Chapter 4

Accounting for Change with Variance Analysis

In This Chapter

![]() Understanding and setting standard costs

Understanding and setting standard costs

![]() Figuring out direct materials prices and direct labor rates

Figuring out direct materials prices and direct labor rates

![]() Using formulas to compute variances

Using formulas to compute variances

![]() Exploiting a shortcut for calculating direct material and direct labor variances

Exploiting a shortcut for calculating direct material and direct labor variances

![]() Identifying variances that require further investigation

Identifying variances that require further investigation

When things don't go according to plan, inevitably you're left asking “Why?” To find the answer, examine the factors under your control. For example, suppose you don't like to diet. As an accountant, you should enjoy counting calories. But maybe you don't. Maybe you don't like to exercise either. That said, if you weigh yourself only to find that you're gaining rather than losing weight, you may ask “Why?” You thought you were being so careful this week. Why did you gain three pounds? It all comes down to three factors under your control: what you eat and drink, how much you eat and drink, and how much you exercise. Examining each of these factors helps you change your routine so that you can more successfully manage your weight in the future.

Variance analysis plays a similar role for business. When things go wrong, or even when they go more right than expected, variance analysis explains why. What caused higher-than-expected profits? What about unexpected losses? You can use all this information to improve future operations.

Setting Up Standard Costs

You can't measure variances without first setting standard costs or standards — predetermined unit costs of materials, labor, and overhead. Standards are really the building blocks of budgets; budgets predict total costs (as explained in Book VI, Chapters 4 and 5), but standards predict the cost of each unit of direct materials, direct labor, and overhead. Standard costs provide a number of important benefits for managers. For example, they

- Help managers budget for the future.

- Help employees focus on keeping costs down.

- Help set sales prices.

- Give managers a benchmark for measuring variances and identifying related problems.

- Simplify collecting and managing the cost of inventory.

- Provide useful information for variance analysis (as explained in this chapter).

Implementing standards often forces managers to face a critical dilemma: Should standards be aspirational or realistic?

- Ideal or aspirational standards can encourage employees to work hard to achieve rigorous goals. However, overly aggressive standards can unduly pressure employees, causing them to report false information or to just give up on the standards out of frustration, deeming them unattainable.

- Realistic standards provide more accurate cost information and are less likely to lead to the kind of unfavorable variances that result in lower-than-expected income. However, realistic standards don't always encourage employees to “go the extra mile” to improve cost control and productivity.

Therefore, the first step in variance analysis is to set up expectations: your standards. These standards must include both the cost and the quantity needed of direct materials and direct labor, as well as the amount of overhead required.

After you establish standards, you can use them to compute variances. Whenever actual performance strays from expectations, variances help you identify the reasons why.

After you establish standards, you can use them to compute variances. Whenever actual performance strays from expectations, variances help you identify the reasons why.

Establishing direct materials standards

Direct materials are raw materials traceable to the manufactured product, such as the amount of flour used to make a cake. To compute the direct materials standard price (SP), consider all the costs that go into a single unit of direct materials. Because several different kinds of direct materials are often necessary for any given product, you need to establish separate direct materials standard prices and quantities for every kind of direct materials needed.

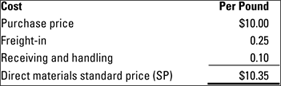

Suppose that the Band Book Company usually pays $10 per pound for paper. It typically pays $0.25 per pound for freight and another $0.10 per pound for receiving and handling. Therefore, as shown in Figure 4-1, total cost per pound equals $10.35.

©John Wiley & Sons, Inc.

Figure 4-1: Adding up direct materials standard price (SP).

Another standard to consider is the direct materials standard quantity (SQ) per unit. This number is the amount of direct materials needed to make a single unit of finished product. It includes not only the direct materials actually used but also any direct materials likely to get scrapped or spoiled in the production process.

Variance costing involves juggling many different figures and terms. To simplify matters, use abbreviations such as SP (for direct materials standard price) and SQ (for direct materials standard quantity). Doing so makes remembering how to calculate variances easier later in this chapter. For example, assume that Band Book Company needs 25 pounds of paper to make a case of books. For every case, three pounds of paper are deemed unusable because of waste and spoilage. Therefore, the direct materials standard quantity per unit equals 28 pounds, as shown in Figure 4-2.

