Module 25: Business Structure

Overview

A sole proprietorship has only one owner, which creates both advantages and disadvantages. A partnership is an association of two or more persons to carry on a business as co-owners for profit. The major areas tested about partnerships are the characteristics of a partnership, comparisons with other structures, rights and liabilities of the partnership itself, the rights, duties, and liabilities of the partners among themselves and to third parties, the allocation of profits and losses, and the rights of various parties, including creditors, upon dissolution.

A. Nature of Sole Proprietorships

B. Nature of Partnerships

C. Formation of Partnership

D. Partners’ Rights and Operation of Partnership

E. Relationship to Third Parties

F. Termination of a Partnership

G. Limited Partnerships

H. Joint Ventures

I. Limited Liability Companies (LLC)

J. Limited Liability Partnerships (LLP)

K. Subchapter C Corporations

L. Characteristics and Advantages of Corporate Form

M. Disadvantages of Corporate Business Structure

N. Types of Corporations

O. Formation of Corporation

P. Corporate Financial Structure

Q. Powers and Liabilities of Corporation

R. Directors and Officers of Corporations

S. Stockholder’s Rights

T. Stockholder’s Liability

U. Substantial Change in Corporate Structure

V. Subchapter S Corporation

Key Terms

Multiple-Choice Questions

Multiple-Choice Answers and Explanations

Simulation

Simulation Solution

The law of joint ventures is similar to that of partnerships with some exceptions. Note that the joint venture is more limited in scope than the partnership form of business. The former is typically organized to carry out one single business undertaking or a series of related undertakings; whereas, the latter is formed to conduct ongoing business.

Subchapter S corporations are those corporations that elect to be taxed similar to partnerships under Subchapter S. Corporations that do not make this election are called Subchapter C corporations. In both cases, a corporation is an artificial person that is created by or under law and which operates under a common name through its elected management. It is a legal entity, separate and distinct from its shareholders. The corporation has the authority vested in it by statute and its corporate charter. The candidate should understand the characteristics and advantages of the corporate form over other forms of business organization.

Basic to preparation for questions on corporation law is an understanding of the following: the liabilities of a promoter who organizes a new corporation; the liability of shareholders; the liability of the corporation with respect to the preincorporation contracts made by the promoter; the fiduciary relationship of the promoter to the stockholders and to the corporation; the various circumstances under which a stockholder may be liable for the debts of the corporation; the rights of shareholders particularly concerning payment of dividends; the rights and duties of officers, directors, and other agents or employees of the corporation to the corporation, to stockholders, and to third persons; subscriptions; and the procedures necessary to merge, consolidate, or otherwise change the corporate structure.

State laws are now widely based on the Revised Business Corporation Act upon which changes to this module are based.

For all the business structures listed in this module you should know the basic characteristics of each. The Examiners expect you to understand the basic strengths and weaknesses of each business structure and to be able to select the appropriate business structure for given situations. Before beginning the reading you should review the key terms at the end of the module.

A. Nature of Sole Proprietorships

B. Nature of Partnerships

C. Formation of Partnership

D. Partner’s Rights and Operation of Partnership

E. Relationship to Third Parties

F. Termination of a Partnership

G. Limited Partnerships

H. Joint Ventures

I. Limited Liability Companies (LLC)

J. Limited Liability Partnerships (LLP)

K. Subchapter C Corporations

L. Characteristics and Advantages of Corporate Form

M. Disadvantages of Corporate Business Structure

N. Types of Corporations

O. Formation of Corporation

P. Corporate Financial Structure

Q. Powers and Liabilities of Corporation

R. Directors and Officers of Corporations

S. Stockholder’s Rights

T. Stockholder’s Liability

U. Substantial Change in Corporate Structure

V. Subchapter S Corporation

KEY TERMS

Business judgment rule. Officers and/or directors of a corporation will not breach their fiduciary duty of care by simply making a poor business decision. Rather their action must be negligent to breach the duty of care.

C corporation. The assumed corporate form unless party affirmatively selects S corporation status. The typical form for large publically traded companies subject to double taxation. Generally, no personal liability for shareholders.

Derivative action. When a shareholder, or group of shareholders, sue, on behalf of the corporation a director or corporate officer for damages caused to the corporation.

Dissociation. When a partner is no longer affiliated with the partnership.

Dissolution. The process of ending a partnership.

General partnership. An association of two or more persons to carry on a business as co-owners for profit. Partners have unlimited personal liability.

Joint venture. An association of two or more persons/entities engaged in a business for a specific purpose.

Limited liability company (LLC). A business entity that is run primarily like a general partnership, but affords its members (owners) limited liability.

Limited liability partnership. A general partnership that affords its partners limited liability from the actions of the other partners.

Limited partner. In a limited partnership this partner has no personal liability; however, the limited partner is not allowed to participate in the running of the business.

Limited partnership. A partnership with two types of partners; general and limited. General partners have unlimited liability; limited partners have no personal liability.

Partnership agreement. The rules by which a partnership is run. When a partnership agreement is silent about a particular rule, then the Revise Uniform Partnership Act (RUPA) will apply to the situation.

Partnership interest. The partner’s right to profits. This is freely transferable. Contrast this with the ownership interest, the right to be a partner, which can only be transferred with the consent of all the other partners.

S-corporation. A type of corporation which must be affirmatively elected by the organizers. Taxed like a partnership, but the shareholders have no personal liability.

Sole proprietorship. One-owner business, owner has unlimited liability.

Ultra vires (Latin). An action that goes beyond the power or the authority of the corporation. Such actions violate the fiduciary duty of obedience.

Winding up. The liquidation of the partnership.

Multiple-Choice Questions (1–97)

A. Nature of Sole Proprietorships

1. Which of the following statements is not true of a sole proprietorship?

a. Federal and state governments typically require a formal filing with the appropriate government officials whether or not the sole proprietorship uses a fictitious name.

b. The sole proprietorship is not a separate legal entity apart from its owner.

c. The capital to start the business is generally limited to the funds the sole proprietor either has or can borrow.

d. It is generally considered to be the simplest type of business structure.

B. Nature of Partnerships

2. A general partnership must

a. Pay federal income tax.

b. Have two or more partners.

c. Have written articles of partnership.

d. Provide for apportionment of liability for partnership debts.

3. Which of the following can be a partnership?

a. Karen and Sharon form a charitable organization in which they received donations to give to their favorite charities.

b. Frank and Pablo are members of a union at work that has 150 members.

c. Janice and Stanley form a club to encourage business contacts for computer programmers.

d. None of the above.

4. A silent partner in a general partnership

a. Helps manage the partnership without letting those outside the partnership know this.

b. Retains unlimited liability for the debts of the partnership.

c. Both of the above are correct.

d. None of the above is correct.

C. Formation of Partnership

5. A partnership agreement must be in writing if

a. Any partner contributes more than $500 in capital.

b. The partners reside in different states.

c. The partnership intends to own real estate.

d. The partnership’s purpose cannot be completed within one year of formation.

D. Partner’s Rights and Operation of Partnership

6. Sydney, Bailey, and Calle form a partnership under the Revised Uniform Partnership Act. During the first year of operation, the partners have fundamental questions regarding the rights and obligations of the partnership as well as the individual partners. Which of the following questions can correctly be answered in the affirmative?

I. Is the partnership allowed legally to own property in the partnership’s name?

II. Do the partners have joint and several liability for breaches of contract of the partnership?

III. Do the partners have joint and several liability for tort actions against the partnership?

a. I only.

b. I and II only.

c. II and III only.

d. I, II, and III.

