12.1 PRICING OF DERIVATIVE CONTRACTS UNDER COLLATERAL AGREEMENTS

The liquidity risk embedded in derivative contracts requires careful analysis because of the complex nature of payoffs and of cash flow profiles. For derivative contracts too the general principle is that the value at inception should be the present value of all future (expected) cash flows, and it should be zero in order to be defined “fair”. All costs and remuneration for risks must be included in the fair value to one of the parties involved,1 hence funding costs and remuneration for liquidity risks have to be considered as well.

Funding costs arise from the replication (i.e., dynamic hedging) strategy of derivative contracts, and in the first part of this chapter we will study how these costs are originated: we will investigate all the components related to funding of the replication strategy and of the collateral accounts in case the contract provides for it.

Currently, most contracts dealt in interbank OTC derivatives are collateralized. A collateral agreement is characterized by the following features, amongst others:

- Initial margin (in some contracts defined as independent amount): This is the amount of cash (or other eligible assets, possibly illiquid) that a counterparty has to post to the other in order to cover potential negative exposure of the derivative contract. It is usually related to as the VaR of the deal and theoretically should be exchanged between parties in a symmetric way.

- Variation margin: This is variation of the collateral subsequent to variation in the NPV of the derivative contract.

- Maintenance margin: This is the level of the collateral below which it is not possible to drop after variation margins are posted. If the balance drops below the level, the initial margin has to be restored.

The most widespread form of collateral agreement is represented by the CSA (i.e., a credit support annex to the ISDA Master Agreement for derivative transactions). Though a legal document, it is not mandatory (banks can in theory sign an ISDA agreement without a CSA), and regulates credit support, represented by collateral, for derivative products.

The CSA defines the asset classes of covered transactions and rules under the terms of which collateral is posted or transferred between derivative counterparties to mitigate credit risk arising from in-the-money derivative positions. If on any valuation date, the delivery amount equals or exceeds the pledgor's minimum transfer amount (MTA), the pledgor is required to transfer eligible collateral with a value at least equal to the delivery amount. The delivery amount is the amount of the CSA that exceeds the value of all posted collateral held by the secured party.

The CSA is equal to the secured party's exposure plus pledgor's independent amount (if any) minus secured party's independent amount (if any) minus the pledgor's threshold.

The collateral to post must meet the eligibility criteria in the agreement (e.g., which currencies it may be in, what types of bonds are allowed, and which haircuts are applied. Rules are defined in order to settle disputes arising over the valuation of derivative positions.

Although a standard CSA is a long way from being defined by practitioners, some market conventions are common features for many CSAs, as there is no threshold or symmetric terms between parties – only cash as eligible collateral is remunerated at the OIS rate.

It is also worthy of note that CSA agreements usually operate on an aggregated basis: the NPVs of all contracts (also for different types of underlying) included in a netting set are summed algebraically and the net amount is posted as collateral by the counterparty who has a negative total NPV. Clauses relating to minimum transfer amount and thresholds also apply. We will not dwell on netting sets, minimum transfer amounts and thresholds in what follows.

Variation and initial margins are commonly remunerated at different rates. The cash posted for variation margin is remunerated at the OIS rate defined for the reference currency, the cash posted for initial margin is typically remunerated at the OIS rate minus. Eligible assets are not remunerated at all and they are typically transferred “free of payment”.

Futures contracts have features similar to CSA agreements, but: the initial margin (collateral) is always required by the clearing house and is determined as a small percentage of the value of future delivery (futures price times the notional of the contract), based on the VaR of the contract. Variation margins occur daily but, differently from the CSA,2 they can be withdrawn if positive to a counterparty, provided that the maintenance margin has not be eroded. In the end they are not real variation margins, but daily liquidation of the variation in terminal value of the contract. There is remuneration for the initial margin, but no remuneration for variation margins.

In what follows we analyse the pricing of derivatives under a CSA agreement, without considering netting, minimum transfer amounts and thresholds. So, we will investigate the pricing of a contract on a “standalone” basis, although we are aware that “incremental” pricing, when netting is considered, may significantly alter the result and then it should not be overlooked if a more refined methodology needs to be applied.

Fujii and Takahashi [70] is a work closely related to the analysis below: they study the effects of imperfect collateralization and introduce a decomposition of total contract value which resembles the one we offer below, which also includes bilateral CVA. On the other hand, we extend their analysis to include the effects that funding costs have on final contract value, disregarding the residual counterparty credit risk due to imperfect collateralization.

Another recent work related to our analysis is [104], which studies the effects of partial collateralization on bilateral credit risk, keeping the costs due to different rates paid and received on the collateral account in mind. Although their pricing fomulae somehow encompass the formulae we give below as well, we believe we offer a different and intuitive approach to the inclusion of funding costs, with the same proviso as before of not considering credit risk. We also have to stress the fact that [104] focuses on deriving a general formula to calculate the price of the contract,3 whereas we try and derive the value of the contract to a counterparty.

12.1.1 Pricing in a simple discrete setting

Let us assume we have an underlying asset S at time 0 that can go up to Su = Su or down to Sd = Sd, with d < 1, u > 1 and u × d = 1 in the next period. Let VC be the price of a contingent claim at time 0 (the “C” at the exponent stands for “collateralized”), and ![]() and

and ![]() its value when the underlying jumps to, respectively, Su and Sd. C is the value of the collateral account to be posted to the counterparty holding a position in the contingent claim when the NPV is positive to it; the collateral account earns collateral rate c. We will assume that percentage γ of the contract's NPV is continuously collateralized, so that at any time C = γV.4 B is the value of a bank account earning risk-free rate r at each period. In this framework, following the classical binomial approach in [56], we build a portfolio of underlying asset S and bank account B perfectly replicating the value of the contingent claim in each of the two states of the world (i.e., possible outcomes of the underlying asset's price), jointly with the value of the collateral account. In other words, we want to replicate a long position in the collateralized contingent claim.

its value when the underlying jumps to, respectively, Su and Sd. C is the value of the collateral account to be posted to the counterparty holding a position in the contingent claim when the NPV is positive to it; the collateral account earns collateral rate c. We will assume that percentage γ of the contract's NPV is continuously collateralized, so that at any time C = γV.4 B is the value of a bank account earning risk-free rate r at each period. In this framework, following the classical binomial approach in [56], we build a portfolio of underlying asset S and bank account B perfectly replicating the value of the contingent claim in each of the two states of the world (i.e., possible outcomes of the underlying asset's price), jointly with the value of the collateral account. In other words, we want to replicate a long position in the collateralized contingent claim.

To do so, we have to set the following equalities in each of the two states of the world:

and

Equation (12.1) states that the value of the contingent claim ![]() , when the underlying jumps to Su from the starting value S, minus the value of the collateral account, must be equal to the value of the replicating portfolio, comprised of α units of the underlying and β units of the bank account. The collateral account at the end of the period will be equal to the initial value C at time 0, plus the interest rate accrued c. The replicating portfolio has to be revalued at prices prevailing at the end of the period (i.e., Su for the underlying asset and initial value B plus accrued interest r for the bank account). In a very similar way, equation (12.2) states that the value of the contingent claim, minus the value of the collateral account, must be equal to the value of the replicating portfolio when the underlying jumps to Sd.

, when the underlying jumps to Su from the starting value S, minus the value of the collateral account, must be equal to the value of the replicating portfolio, comprised of α units of the underlying and β units of the bank account. The collateral account at the end of the period will be equal to the initial value C at time 0, plus the interest rate accrued c. The replicating portfolio has to be revalued at prices prevailing at the end of the period (i.e., Su for the underlying asset and initial value B plus accrued interest r for the bank account). In a very similar way, equation (12.2) states that the value of the contingent claim, minus the value of the collateral account, must be equal to the value of the replicating portfolio when the underlying jumps to Sd.

Equations (12.1) and (12.2) can be easily solved for quantities α and β, yielding:

and

We indicated α = Δ because it is easily seen in (12.3) that it is the numerical first derivative of the price of the contingent claim with respect to the underlying asset, as usually indicated in option pricing theory.

If the replicating portfolio is able to mimic payoff of the collateralized contingent claim, then its value at time 0 is also the arbitrage-free price of the collateralized contingent claim:

It is possible to express (12.5) in terms of discounted expected value under the risk-neutral measure and, recalling that C = γVC and rearranging, we get:

with ![]() . The value of the collateralized contingent claim VC is trivially:

. The value of the collateralized contingent claim VC is trivially:

which is the expected risk-neutral value multiplied by the factor ![]() , making the final formula look like the expected value discounted by a rate that is a weighted average of the risk-free and collateral rate, instead of just the risk-free rate, despite the fact we are still in a risk-neutral world.

, making the final formula look like the expected value discounted by a rate that is a weighted average of the risk-free and collateral rate, instead of just the risk-free rate, despite the fact we are still in a risk-neutral world.

The right-hand side of equation (12.6) is also equal to the expression we would get when replicating a contingent claim without any collateral agreement.5 Let VNC be the value of such a claim, then we have:

Equation (12.8) states that a non-collateralized contingent claim is equal to an otherwise identical collateralized claim, minus a quantity we name liquidity value adjustment (LVA) and precisely define as follows.