Variance costing involves juggling many different figures and terms. To simplify matters, use abbreviations such as SP (for direct materials standard price) and SQ (for direct materials standard quantity). Doing so makes remembering how to calculate variances easier later in this chapter. For example, assume that Band Book Company needs 25 pounds of paper to make a case of books. For every case, three pounds of paper are deemed unusable because of waste and spoilage. Therefore, the direct materials standard quantity per unit equals 28 pounds, as shown in Figure 4-2.

©John Wiley & Sons, Inc.

Figure 4-2: Computing direct materials standard quantity (SQ) per unit.

Determining direct labor standards

Direct labor is the cost of paying your employees to make products. Proper planning requires setting standards with respect to two factors: the direct labor standard rate and the direct labor standard hours per unit.

To compute the direct labor standard rate or SR (the cost of direct labor), consider all the costs required for a single hour of direct labor. For example, suppose Band Book usually pays employees $9 per hour. Furthermore, it pays an additional $1 per hour for payroll taxes and, on average, $2 per hour for fringe benefits. As shown in Figure 4-3, the direct labor standard rate equals $12 per hour.

©John Wiley & Sons, Inc.

Figure 4-3: Computing the direct labor standard rate (SR).

You also need to estimate the amount of direct labor time needed to make a single unit, the direct labor standard hours (SH) per unit. This measurement estimates how long employees take, on average, to produce a single unit. Include in this rate the time needed for employee breaks, cleanups, and setups.

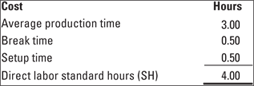

For example, employees at Band Book Company need three hours to produce a single case of books, plus an average of 30 minutes of setup time and 30 minutes of break time. Therefore, the direct materials standard quantity equals four hours, as shown in Figure 4-4.

©John Wiley & Sons, Inc.

Figure 4-4: Computing direct labor standard hours (SH).

Calculating the overhead rate

Standard costs also need to account for overhead (the miscellaneous costs of running a business) in addition to direct materials and direct labor. Overhead is much more difficult to measure than direct materials or direct labor standards because overhead consists of indirect materials, indirect labor, and other costs not easily traced to units produced. Therefore, measuring how much overhead should be applied to different units produced is very challenging. To assign overhead costs to individual units, you need to compute an overhead allocation rate.

Remember that overhead allocation entails three steps:

- Add up total overhead.

Add up estimated indirect materials, indirect labor, and all other product costs not included in direct materials and direct labor. This amount includes both fixed and variable overhead.

For example, assume that total overhead for Band Book Company is estimated to cost $100,000.

- Compute the overhead allocation rate.

The allocation rate calculation requires an activity level. You choose an activity that closely relates to the cost incurred. The most common activity levels used are direct labor hours or machine hours. Divide total overhead (calculated in Step 1) by the number of direct labor hours.

Assume that Band Book plans to utilize 4,000 direct labor hours:

Overhead allocation rate = Total overhead ÷ Total direct labor hours = $100,000 ÷ 4,000 hours = $25.00

Therefore, for every hour of direct labor needed to make books, Band Book applies $25 worth of overhead to the product.

- Apply overhead.

Multiply the overhead allocation rate by the number of direct labor hours needed to make each product.

Suppose a department at Band Book actually worked 20 hours on a product. Apply 20 hours × $25 = $500 worth of overhead to this product.

Adding up standard cost per unit

To find the standard cost, you first compute the cost of direct materials, direct labor, and overhead per unit, as explained in the previous sections. Then you add up these amounts.

Figure 4-5 applies this approach to Band Book Company. To calculate the standard cost of direct materials, multiply the direct materials standard price of $10.35 by the direct materials standard quantity of 28 pounds per unit. The result is a direct materials standard cost of $289.80 per case. To compute direct labor standard cost per unit, multiply the direct labor standard rate of $12 per unit by the direct labor standard hours per unit of 4 hours. The standard cost per unit is $48 for direct labor. Now multiply the overhead allocation rate of $10 per hour by the direct labor standard hours of 4 hours per unit to come to a standard cost of overhead per unit of $40.