7. Which of the following is not true of a general partnership?

a. Ownership by the partners may be unequal.

b. It is a separate legal entity.

c. An important characteristic is that the partners share in the profits equally.

d. The partner may agree on unequal rights to participate in management.

8. The partnership agreement for Owen Associates, a general partnership, provided that profits be paid to the partners in the ratio of their financial contribution to the partnership. Moore contributed $10,000, Noon contributed $30,000, and Kale contributed $50,000. For the year ended December 31, 2012, Owen had losses of $180,000. What amount of the losses should be allocated to Kale?

a. $ 40,000

b. $ 60,000

c. $ 90,000

d. $100,000

9. Lark, a partner in DSJ, a general partnership, wishes to withdraw from the partnership and sell Lark’s interest to Ward. All of the other partners in DSJ have agreed to admit Ward as a partner and to hold Lark harmless for the past, present, and future liabilities of DSJ. As a result of Lark’s withdrawal and Ward’s admission to the partnership, Ward

a. Acquired only the right to receive Ward’s share of DSJ profits.

b. Has the right to participate in DSJ’s management.

c. Is personally liable for partnership liabilities arising before and after being admitted as a partner.

d. Must contribute cash or property to DSJ to be admitted with the same rights as the other partners.

10. Cobb, Inc., a partner in TLC Partnership, assigns its partnership interest to Bean, who is not made a partner. After the assignment, Bean asserts the rights to

I. Participate in the management of TLC.

II. Cobb’s share of TLC’s partnership profits.

Bean is correct as to which of these rights?

a. I only.

b. II only.

c. I and II.

d. Neither I nor II.

E. Relationship to Third Parties

11. The apparent authority of a partner to bind the partnership in dealing with third parties

a. Will be effectively limited by a formal resolution of the partners of which third parties are aware.

b. Will be effectively limited by a formal resolution of the partners of which third parties are unaware.

c. Would permit a partner to submit a claim against the partnership to arbitration.

d. Must be derived from the express powers and purposes contained in the partnership agreement.

12. In a general partnership, which of the following acts must be approved by all the partners?

a. Dissolution of the partnership.

b. Admission of a partner.

c. Authorization of a partnership capital expenditure.

d. Hiring an employee.

13. Under the Revised Uniform Partnership Act, partners have joint and several liability for

a. Breaches of contract.

b. Torts committed by one of the partners within the scope of the partnership.

c. Both of the above.

d. None of the above.

14. Which of the following actions require(s) unanimous consent of the partners under partnership law?

I. Making partnership a surety.

II. Admission of a new partner.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

15. Which of the following statements best describes the effect of the assignment of an interest in a general partnership?

a. The assignee becomes a partner.

b. The assignee is responsible for a proportionate share of past and future partnership debts.

c. The assignment automatically dissolves the partnership.

d. The assignment transfers the assignor’s interest in partnership profits and surplus.

F. Termination of a Partnership

16. Under the Revised Uniform Partnership Act, in which of the following cases will property be deemed to be partnership property?

I. A partner acquires property in the partnership name.

II. A partner acquires title to it in his/her own name using partnership funds.

III. Property owned previously by a partner is used in the partnership business.

a. I only.

b. I and II only.

c. II only.

d. I, II, and III.

17. Wind, who has been a partner in the PLW general partnership for four years, decides to withdraw from the partnership despite a written partnership agreement that states, “no partner may withdraw for a period of five years.” Under the Uniform Partnership Act, what is the result of Wind’s withdrawal?

a. Wind’s withdrawal causes a dissolution of the partnership by operation of law.

b. Wind’s withdrawal has no bearing on the continued operation of the partnership by the remaining partners.

c. Wind’s withdrawal is not effective until Wind obtains a court-ordered decree of dissolution.

d. Wind’s withdrawal causes a dissolution of the partnership despite being in violation of the partnership agreement.

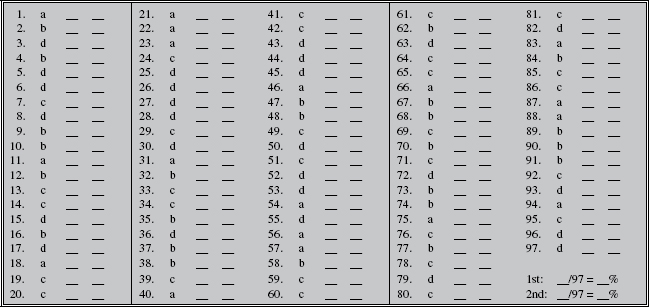

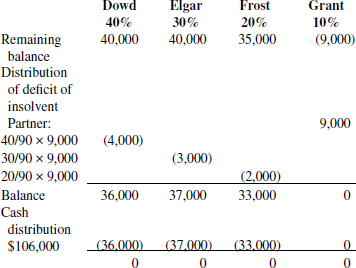

18. Dowd, Elgar, Frost, and Grant formed a general partnership. Their written partnership agreement provided that the profits would be divided so that Dowd would receive 40%; Elgar, 30%; Frost, 20%; and Grant, 10%. There was no provision for allocating losses. At the end of its first year, the partnership had losses of $200,000. Before allocating losses, the partners’ capital account balances were: Dowd, $120,000; Elgar, $100,000; Frost, $75,000; and Grant, $11,000. Grant refuses to make any further contributions to the partnership. Ignore the effects of federal partnership tax law.

After losses were allocated to the partners’ capital accounts and all liabilities were paid, the partnership’s sole asset was $106,000 in cash. How much would Elgar receive on dissolution of the partnership?

a. $37,000

b. $40,000

c. $47,500

d. $50,000

G. Limited Partnerships

19. Which of the following statements is correct with respect to a limited partnership?

a. A limited partner may not be an unsecured creditor of the limited partnership.

b. A general partner may not also be a limited partner at the same time.

c. A general partner may be a secured creditor of the limited partnership.

d. A limited partnership can be formed with limited liability for all partners.

20. Sharif, Hirsch, and Wolff formed a limited partnership with Sharif and Hirsch as general partners. Wolff was the limited partner. They failed to agree upon a profit-sharing plan but put in capital contributions of $120,000, $140,000, and $150,000, respectively. At the end of the first year how should they divide the profits?

a. Sharif and Hirsch each receives half and Wolff receives none.

b. Each of the three partners receives one-third.

c. The profits are shared in proportion to their capital contribution.

d. None of the above.

21. Which of the following is (are) true of a limited partnership?

I. Limited partnerships must have at least one general partner.

II. The death of a limited partner terminates the partnership.

a. I only.

b. II only.

c. Neither I nor II.

d. Both I and II.

22. Alchorn, Black, and Chan formed a limited partnership with Chan becoming the only limited partner. Capital contributions from these partners were $20,000, $40,000, and $50,000, respectively. Chan, however, helped in the management of the partnership and Ham, who had several contracts with the partnership, thought Chan was a general partner. Ham won several breach of contract actions against the partnership and the partnership does not have sufficient funds to pay these claims. What is the potential liability for Alchorn, Black, and Chan?

a. Unlimited liability for all three partners.

b. Unlimited liability for Alchorn and Black; $50,000 for Chan.

c. Up to each partner’s capital contribution.

d. None of the above.

23. To create a limited partnership, a certificate of limited partnership must be filed with the Secretary of State. Which of the following must be included in this certificate under the Revised Uniform Limited Partnership Act?

I. Names of all of the general partners.

II. Names of the majority of the general partners.

III. Names of all of the limited partners.

IV. Names of the majority of the limited partners.

a. I only.

b. II only.

c. I and III only.

d. I and IV only.

24. Mandy is a limited partner in a limited partnership in which Strasburg and Hua are the general partners. Which of the following may Mandy do without losing limited liability protection?

