Module 35: Individual Taxation

Overview

This module covers the area of individual taxation in the same order in which topics appear in the individual tax formula. The module begins with exclusions and progresses to items to be included in gross income, tax accounting periods and methods, business income and deductions including depreciation, and deductions subtracted from gross income to arrive at adjusted gross income. Next reviewed is the standard deduction as well as the various categories of itemized deductions, together with personal and dependency exemptions, all of which are subtracted from adjusted gross income to arrive at taxable income. This is followed by a review of filing status, alternative minimum tax, and the various tax credits for which an individual might be eligible. The module concludes with an overview of farming income and expenses, tax procedures including assessments and claims for refund, choice of courts, and taxpayer penalties.

I. Gross Income on Individual Returns

A. In General

B. Exclusions from Gross Income

C. Items to Be Included in Gross Income

D. Accounting Periods

E. Tax Accounting Methods

F. Business Income and Deductions

G. Depreciation, Depletion, and Amortization

H. Domestic Production Activities Deduction

(DPAD)

II. “Above the Line” Deductions

A. Reimbursed Employee Business Expenses

B. Expenses Attributable to Property

C. Self-Employment Tax

D. Self-Employed Medical Insurance

Deduction

E. Moving Expenses

F. Contributions to Certain Retirement Plans

G. Deduction for Interest on Education Loans

H. Deduction for Qualified Tuition and Related

Expenses

I. Penalties for Premature Withdrawals from

Time Deposits

J. Alimony

K. Jury Duty Pay Remitted to Employer

L. Costs Involving Discrimination Suits

M. Expenses of Elementary and Secondary

Teachers

III. Itemized Deductions from Adjusted Gross

Income

A. Medical and Dental Expenses

B. Taxes

C. Interest Expense

D. Charitable Contributions

E. Personal Casualty and Theft Gains and

Losses

F. Miscellaneous Deductions

G. Reduction of Total Itemized Deductions

IV. Exemptions

V. Tax Computation

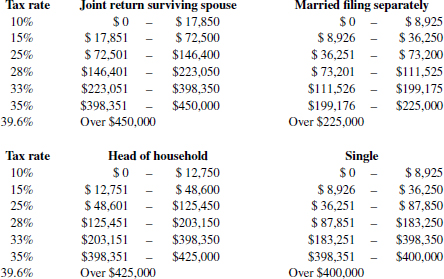

A. Tax Tables

B. Tax Rate Schedules

C. Filing Status

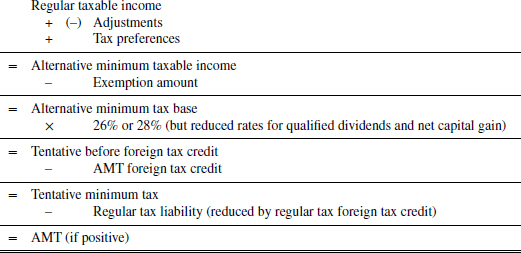

D. Alternative Minimum Tax (AMT)

E. Other Taxes

VI. Tax Credits/Estimated Tax Payments

A. General Business Credit

B. Business Energy Credit

C. Credit for Rehabilitation Expenditures

D. Work Opportunity Credit

E. Alcohol Fuels Credit

F. Research Credit

G. Low-Income Housing Credit

H. Disabled Access Credit

I. Empowerment Zone Employment Credit

J. Employer Social Security Credit

K. Employer-Provided Child Care Credit

L. Credit for the Elderly and the Disabled

M. Child and Dependent Care Credit

N. Foreign Tax Credit

O. Earned Income Credit

P. Credit for Adoption Expenses

Q. Child Tax Credit

R. American Opportunity Credit (AOC)

S. Lifetime Learning Credit

T. Credit for Qualified Retirement Savings

U. Estimated Tax Payments

VII. Filing Requirements

VIII. Farming Income and Expenses

IX. Tax Procedures

A. Audit and Appeal Procedures

B. Choice of Courts

C. Assessments

D. Collection from Transferees and Fiduciaries

E. Closing Agreement and Compromise

F. Claims for Refund

G. Interest

H. Taxpayer Penalties

Key Terms

Multiple-Choice Questions

Multiple-Choice Answers and Explanations

Simulations

Simulation Solutions

This section outlines (1) gross income in general, (2) exclusions from gross income, (3) items to be included in gross income, (4) tax accounting methods, and (5) items to be included in gross income net of deductions (e.g., business income, sales, and exchanges).

I. GROSS INCOME ON INDIVIDUAL RETURNS

A. In General

1.

Gross income includes all income from whatever source derived, unless specifically excluded

a. Does not include a return of capital (e.g., if a taxpayer loans $6,000 to another and is repaid $6,500 at a later date, only the $500 difference is included in gross income)

b. The income must be

realized (i.e., there must be a transaction which gives rise to the income)

(1) A mere appreciation in the value of property is not income (e.g., value of one’s home increases $2,000 during year. Only if the house is sold will the increase in value be realized)

(2) A transaction may be in the form of actual receipt of cash or property, accrual of a receivable, or sale or exchange

c. The income must also be recognized (i.e., the transaction must be a taxable event, and not a transaction for which non recognition is provided in the Internal Revenue Code)

d. An

assignment of income will not be recognized for tax purposes

(1) If income from property is assigned, it is still taxable to the owner of the property.

EXAMPLE

X owns a building and assigns the rents to Y. The rents remain taxable to X, even though the rents are received by Y.

(2) If income from services is assigned, it is still taxable to the person who earns it.

EXAMPLE

X earns $200 per week. To pay off a debt owed to Y, he assigns half of it to Y. $200 per week remains taxable to X.

2. Distinction between exclusions, deductions, and credits

a.

Exclusions—income items which are not included in gross income

(1) Exclusions must be specified by law. Remember, gross income includes all income except that specifically excluded.

(2) Although exclusions are exempt from income tax, they may still be taxed under other tax rules (e.g., gifts may be subject to the gift tax).

b.

Deductions—amounts that are subtracted from income to arrive at adjusted gross income or taxable income

(1) Deductions for adjusted gross income (above the line deductions)—amounts deducted from gross income to arrive at adjusted gross income

(2) Itemized deductions (below the line deductions)—amounts deducted from adjusted gross income to arrive at taxable income

c. Credits—amounts subtracted from the computed tax to arrive at taxes payable

B. Exclusions from Gross Income (not reported)

1. Payments received for

support of minor children

a. Must be children of the parent making the payments

b. Decree of divorce or separate maintenance generally must specify the amount to be treated as child support, otherwise payments may be treated as alimony

2. Property settlement (division of capital) received in a divorce

3.

Annuities and pensions are excluded to the extent they represent a return of capital

a. Excluded portion of each payment is

b. “Expected total annuity payments” is calculated by multiplying the annual return by

(1) The number of years receivable if it is an annuity for a definite period

(2) A life expectancy multiple (from IRS tables) if it is an annuity for life

c. Once this exclusion ratio is determined, it remains constant until the cost of the annuity is completely recovered. Any additional payments will be fully taxable.

EXAMPLE

Mr. Jones purchased an annuity contract for $3,600 that will pay him $1,500 per year beginning in 2013. His expected return under the contract is $10,800. Mr. Jones’ exclusion ratio is $3,600 ÷ $10,800 = 1/3. For 2013, Mr. Jones will exclude $1,500 × 1/3 = $500; and will include the remaining $1,000 in gross income.

d. If the taxpayer dies before total cost is recovered, unrecovered cost is allowed as a miscellaneous itemized deduction on the taxpayer’s final tax return.

4.

Life insurance proceeds (face amount of policy) are generally excluded if paid by reason of death

a. If proceeds are received in installments, amounts received in excess of pro rata part of face amount are taxable as interest.

b. Dividends on unmatured insurance policies are excluded to the extent not in excess of cumulative premiums paid.

c.

