Appendix C: 2013 Released AICPA Questions for Regulation

1. To which of the following transactions does the common law Statute of Frauds not apply?

a. Contracts for the sale of real estate.

b. Agreements made in consideration of marriage.

c. Promises to pay the debt of another.

d. Contracts that can be performed within one year.

1. (d) The question requires that you identify the type of contract that does not require a writing under the Statute of Frauds. Contracts that cannot be performed within one year need a writing, not contract that can be performed within one year. Answers (a), (b), and (c) are incorrect because each of those answers describe contracts that need a writing under the Statute of Frauds.

2. Gulde’s tax basis in Chyme Partnership was $26,000 at the time Gulde received a liquidating distribution of $12,000 cash and land with an adjusted basis to Chyme of $10,000 and a fair market value of $30,000. Chyme did not have unrealized receivables, appreciated inventory, or properties that had been contributed by its partners. What was the amount of Gulde’s basis in the land?

a. $0

b. $10,000

c. $14,000

d. $30,000

2. (c) The requirement is to determine Guide’s basis for the land that was received in a liquidating distribution from a partnership. Generally, no gain or loss is recognized on a liquidating distribution made to a partner. If both cash and land are received in the liquidating distribution, the basis for the partner’s partnership interest is first reduced by the $12,000 of cash, before being reduced by the land. Since this is a liquidating distribution that completely terminates the partner’s interest, the land must absorb the partner’s remaining partnership basis after first being reduced by the cash. Here, Guide’s basis for the land is $26,000 − $12,000 cash = $14,000.

3. Under the Sales Article of the UCC, which of the following circumstances best describes how the implied warranty of fitness for a particular purpose arises in a sale of goods transaction?

a. The buyer is purchasing the goods for a particular purpose and is relying on the seller’s skill or judgment to select suitable goods.

b. The buyer is purchasing the goods for a particular purpose and the seller is a merchant in such goods.

c. The seller knows the particular purpose for which the buyer will use the goods and knows the buyer is relying on the seller’s skill or judgment to select suitable goods.

d. The seller knows the particular purpose for which the buyer will use the goods and the seller is a merchant in such goods.

3. (c) Under the UCC, the warranty of fitness for a particular purpose arises when the seller has reason to know that the buyer is purchasing goods for a particular purpose and relying on the seller’s expertise to choose the appropriate goods. Answer (a) is incorrect because no information is provided that the seller knows of the buyer’s reliance upon the seller’s expertise. Answer (b) is incorrect for the same reason as answer (a) and that there is no requirement that the seller be a merchant. Answer (d) is incorrect because the seller does not need to be a merchant for the warranty of fitness for a particular purpose to arise.

4. Randolph is a single individual who always claims the standard deduction. Randolph received the following in the current year:

| Wages | $22,000 |

| Unemployment compensation | 6,000 |

| Pension distribution (100% taxable) | 4,000 |

| A state tax refund from the previous year | 425 |

What is Randolph’s gross income?

a. $22,000

b. $28,425

c. $32,000

d. $32,425

4. (c) The requirement is to determine Randolph’s gross income for the current year. Randolph’s gross income totals $32,000 and consists of the $22,000 of wages, $6,000 of unemployment compensation, and $4,000 of pension distribution. Because Randolph always claims the standard deduction and did not deduct state taxes, the state tax refund is excluded from gross income.

5. Which of the following conditions must be met to form an agency?

a. An agency agreement must be in writing.

b. An agency agreement must be signed by both parties.

c. The principal must furnish legally adequate consideration for the agent’s services.

d. The principal must possess contractual capacity.

5. (d) An agency relationship does require that the principal have contractual capacity to enter into the agency relationship. (Minors may enter into an agency relationship as an agent, but retain their power to disaffirm the agency relationship.) Answer (a) is incorrect: Unless the Statute of Frauds would require the agreement to be in writing, agency relationships may be orally agreed to. Answer (b) is incorrect: As discussed in answer (a), the agreement does not need to be in writing, and thus would not need to be signed. Even if the Statute of Frauds required the agency agreement to be in writing, then the only necessary signature is the signature of the party to be charged, not both parties. Answer (c) is incorrect because unlike a typical contract an agency can be gratuitous (without consideration) and still be a valid agency agreement.

6. Johnson worked for ABC Co. and earned a salary of $100,000. Johnson also received, as a fringe benefit, group term-life insurance at twice Johnson’s salary. The annual IRS-established uniform cost of insurance is $2.76 per $1,000. What amount must Johnson include in gross income?

a. $100,000

b. $100,276

c. $100,414

d. $100,552

6. (c) The requirement is to determine the amount that Johnson must include in gross income. Only the cost of the first $50,000 of group-term life insurance coverage can be excluded from an employee’s gross income. Since Johnson was provided with $200,000 of group-term insurance, his gross income would include $2.76 × 150 = $414, resulting in total gross income of $100,414.