©John Wiley & Sons, Inc.

Figure 4-5: Summing up standard cost per unit.

Add together direct materials, direct labor, and overhead to arrive at the standard cost per unit of $289.80 + $48 + $40 = $377.80. Making a single case of books costs Band Book $377.80.

Understanding Variances

A variance is the difference between the actual cost and the standard cost that you expected to pay. (Standard costs are covered earlier in this chapter.) When actual cost exceeds the standard, then the resulting variance is considered unfavorable because it reduces net income. On the other hand, when actual costs come in under standard costs, then the resulting variance is considered favorable because it increases net income.

Variances can arise from direct materials, direct labor, and overhead. In fact, the variances arising from each of these three areas, when added together, should equal the total variance:

Total variance = Direct materials variance + Direct labor variance + Overhead variance

In turn, you can further break down direct materials and direct labor variances into additional price and quantity variances to understand how changes in materials prices, materials quantities used, direct labor rates, and direct labor hours affect overall profitability.

Generally, you incur a variance for one of two reasons: Either you used more or less than you planned (a quantity variance), or you paid more or less than you planned (a price or rate variance).

Computing direct materials variances

A direct materials variance results from one of two conditions: differences in the prices paid for materials or discrepancies in the quantities used in production. To find these variances, you can use formulas or a simple diagram approach.

Using formulas to calculate direct materials variances

The total direct materials variance is comprised of two components: the direct materials price variance and the direct materials quantity variance.

To compute the direct materials price variance, take the difference between the standard price (SP) and the actual price (AP), and then multiply that result by the actual quantity (AQ):

Direct materials price variance = (SP – AP) × AQ

To get the direct materials quantity variance, multiply the standard price by the difference between the standard quantity (SQ) and the actual quantity:

Direct materials quantity variance = SP × (SQ – AQ)

The total direct materials variance equals the difference between total actual cost of materials (AP × AQ) and the budgeted cost of materials, based on standard costs (SP × SQ):

Total direct materials variance = (SP × SQ) – (AP × AQ)

Consider the Band Book Company example described in “Setting Up Standard Costs” earlier in the chapter. Band Book's standard price is $10.35 per pound. The standard quantity per unit is 28 pounds of paper per case. This year, Band Book made 1,000 cases of books, so the company should have used 28,000 pounds of paper, the total standard quantity (1,000 cases × 28 pounds per case). However, the company purchased 30,000 pounds of paper (the actual quantity), paying $9.90 per case (the actual price).

Based on the given formula, the direct materials price variance comes to a positive $13,500, a favorable variance:

Direct materials price variance = (SP – AP) × AQ = ($10.35 – $9.90) × 30,000 = $13,500 favorable

This variance means that savings in direct materials prices cut the company's costs by $13,500.

The direct materials quantity variance focuses on the difference between the standard quantity and the actual quantity, arriving at a negative $20,700, an unfavorable variance:

Direct materials quantity variance = SP × (SQ – AQ) = $10.35 × (28,000 – 30,000) = –$20,700 unfavorable

This result means that the 2,000 additional pounds of paper used by the company increased total costs $20,700. Now, you can plug both parts in to find the total direct materials variance. (You could just plug in the final results, but I show you the longer math here.) Compute the total direct materials variance as follows:

Total direct materials variance = (SP × SQ) – (AP × AQ) = ($10.35 × 28,000) – ($9.90 × 30,000) = $289,800 – $297,000 = –7,200 unfavorable

Diagramming direct materials variances

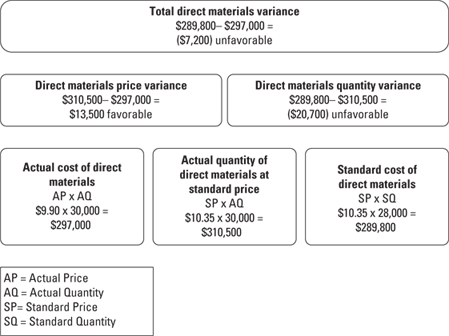

Figure 4-6 provides an easier way to compute price and quantity variances. To use this diagram approach, just compute the totals in the third row: actual cost, actual quantity at standard price, and the standard cost. The actual cost less the actual quantity at standard price equals the direct materials price variance. The difference between the actual quantity at standard price and the standard cost is the direct materials quantity variance. The total of both variances equals the total direct materials variance.