Accelerated death benefits received under a life insurance policy by a

terminally or chronically ill individual are generally excluded from gross income

(1) Similarly, if a portion of a life insurance contract on the life of a terminally or chronically ill individual is assigned or sold to a viatical settlement provider, proceeds received from the provider are excluded.

(2) For a chronically ill individual, the exclusion is limited to the amount paid by the individual for unreimbursed long-term care costs. Payments made on a per diem basis, up to $300 per day for 2011, are excludable regardless of actual long-term care costs incurred.

d. All interest is taxable if proceeds are left with insurance company under agreement to pay only interest.

e. If insurance proceeds are paid for reasons other than death or under c. above, or if the policy was obtained by the beneficiary in exchange for valuable consideration from a person other than the insurance company, all proceeds in excess of cost are taxable. Annuity rules apply to installment payments.

EXAMPLE

Able was the owner and beneficiary of a $30,000 life insurance policy on Baker. Able sold the policy for $10,000 to Carr who subsequently paid $6,000 of premiums. If Baker dies, Carr’s gross income from the proceeds of the life insurance policy would total $30,000 − ($10,000 + $6,000) = $14,000.

f.

Company-owned life insurance. In the case of an

employer-owned life insurance contract, the amount of insurance proceeds that can be excluded from gross income by the employer (or related person) is generally

limited to the sum of the premiums and other amounts paid by the policyholder for the contract. However, the full amount of proceeds paid at death can be excluded if specified notice and consent requirements as well as additional requirements are met.

(1) The notice and consent requirements specify that the employee must (a) be notified in writing of the intent to insure the employee’s life and the maximum amount for which the employee could be insured, (b) provide written consent to being insured and acknowledge that coverage may continue after the employee terminates employment, and (c) be informed in writing that the employer (or related person) will be the beneficiary of proceeds payable upon the death of the employee.

(2) Additionally, the insured must have been an employee at any time during the 12-month period before the insured’s death, or at the time the contract was issued was a director or highly compensated employee. Alternatively, the proceeds must be paid to a member of the insured’s family or designated beneficiary of the insured, or the proceeds are used to buy an equity (or capital or profits) interest in the employer from insured’s heir.

5. Certain

employee benefits are excluded

a. Group-term life insurance premiums paid by employer (the cost of up to $50,000 of insurance coverage is excluded). Exclusion not limited if beneficiary is the employer or a qualified charity.

b. Insurance premiums employer pays to fund an accident or health plan for employees are excluded.

c.

Accident and health benefits provided by employer are excluded if benefits are for

(1) Permanent injury or loss of bodily function

(2) Reimbursement for medical care of employee, spouse, or dependents

(a) Employee cannot take itemized deduction for reimbursed medical expenses

(b) Exclusion may not apply to highly compensated individuals if reimbursed under a discriminatory self-insured medical plan

d. Employees of small businesses (50 or fewer employees) and self-employed individuals may qualify for a

medical savings account (MSA) if covered under a high-deductible health insurance plan. An MSA is similar to an IRA, except used for health care.

(1) Employer contributions to an employee’s MSA are excluded from gross income (except if made through a cafeteria plan), and employee contributions are deductible for AGI.

(2) Contributions are limited to 65% (75% for family coverage) of the annual health insurance deductible amount.

(3) Earnings of an MSA are not subject to tax; distributions from an MSA used to pay qualified medical expenses are excluded from gross income.

e.

Meals or lodging furnished for the convenience of the employer on the employer’s premises are excluded.

(1) For the convenience of the employer means there must be a non compensatory reason such as the employee is required to be on duty during this period.

(2) In the case of lodging, it also must be a condition of employment.

f. Employer-provided educational assistance (e.g., payment of tuition, books, fees) derived from an employer’s qualified educational assistance program is excluded up to maximum of $5,250 per year. The exclusion applies to both undergraduate as well as graduate-level courses, but does not apply to assistance payments for courses involving sports, games, or hobbies, unless they involve the employer’s business or are required as part of a degree program. Excludable assistance does not include tools or supplies that the employee retains after completion of the course, nor the cost of meals, lodging, or transportation.

g. Employer payments to an employee for dependent care assistance are excluded from an employee’s income if made under a written, nondiscriminatory plan. Maximum exclusion is $5,000 per year ($2,500 for a married person filing a separate return).

h. Qualified adoption expenses paid or incurred by an employer in connection with an employee’s adoption of a child are excluded from the employee’s gross income. For 2013, the maximum exclusion is $12,970 per eligible child (including special needs children) and the exclusion is ratably phased out for modified AGI between $194,580 and $234,580.

i.

Employee fringe benefits are generally excluded if

(1) No additional-cost services—for example, airline pass

(2) Employee discount that is nondiscriminatory

(3) Working condition fringes—excluded to the extent that if the amount had been paid by the employee, the amount would be deductible as an employee business expense

(4) De minimis fringes—small value, impracticable to account for (e.g., coffee, personal use of copying machine)

(5)

Qualified transportation fringes

(a) Up to $245 per month for 2013 can be excluded for employer-provided transit passes and transportation in a commuter highway vehicle if the transportation is between the employee’s home and work place.

(b) Up to $245 per month for 2013 can be excluded for employer-provided parking on or near the employer’s place of business.

(6) Qualified moving expense reimbursement—an individual can exclude any amount received from an employer as payment for (or reimbursement of) expenses which would be deductible as moving expenses if directly paid or incurred by the individual. The exclusion does not apply to any payment (or reimbursement of) an expense actually deducted by the individual in a prior taxable year.

j. Workers’ compensation is fully excluded if received for an occupational sickness or injury and is paid under a workers’ compensation act or statute.

6. Accident and health insurance benefits derived from policies purchased by the taxpayer are excluded, but not if the medical expenses were deducted in a prior year and the tax benefit rule applies.

7.

Damages for physical injury or physical sickness are excluded.

a. If an action has its origin in a physical injury or physical sickness, then all damages therefrom (other than punitive damages) are excluded (e.g., damages received by an individual on account of a claim for loss due to a physical injury to such individual’s spouse are excludible from gross income).

b. Damages (other than punitive damages) received on account of a claim of wrongful death, and damages that are compensation for amounts paid for medical care (including medical care for emotional distress) are excluded.

c. Emotional distress is not considered a physical injury or physical sickness. No exclusion applies to damages received from a claim of employment discrimination, age discrimination, or injury to reputation (even if accompanied by a claim of emotional distress).

d. Punitive damages generally must be included in gross income, even if related to a physical injury or physical sickness.

8.

Gifts, bequests, devises, or inheritances are excluded.

a. Income subsequently derived from property so acquired is not excluded (e.g., interest or rent).

b. “Gifts” from employer except for noncash holiday presents are generally not excluded.

9. The receipt of

stock dividends (or stock rights) is generally excluded from income, but the FMV of the stock received will be included in income if the distribution

a. Is on preferred stock

b. Is payable, at the election of any shareholder, in stock or property

c. Results in the receipt of preferred stock by some common shareholders, and the receipt of common stock by other common shareholders

d. Results in the receipt of property by some shareholders, and an increase in the proportionate interests of other shareholders in earnings or assets of the corporation

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 1 THROUGH 14

10. Certain

interest income is excluded.

a. Interest on obligations of a state or one of its political subdivisions (e.g., municipal bonds), the District of Columbia, and US possessions is generally excluded from income if the bond proceeds are used to finance traditional governmental operations.

b. Other state and local government-issued obligations (private activity bonds) are generally fully taxable. An obligation is a private activity bond if (1) more than 10% of the bond proceeds are used (directly or indirectly) in a private trade or business and more than 10% of the principal or interest on the bonds is derived from, or secured by, money or property used in the trade or business, or (2) the lesser of 5% or $5 million of the bond proceeds is used (directly or indirectly) to make or finance loans to private persons or entities.

c. The following bonds are

excluded from the private activity bond category even though their proceeds are not used in traditional government operations. The interest from these bonds is excluded from income.

