect because an accountant is not liable for failure to detect fraud unless (1) a “normal” audit would have detected it, (2) the accountant by agreement has undertaken greater responsibility such as a defalcation audit, or (3) the wording of the audit report indicates greater responsibility for detecting fraud. Answer (d) is incorrect because a CPA can be liable for negligence, which is simply a failure to exercise due care in performing an audit. The CPA does not have to be grossly negligent or intentionally disregard generally accepted auditing standards to be held liable for negligence.

10. (c) A CPA will be liable for negligence when s/he fails to exercise due care. The standard for due care is guided by state and federal statutes, court decisions, contracts with clients, conformity with GAAS and GAAP, and the customs of the profession. Per the AICPA Professional Standards, AU 325, requires that if the auditor becomes aware of weaknesses in the design or operation of the internal control structure, these weaknesses, termed reportable conditions, be communicated to the audit committee of the client. Answer (a) is incorrect because a CPA is not normally liable for failure to detect fraud. Answer (b) is incorrect because including a negligence disclaimer in an engagement letter has no bearing on whether the CPA is negligent. Answer (d) is incorrect because generally a CPA is not required to inform a client’s customers of embezzlements although knowledge of the embezzlements may adversely affect the CPA’s audit opinion.

11. (c) The requirement is to identify the source of law under which the lawsuit would likely be filed. Answer (c) is correct because lawsuits by clients for negligence are filed under common law. Answer (a) is incorrect because suits by investors in securities issued by a public company would be filed under this law. Answer (b) is incorrect because suits by individuals who purchase or sell securities of a public company would be filed under this law. Answer (d) is incorrect because suits by individuals who purchase or sell securities regulated by a state would be filed under these laws.

12. (c) Since Yoke is the client and in privity of contract with Edgar, Yoke need only prove ordinary negligence on the part of Edgar. Therefore, answer (c) is correct. Answer (a) is incorrect because Edgar was not performing an audit. Answer (b) is incorrect because this would not be necessary; ordinary negligence would be sufficient. Answer (d) is incorrect because this would not be necessary; ordinary negligence would be sufficient.

13. (d) The requirement is to identify the item that would not likely be part of Edgar’s defense. Answer (d) is correct because there is no indication that management made any misrepresentations. Answer (a) is incorrect because if Edgar can show that management was negligent in establishing control, some of the responsibility for the losses may be shifted to management. Answer (b) is incorrect because performance of the engagement in conformity with professional standards would establish that Edgar was not negligent. Answer (c) is incorrect because Edgar would try to establish the limitations of the engagement.

14. (b) The requirement is to identify the accurate statement about damages. The court tries to establish a link between (causation) the losses and the defendant’s negligence. Therefore, answer (b) is correct because Edgar should be held responsible for the losses that have occurred since Edgar should have discovered the scheme. Answer (a) is incorrect because Edgar should not be held liable for losses that were incurred prior to the time he should have detected the scheme. Answer (c) is incorrect because Edgar would be responsible for more than just returning the fees. Answer (d) is incorrect because in civil proceedings there is no need to provide criminal liability.

15. (d) A CPA’s duty of due care is guided by the following standards: (1) state and federal statutes, (2) court decisions, (3) contract with the client, (4) GAAS and GAAP, and (5) customs of the profession. Therefore, failure to follow GAAS constitutes a breach of a CPA’s duty of due care. Answer (a) is incorrect because issuance of an oral rather than written report does not necessarily constitute a failure to exercise due care. Answers (b) and (c) are incorrect because the standard of due care requires the CPA to exercise the skill and judgment of an ordinary, prudent accountant. An honest error of judgment or failure to provide money saving tax advice would not breach the duty of due care if the CPA acted in a reasonable manner.

16. (a) A CPA’s liability for constructive fraud is established by the following elements: (1) misrepresentation of a material fact, (2) reckless disregard for the truth, (3) reasonable reliance by the injured party, and (4) actual damages. Gross negligence constitutes a reckless disregard for the truth. Answer (b) is incorrect because ordinary negligence is not sufficient to support a finding of constructive fraud. Answer (c) is incorrect because the liability for constructive fraud does not depend upon the identification of third-party users. Answer (d) is incorrect because the presence of the intent to deceive is needed to satisfy the scienter requirement for fraud. However, even in the absence of the intent to deceive, the CPA can be liable for constructive fraud based on reckless disregard of the truth.

17. (b) A foreseeable third party is someone not identified to the CPA, but who may be expected to receive the accountant’s audit report and rely upon it. Even though this party is unknown to the CPA, the CPA is liable for gross negligence or fraud.