Definition 12.1.1. LVA is the discounted value of the difference between the risk-free rate and the collateral rate paid (or received) on the collateral over the life of the contract. It is the gain (or loss) produced by liquidation of the NPV of the derivative contract due to the collateralization agreement.

The fact that we are still working in a risk-neutral world is confirmed by the expected return on the underlying asset:

pSu + (1 − p)Sd = (1 + r)S

which is equal to the risk-free rate.

Note that by extending the binomial approach to a multi-period setting, thus introducing a dynamical replicating strategy whereby the contingent claim is replicated by dynamically rebalancing the underlying asset and bond portfolio, the final result of the replica is not terminal payoff of the contingent claim, but includes both the latter and the terminal value of cumulated losses/gains arising from LVA. This has some very important implications at the dealing room level which we examine in Section 13.2.

Example 12.1.1 clarifies how the replication argument works under the collateral and payoff attained at expiry.

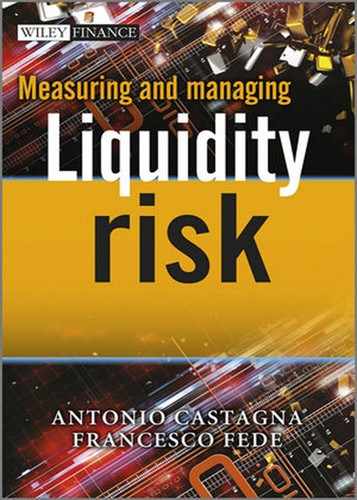

Example 12.1.1. Assume6 we want to price a call option that is fully collateralized (γ = 100%) and written on an underlying asset whose starting value is 80, which is also the strike price. The risk-free rate for one period is r = 0.10, whereas the collateral rate for each period is c = 0:06. The option expires in three periods; at the end of each period the underlying asset can jump upward or downward by a factor, respectively, of u = 1.5 and d = 0.5, so that the probability to jumping upward is p = 0.6. In Table 12.1 we show how the underlying asset price evolves (with the associated probability below each possible outcome).

Table 12.1. Evolution of the underlying asset and (in italics) associated probabilities below each possible outcome

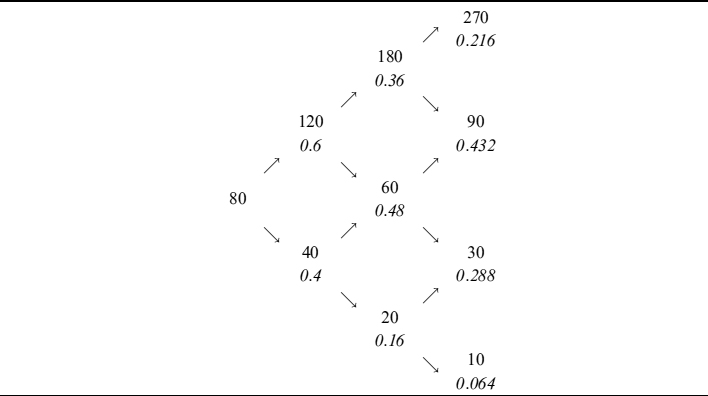

The value of the option can be computed via (12.7) backward recursion starting from the known terminal payoff. The value of the option at each point of the binomial grid is also the value of the collateral account (with the sign reversed). Table 12.2 gives the results and shows the value of the collateralized option at time 0 is VC = 38.0851.

Table 12.2. Value of the call option at each point of the grid and of the collateral account (same but with the sign reversed)

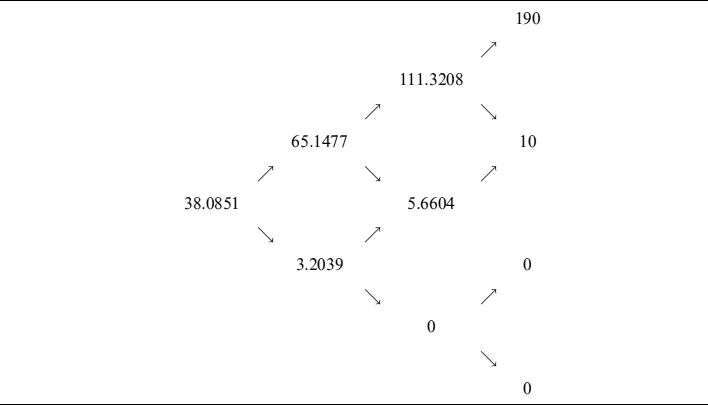

A replicating portfolio can be built be computing the Δ for the underlying asset and the quantity β of the bank account needed to finance the purchase. In Table 12.3 the Δ is shown for each node of the binomial tree along a predefined path of the underlying asset (it is arbitrary and for illustration purposes only); below each Δ we also indicate the quantity to trade in the bank account, plus the interest paid on the amount of the bank account traded in the previous period. At the end of the last period we consider both types of jumps, so as to examine what happens when the option terminates in-the-money or out-of-the-money.

Table 12.3. Amount of underlying asset to trade at each point of the predefined path. Below each Δ the amount of the bank account plus accrued interests from the previous period are shown (in italics)

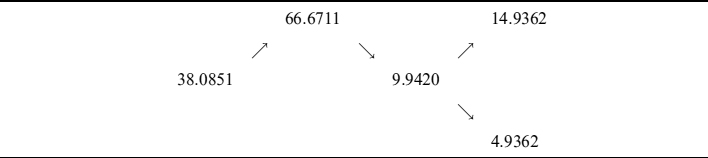

At time 0, the quantity of the underlying to hold in the portfolio to replicate one call option is 0.7743. To finance this purchase, we have to borrow money by selling a bank account for an amount of −23.8586. The difference is the amount of money we have to invest to begin the replication strategy, and it is exactly the value of the option at time 0.

At time 1, Δ = 0.8805 so we have to buy more assets and increase selling the value of the bank account to borrow more money, besides paying accrued interest on the initial borrowing of 23.8586, which we still have. The value of the bank account is then −38.9892. When we arrive at the last period either with one asset in the portfolio or a bank account value of −75.0638, when the option expires in-the-money; otherwise, we end up with no asset or a bank account value of 4.9362 when the option expires out-of-the-money.

There is an additional amount of money to be borrowed when replicating a collateralized option, and this is the amount needed to finance the collateral account value. Hence, a long position in a collateralized option entails a short position in the collateral account, since we have a cash amount of money equal to the value of the contingent claim. The total cost to replicate the collateral account is given by the difference between the risk-free and collateral rate, times the amount of the collateral account at the previous period. In Table 12.4 we show the cost associated to each point of the predefined path we have chosen for the underlying asset; the cost is nil at time 0 and has to be financed for the other periods.

Table 12.4. Cost to replicate the collateral account at each point of the predefined underlying asset's path

Let us now investigate the replicated value of the call option. This is shown in Table 12.5, where we revaluate at each point of the predefined path the replicating portfolio as far as the quantity of the underlying asset and bank account needed to finance its purchase are concerned. As can easily be seen, the replicating portfolio does not exactly mimic the value of the call, and at expiry the two possible payoffs (i.e., 10 when the call terminates in-the-money and 0 otherwise) do not actually match in either case.

Table 12.5. Replica of the call option with the underlying asset and bank account portfolio

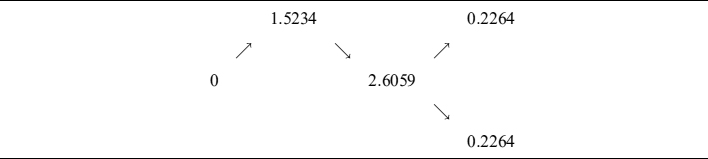

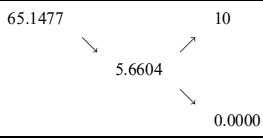

The error in the replica is exactly equal to the cost to finance the collateral account. Actually, when adding the sum of values from Table 12.4 and compounding them at each period with the risk-free rate, we get the total result in Table 12.6, which shows that at each period, including at expiry, the call option value is exactly replicated. At the first period, the total replica is 66.6711 plus the cost of the collateral account 1.5234, for a total of 65.14774, which is exactly the call value in Table 12.2. At the end of the second period, we need to compound 1.5234 at the risk-free rate (0.10) and sum it to the cost for the second period (2.6059). By adding this total cost to the replicated value of the option (9.9420) we finally get the total replication value of 5.6604, once again the same as in Table 12.2. By the same token we can also derive the total replication value at expiry for the two cases of moneyness.

Table 12.6. Call replica including the cost to finance the collateral account

12.1.2 The replicating portfolio in continuous time

Now we extend the binomial approach we sketched above to a continuous and more general setting. Assume the underlying asset follows dynamics of the type:

The underlying has a continuous yield of yt and volatility σt.