(1) Qualified bonds issued for the benefit of schools, hospitals, and other charitable organizations

(2) Bonds used to finance certain exempt facilities, such as airports, docks, wharves, mass commuting facilities, etc.

(3) Qualified redevelopment bonds, small-issue bonds (i.e., bonds not exceeding $1 million), and student loan bonds

(4) Qualified mortgage and veterans’ mortgage bonds

d. Interest on US obligations is included in income.

11.

Savings bonds for higher education

a. The accrued interest on Series EE US savings bonds that are redeemed by the taxpayer is excluded from gross income to the extent that the aggregate redemption proceeds (principal plus interest) are used to finance the higher education of the taxpayer, taxpayer’s spouse, or dependents.

(1) The bonds must be issued after December 31, 1989, to an individual age twenty-four or older at the bond’s issue date.

(2) The purchaser of the bonds must be the sole owner of the bonds (or joint owner with his or her spouse). Married taxpayers must file a joint return to qualify for the exclusion.

(3) The redemption proceeds must be used to pay qualified higher education expenses (i.e., tuition and required fees less scholarships, fellowships, and employer-provided educational assistance) at an accredited university, college, junior college, or other institution providing postsecondary education, or at an area vocational education school.

(4) If the redemption proceeds exceed the qualified higher education expenses, only a pro rata amount of interest can be excluded.

EXAMPLE

During 2013, a married taxpayer redeems Series EE bonds receiving $6,000 of principal and $4,000 of accrued interest. Assuming qualified higher education expenses total $9,000, accrued interest of $3,600 ($9,000/$10,000 × $4,000) can be excluded from gross income.

b. If the taxpayer’s modified AGI exceeds a specified level, the exclusion is subject to phase-out as follows:

| Filing status |

2013 AGI phase-out range |

| Married filing jointly |

$112,050 − $142,050 |

| Single (including head of household) |

$74,700 − $89,700 |

(1) The reduction of the exclusion is computed as

(2) If the taxpayer’s modified AGI exceeds the applicable phase-out range, no exclusion is available.

EXAMPLE

Assume the joint return of the married taxpayer in the above example has modified AGI of $132,050 for 2013. The reduction would be ($20,000/$30,000) × $3,600 = $2,400. Thus, of the $4,000 of interest received, a total of $1,200 could be excluded from gross income.

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 15 THROUGH 22

12.

Scholarships and fellowships

a. A degree candidate can exclude the amount of a scholarship or fellowship that is used for tuition and course-related fees, books, supplies, and equipment. Amounts used for other purposes including room and board are included in income.

b. Amounts received as a grant or a tuition reduction that represent payment for teaching, research, or other services are generally not excludable.

c. Non degree students may not exclude any part of a scholarship or fellowship grant.

d. The exclusion from gross income also applies to scholarships with obligatory service requirements received by degree candidates at qualified educational organizations from the National Health Service Corps Scholarship Program and the F. Edward Hebert Armed Forces Health Professions Scholarship Program.

13. Political contributions received by candidates’ campaign funds are excluded from income, but included if put to personal use.

14. Rental value of parsonage or cash rental allowance for a parsonage is excluded by a minister.

15.

Discharge of indebtedness normally results in income to debtor, but may be

excluded if

a. A discharge of certain student loans pursuant to a loan provision providing for discharge if the individual works in a certain profession for a specified period of time

b. A discharge of a corporation’s debt by a shareholder (treated as a contribution to capital)

c. The discharge is a gift

d. The discharge is a purchase money debt reduction (treat as a reduction of purchase price)

e. The discharge is a cancellation of up to $2 million ($1 million for married filing separately) of acquisition indebtedness on a principal residence before January 1, 2014. The amount excluded from income reduces the taxpayer’s basis for the principal residence (but not below zero).

f. Debt is discharged in a bankruptcy proceeding, or debtor is insolvent both before and after discharge

(1) If debtor is insolvent before but solvent after discharge of debt, income is recognized to the extent that the FMV of assets exceeds liabilities after discharge

(2) The amount excluded from income in e. above must be applied to reduce tax attributes in the following order

(a) Net Operating Loss (NOL) for taxable year and loss carryovers to taxable year

(b) General business credit

(c) Minimum tax credit

(d) Capital loss of taxable year and carryovers to taxable year

(e) Reduction of the basis of property

(f) Passive activity loss and credit carryovers

(g) Foreign tax credit carryovers to or from taxable year

(3) Instead of reducing tax attributes in the above order, taxpayer may elect to first reduce the basis of depreciable property

16. Lease improvements. Increase in value of property due to improvements made by lessee is excluded from lessor’s income unless improvements are made in lieu of fair value rent.

17.

Foreign earned income exclusion. An individual meeting either a bona fide residence test or a physical presence test may elect to exclude up to $97,600 of income earned in a foreign country for 2013. Qualifying taxpayers also may elect to exclude additional amounts based on foreign housing costs.

a. To qualify, an individual must be a (1) US citizen who is a foreign resident for an uninterrupted period that includes an entire taxable year (bona fide residence test), or (2) US citizen or resident present in a foreign country for at least 330 full days in any twelve-month period (physical presence test).

b. An individual who elects to exclude the housing cost amount can exclude only the lesser of (1) the housing cost amount attributable to employer-provided amounts, or (2) the individual’s foreign earned income for the year.

c. Housing cost amounts not provided by an employer can be deducted for AGI, but deduction is limited to the excess of the taxpayer’s foreign earned income over the applicable foreign earned income exclusion.

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 23 THROUGH 25

C. Items to Be Included in Gross Income

Gross income includes all income from any source except those specifically excluded. The more common items of gross income are listed below. Those items requiring a detailed explanation are discussed on the following pages.

1. Compensation for services, including wages, salaries, bonuses, commissions, fees, and tips

a. Property received as compensation is included in income at FMV on date of receipt.

b. Bargain purchases by an employee from an employer are included in income at FMV less price paid.

c. Life insurance premiums paid by employer must be included in an employee’s gross income except for group-term life insurance coverage of $50,000 or less.

d. Employee expenses paid or reimbursed by the employer unless the employee has to account to the employer for these expenses and they would qualify as deductible business expenses for employee.

e.

Tips must be included in gross income

(1) If an individual receives less than $20 in tips while working for one employer during one month, the tips do not have to be reported to the employer, but the tips must be included in the individual’s gross income when received.

(2) If an individual receives $20 or more in tips while working for one employer during one month, the individual must report the total amount of tips to the employer by the tenth day of the following month for purposes of withholding of income tax and social security tax. Then the total amount of tips must be included in the individual’s gross income for the month in which reported to the employer.

2. Gross income derived from business or profession

3. Distributive share of partnership or S corporation income

4. Gain from the sale or exchange of real estate, securities, or other property

5. Rents and royalties

6. Dividends

7.

Interest including

a. Earnings from savings and loan associations, mutual savings banks, credit unions, etc.

b. Interest on bank deposits, corporate or US government bonds, and Treasury bills

(1) Interest from US obligations is included, while interest on state and local obligations is generally excluded.

(2) If a taxpayer elects to amortize the bond premium on taxable bonds acquired after 1987, any bond premium amortization is treated as an offset against the interest earned on the bond. The amortization of bond premium reduces taxable income (by offsetting interest income) as well as the bond’s basis.

c. Interest on tax refunds

d. Imputed interest from interest-free and low-interest loans

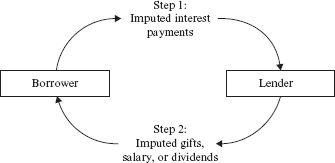

(1) Borrower is treated as making imputed interest payments (subject to the same deduction restrictions as actual interest payments) which the lender reports as interest income.

(2) Lender is treated as making gifts (for personal loans) or paying salary or dividends (for business-related loans or corporation-shareholder loans) to the borrower.

(3) Rate used to impute interest is tied to average yield on certain federal securities and is compounded semiannually; if the federal rate is greater than the interest rate charged on a loan (e.g., a low-interest loan), impute interest only for the excess.