I. Mandy acts as an agent of the limited partnership.

II. Mandy votes to remove Strasburg as a general partner.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

25. In a limited partnership, the limited partners’ capital contribution may be in which of the following forms?

a. A promise to perform services in the future for the partnership.

b. An agreement to pay cash.

c. A promise to give property.

d. All of the above.

26. Hart and Grant formed Hart Limited Partnership. Hart put in a capital contribution of $20,000 and became a general partner. Grant put in a capital contribution of $10,000 and became a limited partner. During the second year of operation, a third party filed a tort action against the partnership and both partners. What is the potential liability of Hart and Grant respectively?

a. $20,000 and $0.

b. $20,000 and $10,000.

c. Unlimited liability and $0.

d. Unlimited liability and $10,000.

27. The admission of a new general partner to a limited partnership requires approval by

I. A majority of the general partners.

II. All of the general partners.

III. A majority of the limited partners.

IV. All of the limited partners.

a. I only.

b. II only.

c. I and III only.

d. II and IV only.

28. The admission of a new limited partner to a limited partnership requires approval by

I. A majority of the general partners.

II. All of the general partners.

III. A majority of the limited partners.

IV. All of the limited partners.

a. I only.

b. II only.

c. I and III only.

d. II and IV only.

29. Riewerts, Morgan and Stonk form a limited partnership. Riewerts is the one general partner. Which of the following events will cause this limited partnership to be dissolved?

I. Riewerts dies and is survived by the other two partners.

II. Morgan dies leaving Riewerts and Stonk.

III. Riewerts takes out personal bankruptcy.

IV. Stonk takes out personal bankruptcy.

a. I only.

b. I and II only.

c. I and III only.

d. III and IV only.

H. Joint Ventures

30. Which of the following is not true of a joint venture?

a. Each joint venturer is personally liable for the debts of a joint venture.

b. Each joint venturer has the right to participate in the management of the joint venture.

c. The joint venturers owe each other fiduciary duties.

d. Death of a joint venturer dissolves the joint venture.

I. Limited Liability Companies (LLC)

31. Which form(s) of a business organization can have characteristics common to both the corporation and the general partnership?

| Limited liability company | Subchapter S corporation | |

| a. | Yes | Yes |

| b. | Yes | No |

| c. | No | Yes |

| d. | No | No |

32. Which of the following is true of a limited liability company under the laws of the majority of states?

a. At least one of the owners must have personal liability.

b. The limited liability company is a separate legal entity apart from its owners.

c. Limited liability of the owners is lost if they fail to follow the usual formalities in conducting the business.

d. All of the above are true.

33. Which of the following is not characteristic of the typical limited liability company?

a. Death of a member (owner) causes it to dissolve unless the remaining members decide to continue the business.

b. All members (owners) are allowed by law to participate in the management of the firm.

c. The company has, legally, a perpetual existence.

d. All members (owners) have limited liability.

34. Owners and managers of a limited liability company (LLC) owe

a. A duty of due care.

b. A duty of loyalty.

c. Both a duty of due care and a duty of loyalty.

d. None of the above.

35. Which of the following is true of the typical limited liability company?

a. It provides for limited liability for some of its members (owners), that is, those identified as limited members (owners).

b. The members’ (owners’) interests are not freely transferable.

c. Voting members (owners) but not all members can help choose the managers of the company.

d. No formalities are required for its formation.

J. Limited Liability Partnerships (LLP)

36. In which of the following respects do general partnerships and limited liability partnerships differ?

I. In the level of liability of the partners for torts they themselves commit.

II. In the level of liability of the partners for torts committed by other partners in the same firm.

III. In the amount of liability of the partners for contracts signed by other partners on behalf of the partnership.

a. I only.

b. II only.

c. I and II only.

d. II and III only.

K. Subchapter C Corporations

37. Under the federal Subchapter S Revision Act, all corporations are designated as

a. Subchapter S corporations only.

b. Either a Subchapter S corporation or a Subchapter C corporation.

c. One of seven different types of corporations.

d. Both a Subchapter S corporation and a Subchapter C corporation at the same time.

38. Under the federal Subchapter S Revision Act all corporations are

a. Now treated as Subchapter S corporations.

b. Divided into either a Subchapter C corporation or a Subchapter S corporation.

c. Divided into either a Subchapter C corporation, a Subchapter E corporation, or a Subchapter S corporation.

d. None of the above.

39. Which of the following statements is (are) true?

a. Both Subchapter C corporations and Subchapter S corporations have limited liability for their shareholders.

b. Both Subchapter C corporations and Subchapter S corporations are similar in their corporate management structure.

c. All of the above are true.

d. None of the above are true.

40. The main difference between Subchapter S corporations and Subchapter C corporations is

a. Their tax treatment.

b. That the federal Subchapter S Revision Act covers Subchapter S corporations but does not cover Subchapter C corporations.

c. Their limited liability of their shareholders.

d. Their structure of their corporate management.

L. Characteristics and Advantages of Corporate Form

41. Which of the following statements best describes an advantage of the corporate form of doing business?

a. Day-to-day management is strictly the responsibility of the directors.

b. Ownership is contractually restricted and is not transferable.

c. The operation of the business may continue indefinitely.

d. The business is free from state regulation.

42. Which of the following is not considered to be an advantage of the corporate form of doing business over the partnership form?

a. A potential perpetual and continuous life.

b. The interests in the corporation are typically easily transferable.

c. The managers in the corporation and shareholders have limited liability.

d. Persons who manage the corporation are not necessarily shareholders.

43. Which of the following is not a characteristic of a corporation?

a. It has a continuous life.

b. Shares in the corporation can normally be freely transferred.

c. A corporation is treated as a legal entity separate from its shareholders.

d. A corporation is automatically terminated upon the death of a majority of its shareholders.

44. A corporation as a separate legal entity can do which of the following?

a. Contract in its own name with its own shareholders.

b. Contract in its own name with its own shareholders only if a majority of its shareholders agree that such a contract can be made.

c. Contract in its own name with third parties.

d. Both a. and c. are correct.

45. Which of the following are characteristics of the corporate form of doing business?

a. Persons who manage corporations need not be shareholders.

b. The corporation may convey or hold property in its own name.

c. The corporation can sue or be sued in its own name.

d. All of the above are true.

M. Disadvantages of Corporate Business Structure

46. Which of the following is a disadvantage of a Subchapter C corporation?

a. It may face higher tax burdens than a Subchapter S corporation.

b. The shareholders lose their limited liability when they switch from a general partnership to a corporation.

c. A Subchapter C corporation is not well defined under the law.

d. A Subchapter C corporation does not protect its shareholders from liability as well as a Subchapter S corporation does.

N. Types of Corporations

47. Bond Company is incorporated in Florida but not in Georgia. Bond has branch offices in both states. Which of the following is correct?

I. Bond is a domestic corporation in Georgia.

II. Bond is a domestic corporation in Florida.

III. Bond needs to incorporate also in Georgia.

a. I and II only.

b. II only.

c. II and III only.

d. I, II, and III.

48. Colby formed a professional corporation along with two other attorneys. They took out loans in the name of the corporation. During the first year, Colby failed to file some papers on time for a client causing the client to lose a very good case. For which does Colby have the corporate protection of limited liability?

I. The negligence for failure to file the papers on time.

II. The corporate loans.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

49. Macro Corporation was incorporated and doing business in Illinois. It is doing business in various other states including Nevada. Which of the following statements is (are) true?

a. Macro must incorporate in Nevada.

b. Macro is a domestic corporation in Nevada.

c. Macro is a domestic corporation in Illinois.

d. All of the above are true.

