Chapter 5

Computing and Reporting Payroll Taxes

In This Chapter

![]() Tallying the employer's share of Social Security and Medicare

Tallying the employer's share of Social Security and Medicare

![]() Filing and paying unemployment taxes

Filing and paying unemployment taxes

![]() Figuring out workers’ compensation

Figuring out workers’ compensation

![]() Keeping accurate employee records

Keeping accurate employee records

After your company hires employees, you need to complete regular reports for the government regarding the taxes you must pay toward the employees’ Social Security and Medicare, as well as unemployment taxes. In most states, employers also are required to buy workers’ compensation insurance based on employees’ salary and wages.

This chapter reviews the federal, state, and local government reporting requirements for employers as well as the records you, the accountant, must keep in order to complete these reports. You also find out about the requirements for buying workers’ compensation insurance.

Paying Employer Taxes on Social Security and Medicare

In the United States, both employers and employees must contribute to the Social Security and Medicare systems. In most cases, employers share equally with employees the tax obligation for both Social Security and Medicare.

As discussed in Chapter 4, the employer and the employee each must pay a certain percentage of an employee's compensation for Social Security. Employer and employee must also pay a percentage of wages toward Medicare.

When you finish calculating payroll checks, you calculate the employer's portion of Social Security and Medicare. When you post the payroll to the books, you set aside the employer's portion of Social Security and Medicare in an accrual account.

Filing Form 941

Each quarter you must file federal Form 941, Employer's Federal Tax Return, which details the number of employees who received wages, tips, or other compensation for the quarter. In Chapter 4, you can see what the form looks like. Table 5-1 shows you what months are reported during each quarter and when the reports are due.

Table 5-1 Filing Requirements for Employer's Quarterly Federal Tax Return (Form 941)

|

Months in Quarter |

Report Due Date |

|

January, February, March |

On or before April 30 |

|

April, May, June |

On or before July 31 |

|

July, August, September |

On or before October 31 |

|

October, November, December |

On or before January 31 |

The following key information must be included on Form 941:

- Number of employees who received wages, tips, or other compensation in the pay period

- Total of wages, tips, and other compensation paid to employees

- Total tax withheld from wages, tips, and other compensation

- Taxable Social Security and Medicare wages

- Total paid out to employees in sick pay

- Adjustments for tips and group-term life insurance

- Amount of income tax withholding

- Advance earned income credit payments made to employees (see Chapter 4 for an explanation)

- Amount of tax liability per month

Knowing how often to file

As an employer, you file Form 941 on a quarterly basis, but you may have to pay taxes more frequently. Most new employers start out making monthly deposits for taxes due by using Form 8109 (shown in Chapter 4), which is a payment coupon that your company can get from a bank approved to collect deposits or from the Federal Reserve branch near you. Others make deposits online by using the IRS's Electronic Federal Tax Payment System (EFTPS). For more information on EFTPS, go to www.eftps.gov.

Employers on a monthly payment schedule (usually small companies) must deposit all employment taxes due by the 15th day of the following month. For example, the taxes for the payroll in April must be paid by May 15. Larger employers must pay taxes more frequently, depending on the number of workers employed and the dollar amount of payroll.

Completing Unemployment Reports and Paying Unemployment Taxes

As an employer, you're responsible for paying a share of unemployment compensation based on your record of firing and laying off employees. The fund you pay into is known as the Federal Unemployment Tax Act (FUTA) fund. For FUTA, employers pay a percentage rate based on each employee's earnings.

The employee earnings are capped at a certain dollar amount. So, even though each employee earns a different level of salary, FUTA taxes are calculated only on the first dollars each employee earns. As of this writing, the cap for FUTA taxes is on the first $7,000 of income.

States also collect taxes to fill their unemployment fund coffers. The federal government allows you to subtract a portion of the state unemployment payments from your federal contributions. Essentially, the amount you pay to the state can serve as a credit toward the amount you must pay to the federal government.