(a) For demand loans, the deemed transfers are generally treated as occurring at the end of each year, and will fluctuate with interest rates.

(b) For term loans, the interest payments are determined at the date of the loan and then allocated over the term of the loan; lender’s payments are treated as made on date of loan.

(4) No interest is imputed to either the borrower or the lender for any day on which the aggregate amount of loans between such individuals (and their spouses) does not exceed $10,000.

(5) For any day that the aggregate amount of loans between borrower and lender (and their spouses) does not exceed $100,000, imputed interest is limited to borrower’s “net investment income;” no interest is imputed if borrower’s net investment income does not exceed $1,000.

EXAMPLE

Parents make a $200,000 interest-free demand loan to their unmarried daughter on January 1, 2013. Assume the average federal short-term rate is 3% for 2013. If the loan is outstanding for the entire year, under Step 1, the daughter is treated as making a ($200,000 × 3% ×1/2) + ($203,000 × 3% × 1/2) = $6,045 interest payment on 12/31/13, which is included as interest income on the parents’ 2013 tax return. Under Step 2, the parents are treated as making a $6,045 gift to their daughter on 12/31/13. (Note that the gift will be offset by annual exclusions totaling $28,000 (for 2013) for gift tax purposes as discussed in Module 39.)

8.

Alimony and separate maintenance payments

a. Alimony is included in the recipient’s gross income and is deductible toward AGI by the payor. In order for a payment to be considered as alimony, the payment must

(1) Be made pursuant to a decree of divorce or written separation instrument

(2) Be made in cash and received by or on behalf of the payee’s spouse

(3) Terminate upon death of the recipient

(4) Not be made to a member of the same household at the time the payments are made

(5) Not be made to a person with whom the taxpayer is filing a joint return

(6) Not be characterized in the decree or written instrument as other than alimony

b.

Alimony recapture may occur if payments sharply decline in the second or third years. This is accomplished by making the payor report the recaptured alimony from the first and second years as income (and allowing the payee to deduct the same amount) in the third year.

(1) Recapture for the second year occurs to the extent that the alimony paid in the second year exceeds the third-year alimony by more than $15,000.

(2) Recapture for the first year occurs to the extent that the alimony paid in the first year exceeds the average alimony paid in the second year (reduced by the recapture for that year) and third year by more than $15,000.

(3) Recapture will not apply to any year in which payments terminate as a result of the death of either spouse or the remarriage of the payee.

(4) Recapture does not apply to payments that may fluctuate over three years or more and are not within the control of the payor spouse (e.g., 20% of the net income from a business).

EXAMPLE

If a payor makes alimony payments of $50,000 in 2011 and no payments in 2012 or 2013, $50,000 − $15,000 = $35,000 will be recaptured in 2013 (assuming none of the exceptions apply).

EXAMPLE

If a payor makes alimony payments of $50,000 in 2011, $20,000 in 2012, and nothing in 2013, the recapture amount for 2012 is $20,000 − $15,000 = $5,000. The recapture amount for 2011 is $50,000 − ($15,000 + $7,500) = $27,500. The $7,500 is the average payments for 2012 and 2011 after reducing the $20,000 year 2012 payment by the $5,000 of recapture for 2012. The recapture amounts for 2011 and 2012 total $32,500 and are reported in 2013.

c. Any amounts specified as

child support are not treated as alimony.

(1) Child support is not gross income to the payee and is not deductible by the payor.

(2) If the decree or instrument specifies both alimony and child support, but less is paid than required, then amounts are first allocated to child support, with any remainder allocated to alimony.

(3) If a specified amount of alimony is to be reduced upon the happening of some contingency relating to a child, then an amount equal to the specified reduction will be treated as child support rather than alimony.

EXAMPLE

A divorce decree provides that payments of $1,000 per month will be reduced by $400 per month when a child reaches age twenty-one. Here, $400 of each $1,000 monthly payment will be treated as child support.

9.

Social security, pensions, annuities (other than excluded recovery of capital)

a. Up to 50% of social security retirement benefits may be included in gross income if the taxpayer’s provisional income (AGI + tax-exempt income + 50% of the social security benefits) exceeds a threshold that is $32,000 for a joint return, $0 for married taxpayers filing separately, and $25,000 for all other taxpayers. The amount to be included in gross income is the lesser of

(1) 50% of the social security benefits, or

(2) 50% of the excess of the taxpayer’s provisional income over the base amount.

EXAMPLE

A single taxpayer with AGI of $20,000 received tax-exempt interest of $2,000 and social security benefits of $7,000. The social security to be included in gross income is the lesser of

1/2 ($7,000) = $3,500; or

1/2 ($25,500 − $25,000) = $250.

b.

Up to 85% of social security retirement benefits may be included in gross income for taxpayers with provisional income above a higher second threshold that is $44,000 for a joint return, $0 for married taxpayers filing separately, and $34,000 for all other taxpayers. The amount to be included in gross income is the lesser of

(1) 85% of the taxpayer’s social security benefits, or

(2) The sum of (a) 85% of the excess of the taxpayer’s provisional income above the applicable higher threshold amount plus (b) the smaller of (i) the amount of benefits included under a. above, or (ii) $4,500 for single taxpayers or $6,000 for married taxpayers filing jointly.

c. Rule of thumb: Social security retirement benefits are fully excluded by low-income taxpayers (i.e., provisional income less than $25,000); 85% of benefits must be included in gross income by high-income taxpayers (i.e., provisional income greater than $60,000).

d.

Lump-sum distributions from qualified pension, profit-sharing, stock bonus, and Keogh plans (but not IRAs) may be eligible for special tax treatment.

(1) The portion of the distribution allocable to pre-1974 years is eligible for long-term capital gain treatment.

(2) If the employee was born before 1936, the employee may elect ten-year averaging.

(3) Alternatively, the distribution may be rolled over tax-free (within sixty days) to a traditional IRA, but subsequent distributions from the IRA will be treated as ordinary income.

10. Income in respect of a decedent is income that would have been income of the decedent before death but was not includible in income under the decedent’s method of accounting (e.g., installment payments that are paid to a decedent’s estate after his/her death). Such income has the same character as it would have had if the decedent had lived and must be included in gross income by the person who receives it.

11. Employer supplemental unemployment benefits or strike benefits from union funds

12. Fees, including those received by an executor, administrator, director, or for jury duty, or precinct election board duty

13. Income from discharge of indebtedness unless specifically excluded

14.

Stock options

a. An

incentive stock option receives favorable tax treatment.

(1) The option must meet certain technical requirements to qualify.

(2) No income is recognized by employee when option is granted or exercised.

(3) If employee holds the stock acquired through exercise of the option at least two years from the date the option was granted, and holds the stock itself at least one year, the

(a) Employee’s realized gain will be long-term capital gain

(b) Employer receives no deduction

(4) If the holding period requirements above are not met, the employee has ordinary income to the extent that the FMV at date of exercise exceeds the option price.

(a) Remainder of gain is short-term or long-term capital gain.

(b) Employer receives a deduction equal to the amount employee reports as ordinary income.

(5) An incentive stock option may be treated as a nonqualified stock option if a corporation so elects at the time the option is issued.

b. A

nonqualified stock option is included in income when received if option has a determinable FMV.

(1) If option has no ascertainable FV when received, then income arises when option is exercised; to the extent of the difference between the FV when exercised and the option price.

(2) Amount recognized (at receipt or when exercised) is treated as ordinary income to employee; employer is allowed a deduction equal to amount included in employee’s income.

c. An

employee stock purchase plan that does not discriminate against rank and file employees

(1) No income when employee receives or exercises option

(2) If the employee holds the stock at least two years after the option is granted and at least one year after exercise, then

(a) Employee has ordinary income to the extent of the lesser of

[1] FMV at time option granted over option price, or

[2] FMV at disposition over option price

(b) Capital gain to the extent realized gain exceeds ordinary income

(3) If the stock is not held for the required time, then

(a) Employee has ordinary income at the time of sale for the difference between FV when exercised and the option price. This amount also increases basis.