50. Cleanit Corporation was incorporated in Colorado. Cleanit wishes to perform some transactions in other states but does not want to incorporate or obtain a certificate of authority to qualify to do business in those other states. Which of the following normally would require Cleanit to obtain a certificate of authority in other states?

a. Using the US mail to solicit orders in those states.

b. Holding bank accounts in those states.

c. Collecting debts in those states.

d. None of the above.

51. Which of the following statements is true of professional corporations under the various state laws?

I. The professionals in the corporation have personal liability for their professional acts.

II. Normally under state laws, only licensed professionals are permitted to own shares in professional corporations.

a. I only is true.

b. II only is true.

c. Both I and II are true.

d. Neither I nor II is true.

O. Formation of Corporation

52. Which of the following statements is correct with respect to the differences and similarities between a corporation and a limited partnership?

a. Stockholders may be entitled to vote on corporate matters but limited partners are prohibited from voting on any partnership matters.

b. Stock of a corporation may be subject to the registration requirements of the federal securities laws but limited partnership interests are automatically exempt from those requirements.

c. Directors owe fiduciary duties to the corporation and limited partners owe such duties to the partnership.

d. A corporation and a limited partnership may be created only under a state statute and each must file a copy of its organizational document with the proper governmental body.

53. Under the Revised Model Business Corporation Act, which of the following must be contained in a corporation’s Articles of Incorporation?

a. Quorum voting requirements.

b. Names of stockholders.

c. Provisions for issuance of par and nonpar shares.

d. The number of shares the corporation is authorized to issue.

54. Which of the following facts is (are) generally included in a corporation’s Articles of Incorporation?

| Name of registered agent | Number of authorized shares | |

| a. | Yes | Yes |

| b. | Yes | No |

| c. | No | Yes |

| d. | No | No |

55. Absent a specific provision in its Articles of Incorporation, a corporation’s board of directors has the power to do all of the following, except

a. Repeal the bylaws.

b. Declare dividends.

c. Fix compensation of directors.

d. Amend the Articles of Incorporation.

56. Which of the following statements is correct concerning the similarities between a limited partnership and a corporation?

a. Each is created under a statute and must file a copy of its certificate with the proper state authorities.

b. All corporate stockholders and all partners in a limited partnership have limited liability.

c. Both are recognized for federal income tax purposes as taxable entities.

d. Both are allowed statutorily to have perpetual existence.

57. Promoters of a corporation which is not yet in existence

a. Are persons that form the corporation and arrange for capitalization to help begin the corporation.

b. Are agents of the corporation.

c. Can bind the future corporation to presently made contracts they make for the future corporation.

d. Are shielded from personal liability on contracts they make with third parties on behalf of the future corporation.

P. Corporate Financial Structure

58. Johns owns 400 shares of Abco Corp. cumulative preferred stock. In the absence of any specific contrary provisions in Abco’s Articles of Incorporation, which of the following statements is correct?

a. Johns is entitled to convert the 400 shares of preferred stock to a like number of shares of common stock.

b. If Abco declares a cash dividend on its preferred stock, Johns becomes an unsecured creditor of Abco.

c. If Abco declares a dividend on its common stock, Johns will be entitled to participate with the common stock shareholders in any dividend distribution made after preferred dividends are paid.

d. Johns will be entitled to vote if dividend payments are in arrears.

59. Gallagher Corporation issued 100,000 shares of $40 par value stock for $50 per share to various investors. Subsequently, Gallagher purchased back 10,000 of those shares for $30 per share and held them as treasury stock. When the price of the stock recovered somewhat, Gallagher sold this treasury stock to Thomas for $35 per share. Which of the following statements is correct?

I. Gallagher’s purchase of the stock at below par value is illegal.

II. Gallagher’s purchase of the stock at below par value is void as an ultra vires act.

III. Gallagher’s resale of the treasury stock at below par value is valid.

a. I only.

b. II only.

c. III only.

d. I and II only.

60. An owner of common stock will not have any liability beyond actual investment if the owner

a. Paid less than par value for stock purchased in connection with an original issue of shares.

b. Agreed to perform services that were worth less than par value for the corporation in exchange for original issue par value shares.

c. Purchased treasury shares for less than par value.

d. Failed to pay the full amount owed on a subscription contract for no-par shares.

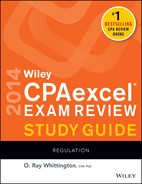

61. Which of the following securities are corporate debt securities?

62. All of the following distributions to stockholders are considered asset or capital distributions, except

a. Liquidating dividends.

b. Stock splits.

c. Property distributions.

d. Cash dividends.

63. Which of the following constitute(s) valid consideration or value to purchase shares of stock?

a. Services performed.

b. Intangible property.

c. Services contracted to be performed in the future.

d. All of the above.

64. Brawn subscribed to 1,000 shares of $1 par value stock of Caldo Corporation at the agreed amount of $20 per share. She paid $5,000 on April 1 and then paid $9,000 on August 1. Caldo Corporation filed for bankruptcy on December 1 and the creditors of the corporation sought to hold Brawn liable under her subscription agreement. Which of the following is true?

a. Brawn has no liability to the creditors because subscription contract was with the corporation, not the creditors.

b. Brawn has no liability to the creditors because she has paid more than $1,000 to the corporation which is the par value of the 1,000 shares.

c. Brawn is liable for $6,000 to the creditors for the amount unpaid on the subscription price.

d. Brawn is liable for $6,000 to the creditors based on the doctrine of ultra vires.

65. Pearl Corporation has some treasury stock on hand. Which of the following is (are) true?

a. Pearl may not vote these shares of treasury stock.

b. Pearl’s treasury stock does not receive any dividends.

c. Both of the above statements are true.

d. None of the above statements are true.

66. Treasury stock of a corporation is stock that

a. Has been issued by that corporation but is not outstanding.

b. Was purchased from another corporation and is retained for a specified purpose.

c. Has been cancelled.

d. None of the above is true.

67. By law, a corporation

a. Must issue both common stock and preferred stock.

b. May issue more than one class of common stock as well as more than one class of preferred stock.

c. Must issue dividends if it has earned a profit.

d. Must issue at least some cumulative preferred stock.

68. Mesa Corporation is planning on issuing some debt securities. Which of the following statements is true?

a. The holders of debt securities are owners of the corporation.

b. A bond is an instrument for long-term secured debt.

c. A debenture is an instrument for long-term secured debt.

d. None of the above is true.

69. Stock of a corporation is called watered stock when the cash or property exchanged to acquire the stock is

a. Less than the market value of the stock.

b. More than the market value of the stock.

c. Less than the par value or stated value of the stock.

d. More than the par value or stated value of the stock.

Q. Powers and Liabilities of Corporation

70. Corporations generally have which of the following powers without shareholder approval?

I. Power to acquire their own shares.

II. Power to make charitable contributions.

III. Power to make loans to directors.

a. I only.

b. I and II only.

c. II and III only.

d. I, II, and III.

71. Murphy is an employee of Landtry Corporation. Which of the following acts would make the corporation liable for Murphy’s actions?

I. Murphy deceived a customer to convince him to purchase one of Landtry’s products.

II. Murphy hit a customer with his fist, breaking his jaw. The management had warned Murphy that he and not the corporation would be responsible for any aggression against customers.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

72. Which of the following statements is (are) true?

I. Corporations can be found liable for crimes.

II. Directors can face prison sentences for crimes committed by their corporations.

III. Employees can be found guilty of crimes they commit while working for their corporation.

a. I only.

b. I and II only.

c. III only.

d. I, II, and III.