7. In return for a 20% partnership interest, Skinner contributed $5,000 cash and land with a $12,000 basis and a $20,000 fair market value to the partnership. The land was subject to a $10,000 mortgage that the partnership assumed. In addition, the partnership had $20,000 in recourse liabilities that would be shared by partners according to their partnership interests. What amount represents Skinner’s basis in the partnership interest?

a. $27,000

b. $21,000

c. $19,000

d. $13,000

7. (d) The requirement is to determine Skinner’s basis for the 20% partnership interest. Generally no gain or loss is recognized on the contribution of property in exchange for a partnership interest. Skinner’s basis would consist of the $5,000 cash plus the $12,000 basis for the land, reduced by the 80% × $10,000 = $8,000 net decrease in Skinner’s liability that results from having transferred the mortgage to the partnership, and increased by Skinner’s 20% × $20,000 = $4,000 share of partnership recourse liabilities. As a result, Skinner’s initial basis for the partnership interest is $5,000 + $12,000 − $8,000 + $4,000 = $13,000.

8. Azure, a C corporation, reports the following:

What is Azure’s taxable income?

a. $528,000

b. $543,000

c. $544,000

d. $559,000

8. (c) The requirement is to determine Azure Corporation’s taxable income given book income of $543,000. Azure’s book income would be reduced by the $20,000 of additional tax depreciation and $25,000 of nontaxable bond interest, and would increase by the $36,000 of rental income and the nondeductible $10,000 of pollution fines. $543,000 − $20,000 − $25,000 + $36,000 + $10,000 = $544,000.

9. Which of the following cannot be amortized for tax purposes?

a. Incorporation costs.

b. Temporary directors’ fees.

c. Stock issuance costs.

d. Organizational meeting costs.

9. (c) The requirement is to determine the cost that cannot be amortized for tax purposes. The costs incurred in issuing and selling stock (e.g., professional fees to issue stock, printing costs, underwriting commissions) do not qualify as organization expenditures and are not tax deductible. On the other hand, incorporation costs, temporary directors’ fees, and organizational meeting costs are amortizable organizational expenditures.

10. PDK, LLC had three members with equal ownership percentages. PDK elected to be treated as a partnership. For the tax year ending December 31, year 1, PDK had the following income and expense items:

| Revenues | $120,000 |

| Interest income | 6,000 |

| Gain on sale of securities | 8,000 |

| Salaries | 36,000 |

| Guaranteed payments | 10,000 |

| Rent expense | 21,000 |

| Depreciation expense | 18,000 |

| Charitable contributions | 3,000 |

What would PDK report as nonseparately stated income for year 1 tax purposes?

a. $30,000

b. $35,000

c. $43,000

d. $51,000

10. (b) The requirement is to determine PDK’s nonseparately stated income (ordinary income) for the year. PDK’s nonseparately stated income would consist of its revenues of $120,000 reduced by salaries of $36,000, guaranteed payments of $10,000, rent expense of $21,000, and depreciation expense of $18,000, resulting in net nonseparately stated income of $35,000. The interest income, gain on sale of securities, and charitable contributions have special tax characteristics and must be separately passed through in order to retain those special characteristics when taxed to the owners of the LLC.

11. For an individual business owner, which of the following would typically be classified as a capital asset for federal income tax purposes?

a. Accounts receivable.

b. Marketable securities.

c. Machinery and equipment used in a business.

d. Inventory.

11. (b) The requirement is to determine the item that would be considered a capital asset. The definition of capital assets includes property held for investment and would include marketable securities. In contrast, the definition specifically excludes accounts receivable, property used in a trade or business, and inventory.

12. A CPA prepares a client’s tax return containing business travel expenses without inquiring about the existence of documentation for the expenses. Which statement best describes the consequence of the CPA’s lack of inquiry?

a. The CPA may be assessed a tax return preparer penalty.

b. The CPA may be charged with preparing a fraudulent return.

c. The client will not owe an understatement penalty if the return is audited and the expenses disallowed.

d. The client will not be subject to a fraud penalty.

12. (a) The requirement is to determine the statement that best describes the consequences if a CPA prepares a client’s return containing business travel expenses without inquiring about the existence of documentation for the expense. Generally, a preparer is not required to examine or verify supporting data, but may rely on information furnished by the taxpayer unless it appears to be incorrect, incomplete, or inconsistent. However, there is a need to determine by inquiry that a specifically required condition, such as the client maintaining books and records substantiating business travel expenses, has been satisfied. Here, the CPA failed to make that inquiry and may be assessed a preparer penalty.

13. What is the due date of a federal estate tax return (Form 706), for a taxpayer who died on May 15, year 2, assuming that a request for an extension of time is not filed?

a. September 15, year 2.

b. December 31, year 2.

c. January 31, year 3.

d. February 15, year 3.

13. (d) The requirement is to determine the due date for a federal estate tax return for a taxpayer who died May 15 of year 2. The federal estate tax return (Form 706) must be filed within nine months of the decedent’s date of death, unless an extension of time has been granted. Here the return is due February 15, year 3.

