Multiple-Choice Answers and Explanations

Answers

Explanations

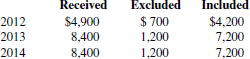

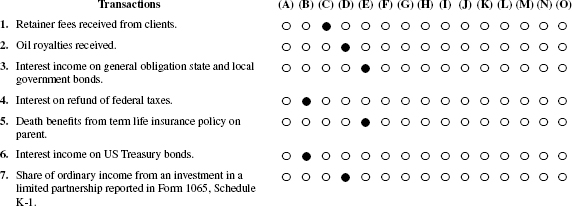

1. (c) The requirement is to determine the pension (annuity) amounts excluded from income for 2012, 2013, and 2014. Brown’s contribution of $12,000 will be recovered pro rata over the life of the annuity. Under this rule, $100 per month (12,000 ÷ 120 months) is excluded from income.

2. (b) The requirement is to determine the amount of life insurance proceeds that must be included in gross income by Decker, on the death of Fuller’s parent. Life insurance proceeds paid because of the insured person’s death are generally excluded from gross income. However, the exclusion generally does not apply if the insurance policy was obtained by the beneficiary in exchange for valuable consideration from a person other than the insurance company. Here, Decker purchased the policy from Fuller for $25,000 and paid an additional $40,000 in premiums, so Decker must include in gross income the excess of insurance proceeds over his investment in the policy [$200,000 − ($25,000 + $40,000) = $135,000.

3. (b) The requirement is to determine the amount of life insurance payments to be included in a widow’s gross income. Life insurance proceeds paid by reason of death are excluded from income if paid in a lump sum or in installments. If the payments are received in installments, the principal amount of the policy divided by the number of annual payments is excluded each year. Therefore, $1,200 of the $5,200 insurance payment is included in Penelope’s gross income.

| Annual installment | $ 5,200 |

| Principal amount ($100,000 ÷ 25) | – 4,000 |

| Gross income | $ 1,200 |

4. (c) The requirement is to determine the correct statement regarding a “cafeteria plan” maintained by an employer. Cafeteria plans are employer-sponsored benefit packages that offer employees a choice between taking cash and receiving qualified benefits (e.g., accident and health insurance, group-term life insurance, coverage under a dependent care or group legal services program). Thus, employees “may select their own menu of benefits.” If an employee chooses qualified benefits, they are excluded from the employee’s gross income to the extent allowed by law. If an employee chooses cash, it is includible in the employee’s gross income as compensation. Answer (a) is incorrect because participation is restricted to employees only. Answer (b) is incorrect because there is no minimum service requirement that must be met before an employee can participate in a plan. Answer (d) is incorrect because deferred compensation plans other than 401(k) plans are not included in the definition of a cafeteria plan.

5. (a) The requirement is to determine the amount of group-term life insurance proceeds that must be included in gross income by Autrey’s widow. Life insurance proceeds paid by reason of death are generally excluded from gross income. Note that although only the cost of the first $50,000 of group-term insurance coverage can be excluded from gross income during the employee’s life, the entire amount of insurance proceeds paid by reason of death will be excluded from the beneficiary’s income.

6. (d) The requirement is to determine the amount of employee death payments to be included in gross income by the widow and the son. The $5,000 employee death benefit exclusion was repealed for decedents dying after August 20, 1996.

7. (b) The requirement is to determine the maximum amount of tax-free group-term life insurance coverage that can be provided to an employee by an employer. The cost of the first $50,000 of group-term life insurance coverage provided by an employer will be excluded from an employee’s income.

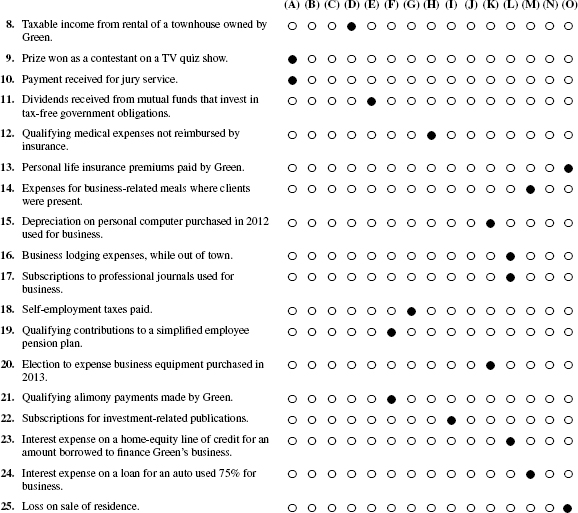

8. (d) The requirement is to determine the amount to be included in Hal’s gross income for the current year. All three amounts that Hal received as a result of his injury are excluded from gross income. Benefits received as workers’ compensation and compensation for damages for physical injuries are always excluded from gross income. Amounts received from an employer’s accident and health plan as reimbursement for medical expenses are excluded so long as the medical expenses are not deducted as itemized deductions.

9. (a) James Martin’s gross income consists of

| Salary | $50,000 |

| Bonus | 10,000 |

| $60,000 |

Medical insurance premiums paid by an employer are excluded from an employee’s gross income. Additionally, qualified moving expense reimbursements are an employee fringe benefit and can be excluded from gross income. This means that an employee can exclude an amount paid by an employer as payment for (or reimbursement of) expenses that would be deductible as moving expenses if directly paid or incurred by the employee.

10. (d) The requirement is to determine how much income Hall should include in his 2013 tax return for the inheritance of stock which he received from his father’s estate. Since the definition of gross income excludes property received as a gift, bequest, devise, or inheritance, Hall recognizes no income upon receipt of the stock. Since the executor of his father’s estate elected the alternate valuation date (August 1), and the stock was distributed to Hall before that date (June 1), Hall’s basis for the stock would be its $4,500 FMV on June 1. Since Hall also sold the stock on June 1 for $4,500, Hall would have no gain or loss resulting from the sale.

11. (b) The requirement is to determine the amount of dividend income that should be reported by Gail Judd. The $100 dividend on Gail’s life insurance policy is treated as a reduction of the cost of insurance (because total dividends have not yet exceeded accumulated premiums paid) and is excluded from gross income. Thus, Gail will report the $300 dividend on common stock and the $500 dividend on preferred stock, a total of $800 as dividend income.

12. (b) The requirement is to determine the amount of dividend income to be reported on Amy’s 2013 return. Dividends are included in income at earlier of actual or constructive receipt. When corporate dividends are paid by mail, they are included in income for the year in which received. Thus, the $875 dividend received 1/2/13 is included in income for 2013. The $500 dividend on a life insurance policy from a mutual insurance company is treated as a reduction of the cost of insurance and is excluded from gross income.

13. (c) The requirement is to determine the amount of dividends to be reported by the Mitchells on a joint return. The amount of dividends would be ($400 + $50 + $300) = $750. The $200 dividend on the life insurance policy is not gross income, but is considered a reduction of the cost of the policy.

14. (d) The requirement is to determine Karen’s basis in the 10 shares of preferred stock received as a stock dividend. Generally, stock dividends are nontaxable, and a taxpayer’s basis for original stock is allocated to the dividend stock in proportion to fair market values. However, any stock that is distributed on preferred stock results in a taxable stock dividend. The amount to be included in the shareholder’s income is the stock’s fair market value on date of distribution. Similarly, the shareholder’s basis for the dividend shares will be equal to their fair market value on date of distribution (10 × $60 = $600).

15. (c) The requirement is to determine the correct statement(s) regarding the amortization of bond premium on a taxable bond. The amount of premium amortization on taxable bonds acquired by the taxpayer after 1987 is treated as an offset to the amount of interest income reported on the bond. The method of calculating the annual amortization is determined by the date the bond was issued, as opposed to the acquisition date. If the bond was issued after September 27, 1985, the amortization must be calculated under the constant yield to maturity method. Otherwise, the amortization must be made ratably over the life of the bond. Under the constant yield to maturity method, the amortizable bond premium is computed on the basis of the taxpayer’s yield to maturity, using the taxpayer’s basis for the bond, and compounding at the close of each accrual period.