(b) Capital gain or loss for the difference between selling price and increased basis

15.

Prizes and awards are generally taxable.

a. Prizes and awards received for religious, charitable, scientific, educational, artistic, literary, or civic achievement can be excluded only if the recipient

(1) Was selected without any action on his/her part,

(2) Is not required to render substantial future services, and

(3) Designates that the prize or award is to be transferred by the payor to a governmental unit or a tax-exempt charitable, educational, or religious organization

(4) The prize or award is excluded from the recipient’s income, but no charitable deduction is allowed for the transferred amount.

b.

Employee achievement awards are excluded from an employee’s income if the cost to the employer of the award does not exceed the amount allowable as a deduction (generally from $400 to $1,600).

(1) The award must be for length of service or safety achievement and must be in the form of tangible personal property (cash does not qualify).

(2) If the cost of the award exceeds the amount allowable as a deduction to the employer, the employee must include in gross income the greater of

(a) The portion of cost not allowable as a deduction to the employer, or

(b) The excess of the award’s FMV over the amount allowable as a deduction.

16.

Tax benefit rule. A recovery of an item deducted in an earlier year must be included in gross income to the extent that a tax benefit was derived from the prior deduction of the recovered item.

a. A tax benefit was derived if the previous deduction reduced the taxpayer’s income tax.

b. A recovery is excluded from gross income to the extent that the previous deduction did not reduce the taxpayer’s income tax.

(1) A deduction would not reduce a taxpayer’s income tax if the taxpayer was subject to the alternative minimum tax in the earlier year and the deduction was not allowed in computing AMTI (e.g., state income taxes).

(2) A recovery of state income taxes, medical expenses, or other items deductible on Schedule A (Form 1040) will be excluded from gross income if an individual did not itemize deductions for the year the item was paid.

EXAMPLE

Individual X, a single taxpayer, did not itemize deductions but instead used the standard deduction of $5,950 for 2012. In 2013, a refund of $300 of 2012 state income taxes is received. X would exclude the $300 refund from income in 2013.

EXAMPLE

Individual Y, a single taxpayer, had total itemized deductions of $6,150 for 2012, including $800 of state income taxes. In 2013, a refund of $300 of 2012 state income taxes is received. Since Y’s total itemized deductions of $6,150 exceeded his available standard deduction of $5,950 by $200, Y must include $200 of the refund in gross income for 2013.

17. Embezzled or other illegal income

18. Gambling winnings

19. Unemployment compensation must generally be included in gross income.

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 26 THROUGH 43

D. Accounting Periods

1. The term

taxable year refers to a taxpayer’s annual accounting period. Annual accounting period means the annual period that the taxpayer uses to compute income in keeping his books.

a. Calendar year is a period of 12 months ending on December 31.

b. Fiscal year is a period of 12 months ending on the last day of a month other than December.

c. 52–53 week year is an annual period always ending on the same day of the week (e.g., last Sunday of a month, or the Sunday closest to the end of a month).

2. Taxpayer establishes an accounting period by filing first tax return. A taxpayer who does not keep books (e.g., an employee with wage income) must use a calendar year.

3. Rules for adoption of taxable year.

a. Corporation that is a “C” corporation (other than a personal service corporation) may adopt any taxable year that it chooses. A personal service corporation generally must adopt a calendar year.

b. Sole proprietor must use same taxable year for business as is used for personal return.

c. Partnership is a pass-through entity and generally must use the same tax year as that used by its partners owning more than 50% of partnership income and capital. A different taxable year may be permitted if there is a substantial business purpose.

d. S corporation is a pass-through entity and generally must adopt a calendar year. A different taxable year may be permitted if there is a substantial business purpose.

e. Estate may adopt any taxable year for its income tax return that it chooses.

f. Trust (other than charitable and tax-exempt trusts) must adopt a calendar year.

4. Substantial business purpose and IRS approval are generally required to

change a taxable year. Taxpayers can request permission to change a year by filing Form 1128, Application for Change in Accounting Period, by the 15th day of the second month after the close of a short period.

a. The business purpose requirement may be satisfied if the taxpayer is requesting a change to a natural business year. The business purpose test will be met if the taxpayer receives at least 25% of its gross receipts in the last two months of the selected year, and this 25% test has been satisfied for three consecutive years.

b. The IRS may require that certain conditions be met before it approves a request for change (e.g., the IRS may require partners to switch to the same year as is being requested by the partnership).

5. Some changes in tax years require

no approval.

a. Newly married individuals may adopt the taxable year of the other spouse without prior approval.

b. A corporation (other than an S Corporation) may change its year if its taxable year has not changed within the past 10 years ending with the calendar year of change; the resulting short period does not have a NOL; the corporation’s annualized taxable income for the short period is at least 90% of its taxable income for the preceding year; and the corporation’s status (e.g., personal holding company) for the short period is the same as the preceding year.

c. A newly acquired subsidiary that will be included in a consolidated return must change its taxable year to the same year as used by its parent.

6. Taxable periods of less than 12 months

a. If due to beginning or ending of taxpayer’s existence, tax is computed in normal way (e.g., corporation is formed, or individual dies). The taxpayer’s exemptions and credits are not prorated. In the case of a decedent, the income tax return can be filed as if the decedent lived throughout the entire tax year.

b. If the short period is due to a

change in taxable year, taxable income generally must be

annualized. However, a new subsidiary that has a short year because of being included in a consolidated return is not required to annualize.

(1) When annualizing, an individual cannot use the tax tables and must itemize deductions. Personal exemptions must be prorated.

(2) Taxable income is multiplied by 12 and divided by the number of months in short period.

(3) The tax is computed and multiplied by the number of months in the short period, then divided by 12.

EXAMPLE

Pearl Corp. is a C Corporation that has been using a fiscal year ending June 30. It changes to a fiscal year ending September 30 for 2013. Pearl must file a tax return for its fiscal year ending June 30, 2013, as well as a tax return for its short period beginning July 1, 2013, and ending September 30, 2013. Pearl determines that its taxable income for the short period ending September 30 is $30,000. Because Pearl’s short period is the result of a change in taxable year, Pearl must annualize its taxable income for the short period and determine its tax as follows:

| Taxable income $30,000 × 12/3 |

= |

$120,000 |

| Tax on $120,000 |

= |

$ 30,050 |

| Tax for short period $30,050 × 3/12 |

= |

$ 7,513 |

E. Tax Accounting Methods

Tax accounting methods often affect the period in which an item of income or deduction is recognized. Note that the classification of an item is not changed, only the time for its inclusion in the tax computation.

1. Cash method or accrual method is commonly used.

a.

Cash method recognizes income when first received or constructively received; expenses are deductible when paid.

(1) Constructive receipt means that an item is unqualifiedly available without restriction (e.g., interest on bank deposit is income when credited to account).

(2) Not all receipts are income (e.g., loan proceeds, return of investment); not all payments are deductible (e.g., loan repayment, expenditures benefiting future years generally must be capitalized and deducted over cost recovery period).

b. Under the cash method, expenses are generally deductible when paid. Payment by check is considered payment so long as the check is honored by the bank. A payment by credit card is considered a payment at the time of the charge.

(1) Generally, a capital expenditure or prepayment that results in a benefit that extends substantially beyond the end of the tax year does not result in an immediate deduction. However, a cash method taxpayer is not required to capitalize a payment so long as (1) the benefit does not extend beyond 12 months after the first date that the benefit is received, and (2) the benefit does not extend beyond the end of the taxable year following the taxable year in which payment is made.

EXAMPLE

On December 1, 2013, a calendar-year taxpayer pays a $10,000 property insurance premium with a 1-year term that begins on February 1, 2014. The amount paid must be capitalized and is not deductible for 2013 because the benefit attributable to the $10,000 payment extends beyond the end of the taxable year following the taxable year in which the payment is made. The premium will be deductible over the period to which it relates.