18. (a) Lack of privity can be a viable defense against third parties in a common law case of negligence or breach of contract. A client’s creditor is not in privity of contract with the accountant. Answers (b) and (d) are incorrect because plaintiffs who are suing for fraud, constructive fraud, or gross negligence, which involves a reckless disregard for the truth, need not show privity of contract. Answer (c) is incorrect because the accountant’s client is in privity of contract with the accountant due to their contractual agreement.

19. (c) Since Sanco was a foreseeable third party instead of an actually foreseen third party by the CPA, Sanco in most states cannot recover. Answer (a) is incorrect because most states do not extend liability to mere foreseeable third parties for simple negligence. Answer (b) is incorrect because the Ultramares decision limited liability to parties in privity of contract with the CPA. Answer (d) is incorrect because the client can recover for damages caused to it when negligence is established.

20. (b) Under the Ultramares rule, the accountant is held liable only to parties whose primary benefit the financial statements are intended. This generally means only the client or third-party beneficiaries who are in privity of contract with the accountant. Many courts have more recently departed from the Ultramares decision to allow foreseen third parties to recover from the accountant. However, those courts that adhere to the Ultramares rule do not expand liability to foreseen parties.

21. (a) In order to establish common law liability against an accountant based upon negligence, it must be proven that (1) the accountant had the duty to exercise due care, (2) the accountant breached the duty of due care, (3) damage or loss resulted, and (4) a causal relationship exists between the fault of the accountant and the resulting damages. The accountant may escape liability if due care can be established. The standard for due care is guided by state and federal statute, court decisions, contract with client, GAAS and GAAP, and customs of the profession. Although following GAAS does not automatically preclude negligence, it is strong evidence for the presence of due care. Answer (b) is incorrect because although the client may be aware of the misstatement, the auditor has the responsibility to detect the material misstatement if it is such that an average, reasonable accountant should have detected it. Answer (c) is incorrect because the client and Larson intended for the opinion and the financial statements to be used by purchasers. Therefore, a purchaser is considered a third-party beneficiary and is in privity of contract. Answer (d) is incorrect because the accountant need not know the specific identity of a third-party beneficiary to be held liable for negligence.

22. (a) To establish a CPA’s liability for common law fraud, the following elements must be present: (1) misrepresentation of a material fact or the accountant’s expert opinion, (2) scienter, shown by either an intent to mislead or reckless disregard for the truth, (3) reasonable or justifiable reliance by injured party, and (4) actual damages resulted. If Larson did not have actual or constructive knowledge of the misstatements, the scienter element would not be present and thus Larson would not be liable. Answers (b) and (d) are incorrect because neither contributory negligence of the client nor lack of privity of contract are defenses available to the accountant in cases of fraud. Answer (c) is incorrect because an accountant is generally liable to all parties defrauded. Therefore, the accountant need not have actual knowledge that the purchaser was an intended beneficiary.

23. (b) The Securities Act of 1933 requires that a plaintiff need only prove that damages were incurred and that there was a material misstatement or omission in order to establish a prima facie case against a CPA. The Act does not require that the plaintiff prove that s/he relied on the financial information or that there was negligence or fraud present. The Securities Act of 1933 eliminates the necessity for privity of contract.

24. (c) Mac is a third party that the accountant knew would rely on the financial statements. Queen’s financial statements contained material misstatements. Mac can recover by showing that the accountant was negligent in the audit. Mac also needs to establish that it did rely on the financial statements in order to recover from the accountant for the losses on Queen.

25. (c) Under the Securities Act of 1933, a CPA is liable to any third-party purchaser of registered securities for losses resulting from misstatements in the financial statements included in the registration statement. The plaintiff (purchaser) must establish that damages were incurred, and that the misstatements were material misstatements of facts. Answer (a) is incorrect because under the 1933 Act it is not necessary for the purchaser of securities to prove “scienter,” or knowledge of material misstatement, on the part of the CPA. Answers (b) and (d) are incorrect because under the 1933 Act, the plaintiff need not prove negligence on the part of the CPA or that there was reliance by the plaintiff on the financial statements included in the registration statement.

26. (c) In a Section 11 suit under the 1933 Act, the plaintiff may recover damages equal to the difference between the amount paid and the market value of the stock at the time of the suit. If the stock has been sold, then the damages are the difference between the amount paid and the sale price. Answer (a) is incorrect because damages of triple the original price are not provided for under this act. Answer (b) is incorrect because rescission is not a remedy under this act. Answer (d) is incorrect because if the shares have not been sold before the suit, then the court uses the difference between the amount paid and the market value at the time of the suit.