Each state sets its own unemployment tax rate. Many states also charge additional fees for administrative costs and job-training programs. You can check out the full charges for your state at payroll-taxes.com.

How states calculate the FUTA tax rate

States use four different methods to calculate how much you may need to pay in FUTA taxes:

- Benefit ratio formula: The state looks at the ratio of benefits collected by former employees to your company's total payroll over the past three years. States also adjust your rate depending upon the overall balance in the state unemployment insurance fund.

- Benefit wage formula: The state looks at the proportion of your company's payroll that's paid to workers who become unemployed and receive benefits, and then divides that number by your company's total taxable wages.

- Payroll decline ratio formula: The state looks at the decline in your company's payroll from year to year or from quarter to quarter.

- Reserve ratio formula: The state keeps track of your company's balance in the unemployment reserve account, which gives a cumulative representation of its use by your former employees who were laid off and paid unemployment. This recordkeeping dates back from the date you were first subject to the state unemployment rate. The reserve account is calculated by adding up all your contributions to the account and then subtracting total benefits paid. This amount is then divided by your company's total payroll. The higher the reserve ratio, the lower the required contribution rate.

These formulas can be very complicated, so your best bet is to contact your state's unemployment office to review how your company's unemployment rate will be set. In addition to getting a better idea of what may impact your FUTA tax rate, you can also discuss how best to minimize that rate.

These formulas can be very complicated, so your best bet is to contact your state's unemployment office to review how your company's unemployment rate will be set. In addition to getting a better idea of what may impact your FUTA tax rate, you can also discuss how best to minimize that rate.

Calculating FUTA tax

After you know what your rate is, calculating the actual FUTA tax you owe isn't difficult. Here's what you do:

- Multiply $7,000 by the federal unemployment tax rate to determine how much you owe per employee in federal unemployment. That $7,000 is the cap on earnings, which was discussed earlier.

- Multiply the result from Step 1 by the number of employees to determine the total federal unemployment tax you owe. If the state rate is lower than the federal rate, you're done. You pay the federal program the federal calculation, less the amount you pay into the state unemployment fund. If the state rate is higher than the federal rate, proceed to Step 3.

- Subtract the state rate from the federal rate.

- Multiply the result from Step 3 by $7,000 to determine the additional amount of state unemployment tax you must pay per employee.

- Multiply the result from Step 4 by the number of employees.

- Add the amounts from Steps 2 and 5.

Here's an example, assuming a state tax rate of 2.7 percent and a federal rate of 6.2 percent:

- State unemployment taxes:

- $7,000 × 0.027 = $189 per employee

- $189 × 10 employees = $1,890

- Federal unemployment taxes:

- $7,000 × 0.062 = $434

- $434 × 10 employees = $4,340

Because the federal rate is higher than the state rate, you can subtract the amount in state unemployment tax you owe from the total. In this case, you would pay $1,890 to the state, and $2,450 ($4,340 – $1,890) to the federal unemployment fund.