14. Under Treasury Circular 230, in which of the following situations is a CPA prohibited from giving written advice concerning one or more federal tax issues?

a. The CPA takes into account the possibility that a tax return will not be audited.

b. The CPA reasonably relies upon representations of the client.

c. The CPA considers all relevant facts that are known.

d. The CPA takes into consideration assumptions about future events related to the relevant facts.

14. (a) The requirement is to determine the situation in which a CPA would be prohibited from giving written advice concerning one or more federal tax issues. A CPA must not give written advice concerning one or more federal tax issues if the CPA bases the written advice on unreasonable factual or legal assumptions (including assumptions as to future events), unreasonably relies upon representations, statements, findings or agreements of the taxpayer or any other person, does not consider all relevant facts that the practitioner knows or should know, or, in evaluating a federal tax issue, takes into account the possibility that a tax return will not be audited.

15. A CPA prepares income tax returns for a client. After the client signs and mails the returns, the CPA discovers an error. According to Treasury Circular 230, the CPA must

a. Document the error in the workpapers.

b. Prepare an amended return within 30 days of the discovery of the error.

c. Promptly advise the client of the error.

d. Promptly resign from the engagement and cooperate with the successor accountant.

15. (c) The requirement is to determine what a CPA should do upon discovering an error in a client’s previously filed income tax return. The CPA should promptly advise the client of the error and its consequences and recommend the appropriate action to be taken. In the event that the client does not correct the error, the CPA should consider whether to continue a professional relationship with the client.

16. A corporate taxpayer plans to switch from the FIFO method to the LIFO method of valuing inventory. Which of the following statements is accurate regarding the use of the LIFO method?

a. In periods of rising prices, the LIFO method results in a lower cost of sales and higher taxable income, when compared to the FIFO method.

b. The taxpayer is required to receive permission each year from the Internal Revenue Service to continue the use of the LIFO method.

c. The LIFO method can be used for tax purposes even if the FIFO method is used for financial statement purposes.

d. Under the LIFO method, the inventory on hand at the end of the year is treated as being composed of the earliest acquired goods.

16. (d) The requirement is to determine the correct statement regarding the use of the LIFO method. Under the LIFO (last-in, first-out) inventory method, the inventory on hand at the end of the year is treated as being composed of the earliest acquired goods. The most recently acquired goods are considered sold, resulting in a higher cost of sales and a lower taxable income during a period of rising prices. A taxpayer need not obtain advance permission to adopt the LIFO method. However, if LIFO is used for tax purposes, it generally must be used for financial reporting purposes.

17. Which of the following statements regarding an individual’s suspended passive activity losses is correct?

a. $3,000 of suspended losses can be utilized each year against portfolio income.

b. Suspended losses can be carried forward, but not back, until utilized.

c. Suspended losses must be carried back three years and forward seven years.

d. A maximum of 50% of the suspended losses can be used each year when an election is made to forgo the carryback period.

17. (b) The requirement is to determine the correct statement regarding an individual’s suspended passive activity losses. Generally, passive activity losses can only be used to offset passive activity income. Suspended passive activity losses cannot be carried back, but can be carried forward indefinitely to future years to offset passive activity income, and may be deducted when a taxpayer’s entire interest in the activity that gave rise to the unused losses is disposed of in a fully taxable transaction.

18. Simmons gives her child a gift of publicly traded stock with a basis of $40,000 and a fair market value of $30,000. No gift tax is paid. The child subsequently sells the stock for $36,000. What is the child’s recognized gain or loss, if any?

a. $4,000 loss.

b. No gain or loss.

c. $6,000 gain.

d. $36,000 gain.

18. (b) The requirement is to determine the child’s recognized gain or loss from the sale of stock received as a gift. The child’s basis for computing a gain would be the donor’s transferred basis of $40,000, while the child’s basis for computing a loss would be the stock’s $30,000 FMV on date of gift. Since the stock was sold for $36,000, the sale results in neither gain nor loss.

19. Under the Negotiable Instruments Article of the UCC, what kind of endorsement is made by the use of the words “Lee Louis”?

a. Blank, nonrestrictive, and unqualified.

b. Blank, nonrestrictive, and qualified.

c. Special, nonrestrictive, and unqualified.

d. Special, nonrestrictive, and qualified.

19. (a) An endorsement that is just a signature alone is a blank endorsement. An endorser that disclaims secondary contract liability, usually by signing “without recourse,” creates a qualified endorsement. There was no such disclaimer here, so the endorsement is unqualified. Answer (b) is incorrect: Although the endorsement is blank and nonrestrictive, it is not qualified because it fails to disclaim secondary contract liability. Answers (c) and (d) are incorrect because a special endorsement states to whom the instrument is further payable and no such statement is present here. Additionally, answer (d) is incorrect because the endorsement is unqualified.

20. An individual entered into several exchanges during the current tax year. Which of the following exchanges is classified as like-kind?

a. Partnership interest for partnership interest.

b. Common stock for common stock.

c. Apartment building for unimproved land.

d. Manufacturing equipment for factory building.