To apply this method to the Band Book example, take a look at Figure 4-7. Start at the bottom. Direct materials actually cost $297,000, even though the standard cost of the direct materials is only $289,800. The actual quantity of direct materials at standard price equals $310,500.

©John Wiley & Sons, Inc.

Figure 4-6: Diagram of how price and quantity variances contribute to direct materials variance.

To compute the direct materials price variance, subtract the actual cost of direct materials ($297,000) from the actual quantity of direct materials at standard price ($310,500). This difference comes to a $13,500 favorable variance, meaning that the company saves $13,500 by buying direct materials for $9.90 rather than the original standard price of $10.35.

To compute the direct materials quantity variance, subtract the actual quantity of direct materials at standard price ($310,500) from the standard cost of direct materials ($289,800), resulting in an unfavorable direct materials quantity variance of $20,700. Because the company uses 30,000 pounds of paper rather than the 28,000-pound standard, it loses an additional $20,700.

This setup explains the unfavorable total direct materials variance of $7,200 — the company gains $13,500 by paying less for direct materials, but loses $20,700 by using more direct materials.

©John Wiley & Sons, Inc.

Figure 4-7: Computing direct materials variances by using a diagram.

Calculating direct labor variances

A direct labor variance is caused by differences in either wage rates or hours worked. As with direct materials variances, you can use either formulas or a diagram to compute direct labor variances.

Utilizing formulas to figure out direct labor variances

To estimate how the combination of wages and hours affects total costs, compute the total direct labor variance. As with direct materials, the price and quantity variances add up to the total direct labor variance. To compute the direct labor price variance (also known as the direct labor rate variance), take the difference between the standard rate (SR) and the actual rate (AR), and then multiply the result by the actual hours worked (AH):

Direct labor price variance = (SR – AR) × AH

To get the direct labor quantity variance (also known as the direct labor efficiency variance), multiply the standard rate (SR) by the difference between total standard hours (SH) and the actual hours worked (AH):

Direct labor quantity variance = SR × (SH – AH)

The direct labor variance equals the difference between the total budgeted cost of labor (SR × SH) and the actual cost of labor, based on actual hours worked (AR × AH):

Total direct labor variance = (SR × SH) – (AR × AH)

Now you can plug in the numbers for the Band Book Company example from earlier in the chapter. Band Book's direct labor standard rate (SR) is $12 per hour. The standard hours (SH) come to 4 hours per case. Because Band made 1,000 cases of books this year, employees should have worked 4,000 hours (1,000 cases × 4 hours per case). However, employees actually worked 3,600 hours, for which they were paid an average of $13 per hour.

With these numbers in hand, you can apply the formula to compute the direct labor price variance:

Direct labor price variance = (SR – AR) × AH = ($12.00 – $13.00) × 3,600 = –$1.00 × 3,600 = –$3,600 unfavorable

According to the direct labor price variance, the increase in average wages from $12 to $13 causes costs to increase by $3,600. Now plug the numbers into the formula for the direct labor quantity variance:

Direct labor quantity variance = SR × (SH – AH) = $12.00 × (4,000 – 3,600) = $12.00 × 400 = $4,800 favorable

Employees worked fewer hours than expected to produce the same amount of output. This change saves the company $4,800 — a favorable variance. To compute the total direct labor variance, use the following formula:

Total direct labor variance = (SR × SH) – (AR × AH) = ($12.00 × 4,000) – ($13.00 × 3,600) = $48,000 – $46,800 = $1,200 favorable

According to the total direct labor variance, direct labor costs were $1,200 lower than expected, a favorable variance.

