15_9781118758007-pp03.xhtml

by Jill Gilbert Welytok, Tage C. Tracy, John A. Tracy, Vijay S. Sampath, Maire Loug

Accounting All-in-One For Dummies

15_9781118758007-pp03.xhtml

by Jill Gilbert Welytok, Tage C. Tracy, John A. Tracy, Vijay S. Sampath, Maire Loug

Accounting All-in-One For Dummies

- Introduction

- Introduction

- Book I: Setting Up Your Accounting System

- Chapter 1: Grasping Bookkeeping and Accounting Basics

- Chapter 2: Outlining Your Financial Road Map with a Chart of Accounts

- Chapter 3: Using Journal Entries and Ledgers

- Chapter 4: Choosing an Accounting Method

- Book II: Recording Accounting Transactions

- Chapter 1: Keeping the Books

- Chapter 2: Tracking Purchases

- Chapter 3: Counting Your Sales

- Chapter 4: Processing Employee Payroll and Benefits

- Chapter 5: Computing and Reporting Payroll Taxes

- Book III: Adjusting and Closing Entries

- Chapter 1: Depreciating Your Assets

- Chapter 2: Paying and Collecting Interest

- Chapter 3: Proving Out the Cash

- Chapter 4: Reconciling Accounts and Closing Journal Entries

- Chapter 5: Checking Your Accuracy

- Chapter 6: Adjusting the Books

- Book IV: Preparing Income Statements and Balance Sheets

- Chapter 1: Brushing Up on Accounting Standards

- Chapter 2: Preparing an Income Statement and Considering Profit

- Understanding the Nature of Profit

- Choosing the Income Statement Format

- Deciding What to Disclose in the Income Statement

- Examining How Sales and Expenses Change Assets and Liabilities

- Considering the Diverse Financial Effects of Making a Profit

- Reporting Extraordinary Gains and Losses

- Correcting Common Misconceptions about Profit

- Chapter 3: Assessing the Balance Sheet’s Asset Section

- Chapter 4: Digging for Debt in the Balance Sheet’s Liabilities Section

- Chapter 5: Explaining Ownership in the Equity Section of the Balance Sheet

- Chapter 6: Coupling the Income Statement and Balance Sheet

- Book V: Reporting on Your Financial Statements

- Chapter 1: Presenting Financial Condition and Business Valuation

- Chapter 2: Laying Out Cash Flows and Changes in Equity

- Understanding the Difference between Cash and Profit

- Realizing the Purpose of the Statement of Cash Flows

- Walking through the Cash Flow Sections

- Recognizing Methods for Preparing the Statement of Cash Flows

- Interpreting the Statement of Cash Flows

- Looking Quickly at the Statement of Changes in Stockholders Equity

- Chapter 3: Analyzing Financial Statements

- Chapter 4: Reading Explanatory Notes and Disclosures

- Chapter 5: Studying the Report to the Shareholders

- Book VI: Planning and Budgeting for Your Business

- Chapter 1: Incorporating Your Business

- Chapter 2: Choosing a Legal Structure for a Business

- Chapter 3: Drawing Up a Business Plan to Secure Cash

- Chapter 4: Budgeting for a Better Bottom Line

- Chapter 5: Mastering and Flexing Your Budgeting

- Chapter 6: Planning for Long-Term Obligations

- Book VII: Making Savvy Business Decisions

- Chapter 1: Estimating Costs with Job Costing

- Chapter 2: Performing Activity-Based Costing

- Chapter 3: Examining Contribution Margin

- Chapter 4: Accounting for Change with Variance Analysis

- Chapter 5: Making Smart Pricing Decisions

- Book VIII: Handling Cash and Making Purchase Decisions

- Chapter 1: Identifying Costs and Matching Costs with Revenue

- Chapter 2: Exploring Inventory Cost Flow Assumptions

- Chapter 3: Answering the Question: Should I Buy That?

- Chapter 4: Knowing When to Use Debt to Finance Your Business

- Chapter 5: Interpreting Your Financial Results as a Manager

- Book IX: Auditing and Detecting Financial Fraud

- Chapter 1: Mulling Over Sarbanes-Oxley Regulation

- Chapter 2: Preventing Cash Losses from Embezzlement and Fraud

- Chapter 3: Assessing Audit Risk

- Chapter 4: Collecting and Documenting Audit Evidence

- Chapter 5: Auditing a Client's Internal Controls

- Defining Internal Controls

- Identifying the Five Components of Internal Controls

- Determining When You Need to Audit Internal Controls

- Testing a Client's Reliability: Assessing Internal Control Procedures

- Limiting Audit Procedures When Controls Are Strong

- Tailoring Tests to Internal Control Weaknesses

- Timing a Client's Control Procedures

- Chapter 6: Getting to Know the Most Common Fraud Schemes

- Chapter 7: Cooked Books: Finding Financial Statement Fraud

- About the Authors

- Cheat Sheet

- More Dummies Products

Book III

Adjusting and Closing Entries

Check out www.dummies.com/extras/accountingaio for specifics on how to adjust your accounting records with accruals and deferrals.

Check out www.dummies.com/extras/accountingaio for specifics on how to adjust your accounting records with accruals and deferrals.

In this book…

- Choose the best depreciation method for your long-term assets. Assets are used to generate revenue, and depreciation expenses the cost of the asset as it's used in business.

- Account for interest your business pays or receives. If your business borrows or lends money, it pays or collects interest. Either way, you need to account for that interest.

- Prove out the cash to ensure that what's on paper matches the real dollar amounts in a store or office. Your cash account typically has a lot of transactions. As a result, you need to carefully account for cash to ensure that all the activity is properly recorded.

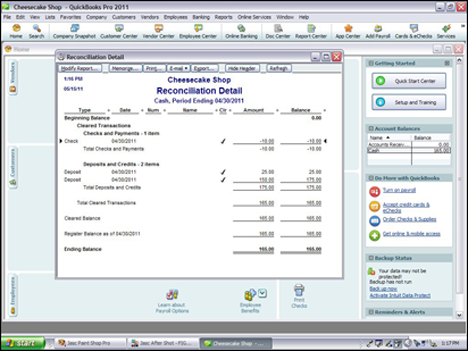

- Reconcile accounts and confirm that your journals and general ledger are correct. Reconciling your books is a great way to check your work, correct any errors, and even spot signs of fraud!

- Double-check your books by running a trial balance, correct any errors, and prepare a financial statement worksheet. A trial balance lists all your accounts and their dollar balances.

- Adjust the books in preparation of preparing financial reports. Trial balances are adjusted before being used to create financial statements to ensure accuracy in financial reports.

-

No Comment

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.