The dynamics of the contingent claim are derived via Ito's lemma:

where we used the operator ![]() a· defined as:

a· defined as:

Moreover, we will also set ![]() in what follows. The dynamics of the cash collateral account are defined as

in what follows. The dynamics of the cash collateral account are defined as

where the first part on the left-hand side is variation of collateral dCt = γdVt, equal to fraction γ of variation of the NPV of the contract (the initial value of the collateral account is equal to the collateral C0 = C = γV0); the second part on the left-hand side is the amount of interest produced by the collateral during period dt, given the collateral rate ct. We denote the funding/investment rate by rt. The collateral account can be seen as a bank account (actually, it is a bank account), so that receiving cash collateral means being short the collateral account (such as when shorting a bond and receiving cash). At the end the collateral account (i.e., collateral plus interest) is returned to the transferor (at the same time the final payoff of the contingent claim is received by the transferee).

Remark 12.1.1. It is worth stressing the difference between “collateral” and “collateral account”. Collateral is posted by the party for whom the contract has a negative value, to protect the other party against the risk of default. The collateral account is the sum of collateral received by the party for whom the contract has a positive value, plus the interest it generates, which the receiving party has to pay to the other side.

Evolution of the cash account of a bank is deterministic and equal to:

where, as was the case with the cash collateral account, being short B means receiving cash.

At time 0, the replication portfolio in a long position in derivatives V that is cash-collateralized is set up. It comprises a given quantity of the underlying asset and of the bank account such that their value equals the starting value of the contract and of the collateral:

We have to find a trading strategy {αt, βt} such that it satisfies the following well-known conditions:

- Self-financing condition: No other investment is required to operate the strategy besides the initial one:

- Replicating condition: At any time t the replicating portfolio's value equals the value of the contract and of the collateral:

for t ∈ [0, T].

The way in which the replicating portfolio evolves can be written as:

On the other hand:

Remark 12.1.2. Although evolution of the collateral is equal to fraction γ of the value of contract Vt (i.e., dCt = γdVt), the collateral account Ct also generates an additional cash flow equal to collateral rate ct times collateral amount Ct (i.e., ctCtdt). We added these interest amounts when computing variation of the contract value and of the collateral on the left-hand side of (12.18). We are interested in variation of the collateral account – not simply the collateral – since the strategy needs to replicate the former and not just the latter.

Equating (12.17) and (12.18) and imposing self-financing and replicating conditions, we get:

We can determine α and β such that the stochastic part in (12.19) is cancelled out:

Substituting in (12.19):

Let us split (12.22) in two parts. The first is a standard PDE under the risk-neutral argument:

The second part is more unusual:

It shows how a collateral account evolves under a real world measure by equating the cost of the bank account used to finance it.

Equation (12.22) has a solution that can be found by means of the Feynman–Kac theorem:

Keeping in mind the fact that the collateral at expiry will be paid back to the counterparty who posted it, CT = 0, we have:

![]()

so that equation (12.25) can be written as:

Equation (12.26) states the same result derived in a binomial setting above: a collateralized claim is equal to the value of an otherwise identical non-collateralized claim, plus the present value of the cost incurred to finance the collateral, or LVA:

![]()

Note that we have not introduced any credit risk until now, so LVA cannot be confused with any adjustment due to the risk of default. On the other hand, it is still possible to derive an arbitrage-free price when the risk-free rate and collateral rate are different, something counterintuitive at first sight.

Recalling that Ct = γVt, equation (12.22) can be equivalently decomposed as:

The solution to (12.27) as a result of applying the Feynman–Kac theorem is:

The second part on the right-hand side is nil, since as before:

We have added the dependency of the value of the claim on the underlying price, whose drift is indicated as superscript characters. Thus, we have perfect analogy with the discrete case examined above.

When the deal is fully collateralized (i.e., γ = 100%), the discount rate in equation (12.29) collapses to collateral rate ct, which is a well-known result (see, amongst others, [69], [89] and [105]). We think equation (12.26) offers more insight. Actually, discounting by means of the collateral rate is a good way of using an effective rate to reproduce the effects of risk-free discounting and LVA. Should we want to disentangle the effects, however, then we should resort to (12.29). For example, in a dealing room correct evaluation of the LVA allows liquidity costs related to collateralization on relevant desks to be correctly allocated. If a collateral desk exists, LVA can be the compensation it receives for managing a given deal, whereas the trading desk closing the deal will be left to manage just the risk-free value of the contract.

12.1.3 Pricing with a funding rate different from the investment rate

Let us assume the operator of the replication strategy is a bank. The difference between the investment and funding rate is due mainly to credit factors (barring the trivial bid/ask factor and liquidity premiums), so that when considering rates actually paid or received by the bank, we should also model default. Nevertheless, this is not necessary since we are assuming that pricing is operated from the bank's perspective.

Actually, the funding rate rF that a bank has to pay, when financing its activity, should just be considered a cost from its own perspective, on the basis of the going concern principle. On the other hand, from the lender's perspective, the spread over the risk-free rate paid by the bank, is the remuneration for bearing the risk of default of the borrowing bank.7

When the bank sells a bank account, it will pay interest rF on received funds until maturity; conversely, when the bank buys a bank account, we assume there is a default risk-free borrower paying risk-free rate r. Evolution of the bank account in (12.13) becomes:

where ![]() and 1{} is an indicator function equal to 1 when the condition at the subscript is verified. If quantity β of the bank account is negative (i.e., the bank borrows money) then the bank account grows at funding rate

and 1{} is an indicator function equal to 1 when the condition at the subscript is verified. If quantity β of the bank account is negative (i.e., the bank borrows money) then the bank account grows at funding rate ![]() ; when quantity β is positive (i.e., the bank lends money) the bank account grows at risk-free rate rt.

; when quantity β is positive (i.e., the bank lends money) the bank account grows at risk-free rate rt.

If a risk-free borrower does not exist such that we actually have to buy bank accounts issued by other defaultable banks, then we can invest at rate rB > r, and the difference between the two rates is remuneration for credit risk. The expected return earned on the investment will be in any case risk-free rate r. Default of the counterparty, to whom the bank lends money, will affect the performance of the replication strategy of the contingent claim in any event, so that counterparty credit risk should be eliminated or mitigated whenever possible. We will come back to this issue later.

Assuming that the funding rate is the risk-free rate plus spread ![]() , we can write the rate at which bank account interest accrues as:

, we can write the rate at which bank account interest accrues as:

Replacing the risk-free rate rt with ![]() in equation (12.22), we get:

in equation (12.22), we get:

From (12.32) we can easily derive two ways to express the value of the contingent claim at time 0 equivalent to formulae (12.26) and (12.29), respectively, as:

and

Equation (12.33) breaks the value of the collateralized contract down as the sum of an otherwise identical non-collateralized deal and of LVA.

To get even more insight and allow for further decomposition useful when allocating revenues and costs within a dealing room, we rewrite equation (12.32) as:

The solution to (12.35) is:

where VNC is the price of a non-collateralized contract assuming no funding spread and LVA is liquidity value adjustment originated by the difference between the collateral and risk-free rate:

and finally FVA is funding value adjustment due to the funding spread and paid to replicate the contract and the collateral account:

where β has been defined above and FVA is a correction to the risk-free value of the non-collateralized contract, which has to be (algebraically) added to the LVA correction. We define it as:

Definition 12..2. FVA is the discounted value of the spread paid by the bank over the risk-free interest rate to finance the net amount of cash needed for the collateral account and the underlying asset position in the dynamic replication strategy.

It is interesting to break total FVA down into its components: this decomposition is not essential as far as pricing is concerned, but it is very useful within a dealing room to charge the desks involved in trading (we will dwell more on this later). Let us now isolate the initial part of total FVA due to the funding cost of the replication strategy of the premium and the collateral:

and the second part relating to the funding cost borne to carry the position of the underlying asset in the replication strategy:

Hence, total funding value adjustment is FVA = FVAP + FVAU. Since the indicator function 1{β<0} appears in both components, the FVA of individual components takes the net funding need into account at the financial institution level. Thus, single trading desks also enjoy funding benefit at an aggregated level.

For example, consider the FVA for the cost borne to fund the underlying asset's position: the derivatives desk should pay the funding costs when it has a positive position, but this cost is paid only if the net amount of the bank account is negative (β < 0). When the underlying asset's position is positive but the net amount in the bank account is positive (β > 0), the derivatives desk will not be charged for any funding cost, although it actually requires funds to buy the asset.

We are now in a position to analyse five different cases:

- Let us assume we have to replicate a contingent claim that has a constant positive-sign NPV (e.g., a long European call option) with a constant positive-sign Δt. Since Vt − Ct − ΔSt is always negative (implying borrowing), the total amount of bank account β is always negative, implying that we always have to borrow money in the replica at rate rF. The pricing equation (12.35) then reads:

Although the decomposition in (12.36) still applies, pricing can be performed very simply by means of an effective discount rate:

So we can simply replace the risk-free rate with the funding rate paid by the bank and perform the same pricing as when lending and borrowing rates are equal. Equation (12.42) is a very convenient way of computing the price at 0 of the contracts, but is of little use in allocating its components to the different desks of the bank.

- When the same (as in point 1) contingent claim (constant positive-sign NPV and Δ) is short, the underlying asset has to be sold in the replication strategy as well, which implies that β > 0 and that the bank always has to invest at the risk-free rate. The pricing formula will be as in formula (12.26) (with reversed signs since we are selling the contract). In this case FVA will be nil. An example of this claim is a short European call option.