27. (b) Under Section 11 of the 1933 Act, if the plaintiff proves damages and the existence of a material misstatement or omission in the financial statements included in the registration statement, these are sufficient to win against the CPA unless the CPA can prove one of the applicable defenses. Due diligence is one of the defenses. Answer (a) is incorrect because contributory negligence is not a defense under Section 11. Answer (c) is incorrect because the purchaser need not prove privity with the CPA. Answer (d) is not correct because the purchaser needs to prove the above two elements but not scienter.

28. (d) To impose liability under Section 11 of the Securities Act of 1933 for a misleading registration statement, the plaintiff must prove the following: (1) damages were incurred, and (2) a material misstatement or omission was present in financial statements included in the registration statement. The plaintiff generally is not required to prove the defendant’s intent to deceive nor must the plaintiff prove reliance on the registration statement.

29. (c) The proof requirements necessary to establish an accountant’s liability under the Securities Act of 1933, Section 11 are as follows: (1) the plaintiff must prove damages were incurred, and (2) the plaintiff must prove there was a material misstatement or omission in financial statements included in the registration statement. To establish an accountant’s liability under the Securities Exchange Act of 1934, Section 10(b), Rule 10b-5, the following elements must be proven: (1) damages resulted to the plaintiff in connection with the purchase or sale of a security in interstate commerce, (2) a material misstatement or omission existed in information released by the firm, (3) the plaintiff justifiably relied on the financial information, and (4) the existence of scienter. Because Sharp can prove that damages were incurred and that the statements contained material misstatements, Sharp is likely to prevail in a lawsuit under the Securities Act of 1933, Section 11. However, Sharp would be unable to prove justifiable reliance on the misstated information or the existence of scienter; thus, recovery under the Securities Exchange Act of 1934, Section 10(b), Rule 10b-5, is unlikely.

30. (d) If an accountant is negligent, s/he may have liability not only for a negligently performed audit but also for a negligently performed review when there were facts that should require the accountant to investigate further because of their suspicious nature. This is true even though a review is not a full audit.

31. (a) In order to establish a case under the antifraud provisions of Section 10(b) and Rule 10b-5 of the 1934 Act, the plaintiff has to prove that the defendant either had knowledge of the falsity in the registration statement or acted with reckless disregard for the truth. In addition, the plaintiff must show that the transaction involved interstate commerce so that there is a constitutional basis for using this federal law. S/he also must prove justifiable reliance. The plaintiff need not prove that s/he was an intended user of the false registration statement.

32. (d) Under Rule 10b-5 of Section 10(b) of the Securities Exchange Act of 1934, a CPA may be liable if s/he makes a false statement of a material fact or an omission of a material fact in connection with the purchase or sale of a security. Scienter is required which is shown by either knowledge of falsity or reckless disregard for the truth. Of the four answers given, lack of good faith best describes this scienter requirement. Answer (a) is incorrect because negligence is not enough under this rule. Answer (b) is incorrect because independence is not the issue under scienter. Answer (c) is incorrect because although due diligence can be a defense under Section 11 of the Securities Act of 1933, it is not the standard used under Section 10(b) of the Securities Exchange Act of 1934.

33. (b) Under Section 11 of the Securities Act of 1933, the CPA may be liable for material misstatements or omissions in certified financial statements. The CPA may escape liability by showing due diligence. This can often be proven by the CPA showing that s/he followed Generally Accepted Accounting Principles. There are not generally accepted fraud detection standards that the CPA can use as a defense.

34. (c) In a civil suit under Section 10(b) and Rule 10b-5, the damages are generally the difference between the amount paid and the market value at the time of suit, or the difference between the amount paid and the sales price if sold. Answer (a) is incorrect because recovery of the full original public offering price is not used as the damages. Answer (b) is incorrect because the above described monetary damages are used. Answer (d) is incorrect because punitive damages are not given under this rule.

35. (b) In general, the accountant’s workpapers are owned by the accountant. However, the CPA’s ownership of the working papers is custodial in nature and the CPA is required to preserve confidentiality of the client’s affairs. Normally, the CPA firm cannot allow transmission of information included in the working papers to third parties without the client’s consent. This prevents a CPA firm from transferring workpapers to a purchaser of a CPA practice unless the client consents. Answer (c) is incorrect because the privileged communication rule does not exist at common law and has only been enacted by a few states. Additionally, the privileged communications rule only applies to communications which were intended to be privileged at the time of communication. Answer (a) is incorrect because working papers may be obtained by third parties without the client’s consent when they appear to be relevant to issues raised in litigation (through a subpoena).

