13.1 INTRODUCTION

What are the likely future developments in the liquidity risk area? Obviously, answering such a question is very challenging because, even for the few topics treated in the previous chapters, state-of-the-art practices and metrics still have to be fully explored and some are a long way from being consolidated among practitioners and supervisors.

When analysing liquidity risk, the main thing to keep in mind is the specificity of each financial institution. Every bank is different from all other financial firms: it represents therefore a single case of study, with its peculiar balance sheet mix and dependence on funding sources, specific business models and processes. Understanding the bank, its customers' behaviour, its competitive environment, the characteristics of its assets and liabilities is a prerequisite not only to define sound risk management practices, but also to find a solution that best fits from the organization's point of view.

There is little value in writing pages about organization of the treasury or ALM functions let alone their missions: the best we could do would be to define a hypothetical organization that would not fit the actual structure of a real bank. Every financial firm is tasked with finding its own solutions based on its specific features. Nevertheless, there are some topics deserving further analysis because they represent the more likely “open issues” for some time to come and may affect the interaction between the treasury's function and other functions of the bank, or the core activity of the treasury itself.

13.2 ORGANIZATION OF THE TREASURY AND THE DEALING ROOM

Let us start by considering the bank's activity in derivative products. In the daily manufacture of derivative contracts in banks' dealing rooms, positions are typically hedged so that an offsetting payoff is synthetically replicated. This happens on an aggregated portfolio level, thus allowing for natural compensation of exposures originated by the dealing activity.

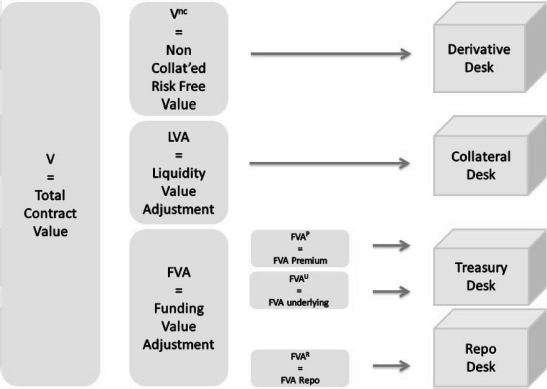

As shown in Chapter 12, if the relevant desks operate a replication strategy that considers a formula encompassing, for example, the LVA (or equivalently, using an effective discount rate accounting for the collateral rate), the final payoff attained is not equal to the contract's payoff, as is manifest from Example 12.1.1. This difference is due to the LVA and should be assigned to the collateral desk, if one exists in the dealing room, to compensate the costs it bears (or the gains it earns) in managing the collateral account. As a consequence the derivatives desk should try and replicate only the risk-free component of the contract, disregarding the LVA and leaving it to the collateral desk. When trading the contract, the risk-free component of the premium is assigned to the derivatives desk, while the LVA is left to the collateral desk.

Figure 13.1. Attribution of the components of a derivative contract's value to the relevant desks of a dealing room

By the same token, the FVA should be assigned to the treasury desk, and the repo component of the FVA, if present, to the repo desk.1 The FVA is the premium that the derivative desk pays to (or receives from) the other desks involved in dealing room activity, to be ensured of execution of the dynamic replication at a cost equal to what it would pay in a virtual default risk-free, perfectly efficient market, where no collateral and funding effects are operating. In this way, the derivative desk's performance is measured on a proper basis, without including contributions other than the correct hedging of the contract's payoff and the margin that the desk is able to create and preserve.

On the other hand, the collateral desk is remunerated (or charged) with the LVA to run its specific activity, which is the management of collateral cash flows on which it receives or pays the collateral rate, and conversely pays or receives the risk-free rate by investing or funding them.

The treasury desk lends money to and borrows money from the other desks at the risk-free rate. In the money market the treasury desk pays the funding rate of the bank and may invest in risk-free assets receiving the risk-free rate. For this activity it is paid the FVA.

The repo desk buys and sells the quantity of the underlying asset needed for the dynamic replica. The asset is sold to or bought from the derivative desk as if it were financed at the risk-free rate. The repo component of the FVA is attributed to the repo desk to account for the difference between the repo rate and the risk-free rate.