- Let us now assume that the contingent claim has a constant positive-sign NPV, but its replication implies a negative position in the underlying asset (e.g., a long European put option), then once again we have β > 0 at any time. The pricing formula is (12.26) in this case too (i.e., the same as in the case with no funding spread).

- If the NPV has a constant negative sign and the replica entails a long position in the underlying (e.g., short European put option), then the total amount of bank account β is always negative, implying that we always have to borrow money in the replica at rate rf. The pricing formula is (12.42) (as in point 1).

- Finally, if the NPV has a constant positive or negative sign and the Δ can flip from one sign to the other, then it is not possible to determine the sign of amount β of the bank account throughout the entire life of the contract. In this case the pricing formula (12.35) cannot be reduced to a convenient representation as in the cases above, and very likely has to be computed numerically. Examples of contracts with non-constant sign Δ are exotic options, such as reverse knockouts.

From the analysis above it is also clear that when the contract is fully collateralized, the effective discount rate is just the collateral rate, whereas the drift rate of the asset can be either the risk-free rate or the funding rate depending on whether the bank account always preserves, respectively, a positive or negative sign until expiry.

Example 12.1.2. We now show a simple example of how these ideas can be put into practice for a European call option on an underlying asset that could be an equity, an FX spot rate or a commodity. Typically, the model used to price options in these cases is the standard Black and Scholes one:

where N() is the normal cumulated distribution function, F = Se(r−y)T is the forward price and:

Equation (12.43) valuates a call expiring at T, struck at K, when the underlying spot price is S.

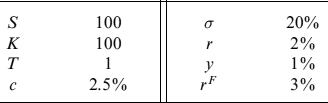

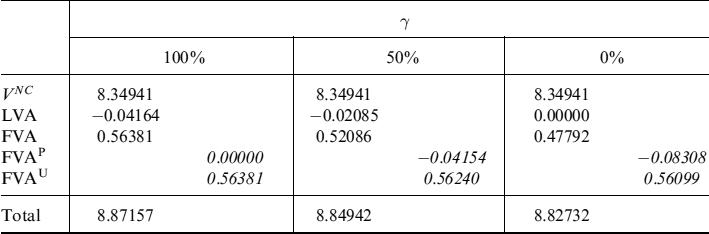

Assume we want to price the call option with the input data in Table 12.7. Since a European call option is a contract of the type shown in point 1 of our list, decomposition of the total value into the several components can be done withut computing the integral in the definition of LVA and FVA.

Actually, the risk-free non-collateralized value of the call (with risk-free rate drift to set the forward price) can immediately be computed as:

VNC = VNC−RF−RD = C(S, K, T, σ, r, y, r)

Table 12.7. Input data for a European call option

The total adjustment of a collateralized option, keeping in mind funding costs both in the discounting and in the drift of the asset to set the forward price, is:

Superscript C/NC stands for collateralized/non-collateralized, RF/FU for risk-free/funding rate discounting and RD/FD for risk-free/funding rate drift.

The quantity TA can be decomposed as follows:

Now, LVA is represented by the third line of equation (TA) and can be computed by the Black and Scholes formula:

Total FVA is represented by the first two lines of equation (TA); namely, the difference between the collateralized option, discounted by the funding rate and drift equal to the funding rate, and the non-collateralized option, discounted by the risk-free rate and drift equal to the risk-free rate:

FVA = VC−FU−FD − VC−RF−RD

We can break total FVA down by recognizing that FVAU (i.e., FVA due to the underlying asset) is the difference in the first line of equation (TA):

FVA due to the premium and collateral is:

In Table 12.8 we show decomposition of the total option value into the components examined for different percentages γ of collateralization of the contract's NPV. It is quite obvious that for the non-collateralized contract (γ = 0%) LVA is nil. Note also that the total values can be computed straightforwardly via formula (12.42), clearly obtaining the same result. Nevertheless, with this slightly longer procedure we are able to exactly disentangle the different cost contributions.

Table 12.8. Decomposition of the call option value into the risk-free, LVA and FVA components

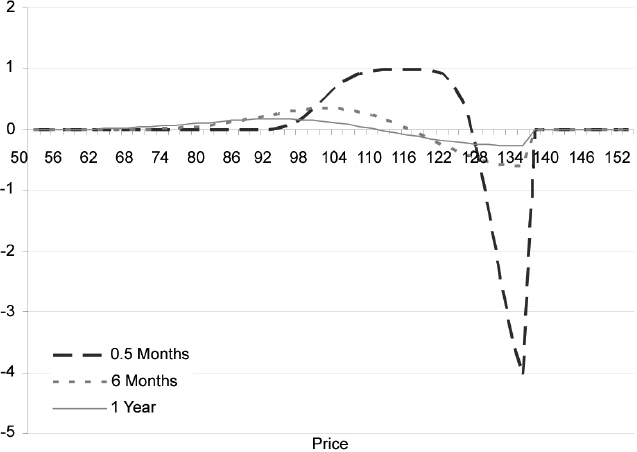

Figure 12.1. Delta of an up-and-out call option with different times to maturities as a function of the price of the underlying asset. The barrier is at 135 and all other data are as in Example 12.1.2

Example 12.1.3. Let us now assume we have the same data as in Example 12.1.2 and that the European call is no more plain vanilla, but has a barrier set above the strike level at 135. The option is an up-and-out call and can be priced in a closed-form formula in a Black and Scholes economy (see [44] for a thorough discussion of barrier options and for pricing formulae, with a focus on the FX market).

In this case it is not possible to use the decomposition used in Example 12.1.2 because the Δ of the up-and-out call can flip from one sign to the other, depending on the level of the underlying asset. We are now in the fifth case of the above list. In Figure 12.1 we depict the Δ as a function of the price of the underlying asset, for three different times to maturity, progressively approaching the contract's expiry: the plots simply confirm what we have written. In this case we resort to a numerical integration of formulae (12.37) and (12.38).8

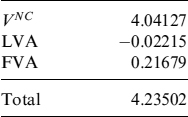

Table 12.9. Decomposition of the value of an up-and-out call option in its non-collateralized risk-free value, LVA and FVA

Decomposition of the price is given in Table 12.9 only for the case when the contract if fully collateralized (γ = 100%). This means that FVA contains only the component related to financing of the underlying asset. The lower amount of both LVA and FVA with respect to the corresponding European plain vanilla call just examined is easily justified.

12.1.4 Funding rate different from investment rate and repo rate

We now introduce the possibility of lending and borrowing money (or, alternatively, the underlying asset) via a repo transaction. This is actually the way traders finance and buy the underlying asset (typically in the stock market), by borrowing money and lending the asset as collateral until expiry of the contract.

A repo transaction can be seen as a collateralized loan and the rate paid is lower than the unsecured funding rate of the bank, since in case of default of the borrower, the asset can be sold to guarantee the (possibly only partial) recovery of the lent sum. The difference between repo rate rE and the risk-free rate is due to the fact that the underlying asset can be worth less than the lent amount when default occurs: so volatility of the asset and probability of default both affect the repo rate.

We assume that the repo rate is the same when borrowing money or lending money against the underlying asset (repo and reverse repo). This means that we are assuming that the two banks involved in the transaction have the same probability of default with the same recovery rate in the event of default. We will investigate replication costs and the pricing formulae for four of the five possible cases in the list above.

A repo transaction is the proper way to finance buying the underlying asset in the replication strategy. On the other hand, if we really want to consider the actual alternatives that are available to a trader to invest received sums in a less credit-risky way, reverse repo seems an effective option in most cases. So, as far as the buying and selling of the underlying asset are concerned, we go back to the case when there is no asymmetry between investment (lending) and the funding rate, although the risk-free rate is replaced by the repo rate. The amount to be lent/borrowed via the bank account is now:

whereas the quantity αt = Δt of the underlying asset is repoed/reverse-repoed, thus paying/receiving interest ![]() . Replacing these quantities in equation (12.22), we get:

. Replacing these quantities in equation (12.22), we get:

The solution to (12.45) is:

where, as usual, VNC is the price of the non-collateralized contract assuming no funding spread and repo, LVA is liquidity value adjustment due to the collateral agreement:

![]()

and FVA is funding value adjustment:

FVA in this case is split into the funding cost needed to finance the collateral ![]() and the spread of the repo rate over the risk-free rate

and the spread of the repo rate over the risk-free rate ![]() paid on the position of amount Δt of the underlying asset.

paid on the position of amount Δt of the underlying asset.

To better understand how total FVA is built, we split formula (12.47) into two components: the first is FVAP, the cost borne to fund the premium and the collateral (it is the same as in (12.39)). The second part refers to the repo cost to buy or sell the underlying asset to replicate the payoff:

Furthermore, it is possible in this case to rewrite (12.46) in a more convenient fashion for computational purposes:

Formula (12.49) applies to the five cases analysed in the previous section: the discount factor depends on the sign of the bank account needed to fund the collateral account, whereas the drift of the underlying asset is always the repo rate rE.