R. Directors and Officers of Corporations

73. Norwood was a promoter of Parker Corporation. On March 15, Norwood purchased some real estate from Burrows in Parker’s name and signed the contract “Norwood, as agent of Parker Corporation.” Parker Corporation, however, did not legally come into existence until June 10. Norwood never informed Burrows on or before March 15 that Parker Corporation was not yet formed. After the corporation was formed, the board of directors refused to adopt the preincorporation contract made by Norwood concerning the real estate deal with Burrows. Burrows sued Parker, Norwood, and the board of directors. Which of the following is correct?

a. None of these parties can be held liable.

b. Norwood only is liable.

c. Norwood and Parker are liable but not the board of directors.

d. Norwood, Parker, and the board of directors are all liable.

74. Under the Revised Model Business Corporation Act, which of the following statements is correct regarding corporate officers of a public corporation?

a. An officer may not simultaneously serve as a director.

b. A corporation may be authorized to indemnify its officers for liability incurred in a suit by stockholders.

c. Stockholders always have the right to elect a corporation’s officers.

d. An officer of a corporation is required to own at least one share of the corporation’s stock.

75. The officers of West Corporation wish to buy some used equipment for West Corporation. The used equipment is actually owned by Parks, a director of West Corporation. For this transaction to not be a conflict of interest for Parks, which of the following is (are) required to be true?

I. Parks sells the used equipment to West Corporation in a contract that is fair and reasonable to the corporation.

II. Parks’ ownership of the used equipment is disclosed to the shareholders of West who approve it by majority vote.

III. Parks’ ownership of the used equipment is disclosed to the board of directors, who approve it by a majority vote of the disinterested directors.

a. Any one of I, II, or III.

b. I and II are both required.

c. I and III are both required.

d. All three of I, II, and III are required.

76. The following are two statements concerning a fiduciary duty in a corporation.

I. Officers and directors of a corporation owe a fiduciary duty to that corporation.

II. Majority shareholders of a corporation can owe a fiduciary duty to the minority shareholders.

Which of the statements is (are) correct?

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

77. Hogan is a director of a large corporation. Hogan owns a piece of land that the corporation wishes to purchase and Hogan desires to sell this land at the fair market price. If he sells the land to the corporation, has he breached any fiduciary duty?

a. No, a director does not owe a fiduciary duty to his corporation.

b. No, since Hogan is selling the land to his corporation in a fair and reasonable contract.

c. Yes, unless he discloses his conflict of interest to the shareholders who must then approve the sale of by a simple majority.

d. Yes, unless he discloses his conflict of interest to the shareholders who must then approve the sale by a two-thirds vote.

78. Which of the following is not a power of the board of directors?

a. May select the officers of the corporation.

b. May declare the dividends to be paid to the shareholders.

c. May amend the Articles of Incorporation.

d. All of the above are powers of the board of directors.

79. Which of the following statements is (are) true under the law affecting corporations?

I. A corporation may indemnify directors against lawsuits based on their good-faith actions for the corporation.

II. A corporation may indemnify officers against lawsuits based on their good-faith actions for the corporation.

III. A corporation is allowed to purchase liability insurance for its directors.

a. I only.

b. I and II only.

c. I and III only.

d. I, II, and III.

80. Which of the following is (are) true concerning corporations?

a. Directors owe a fiduciary duty to the corporation.

b. Officers owe a fiduciary duty to the corporation.

c. Both of the above are true.

d. None of the above are true.

81. McGarry is an officer of Norton Corporation. McGarry has committed a tort while acting for Norton Corporation within the scope of her authority. Which of the following is (are) true?

a. Only McGarry is liable for the tort committed.

b. Only Norton Corporation is liable for the tort committed.

c. Both McGarry and Norton are liable for the tort committed.

d. Neither McGarry nor Norton are liable for the tort committed.

S. Stockholders’ Rights

82. Acorn Corp. wants to acquire the entire business of Trend Corp. Which of the following methods of business combination will best satisfy Acorn’s objectives without requiring the approval of the shareholders of either corporation?

a. A merger of Trend into Acorn, whereby Trend shareholders receive cash or Acorn shares.

b. A sale of all the assets of Trend, outside the regular course of business, to Acorn for cash.

c. An acquisition of all the shares of Trend through a compulsory share exchange for Acorn shares.

d. A cash tender offer, whereby Acorn acquires at least 90% of Trend’s shares, followed by a short-form merger of Trend into Acorn.

83. Price owns 2,000 shares of Universal Corp.’s $10 cumulative preferred stock. During its first year of operations, cash dividends of $5 per share were declared on the preferred stock but were never paid. In the second year, dividends on the preferred stock were neither declared nor paid. If Universal is dissolved, which of the following statements is correct?

a. Universal will be liable to Price as an unsecured creditor for $10,000.

b. Universal will be liable to Price as a secured creditor for $20,000.

c. Price will have priority over the claims of Universal’s bond owners.

d. Price will have priority over the claims of Universal’s unsecured judgment creditors.

84. Under the Revised Model Business Corporation Act, when a corporation’s Articles of Incorporation grant stockholders preemptive rights, which of the following rights is (are) included in that grant?

| The right to purchase a proportionate share of a newly issued stock | The right to a proportionate share of corporate assets remaining on corporate dissolution | |

| a. | Yes | Yes |

| b. | Yes | No |

| c. | No | Yes |

| d. | No | No |

85. Under the Revised Model Business Corporation Act, which of the following actions by a corporation would entitle a stockholder to dissent from the action and obtain payment of the fair value of his/her shares?

I. An amendment to the articles of incorporation that materially and adversely affects rights in respect of a dissenter’s shares because it alters or abolishes a preferential right of the shares.

II. Consummation of a plan of share exchange to which the corporation is a party as the corporation whose shares will be acquired, if the stockholder is entitled to vote on the plan.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

86. To which of the following rights is a stockholder of a public corporation entitled?

a. The right to have annual dividends declared and paid.

b. The right to vote for the election of officers.

c. The right to a reasonable inspection of corporate records.

d. The right to have the corporation issue a new class of stock.

87. Which of the following is correct pertaining to the rights of stockholders in a corporation?

a. Stockholders have no right to manage their corporation unless they are also directors or officers.

b. Stockholders have a right to receive dividends.

c. Stockholders have no right to inspect the books and records of their corporation.

d. Stockholders have a right to get a list of their corporation’s customers to use for the stockholder’s personal business mailing list.

T. Stockholders’ Liability

88. The limited liability of a stockholder in a closely held corporation may be challenged successfully if the stockholder

a. Undercapitalized the corporation when it was formed.

b. Formed the corporation solely to have limited personal liability.

c. Sold property to the corporation.

d. Was a corporate officer, director, or employee.

89. The corporate veil is most likely to be pierced and the shareholders held personally liable if

a. The corporation has elected S corporation status under the Internal Revenue Code.

b. The shareholders have commingled their personal funds with those of the corporation.

c. An ultra vires act has been committed.

d. A partnership incorporates its business solely to limit the liability of its partners.

90. Which of the following is correct about the law of corporations?

a. Each shareholder owes a fiduciary duty to his or her corporation.

b. Majority shareholders owe a fiduciary duty to their corporation.

c. Majority shareholders do not owe a fiduciary duty to minority shareholders.

d. All of the above are correct.

U. Substantial Change in Corporate Structure

91. A parent corporation owned more than 90% of each class of the outstanding stock issued by a subsidiary corporation and decided to merge that subsidiary into itself. Under the Revised Model Business Corporation Act, which of the following actions must be taken?

a. The subsidiary corporation’s board of directors must pass a merger resolution.

b. The subsidiary corporation’s dissenting stockholders must be given an appraisal remedy.

c. The parent corporation’s stockholders must approve the merger.

d. The parent corporation’s dissenting stockholders must be given an appraisal remedy.