16. (c) The requirement is to determine whether two statements are true concerning the exclusion of interest income on US Series EE Bonds that are redeemed to pay for higher education. The accrued interest on US Series EE savings bonds that are redeemed by a taxpayer is excluded from gross income to the extent that the aggregate redemption proceeds (principal plus interest) are used to finance the higher education of the taxpayer, taxpayer’s spouse, or dependents. Qualified higher educational expenses include tuition and fees, but not room and board or the cost of courses involving sports, games, or hobbies that are not part of a degree program. In determining the amount of available exclusion, qualified educational expenses must be reduced by qualified scholarships that are exempt from tax, and any other nontaxable payments such as veteran’s educational assistance and employer-provided educational assistance.

17. (a) The requirement is to determine the amount of interest subject to tax in Kay’s 2013 tax return. Interest must generally be included in gross income, unless a specific statutory provision provides for its exclusion (e.g., interest on municipal bonds). Interest on US Treasury certificates and on a refund of federal income tax would be subject to tax on Kay’s 2013 tax return.

18. (c) The requirement is to determine the amount of interest income taxable on Charles and Marcia’s joint income tax return. A taxpayer’s income includes interest on state and federal income tax refunds and interest on federal obligations, but excludes interest on state obligations. Here, their joint taxable income must include the $500 interest on federal income tax refund, $600 interest on state income tax refund, and $800 interest on federal government obligations, but will exclude the $1,000 tax-exempt interest on state government obligations. Although a refund of federal income tax would be excluded from gross income, any interest on a refund must be included in gross income.

19. (a) The requirement is to determine the condition that must be met for tax exemption of accumulated interest on Series EE US Savings Bonds. An individual may be able to exclude from income all or a part of the interest received on the redemption of Series EE US Savings Bonds. To qualify, the bonds must be issued after December 31, 1989, the purchaser of the bonds must be the sole owner of the bonds (or joint owner with his or her spouse), and the owner(s) must be at least twenty-four years old before the bond’s issue date. To exclude the interest the redemption proceeds must be used to pay the tuition and fees incurred by the taxpayer, spouse, or dependents to attend a college or university or certain vocational schools.

20. (d) The requirement is to determine the amount of tax-exempt interest. Interest on obligations of a state or one of its political subdivisions (e.g., New York Port Authority bonds), or a possession of the US (e.g., Puerto Rico Commonwealth bonds) is tax-exempt.

21. (c) Stone will report $1,700 of interest income. Interest on FIT refunds, personal injury awards, US savings bonds, and most other sources is fully taxable. However, interest on state or municipal bonds is generally not taxable.

22. (d) The requirement is to determine how Don Raff’s $500 interest forfeiture penalty should be reported. An interest forfeiture penalty for making a premature withdrawal from a certificate of deposit should be deducted from gross income in arriving at adjusted gross income in the year in which the penalty is incurred, which in this case is 2013.

23. (c) The requirement is to determine which payment(s) must be included in a recipient’s gross income. A candidate for a degree can exclude amounts received as a scholarship or fellowship if, according to the conditions of the grant, the amounts are used for the payment of tuition and fees, books, supplies, and equipment required for courses at an educational institution. All payments received for services must be included in income, even if the services are a condition of receiving the grant or are required of all candidates for the degree. Here, the payment to a graduate assistant for a part-time teaching assignment and the grant to a Ph.D. candidate for participation in research are payments for services and must be included in income.

24. (c) The requirement is to determine the amount of scholarship awards that Majors should include as taxable income in 2013. Only a candidate for a degree can exclude amounts received as a scholarship award. The exclusion available to degree candidates is limited to amounts received for the payment of tuition and fees, books, supplies, and equipment required for courses at the educational institution. Since Majors is a candidate for a graduate degree, Majors can exclude the $10,000 received for tuition, fees, books, and supplies required for courses. However, the $2,000 stipend for research services required by the scholarship must be included in taxable income for 2013.

25. (a) The requirement is to determine a lessor’s 2013 gross income. A lessor excludes from income any increase in the value of property caused by improvements made by the lessee, unless the improvements were made in lieu of rent. In this case, there is no indication that the improvements were made in lieu of rent. Therefore, for 2013, Farley should only include the six rent payments in income: 6 × $1,000 = $6,000.

26. (d) The requirement is to determine the amount of alimony recapture that must be included in Bob’s gross income for 2013. Alimony recapture may occur if alimony payments sharply decline in the second and third years that payments are made. The payor must report the recaptured alimony as gross income in the third year, and the payee is allowed a deduction for the same amount. Recapture for the second year (2012) occurs to the extent that the alimony paid in the second year ($20,000) exceeds the alimony paid in the third year ($0) by more than $15,000 [i.e., $20,000 − ($0 + $15,000) = $5,000 of recapture].

Recapture for the first year (2011) occurs to the extent that the alimony paid in the first year ($50,000) exceeds the average alimony paid in the second and third years by more than $15,000. For this purpose, the alimony paid in the second year ($20,000) must be reduced by the amount of recapture for that year ($5,000).

| First year (2011) payment | $500 | |

| Second year (2012) payment ($20,000 − $5,000) | $15,000 | |

| Third year (2013) payment | +0 | |

| Total | $15,000 | |

| ÷2 | (7,500) | |

| (15,000) | ||

| Recapture for first year (2011) | $27,500 |

Thus, the total recapture to be included in Bob’s gross income for 2013 is $5,000 + $27,500 = $32,500.

27. (c) The requirement is to determine which conditions must be present in a divorce agreement for a payment to qualify as deductible alimony. In order for a payment to be deductible by the payor as alimony, the payment must be made in cash or its equivalent, the payment must be received by or on behalf of a spouse under a divorce or separation instrument, the payments must terminate at the recipient’s death, and must not be designated as other than alimony (e.g., child support).

28. (d) The requirement is to determine which of the following would be included in gross income by Darr who is an employee of Sorce C corporation. The definition of gross income includes income from whatever source derived and would include the dividend income on shares of stock that Darr received for services rendered. However, items specifically excluded from gross income include amounts received as a gift or inheritance, as well as employer-provided medical insurance coverage under a health plan.

29. (c) The requirement is to determine the correct statement regarding the inclusion of social security benefits in gross income for 2013. A maximum of 85% of social security benefits may be included in gross income for high-income taxpayers. Thus, no matter how high a taxpayer’s income, 85% of the social security benefits is the maximum amount of benefits to be included in gross income.

30. (c) The requirement is to determine the amount that Perle should include in taxable income as a result of performing dental services for Wood. An exchange of services for property or services is sometimes called bartering. A taxpayer must include in income the amount of cash and the fair market value of property or services received in exchange for the performance of services. Here, Perle’s taxable income should include the $200 cash and the bookcase with a comparable value of $350, a total of $550.

31. (b) The requirement is to determine the amount of payments to be included in Mary’s income tax return for 2013. Alimony must be included in gross income by the payee and is deductible by the payor. In order to be treated as alimony, a payment must be made in cash and be received by or paid on behalf of the former spouse. Amounts treated as child support are not alimony; they are neither deductible by the payor, nor taxable to the payee. Payments will be treated as child support to the extent that payments will be reduced upon the happening of a contingency relating to a child (e.g., the child attaining a specified age, marrying, becoming employed). Here, since future payments will be reduced by 20% on their child’s 18th birthday, the total cash payments of $10,000 ($7,000 paid directly to Mary plus the $3,000 of tuition paid on Mary’s behalf) must be reduced by 20% and result in $8,000 of alimony income for Mary. The remaining $2,000 is treated as child support and is not taxable.

32. (b) The requirement is to determine the amount of interest for overpayment of 2012 state income tax and state income tax refund that is taxable in Clark’s 2013 federal income tax return. The $10 of interest income on the tax refund is taxable and must be included in gross income. On the other hand, a state income tax refund is included in gross income under the “tax benefit rule” only if the refunded amount was deducted in a prior year and the deduction provided a benefit because it reduced the taxpayer’s federal income tax. The payment of state income taxes will not result in a “benefit” if an individual does not itemize deductions, or is subject to the alternative minimum tax for the year the taxes are paid. Individuals who file Form 1040EZ are not allowed to itemize deductions and must use the standard deduction. Since state income taxes are only allowed as an itemized deduction and Clark did not itemize for 2012 (he used Form 1040EZ), his $900 state income tax refund is nontaxable and is excluded from gross income.