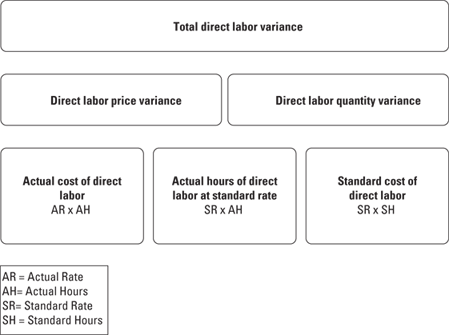

Employing diagrams to work out direct labor variances

Figure 4-8 shows you how to use a diagram to compute price and quantity variances quickly and easily. First, compute the totals in the third row: actual cost, actual hours at standard rate, and the standard cost. To get the direct labor price variance, subtract the actual cost from the actual hours at standard. The difference between the standard cost of direct labor and the actual hours of direct labor at standard rate equals the direct labor quantity variance. The total of both variances equals the total direct labor variance.

Take a look at Figure 4-9 to see this diagram in action for Band Book: Starting from the bottom, the actual cost of direct labor amounts to $46,800. The actual hours of direct labor at standard rate equals $43,200. The standard cost of direct labors comes to $48,000.

©John Wiley & Sons, Inc.

Figure 4-8: How price and quantity variances add up to direct labor variance.

To compute the direct labor price variance, subtract the actual hours of direct labor at standard rate ($43,200) from the actual cost of direct labor ($46,800) to get a $3,600 unfavorable variance. This result means the company incurs an additional $3,600 in expense by paying its employees an average of $13 per hour rather than $12.

To compute the direct labor quantity variance, subtract the standard cost of direct labor ($48,000) from the actual hours of direct labor at standard rate ($43,200). This math results in a favorable variance of $4,800, indicating that the company saves $4,800 in expenses because its employees work 400 fewer hours than expected.

The $1,200 favorable variance arises because of two factors: the company saves $4,800 from fewer hours worked but incurs an additional $3,600 expense by paying its employees more money per hour than planned. This scenario begs the question “Are higher-paid workers more productive?” But that's a discussion for the human resources experts.

©John Wiley & Sons, Inc.

Figure 4-9: Computing the direct labor variances the easy way with a diagram.

Computing overhead variances

Whenever you see direct labor and direct materials, overhead can't be far behind. To compute overhead applied, multiply the overhead application rate by the standard number of hours allowed:

Overhead applied = Overhead application rate × SH

So you can determine overhead variance by subtracting actual overhead from applied overhead:

Overhead variance = Overhead applied – Actual overhead

Band Book Company incurs actual overhead costs of $95,000. The company's overhead application rate is $25 per hour. (You can find the math for that calculation in the earlier section “Calculating the overhead rate.”) In that prior section, you use direct labor hours as the activity level for applying overhead. In order for Band Book's workers to produce 1,000 cases, you can expect them to work standard hours of 4 direct labor hours per case.

SH equals 1,000 cases produced × 4 direct labor hours per case, or 4,000 direct labor hours. This amount results in overhead applied of $100,000:

Overhead applied = Overhead application rate × SH = $25.00 × 4,000 = $100,000

To compute the variance, subtract actual overhead from the overhead applied:

Overhead variance = Overhead applied – Actual overhead = $100,000 – $95,000 = $5,000

Because actual overhead is less than overhead applied, the $5,000 variance is favorable.

Spending too much or too little on overhead — or using overhead inefficiently — often causes overhead variance.

Like direct labor and direct materials, overhead, too, can have price and quantity variables. However, fixed and variable cost behaviors considerably complicate the calculation of overhead variances. These complexities are outside the scope of this book.

Looking past the favorable/unfavorable label

The unfavorable and favorable labels describe variances only in terms of how they affect income; favorable variances aren't necessarily always good, and unfavorable variances aren't necessarily always bad. For example, a favorable variance may result because a company purchases cheaper direct materials of poorer quality. These materials lower costs, but they also hurt the quality of finished goods, damaging the company's reputation with customers. This kind of favorable variance can work against a company. On the other hand, an unfavorable variance may occur because a department chooses to scrap poor-quality goods. In the long run, the company benefits from incurring a short-term unfavorable variance to provide better-quality goods to its customers.