92. Under the Revised Model Business Corporation Act, a merger of two public corporations usually requires all of the following except

a. A formal plan of merger.

b. An affirmative vote by the holders of a majority of each corporation’s voting shares.

c. Receipt of voting stock by all stockholders of the original corporations.

d. Approval by the board of directors of each corporation.

93. Which of the following statements is a general requirement for the merger of two corporations?

a. The merger plan must be approved unanimously by the stockholders of both corporations.

b. The merger plan must be approved unanimously by the boards of both corporations.

c. The absorbed corporation must amend its articles of incorporation.

d. The stockholders of both corporations must be given due notice of a special meeting, including a copy or summary of the merger plan.

94. Which of the following must take place for a corporation to be voluntarily dissolved?

a. Passage by the board of directors of a resolution to dissolve.

b. Approval by the officers of a resolution to dissolve.

c. Amendment of the certificate of incorporation.

d. Unanimous vote of the stockholders.

95. A corporate stockholder is entitled to which of the following rights?

a. Elect officers.

b. Receive annual dividends.

c. Approve dissolution.

d. Prevent corporate borrowing.

96. When a consolidation takes place under the law of corporations, which of the following is true?

a. Two or more corporations are joined into one new corporation.

b. All assets are acquired by the new corporation.

c. The new corporation is liable for the debts of each of the old corporations.

d. All of the above are true.

V. Subchapter S Corporation

97. When a corporation elects to be a Subchapter S corporation, which of the following statements is (are) true regarding the federal tax treatment of the corporation’s income or loss?

I. The corporation’s income is taxed at the corporate level and not the shareholders’ level.

II. The shareholders report the corporation’s income on their tax returns when the income is distributed to them.

III. The shareholders report the corporation’s income on their tax returns even if the income is not distributed to them.

IV. The shareholders generally report the corporation’s loss on their tax returns.

a. I only is true.

b. II only is true.

c. III only is true.

d. III and IV only are true.

Multiple-Choice Answers and Explanations

Answers

Explanations

1. (a) Federal or state governments do not typically require any formal filing. If the business operates under a name different from that of the sole proprietor, most states require that a fictitious name statement be filed. Answer (b) is incorrect because the sole proprietorship and the sole proprietor are not separate legal entities. Answer (c) is incorrect because a sole proprietor does not have partners or shareholders from whom to obtain capital. Answer (d) is incorrect because the simplicity of this business structure is one of its advantages in its formation and operation.

2. (b) A general partnership is an association of two or more persons to carry on a business as co-owners for profit. There must be at least two partners involved in order for a partnership to exist. Answer (a) is incorrect because a general partnership is normally not recognized as a taxable entity under federal income tax laws. Answer (c) is incorrect because execution of written articles of partnership is not required to create a general partnership. A partnership agreement may be oral or in writing. Answer (d) is incorrect because a partnership does not have to provide for apportionment of liability for partnership debt. Note that even if the partners agreed to split partnership liability in a specified proportion, third parties can still hold each partner personally liable despite the agreement.

3. (d) A partnership involves two or more persons to carry on a business as co-owners for a profit. Partnerships do not include nonprofit associations such as charitable organizations, labor unions or clubs.

4. (b) A silent partner does not help manage the partnership but still has unlimited liability.

5. (d) A partnership agreement may be expressed or implied based upon the activities and conduct of the partners. The expressed agreement may be oral or in writing with, in general, one exception. A partnership agreement that cannot be completed within one year from the date on which it is entered into must be in writing. Answer (b) is incorrect because the partners may reside in different states without having to put the partnership agreement in writing. Answer (a) is incorrect because the $500 amount applies to the sale of goods which must be in writing, not partnerships. Answer (c) is incorrect because the purpose of the partnership is irrelevant. Agreements to buy and sell real estate must be in writing, while an agreement to form a partnership whose principal activity will involve the buying and selling of real estate normally need not be in writing unless the stated duration exceeds one year.

6. (d) Under RUPA, the partnership is a legal entity that can own property in its own name. The partners also have joint and several liability for all debts whether they are based in contract or tort.

7. (c) The partners may agree to share profits as well as losses unequally. Answer (a) is incorrect because the partners may agree that ownership in the partnership is unequal. Answer (b) is incorrect because under RUPA, the partnership is a separate legal entity. Answer (d) is incorrect because the partners may agree to unequal management rights.

8. (d) Profits and losses in a general partnership are shared equally unless otherwise specified in the partnership agreement. If partners agree on unequal profit sharing but are silent on loss sharing, then losses are shared per the profit sharing proportions. The partnership agreement for Owen Associates provided that profits be paid to the partners in the ratio of their financial contribution to the partnership. The ratios are as follows:

Total contributed $10,000 + 30,000 + 50,000 = $90,000

For the year ended December 31, 2012, Owen had losses of $180,000. Therefore, Kale would be allocated $100,000 of the losses ($180,000 × 5/9).

9. (b) An incoming partner has the same rights as all of the existing partners. Thus, an incoming partner has the right to participate in the management of the partnership. Answer (a) is incorrect since the incoming partner acquires more than just the right to profits. Answer (c) is incorrect since a person admitted as a partner into an existing partnership is only liable for existing debts of the partnership to the extent of the incoming partner’s capital contribution. Answer (d) is incorrect because a partner need not make a capital contribution to be admitted with the same rights as the other partners.

10. (b) A partner is free to assign his interest in any partnership to a third party. However, the assignee does not become a partner by virtue of this assignment, but merely succeeds to the assignor’s rights as to profits and return of partner’s capital contribution. The assignee does not receive the right to manage, to have an accounting, to inspect the books, or to possess or use any individual partnership property. Since Bean was not made a partner, he is entitled to Cobb’s share of TLC’s profits, but does not have the right to participate in the management of TLC.

11. (a) A partner’s apparent authority is derived from the reasonable perceptions of third parties due to the manifestations or representations of the partnership concerning the authority each partner possesses to bind the partnership. However, if third parties are aware of a formal resolution which limits the partner’s actual authority to bind the partnership, then that partner’s apparent authority will also be limited. Answer (b) is incorrect because if third parties are unaware of such a resolution which limits the partner’s actual authority, then the partner retains apparent authority to bind the partnership. Answer (c) is incorrect because third parties should be aware that in order for a partner to submit a claim against the partnership to arbitration, unanimous consent of the partners is needed. Therefore, a partner has no apparent authority to take such an action. Answer (d) is incorrect because as stated above, the apparent authority of a partner to bind the partnership is not derived from the express powers and purposes contained in the partnership agreement.

12. (b) In a general partnership, unanimous consent is required of all of the partners to admit a new partner. Answer (a) is incorrect because any one partner can cause a dissolution by actions such as withdrawing. Answer (c) is incorrect because each partner is an agent of the general partnership and thus may purchase items for the business of the firm. Answer (d) is incorrect; an individual partner may hire an employee because such an action is viewed as within the regular course of business.

13. (c) Under the Revised Uniform Partnership Act, partners have joint and several liability for not only torts but also breaches of contract. This is a change from previous lawand differs from the normal rules of agency law.

14. (c) Although individual partners normally have implied authority to buy and sell goods for the partnership; they do not have implied authority to do such things as making the partnership a surety or admitting a new partner. Such matters are not considered to be the ordinary business of the partnership, and thus require the consent of all partners.