33. (d) The requirement is to determine the amount to be reported in Hall’s 2013 return as alimony income. If a divorce agreement specifies both alimony and child support, but less is paid than required, then payments are first allocated to child support, with only the remainder in excess of required child support to be treated as alimony. Pursuant to Hall’s divorce agreement, $3,000 was to be paid each month, of which $600 was designated as child support, leaving a balance of $2,400 per month to be treated as alimony. However, during 2013, only $5,000 was paid to Hall by her former husband which was less than the $36,000 required by the divorce agreement. Since required child support payments totaled $600 × 12 = $7,200 for 2013, all $5,000 of the payments actually received by Hall during 2013 is treated as child support, with nothing remaining to be reported as alimony.

34. (b) The requirement is to determine the amount of income to be reported by Lee in connection with the receipt of stock for services rendered. Compensation for services rendered that is received by a cash method taxpayer must be included in income at its fair market value on the date of receipt.

35. (c) The requirement is to determine when Ross was subject to “regular tax” with regard to stock that was acquired through the exercise of an incentive stock option. There are no tax consequences when an incentive stock option is granted to an employee. When the option is exercised, any excess of the stock’s FMV over the option price is a tax preference item for purposes of the employee’s alternative minimum tax. However, an employee is not subject to regular tax until the stock acquired through exercise of the option is sold.

If the employee holds the stock acquired through exercise of the option at least two years from the date the option was granted (and holds the stock itself at least one year), the employee’s realized gain is treated as long-term capital gain in the year of sale, and the employer receives no compensation deduction. If the preceding holding period rules are not met at the time the stock is sold, the employee must report ordinary income to the extent that the stock’s FMV at date of exercise exceeded the option price, with any remaining gain reported as long-term or short-term capital gain. As a result, the employer receives a compensation deduction equal to the amount of ordinary income reported by the employee.

36. (a) The requirement is to determine the amount that is taxable as alimony in Ann’s return. In order to be treated as alimony, a payment must be made in cash and be received by or on behalf of the payee spouse. Furthermore, cash payments must be required to terminate upon the death of the payee spouse to be treated as alimony. In this case, the transfer of title in the home to Ann is not a cash payment and cannot be treated as alimony. Although the mortgage payments are cash payments made on behalf of Ann, the payments are not treated as alimony because they will be made throughout the full twenty-year mortgage period and will not terminate in the event of Ann’s death.

37. (c) The requirement is to determine the correct statement with regard to income in respect of a cash basis decedent. Income in respect of a decedent is income earned by a decedent before death that was not includible in the decedent’s final income tax return because of the decedent’s method of accounting (e.g., receivables of a cash basis decedent). Such income must be included in gross income by the person who receives it and has the same character (e.g., ordinary or capital) as it would have had if the decedent had lived.

38. (d) The requirement is to determine the amount of gross income. Drury’s gross income includes the $36,000 salary, the $500 of premiums paid by her employer for group-term life insurance coverage in excess of $50,000, and the $5,000 proceeds received from a state lottery.

39. (b) The requirement is to determine the amount of foster child payments to be included in income by the Charaks. Foster child payments are excluded from income to the extent they represent reimbursement for expenses incurred for care of the foster child. Since the payments ($3,900) exceeded the expenses ($3,000), the $900 excess used for the Charaks’ personal expenses must be included in their gross income.

40. (b) The requirement is to determine the amount and the year in which the tip income should be included in Pierre’s gross income. If an individual receives less than $20 in tips during one month while working for one employer, the tips do not have to be reported to the employer and the tips are included in the individual’s gross income when received. However, if an individual receives $20 or more in tips during one month while working for one employer, the individual must report the total amount of tips to that employer by the tenth day of the next month. Then the tips are included in gross income for the month in which they are reported to the employer. Here, Pierre received $2,000 in tips during December 2013 that he reported to his employer in January 2014. Thus, the $2,000 of tips will be included in Pierre’s gross income for 2014.

41. (c) The requirement is to determine the correct statement regarding the alimony deduction in connection with a divorce. To be considered alimony, cash payments must terminate on the death of the payee spouse. Answer (a) is incorrect because alimony payments cannot be contingent on the status of the divorced couple’s children. Answer (b) is incorrect because the divorced couple cannot be members of the same household at the time the alimony is paid. Answer (d) is incorrect because only cash payments can be considered alimony.

42. (d) The requirement is to determine the amount of a $10,000 award for outstanding civic achievement that Joan should include in her 2013 adjusted gross income. An award for civic achievement can be excluded from gross income only if the recipient was selected without any action on his/her part, is not required to render substantial future services as a condition of receiving the award, and designates that the award is to be directly transferred by the payor to a governmental unit or a tax-exempt charitable, educational, or religious organization. Here, since Joan accepted and actually received the award, the $10,000 must be included in her adjusted gross income.

43. (d) The requirement is to determine the amount of lottery winnings that should be included in Gow’s taxable income. Lottery winnings are gambling winnings and must be included in gross income. Gambling losses are deductible from AGI as a miscellaneous deduction (to the extent of winnings) not subject to the 2% of AGI floor if a taxpayer itemizes deductions. Since Gow elected the standard deduction for 2013, the $400 spent on lottery tickets is not deductible. Thus, all $5,000 of Gow’s lottery winnings are included in his taxable income.

44. (d) The requirement is to determine the amount of advance rents and lease cancellation payments that should be reported on Lake Corp.’s 2013 tax return. Advance rental payments must be included in gross income when received, regardless of the period covered or whether the taxpayer uses the cash or accrual method. Similarly, lease cancellation payments are treated as rent and must be included in income when received, regardless of the taxpayer’s method of accounting.

45. (c) The requirement is to determine the amount to be reported as gross income. Gross income includes the $50,000 of recurring rents plus the $2,000 lease cancellation payment. The $1,000 of lease improvements are excluded from income since they were not required in lieu of rent.

46. (c) The requirement is to determine the amount of net rental income that Gow should include in his adjusted gross income. Since Gow lives in one of two identical apartments, only 50% of the expenses relating to both apartments can be allocated to the rental unit.

| Rent | $7,200 |

| Less: | |

| Real estate taxes (50% × $6,400) | (3,200) |

| Painting of rental apartment | (800) |

| Fire insurance (50% × $600) | (300) |

| Depreciation (50% × $5,000) | (2,500) |

| Net rental income | $400 |

47. (a) The requirement is to determine the amount of rent income to be reported on Amy’s 2013 return. Both the $6,000 of rent received for 2013, as well as the $1,000 of advance rent received in 2013 for the last two months of the lease must be included in income for 2013. Advance rent must be included in income in the year received regardless of the period covered or the accounting method used.

48. (a) The requirement is to determine the amount to be reported as rent revenue in an accrual-basis taxpayer’s tax return for 2013. An accrual-basis taxpayer’s rent revenue would consist of the amount of rent earned during the taxable year plus any advance rent received. Advance rents must be included in gross income when received under both the cash and accrual methods, even though they have not yet been earned. In this case, Royce’s rent revenue would be determined as follows:

| Rent receivable 12/31/12 | $35,000 |

| Rent receivable 12/31/13 | 25,000 |

| Decrease in receivables | (10,000) |

| Rent collections during 2013 | 50,000 |

| Rent deposits | 5,000 |

| Rent revenue for 2013 | $45,000 |

The rent deposits must be included in gross income for 2013 because they are nonrefundable deposits.

49. (a) The requirement is to determine the amount of state unemployment benefits that should be included in adjusted gross income for 2013. Unemployment compensation benefits received must generally be included in gross income.

50. (d) The requirement is to determine the correct statement regarding the reporting of income by a cash-basis taxpayer. A cash-basis taxpayer should report gross income for the year in which income is either actually or constructively received, whether in cash or in property. Constructive receipt means that an item of income is unqualifiedly avail-able to the taxpayer without restriction (e.g., interest on bank deposit is income when credited to account).