EXAMPLE

Assume the same facts as in the example above, except that the policy has a term beginning on December 15, 2013. The 12-month rule applies to the $10,000 payment because the benefit attributable to the payment extends neither more than 12 months beyond December 15, 2013, nor beyond the end of the taxable year following the taxable year in which the payment is made. Thus, the taxpayer is not required to capitalize the payment, and may deduct the $10,000 payment in 2013.

(2) The 12-month rule in (1) above does not apply to prepaid interest, which generally must be deducted over the loan period to which it is allocated.

c. The cash method cannot generally be used if inventories are necessary to clearly reflect income, and cannot generally be used by C corporations, partnerships that have a C corporation as a partner, tax shelters, and certain tax-exempt trusts. However, the following may use the cash method:

(1) A qualified personal service corporation (e.g., corporation performing services in health, law, engineering, accounting, actuarial science, performing arts, or consulting) if at least 95% of stock is owned by specified shareholders including employees.

(2) An entity (other than a tax shelter) if for every year it has average annual gross receipts of $5 million or less for any prior three-year period and provided it does not have inventories for sale to customers.

(3) A small business taxpayer with average annual gross receipts of $1 million or less for any prior three-year period can use the cash method and is excepted from the requirements to account for inventories and use the accrual method for purchases and sales of merchandise.

(4) A

small business taxpayer is eligible to use the cash method of accounting if, in addition to having average gross receipts of more than $1 million and less than $10 million, the business meets any one of three requirements.

(a) The principal business activity is not retailing, wholesaling, manufacturing, mining, publishing, or sound recording;

(b) The principal business activity is the provision of services, or custom manufacturing; or

(c) Regardless of the principal business activity, a taxpayer may use the cash method with respect to any separate business that satisfies (a) or (b) above.

(5) A taxpayer using the accrual method who meets the requirements in (3) or (4) can change to the cash method but must treat merchandise inventory as a material or supply that is not incidental (i.e., only deductible in the year actually consumed or used in the taxpayer’s business).

d.

Accrual method must be used by taxpayers (other than small business taxpayers) for purchases and sales when inventories are required to clearly reflect income.

(1) Income is recognized when “all events” have occurred that fix the taxpayer’s right to receive the item of income and the amount can be determined with reasonable accuracy.

(2) An

expense is deductible when “all events” have occurred that establish the fact of the liability and the amount can be determined with reasonable accuracy. The all-events test is not satisfied until

economic performance has taken place.

(a) For property or services to be provided to the taxpayer, economic performance occurs when the property or services are actually provided by the other party.

(b) For property or services to be provided by the taxpayer, economic performance occurs when the property or services are physically provided by the taxpayer.

(3) An exception to the economic performance rule treats certain

recurring items of expense as incurred in advance of economic performance provided

(a) The all-events test, without regard to economic performance, is satisfied during the tax year;

(b) Economic performance occurs within a reasonable period (but in no event more than 8.5 months after the close of the tax year);

(c) The item is recurring in nature and the taxpayer consistently treats items of the same type as incurred in the tax year in which the all-events test is met; and

(d) Either the amount is not material or the accrual of the item in the year the all-events test is met results in a better matching against the income to which it relates.

2.

Special rules regarding methods of accounting

a.

Rents and royalties received in advance are included in gross income in the year received under both the cash and accrual methods.

(1) A security deposit is included in income when not returned to tenant.

(2) An amount called a “security deposit” that may be used as final payment of rent is considered to be advance rent and included in income when received.

EXAMPLE

In 2013, a landlord signed a five-year lease. During 2013, the landlord received $5,000 for that year’s rent, and $5,000 as advance rent for the last year (2017) of the lease. All $10,000 will be included in income for 2013.

b. Dividends are included in gross income in the year received under both the cash and accrual methods.

c. No advance deduction is generally allowed for accrual method taxpayers for estimated or contingent expenses; the obligation must be “fixed and determinable.”

3. The

installment method applies to gains (not losses) from the disposition of property where at least one payment is to be received after the year of sale. The installment method does not change the character of the gain to be reported (e.g., ordinary, capital, etc.), and is required unless the taxpayer makes a negative election to report the full amount of gain in year of sale.

a. The installment method cannot be used for property held for sale in the ordinary course of business (except time-share units, residential lots, and property used or produced in farming), and cannot be used for sales of stock or securities traded on an established securities market.

b. The amount to be reported in each year is determined by the formula

(1) Contract price is the selling price reduced by the seller’s liabilities that are assumed by the buyer, to the extent not in excess of the seller’s basis in the property.

EXAMPLE

Taxpayer sells property with a basis of $80,000 to buyer for a selling price of $150,000. As part of the purchase price, buyer agrees to assume a $50,000 mortgage on the property and pay the remaining $100,000 in 10 equal annual installments together with adequate interest.

The contract price is $100,000 ($150,000 − $50,000); the gross profit is $70,000 ($150,000 − $80,000); and the gross profit ratio is 70% ($70,000 ÷ $100,000). Thus, $7,000 of each $10,000 payment is reported as gain from the sale.

EXAMPLE

Assume the same facts as above except that the seller’s basis is $30,000. The contract price is $120,000 ($150,000 − mortgage assumed but only to extent of seller’s basis of $30,000); the gross profit is $120,000 ($150,000 − $30,000); and the gross profit ratio is 100% ($120,000 ÷ $120,000). Thus, 100% of each $10,000 payment is reported as gain from the sale. In addition, the amount by which the assumed mortgage exceeds the seller’s basis ($20,000) is deemed to be a payment in year of sale. Since the gross profit ratio is 100%, all $20,000 is reported as gain in the year the mortgage is assumed.

(2) Any depreciation recapture under Sections 1245, 1250, and 291 must be included in income in the year of sale. Amount of recapture included in income is treated as an increase in the basis of the property for purposes of determining the gross profit ratio. Remainder of gain is spread over installment payments.

EXAMPLE

Baxter sells equipment with an adjusted basis of $50,000 to a buyer for $50,000 cash plus a $50,000 interest-bearing note to be paid next year. The equipment had originally cost $90,000, and Baxter had deducted depreciation of $40,000 on the equipment. Baxter realizes a gain of $100,000 − $50,000 = $50,000 on the installment sale, and must immediately recognize gain to the extent of Sec. 1245 depreciation recapture of $40,000, which is not eligible for installment reporting. The gross profit ratio is determined after adding the $40,000 of recapture to the $50,000 of adjusted basis, resulting in a gross profit ratio of 10% [$100,000 − $90,000)/$100,000]. As a result, the $40,000 of depreciation recapture plus 10% × $50,000 cash payment = $5,000 must be recognized this year, while the remaining 10% × $50,000 = $5,000 of gain will be recognized next year when payment on the note is received.

(3) The receipt of readily tradable debt or debt that is payable on demand is considered the receipt of a payment for purposes of the installment method. Additionally, if installment obligations are pledged as security for a loan, the net proceeds of the loan are treated as payments received on the installment obligations.

(4) Installment obligations arising from non dealer sales of property used in the taxpayer’s trade or business or held for the production of rental income (e.g., factory building, warehouse, office building, apartment building) are subject to an interest charge on the tax that is deferred on such sales to the extent that the amount of deferred payments arising from all dispositions of such property during a taxable year and outstanding as of the close of the taxable year exceeds $5,000,000. This provision does not apply to installment sales of property if the sales price does not exceed $150,000, to sales of personal use property, and to sales of farm property.

4.

Percentage-of-completion method can be used for contracts that are not completed within the year they are started.

a. Percentage-of-completion method recognizes income each year based on the percentage of the contract completed that year.

b. Taxpayer may elect not to recognize income or account for costs from a contract for a tax year if less than 10% of the estimated total contract costs have been incurred as of the end of the year.