Figure 13.1 shows the breakdown of the total premium into different components and their attribution to the relevant desks.

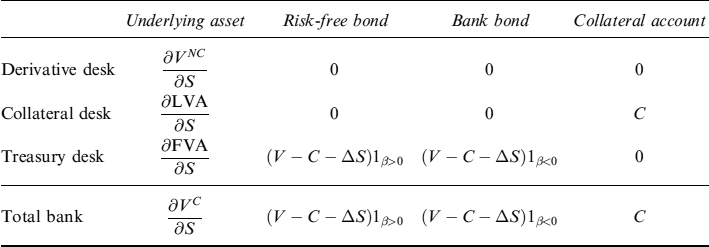

Table 13.1. Amount of underlying asset, risk-free bonds and bank's own bonds held by each desk to dynamically replicate the derivative contract

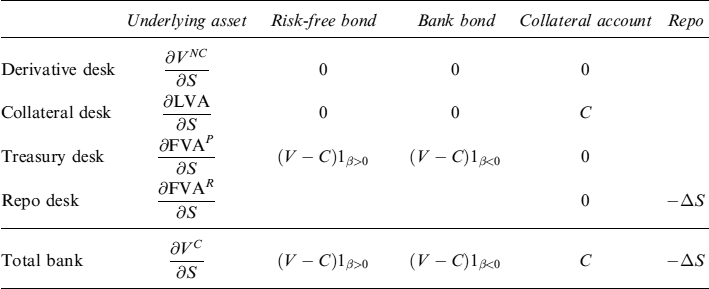

Table 13.2. Amount of underlying asset, risk-free bonds and bank's own bonds held by each desk to dynamically replicate the derivative contract

In Table 13.1 we show the amount of cash and underlying asset held by each desk in the replication strategy process. Table 13.2 shows the same when the underlying asset is bought or sold via repo transactions, so that the repo desk is involved as well.

Understandably, this has profound implications for the organization of a dealing room. In fact, until recently desks such as treasury and repo were strongly specialized on linear contracts (deposits, FRAs, repo, reverse repo and so on) and their skills were only marginally involved in the trading and risk management of nonlinear derivative contracts, such as options. Nowadays, the importance of funding costs forces these desks to grow their skills so as to encompass nonlinear contract risk management as well. The same logic applies to the collateral desk, which should be considered more than a manager of cash flows originating from CSA agreements.

Organizing things in this way can be achieved in two ways, either by training money market and repo traders or by creating treasury, repo and collateral desks with very diffuse competences and hiring traders with money market-making and derivative market-making experience. The second option in our view is easier, quicker and more effective to adopt.

13.3 BANKING VS TRADING BOOK

In our opinion, the distinction between the trading and banking book will fade away in the near future for a number of reasons, which we briefly list below.

13.3.1 Collateralization

As already abundantly stated, the components that make up funding currently affect the price and management of a derivative portfolio. Such a portfolio basically depends on, first, the increased cost of funding of the bank sector, which is no longer able to fund itself to the risk-free rate or close to the rate used for collateral remuneration;2 second, the fact that many hedgers in derivative markets (mainly sovereigns, supranational entities and corporate firms) do not have (or will not have in the near future) to collateralize their exposures through central clearing counterparties or under bilateral symmetric CSA agreements, thus producing strong asymmetries in terms of cash flows, although market risk is fully hedged.

So, many banks are tasked with handling a structural mismatch within their derivative portfolio, between their uncollateralized and collateralized derivative transactions. They actually have to manage two different derivative portfolios, each with their own specific dynamics and risk factors. As already explained in Chapter 12, for uncollateralized derivative transactions it is necessary to calculate the FVA whenever the cash flow profile of a new derivative transaction is not balanced over the life of the contract; for collateralized derivative transactions changes in the derivative portfolio's expected exposure to market risk (interest rate, credit, equity, forex) and in the term structure of the funding spread require dynamic hedging at the portfolio level through derivative products in order to offset negative economic effects, which will be recorded by the P&L statement only on an accrual basis.