51. (b) The requirement is to determine which taxpayer may use the cash method of accounting. The cash method cannot generally be used if inventories are necessary to clearly reflect income, and cannot generally be used by C corporations, partnerships that have a C corporation as a partner, tax shelters, and certain tax-exempt trusts. Taxpayers permitted to use the cash method include a qualified personal service corporation, an entity (other than a tax shelter) if for every year it has average gross receipts of $5 million or less for any prior three-year period (and provided it does not have inventories), and a small taxpayer with average annual gross receipts of $1 million or less for any prior three-year period may use the cash method and is excepted from the requirement to account for inventories.

52. (b) The requirement is to select the correct statement regarding the $1,000 of additional income determined by Stewart, an accrual method corporation. Under the accrual method, income generally is reported in the year earned. If an amount is included in gross income on the basis of a reasonable estimate, and it is later determined that the exact amount is more, then the additional amount is included in income in the tax year in which the determination of the exact amount is made. Here, Stewart properly accrued $5,000 of income for 2012 on the basis of a reasonable estimate and discovered that the exact amount was $6,000 in 2013. Therefore, the additional $1,000 of income is properly includible in Stewart’s 2013 income tax return.

53. (b) The requirement is to determine the correct statement regarding Axis Corp.’s deduction for its employees bonus expense. An accrual-method taxpayer can deduct compensation (including a bonus) when there is an obligation to make payment, the services have been performed, and the amount can be determined with reasonable accuracy. It is not required that the exact amount of compensation be determined during the taxable year. As long as the computation is known and the liability is fixed, accrual is proper even though the profits upon which the compensation are based are not determined until after the end of the year.

Although compensation is generally deductible only for the year in which the compensation is paid, an exception is made for accrual method taxpayers so long as payment is made within 2 1/2 months after the end of the year. Here, since the services were performed, the method of computation was known, the amount was reasonable, and payment was made by March 15, 2013, the bonus expense may be deducted on Axis Corp.’s 2012 tax return. Note that the bonus could not be a disguised dividend because none of the employees were shareholders.

54. (b) The requirement is to determine the amount of the 2012 interest payment of $12,000 that was deductible on Michaels’ 2013 income tax return. Generally, there is no deduction for prepaid interest. When a taxpayer pays interest for a period that extends beyond the end of the tax year, the interest paid in advance must be spread over the period to which it applies. Michaels paid $12,000 of interest during 2012 that relates to the period beginning December 1, 2012, and ending November 30, 2013. Therefore, 1/12 × $12,000 = $1,000 of interest was deductible for 2012, and 11/12 × $12,000 = $11,000 is deductible for 2013.

55. (c) The requirement is to determine the amount of income to be reported in Blair’s 2013 return for the stock received in satisfaction of a client fee owed to Blair. Since Blair is a cash method taxpayer, the amount of income to be recognized equals the $4,000 fair market value of the stock on date of receipt. Note that the $4,000 of income is reported by Blair in 2013 when the stock is received; not in 2014 when the stock is sold.

56. (d) The requirement is to determine whether the accrual method of tax reporting is mandatory for a sole proprietor when there are accounts receivable for services rendered, or year-end merchandise inventories. A taxpayer’s taxable income should be computed using the method of accounting by which the taxpayer regularly computes income in keeping the taxpayer’s books. Either the cash or the accrual method generally can be used so long as the method is consistently applied and clearly reflects income. However, when the production, purchase, or sale of merchandise is an income producing factor, inventories must be maintained to clearly reflect income. If merchandise inventories are necessary to clearly determine income, only the accrual method of tax reporting can be used for purchases and sales.

57. (d) The requirement is to determine the amount of salary taxable to Burg in 2013. Since Burg is a cash-basis taxpayer, salary is taxable to Burg when actually or constructively received, whichever is earlier. Since the $30,000 of unpaid salary was unqualifiedly available to Burg during 2013, Burg is considered to have constructively received it. Thus, Burg must report a total of $80,000 of salary for 2013; the $50,000 actually received plus $30,000 constructively received.

58. (d) The requirement is to determine the 2013 medical practice net income for a cash basis physician. Dr. Berger’s income consists of the $200,000 received from patients and the $30,000 received from third-party reimbursers during 2013. His 2013 deductions include the $20,000 of salaries and $24,000 of other expenses paid in 2013. The year-end bonuses will be deductible for 2014.

59. (c) The requirement is to determine which taxpayer may use the cash method of accounting for tax purposes. The cash method generally cannot be used (and the accrual method must be used to measure sales and cost of goods sold) if inventories are necessary to clearly determine income. Additionally, the cash method generally cannot generally be used by (1) a corporation (other than an S corporation), (2) a partnership with a corporation as a partner, and (3) a tax shelter. However, this prohibition against the use of the cash method in the preceding sentence does not apply to a farming business, a qualified personal service corporation (e.g., a corporation performing services in health, law, engineering, architecture, accounting, actuarial science, performing arts, or consulting), and a corporation or partnership (that is not a tax shelter) that does not have inventories and whose average annual gross receipts for the most recent three-year period do not exceed $5 million.

60. (a) Uniform capitalization rules generally require that all costs incurred (both direct and indirect) in manufacturing or constructing real or personal property, or in purchasing or holding property for sale, must be capitalized as part of the cost of the property. However, these rules do not apply to a “small retailer or wholesaler” who acquires personal property for resale if the retailer’s or wholesaler’s average annual gross receipts for the three preceding taxable years do not exceed $10 million.

61. (a) The requirement is to determine whether the cost of merchandise, and business expenses other than the cost of merchandise, can be deducted in calculating Mock’s business income from a retail business selling illegal narcotic substances. Generally, business expenses that are incurred in an illegal activity are deductible if they are ordinary and necessary, and reasonable in amount. Under a special exception, no deduction or credit is allowed for any amount that is paid or incurred in carrying on a trade or business which consists of trafficking in controlled substances. However, this limitation that applies to expenditures in connection with the illegal sale of drugs does not alter the normal definition of gross income (i.e., sales minus cost of goods sold). As a result, in arriving at gross income from the business, Mock may reduce total sales by the cost of goods sold, and thus is allowed to deduct the cost of merchandise in calculating business income.

62. (b) The requirement is to determine the percentage of business meals expense that Banks Corp. can deduct for 2013. Generally, only 50% of business meals and entertainment is deductible. When an employer reimburses its employees’ substantiated qualifying business meal expenses, the 50% limitation on deductibility applies to the employer.

63. (a) The requirement is to determine which of the costs is not included in inventory under the Uniform Capitalization (UNICAP) rules for goods manufactured by a taxpayer. UNICAP rules require that specified overhead items must be included in inventory including factory repairs and maintenance, factory administration and officers’ salaries related to production, taxes (other than income taxes), the costs of quality control and inspection, current and past service costs of pension and profit-sharing plans, and service support such as purchasing, payroll, and warehousing costs. Nonmanufacturing costs such as selling, advertising, and research and experimental costs are not required to be included in inventory.

64. (d) If no exceptions are met, the uniform capitalization rules generally require that all costs incurred in purchasing or holding inventory for resale must be capitalized as part of the cost of the inventory. Costs that must be capitalized with respect to inventory include the costs of purchasing, handling, processing, repackaging and assembly, and off-site storage. An off-site storage facility is one that is not physically attached to, and an integral part of, a retail sales facility. Service costs such as marketing, selling, advertising, and general management are immediately deductible and need not be capitalized as part of the cost of inventory.

65. (d) The requirement is to determine the correct statement regarding the deduction for bad debts in the case of a corporation that is not a financial institution. Except for certain small banks that can use the experience method of accounting for bad debts, all taxpayers (including those that previously used the reserve method) are required to use the direct charge-off method of accounting for bad debts.

66. (d) The requirement is to determine the amount of life insurance premium that can be deducted in Ram Corp.’s income tax return. Generally, no deduction is allowed for expenditures that produce tax-exempt income. Here, no deduction is allowed for the $6,000 life insurance premium because Ram is the beneficiary of the policy, and the proceeds of the policy will be excluded from Ram’s income when the officer dies.