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 44 THROUGH 59

F. Business Income and Deductions

1.

Gross income for a business includes sales less cost of goods sold plus other income. In computing cost of goods sold

a. Inventory is generally valued at (1) cost, or (2) market, whichever is lower

b. Specific identification, FIFO, and LIFO are allowed

c. If LIFO is used for taxes, it must also be used on books

d. Lower of cost or market cannot be used with LIFO

2. All

ordinary (customary and not a capital expenditure) and

necessary (appropriate and helpful)

expenses incurred in a trade or business are deductible.

a. Business expenses that violate public policy (fines or illegal kickbacks) are not deductible.

b. No deduction or credit is allowed for any amount paid or incurred in carrying on a trade or business that consists of trafficking in controlled substances. However, this limitation does not alter the definition of gross income (i.e., sales less cost of goods sold).

c. Business expenses must be reasonable.

(1) If salaries are excessive (unreasonable compensation), they may be disallowed as a deduction to the extent unreasonable.

(2) Reasonableness of compensation issue generally arises only when the relationship between the employer and employee exceeds that of the normal employer-employee relationship (e.g., employee is also a shareholder).

(3) Use test of what another enterprise would pay under similar circumstances to an unrelated employee.

d. In the case of an individual, any charge (including taxes) for basic local telephone service with respect to the first telephone line provided to any residence of the taxpayer shall be treated as a nondeductible personal expense. Disallowance does not apply to charges for long-distance calls, charges for equipment rental, and optional services provided by a telephone company, or charges attributable to additional telephone lines to a taxpayer’s residence other than the first telephone line.

e.

Uniform capitalization rules (UNICAP) generally require that all costs incurred (both direct and indirect) in manufacturing or constructing real or personal property, or in purchasing or holding property for sale, must be capitalized as part of the cost of the property.

(1) These costs become part of the basis of the property and are recovered through depreciation or amortization, or are included in inventory and recovered through cost of goods sold as an offset to selling price.

(2) The rules apply to inventory, non inventory property produced or held for sale to customers, and to assets or improvements to assets constructed by a taxpayer for the taxpayer’s own use in a trade or business or in an activity engaged in for profit.

(3) Taxpayers subject to the rules are required to capitalize not only direct costs, but also most indirect costs that benefit the assets produced or acquired for resale, including general, administrative, and overhead costs.

(4) Retailers and wholesalers must include in inventory all costs incident to purchasing and storing inventory such as wages of employees responsible for purchasing inventory, handling, processing, repackaging and assembly of goods, and off-site storage costs. These rules do not apply to “small retailers and wholesalers” (i.e., a taxpayer who acquires personal property for resale if the taxpayer’s average annual gross receipts for the three preceding taxable years do not exceed $10,000,000).

(5) Interest must be capitalized if the debt is incurred or continued to finance the construction or production of real property, property with a recovery period of twenty years, property that takes more than two years to produce, or property with a production period exceeding one year and a cost exceeding $1 million.

(6) The UNICAP rules do not apply to advertising, selling, and research and experimentation expenditures, mine development and exploration costs, property held for personal use, and to freelance authors, photographers, and artists whose personal efforts create the product.

f.

Business meals, entertainment, and travel

(1) Receipts must be maintained for all lodging expenditures and for other expenditures of $75 or more except transportation expenditures where receipts are not readily available.

(2) Adequate contemporaneous records must be maintained for business meals and entertainment to substantiate the amount of expense, for example, who, when, where, and why (the 4 W’s).

(3) Business meals and entertainment must be directly related or associated with the active conduct of a trade or business to be deductible. The taxpayer or a representative must be present to satisfy this requirement.

(4) The amount of the otherwise allowable deduction for business meals or entertainment must be reduced by 50%. This

50% reduction rule applies to all food, beverage, and entertainment costs (even though incurred in the course of travel away from home) after determining the amount otherwise deductible. The 50% reduction rule will not apply if

(a) The full value of the meal or entertainment is included in the recipient’s income or excluded as a fringe benefit.

(b) An employee is reimbursed for the cost of a meal or entertainment (the 50% reduction rule applies to the party making the reimbursement).

(c) The cost is for a traditional employer-paid employee recreation expense (e.g., a company Christmas party).

(d) The cost is for samples and other promotional activities made available to the public.

(e) The expense is for a sports event that qualifies as a charitable fund-raising event.

(f) The cost is for meals or entertainment sold for full consideration.

(5) The cost of a ticket to any entertainment activity is limited (prior to the 50% reduction rule) to its face value.

(6) No deduction is generally allowed for expenses with respect to an entertainment, recreational, or amusement facility.

(a) Entertainment facilities include yachts, hunting lodges, fishing camps, swimming pools, etc.

(b) If the facility or club is used for a business purpose, the related out-of-pocket expenditures are deductible even though depreciation, etc. of the facility is not deductible.

(7) No deduction is allowed for dues paid to country clubs, golf and athletic clubs, airline clubs, hotel clubs, and luncheon clubs. Dues are generally deductible if paid to professional organizations (accounting, medical, and legal associations), business leagues, trade associations, chambers of commerce, boards of trade, and civic and public service organizations (Kiwanis, Lions, Elks).

(8)

Transportation and travel expenses are deductible if incurred in the active conduct of a trade or business.

(a) Deductible transportation expenses include local transportation between two job locations, but excludes commuting expenses between residence and job.

(b) Deductible travel expenses are those incurred while temporarily “away from tax home” overnight including meals, lodging, transportation, and expenses incident to travel (clothing care, etc.).

[1] Travel expenses to and from domestic destination are fully deductible if business is the primary purpose of trip.

[2] Actual automobile expenses can be deducted, or taxpayers can use standard mileage rate of 56.5¢ per mile beginning January 1, 2013, for all business miles (plus parking and tolls).

[3] No deduction is allowed for travel as a form of education. This rule applies when a travel expense would otherwise be deductible only on the ground that the travel itself serves educational purposes.

[4] No deduction is allowed for expenses incurred in attending a convention, seminar, or similar meeting for investment purposes.

g. Deductions for

business gifts are limited to

$25 per recipient each year.

(1) Advertising and promotional gifts costing $4 or less are not limited.

(2) Gifts of tangible personal property costing $400 or less are deductible if awarded as an employee achievement award for length of service or safety achievement.

(3) Gifts of tangible personal property costing $1,600 or less are deductible if awarded as an employee achievement award under a qualified plan for length of service or safety achievement.

(a) Plan must be written and nondiscriminatory.

(b) Average cost of all items awarded under the plan during the tax year must not exceed $400.

h.

Bad debts are generally deducted in the year they become worthless.

(1) There must have been a valid “debtor-creditor” relationship.

(2) A

business bad debt is one that is incurred in the trade or business of the lender.

(a) Deductible against ordinary income (toward AGI)

(b) Deduction allowed for partial worthlessness

(3) Business bad debts must be deducted under the specific charge-off method (the reserve method generally cannot be used).

(a) A deduction is allowed when a specific debt becomes partially or totally worthless.

(b) A bad debt deduction is available for accounts or notes receivable only if the amount owed has already been included in gross income for the current or a prior taxable year. Since receivables for services rendered of a cash method taxpayer have not yet been included in gross income, the receivables cannot be deducted when they become uncollectible.

(4) A

nonbusiness bad debt (not incurred in trade or business) can only be deducted

(a) If totally worthless

(b) As a short-term capital loss

(5) Guarantor of debt who has to pay takes same deduction as if the loss were from a direct loan

(a) Business bad debt if guarantee related to trade, business, or employment

(b) Nonbusiness bad debt if guarantee entered into for profit but not related to trade or business

i. A

hobby is an activity not engaged in for profit (e.g., stamp or card collecting engaged in for recreation and personal pleasure).

(1) Special rules generally limit the deduction of hobby expenses to the amount of hobby gross income. No net loss can generally be deducted for hobby activities.