20. (c) The requirement is to determine the exchange that would qualify as a like-kind exchange. The exchange of business or investment property for like-kind business or investment property is treated as a nontaxable exchange. Like-kind means “the same class of property;” the exchange of an apartment building for unimproved land would qualify as a like-kind exchange. The like-kind exchange provision does not apply to an exchange of stock nor to an exchange of partnership interests. An exchange of manufacturing equipment for a factory building would not be a like-kind exchange because it is an exchange of personal property for real estate.

21. When the AQR partnership was formed, partner Acre contributed land with a fair market value of $100,000 and a tax basis of $60,000 in exchange for a one-third interest in the partnership. The AQR partnership agreement specifies that each partner will share equally in the partnership’s profits and losses. During its first year of operation, AQR sold the land to an unrelated third party for $160,000. What is the proper tax treatment of the sale?

a. Each partner reports a capital gain of $33,333.

b. The entire gain of $100,000 must be specifically allocated to Acre.

c. The first $40,000 of gain is allocated to Acre, and the remaining gain of $60,000 is shared equally by the other two partners.

d. The first $40,000 of gain is allocated to Acre, and the remaining gain of $60,000 is shared equally by all the partners in the partnership.

21. (d) The requirement is to determine the proper tax treatment for the partnership’s gain on sale of land that had a basis of $60,000 and an FMV of $100,000 when contributed by Acre. Since the partnership sold the land for a $160,000 − $60,000 = $100,000 gain, the $40,000 of built-in gain at time of contribution must be allocated solely to Acre. The remaining $100,000 − $40,000 of built-in gain = $60,000 would be shared equally by all the partners.

22. Summer, a single individual, had a net operating loss of $20,000 three years ago. A Code Sec. 1244 stock loss made up three-fourths of that loss. Summer had no taxable income from that year until the current year. In the current year, Summer has gross income of $80,000 and sustains another loss of $50,000 on Code Sec. 1244 stock. Assuming that Summer can carry the entire $20,000 net operating loss to the current year, what is the amount and character of the Code Sec. 1244 loss that Summer can deduct for the current year?

a. $35,000 ordinary loss.

b. $35,000 capital loss.

c. $50,000 ordinary loss.

d. $50,000 capital loss.

22. (c) The requirement is to determine the amount and character of the Sec. 1244 loss that Summer can deduct for the current year. Sec. 1244 permits a shareholder to deduct an ordinary loss of up to $50,000 ($100,000 if married filing jointly) if qualifying stock is sold, exchanged, or becomes worthless. The $50,000 ($100,000) limit is an annual limitation.

23. Which of the following types of conduct renders a contract void?

a. Mutual mistake as to facts forming the basis of the contract.

b. Undue influence by a dominant party in a confidential relationship.

c. Duress through physical compulsion.

d. Duress through improper threats.

23. (c) An agreement that contains the necessary elements to form a contract may still be void or voidable, if a formation defense exists. Duress is a formation defense where one party forces another party to enter into the agreement. When that force involves physical coercion, then the agreement is void. Answer (d) is incorrect, although duress is present here as well. When duress involves only threats, as opposed to physical coercion, then the contract is only voidable, not void. Answer (a) is incorrect because mutual mistake creates a voidable contract, not a void contract. Answer (b) is incorrect because undue influence creates a voidable contract, not a void contract.

24. On day 1, Jackson, a merchant, mailed Sands a signed letter that contained an offer to sell Sands 500 electric fans at $10 per fan. The letter was received by Sands on day 3. The letter contained a promise not to revoke the offer but no expiration date. On day 4, Jackson mailed Sands a revocation of the offer to sell the fans. Sands received the revocation on day 6. On day 7, Sands mailed Jackson an acceptance of the offer. Jackson received the acceptance on day 9. Under the Sales Article of the UCC, was a contract formed?

a. No contract was formed because the offer failed to state an expiration date.

b. No contract was formed because Sands received the revocation of the offer before Sands accepted the offer.

c. A contract was formed on the day Jackson received Sands’ acceptance.

d. A contract was formed on the day Sands mailed the acceptance to Jackson.

24. (d) This contract involves goods (fans) which means Article 2 of the UCC applies to this transaction. Under the UCC an offer made in writing by a merchant is called a firm offer. Firm offers are irrevocable even if the offeree did not provide consideration to hold the offer open. Where, as in this problem, no period is stated for which the offer will remain open, then the offer remains open for a reasonable period of time that cannot exceed three months. Here, the offeree, Sands, accepted only four days after receiving the offer which would be a reasonable amount of time. Answer (a) is incorrect because even if a firm offer fails to state an expiration date, then the firm offer will stay open for a reasonable time; it will not prevent formation of a contract. Answer (b) is incorrect because firm offers are irrevocable for a reasonable time when the offer fails to state an expiration date. Answer (c) is incorrect because acceptances are valid when sent, not received.