67. (a) The requirement is to determine the amount of bad debt deduction for a cash-basis taxpayer. Accounts receivable resulting from services rendered by a cash-basis taxpayer have a zero tax basis, because the income has not yet been reported. Thus, failure to collect the receivable results in a nondeductible loss.

68. (c) The requirement is to determine the loss that Cook can claim as a result of the worthless note receivable in 2013. Cook’s $1,000 loss will be treated as a nonbusiness bad debt, deductible as a short-term capital loss. The loss is not a business bad debt because Cook was not in the business of lending money, nor was the loan required as a condition of Cook’s employment. Since Cook owned no stock in Precision, the loss could not be deemed to be a loss from worthless stock, deductible as a long-term capital loss.

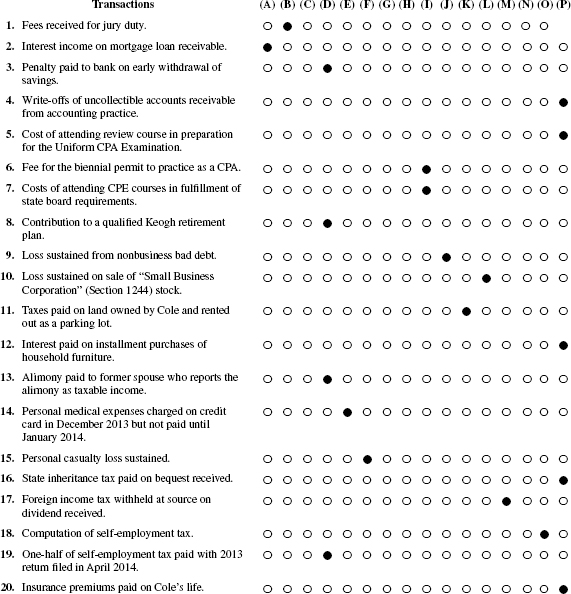

69. (b) The requirement is to determine the amount of gifts deductible as a business expense. The deduction for business gifts is limited to $25 per recipient each year. Thus, Palo Corporation’s deduction for business gifts would be [(4 × $10) + (13 × $25)] = $365.

70. (b) The requirement is to determine Jennifer’s net operating loss (NOL) for 2013. Jennifer’s personal casualty loss of $45,000 incurred as a result of the destruction of her personal residence is allowed as a deduction in the computation of her NOL and is subtracted from her salary income of $30,000, to arrive at a NOL of $15,000. No deduction is allowed for personal and dependency exemptions in the computation of a NOL.

71. (c) The requirement is to determine the amount of net operating loss (NOL) for a self-employed taxpayer for 2013. A NOL generally represents a loss from the conduct of a trade or business and can generally be carried back two years and forward twenty years to offset income in the carryback and carry forward years. Since a NOL generally represents a business loss, an individual taxpayer’s personal and dependency exemptions and an excess of nonbusiness deductions over nonbusiness income cannot be subtracted in computing the NOL. Nonbusiness deductions generally include itemized deductions as well as the standard deduction if the taxpayer does not itemize. In this case, the $6,100 standard deduction offsets the $1,500 of nonbusiness income received in the form of dividends and short-term capital gain, but the excess ($4,600) cannot be included in the NOL computation. Thus, the taxpayer’s NOL simply consists of the $6,000 business loss.

72. (a) The requirement is to determine Destry’s net operating loss (NOL). A net operating loss generally represents a loss from the conduct of a trade or business and can generally be carried back two years and forward twenty years to offset income in the carryback and carry forward years. Since a NOL generally represents a business loss, an individual taxpayer’s personal and dependency exemptions and an excess of nonbusiness deductions (e.g., standard deduction) over nonbusiness income (e.g., interest from savings account) cannot be subtracted in computing the NOL. Similarly, no deduction is allowed for a net capital loss. As a result, Destry’s NOL consists of his net business loss of $16,000 reduced by his business income of $5,000 from wages and $4,000 of net rental income, resulting in a NOL of $7,000.

73. (a) The requirement is to determine the amount of Cobb’s rental real estate loss that can be used as an offset against income from non passive sources. Losses from passive activities may generally only be used to offset income from other passive activities. Although a rental activity is defined as a passive activity regardless of the owner’s participation in the operation of the rental property, a special rule permits an individual to offset up to $25,000 of income that is not from passive activities by losses from a rental real estate activity if the individual actively participates in the rental real estate activity. However, this special $25,000 allowance is reduced by 50% of the taxpayer’s AGI in excess of $100,000, and is fully phased out when AGI exceeds $150,000. Since Cobb’s AGI is $200,000, the special $25,000 allowance is fully phased out and no rental loss can be offset against income from non passive sources.

74. (c) The requirement is to determine the entity to which the rules limiting the deductibility of passive activity losses and credits applies. The passive activity limitations apply to individuals, estates, trusts, closely held C corporations, and personal service corporations. Application of the passive activity loss limitations to personal service corporations is intended to prevent taxpayers from sheltering personal service income by creating personal service corporations and acquiring passive activity losses at the corporate level. A personal service corporation is a corporation (1) whose principal activity is the performance of personal services, and (2) such services are substantially performed by owner-employees. Since passive activity income, losses, and credits from partnerships and S corporations flow through to be reported on the tax returns of the owners of such entities, the passive activity limitations are applied at the partner and shareholder level, rather than to partnerships and S corporations themselves.

75. (c) The requirement is to determine Wolf’s passive loss resulting from his 5% general partnership interest in Gata Associates. A partnership is a pass-through entity and its items of income and loss pass through to partners to be included on their tax returns. Since Wolf does not materially participate in the partnership’s auto parts business, Wolf’s distributable share of the loss from the partnership’s auto parts business is classified as a passive activity loss. Portfolio income or loss must be excluded from the computation of the income or loss resulting from a passive activity, and must be separately passed through to partners.

Portfolio income includes all interest income, other than interest income derived in the ordinary course of a trade or business. Interest income derived in the ordinary course of a trade or business includes only interest income on loans and investments made in the ordinary course of a trade or business of lending money, and interest income on accounts receivable arising in the ordinary course of a trade or business. Since the $20,000 of interest income derived by the partnership resulted from a temporary investment, the interest income must be classified as portfolio income and cannot be netted against the $100,000 operating loss from the auto parts business. Thus, Wolf will report a passive activity loss of $100,000 × 5% = $5,000; and will report portfolio income of $20,000 × 5% = $1,000.

76. (a) The requirement is to determine the correct statement regarding the passive loss rules involving rental real estate activities. By definition, any rental activity is a passive activity without regard as to whether or not the taxpayer materially participates in the activity. Answer (b) is incorrect because interest and dividend income not derived in the ordinary course of business is treated as portfolio income, and cannot be offset by passive rental activity losses when the “active participation” requirement is not met. Answer (c) is incorrect because passive rental activity credits cannot be used to offset the tax attributable to non passive activities. Answer (d) is incorrect because the passive activity rules contain no provision that excludes taxpayers below a certain income level from the limitations imposed by the passive activity rules.

77. (d) The requirement is to determine the correct statement regarding an individual taxpayer’s passive losses relating to rental real estate activities that cannot be currently deducted. Generally, losses from passive activities can only be used to offset income from passive activities. If there is insufficient passive activity income to absorb passive activity losses, the unused losses are carried forward indefinitely or until the property is disposed of in a taxable transaction. Answers (a) and (c) are incorrect because unused passive losses are never carried back to prior taxable years. Answer (b) is incorrect because there is no maximum carry forward period.

78. (b) The requirement is to determine the maximum amount of Sec. 179 expense election that Aviation Corp. will be allowed to deduct for 2013, and the maximum amount of expense election that it can carry over to 2014. Sec. 179 permits a taxpayer to elect to treat up to $500,000 (for 2012 and 2013) of the cost of qualifying depreciable personal property as an expense rather than as a capital expenditure. The $500,000 maximum is reduced dollar-for-dollar by the cost of qualifying property placed in service during the taxable year that exceeds $2 million. Here, since the production machinery cost $570,000, the maximum amount that can be expensed is $500,000. However, this amount is further limited as a deduction for 2013 to Aviation’s taxable income of $405,000 before the Sec. 179 expense deduction. The remainder ($500,000 − $405,000 = $95,000) that is not currently deductible because of the taxable income limitation can be carried over and will be deductible subject to the taxable income limitation in 2014.