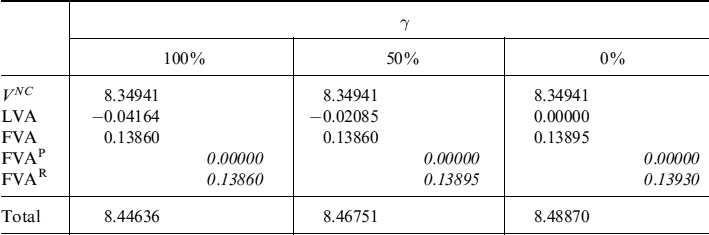

Example 12.1.4. We revert to Example 12.1.2 for the pricing of a European call option, but we now assume that the bank can buy or sell the underlying asset via repo transactions. We ascertain how the components of total value change in this case. We still use the same inputs as in Table 12.7, but we add to them the repo rate set at rE = 2.25%, which is lower than the unsecured funding rate rF = 3%, but higher than the risk-free rate r = 2% to account for volatility of the collateral (the underlying asset) and the possibility of a smaller collateral value on default of the borrower (the bank).

Let us exploit once again the fact that a European option is a type of contract that falls in the first case analysed above and keep the same considerations we made in Section 12.1.2.

Table 12.10. Decomposition of the value of the call option into the risk-free, LVA and FVA components when the underlying asset is traded via repo contracts

We define LVA as above:

and the two components of FVA as:

Decomposition of total option value into the different components for different percentages of collateralization is given in Table 12.10.

12.1.5 Interest rate derivatives

As far as the pricing of interest rate derivatives is concerned, we have to consider the credit issue as being critically important. Despite analysing replication of a contingent contract with repo transactions, which virtually eliminates credit risk, or at least makes it negligible, unfortunately, it is not possible to replicate interest rate derivatives with such a low level of credit risk, since the replication strategy involves unsecured lending (besides the borrowing) as part of the underlying itself. For example, without credit risk, a FRA can be replicated by selling/buying a shorter maturity bond and buying/selling a longer maturity bond. With credit risk this strategy is clearly flawed since the counterparty to whom we lent money can default before expiry of the bond.

This means that in practice basic interest rate derivatives are no longer real derivatives, but primary securities that cannot be replicated by means of other primary securities (e.g., bonds). The derivative contract can be made credit risk-free by a collateral agreement, but we can no longer set up a strategy to replicate the payoff and evolution of the collateral account, as we have done above for derivatives on different assets. The implications of being unable to implement a replication strategy become apparent by analysing a couple of contracts: a forward rate agreement (FRA) and an interest rate swap (IRS).

Forward rate agreement

Let us introduce a setup to price interest rate derivatives under collateral agreements.9 Let us consider times t, Ti−1 and Ti, t ≤ Ti−1 < Ti. The time t forward rate is defined as the rate to be exchanged at time Ti for the Libor rate Li(Ti−1) = L(Ti−1, Ti) fixed at time Ti−1, in a FRA(t; Ti−1, Ti) contract, so that the contract has zero value at time t.

In the absence of credit risk (i.e., in a single-curve environment), the forward rate can be determined via a portfolio of long and short zero-coupon bonds. The absence of arbitrage also implies the existence of a single, risk-free, discounting curve. Let us assume we have a discount curve denoted by D; we then have:

The FRA fair forward rate can be set according to definition of the contract:

Let us now assume we are in a credit-risky economy. Selling and buying bonds does not allow replicating the FRA payoff since it is always possible that the counterparty to whom we lent money defaults. The forward that is being traded in the market in this case should be simply considered as the expected value of Libor at the fixing time. If we accept that market quotes refer to trades between counterparties with a collateral agreement, then we can quite safely assume that the expected value is taken under a risk-free bond numeraire. The pricing formula is similar to the one presented above for contracts on other underlying assets, although in this case it is not derived from a replication argument, rather it is an assertion:

that is, the expected Libor rate under the Ti forward measure of the value of the contract at expiry Ti−1 plus LVA. In (12.52) Ti = Ti − Ti−1.

The LVA in this case is the present value of the difference between the risk-free rate ![]() and the collateral rate Oj(t), fixed at date tj−1 and valid until date tj, applied to fraction γ of the value of contract FRA(tj; Ti−1, T2) for a total of N days between t and the forward settlement T1, so that tN = T1:

and the collateral rate Oj(t), fixed at date tj−1 and valid until date tj, applied to fraction γ of the value of contract FRA(tj; Ti−1, T2) for a total of N days between t and the forward settlement T1, so that tN = T1:

where ![]() is the difference in the fraction into which the year is split between two rebalancing times of the collateral: one day in our case. Formula (12.52), given the definition of LVA in (12.53), is recursive. We assume that market quotes for FRAs refer to the case when LVA is nil. This means that the collateral rate is supposed to be risk-free rate LD(t; tj−1, tj) = O(t; tj−1, tj), for all j, which is not unreasonable since standard CSA agreements between banks provide for remuneration of the collateral account at the OIS (or equivalent for other currencies) rate. The OIS rate can also be considered as a virtually risk-free rate or at least as embedding a negligible spread for default risk. If this holds true, then equation (12.52) reads as:

is the difference in the fraction into which the year is split between two rebalancing times of the collateral: one day in our case. Formula (12.52), given the definition of LVA in (12.53), is recursive. We assume that market quotes for FRAs refer to the case when LVA is nil. This means that the collateral rate is supposed to be risk-free rate LD(t; tj−1, tj) = O(t; tj−1, tj), for all j, which is not unreasonable since standard CSA agreements between banks provide for remuneration of the collateral account at the OIS (or equivalent for other currencies) rate. The OIS rate can also be considered as a virtually risk-free rate or at least as embedding a negligible spread for default risk. If this holds true, then equation (12.52) reads as:

so that we retrieve the standard result, as in [89], that the FRA fair rate is the expected value of Libor at the settlement date of the contract under the Ti forward risk measure at expiry:

Despite assuming that the market FRA settles at Ti, according to market conventions it actually settles the present value of the Ti payoff at Ti−1. The market FRA fair rate is then different from the “theoretical” rate in (12.55), since the latter should be corrected by means of convexity adjustment as discussed in [91]. The adjustment is nevertheless quite small (fraction of a basis point) and can be neglected under typical market conditions, so we will not consider it.

When the collateral agreement provides for remuneration of the collateral that is different from the OIS rate, then we have LVA ≠ 0, and the FRA fair rate has to be valued recursively. Let ![]() be the spread between the daily risk-free rate and the collateral rate and assume it is a stochastic process independent of the value of the FRA; we can rewrite equation (12.53) as:

be the spread between the daily risk-free rate and the collateral rate and assume it is a stochastic process independent of the value of the FRA; we can rewrite equation (12.53) as:

The second expectation in (12.56) is ![]() , so that we finally get:

, so that we finally get:

In much the same way, we can derive the FVA for an FRA: let ![]() be the funding rate paid by the bank (same notation as above). When financing the collateral (i.e., when the NPV of the contract is negative to the bank), it has to pay this rate to fund the collateral it has to post. In the opposite situation (i.e., when the NPV is positive), the bank invests the collateral received at the risk-free rate, paying the collateral rate.

be the funding rate paid by the bank (same notation as above). When financing the collateral (i.e., when the NPV of the contract is negative to the bank), it has to pay this rate to fund the collateral it has to post. In the opposite situation (i.e., when the NPV is positive), the bank invests the collateral received at the risk-free rate, paying the collateral rate.

Let ![]() be the funding spread over the risk-free rate and assume it is not correlated with the NPV of the FRA. FVA is then:

be the funding spread over the risk-free rate and assume it is not correlated with the NPV of the FRA. FVA is then:

where E[X−] = E[min(X, 0 )]. It is easy to check that:

where Floorlet(tj; Ti−1, Ti, K) is the price of a floorlet at time tj, expiry at Ti−1, settlement at Ti, with strike K. If the bank has a short position in the FRA, then FVA is

where Caplet(ti; Ti−1, Ti, K) is the price of a caplet and the arguments of the function are the same as for the floorlet.

The total value of the FRA is:

In any case, the fair rate making the value of the contract at inception zero, has to be computed recursively.

Interest rate swap

Let us now consider an IRS whose fixed leg pays a rate denoted by K on dates ![]() . The present value of these payments is obtained by discounting them with discount curve D. The floating leg receives Libor fixings on dates Ta, …, Tb and the present value is also obtained by discounting with discount curve D. We assume that the set of floating rate dates includes the set of fixed rate dates. The value at time t of the IRS is:

. The present value of these payments is obtained by discounting them with discount curve D. The floating leg receives Libor fixings on dates Ta, …, Tb and the present value is also obtained by discounting with discount curve D. We assume that the set of floating rate dates includes the set of fixed rate dates. The value at time t of the IRS is:

where LVA is defined as:

where ![]() . LVA in this case is once again the difference between the risk-free rate and the collateral rate applied to fraction γ of the NPV, for a total of N days occurring between valuation date t and the end of the contract tN = Tb.

. LVA in this case is once again the difference between the risk-free rate and the collateral rate applied to fraction γ of the NPV, for a total of N days occurring between valuation date t and the end of the contract tN = Tb.