25. The sole shareholder of an S corporation contributed equipment with a fair market value of $20,000 and a basis of $6,000 subject to $12,000 liability. What amount is the gain, if any, that the shareholder must recognize?

a. $0

b. $ 6,000

c. $ 8,000

d. $12,000

25. (b) The requirement is to determine the amount of gain recognized by a sole shareholder on the transfer of property to an S corporation. Since Sec. 351 would apply to the sole shareholder’s transfer of property, the shareholder’s gain would be recognized only to the extent that the liability relief of $12,000 exceeded the shareholder’s $6,000 basis for the transferred property, which results in a recognized gain of $6,000.

26. In year 6, an IRS agent completed an examination of a corporation’s year 5 tax return and proposed an adjustment that will result in an increase in taxable income for each of years 1 through year 5. All returns were filed on the original due date. The proposed adjustment relates to the disallowance of corporate jet usage for personal reasons. The agent does not find the error to be fraudulent or substantial in nature. Which of the following statements regarding this adjustment is correct?

a. The adjustment is improper because an agent may only propose adjustments to the year under examination.

b. The adjustment is proper because there is no statute of limitations for improperly claiming personal expenses as business expenses.

c. The adjustment is proper because it relates to a change in accounting method, which can be made retroactively irrespective of the statute of limitations.

d. The adjustment is improper because the statute of limitations has expired for several years of the adjustment.

26. (d) The requirement is to determine the correct statement regarding an IRS agent’s proposed adjustment in year 6 to the tax returns of years 1 through 5. Since the agent did not find the error to be fraudulent nor substantial in nature, the normal three-year statute of limitations would apply to years 1 through 5. That means that the time period for additional assessments of tax for the year 1 tax return would have expired during year 5, and an additional assessment for year 2 would have expired during year 6. As a result, the proposed adjustment is improper.

27. Carson owned 40% of the outstanding stock of a C corporation. During a tax year, the corporation reported $400,000 in taxable income and distributed a total of $70,000 in cash dividends to its shareholders. Carson accurately reported $28,000 in gross income on Carson’s individual tax return. If the corporation had been an S corporation and the distributions to the owners had been proportionate, how much income would Carson have reported on Carson’s individual return?

a. $ 28,000

b. $132,000

c. $160,000

d. $188,000

27. (c) The requirement is to determine how much income Carson would have reported if the corporation had been an S corporation. The income of an S corporation passes through and is taxed to shareholders at the end of an S Corporation’s tax year, increasing a shareholder’s stock basis. In contrast, S corporation distributions are generally nontaxable and are treated as a return of stock basis. Here, Carson would have been taxed on $400,000 × 40% = $160,000 of income and Carson’s distribution of $28,000 would be treated as a nontaxable return of stock basis.

28. Which of the following may not be deducted in the computation of alternative minimum taxable income of an individual?

a. Traditional IRA account contribution.

b. One-half of the self-employment tax deduction.

c. Personal exemptions.

d. Charitable contributions.

28. (c) The requirement is to determine the item that cannot be deducted in the computation of alternative minimum taxable income (AMTI) for an individual. An individual’s personal exemptions which are subtracted in computing regular taxable income are not deductible when computing an individual’s AMTI.

29. The sale of which of the following types of business property should be reported as Section 1231 (Property Used in the Trade or Business and Involuntary Conversions) property?

a. Inventory held for resale.

b. Machinery held for 6 months.

c. Cattle held for 6 months.

d. Land held for 18 months.

29. (d) The requirement is to determine which sale should be treated as a sale of Sec. 1231 property. Sec. 1231 property generally includes both depreciable and non depreciable property used in a trade or business or held for the production of income if held for more than twelve months. The land held 18 months for business use would be Sec. 1231 property, but the inventory held for resale, machinery held for six months, and cattle held for six months would not qualify as Sec. 1231 property.

30. Smith has an adjusted gross income (AGI) of $120,000 without taking into consideration $40,000 of losses from rental real estate activities. Smith actively participates in the rental real estate activities. What amount of the rental losses may Smith deduct in determining taxable income?

a. $0

b. $15,000

c. $20,000

d. $40,000

30. (b) The requirement is to determine the amount of the $40,000 rental real estate loss that Smith may deduct in determining taxable income. Although a rental activity is a passive activity, a special rule permits up to $25,000 of rental real estate loss to offset income that is not from passive activities if the individual actively participates in the rental activity. However, the maximum $25,000 allowance is reduced by 50% of the individual’s AGI in excess of $100,000. Here, the current year’s deductibility of the $40,000 rental real estate loss would be limited to $25,000 − (50%)($120,000 − $100,000) = $15,000.

31. Pat created a trust, transferred property to this trust, and retained certain interests. For income tax purposes, Pat was treated as the owner of the trust. Pat has created which of the following types of trusts?

a. Simple.

b. Grantor.

c. Complex.

d. Pre-need funeral.

31. (b) The requirement is to determine the type of trust created by Pat who is considered to be the owner of the trust for income tax purposes. Grantor trusts are trusts over which the grantor (or grantor’s spouse) retains substantial control. As a result, the grantor is treated as the owner of the trust property and the income of the trust is taxed to the grantor, not to the trust or beneficiaries.