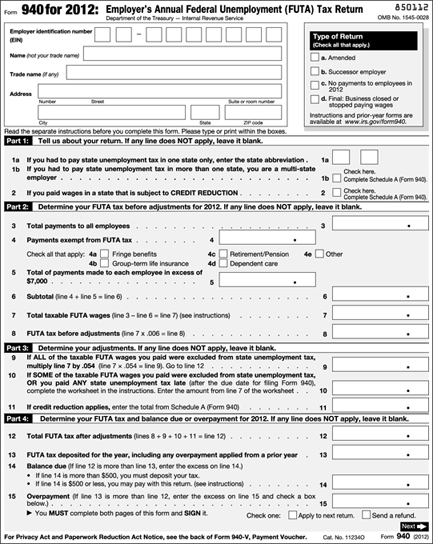

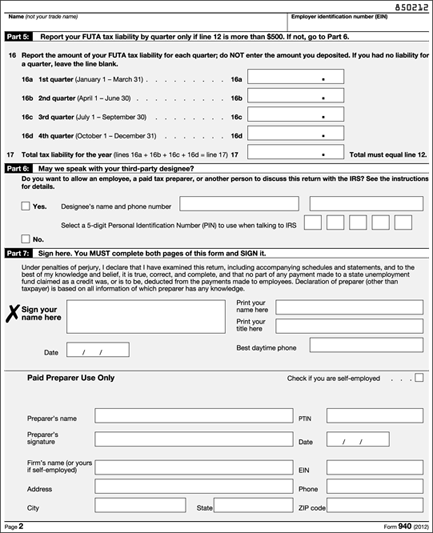

Each year, you must file IRS Form 940 Federal Unemployment (FUTA) Tax Return, shown in Figure 5-1. You can find Form 940 online at www.irs.gov/pub/irs-pdf/f940.pdf.

Courtesy of IRS

Figure 5-1: Employers report their FUTA tax on Form 940.

You can pay taxes for Form 940 by using the same coupon (Form 8109) used to pay Form 941 taxes (see “Filing Form 941” earlier in this chapter for an explanation). Most employers pay unemployment taxes quarterly.

Filing and paying unemployment taxes to state governments

Many states collect their unemployment taxes on a quarterly basis, and most states allow you to pay your unemployment taxes online. Check with your state to find out how to file and make unemployment tax payments.

Unfortunately, the filing requirements for state unemployment taxes may be more difficult to complete than those for federal taxes (see the discussion of Federal Form 940 in the previous section). States require you to detail each employee by name and Social Security number. The state must know how much an employee was paid each quarter in order to determine his or her unemployment benefit, if the need arises. Some states also require you to report the number of weeks an employee worked in each quarter because the employee's unemployment benefits are calculated based on the number of weeks worked.

Each state has its own form and filing requirements. Some states require a detailed report as part of your quarterly wage and tax reports. Other states allow a simple form for state income tax and a more detailed report with your unemployment tax payment.

Carrying Workers’ Compensation Insurance

Taxes aren't the only thing you need to worry about when figuring out your state obligations after hiring employees. Nearly every state requires employers to carry workers’ compensation insurance, which covers your employees in case they're injured on the job.

If an employee gets hurt on the job, workers’ compensation covers costs of lost income, medical expenses, vocational rehabilitation, and, if applicable, death benefits. Each state sets its own rules regarding how much medical coverage you must provide. If the injury also causes the employee to miss work, the state determines the percentage of the employee's salary you must pay and how long you pay that amount. If the injury results in the employee's death, the state also sets the amount you must pay toward funeral expenses and the amount of financial support you must provide the employee's family.

Each state makes up its own rules about how a company must insure itself against employee injuries on the job. Some states create state-based workers’ compensation funds to which all employers must contribute. Other states allow you the option of participating in a state-run insurance program or buying insurance from a private company. A number of states permit employers to use HMOs, PPOs, or other managed-care providers to handle workers’ claims.

If your state doesn't have a mandatory state pool, you have some other resources to obtain workers’ compensation insurance coverage. States set the requirements for coverage, and either a national rating bureau called the National Council on Compensation Insurance (NCCI) or a state rating bureau establishes the premiums. For the lowdown on NCCI and workers’ compensation insurance, visit www.ncci.com.

You may find lower rates over the long term if your state allows you to buy private workers’ compensation insurance. Many private insurers give discounts to companies with good safety standards in place and few past claims. So the best way to keep your workers’ compensation rates low is to encourage safety and minimize your company's claims.

Your company's rates are calculated based on risks identified in two areas:

- Classification of the business: These classifications are based on historic rates of risk in different industries. For example, if you operate a business in an industry that historically has a high rate of employee injury, such as a construction business, your base rate for workers’ compensation insurance is higher than that of a company in an industry without a history of frequent employee injury, such as an office that sells insurance.

- Classification of the employees: The NCCI publishes classifications of hundreds of jobs in a book called the Scopes Manual. Most states use this manual to develop the basis for their classification schedules. For example, businesses that employ most workers at desk jobs pay less in workers’ compensation than businesses with a majority of employees operating heavy machinery.