15. (d) A partner’s interest in a partnership is freely assignable without the other partners’ consent. A partner’s interest refers to the partners’ right to share in profits and return of contribution. Answer (a) is incorrect because the assignee does not become a partner without the consent of all the other partners. Answer (b) is incorrect because the assignor remains liable as a partner. The assignee has only received the partner’s right to share in profits and capital return. Answer (c) is incorrect because assignment of a partner’s interest does not cause dissolution unless the assignor also withdraws.

16. (b) Under RUPA, partnership property not only includes property purchased in the partnership name but also includes property purchased by a partner, who is an agent of the partnership, with partnership funds. Note that a partner may use property in the partnership business without it becoming partnership property.

17. (d) Even if a partner has agreed not to withdraw before a certain period of time, s/he has the power to do so anyway. That partner’s withdrawal is a break of contract and causes a dissolution of the partnership. If the remaining partners agreed to continue the partnership, this would prevent the dissolution, but there is no mention of such an agreement in the facts presented here. Answer (a) is incorrect because this dissolution is caused by an act of a partner rather than by operation of law. Answer (b) is incorrect because Wind’s withdrawal does have an effect on the remaining partners because they must decide on what new terms they will operate or else wind up and terminate the partnership. Answer (c) is incorrect because the dissolution is effective once Wind does withdraw from the partnership. A court decree is not necessary.

18. (a) The best approach to answer this question is to make a chart as follows:

A capital deficit may be corrected by the partner investing more cash or assets to eliminate the deficit or by distributing the deficit to the other partners in their resulting profit and loss sharing ratio. The latter was done in this case, as the facts in the question indicated that Grant refuses to make any further contributions to the partnership. The remaining cash is then used to pay the three partners’ capital balances.

19. (c) A general partner has a voice in management and has unlimited personal liability. Anyone, including a secured creditor of the limited partnership, may be a general partner if he/she takes on these responsibilities. Answer (a) is incorrect because an unsecured creditor of the limited partnership may also be a limited partner. A limited partner is defined as having no voice in management and his/her liability is limited to the extent of his/her capital contribution. Answer (b) is incorrect because a general partner may also be a limited partner at the same time. This partner would have the rights, powers, and liability of a general partner, and the rights against other partners with respect to his/her contribution as both a limited and a general partner. Answer (d) is incorrect because every limited partnership must have at least one general partner who will be liable for the partnership obligations.

20. (c) Under the Revised Uniform Limited Partnership Act, when the partners do not agree how to split profits, the split is made in proportion to their capital contributions. Note that this is different for general partners under the Revised Uniform Partnership Act.

21. (a) Limited partnerships must have at least one general partner who has the unlimited personal liability of the firm. Unlike a general partner, the death of a limited partner does not cause a dissolution or termination of a partner.

22. (a) Since Chan acted like a general partner and Ham thought he was a general partner, Chan has the liability of a general partner to Ham. Answers (b), (c), and (d) are incorrect because Ham believed Chan was a general partner based on Chan’s actions. Therefore, Chan had the liability of a general partner, that is, unlimited liability.

23. (a) Under the Revised Uniform Limited Partnership Act, none of the names of the limited partners need to be listed in the certificate of limited partnership that is filed with the Secretary of State. However, all of the general partners must be listed.

24. (c) A limited partner is allowed, without losing the protection of limited liability, to act as an agent of the limited partnership. The limited partner may also vote on the removal of a general partner.

25. (d) Partners’ capital may not only be in cash, property, or services already performed, but also may be in the form of promises to give or perform these at a future date.

26. (d) If the liability is more than the partnership can pay, each partner loses its capital contribution and then the general partner has personal, unlimited liability for the debt.

27. (d) The admission of a new general partner to a limited partnership under the Revised Uniform Limited Partnership Act requires the approval of all partners, including limited partners.

28. (d) The admission of a new limited partner requires the approval of all the partners.

29. (c) Death or bankruptcy of a general partner in a limited partnership will cause dissolution of the limited partnership. However, this is not true if a limited partner dies or goes bankrupt.

30. (d) The law of joint ventures is similar to the law of partnerships with some exceptions. One of these exceptions is that the death of a joint venturer does not automatically dissolve the joint venture. Answers (a), (b), and (c) are all incorrect because these are all examples in which joint venture law and partnership law are similar, involving liability, right to participate in management, and fiduciary duties.

31. (a) A limited liability company provides for limited liability of its members, similar to the limited liability of the shareholders of a corporation. However, it typically has a limited duration of existence, similar to that of a partnership in which the death or withdrawal of a member or partner causes the business to dissolve unless the remaining members or partners choose to continue the business. The limited liability company can also be taxed similar to a partnership if formed to do so. The Subchapter S corporation has the limited liability of the corporation but is taxed similar to a partnership.

32. (b) The limited liability company statutes provide that it is a separate legal entity apart from its owners. Thus it may sue or be sued in its own name. Answer (a) is incorrect because all owners have limited rather than personal liability. Answer (c) is incorrect because limited liability is normally retained even if the owners fail to follow the formalities usual in conducting the business. Answer (d) is incorrect because (b) is correct.

33. (c) Limited liability companies typically have a limited life. Provisions often provide that they exist for thirty years at most and dissolve if a member dies. Therefore (a) is an incorrect response. Answer (b) is also not chosen because members (owners) are permitted to participate in the management of the LLC or can choose the management. Answer (d) is an incorrect response because one of the main benefits of an LLC is the limited liability of its members (owners).

34. (c) Owners and managers of an LLC owe a duty of due care. They also owe a duty to be loyal to their LLC.

35. (b) In the typical limited liability company (LLC), unlike the common corporation, the interests of the members are not freely transferable. The other members have to agree to admit new members. Answer (a) is incorrect because it provides for limited liability of all of its members. Answer (c) is incorrect because all members have a voice in the management of the LLC. Answer (d) is incorrect because a limited liability company must be formed pursuant to the filing requirements of the relevant state statute.

36. (d) In most states a limited liability partnership (LLP), insulates partners from personal liability for all debts and obligations of the partnership regardless of whether those debts arose from contract or tort. Answer (a) is incorrect because both in the LLP and the general partnership, the partners have unlimited liability for their own torts. Answer (b) is incorrect because partners are insulated from contractual debts as well as debts arising from tort. Answer (c) is incorrect because partners have personal liability for their own actions.

37. (b) The federal Subchapter S Revision Act specifies that all corporations that do not meet the criteria of a Subchapter S corporation are categorized as a Subchapter C corporation. Answers (a), (c), and (d) are incorrect because the Act provides that a corporation is either a Subchapter S or Subchapter C corporation but not both at the same time.

38. (b) All corporations are divided under the federal Subchapter S Revision Act as being either a Subchapter C corporation or a Subchapter S corporation. Answer (a) is incorrect because the federal Subchapter S Revision Act provides that there are two categories of corporations: Subchapter C and Subchapter S corporations. Answer (c) is incorrect because this federal law provides for only two categories of corporations. A Subchapter E corporation is not one of these. Answer (d) is incorrect because answer (c) is correct.

39. (c) Both Subchapter C corporations and Subchapter S corporations are similar in their provisions for the limited liability of their shareholders and also in their corporate management structures. Answer (a) is incorrect because it does not include the similarity of the corporate management structures. Answer (b) is incorrect because it does not mention the similarity of the shareholders’ limited liability. Answer (d) is incorrect for the reason that answer (c) is correct.

40. (a) Tax treatment is the main reason why Subchapter S corporations are formed instead of Subchapter C corporations. Answer (b) is incorrect because this federal Act covers both types of corporations. Answers (c) and (d) are incorrect because the provisions on the limited liability of shareholders and the provisions for the structure of corporate management are some of the ways that Subchapter C and Subchapter S corporations are generally similar.