32. Individual Lark’s year 2 brokerage account statement listed the following capital gains and losses from the sale of stock investments:

| Short-term capital gain | $6,000 |

| Long-term capital gain | 14,000 |

| Short-term capital loss | 4,000 |

| Long-term capital loss | 8,000 |

In addition, two stock investments became worthless in year 2. Public Company X stock was purchased in December, year 1, for $5,000, and formal notification was received by Lark on July, year 2, that it was worthless. Private company Section 1244 stock was issued to Lark for $10,000 in January, year 1, and was determined to be worthless in December, year 2. What is Lark’s year 2 net capital gain or loss before any capital loss limitation?

a. $2,000 net capital loss.

b. $3,000 net capital gain.

c. $7,000 net capital loss.

d. $8,000 net capital gain.

32. (b) The requirement is to determine Lark’s year 2 net capital gain or loss. The Company X stock that becomes worthless during year 2 is treated as a loss occurring on the last day of year 2 resulting in a LTCL of $5,000. In contrast, the worthless Sec. 1244 stock results in a $10,000 ordinary loss, not a capital loss. Here, Lark has capital gains totaling $20,000 and capital losses totaling $17,000, which results in a net capital gain of $3,000.

33. The selection of an accounting method for tax purposes by a newly incorporated C corporation.

a. Is made on the initial tax return by using the chosen method.

b. Is made by filing a request for a private letter ruling from the IRS.

c. Must first be approved by the company’s board of directors.

d. Must be disclosed in the company’s organizing documents.

33. (a) The requirement is to determine the correct statement regarding the selection of an accounting method by a newly incorporated C corporation. A newly formed C corporation adopts an accounting method by using that method on its initial tax return. The adopted method does not have to be disclosed in organizing documents nor approved by directors. Furthermore, advance permission from the IRS is unnecessary.

34. A review of Bearing’s year 2 records disclosed the following tax information:

| Wages | $18,000 |

| Taxable interest and qualifying dividends | 4,000 |

| Schedule C trucking business net income | 32,000 |

| Rental (loss) from residential property | (35,000) |

| Limited partnership (loss) | (5,000) |

Bearing actively participated in the rental property and was a limited partner in the partnership. Bearing had sufficient amounts at risk for the rental property and the partnership. What is Bearing’s year 2 adjusted gross income?

a. $14,000

b. $19,000

c. $29,000

d. $54,000

34. (c) The requirement is to determine Bearing’s year 2 adjusted gross income. Both the $5,000 limited partnership loss as well as the $35,000 residential rental loss are passive losses which can generally be used to offset only passive activity income. However, a special rule permits up to $25,000 of rental real estate loss to offset income that is not from passive activities if the individual actively participated in the rental real estate activity and the individual’s AGI does not exceed $100,000. Here, Bearing’s AGI consist of the wages of $18,000, interest and qualifying dividends of $4,000, and Schedule C net income of $32,000, reduced by a rental real estate loss of $25,000, resulting in an AGI of $29,000.

35. Joe is the trustee of a trust set up for his father. Under the Internal Revenue Code, when Joe prepares the annual trust tax return, Form 1041, he

a. Must obtain the written permission of the beneficiary prior to signing as a tax return preparer.

b. Is not considered a tax return preparer.

c. May not sign the return unless he receives additional compensation for the tax return.

d. Is considered a tax return preparer because his father is the grantor of the trust.

35. (b) The requirement is to determine the correct statement with regard to Joe who prepares Form 1041 (US Fiduciary Income Tax Return) in his capacity as trustee of a trust. The term tax return preparer includes any person who prepares for compensation any federal tax return including income, employment, excise, exempt organization, gift, and estate tax returns. However, a trustee is a fiduciary and a person will not be considered a tax return preparer merely because such person prepares as a fiduciary a return or claim for refund.

36. A CPA prepared a tax return that involved a tax shelter transaction that was disclosed on the return. In which of the following situations would a tax return preparer penalty not be applicable?

a. There was substantial authority for the position.

b. It is reasonable to believe that the position would more likely that not be upheld.

c. There was a reasonable possibility of success for the position.

d. There was a reasonable basis for the position.

36. (b) The requirement is to determine the situation in which a tax return preparer would not be subject to penalty if the tax return involved a disclosed tax shelter transaction. The preparer would not be subject to penalty for a return that involves a disclosed tax shelter transaction if it is reasonable to believe that the position would more likely than not be upheld. This requires a more than 50% probability of the position being sustained on its merits. The lesser standards of reasonable basis (20% probability) and substantial authority (40% probability) are not applicable to tax shelter transactions.

37. What is the tax treatment of net losses in excess of the at-risk amount for an activity?

a. Any loss in excess of the at-risk amount is suspended and is deductible in the year in which the activity is disposed of in full.

b. Any losses in excess of the at-risk amount are suspended and carried forward without expiration and are deductible against income in future years from that activity.

c. Any losses in excess of the at-risk amount are deducted currently against income from other activities; the remaining loss, if any, is carried forward without expiration.

d. Any losses in excess of the at-risk amount are carried back two years against activities with income and then carried forward for 20 years.