36. (d) The working papers are owned by the CPA, but the CPA must preserve confidentiality. They cannot be transmitted to another party unless the client consents or unless the CPA is required to under a valid court or governmental agency subpoena. Answers (a) and (c) are incorrect because these do not preserve the confidentiality. Answer (b) is incorrect because the CPA retains the working papers as evidence of the work done.

37. (c) Any of the partners of a CPA partnership can have access to the partnership’s working papers. Third parties outside the firm need to have the client’s consent or a legal subpoena.

38. (d) To preserve confidentiality, a CPA (including a CPA partnership) may not allow transmission of information in the working papers to other parties. Exceptions are consent of the client or the production of an enforceable subpoena. There are no exceptions for the IRS or the FASB, thus making answers (a), (b), and (c) incorrect.

39. (d) In a jurisdiction having an accountant-client privilege statute, the CPA generally may not turn over workpapers without the client’s permission. It is allowable to do so, however, for use in a quality review under AICPA authorization or to be given to the state CPA society quality control panel. Answers (a), (b), and (c) are incorrect because the client would have to give permission for the CPA to turn over the confidential workpapers to the purchaser of the CPA practice, as well as to another CPA firm in regard to suspected tax return irregularities.

40. (a) Privileged communications between the accountant and client are recognized only in a few states. Therefore, if a state statute has been enacted creating such a privilege, Ivor will be able to prevent Thorp from testifying. Answer (b) is incorrect because federal law does not recognize accountant-client privileged communication. Answer (d) is incorrect because Ivor will not be able to prevent Thorp from testifying about the nature of the work performed in the audit unless a privileged communication statute has been enacted in that state. Answer (c) is incorrect because privileged communication does not exist at common law but must be created by state statute. Criminal law is based on common law and varies by state. However, as a general rule, in states that recognize accountant-client privilege, it can be claimed in both civil and criminal suits.

41. (a) The requirement is to identify the situation in which it is most likely that a violation of the profession’s ethical standards would have occurred. Answer (a) is correct because independence is impaired if fees remain unpaid for professional services of the preceding year when the report on the client’s current year is issued. Accordingly, no report should have been issued on the 2002 financial statements when fees for the 2001 audit were unpaid. Answer (b) is incorrect because CPAs may recommend a position description (ET 191) without violating the profession’s ethical standards. Answer (c) is incorrect because a practice may be purchased for a percentage of fees to be received. Answer (d) is incorrect because the Code of Professional Conduct does not prohibit arrangements with financial institutions to collect notes issued by a client in payment of professional fees.

42. (b) A CPA must not disclose confidential information of a client unless the client gives consent to disclose it to that third party. Answer (a) is incorrect because state agencies need a subpoena before the CPA must comply. Answer (c) is incorrect because the IRS does not have the right to force a CPA to turn over confidential information of a client without either the client’s consent or an enforceable subpoena. Answer (d) is incorrect because although the CPA can use the client information to defend a lawsuit, the CPA is not normally requested to disclose confidential information to comply with generally accepted accounting principles.

43. (b) The requirement is to identify the source of law which may not result in criminal liability. Answer (b) is correct because common law can only result in civil liability.

44. (a) The requirement is to identify the act that provides for possible treble damages. Answer (a) is correct because only the Racketeer Influenced and Corrupt Organizations Act provides for potential treble damages.

45. (c) Under the Private Securities Litigation Reform Act, the auditor should inform first the audit committee or the board of directors. Answer (a) is incorrect because the Securities Litigation Reform Act does not require that the SEC be informed unless after the audit committee or board of directors is informed, no remedial action is taken. Answer (b) is incorrect because the Justice Department need not be informed of this under the Private Securities Litigation Reform Act. Answer (d) is incorrect because inclusion of the problem in a note of the financial statements is not enough; the audit committee or the board of directors should be informed.

46. (a) The Private Securities Litigation Reform Act requires that auditors of firms covered under the Securities Exchange Act of 1934 establish procedures to do the items in (b), (c), and (d). Developing a comprehensive internal control system is not specifically mentioned, although part of this would be helpful in accomplishing the three stated items.

47. (d) Under the Private Securities Litigation Reform Act, an auditor who audits financial statements under the Federal Securities Exchange Act of 1934 is required to establish procedures to (1) detect illegal acts, (2) identify material related-party transactions, and (3) evaluate the ability of the firm to continue as a going concern.