41. (c) One advantage of the corporate form of business is that it has a continuous life and is not terminated by the death of a shareholder or manager. Answer (a) is incorrect because although the power to manage the corporation is vested in the board of directors, they usually delegate the day-to-day management responsibilities to various managers. Answer (b) is incorrect because in most corporations, ownership is not contractually restricted. In fact, free transferability of the shares of stock is a major advantage of the corporate form of business. Answer (d) is incorrect because corporations are not free from state regulation.

42. (c) A major advantage is that shareholders have limited liability, that is, typically limited to what they paid for the stock. However, managers do not have limited liability for their actions as managers. If a manager is also a shareholder, that person has limited liability for the ownership in the stock but can still be sued for misdeeds as a manager. Answers (a), (b), and (d) are all considered to be advantages of a corporation. Note that since a person can manage a corporation without necessarily being an owner, this can encourage professional managers to get involved.

43. (d) The death of one or more of a corporation’s shareholders does not automatically terminate it. Answer (a) is incorrect because a corporation continues to exist until it is dissolved, merged or otherwise terminated. Answer (b) is incorrect because shares in a corporation, represented by stocks, can be freely bought, sold, or assigned unless the shareholders have agreed to restrict this. Answer (c) is incorrect because a corporation is legally a separate entity apart from its shareholders.

44. (d) A corporation may make contracts in its own name with both its shareholders and third parties. Answer (a) is incorrect because it may also make contracts with third parties. Answer (b) is incorrect because corporations do not generally need the consent of other shareholders to contract with one shareholder. Answer (c) is incorrect because it may also contract with its shareholders.

45. (d) Persons who manage a corporation may be, but need not be, shareholders of that corporation. Also, a corporation as a separate legal entity may convey or hold property. It may also sue or be sued in its own name. Answers (a), (b), and (c) are not comprehensive enough.

46. (a) A Subchapter S corporation is often formed to help avoid the double taxation that a Subchapter C corporation may face. Answer (b) is incorrect because partners in a general partnership have unlimited personal liability. Shareholders of a corporation have limited liability with few exceptions. Answer (c) is incorrect because a Subchapter C corporation is any corporation that is not a Subchapter S corporation. Answer (d) is incorrect because both Subchapter C and Subchapter S corporations provide their shareholders with limited liability with few exceptions.

47. (b) Bond is a domestic corporation in Florida since it incorporated there. It is a foreign corporation in Georgia since it did not incorporate there. Bond does not need to incorporate in Georgia but must qualify to do business there because it has branch offices in Georgia. This qualifying normally entails filing required documents with the state.

48. (b) In a professional corporation, the professional has most of the benefits of a corporation such as limited liability for corporate debts. However, the professional has personal liability for professional acts. Colby cannot avoid liability for the damage caused the client due to negligence in a professional act.

49. (c) A domestic corporation is one that operates and does business in the state in which it was incorporated. Answer (a) is incorrect because Macro, instead of incorporating in Nevada, may qualify to do business by obtaining a certificate of authority from Nevada. Answer (b) is incorrect because Macro is a foreign corporation in Nevada because it did not incorporate there. Answer (d) is incorrect because the statement in (c) is the only one that is true.

50. (d) None of the listed items are normally considered doing business in the other states such that Cleanit would be required to qualify to do business and thus have to obtain certificates of authority from those states. Therefore, answers (a), (b), and (c) are incorrect.

51. (c) Normally, under state laws, only licensed professionals may own shares in professional corporations. Furthermore, the licensed professionals retain personal liability for their professional acts in the professional corporation. Therefore (a), (b), and (d) are incorrect.

52. (d) Corporations and limited partnerships may only be created pursuant to state statutes. Normally, both the Articles of Incorporation and a Certificate of Limited Partnership must be filed with the Secretary of State. Answer (c) is incorrect since limited partners do not owe fiduciary duties to the partnership. Answer (a) is incorrect since limited partners have the right to vote on partnership matters such as the dissolution or winding up of the partnership, loans of the partnership, a change in the nature of the business of a partnership, and the removal of a general partner without jeopardizing their limited partner status. Answer (b) is incorrect since sale of limited partnership interests is not automatically exempted from the general securities laws’ registration requirements.

53. (d) Under the Revised Model Business Corporation Act, a corporation’s Articles of Incorporation generally must include the name of the corporation, the purpose of the corporation, the powers of the corporation, the name of the incorporators, the name of the registered agent of the corporation and the number of shares of stock the corporation is authorized to issue.

54. (a) The Articles of Incorporation are filed with the state and contain the names of the corporation, registered agent, and incorporators. This document also contains the purpose and powers of the corporation as well as a description of the types of stock and number of authorized shares.

55. (d) Normally, the board of directors of a corporation has the power to adopt, amend, and repeal the bylaws. It also has the power to declare dividends and fix the compensation of the directors. However, it does not have the power to amend the Articles of Incorporation.

56. (a) Corporations and limited partnerships may only be created pursuant to state statutes. Normally, both the Articles of Incorporation and a Certificate of Limited Partnership must be filed with the Secretary of State. Answer (b) is incorrect because a limited partnership requires at least one general partner who retains unlimited personal liability. Answer (c) is incorrect because a limited partnership is treated the same as a general partnership for tax purposes in that it is not recognized as a separate taxable entity. Answer (d) is incorrect because a limited partnership is not statutorily allowed perpetual existence.

57. (a) The basic concept of a promoter is one who forms a corporation with the goal of the corporation eventually coming into existence. Answer (b) is incorrect because for there to be an agent, there must be a principal. There is no principal yet because the corporation is not yet formed. Answer (c) is incorrect because the promoters are not agents, since there is no principal yet, thus have no authority to bind the future corporations to contracts. Answer (d) is incorrect because the promoters are not agents and thus cannot use agency law to protect them.

58. (b) The Articles of Incorporation must include, among other things, the amount of capital stock authorized and the types of stock to be issued. Specific provisions applicable to stock must also be stated. Examples of stock provisions which must be authorized by the Articles of Incorporation include number of authorized shares, whether the stock is to be par value or no-par value, and classes of stock, including voting rights and dividend provisions. When, as here, a shareholder owns a cumulative stock the shareholder becomes an unsecured creditor of the corporation to the extent declared dividends are not paid; this includes dividends that were declared, but not paid, in previous years. Therefore, Johns becomes an unsecured creditor upon Abco’s declaration of preferred stock dividend. In order for Johns to be entitled to convert his/her preferred shares to common shares, to participate with common shareholders in any dividend distribution made after preferred dividends are paid, or to be entitled to vote if dividend payments are in arrears, it must be stated in the Articles of Incorporation; therefore, (a), (c), and (d) are incorrect.

59. (c) Par value is the minimum amount that a corporation may sell stock initially. Par value does not apply to the corporation’s purchase of stock; nor does par value apply to treasury stock. Gallagher originally sold the stock at above par value.

60. (c) A corporation may resell treasury shares without regard to par value. Therefore, an owner of common stock who purchased treasury shares for less than par value will not have any liability beyond actual investment. Answer (a) is incorrect because an owner of common stock who paid less than par value for stock purchased in connection with an original issue of shares is contingently liable in many states to creditors for the difference between the amount paid and par value. Answer (b) is incorrect because a promise to perform services is valid consideration, but only if it is for at least par value. Answer (d) is incorrect because once the corporation accepts an offer to buy stock subscriptions, the subscriber becomes liable for the purchase. Therefore, an owner of common stock who failed to pay the full amount owed on a subscription contract for no-par shares is liable for the difference between any amounts already paid and the full amount owed according to the contract.