37. (b) The requirement is to determine the tax treatment of net losses in excess of the at-risk amount for an activity. Losses from an activity are deductible to the extent that a taxpayer’s investment is at-risk. Any losses in excess of the at-risk basis amount are suspended and carried forward indefinitely, and can be deducted against income in future years from that activity. Losses suspended under the at-risk rules cannot be carried back to prior years.

38. What type of conduct generally will make a contract voidable?

a. Fraud in the execution.

b. Fraud in the inducement.

c. Physical coercion.

d. Contracting with a person under guardianship.

38. (b) A contract can be voidable if one of the parties to the contract commits fraud in the inducement. Answer (a) is incorrect because fraud in the execution creates a void contract, not a voidable contract. Answer (c) is incorrect because physical coercion creates a void contract. Answer (d) is incorrect because contracts made with a person under guardianship is a person who legally lacks capacity and such contracts are void.

39. A trust has distributable net income of $14,000 and distributes $20,000 to the sole beneficiary. What amounts are taxable to the trust and to the beneficiary?

| Trust | Beneficiary | |

| a. | $14,000 | $0 |

| b. | $0 | $14,000 |

| c. | $14,000 | $20,000 |

| d. | $0 | $20,000 |

39. (b) The requirement is to determine the amount taxable to the trust and to the beneficiary if a trust has distributable net income (DNI) of $14,000 and distributes $20,000 to its sole beneficiary. A trust acts as a conduit and receives a distribution deduction if it distributes its income to a beneficiary, who then is taxed on the income. The maximum deduction that a trust can receive for distributions is limited to its DNI, which also represents the maximum amount that can be taxed to the beneficiary. Here, the trust is not taxed because the $20,000 distribution results in a distribution deduction of $14,000. The beneficiary is then taxed on the distribution to the extent of $14,000.

40. An individual paid taxes 27 months ago, but did not file a tax return for that year. Now the individual wants to file a claim for refund of federal income taxes that were paid at that time. The individual must file the claim for refund within which of the following time periods after those taxes were paid?

a. One year.

b. Two years.

c. Three years.

d. Four years.

40. (b) The requirement is to determine the period of time during which an individual can file a claim for a refund of taxes paid if no tax return was filed. If no tax return was filed, the claim for refund must be filed within two years from the date the taxes were paid.

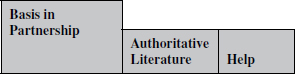

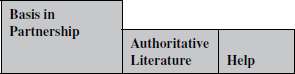

Task-Based Simulation 1

Scroll down to complete all parts of this task.

During years 1 and 2, Smith and Parker were equal partners in the ABC Partnership, a computer technology business involving website design and computer hardware repair. At start-up of the ABC Partnership on January 1, year 1, Smith and Parker each contributed $50,000 in cash.

ABC Partnership reports the following items during year 1.

Item |

Year 1 | |

| Ordinary income from trade or business activities as reported on Schedule K of the partnership return for allocation to the partners. | 46,000 | |

| Interest income | 1,400 | |

| Life insurance premiums paid on lives of partners (partnership is beneficiary) | 800 | |

| Penalties paid for late payment of payroll taxes | 200 | |

| Guaranteed payment to Parker | 10,000 | |

| Purchase of land for investment | 6,000 | |

| Cash distributions to Smith | 2,000 |

Use the table below to determine Smith’s tax basis in the partnership interest at the end of year 1. Not all entries may be needed for the determination. For any item not needed, enter a zero (0). Decreases in tax basis should be shown as negative values.

A |

B |

|

1 |

Item |

Year 1 |

2 |

Smith’s beginning tax basis | |

3 |

Ordinary income from trade or business activities | |

4 |

Interest income | |

5 |

Life insurance premiums paid on lives of partners (partnership is beneficiary) | |

6 |

Penalties paid for late payment of payroll taxes | |

7 |

Guaranteed payment to Parker | |

8 |

Additional capital contributions | |

9 |

Distributions | |

10 |

Purchase of land for investment | |

11 |

Smith’s tax basis at end of year |

Solution to Task-Based Simulation 1

A |

B |

|

1 |

Item |

Year 1 |

2 |

Smith’s beginning tax basis | 50,000 |

3 |

Ordinary income from trade or business activities | 23,000 |

4 |

Interest income | 700 |

5 |

Life insurance premiums paid on lives of partners (partnership is beneficiary) | (400) |

6 |

Penalties paid for late payment of payroll taxes | (100) |

7 |

Guaranteed payment to Parker | 0 |

8 |

Additional capital contributions | 15,000 |

9 |

Distributions | (2,000) |

10 |

Purchase of land for investment | 0 |

11 |

Smith’s tax basis at end of year | 86,200 |

A partner’s basis for a partnership interest is increased by the pass-through of all income items (including tax-exempt income), and reduced by the pass-through of all loss and deduction items (including nondeductible items). Additionally, a partner’s basis is increased by additional capital contributions and decreased by distributions.

Required: The requirement is to determine the basis for Smith’s 50% partnership interest at the end of year 1.