(2) Hobby expenses are deductible as itemized deductions in the following order:

(a) First deduct taxes, interest, and casualty losses pertaining to the hobby.

(b) Then other hobby operating expenses are deductible to the extent they do not exceed hobby gross income reduced by the amounts deducted in (a). Out-of-pocket expenses are deducted before depreciation. These hobby expenses are aggregated with other miscellaneous itemized deductions that are subject to the 2% of AGI floor.

EXAMPLE

Glenn is an engineer who races a Formula Three car as a hobby. This year Glenn received a salary of $97,000 from his employer and won $3,000 in various car races, while incurring $9,000 of out-of-pocket expenses in his racing hobby. Glenn must include the $3,000 of prizes in his gross income, raising his AGI to $100,000. His $9,000 of hobby expenses are only deductible to the extent of $3,000. Assuming that Glenn itemizes his deductions but has no other miscellaneous itemized deductions, his hobby expenses would result in a deduction of $3,000 − (2% × $100,000) = $1,000.

(3) An activity is presumed to be for profit (not a hobby) if it produces a net profit in at least three out of five consecutive years (two out of seven years for horses).

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 60 THROUGH 69

3.

Net operating loss

a. A NOL is generally a business loss but may occur even if an individual is not engaged in a separate trade or business (e.g., a NOL created by a personal casualty loss).

b. A NOL may be carried

back two years and carried

forward twenty years to offset taxable income in those years.

(1) Carryback is first made to the second preceding year.

(2) Taxpayer may elect not to carryback and only carry forward twenty years.

(3) A three-year carryback period is permitted for the portion of the NOL that relates to casualty and theft losses of individual taxpayers, and to NOLs that are attributable to presidentially declared disasters and are incurred by taxpayers engaged in farming or by a small business.

(4) A small business is any trade or business (including one conducted by a corporation, partnership, or sole proprietorship) with average annual gross receipts of $5 million or less for the three-year tax period preceding the loss year.

c. The following cannot be included in the computation of a NOL:

(1) Any NOL carry forward or carry back from another year

(2) Excess of capital losses over capital gains. Excess of nonbusiness capital losses over nonbusiness capital gains even if overall gains exceed losses

(3) Personal and dependency exemptions

(4) Excess of nonbusiness deductions (usually itemized deductions) over nonbusiness income

(a) The standard deduction is treated as a nonbusiness deduction.

(b) Contributions to a self-employed retirement plan are considered nonbusiness deductions.

(c) Casualty losses (even if personal) are considered business deductions.

(d) Dividends and interest are nonbusiness income; salary and rent are business income.

(5) The domestic production activities deduction (DPAD).

(6) Any remaining loss is a NOL and must be carried back first, unless election is made to carry forward only.

EXAMPLE

George, single with no dependents, started his own delivery business and incurred a loss from the business for 2012. In addition, he earned interest on personal bank deposits of $1,800. After deducting his itemized deductions for interest and taxes of $9,000, and his personal exemption of $3,800, the loss shown on George’s Form 1040 was $20,700. George’s net operating loss would be computed as follows:

| Taxable income |

|

$(20,700) |

| Nonbusiness deductions |

$9,000 |

|

| Nonbusiness income |

−1,800 |

7,200 |

| Personal exemption |

|

3,800 |

| Net operating loss |

|

$(9,700) |

NOW REVIEW MULTIPLE-CHOICE QUESTIONS 70 THROUGH 72

4. Limitation on deductions for

business use of home. To be deductible

a. A portion of the home must be used exclusively and regularly as the

principal place of business, or as a meeting place for patients, clients, or customers.

(1) Exclusive use rule does not apply to the portion of the home used as a day care center and to a place of regular storage of business inventory or product samples if the home is the sole fixed location of a trade or business selling products at retail or wholesale.

(2) If an employee, the exclusive use must be for the convenience of the employer.

(3) A home office qualifies as a taxpayer’s

principal place of business if

(a) It is the place where the primary income-generating functions of the trade or business are performed; or

(b) The office is used to conduct administrative or management activities of the taxpayer’s business, and there is no other fixed location of the business where substantial administrative or management activities are performed. Activities that are administrative or managerial in nature include billing customers, clients, or patients; keeping books and records; ordering supplies; setting up appointments; and forwarding orders or writing reports.

b. Deduction is limited to the excess of gross income derived from the business use of the home over deductions otherwise allowable for taxes, interest, and casualty losses.

c. Any business expenses not allocable to the use of the home (e.g., wages, transportation, supplies) must be deducted before home use expenses.

d. Any business use of home expenses that are disallowed due to the gross income limitation can be carried forward and deducted in future years subject to the same restrictions.

EXAMPLE

Taxpayer uses 10% of his home exclusively for business purposes. Gross income from his business totaled $750, and he incurred the following expenses:

|

Total |

10% Business |

| Interest |

4,000 |

$400 |

| Taxes |

2,500 |

250 |

| Utilities, insurance |

1,500 |

150 |

| Depreciation |

2,000 |

200 |

Since total deductions for business use of the home are limited to business gross income, the taxpayer can deduct the following for business use of his home: $400 interest; $250 taxes; $100 utilities and insurance; and $0 depreciation (operating expenses such as utilities and insurance must be deducted before depreciation). The remaining $50 of utilities and insurance, and $200 of depreciation can be carried forward and deducted in future years subject to the same restrictions.

e. For tax years beginning after 2012, a taxpayer may elect to use an optional safe harbor method for deducting business use of home expenses. Under this method, a prescribed rate of $5 is multiplied by the square footage devoted to business use (limited to 300 square feet). The business use of home deduction (maximum of $1,500) is then limited to business gross income less business expenses not allocable to the use of the home. No depreciation deduction for the business use of the home is allowed for a year in which the safe harbor method is used.

5. Loss deductions incurred in a trade or business, or in the production of income, are limited to the amount a taxpayer has “

at risk.”

a. Applies to all activities except the leasing of personal property by a closely held corporation (5 or fewer individuals own more than 50% of stock)

b. Applies to individuals and closely held regular corporations

c. Amount “at risk” includes

(1) The cash and adjusted basis of property contributed by the taxpayer, and

(2) Liabilities for which the taxpayer is personally liable; excludes nonrecourse debt.

d. For real estate activities, a taxpayer’s amount at risk includes “qualified” nonrecourse financing secured by the real property used in the activity.

(1) Nonrecourse financing is qualified if it is borrowed from a lender engaged in the business of making loans (e.g., bank, savings and loan) provided that the lender is not the promoter or seller of the property or a party related to either; or is borrowed from or guaranteed by any federal, state, or local government or instrumentality thereof.

(2) Nonrecourse financing obtained from a qualified lender who has an equity interest in the venture is treated as an amount at risk, as long as the terms of the financing are commercially reasonable.

(3) The nonrecourse financing must not be convertible, and no person can be personally liable for repayment.

e. Excess losses can be carried over to subsequent years (no time limit) and deducted when the “at risk” amount has been increased.

f. Previously allowed losses will be recaptured as income if the amount at risk is reduced below zero.

6.

Losses and credits from passive activities may generally only be used to offset income from (or tax allocable to) passive activities. Passive losses may not be used to offset active income (e.g., wages, salaries, professional fees, etc.) or portfolio income (e.g., interest, dividends, annuities, royalties, etc.).

EXAMPLE

Ken has salary income, a loss from a partnership in whose business Ken does not materially participate, and income from a limited partnership. Ken may offset the partnership loss against the income from the limited partnership, but not against his salary income.

EXAMPLE

Robin has dividend and interest income of $40,000 and a passive activity loss of $30,000. The passive activity loss cannot be offset against the dividend and interest income.

a. Applies to individuals, estates, trusts, closely held C corporations, and personal service corporations

(1) A closely held C corporation is one with five or fewer shareholders owning more than 50% of stock.

(2) Personal service corporation is an incorporated service business with more than 10% of its stock owned by shareholder-employees.

b.