Teasing Out Variances

In your business, variance analysis helps you identify problem areas that require attention, such as

- Poor productivity

- Poor quality

- Excessive costs

- Excessive spoilage or waste of materials

Identifying and working on these problems helps managers improve production flow and profitability. Managers and accountants often talk about management by exception — using variance analysis to identify exceptions, or problems, where actual results significantly vary from standards. By paying careful attention to these exceptions, managers can root out and rectify manufacturing problems and inefficiencies, thereby improving productivity, efficiency, and quality.

Interpreting variances in action

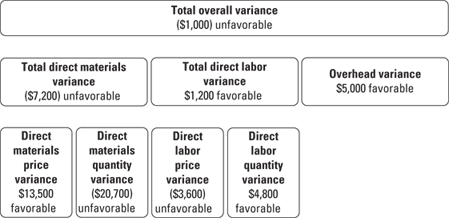

The previous sections in this chapter lay out what happens to the costs of the Band Book Company over the course of a year. Figure 4-10 summarizes Band Book's variances.

©John Wiley & Sons, Inc.

Figure 4-10: Band Book's variances.

A complete analysis of Band Book's variances provides an interesting story to explain why the company has a $1,000 unfavorable variance. The following events transpire:

- The company pays less than expected for direct materials, leading to a favorable $13,500 direct materials price variance.

- Perhaps because of the cheaper, lower-quality direct materials, the company uses an excessive amount of direct materials. This overage results in a $20,700 unfavorable direct materials quantity variance.

- The company pays its employees a higher wage rate, resulting in an unfavorable direct labor price variance of $3,600.

- The company saves money because employees work fewer hours than expected, perhaps because they're more productive, higher-paid workers. The favorable direct labor quantity variance is $4,800.

- The company saves $5,000 in reduced overhead costs.

Focusing on the big numbers

Management by exception directs managers to closely investigate the largest variances. For example, the two largest variances in Figure 4-10 are the direct materials quantity variance ($20,700 unfavorable) and the direct materials price variance ($13,500 favorable). Band Book's managers should focus on how the company buys and uses its direct materials.

Here, the direct materials quantity variance resulted because the company should have used 28,000 pounds of paper but actually used 30,000 pounds of paper. Why? Here are a few possibilities:

- The paper was poor quality, and much of it needed to be scrapped.

- The company underestimated the amount of paper needed (the standard quantity needs to be changed).

- Someone miscounted the amount of paper used; 2,000 pounds of paper are sitting in the back of the warehouse (oops).

- A new employee misused the machine, shredding several thousand pounds of paper.

Management by exception directs managers to where the problem may have occurred so that they can investigate what happened and take corrective action.

Now take a look at the favorable direct materials price variance of $13,500. How did the purchasing department come to purchase direct materials for only $9.90 a pound, rather than the $10.35 standard? Did the purchased materials meet all of the company's quality standards? Should the company reduce its standard price in the future?

Consider setting control limits to determine which items are sufficiently large to investigate. A variance exceeding its control limit takes priority over less significant variances.

Tracing little numbers back to big problems

Be careful! Don't focus exclusively on the big numbers and ignore the little numbers. Big problems can also hide in the small numbers. For example, although many frauds (such as stealing raw materials) may trigger large variances, a well-planned fraud may be designed to manipulate variances so that they stay low, below the radar, where managers won't notice them.

Be careful! Don't focus exclusively on the big numbers and ignore the little numbers. Big problems can also hide in the small numbers. For example, although many frauds (such as stealing raw materials) may trigger large variances, a well-planned fraud may be designed to manipulate variances so that they stay low, below the radar, where managers won't notice them.

For example, knowing the standard price of a raw material is $100 per unit, a crooked purchasing manager may arrange to purchase the units for exactly that price — $100 per unit — while receiving $10 per unit as a kick-back gratuity from the supplier. This scheme results in a direct materials price variance of zero, but it doesn't reflect what should be the company's actual cost of doing business. A more scrupulous purchasing manager would have arranged a purchase price of $90, resulting in a large positive direct materials price variance.

To avoid these problems, managers should still investigate all variances, even while focusing most of their time on the largest figures.