Smith’s beginning basis is increased by Smith’s 50% share of the ordinary income and interest income, and is decreased by 50% of the nondeductible life insurance premiums and nondeductible penalties. Also, Smith’s basis is increased by the additional capital contribution, and is decreased by the amount of distribution made to Smith.

Note that the purchase of land has no effect on Smith’s basis, and that the partnership’s guaranteed payment to Parker would already be deducted in the partnership’s computation of ordinary income and is not separately taken into account in determining Smith’s basis for the partnership interest.

Task-Based Simulation 2

Scroll down to complete all parts of this task.

The Internal Revenue Service (IRS) is auditing Form 1040, U.S. Individual Income Tax Return, for the following individual clients for year 2 and the audits are focused on medical expenses claimed. Calculate the allowable year 2 medical expense deduction for each taxpayer, if any, before the adjusted gross income (AGI) limitation. Assume that there are no insurance reimbursements of medical expenses, unless otherwise noted.

For each of the taxpayers, enter the correct amount in the associated shaded cell in the “Allowable deduction” column. Enter a zero (0), if the taxpayer is not entitled to a year 2 medical expense deduction. Enter all amounts as positive values.

B |

C |

|

1 |

Taxpayers |

Allowable deduction |

2 |

Taxpayer A Medical costs reported in year 2 include the following:

|

|

3 |

Taxpayer B Medical costs reported in year 2 include the following:

|

|

4 |

Taxpayer C Medical costs reported in year 2 include the following:

|

|

5 |

Taxpayer D Medical costs reported in year 2 include the following:

|

|

6 |

Taxpayer E Medical costs reported in year 2 include the following:

|

|

7 |

Taxpayer F Medical costs reported in year 2 include the following:

|

Solution to Task-Based Simulation 2

B |

C |

|

1 |

Taxpayers |

Allowable deduction |

2 |

Taxpayer A Medical costs reported in year 2 include the following:

|

$3,900 |

3 |

Taxpayer B Medical costs reported in year 2 include the following:

|

$4,500 |

4 |

Taxpayer C Medical costs reported in year 2 include the following:

|

$12,700 |

5 |

Taxpayer D Medical costs reported in year 2 include the following:

|

$4,650 |

6 |

Taxpayer E Medical costs reported in year 2 include the following:

|

$4,950 |

7 |

Taxpayer F Medical costs reported in year 2 include the following:

|

$12,850 |

Medical expenses that qualify for deduction include amounts paid for the diagnosis, cure, mitigation, treatment, or prevention of disease, or for the purpose of affecting any structure or function of the body. Deductible medical expenses include transportation and lodging, qualified long-term care services, prescription drugs, and medical insurance. Expenses for elective cosmetic surgery are not deductible unless the surgery or procedure is necessary to ameliorate a deformity arising from, or is directly related to, a congenital abnormality, a personal injury resulting from an accident or trauma, or a disfiguring disease.

The medical expense deduction is limited to unreimbursed medical expenses. A reimbursement received for expenses incurred in a previous tax year will generally be included in gross income for the year in which the reimbursement is received, to the extent that the medical expenses were previously deducted and provided a tax benefit. A reimbursement received for a previous year does not affect the previous year’s medical expense deduction.

Required: Calculate the year 2 allowable medical expense deduction for each tax payer before the adjusted gross income (AGI) limitation.

Explanations

A. ($3,900) The prescription drugs, eye exam and glasses, and removal of appendix are deductible. The herbal weight-loss supplement and vitamins are not deductible.

B. ($4,500) The medical insurance premiums, tooth extraction, and hearing aid are deductible and the total is reduced by the $500 insurance reimbursement received in year 2. The reimbursement received in year 3 does not affect the year 2 deduction. The cosmetic surgery and nonprescription drugs are not deductible.

C. ($12,700) The drug rehabilitation expenses, wheelchair purchase, and plastic surgery to correct injuries sustained in an auto accident are deductible. The health club membership fee is not deductible.

D. ($4,650) The emergency room fees, cost of crutches, dental insurance, and the cost of wigs related to hair loss because of chemotherapy treatments are deductible and the total is reduced by the $1,000 insurance reimbursement received in year 2.

E. ($4,950) The prescription drugs, annual physical exam, and the cost of foot surgery are deductible. The cost of liposuction is not deductible.

F. ($12,850) The costs of transportation and physical therapy, dental implants, and hearing aid batteries are deductible. The nonprescription drugs are not deductible and the year 3 reimbursement does not affect the year 2 deduction.

Task-Based Simulation 3

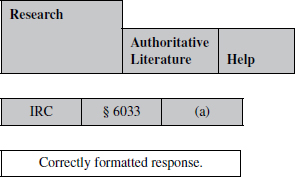

The trustee of a tax-exempt organization would like to know if the organization is required to file an annual information return. What section and subsection of the Internal Revenue Code provides the requirements for tax-exempt organizations to file an annual information return?

Enter your response in the answer fields below. Guidance on correctly structuring your response appears above and below the answer fields.

Solution to Task-Based Simulation 3