48. (b) Under the Private Securities Litigation Reform Act, he is required to report this to the audit committee of the firm or the board of directors. Answer (a) is incorrect because he need not report this to the shareholders but to the audit committee or the board of directors. Answers (c) and (d) are incorrect because he is required under the Reform Act to inform the audit committee or the board of directors.

49. (c) The Private Securities Litigation Reform Act amends both the 1933 and 1934 Acts. Answer (a) is incorrect because it applies to the 1933 and 1934 Acts which apply to stocks sold on a stock exchange. Answers (b) and (d) are incorrect because this Reform Act applies to securities covered under the 1933 and 1934 Acts which may include both common and preferred stock of a publicly held corporation.

50. (b) Bran is liable under the Private Securities Litigation Reform Act for her proportionate fault of the liability since she acted unknowingly. Answer (a) is incorrect because Bran was determined to be 20% at fault. Answers (c) and (d) are incorrect because the Reform Act changes the joint and several liability for unknowing conduct and substitutes proportionate liability.

51. (c) The Sarbanes-Oxley Act of 2002 established a number of nonattest services that may not be performed by the auditor for a public company. Tax services may be performed but must be approved by the company’s audit committee.

52. (c) The Sarbanes-Oxley Act established the Public Accounting Oversight Board to regulate CPA firms that audit public companies.

53. (d) The requirement is to identify the provision that is not part of the Sarbanes-Oxley Act of 2002. Answer (d) is correct because Sarbanes-Oxley does not contain a provision for minimum partner experience. All of the others items are provisions of Sarbanes-Oxley.

54. (a) The requirement is to identify the individuals who must personally certify to the accuracy of the financial statements filed with the SEC. Answer (a) is correct because only the chief financial officer and the chief executive officer must certify.

55. (c) The requirement is to identify when a Form 8-K must be filed with the SEC. Answer (c) is correct because the form generally must be filed within 4 days of the occurrence of the triggering event.

56. (b) The requirement is to identify the required partner rotation period under the Sarbanes-Oxley Act. Answer (b) is correct because the act requires rotation at least every 5 years.

57. (b) The requirement is to determine which act(s) constitute(s) grounds for a tax preparer penalty. A return preparer will be subject to penalty if the preparer knowingly or recklessly discloses information furnished in connection with the preparation of a tax return, unless such information is furnished for quality or peer review, under an administrative order by a regulatory agency, or pursuant to an order of a court. Additionally, a return preparer will be subject to penalty if any part of an understatement of liability with respect to a return or refund claim is due to the preparer’s willful attempt to understate tax liability, or to any reckless or intentional disregard of rules and regulations.

58. (d) The requirement is to determine Water’s responsibility regarding Vee’s unfiled 2008 income tax return. A CPA should promptly inform the client upon becoming aware of the client’s failure to file a required return for a prior year. However, the CPA is not obligated to inform the IRS and the CPA may not do so without the client’s permission, except where required by law. If the CPA is requested to prepare the current year’s return (2013) and the client has not taken action to file the return for the earlier year (2008), the CPA should consider whether to withdraw from preparing the current year’s return and whether to continue a professional relationship with the client. Also, note that the normal statue of limitations for the assessment of a tax deficiency is three years after the due date of the return or three years after the return is filed, whichever is later. Thus, the statute of limitations is still open with regard to 2008 since there is no time limit for the assessment of tax if no tax return was filed.

59. (c) The requirement is to determine which action a tax return preparer must take to avoid tax preparer penalties for a return’s understated tax liability due to a taxpayer’s intentional disregard of regulations. A return preparer may, in good faith, rely without verification upon information furnished by the client or by third parties, and is not required to audit, examine, or review books, records, or documents in order to independently verify the taxpayer’s information. However, the preparer should not ignore the implications of information furnished and should make reasonable inquiries if the furnished information appears incorrect, incomplete, or inconsistent.

60. (d) According to the Statements on Standards for Tax Services, in preparing a tax return a CPA may in good faith rely upon information furnished by the client or third parties without further verification.

61. (d) The requirement is to determine the correct statement regarding the imposition of a preparer penalty for understated corporate tax liability. A return preparer may in good faith rely without verification upon information furnished, and is not required to audit, examine, or review books, records, or documents in order to independently verify a taxpayer’s information. However, the preparer should not ignore the implications of information furnished and should make reasonable inquiries if information appears incorrect, incomplete, or inconsistent.