As far as central clearing of derivative transactions is concerned, liquidity impacts may be magnified by initial margin-posting requirements, which have to be funded over time. This is an open issue not dealt with in this book, but the preliminary studies we are conducting show that it has a big impact in terms of liquidity requirements and costs borne to satisfy them.

As a result of the steady and seemingly unrelenting trend towards full collateralization of derivative contracts, it is worth stressing that even traditional banking activity is subject to relevant changes in the management of liquidity needs when it operates in the derivative transactions only for hedging purpose (i.e., to reduce the interest rate risk of the mortgage portfolio or, more generally, of the assets). The abovementioned asymmetry of cash flows produced by collateralized transactions hedging non-collateralized contracts will likely become a typical feature of the future liquidity management of the banking book, even more so than that of the trading book.

Dynamic hedging of the FVA and LVA components of the derivative portfolio (even when included in the banking book to hedge market risks) aims at offsetting over time the difference between the interest paid to fund initial and variation margins and the interest received on collateral posted, if the collateral rate is lower than the funding rate of the bank, or if it is required to fund margins on tenors longer than overnight. The dichotomy between hedged items evaluated on an accrual basis (say, loans) and hedging items subject to mark-to-market evaluation (say, a swap), at the portfolio level, could even be exacerbated if the offsetting of some components of the FVA related to the derivative portfolio require some modifications to actual or expected outstanding liabilities, in terms of changes in the liquidity funding plan.

Different accounting rules for derivatives and funding-related items (i.e., liabilities) currently prevent the financial industry from finding a consistent solution to this problem, which will likely become one of the most important open issues in the coming years: it appears increasingly evident that banking and trading books can no longer be considered two separate silos or building blocks.

Supervisors are therefore faced with carrying out a comprehensive evaluation of all accounting and prudential rules in order to properly address increasingly frequent interrelations between trading and banking books. The banking book is doomed to become a natural hedge of some funding risks embedded in the trading book.

13.3.2 Links Amongst Risks

The close interconnection between the trading book and the banking book requires unavoidable rethinking of the traditional separation between treasury (focused on the short term) and ALM (focused on the medium and long term). The web of risks examined in Chapter 5 makes clear that it is not possible to disregard the links amongst the different types of risks. However, even limiting the analysis to market and liquidity risks, it is manifest that the ALM is already, and will be more in the future, subject to risks traditionally managed by treasurers and traders, such as basis risk between different indexes (Eonia, Euribor on different tenors, Libor and so on) and the bank's own funding spread volatility, which may affect economic results over time in a significant way.3

The challenges facing supervisors and practitioners have been put on the table: in this environment, traditional risk measures used to monitor the banking book, such as the duration gap or interest rate sensitivity of the interest margin, need to be integrated using more detailed analytical tools, in order to capture and monitor the different risks affecting the most stable part of the balance sheet: it is up to supervisors to accept for the banking book new metrics closer to trading book standards, in line with models and practices in some cases already adopted by the industry. In Chapters 8 and 9 we introduced new models to monitor the liquidity risks of specific contracts and to adapt approaches usually adopted in the trading book to liquidity risk.

On the asset side, it would be of little use to have more advanced tools to monitor risks without appropriate trading skills: diffuse market competences are therefore required not only for treasurers but also for ALM operators in order to manage the increased complexity of their business. This is probably one of the most delicate problemsthat need to be dealt with, because managing the banking book was relatively easy in the past environment and asset–liability managers were not skilled enough to cope with more turbulent and complex market environments. We are quite sure, from our personal experience, that the learning-by-doing process is proceeding quickly in most cases, but it requires time and, more importantly, losses to be suffered by the banks.4