79. (c) The requirement is to determine which conditions must be satisfied to enable a taxpayer to expense the cost of new or used tangible depreciable personal property under Sec. 179. For 2012 and 2013, a taxpayer may elect to expense up to $500,000 of the cost of new or used tangible depreciable personal property placed in service during the taxable year. To qualify, the property must be acquired by purchase from an unrelated party for use in the taxpayer’s active trade or business. The maximum cost that can be expensed of $500,000 is reduced dollar-for-dollar by the cost of qualifying property that is placed in service during the year that exceeds $2 million. Additionally, the amount that can be expensed is further limited to the aggregate taxable income derived from the active conduct of any trade or business of the taxpayer.

80. (a) The requirement is to determine the MACRS deduction for the used furniture and fixtures placed in service during 2013. The furniture and fixtures qualify as seven-year property and under MACRS will be depreciated using the 200% declining balance method. Normally, a half-year convention applies to the year of acquisition. However, the mid-quarter convention must be used if more than 40% of all personal property is placed in service during the last quarter of the taxpayer’s taxable year. Since this was Krol’s only acquisition of personal property and the property was placed in service during the last quarter of Krol’s calendar year, the mid-quarter convention must be used. Under this convention, property is treated as placed in service during the middle of the quarter in which placed in service. Since the furniture and fixtures were placed in service in November, the amount of allowable MACRS depreciation is limited to $56,000 × 2/7 × 1/8 = $2,000.

81. (b) The requirement is to determine Sullivan’s MACRS deduction for the apartment building in 2013. The MACRS deduction for residential real property placed in service during 2013 must be determined using the mid-month convention (i.e., property is treated as placed in service at the midpoint of the month placed in service) and the straight-line method of depreciation over a 27.5-year recovery period. Here, the $360,000 cost must first be reduced by the $30,000 allocated to the land, to arrive at a basis for depreciation of $330,000. Since the building was placed in service on June 29, the mid-month convention results in 6.5 months of depreciation for 2013. The MACRS deduction for 2013 is [$330,000 × (6.5 months)/(27.5 × 12 months)] = $6,500.

82. (c) The requirement is to determine the depreciation convention that must be used when a calendar-year taxpayer’s only acquisition of equipment during the year occurs during November. Generally, a half-year convention applies to depreciable personal property, and a mid-month convention applies to depreciable real property. Under the half-year convention, a half-year of depreciation is allowed for the year in which property is placed in service, regardless of when the property is placed in service during the year, and a half-year of depreciation is allowed for the year in which the property is disposed of. However, a taxpayer must instead use a mid-quarter convention if more than 40% of all depreciable personal property acquired during the year is placed in service during the last quarter of the taxable year. Under this convention, property is treated as placed in service (or disposed of) in the middle of the quarter in which placed in service (or disposed of). Since Data Corp. is a calendar-year taxpayer and its only acquisition of depreciable personal property was placed in service during October (i.e., the last quarter of its taxable year), it must use the mid-quarter convention, and will only be allowed a half-quarter of depreciation of its office equipment for 2013.

83. (b) The requirement is to determine the correct statement regarding the modified accelerated cost recovery system (MACRS) of depreciation for property placed in service after 1986. Under MACRS, salvage value is completely ignored for purposes of computing the depreciation deduction, which results in the recovery of the entire cost of depreciable property. Answer (a) is incorrect because used tangible depreciable property is depreciated under MACRS. Answer (c) is incorrect because the cost of some depreciable realty must be depreciated using the straight-line method. Answer (d) is incorrect because the cost of some depreciable realty is included in the ten-year (e.g., single purpose agricultural and horticultural structures) and twenty-year (e.g., farm buildings) classes.

84. (a) The requirement is to determine the correct statement regarding the half-year convention under the general MACRS method. Under the half-year convention that generally applies to depreciable personal property, one-half of the first year’s depreciation is allowed in the year in which the property is placed in service, regardless of when the property is placed in service during the year, and a half-year’s depreciation is allowed for the year in which the property is disposed of, regardless of when the property is disposed of during the year. Answer (b) is incorrect because allowing one-half month’s depreciation for the month that property is placed in service or disposed of is known as the “midmonth convention.”

85. (c) The requirement is to determine the portion of the $600,000 cost of the machine that can be treated as a Sec. 179 expense deduction for 2013. Sec. 179 permits a taxpayer to elect to treat up to $500,000 (for 2012 and 2013) of the cost of qualifying depreciable personal property as an expense rather than as a capital expenditure. However, the $500,000 maximum is reduced dollar-for-dollar by the cost of qualifying property placed in service during the taxable year that exceeds $2 million.

86. (d) The requirement is to determine the amount to be reported in Mel’s gross income for the $400 per month received for business automobile expenses under a nonaccountable plan from Easel Co. Reimbursements and expense allowances paid to an employee under a nonaccountable plan must be included in the employee’s gross income and are reported on the employee’s W-2. The employee must then complete Form 2106 and itemize to deduct business-related expenses such as the use of an automobile.

87. (c) The requirement is to determine the correct statement regarding a second residence that is rented for 200 days and used 50 days for personal use. Deductions for expenses related to a dwelling that is also used as a residence by the taxpayer may be limited. If the taxpayer’s personal use exceeds the greater of 14 days, or 10% of the number of days rented, deductions allocable to rental use are limited to rental income. Here, since Adams used the second residence for 50 days and rented the residence for 200 days, no rental loss can be deducted. All expenses related to the property, including utilities and maintenance, must be allocated between personal use and rental use. Answer (d) is incorrect because only the mortgage interest and taxes allocable to rental use would be deducted in determining the property’s net rental income or loss. Answer (a) is incorrect, since depreciation on the property could be deducted if Adams’ gross rental income exceeds allocable out-of-pocket rental expenses.

88. (a) The requirement is to determine the amount of unreimbursed employee expenses that can be deducted by Gilbert if he does not itemize deductions. Gilbert cannot deduct any of the expenses listed if he does not itemize deductions. The unreimbursed employee business expenses are deductible only as itemized deductions, subsequent to the 2% of AGI floor.

89. (c) The requirement is to determine the amount of moving expense that James can deduct for 2013. Direct moving expenses are deductible if closely related to the start of work at a new location and a distance test (i.e., distance from new job to former residence is at least fifty miles further than distance from old job to former residence) and a time test (i.e., employed at least thirty-nine weeks out of twelve months following move) are met. Since both tests are met, James’ unreimbursed lodging and travel expenses ($1,000), cost of insuring household goods and personal effects during move ($200), cost of shipping household pets ($100), and cost of moving household furnishings and personal effects ($3,000) are deductible. Indirect moving expenses such as pre-move house-hunting, temporary living expenses, and meals while moving are not deductible.

90. (c) The requirement is to determine Martin’s deductible moving expenses. Moving expenses are deductible if closely related to the start of work at a new location and a distance (i.e., new job must be at least fifty miles from former residence) and time (i.e., employed at least thirty-nine weeks out of twelve months following move) tests are met. Here, both tests are met and Martin’s $800 cost of moving his personal belongings is deductible. However, the $300 penalty for breaking his lease is not deductible.

91. (a) Only the direct costs incurred for transporting a taxpayer, his or her family, and their household goods and personal effects from their former residence to their new residence can qualify as deductible moving expenses. The indirect moving expense costs incurred for meals while in transit, house hunting, temporary lodging, to sell or purchase a home, and to break or acquire a lease are not deductible.

92. (d) The requirement is to determine the incorrect statement concerning a Roth IRA. The maximum annual contribution to a Roth IRA is subject to reduction if the taxpayer’s adjusted gross income exceeds certain thresholds. Unlike a traditional IRA, contributions are not deductible and can be made even after the taxpayer reaches age 701/2. The contribution must be made by the due date of the taxpayer’s tax return (not including extensions).