As far as swaps are concerned, we make the assumption that market quotes refer to the situation when LVA = 0, implying that the risk-free and collateral rates are the same. The market swap rate is then the level making the value of the contract at inception Ta zero:

When the risk-free and collateral rates are different, LVA can be evaluated in much the same was as the FRA. We then have:

The second expectation in (12.63) is ![]() , where Ea,b is the expectation taken under the swap measure, with the numeraire equal to annuity

, where Ea,b is the expectation taken under the swap measure, with the numeraire equal to annuity ![]() . So we can finally write:

. So we can finally write:

FVA can also be defined analogously with the FRA case and, using the same notation as above, we have:

We can make use of the option on swaps to express the second expectation in (12.65) as:

where Rec(t; Ta, Tb) is the price of a receiver swaption priced at time tj, expiry at Ta, on a swap starting at Ta and maturing at Tb, with strike K. If the bank has a short position in the IRS (i.e., it is a fixed rate receiver), then FVA is

where Pay(t; Ta, Tb) is the price of a payer swaption and the arguments of the function are the same as for the receiver.

Finally, the total value of IRS is:

At inception, the swap rate K = Sa,b(t) is the level that makes the value of the contract zero, which can be computed recursively from (12.66).10

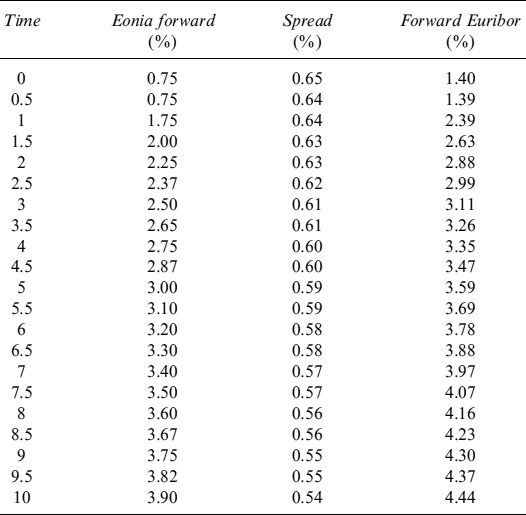

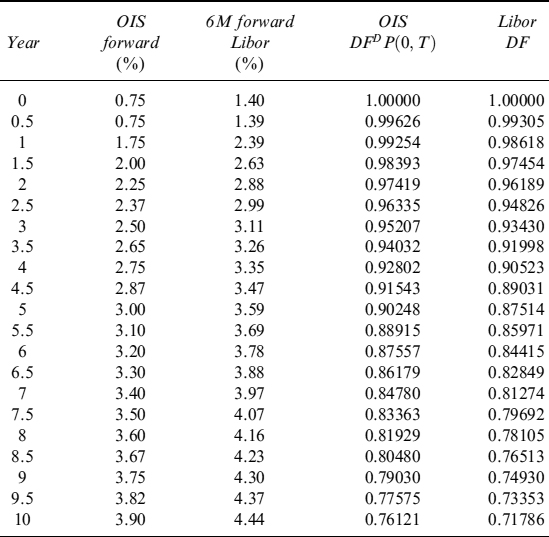

Example 12.1.5. Let us consider an IRS, assuming the risk-free rate is equal to the Eonia rate and Euribor forward fixings are at spreads over the Eonia rate. Yearly Eonia forward rates, spreads and Euribor forward rates are shown in Table 12.11.

Table 12.11. Yearly OIS forward rates and spreads over them for forward Euribor fixings

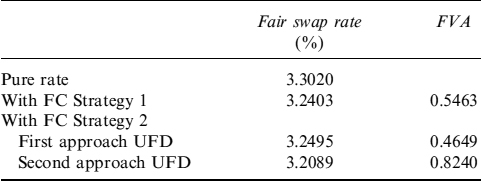

We price, under a CSA agreement with full collateralization (γ = 100%), a receiver swap whereby the bank pays the Euribor fixing semiannually (set at the previous payment date) and receives the fixed rate annually. Keeping market data in mind, the fair rate can easily be calculated by formula (12.62) and found to be equal to 3.3020. We also assume that the bank has to pay a funding spread of ![]() over the Eonia curve. Finally, we assume that collateral is remunerated at the Eonia rate.

over the Eonia curve. Finally, we assume that collateral is remunerated at the Eonia rate.

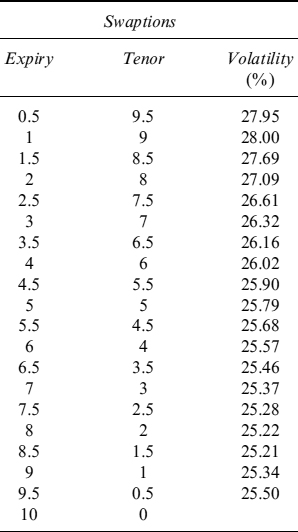

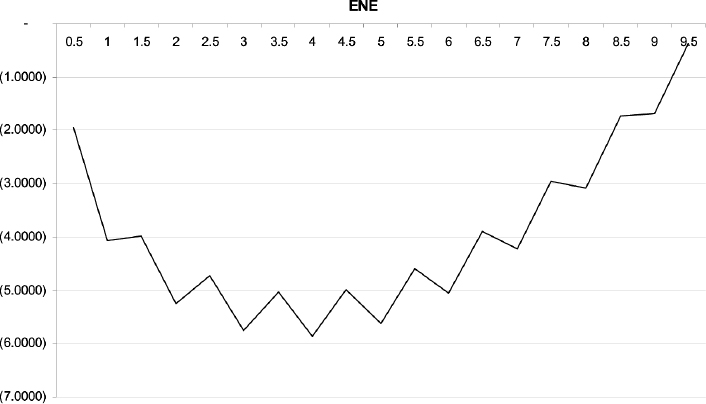

Under these assumptions, the LVA of the swap is nil, as is clear from its definition in (12.64). FVA is different from zero, since there is a funding spread. To compute the FVA in (12.65), we have to compute a portfolio of payer swaptions. To this end we make a simplifying assumption that the NPV of swaptions is constant between two Euribor fixing dates (i.e., it is constant over periods of six months). Swaptions can be computed by means of volatilities in Table 12.12 using a standard Black formula. It is then possible to plot the profile of the NPVs of swaptions, which is actually the (approximated) expected negative exposure (ENE) of the receiver swap (the profile is plotted in Figure 12.2).

The results are given in Table 12.13. FVA is quite small for a swap starting at-the-money, accounting for about half a basis point: an almost negligible impact on the fair swap rate including the funding costs. This rate should be set by a numerical search and is the rate making the value of the swap zero, given by the risk-free component plus FVA at inception.

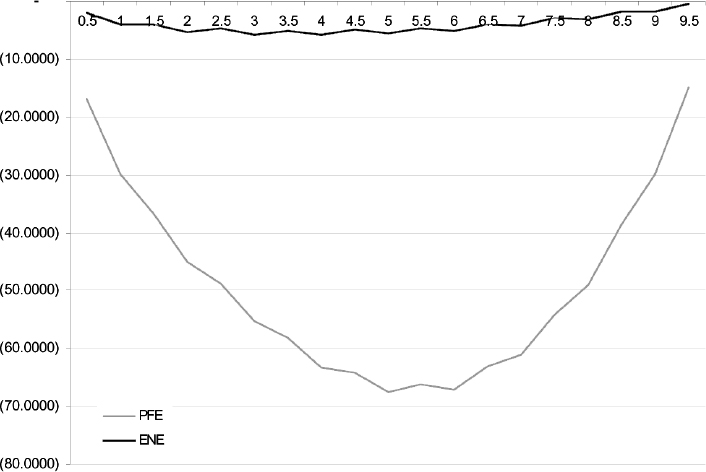

A more conservative FVA can be based on potential future exposure (PFE) rather than expected exposure as we did with ENE. PFE is computed in much the same way as ENE, but considering the level of the future swap rate set at a given confidence level instead of the forward level. We choose 99% as the confidence level.11 PFE is plotted in Figure 12.3 and the results are shown in Table 12.14. In this case, FVA is larger as a percentage of the notional and accounts for about 7 bps when included in the fair rate.

Table 12.12. Implied volatilities for the portfolio of swaptions used to replicate the ENE of the receiver swap

Figure 12.2. ENE of the receiver swap

Table 12.13. Fair swap rate, FVA and FVA-adjusted fair swap rate

| FVA | −0.0512% |

| Fair swap rate | 3.3020% |

| Swap rate including FVA | 3.3079% |

| Difference | 0.0059% |

Figure 12.3. PFE of the receiver swap

Table 12.14. Fair swap rate, FVA and FVA-adjusted fair swap rate using PFE

| FVA | −0.6265% |

| Fair swap rate | 3.3020% |

| Swap rate + collateral fund | 3.3728% |

| Difference | 0.0708% |

FVA is rather small when the swap starts and is at-the-money. It can become bigger and bigger as the NPV of the swaps evolves and becomes more negative, or it can become completely negligible as NPV increases.

12.2 PRICING OF COLLATERALIZED DERIVATIVE CONTRACTS WHEN MORE THAN ONE CURRENCY IS INVOLVED

In this section we complete the analysis conducted in Section 12.1 by investigating the valuation of collateralized derivative contracts when more than one currency is involved. This can happen for three reasons:

- The contract payoff is denominated in some currency YYY but collateral is posted in another currency XXX.