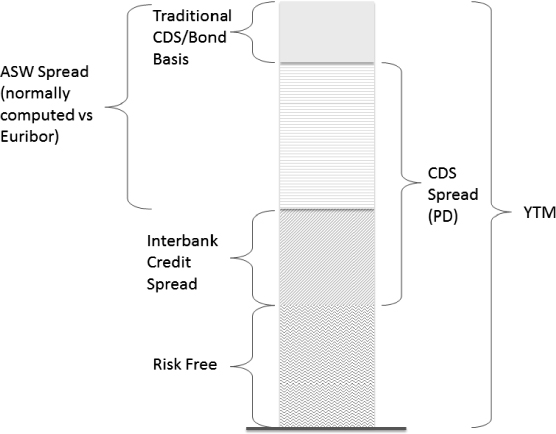

Figure 13.2. Components of the yield to maturity for a generic tenor

On the liability side, the volatility of funding costs deeply impacts management strategies and, more generally, bank profitability. Consider Figure 13.2, which shows the components of the bank's total cost of funding (yield to maturity for a generic tenor) in terms of its spread over Eonia (or the OIS) rate, currently taken in practice as a proxy for the risk-free rate and assigned to the desks (derivative, treasury or ALM) as a risk factor to hedge.

By summing the interbank credit spread (i.e., the spread between Euribor and Eonia, or Libor and OIS) and the asset–swap spread (normally computed vs Euribor or Libor) we arrive at the all-in spread over OIS rate to be used to compute the funding cost for traditional banking contracts or the FVA for derivative contracts. The actual owner of the funding cost or the FVA will be the treasury desk or the ALM desk according to the average weighted life of the portfolio.

Therefore, the treasury desk and/or the ALM desk have to manage three different risk factors:

- The Euribor/Eonia (Libor/OIS) basis.

- The residual CDS spread on its own name (i.e., the CDS spread minus the interbank credit spread).

- The CDS/bond basis.

The basis at point 1 can be hedged on the interbank market through derivative products, the spreads in the other two points require some cross-hedges by using proxies, because it is not possible to buy/sell protection on its own name, as implied by the strategy based on replication of asset–swap spreads in Chapters 10 and 12.5 Because of the impossibility of perfect replication of the components in 2 and 3 it is of the utmost importance for the treasury desk and/or the ALM desk to have the expertise on credit dynamics necessary to manage properly sensitivities to the volatility of its own funding spread at the portfolio level.

13.3.3 Production costs

We have already argued in Chapter 11, when discussing the FTP, that an industrial approach is needed to price banking book contracts: this means that all the components that make up costs have to be properly measured and priced into contracts when sold to clients. This process, in the financial industry, means that sophisticated analytical tools need to be designed and employed to properly appreciate the impact of any possible risk on the value of a contract.

The industrial approach is quite common on the trading book: the discussion in Chapter 12 is an extension to new risks, related to liquidity and funding, of existing frameworks commonly adopted for derivative contracts. The industrial approach is fully supportive of best practices in pricing on the banking book: this is due to the easier, more stable and less risky market environment, to the simpler structure of risks and to the irrelevance of problems related to liquidity and the cost of funding.

Under current market conditions, with business margins squeezed due to the increased volatility of both assets and liabilities, the precise measurement and management of risks is crucial to ensuring profitable survival of the bank. This means that trading book practices need take little more than a gradual approach to the banking book, although we do not mean by this that the trading book does not need to improve its risk management policies nor design new analytical tools: we are sure there is still much to do, yet a firm and robust modus operandi on the trading book is a good starting point toward progressing in the right direction.

We have presented some possible solutions for typical banking book risks, such as prepayment of mortgages or withdrawal of credit lines, and we have shown how analytical tools developed to value derivative contracts can be effectively adapted and used to value traditional banking contracts. Clearly, once these risks are included in the pricing, they also have to be managed and hedged whenever possible: more sophisticated applications and more skilled treasurers and asset/liability managers will be required.

All these developments are moving in the same direction: in the near future the treasury and ALM desks are destined to manage increasingly complex business risks and have increased recourse to nonlinear products in order to hedge the risks embedded in banking book activities in a more accurate way. For this challenging task flexible and open-minded operators will themselves be crucial resources and even more important than any analytic tool or metric like those presented in this book or those that are still to be developed.

1 See Chapter 12 for details on these quantities.

3 In Chapter 11 we presented an approach to monitor and price the volatility of the bank's own funding spread.

4 It is a firm belief, at least for one of the authors (who proposed this in another book), that the only way a trader learns is by losing money in much the same way as does the man in the street.

5 See the discussion on the impossibility of hedging own name DVA in Chapter 10, which also applies to the FVA according to Definitions 10.6.1 and 12.1.2.