93. (d) The requirement is to determine the maximum amount of adjusted gross income that a taxpayer may have and still qualify to roll over a traditional IRA into a Roth IRA for 2013. For tax years beginning before 2010, a conversion or rollover of a traditional IRA to a Roth IRA could occur if the taxpayer’s AGI did not exceed $100,000 and the taxpayer was not married filing a separate return. The IRA conversion or rollover amount was not taken into account in determining the $100,000 AGI ceiling. However, both the AGI limit and the joint filing requirement have been eliminated for tax years beginning after 2009.

94. (d) The requirement is to determine which statement concerning an education IRA is not correct. Contributions to an education IRA are not deductible, but withdrawals of earnings will be tax-free if used to pay the qualified higher education expenses of the designated beneficiary. The maximum amount that can be contributed to an education IRA is limited to $2,000, but the annual contribution is phased out by adjusted gross income in excess of certain thresholds. Contributions generally cannot be made to an education IRA if the designated beneficiary is age eighteen or older.

95. (a) The requirement is to determine the Whites’ allowable IRA deduction on their 2013 joint return. For married taxpayers filing a joint return for 2013, up to $5,500 can be deducted for contributions to the IRA of each spouse (even if one spouse is not working), provided that the combined earned income of both spouses is at least equal to the amounts contributed to the IRAs. Even though Val is covered by his employer’s qualified pension plan, the Whites are eligible for the maximum deduction because their gross income of $55,000 + $4,000 = $59,000 does not exceed the base amount ($95,000) at which the maximum $5,500 deduction would be reduced. Also note that Pat’s $4,000 of taxable alimony payments is treated as compensation for purposes of qualifying for an IRA deduction. Since they each contributed $5,500 to an IRA account, the allowable deduction on their joint return is $11,000.

96. (d) The requirement is to determine the definition of “earned income” for purposes of computing the annual contribution to a Keogh profit-sharing plan by Davis, a sole proprietor. A self-employed individual may contribute to a qualified retirement plan called a Keogh plan. For 2013, the maximum contribution to a Keogh profit-sharing plan is the lesser of $51,000 or 25% of earned income. For this purpose, “earned income” is defined as net earnings from self-employment (i.e., business gross income minus allowable business deductions) reduced by the deduction for one-half of the self-employment tax, and the deductible Keogh contribution itself.

97. (d) A single individual with AGI over $69,000 for 2013 would only be entitled to an IRA deduction if the taxpayer is not covered by a qualified employee pension plan.

98. (c) The requirement is to determine the allowable IRA deduction on the Cranes’ 2013 joint return. Since Sol is covered by his employer’s pension plan, Sol’s contribution of $5,500 is proportionately phased out as a deduction by AGI between $95,000 and $115,000. Since the Cranes’ AGI exceeded $115,000, no deduction is allowed for Sol’s contribution. Although Julia is not employed, $5,500 can be contributed to her IRA because the combined earned income on the Cranes’ return is at least $11,000. The maximum IRA deduction for an individual who is not covered by an employer plan, but whose spouse is, is proportionately phased out for AGI between $178,000 and $188,000 for 2013. Since Julia is not covered by an employer plan and the Cranes’ AGI is below $178,000, the $5,500 contribution to Julia’s IRA is fully deductible for 2013.

99. (d) The requirement is to determine the Lees’ maximum IRA contribution and deduction on a joint return for 2013. Since neither taxpayer is covered by an employer-sponsored pension plan, there is no phase-out of the maximum deduction due to the level of their adjusted gross income. For married taxpayers filing a joint return, up to $5,500 can be deducted for contributions to the IRA of each spouse (even if one spouse is not working), provided that the combined earned income of both spouses is at least equal to the amounts contributed to the IRAs. Additionally, an individual at least age 50 can make a special catch-up contribution of $1,000 for 2013, resulting in an increased maximum contribution and deduction of $6,500 for 2013. Thus, the Lees may contribute and deduct a maximum of $13,000 to their individual retirement accounts for 2013, with a maximum of $6,500 placed into each account.

100. (c) The maximum amount of contributions to a defined contribution self-employed retirement plan is limited to the lesser of $51,000, or 100% of self-employment income for 2013.

101. (d) The requirement is to determine which allowable deduction can be claimed in arriving at an individual’s adjusted gross income. One hundred percent of a self-employed individual’s health insurance premiums are deductible in arriving at an individual’s adjusted gross income for 2013. Charitable contributions, foreign income taxes (if not used as a credit), and tax return preparation fees can be deducted only from adjusted gross income if an individual itemizes deductions.

102. (b) The requirement is to determine the incorrect statement concerning the deduction for interest on qualified education loans. For 2013, an individual is allowed to deduct up to $2,500 for interest on qualified education loans in arriving at AGI. The deduction is subject to an income phase-out and the loan proceeds must have been used to pay for the qualified higher education expenses (e.g., tuition, fees, room, board) of the taxpayer, spouse, or a dependent (at the time the debt was incurred). The education expenses must relate to a period when the student was enrolled on at least a half-time basis. The sixty-month limitation was repealed for tax years beginning after 2002.

103. (c) The requirement is to determine how Dale should treat her $1,000 jury duty fee that she remitted to her employer. Fees received for serving on a jury must be included in gross income. If the recipient is required to remit the jury duty fees to an employer in exchange for regular compensation, the remitted jury duty fees are allowed as a deduction from gross income in arriving at adjusted gross income.

104. (b) The requirement is to determine George’s taxable income. George’s adjusted gross income consists of $3,700 of dividends and $1,700 of wages. Since George is eligible to be claimed as a dependency exemption by his parents, there will be no personal exemption on George’s return and his basic standard deduction is limited to the greater of $1,000, or George’s earned income of $1,700, plus $350. Thus, George’s taxable income would be computed as follows:

| Dividends | $ 3,700 |

| Wages | 1,700 |

| AGI | $ 5,400 |

| Exemption | 0 |

| Std. deduction | (2,050) |

| Taxable income | $3,350 |

105. (c) The item asks you to determine the requirements that must be met in order for a single individual to qualify for the additional standard deduction. A single individual who is age sixty-five or older or blind is eligible for an additional standard deduction ($1,500 for 2013). Two additional standard deductions are allowed for an individual who is age sixty-five or older and blind. It is not required that an individual support a dependent child or aged parent in order to qualify for an additional standard deduction.

106. (b) The requirement is to determine Carroll’s maximum medical expense deduction after the applicable threshold limitation 2013. An individual taxpayer’s unreimbursed medical expenses are deductible to the extent in excess of 10% of the taxpayer’s adjusted gross income. Although the cost of cosmetic surgery is generally not deductible, the cost is deductible if the cosmetic surgery or procedure is necessary to ameliorate a deformity related to a congenital abnormality or personal injury resulting from an accident, trauma, or disfiguring disease. Here, Carroll’s deduction is ($5,000 + $15,000) − ($100,000 × 10%) = $10,000.

107. (b) The requirement is to determine the Blairs’ itemized deduction for medical expenses for 2013. A taxpayer can deduct the amounts paid for the medical care of himself, spouse, or dependents. The Blairs’ qualifying medical expenses include the $800 of medical insurance premiums, $450 of prescribed medicines, $1,000 of unreimbursed doctor’s fees, and $150 of transportation related to medical care. These expenses, which total $3,150, are deductible to the extent they exceed 10% (for 2013) of adjusted gross income, and result in a deduction of $150. Note that nonprescription medicines, including aspirin and over-the-counter cold capsules, are not deductible. Additionally, the Blairs cannot deduct the emergency room fee they paid for their son because they did not provide more than half of his support and he therefore does not qualify as their dependent.

108. (a) The requirement is to determine the amount the Whites may deduct as qualifying medical expenses without regard to the adjusted gross income percentage threshold. The Whites’ deductible medical expenses include the $600 spent on repair and maintenance of the motorized wheelchair and the $8,000 spent for tuition, meals, and lodging at the special school for their physically handicapped dependent child. Payment for meals and lodging provided by an institution as a necessary part of medical care is deductible as a medical expense if the main reason for being in the institution is to receive medical care. Here, the item indicates that the Whites’ physically handicapped dependent child was in the institution primarily for the availability of medical care, and that meals and lodging were furnished as necessary incidents to that care.