- The contract is written on an FX rate.

- The contract payoff depends on assets or market variables denominated in different currencies (e.g., a cross-currency interest rate swap).

In theory, many currencies could be involved, but in what follows we restrict our analysis to when only two currencies have to be considered. We analyse all the cases enumerated above and define liquidity value adjustments and funding value adjustments for collateralized contracts.

12.2.1 Contracts collateralized in a currency other than the payoff currency

Let us assume we have to value a contract whose underlying asset follows dynamics of type:

dSt = (µt − yt)Stdt + σtStdZt

The underlying has a continuous yield of yt and volatility σt and is denominated in a currency that we name “domestic” and refer to as YYY. There is also a foreign currency XXX and an exchange rate X = XXXYYY12 following the dynamics:

dXt = ηtXtdt + vtXtdWt

with dWtdZt = ρdt.

We want to replicate a derivative contract V written on S, which is collateralized continuously in XXX instead of YYY; the latter would normally be the case. Following the same approach outlined in Section 12.1, we build a portfolio replicating both the underlying and the collateral account.

The dynamics of the contingent claim are derived via Ito's lemma:

![]()

where we used operator ![]() a· defined as:

a· defined as:

Moreover, we will set ![]() in what follows. The dynamics of the cash collateral account are defined as

in what follows. The dynamics of the cash collateral account are defined as

![]()

The account is denominated in XXX as long as it earns the collateral rate cft; rft is the funding/investment rate in YYY. For the collateral account it is also true that:

Evolution of the YYY bank cash account is deterministic and equal to:

and evolution of the XXX bank cash account is:

At time 0, the replication portfolio in a long position in derivative V, YYY cash-collateralized, is set up with a given quantity of the underlying asset and of XXX and YYY bank accounts such that their value equals the starting value of the contract and of the collateral account:

As usual, we impose self-financing and replicating conditions to find quantities {αt, βt, θ}. We can write the way in which the replicating portfolio evolves as:

On the other hand:

Equating (12.70) and (12.71) we get:

We can determine α and β such that the stochastic part in (12.72) is cancelled out:

Substituting in (12.72):

We can express equation (12.74) in terms of YYY only by multiplying the second term by FX rate Xt and then we have:

where C is the collateral account converted in YYY units (we suppressed indication of the currency to lighten the notation).

It can be shown (see Section 12.1) that the solution to equation (12.75) is:

which is the same result as when the collateral is posted in YYY, with the only difference that the amount of the collateral account in YYY is multiplied by the difference between the risk-free rate and the collateral rate applied to the collateral amount in XXX units.

We can also denote the second part of the formula as the LVA, which is the present value of the cost incurred to finance the collateral in XXX units:

![]()

Recalling that Cft = γ(Vt/Xt)XXX, or Ct = γVtYYY, equation (12.75) has another solution:

In this equation we added the dependency of the value of the claim on the underlying price, whose drift is indicated by superscripts. In practice, we can use standard valuation formulae derived, for example, in a Black and Scholes economy by simply changing the discount rate: this will no longer be the only domestic YYY risk-free rate, there will also be a correction depending on collateralization percentage γ and on the foreign XXX risk-free and collateral rates.13

Remark 12.2.1. The value of a contract, collateralized in a currency different from the one in which the payoff is denominated, does not depend on the FX rate X, but on the risk-free and collateral rates of currency XXX, in addition to the risk-free rate of currency YYY.

Pricing with funding rate different from investment rate

Let us assume that the replication strategy is operated by an agent (say, a bank), for which the investment and funding rates are different, due mainly to credit factors. The bank pays funding rate rF when financing its activity in the domestic YYY currency; analogously, rfF is the rate that it pays when financing its activity in the foreign YYY currency. Evolution of the domestic bank account in (12.67) is:

where ![]() and 1{} is the indicator function equal to 1 when the condition at the subscript is fulfilled. The XXX bank account evolves as follows:

and 1{} is the indicator function equal to 1 when the condition at the subscript is fulfilled. The XXX bank account evolves as follows:

The funding rate can be written as the risk-free rate plus a spread:

and similarly for the foreign rate

Replacing risk-free rates rt and rft with ![]() and

and ![]() in equation (12.75), we get:

in equation (12.75), we get:

From (12.82) we can easily derive the two ways of expressing the value of the contingent claim at time 0 equivalent to formulae (12.76) and (12.77), respectively, as:

and

In equation (12.83) decomposition of the collateralized contract value is given as the sum of the otherwise identical non-collateralized deal and of LVA.

We would also like to isolate the effect due to the funding spread, so we introduce a further decomposition by rewriting equation (12.82) as:

The solution to (12.85) is:

where VNC is the price of the non-collateralized contract assuming no funding spread, LVA is the liquidity value adjustment originated by the difference between the collateral and risk-free rate:

and, finally, FVA is the funding value adjustment due to the funding spread, which is paid to replicate the contract and the collateral account:

where β is defined as above. FVA is the correction to the risk-free value of the non-collateralized contract that has to be (algebraically) added to the LVA correction. For a definition of LVA and FVA see [45].

We are now in a position to analyse five different cases:

- Let us assume a contingent claim with a constant positive-sign NPV (e.g., a long European call option) with a constant positive-sign Δt has to be replicated. In this case βt = Vt − ΔSt < 0 and θt = −Ct < 0 always (implying borrowing always takes place in both currencies). The pricing equation (12.85) then reads:

Although the decomposition in (12.86) still applies, pricing can be performed very simply by means of an effective discount rate:

So we can simply replace the risk-free rate with the funding rate paid by the bank and perform the same pricing as when lending and borrowing rates are the same.

- When the same contingent claim (constant positive-sign NPV and Δ) as in point 1 is sold, the underlying asset has also to be sold in the replication strategy, which implies that βt > 0 and that the bank always has to invest at the risk-free rate in YYY; the bank account in XXX, θt = −Ct, will always be positive as well. The pricing formula will be the same as in formula (12.77) (with reversed signs since we are selling the contract). In this case FVA will be nil. An example of this claim is a short European call option.

- Let us now assume that the contingent claim has a constant positive-sign NPV, but its replication implies a negative position in the underlying asset (e.g., a long European put option). So, once again we not only always have βt = Vt − ΔSt0 > 0, but also θt = −Ct < 0, implying that the bank has to borrow money in XXX. PDE (12.85) now reads:

Pricing can be performed via the compact formula:

In this case we replace the risk-free rate with the funding rate paid by the bank for XXX.

- If the NPV has a constant negative sign and the replica entails a long position in the underlying (e.g., short European put option), then the total amount of bank account βt = Vt − ΔSt < 0 is always negative, implying that the bank always has to borrow money in the replica at rate rF in YYY; since θt = −Ct > 0 always, the bank will invest the collateral at the risk-free rate rf. The pricing formula is derived similarly to (12.92) and is:

- Finally, if the NPV has a constant positive or negative sign and the Δ can flip from one sign to the other, then it is not possible to determine the sign of amount βt of the bank account throughout the entire life of the contract, although it is always possible to determine whether θt is always positive or negative. In this case pricing formula (12.85) cannot be reduced to a convenient representation as in the cases above and has to be done so numerically.

Funding rate different from investment rate and repo rate

We mentioned in Section 12.1 that the proper way to finance buying of the underlying asset in the replication strategy is through a repo transaction. On the other hand, if we really want to consider the actual alternatives available to a trader to invest received sums in a less credit-risky way, reverse repo seems an effective option in most cases. The amount to be lent/borrowed via domestic and foreign bank accounts is now:

where quantity αt = Δt of the underlying asset is repoed/reverse-repoed, thus paying/receiving interest ![]() . Replacing these quantities in equation (12.75), we get:

. Replacing these quantities in equation (12.75), we get:

The solution to (12.94) is:

where, as usual, VNC is the price of the non-collateralized contract assuming no funding spread or repo, LVA is the liquidity value adjustment due to the collateral agreement:

![]()

and FVA is the funding value adjustment:

FVA is split into the funding cost needed to finance collateral ![]() and the spread of the repo rate over the risk-free rate

and the spread of the repo rate over the risk-free rate ![]() paid on the position of amount Δt of the underlying asset in this case.

paid on the position of amount Δt of the underlying asset in this case.

To better understand how total FVA is built, we split formula (12.96) into two components: the first is FVAP, the cost borne to fund the premium and the collateral, and is the same as in (12.88). The second part refers to the repo cost to buy or sell the underlying asset to replicate the payoff:

Furthermore, in this case it is possible to rewrite (12.95) in a more convenient fashion for computational purposes:

Formula (12.98) is applicable to the five cases analysed in the previous section: the discount factor depends on the sign of the bank account needed to fund the collateral account, whereas the drift of the underlying asset is always repo rate rE.

12.2.2 FX derivatives

We now want to compute the value to the bank of an FX derivative contract: it is a function of FX rate X and of time V(Xt, t). We start with a simple forward contract, named outright in the FX market.