Be careful how you classify your employees. Many small businesses pay more than needed for workers’ compensation insurance because they misclassify employees. Be sure you understand the classification system and properly classify your employee positions before applying for workers’ compensation insurance. Be sure to read the information at www.ncci.com before classifying your employees.

Be careful how you classify your employees. Many small businesses pay more than needed for workers’ compensation insurance because they misclassify employees. Be sure you understand the classification system and properly classify your employee positions before applying for workers’ compensation insurance. Be sure to read the information at www.ncci.com before classifying your employees.

When computing insurance premiums for a company, the insurer (whether the state or a private firm) looks at employee classifications and the rate of pay for each employee. For example, consider the position of an administrative assistant who earns $25,000 per year. If that job classification is rated at 29 cents per $100 of income, the workers’ compensation premium for that employee is:

- ($25,000 ÷ 100) × 0.29 = $72.50

Most states allow you to exclude any overtime paid when calculating workers’ compensation premiums. You may also be able to lower your premiums by paying a deductible on claims. A deductible is the amount you would have to pay before the insurance company pays anything. Deductibles can lower your premium by as much as 25 percent, so consider that as well to keep your upfront costs low.

Maintaining Employee Records

When you consider all the state and federal filing requirements for employee taxes that you must keep, it's clear that you must have very good employee records. Otherwise, you'll have a hard time filling out all the necessary forms and providing detail on your employees and your payroll. The best way to track employee information is to set up an employee journal and create a separate journal page for each employee. You can set this up manually, or through an automated accounting system.

The detailed individual records you keep on each employee should include this basic information, most of which is collected or determined as part of the hiring process:

- Name, address, phone number, and Social Security number

- Department or division within the company

- Start date with the company

- Pay rate

- Pay period (weekly, biweekly, semimonthly, or monthly)

- Whether hourly or salaried

- Whether exempt or nonexempt

- W-4 withholding allowances

- Benefits information

- Payroll deductions

- All payroll activity

If an employee asks to change the number of withholding allowances and file a new W-4 or asks for benefits changes, his or her record must be updated to reflect such changes.

If an employee asks to change the number of withholding allowances and file a new W-4 or asks for benefits changes, his or her record must be updated to reflect such changes.

The personal detail that doesn't change each pay period should appear at the top of the journal page. Then, you divide the remaining information into columns. Here's a sample showing what the top of an employee's journal page may look like.

|

Name: |

SS#: |

|

Address: |

|

|

Tax Info: Married, 2 WH |

|

|

Pay Information: $8 hour, nonexempt, biweekly |

|

|

Benefits: None |

The following is an example of the body of the journal page. It contains columns for date of check, taxable wages, Social Security and Medicare tax (in one total), federal tax withholding, state tax withholding, and the net check amount.

You may want to add other columns to your employee journal to keep track of things such as

- Non-taxable wages

Examples include health or retirement benefits that are paid before taxes are taken out.

- Benefits

If the employee receives benefits, you need at least one column to track any money taken out of the employee's check to pay for those benefits. In fact, you may want to consider tracking each benefit in a separate column. Check out Chapter 4 for more on benefits.

- Sick time

- Vacation time

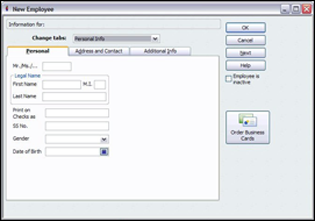

Clearly, these employee journal sheets can get very lengthy very quickly. That's why many small businesses use computerized accounting systems to monitor both payroll and employee records. Figures 5-2 and 5-3 show you how a new employee is added to the QuickBooks system.

Figure 5-2: New employee personal and contact information can be added in QuickBooks to make it easier to keep track of employees.

Figure 5-3: QuickBooks enables you to track salary and deduction information, as well as information about sick time and vacation time.