109. (c) The requirement is to determine the amount Wells can deduct as qualifying medical expenses without regard to the adjusted gross income percentage threshold. Wells’ deductible medical expenses include the $500 premium on the prescription drug insurance policy and the $500 unreimbursed payment for physical therapy. The earnings protection policy is not considered medical insurance because payments are not based on the amount of medical expenses incurred. As a result, the $3,000 premium is a nondeductible personal expense.

110. (d) The requirement is to determine the amount of expenses incurred in connection with the adoption of a child that can be deducted by the Sloans on their 2013 joint return. A taxpayer can deduct the medical expenses paid for a child at the time of adoption if the child qualifies as the taxpayer’s dependent when the medical expenses are paid. Additionally, if a taxpayer pays an adoption agency for medical expenses the adoption agency already paid, the taxpayer is treated as having paid those expenses. Here, the Sloans can deduct the child’s medical expenses of $5,000 that they paid. On the other hand, the legal expenses of $9,000 and agency fee of $4,000 incurred in connection with the adoption are treated as nondeductible personal expenses. However, the Sloans will qualify to claim a nonrefundable tax credit of up to $12,970 (for 2013) for these qualified adoption expenses.

111. (a) The requirement is to determine the amount that can be claimed by the Clines in their 2013 return as qualifying medical expenses. No medical expense deduction is allowed for cosmetic surgery or similar procedures, unless the surgery or procedure is necessary to ameliorate a deformity related to a congenital abnormality or personal injury resulting from an accident, trauma, or disfiguring disease. Cosmetic surgery is defined as any procedure that is directed at improving a patient’s appearance and does not meaningfully promote the proper function of the body or prevent or treat illness or disease. Thus, Ruth’s face-lift and Mark’s hair transplant do not qualify as deductible medical expenses in 2013.

112. (d) The requirement is to determine the amount that Scott can claim as deductible medical expenses. The medical expenses incurred by a taxpayer for himself, spouse, or a dependent are deductible when paid or charged to a credit card. The $4,000 of medical expenses for his dependent son are deductible by Scott in 2013 when charged on Scott’s credit card. It does not matter that payment to the credit card issuer had not been made when Scott filed his return. Expenses paid for the medical care of a decedent by the decedent’s spouse are deductible as medical expenses in the year they are paid, whether the expenses are paid before or after the decedent’s death. Thus, the $2,800 of medical expenses for his deceased spouse are deductible by Scott when paid in 2013, even though his spouse died in 2012.

113. (d) The requirement is to determine which expenditure qualifies as a deductible medical expense. Premiums paid for Medicare B supplemental medical insurance qualify as a deductible expense. Diaper service, funeral expenses, and nursing care for a healthy baby are not deductible as medical expenses.

114. (b) The requirement is to determine Stenger’s net medical expense deduction for 2013. It would be computed as follows:

| Prescription drugs | $ 300 |

| Medical insurance premiums | 1,750 |

| Doctors ($2,550 − $900) | 1,650 |

| Eyeglasses | 75 |

| $3,775 | |

| Less 10% of AGI ($35,000) | 3,500 |

| Medical expense deduction for 2013 | $275 |

115. (d) The requirement is to determine the total amount of deductible medical expenses for the Bensons before the application of any limitation rules. Deductible medical expenses include those incurred by a taxpayer, taxpayer’s spouse, dependents of the taxpayer, or any person for whom the taxpayer could claim a dependency exemption except that the person had gross income of $3,900 or more, or filed a joint return. Thus, the Bensons may deduct medical expenses incurred for themselves, for John (i.e., no dependency exemption only because his gross income is $3,900 or more), and for Nancy (i.e., a dependent of the Bensons).

116. (d) The requirement is to determine the tax that is not deductible as an itemized deduction. One-half of a self-employed taxpayer’s self-employment tax is deductible from gross income in arriving at adjusted gross income. Foreign real estate taxes, foreign income taxes, and personal property taxes can be deducted as itemized deductions from adjusted gross income.

117. (c) The requirement is to determine the amount that Matthews can deduct as taxes on her 2013 Schedule A of Form 1040. An individual’s state and local income taxes are deductible as an itemized deduction, while federal income taxes are not deductible. For a cash-basis taxpayer, state and local taxes are deductible for the year in which paid or withheld. As a result, Matthew’s deduction for 2013 consists of her state and local taxes withheld of $1,500 and the December 30 estimated payment of $400. The state and local income taxes that Matthews paid in April 2014 will be deductible for 2014.

118. (a) The requirement is to determine the correct statement regarding Farb, a cash-basis individual taxpayer who paid an $8,000 invoice for personal property taxes under protest in 2012, and received a $5,000 refund of the taxes in 2013. If a taxpayer receives a refund or rebate of taxes deducted in an earlier year, the taxpayer must generally include the refund or rebate in income for the year in which received. Here, Farb should deduct $8,000 in his 2012 income tax return and should report the $5,000 refund as income in his 2013 income tax return.

119. (d) The requirement is to determine the amount of itemized deduction for realty taxes that can be deducted by Burg. Generally, an individual’s payment of state, local, or foreign real estate taxes is deductible as an itemized deduction if the individual is the owner of the property on which the taxes are imposed. Because the property is jointly owned by Burg, he is individually liable for the entire amount of realty taxes and may deduct the entire payment on his return. Even back taxes can be deducted by Burg as long as he was the owner of the property during the period of time to which the back taxes are related.

120. (b) The requirement is to determine Sara’s deduction for state income taxes in 2013. Sara’s deduction would consist of the $2,000 withheld by her employer in 2013, plus the three estimated payments (3 × $300 = $900) actually paid during 2013, a total of $2,900. Note that the 1/15/14 estimated payment would be deductible for 2014.

121. (b) The requirement is to determine the amount of taxes deductible as an itemized deduction. The $360 vehicle tax based on value is deductible as a personal property tax. The real property tax of $2,700 must be apportioned between the Bronsons and the buyer for tax purposes according to the number of days in the real property tax year that each owns the property even though they did not actually make an apportionment. Taxes are apportioned to the seller up to, but not including, the date of the sale, and apportioned to the buyer beginning with the date of sale. Since the house was sold June 30, the Bronson’s deduction for real estate taxes would be $2,700 × 180/365 = $1,332. The buyer would deduct the remaining $1,368.

122. (a) The requirement is to determine what portion of the $1,300 of realty taxes is deductible by King in 2013. The $600 of delinquent taxes charged to the seller and paid by King are not deductible, but are added to the cost of the property. The $700 of taxes for 2013 are apportioned between the seller and King according to the number of days that each held the property during the year. King’s deduction would be

123. (b) The requirement is to determine the amount of property taxes deductible as itemized deductions. The property taxes on the residence and the land held for appreciation, together with the personal property taxes on the auto are deductible. The special assessment is not deductible, but would be added to the basis of the residence.

124. (a) The requirement is to determine the amount the Burgs should deduct for taxes in their itemized deductions. The $1,200 of state income tax paid by the Burgs is deductible as an itemized deduction. However, the $7,650 of self-employment tax is not deductible as an itemized deduction. Instead, a portion of the self-employment tax is deductible from gross income in arriving at the Burgs’ adjusted gross income.

125. (c) The requirement is to determine the correct statement regarding an individual taxpayer’s deduction for interest on investment indebtedness. The deduction for interest expense on investment indebtedness is limited to the taxpayer’s net investment income. Net investment income includes such income as interest, dividends, and short-term capital gains, less any related expenses.

126. (b) The requirement is to determine the correct statement regarding the interest on the Browns’ $20,000 loan that was secured by their home and used to purchase an automobile. Qualified residence interest consists of interest on acquisition indebtedness and home equity indebtedness. Interest on home equity indebtedness loans of up to $100,000 is deductible as qualified residence interest if the loans are secured by a taxpayer’s principal or second residence regardless of how the loan proceeds are used. The amount of home equity indebtedness cannot exceed the fair market value of a home as reduced by any acquisition indebtedness. Since the Browns’ home had an FMV of $400,000 and was unencumbered by other debt, the interest on the $20,000 home equity loan is deductible as qualified residence interest.