Collateral posted in numeraire currency

When collateral is posted in numeraire currency YYY, the case examined in Section 12.1 for a general derivative contract is applicable, although here we need to replace the underlining asset with the exchange rate. We focus only on the more realistic case of different borrowing/lending rates and apply the replication argument as before.

The difference between FX trades and trades in other securities (say, equities) is that, in the case of FX, we are actually buying money in some currency by paying a price in another currency, and money received can be invested in a bank account that we assume to be default risk free.14 So by buying, for example, foreign currency XXX (which we assumed to be the base), the bank can invest this amount in a XXX-denominated bank account. On the other hand, when the bank needs to short the base currency to buy numeraire currency, it has to borrow money in XXX.

The evolution of contract V(Xt, t) = Vt, according to Ito's lemma, is:

where

The replicating portfolio comprises at time t a given amount αt of the base currency XXX worth Xt and a given amount of cash βt borrowed or invested in YYY. The portfolio must equal the value of the FX derivative at time 0:

Considering that α units of XXX are either invested in or borrowed from a bank account depending on the sign of α, evolution of the replicating portfolio is:

where ![]() and denomination in YYY has been omitted in the last line. Setting

and denomination in YYY has been omitted in the last line. Setting ![]() and βt = (Vt − Ct − ΔtXt)/Bt, and following the same mathematical passages as in Section 12.1, we come up with the PDE:

and βt = (Vt − Ct − ΔtXt)/Bt, and following the same mathematical passages as in Section 12.1, we come up with the PDE:

From (12.103) we can easily derive the two ways of expressing the value of the contingent claim at time 0:

and

We have explicitly indicated the drift that the FX rate must have under the bank's replication measure. In equation (12.104) decomposition of the value of the collateralized contract is given as the sum of the otherwise identical non-collateralized deal and of LVA.

We introduce a further decomposition that can be used to allocate revenues and costs within a dealing room. We rewrite equation (12.103) as:

The solution to (12.106) is:

where VNC is the price of the non-collateralized contract assuming no funding spread, LVA is the liquidity value adjustment originated by the difference between the collateral and risk-free rates:

and, finally, FVA is the funding value adjustment due to the funding spread and paid to replicate the contract and the collateral account:

FVA can be decomposed according to the spread paid in YYY:

and the funding adjustment due to the spread paid in XXX:

Collateral posted in base currency

When collateral is posted in base currency XXX, we can apply the results derived above for a general derivative contract to an FX derivative contract. The replicating portfolio is built as follows

and its evolution is:

Choosing βt = (Vt − ΔtXt)/Bt and θ = − (Cft − Δt)/BftXXX = −(Ct − ΔtXt)/BftYYY, we derive the following PDE:

The solution is

Another solution to (12.114) is:

where VNC is the price of the non-collateralized contract assuming no funding spread, LVA is the liquidity value adjustment originated by the difference between the collateral and risk-free rates:

and, finally, FVA is the funding value adjustment due to the funding spread, which is paid to replicate the contract and the collateral account:

Value of an FX forward (outright) contract

Let us assume collateral is posted in YYY. A (long) FX forward contract, or outright, struck at level X has a terminal value:

so that applying the compact formula (12.105)

The value at inception of the contract is nil: if we disregard for the moment all the adjustments due to the default risk of the bank and its counterparty, we can price the contract and find level X = XC(t, T) that makes the value at the beginning of the contract zero with formula (12.104). If the bank needs to replicate a long position in the outright contract, then the outright price can easily be shown to be:

On the other hand, when the bank wants to replicate a short position, the outright price is:

Remark 12.2.2. In both cases, collateralization and, hence, the collateral rate do not affect the fair level of the outright contract, although LVA contributes to the value of the contract when the outright is seasoned and no longer at-the-money as at inception. On the contrary, funding spreads paid on either currency (YYY or XXX) enter into the formula and are crucial to defining both the replication value of the contract to the bank and the fair level.

Remark 12.2.3. Equation (12.106) makes it abundantly clear that we are still within a risk-neutral framework, where everything is discounted using the risk-free rate, and the drift of the FX rate process Xt is the difference between the numeraire and base currency: a standard result. Using PDE (12.103) leads to more convenient valuation formulae, but in our opinion makes it less clear how the value is composed or why it can be different to different parties, despite still working in a dynamic replication setting that produces a risk-neutral value.15

If collateral is posted in XXX, then the forward price is the level making the contract value at inception zero computed via PDE (12.114) whose solution can be written as the compact formula (12.115), so that

It is quite easy to check that both the long and short outright fair price level is the same as in formulae (12.121) and (12.122), so that XC(t, T) = XCf(t, T), with XCf the outright fair price at time t for maturity T when the collateral is posted in the base currency.

Remark 12.2.4. Although the fair level of the outright (FX forward) price is independent of the currency in which the collateral is posted, the value of the contract does depend on it. The values of two contracts one collateralised in the numeraire and the other in the base currency differ during their life, being equal (i.e., zero) only at inception and at expiry.

Replication with FX swap

The funding spread in both currencies can be strongly abated if the bank uses collateralized instead of unsecured lending. In the FX this can easily be achieved via an FX swap, which is in all respects equal to a repo traded in other markets. The FX swap is the sum of a spot contract plus an outright, but it can also be seen as the borrowing/lending of an XXX amount against collateral represented by the YYY amount.16

FX swaps for given expiry T are quoted in the market in points over the spot rate X, so that the level at which the outright is traded is defined as F(t, T) = X′ + p(t, T), where p(t, T) are the swap points prevailing at time t for an FX swap expiring at time T.17 The outright level also defines the FX swap implied rate, which mainly depends on the differential between the numeraire and the base currency, but there are other factors (even beyond credit risk) that determine the generally defined cross-currency basis. The implied FX swap (continuous) rate is defined as:

Using an FX swap to replicate the FX derivative contract and assuming for the moment that it is CSA-collateralized in YYY, formula (12.102) is modified as follows:

Setting ![]() and βt = (Vt − Ct), the evaluation PDE becomes:

and βt = (Vt − Ct), the evaluation PDE becomes:

The solution to (12.126) is:

where, again, VNC is the price of the non-collateralized contract on exchange rate X, assuming no funding spread and repo rate; LVA is the liquidity value adjustment due to the collateral agreement:

![]()

and FVA is the funding value adjustment:

where FVA is split into two parts: the funding cost needed to finance collateral ![]() and the spread of the repo rate over the risk-free rate

and the spread of the repo rate over the risk-free rate ![]() paid on the position of amount Δt of the underlying asset.

paid on the position of amount Δt of the underlying asset.

It is possible to rewrite (12.127) in a more convenient fashion for computational purposes:

The FX swap can be used to replicate the outright contract shown above: in the end the FX swap is just the replication strategy of an outright operated with a single counterparty, thus minimizing loss given defaults and hence the spread paid. Keeping in mind that the FX swap, being a derivative contract itself, is CSA-collateralized, we also get the same cash flow profile for both the outright and the FX swap, so that funding spreads should not be considered in the evaluation process. The replica of the contract is then independent of the creditworthiness of the replicator bank. This means that, in practice, they are the same contract when a CSA agreement is in operation and that the outright fair price is just the FX swap price:

The dynamics for the FX rate, when replication is operated via the FX swap, are:

Let us now see what happens if replication is performed using a repo contract and the collateral is posted in the base currency (XXX). Equation (12.113) modifies as follows:

Setting βt = Vt/Bt and θ = −Cft/BftXXX = − Ct/BftYYY, we derive the following PDE:

where ![]() . The solution to (12.133) is:

. The solution to (12.133) is:

where, as usual, VNC is the price of the non-collateralized contract on the exchange rate X, assuming no funding spread and repo rate, LVA is the liquidity value adjustment due to the collateral agreement:

![]()

and FVA is the funding value adjustment:

with ![]() as above. A compact solution in this case is:

as above. A compact solution in this case is:

It is clear that the currency of the collateral is immaterial when a FX swap is used to replicate a forward contract, since from (12.136) we can derive the fair outright level when collateral is posted in the base currency, which is the same as in (12.130), so that: XCf = XC.

12.2.3 Interest rate derivatives

We argued above that interest rate derivatives should be considered as primary securities, so that pricing formula cannot be derived by a true replication argument, but they are simply market pricing formulae. We illustrate how to evaluate two basic contracts of the interest rate derivative market: a forward rate agreement (FRA) and an interest rate swap (IRS).

Forward rate agreement

Assume we have the risk-free discount curve in both currencies denoted by D and Df, respectively, for YYY and XXX. The pricing formula for a FRA written on Libor rate Li(Ti−1) in YYY, but with collateral posted in XXX can be written in much the same way as that presented above for contracts on other underlying assets and derived from a replication argument:

that is, the expected Libor rate under the Ti forward measure of the value of the contract at expiry Ti−1 plus the LVA. We used Ti = Ti − Ti−1 in equation (12.137).

LVA is the present value of the difference between the risk-free rate ![]() and the collateral rate

and the collateral rate ![]() , fixed at date tj−1 and valid until date tj, both for currency XXX, applied to fraction γ of the value of contract FRA(tj; Ti−1, T2) for a total of N days between t and the forward settlement T1, so that tN = T1: