![]()

Setting Up a Lean REO Machine

BUILDING YOUR DREAM TEAM

You are about to be the type of REO agent asset managers love. Your secret weapon? Your dream team. Early in my career I quickly learned that asset managers gave a lot of volume and the right kind of volume to the agents they loved. I remember this local agent who was just starting off. He wasn’t big. As a matter of fact, he didn’t have a fancy website and still had an old AOL email account (by the way, if you have any email account other than one attached to your website name, turn to Chapter 7 immediately). However, for some reason this agent would get the highest-priced REO listings in the best neighborhoods.

I’m talking about four bedroom, 3,000 square feet, water front, single family homes that were so hot, they would get under contract within one hour of being listed on the MLS (before the three-day bank rule was in effect—see Chapter 8). He got on the bank’s “A” list and he did it by mastering only one thing—performance. He had a lean, mean, fighting machine system. Not one phone call would be missed, nor would any offers fall through the cracks. He had his system down to a science. We call this “building your dream team.”

In Chapter 2 we discussed the main goals of banks: to sell their REOs for the highest price possible in the shortest amount of time. This is also known as asset recovery. Remember what asset manager’s goals are? To close! They care about one thing and one thing only: closings. This means closing fast, closing early, and closing at their targeted list price or above. If you have ever seen the famous scene in the movie Glengarry Glen Ross, you know the saying: ABC. That is what they base their motto on.

A-LWAYS

B-E

C-LOSING

Remember, asset managers or sales representatives for banks are employees who get a salary and have a bonus structure based on the amount of closings they do. If you can help them perform and make them look good so they can achieve their sales numbers, they are going to love you.

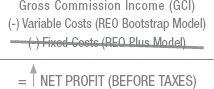

The only way this can happen is by creating a lean REO system with a stellar dream team. When I say lean I am talking about being financially fit; in other words, profitable. There are two models that will help you accomplish this: the “REO Bootstrap Model” and the “REO Plus Model.”

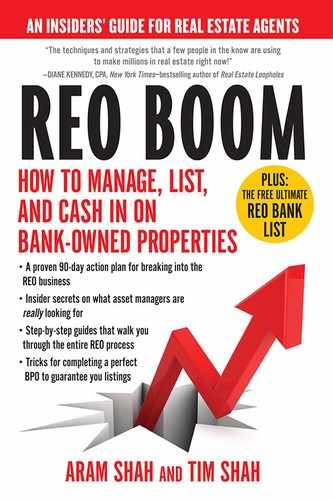

THE REO FOOTPRINT

Before we get into the two systems, let’s go over the big picture of how you fit into the basic REO footprint:

You (or your brokerage company) act as an intermediary between banks and customers. Think of it as operating in a network. It’s a network that provides value to all parties because the more properties you can list and sell for the banks, the more properties you will receive back. Also, the more REO properties you receive, the more you can offer and sell to your customers.

As an REO agent your job is to grow your network by connecting hungry home buyers and investors looking for great deals with distressed banks looking to unload their properties. The bigger you can make this footprint or network, the more value you can add to all parties and the faster you will reach a million dollars net.

LARGE NETWORK IS KEY!

REO banks want an REO agent who has the ability to handle volume. They want to feel confident, comfortable, and secure that the listings they give out will close in time and the property will be taken care of. The more properties you handle and turn within ninety days, the more you receive. Success breeds success.

—Mark Miller

Atlanta, GA

REO listing agent

As an REO agent, your specialty or niche market is bank-owned properties. The more customers you can reach out to, the bigger the network of clients you will have to present to the different banks. Once the banks know you have a big following, they will feel confident about giving you properties to manage and list. It’s a full circle.

AGENT NICHE:

BANK-OWED PROPERTIES

The REO Bootstrap Model footprint will cost you less than $1,000 to get started and should be used after the 90/10 REO Rule (i.e., after you have successfully closed approximately ten REO transactions). You can technically use it from the start, but the goal is to preserve your cash as much as possible to bankroll your operations.

After you have scaled your footprint to a certain threshold, you will start using the REO Plus Model. The great news is both models are easy to start, and are duplicable; both models have been tested throughout different states in the United States with various REO agents.

REO CUSTOMERS

In order to successfully grow your footprint, you have to provide value to your customers. The first question you must ask yourself is, what is your value proposition (VP)? What is the exact problem or need you are solving for your customers? In order to answer this, you also need to figure out the identity of your customers.

![]() INSIDER TIP

INSIDER TIP

The biggest mistake you can make is to not realize who your primary customer is. In the REO business, your primary customer is not the home buyer. It is the bank!

In the REO business, you have two sets of customers. First are the primary customers, which are your suppliers. These are the banks and outsourcers that feed you the properties or “new BPO assignments” to manage. Your number one priority is to take care of your bank and outsourcer contracts (also called “MLA” or “master listing agreements”). When you see in your caller ID that an asset manager is calling, I don’t care if you are on the phone with an in-house (no co-operating agent) cash customer for a $400,000 listing that is at the closing table ready to sign. You tell that customer you will call them back and hang up so you can speak to the asset manager.

In Chapter 1, I mentioned how every REO property sells. Remember, REO symbolizes a free and clear property for a customer at a discounted price that the seller needs (not wants) to get off their books. The question then becomes not if the property will sell, but when it will sell. Therefore, you must take care of your primary customers—the banks who have given you the guaranteed sale of an REO property.

Next are your secondary customers—home owners and investors. Your main focus is to convert each lead who contacts your office and put them into your current upcoming REOs. For example, you may have sixty properties in inventory but only twelve that are active and ready to be sold on the market. The rest of the properties may have a tenant inside, need repairs, etc. Therefore, your job is to pre-sell the remaining inventory.

The easiest way to do this is to pre-qualify your secondary customers through a mortgage partner (Chapter 9) and pre-sell your up and coming inventory. Usually homeowners are first-time buyers who have sufficient income or credit to qualify for their first home. They meet the minimum standards to qualify for a home loan, and usually have a down payment less than 10 percent.

Investors are customers who have usually purchased more than one home before and are looking to either rent out the property or resell the property after three or four months for a profit (this is commonly called “flipping”). They usually purchase with all cash or have a large chunk of money to use as a down payment (i.e., 20% percent or greater).

![]() INSIDER TIP

INSIDER TIP

Investors are looking for an REO home that has been on the market for over ninety days that has substantial repair issues so they can buy it, fix it up, make it financeable through FHA or a conventional loan, and sell to a home buyer.

Regardless of whether the secondary customer is a home owner or an investor, they are looking for a great deal. Sometimes, they are looking for a steal. There is no better deal than you pre-showing your exclusive inventory (since it’s not on the MLS yet), so they have a head start over the competition.

Your job is to provide them with what they need: REOs. You are the direct source of REOs or “deals” in your local market. Never forget this. The value proposition for your customers is exclusive REOs at an incredible price, delivered to them free of charge.

CUSTOMER VP:

EXCLUSIVE REO DEALS FREE

While you are providing your customers a direct list of properties delivered daily or weekly, you are also solving your supplier needs by offering them a large pool of qualified buyers in your local market. By qualifying and screening (via your mortgage partners) your influx of leads, you can match-make buyers and REOs more quickly.

Remember, banks are bleeding; you are an expert in your local market and they need your help. They need to minimize their loss by achieving a fast turn-around time. Therefore, the value propositions for your suppliers are a large qualified network of buyers and faster closings.

SUPPLIER VP:

LARGE POOL OF BUYERS; FAST CLOSINGS

REO BOOTSTRAP MODEL

In the book The Art of the Start, author Guy Kawasaki talks about the art of bootstrapping or growing your business from the inside, using the cash you have in your bank account as opposed to borrowing money or raising venture capital. Sometimes you’re just forced to bootstrap.

Before I received my first assignment I had about $1,000, a strong will, and a desire. As the “housing bubble” was bursting, money was very tight. I had no choice. I had to tread water very carefully. I couldn’t afford to hire staff, I had to count every penny, and I outsourced everything to odesk.com. My tradeoff was time. So it took me a little longer to get up and running. That was OK. Rome wasn’t built in a day.

In Chapter 1, you learned about the 90/10 rule. The first ninety days after you receive your first assignment you will be working long hours and doing everything yourself until you successfully close your first deal. You will then take that commission check and bankroll it orinvest it into more BPO assignments until you successfully close ten REOs. You will then have enough cash saved up in your bank account to bring on your dream team.

The great thing about REOs is that you get new assignments based on performance. Therefore, you perform well (i.e., without mistakes and close on time) and you will be rewarded with another assignment. If you close all ten, you will get ten more. REOs are predictable sales. They are predictable closings because every REO closes; it’s just a matter of when.

Therefore, you can use the REO Bootstrap Model to stay financially lean in the business and offer a value proposition to your customers. Here is how it works.

REO BOOTSTRAP MODEL

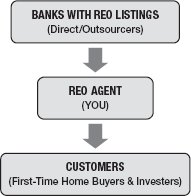

When you have less than thirty active REO listings on the MLS, you will assign properties to your listing specialists (licensed real estate agents) and they will be responsible for the entire REO cycle, from occupancy checks to making sure the transaction closes. You will act as their asset manager. Everything will funnel through you for review, and have your name on it, and then you will submit the tasks to the bank.

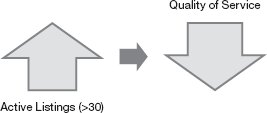

Why thirty? From trial and error, through different parts of the United States, I have found as you continue to build your business north of thirty active REO listings, your quality of work using this model begins to head south. Your listing specialists have a hard time managing the workflow and, more importantly, deadlines.

However, the work load is manageable under thirty active listings. Therefore, as you receive a new property or “BPO assignment” from a bank, you will internally assign each property to a listing specialist in your team. A listing agent has to be a licensed real estate agent, because they will be showing and selling homes.

I have approximately three to five listing specialists in my team per each direct bank contract. This allows me to manage the workflow more easily, as well as maintain proper accountability. These specialists will be responsible for handling every step of the REO cycle until the property closes. This includes changing lockboxes, adding yard signs, driving expenses, posting notices, marketing, updating websites, maintaining utilities, and paying for minor repairs until the bank reimburses them for those expenses. In exchange, you will share 40 percent of your listing commission with them.

If the listing specialist finds their own buyer for the property, you will share the sales commission equally.

Commission Split to Listing Specialist

- 40 percent from listing side

- 50 percent from selling side (if they procure their own buyer)

Example: A $200,000 home closes, and your listing commission (LC) is 2.5 percent (your total commission is $5,000). From the 2.5 percent you are giving up 40 percent to your listing specialist. Also, let’s say your listing specialist finds their own buyer and earned you 3 percent as a selling commission (SC). Remember, selling commission is usually a full 3 percent, as the banks want an incentive for agents to bring in buyer offers. Therefore, the payout to your listing specialist would be as follows:

$200,000 × 2.5% (LC) × 40% = $2,000.00 (to listing specialist)

$200,000 × 3% (SC) × 50% = $3,000.00 (to listing specialist)

By sharing your listing commissions, you will make less, but you’re saving cash. Instead of putting your own money in the business, you are sharing expenses with your listing specialist.

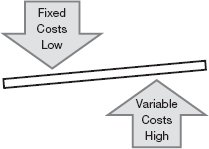

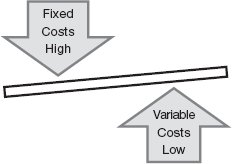

When starting off in the business, it is very important to keep your fixed costs low. Watch every penny. I coach my REO agents to set up free bi-weekly conference calls on skype.com or freeconferencecall.com to talk about the weekly tasks. That way, you can save the cost of travel, hourly office space, and time.

Variable costs are costs that increase with production. For example, you sell a home with an agent in your office. You make a $3,000 commission, but you’re sharing half the commission with her. Therefore, your variable cost is $1,500. Fixed costs remain the same no matter what. If you make a $3,000 commission by yourself and your office space is $1,000 a month, your fixed costs are $1,000 a month.

This model works extremely well when you are first starting and your active listing count stays under thirty. Active listings are the amount of REOs you have listed as “active” in the multiple listing services (MLS). You can have a hundred REOs in inventory, but only thirty of those should be active on the MLS waiting for offers to be placed. Remember, after thirty, the workload gets too heavy and your quality of service will suffer.

Because you are outsourcing almost the entire REO cycle and relying on your team’s skills set, you will have to hire extremely qualified, full-time, dedicated agents. Some criteria I look for in hiring listing specialists are:

- Passion for real estate/foreclosures

- Similar core values and virtues (e.g., ethical, disciplined)

- Is a team player

- Track record of prior results

- Full-time in real estate (no-part timers)

- Bachelor’s degree (or certifications/designation in real estate)

- Possesses some working capital (ability to bring up to $1,000 in startup costs)

Since you will be dealing with very professional and highly educated asset managers, your team must possess skills to match your primary customer’s language. One of the biggest mistakes I see in new agents is that they do not speak the same language as the banks. If the banks expect a very thorough and detailed BPO with some statistics of comparable properties, then you must provide them with exactly that, if not more.

![]() INSIDER TIP

INSIDER TIP

Always offer a unique value proposition to the banks. For example, having a team that all possess bachelor’s degrees or certain designations can set you apart from the rest.

One of the companies I coached in 2009 started up with the REO Bootstrap Model and found an excellent listing specialist (or so they thought). His résumé was outstanding; he was a young real estate agent just out of college and looking to get into REOs. On the first couple of assignments, the agent did OK. He made a couple of mistakes, which is normal in the learning curve process. However, as the work flow began to come in, he began making a lot of small mistakes: spelling errors, incomplete sentences, missing pictures in the BPOs, etc. Mike, as we will call him, was our REO agent who oversaw all the work flow.

Unfortunately, one BPO slipped through the cracks with errors and reached the asset manager. Within fifteen minutes of uploading the BPO into their system, the asset manager emailed Mike saying that he was “re-assigning the property because the BPO looked like a child did it.” Not only did Mike lose the property, he had to fire his listing specialist all on the same day. It wasn’t a good day for Mike, but sometimes that what happens when errors reach the top.

![]() INSIDER TIP

INSIDER TIP

When interviewing your listing specialist, ask him or her whether they value efforts or results more. If they say efforts, quickly thank them for their time and let them go. This business is about results and nothing less.

If you cannot perform at 100 percent all the time, then expect to lose your listing or your bank contract. If even one deadline gets missed, the banks are holding you responsible—not the listing specialist—since you are their sole point of contact. Therefore, quality is dependent on your listing specialist. It is crucial that you bring the right people on to your team and keep a close eye on them. Your bank contract will depend on it.

![]() INSIDER TIP

INSIDER TIP

Do not give access to your log-in password on your supplier’s platform to any listing specialist. Only you should be the point of contact for the banks, especially if you will be letting the specialists go after you scale your business.

One caveat when using the REO Bootstrap Model is that you will forego any communication with your secondary customers: first-time home buyers and investors. Because you are sharing 50 percent of your selling commission with a listing specialist if they find a buyer, you cannot compete directly with them by finding a buyer yourself and keeping all of the commission. You will be working as a team. Whether you or they find a buyer, you will be splitting the commission fifty-fifty. This is good and healthy, but because their name and signs will be in the field, the customers will be associating REOs with them and not with you.

![]() INSIDER TIP

INSIDER TIP

When using the REO Bootstrap Model, always put your name and number on all marketing signs along with the listing specialists’ information; otherwise you will be allowing them to build a brand solely through your bank connections.

REO BOOTSTRAP MODEL PROS AND CONS

|

|

|

1. Entire REO cycle outsourced 2. Very little cash to start 3. Low fixed costs 4. High motivation pool of listing specialists 5. No communications with co-operating agents or customers 6. Limited to under 30 active |

1. Quality dependent on listing specialists 2. Sharing commissions 3. High variable costs 4. More supervision required 5. No branding (listing specialist branded in field) 6. Capacity for volume limited |

REO PLUS MODEL

One of the hardest things I had to do was transition from the REO Bootstrap Model to the REO Plus Model. It was similar to moving on to another decade in life. Remember when you turned thirty? You found your first gray hair, you felt different, maybe things started hurting a little more? That is the same feeling I experienced when I transitioned to a new REO model by letting my all-star specialist go and hiring my new dream team.

I had this one hungry lion working for me. He was a true go-getter—just out of college and ready to be the next Donald Trump. During late 2008 we started moving a lot of units. We might have closed about $25 million in gross volume. During the last week of December, I sat down with him and told him, “I’m sorry John, but you have to go.” He was stunned.

No matter how many ways or times I told him he couldn’t understand it. He was doing well, I was doing well, our team was doing well, so why? Because we had outgrown the business model; John just wasn’t profitable to the business anymore. Sometimes great becomes the enemy of good.

His fate was written from day one of being on board; maybe not the exact date of his departure, but the actual departure itself. It was hard to break to him and hard for him to accept. In actuality, he might have gained more from the relationship than I did, because he made about $250,000 and had an incredible résumé. What I was doing was transitioning to the REO Plus Model to begin the new year.

The model is simple. When you have thirty active listings or greater, you will terminate all your listing specialists and bring on hourly staff. You will pay them per hour (or your broker will—check your state law) and you will control your fixed costs (hourly pay) by increasing or decreasing their hours like a thermostat.

As the heat (volume of properties) is on, you turn the knob—and increase your team’s hours or hire additional staff—to cool off. As the inventory begins slowing down, you turn the knob the opposite way and begin cutting hours. The key is moving your staff from part-time hours to full-time hours.

The goal is to keep all the gross commission income for yourself (no splitting of gross commissions) and hire on staff to cover your routine paperwork. Therefore, instead of outsourcing the entire REO cycle (Chapter 1), you now are in-sourcing or delegating each function of the cycle to separate staff members of your team.

This allows you to focus on what’s most important—communicating to asset managers and selling homes. Your name will be branded at the retail level and your job will be to find your own in-house buyers to make both sides of the real estate commission (listing and selling) to maximize the commission. Why only make 2 or 3 percent when you can shoot for 6 percent?

As home prices continue to fall, foreclosures rise, consumer confi-dence drops, jobs are outsourced overseas, and unemployment rises, more people are looking for work. This is excellent news for you as an REO agent. You have an abundant supply of worker bees looking for a job and a limited number of jobs available. As a real estate entrepreneur, you will be creating jobs and getting a nice return on your investment from them. It’s a true win-win.

ASSEMBLY LINE STANDARDIZATION

I want you to think of a car company or a manufacturing plant. They produce hundreds of car parts that flow down an assembly line. Everything is standardized. They have one person doing one task the whole day, from 9 A.M. to 5 P.M.

From a distance, that person could be a robot. This is what the REO Plus Model is like. It’s an assembly line. You will break each function of the REO cycle into parts and assign one staff person to be in charge of each part.

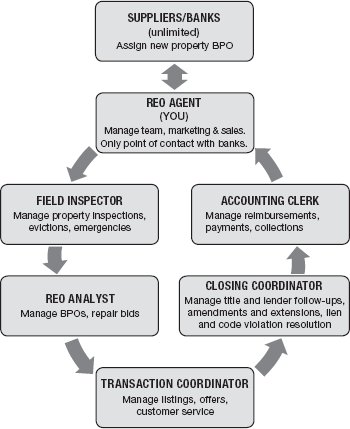

Here is how it works. You will be the main point of contact with the bank, backed up by your dream team:

- Field Inspector

- REO Analyst

- Transaction Coordinator

- Closing Coordinator

- Accounting Clerk

REO PLUS MODEL

Below are the five key staff functions for your dream team:

- Field Inspector. Your field inspector will visit each property weekly and perform your occupancy checks. They will determine whether the home is vacant or occupied and provide weekly reports. They will also place lockboxes and yard signs in the front lawn. As soon as a new BPO assignment comes in, they will go out to the property immediately and post any notices required by the bank. Some key activities include:

- Initial and weekly property inspections

- Signs, lockboxes, and replacing missing keys

- Physical/emergency damage reports

- Eviction and trash out assistance

- REO Analyst. Your REO Analyst will perform the BPOs, prepare repair bids, and manage any contractors who are scheduled to repair your properties so they can be in marketable condition. Some key activities include:

- Gathering comparable listing data for BPOs

- Assessing repair damages and coordinating repair work with contractors

- Contacting homeowner associations for estoppel information, authorization letters, access, and coordination with appraisers

- Obtaining certificates of title when assigned new properties

- Transaction Coordinator. Your transaction coordinator will enter the listings (once marketable) into the MLS and handle all offers, counter-offers, and co-operating agent communications. Finally, they will be the point of contact for the secondary customers (home owners and investors) when they call into the office. Some key activities include:

- Closing Coordinator. Your closing coordinator is the point of contact after the property is under contract. They will be the liaison between the title company, the lender (if needed), and the customer. They will handle the contracts, sales amendments, and extensions needed and will push to close the file within the deadline. Some key activities include:

- Sales amendments and closing coordination

- Managing finance and closing deadlines

- Updating bank platforms on status of closings

- Reviewing HUD-1 for accuracy

- Accounting Clerk. Your accounting clerk takes over the file once the transaction closes and enters all the reimbursements into the bank’s platform. Every expense you as the REO agent incur (water bills, electric, pool covers, etc.) will have to be entered with proof of service (submitting an invoice or receipt) so you can get reimbursed. This is the first staff role you will need to bring to your team. If you do not get your reimbursements in time (within their cut off period), many banks will not pay you and you will be will be stuck footing the bill. This person also collects and deposits your commission checks. Some key activities include:

- Turning on and off utilities (water/electric)

- Entering final invoices for reimbursement

- Monitoring commission checks and reimbursement checks on all closings (a/r)

- Preparing invoices to be paid to vendors

The accounting clerk is your money assistant. You must find someone with quality experience, preferably someone who has done accounting in a real estate office before. I give my accounting clerk all the tasks listed above except accounts payable. Money going out, I handle.

Once your work flow is standardized, your main function will be communicating with the banks, management of your team, and selling homes. Everything else will be in-sourced. I often get asked, “What should the pay structure be like?” Always pay hourly.

On average, each person’s hourly rate will vary from $10/hour to $15/hour. I usually budget around $2,000 a month for each team member. Remember, when times are busy you will increase your staff’s hours or add more people to your team. Conversely, during slow times you will cut hours. It’s always better to go from full-time to part-time than removing the position entirely.

Also, I always over compensate to keep higher retention. Think about it. Two people can make $2,000 a month. The first person can make $200 an hour but only work ten hours a month. The second person can make $10 an hour and work 200 hours a month (50 hours a week). Which sounds better?

![]() INSIDER TIP

INSIDER TIP

It’s always good to over pay but have the flexibility to cut hours when needed.

One caveat when using this model is that you will have to manage the high turnover of staff. Other than paying slightly above market and controlling hours, there are two additional ways to combat this. First is cross-training, and second is promoting. Each member of your staff should be cross-trained in each other’s function. For example, after six months of training, your transaction coordinator can become the closing coordinator and vice versa. First, this creates challenge and excitement in the workforce, and second, it leads to putting your business on autopilot, which we will discuss in Chapter 11.

Next is promoting. Once you land your second or third account you will need to bring on an “account manager” for each account. This person will essentially replace your role. We will go into this in Chapter 11. Therefore, as you grow internally and bring on more bank accounts you can promote from within.

Another caveat when using this model is your high fixed costs. With the REO Plus Model, you are incurring high fixed costs (salaries, rent, etc.) in exchange for giving up a piece of the pie from your gross commission income (i.e., sharing listing commission), so your variable costs are next to nothing.

One final caveat is the size of your bankroll. You need at least $25,000 in working capital to sustain this model. You have to pay (or your broker has to pay) your staff bi-weekly. You also need money to change locks on properties and to do minor repairs, all while waiting to get reimbursed from the bank.

However, because you will only use this model after achieving thirty active MLS listings, you will have closed enough properties and made enough commissionable income to fund your business.

Regardless of the high turnover, high fixed costs, or working capital requirements, the biggest benefit of the REO Plus Model is the amount of net profit you can make per direct bank contract. Once you achieve thirty or more active listings, you will be on track to close twenty to thirty homes a month.

Remember, in the REO Bootstrap Model you are giving up 40 percent of your listing commission, which comes out to 1 percent to your listing specialists (using a conservative 2.5 percent listing commission) in addition to sharing 50 percent of your sales commission. To keep it simple, just do the math on the listing side.

Assuming the median national home sales price of $158,800, you are giving up $1,588 per deal from your top line (gross commission income). Multiply this by twenty closings a month and then by twelve months to get the yearly figure. What do you get? A whole lot of money lost:

$1,588 × 20 CLOSINGS A MONTH × 12 MONTHS = $381,120 A YEAR LOST

This is just one direct bank contract and doesn’t include you receiving anything from the selling commission. Remember, to net a million in this business, you need three direct bank contracts. Therefore multiply $381,120 by three. Now what do you get?

$381,120 × 3 DIRECT BANK CONTRACTS = $1,143,360 A YEAR LOST

If you keep the REO Bootstrap Model after surpassing thirty active listed properties, you are essentially working twice as hard as you need to be. As you can see, triaging the REO Bootstrap Model is imperative to increasing your net profits.

You are trading your variable costs (splitting commissions with listing specialists) for fixed costs (paying salary to a team). You are stretching your fixed costs over volume of properties just as a production plant does; the same amount of people work on an assembly line, but the volume of car parts continues to flow in.

Also, it’s almost impossible to deliver the same quality of service to banks by using the REO Bootstrap Model as you can using the REO Plus Model because you are relying on your listing specialist. Things come up. Priorities are different. Deadlines that are vital to you may be not as important to them. You cannot really control them as you do with your office staff, since you are not paying them a fixed salary.

REO PLUS MODEL PROS/CONS

|

|

|

1. Full control 2. Standardized tasks 3. Low variable costs 4. High ROI on WC 5. Profitable with volume 6. You are branded 7. Less hours worked |

1. Entire REO cycle in-sourced 2. High turn-over of staff 3. High fixed costs 4. Need $25K WC 5. Need >30 listed as active on MLS 6. Deal with agent and customer complaints |

HOW TO START ON A SHOE-STRING BUDGET

The biggest myth in this business is that you need a lot of money to get going. Almost all of the REO agents I coached started with less than $1,000. If you have been in the real estate business for a while, you may feel this is impossible.

Well, we want you to take your beliefs and place them in a drawer and give the key to your spouse or significant other. Below is list of tools you need to make money in the business (see appendix A for help in finding these items):

- Résumé and proposal (Chapter 2)

- Business cards (optional, 500 max)

- Digital camera (35 mm with zoom, wide angle, and date stamp feature)

- GPS

- Twenty to thirty lockboxes (Shurlok brand) and yard signs

- Smart phone (cell phone with internet capabilities)

- Desktop home computer (with Windows 7, 4gb RAM, 1 TB hard drive, Ethernet LAN, DVD +/- RW burner, and video card that supports dual monitors)

- Dual monitors (19 inches or greater)

- Website with a domain name (no AOL/Yahoo/Hotmail/Gmail accounts)

- Social media accounts (Facebook, Twitter, LinkedIn, etc.)

- MLS with tax roll search (comes with Realtor® membership)

- Microsoft Office Suite 2010 (Word/Excel/PowerPoint/Outlook/OneNote/SharePoint)

- REO forms software

- Adobe Acrobat 9 Professional

- Online fax

- VOIP toll free number

- Virtual office (brokers only—if you do not have an office yet)

This list assumes you already have a real estate license, a vehicle, and a membership with your local Realtor® board.

![]() INSIDER TIP

INSIDER TIP

I require each person on my team to have dual monitors. It is extremely efficient and easier on the eyes, and it has increased my team’s productivity by 50 percent.

![]() INSIDER TIP

INSIDER TIP

One of the most frustrating things is your lockboxes getting stolen. Expect about 10 percent of your lockboxes to be stolen by a customer or a competing agent. Get the Shurlok blue lockbox, which requires two codes to open up the shackles, to mitigate this risk.

Once you have your tools in place, you will need to pick the right broker to work with (if you are a broker already—great). If you are on a low commission split, anything less than 80 percent, I want you to walk into your broker’s office and tell him or her you want an 80 percent or greater split because you will be doing REOs.

If they say “no,” find another broker. There are hundreds of brokers who will give you an 80, 90, 95, or 100 percent commission split in exchange for volume. The REO business is strictly volume. Remember, in your first year you will be closing at least 250 transactions.

The second most important thing you need from your broker is rapid communication. If you have a broker who is not good with technology or communications, takes three or four hours to call you back, holds your commission check and pays you after a week, etc., I want you to run. The REO business is fast paced. It’s conventional real estate on steroids. The last thing you need is a broker who will slow you down.

THE REO BUSINESS IS CONVENTIONAL REAL ESTATE

ON STEROIDS

Next, you need to get all the insurance items mentioned in Chapter 2, along with access to a conference room. Many brokers have begun shifting their business model to virtual. This is fine as long as they have a conference room you can use free of charge.

A WORD TO BROKERS

If you are currently a principal broker, manager, or broker owner, you need to keep an eye on your fixed costs. With technology advancing at such a rapid pace, you need to forget about the first floor office space in a shopping center and the “providing your agents with desks as an incentive” mentality. That business model is close to extinct.

Your goal is to stay as financially lean as possible, which means keeping your fixed costs as low as possible. Examples of fixed costs are advertising, marketing, salaries, wages, technology, and rent. One great alternative is to use virtual offices, which are fully functional with conference rooms and live secretaries; they can run as little as $300 per month.

If you need more hours, you pay by the hour. This is all you need in an office. I used this in the beginning for the REO Bootstrap Model and it worked out wonderfully. Once I surpassed thirty active listings, I looked for a small office space with flexible lease terms.

![]() INSIDER TIP

INSIDER TIP

When switching to the REO Plus Model, you will need an office space than can hold your five team members along with a conference area. Keep the office under 1,500 square feet, obtain a gross lease with your utilities included, and do not pay more than $15 per square foot. Commercial landlords are desperate for growing businesses. You are in demand.

LEVERAGING OTHER VENDORS’ MONEY (OVM)

I have a very important message for you that the banks don’t want you to know. You can bankroll each property with zero down. The REO business is wonderful. There are no accounts receivables, very few fixed costs, a pipeline of guaranteed income, and an unlimited stream of contractors who want to be your number one supplier. Having an REO business feels like being Walmart because of the power you have over your vendors.

If you have ever studied Walmart’s business practices or simply attempted to purchase something at one of their mega stores, you can immediately feel their power. Hundreds of thousands of people shop there because of the company’s everyday rock bottom prices, regardless of whether they have to park miles away or wait thirty minutes in line to check out. Walmart is a conglomerate; they have banks, credit unions, mini-stores, pharmacies, almost everything you could imagine or want at one location.

With the ability to draw so many customers Walmart can demand a lot. They tell each of their suppliers how much they will be willing to pay. They have their suppliers come in and stock their shelves and organize. If the suppliers’ quality is poor or they are late on a delivery, Walmart will most likely reject the entire shipment or never do business with them again.

As an REO agent, you are a mini Walmart. Once you are known in your market as a direct REO agent, all the property preservation, rehab, and real estate vendors will be emailing you. Usually, these are the people who made a fortune during the real estate construction boom and are now on the verge of bankruptcy, looking for any type of work they can get their hands on.

Because the banks advertise you on their affiliate national website as the local broker in your market, your name and phone number will be public. This is great news. Because you will be known, you will be leveraging your mini-powerhouse REO business to squeeze a dollar out of every nickel.

When I first started with the REO business, I had a vendor who approached me for business. It was one of many. They were desperate. They were ex–home builders who thought they were on top of the world when the housing market was booming, and now they had succumbed to cleaning up foreclosures for a living with the downturn of the market. They begged me for the business. They called me weekly. They emailed me daily. They even did the unthinkable and came in to see me.

One afternoon, the owner of a company sent me a hand-written note that said, “Give me five minutes, and if you don’t like what I have to say I will pay you $100 for your five minutes of time.” That offer was pretty hard to turn down. I invited him into my office and I started the stopwatch.

Within five minutes, he told me his company had been a “big builder” in the past and was more than qualified to do all property preservation. He said I would not have to pay any money upfront. Further, I would only be required to pay him after I got reimbursed from the banks, up to 180 days later. Basically he was proposing open terms, with him financing my operating expenses for each property for six months. Talk about bootstrapping.

I told him, “OK, I’ll give you one shot; if your quality is poor you are out.” He was thrilled. Remember, as an REO agent you are responsible for maintaining each property until it sells. Don’t be alarmed. Your vendor will foot the bill with open terms. Your job is to receive invoices for the work you need completed, usually minor items under $1,000 (e.g., lock changes, tarps on house, pool cages, etc.), get them approved in writing from the bank, then send an approval email to your vendor to commence work.

THREE STEPS TO OVM

1. Request invoice for job needed from vendor

2. Obtain approval in writing from bank

3. Approve vendor’s invoice and order work

![]() INSIDER TIP

INSIDER TIP

Accept nothing less than 120-day payment terms from your vendors and have a minimum of three vendors you can outsource your work to. Never put all your eggs in one basket.

Once a vendor has completed work, it is important for you go to the property to inspect the premises carefully. Even if it’s something as small as a rekey of the front doors, you want to make sure the quality is good. Never solely rely on one vendor.

OVM RULE = 3 VENDORS

120 DAYS OR GREATER PAYMENT TERMS

Usually you will get reimbursed from your bank within ninety days. Therefore, the longer the period before you have to pay your vendor, the better. For example, if you get paid within ninety days and you pay your vendor within six months, you will have three months of free interest on your money, not to mention you will have put zero down to finance your operations.

Once you spread the word that you are an REO agent, you will be bombarded with emails. The worst thing you can do is pick the first vendor who proposes something favorable. Be cautious. A lot of times vendors can be start-up, fly-by-night companies who paid $200 for a website (or don’t have one at all) and claim to be “property preservation specialists.” Look at details.

Are they using an AOL or Gmail account? If you call the number, does it go to a cell phone or an office? Are they using a P.O. box for their address? Usually, reputable companies have live people answering calls, use a company email, provide a physical address you can visit, and employ a reasonably sized team or staff on site.

TOP THREE DEAL BREAKER QUESTIONS

1. Do you work weekends?

2. Which REO agents or brokerage companies are you working with now?

3. Are you approved as a preferred vendor for banks directly?

In my many attempts to find my top three vendors, I stumbled upon one vendor who told me his company did not work weekends. I told him, “You may be in the wrong business.” In real estate, everyone works weekends, even if it’s only one or two hours a day. His excuse was, “Since the banks are closed, we are too.” Unfortunately, he didn’t realize who his customers were—real estate agents, not banks.

If you come across a company that does not work weekends, run. Emergencies happen. A flood occurs on your property. Someone steals a lockbox or key. You have an emergency eviction. You need someone reliable that can be on call 24/7. Next, make sure your top three vendors can give you real live recommendations from current REO agents. If they cannot, thank them for their time and leave. Remember, there is very little room for error with handling bank accounts. If you are meeting a vendor who just started their business, they will not be a fit for your REO business. Finally, don’t forget to call the references and check them out.

A sign of a good vendor is if they are an approved in-network vendor for a bank. In Chapter 6, you will learn about managing repairs and inspections. If a bank orders a bid, you need to pick a contractor or vendor within their network. These vendors have gone through arduous qualification processes and have the financial capacity and experience to handle your day-to-day property maintenance for items under $1,000.

Top Three Shady Vendor Tactics

I cannot stress how important it is to pick the right vendors. There are many desperate and unethical vendors out there who will do anything to make a fast buck. They will throw you under the bus with a blink of an eye. These types of people will build you a house for your family with Chinese drywall and not disclose it to you.

Shady Tactic #1: Changing Terms and Holding You Hostage

The first thing to look out for is the “too good to be true” offer. If they say something like “don’t worry about it, pay me whenever” or “you have a year to pay me, it’s no problem,” I want you to leave immediately. What shady vendors do is get you hooked on the low ball offer and then, when you have a good amount of volume coming into their office, they change payment terms on you. They will require you to pay all outstanding invoices within thirty days, or else “they no longer will service your properties.” This usually happens when you need them the most, like during critical emergencies.

Even worse, they will threaten you by calling the sales manager or director of the bank you are servicing and allege you are not paying them and are committing fraud by taking the banks money and pocketing it (remember, the bank reimbursed you). They will hold you hostage because they know the last thing a bank wants is to deal with a money problem from its contracted REO agents. Many banks are traded publicly on a stock exchange, and they abhor bad media. Therefore, be prudent in picking the right vendors.

![]() INSIDER TIP

INSIDER TIP

Always get your vendor payment terms in writing and be very specific about what services are to be performed. If they don’t have a contract already written, they most likely are shady vendors.

Shady Tactic #2: Double Invoicing/Billing

The next shady tactic is the vendor who double bills you for the same work. During the summer of 2010, I received a phone call from Tony, an REO agent who needed my consulting. He had hired one vendor, we’ll call him Joe, who invoiced him for the rekeying of locks for several homes after receiving approvals from the bank.

Six months later, Tony received a statement saying he owed over $5,000 across one hundred REOs. What Joe was doing was invoicing Tony for the rekey of $120, which was paid within his payment terms, but then was additionally invoicing him for “trip charges.”

I quickly did the math and realized Joe was charging him an extra $50 for each time he went out to a property. Obviously this wasn’t included within their agreement, especially since Tony had made it very clear (in writing) that he would only pay what was approved by the bank; so, if the bank approves only $120 to rekey a home, the vendor would receive that and not a penny more or less.

I advised Tony to gather all communications in writing, email, and fax, including the contractor agreement. During Tony’s fact-finding session, Joe had the gall to email Tony, stating, “If you do not pay the $5,000 invoice within five days, I will report you to the director of the XYZ bank; or we can settle this for half—$2,500 today.” Basically, Joe was attempting to extort Tony for false charges in attempt to make a fast buck.

After days of digging up old invoices and emails, Tony emailed Joe proof that he had never agreed to the trip charge services and had sent a carbon copy to his asset manager, followed by a phone call letting him know what was going on. That was the last he heard from Joe.

Six months later, Tony told me he received an email from his asset manager saying that Joe had tried becoming a direct in-network vendor for a bank when they were hiring but was rejected. It turned out, every email and conversation had been recorded in their platform. Because he had tried to make a quick buck, the shady vendor lost out on probably the biggest opportunity in his life. That goes to show you that pulling the wool over someone’s eyes doesn’t work. Karma caught up with Joe.

Shady Tactic #3: Offering You a Spiff

The final shady tactic is the vendor who offers you a commission spiff of each work ordered. For example, if the bank approves you to change a lock on a door and reimburses you $120 for the work, the shady vendor will offer you 10 percent off that so you only have to pay him $120 × .90 = $108.00.

If you get offered any type of spiff, commission, or referral, run as if your building were on fire. It violates your MLA bank agreement, is illegal, and is also completely unethical. Most importantly, when things go bad, as they always do with illegal activities, the vendor will claim you shorted him money and will file a complaint against you to your suppliers. It’s a downward spiral that you want to avoid entirely.

USING TECHNOLOGY—FOLDERS, RULES, AND FORWARDS

The final step in setting up a lean REO machine is using technology. Most of the tasks that need to be completed for REOs are standard for each and every property; nailing down a system that works for one will usually work for others as well.

If you are like the majority of real estate agents out there, you are already incorporating a big portion of technology in your real estate business. If you work from a car, have a smart phone, and have an e-fax, then you are 50 percent done. The other 50 percent is using your current tools to their capacity. When I first started I used Microsoft Outlook, since it was included with my computer. However, I did not have the slightest clue as to the power it had. Once I learned about automating my email messages and creating filters, I freed up one or two hours a day.

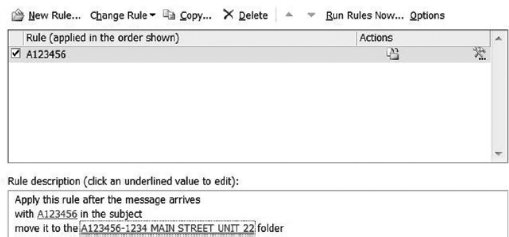

If you want to save a minimum of one hour a day, you need to open up Microsoft Outlook and do the following two things. First, set up new folders. Each folder will have one REO ID as the name. Banks will assign you a REO ID (e.g., A123456), along with the street address of the REO.

The best way we have discovered for you and your team to communicate with each other is through REO IDs. Why? Because when an asset manager contacts you, that is what they will be speaking about. You need to be able to associate an REO ID with its address instantly. Besides, communicating addresses with your team only brings about confusion, as there are many similar addresses with different unit numbers in a complex, and that can waste a good fifteen to twenty minutes of your time. The easiest way is to label each folder with an REO ID as follows:

A101556-1234 Main Street Unit 22

Do this for every single property you are managing. Next, you will create a “Rule” in Microsoft outlook. Any time an email comes in your inbox with either the REO ID or the street address, it will automatically forward to your folder. Don’t worry, it won’t show as if you read the email. It will forward to the folder, and the folder will be highlighted as unread.

To do this, click on any email in Microsoft Outlook. Then, on the top of your screen toward the right, you will see a “Rule” folder. Click on it and hit “Create a rule.” Then follow the instructions. It is pretty straightforward. At the end, your screen should look like this:

The biggest mistake I see new agents making is leaving all of their emails in their inbox. This is a recipe for disaster. At the end of the working day, you should have no new messages. Everything must be read and automatically filtered to your folders. This way, when an asset manager calls, all you do is click on that specific folder, and every single email with that REO ID or address shows up. Then you can quickly find it and be on the same page as the asset manager.

Another nice trick with rules in Microsoft Outlook is forwarding messages to your team automatically without being at a computer. For example, anytime you see an email come into your inbox with the subject “BPO,” you can forward that automatically to your REO analyst or listing specialist by creating a rule.

This way, your team is not wasting time waiting for your email on the next property that is coming in. Remember, banks have a similar feature. They have scripts and programs that automatically assign properties to different REO agents and brokers the same way you will assign rules and automatic forwards to your team.

Finally, you will want to color code your inbox messages depending on importance. Click on any inbox message and then right click on your mouse. Click on “Categorize,” then click on “All Categories.” Follow instructions to assign different colors and short-cuts on your keyboard for different types of emails that come in.

For example, we have the following color codes and short-cut codes per type of email:

- Red—Asset Manager Inquiry (CTRL+F2)

- Green—Offer received from buyer (CTRL+F3)

- Orange—Title response needed (CTRL+F4)

- Blue—Updated needed on file (CTRL+F5)

- Purple—Executed Contract needed (CTRL+F6)

Quick Parts

Quick Parts in Microsoft Outlook is a hidden gem. How many times do you find yourself repeating the same messages to different people?

With Quick Parts from Microsoft, you can pre-type the most frequently asked or requested information about your business in advance and then, when composing or replying to an email, you can choose that message. It’s like a frequently asked question turned upside down. It’s your frequently typed answers or comments ready at your disposal.

QUICK PARTS IS FAQS TURNED UPSIDE DOWN

I discovered this neat feature a long time ago, and it literally shaves off about an hour and a half of time in my day—not to mention how every email I send out is consistent! I’m surprised how many agents do not use this feature.

Here is how it works. After you open up Microsoft Outlook, click “new email” as if you are composing a new message to someone. Next, in the body of the email, type the most frequent phrases you say on a day-to-day basis. Highlight (with your mouse) that phrase, click “Quick Parts” on the top of your screen, and select “Save Selection to Quick Parts Gallery.” Depending on which version of Outlook you have (I use Outlook 2010), the names are slightly different but the concept is the same. You are pre-writing your responses for a future date to save you time.

Once you have all your frequent comments entered, you then can compose a new email message or reply to one. You again click on “Quick Parts” on the top, and this time instead of saving a selection, you scroll down and choose which selection you want to use.

On the next page are the most common Quick Parts I use for different phases in the REO cycle:

- GREAT NEWS! New property. Occupancy check report due in twenty-four hours; BPO due in five calendar days.

- BPO changes needed. Please re-send me the zip file within twenty-four hours.

- Complete bid (scope, contractor bid, addendums, summary sheet) due in seventy-two hours.

- Need status on repair completion by end of business day (EBD) If it wasn’t done properly you need to contact the vendor and tell him to go back to property and complete work. If he objects, email me in writing the circumstances so we can update the system.

- Attached is the complete repair bid.

- X is past due. Please email me X or status on why it is late so we can update the bank platform by EBD.

- Counter offer below. Please let me know whether the buyer “accepts, rejects, or counters” by EBD.

- What is status of closing for X? We need extensions five calendar days prior to closing if it is not going to close. Please advise if we are closing or provide sales extension signed by buyer (remember to name the file correctly: AXXXXXX_Sales Amendment). Need status by 5:30 P.M. today.

- Please email me final executed HUD signed by both buyer and seller so we can turn into our asset manager within twenty-four hours as per bank policy by EBD. Also, please find our attached wiring instructions so you can wire our commissions. It was a pleasure working with you.

- Cash for keys successful. Please enter expense submissions by EBD.

![]() INSIDER TIP

INSIDER TIP

Always assign a deadline in your Quick Parts, whether you’re speaking internally to your team or to an outside vendor. Deadlines create call to actions.

Quick Steps

Quick Steps is an advanced function that Microsoft Outlook provides. Quick Steps allows you to perform multiple steps (forward, reply, erase, move) with multiple emails, all by making one click.

Here’s how it works. Whenever you have standard steps that must be performed, pre-program them in Quick Steps. For example, as soon as you get a new assignment (new BPO order), you have to send various emails either to your listing specialist or to your staff instructing different people to inspect the property, order the rekey, turn on utilities, etc. Because of the sheer volume of properties, you can avoid forgetting certain steps such as turning on utilities by implementing a pre-programmed Quick Step.

Here’s how:

- After you open Outlook, under the HOME tab, click Quick Steps.

- Click New > Custom. The following should show:

- Rename the Quick Step so you can recall it and use it when needed. Example: “rekey, electric, inspection.”

- Following the example above, you want to create three actions: the first is to email your locksmith to rekey the unit, the second is to email your associate to turn on the electric, and the third is to email your associate to do the initial inspection.

- Each action should be a forward, so when you receive your initial assignment by email, simply hit the Quick Step and the email will be forwarded to all three parties. Below is what your Quick Steps should look like, following the above example:

- You should click “Show Options” for each action and insert the body of your message. Remember, since you will be writing practically the same message each time for each of your properties, the body should be standard text. Example for locksmith: “Please rekey the property within four hours and place a lock-box with three keys on the front door.”

- You can also add features, such as sending the message with high importance or flagging the message for review. These are available under “Show Options.”

- Click Finish.

- Now when you receive your initial assignment, simply click on the Quick Step labeled “rekey, electric, inspection,” and you will be able to send three custom pre-written email messages with the click of one button.

Now you can knock out all your emails in one shot. Your emails will be generated all at once, but you will have to use delayed delivery (see Chapter 9) to ensure that the emails are sent at the right time. For example, you want to turn on utilities after the property is rekeyed. Therefore, Quick Steps must be accompanied by delayed deliveries.

By clicking one Quick Step, you can generate pre-filled email messages to assign tasks to your team. There is no limit to the number of prefilled messages you can create. Use this tool as an advanced feature once you master Quick Parts.

Instant Messenger

The most efficient method of communicating with your listing specialists or office team is through an instant messenger chat. This way, you are not wasting valuable time on the phone. Each one of our team members is required to have Microsoft Live Instant Messenger open whenever they are in the office. This way, we can chat and communicate with our team. The greatest benefit of an instant messenger system is that it is free and it saves the entire chat history from day one of your chat. If there are any discrepancies, you can look back to the chat to determine who said what and when.

Email Accounts

Along with instant messaging you want to give each listing specialist or team member a specific company email account. Check with your broker to see if they have extra domain name accounts (for example, [email protected]). If not, you will need to purchase one. Create a team name for yourself and assign each member of your team an email. Example:

This is very important. Do not allow anyone in your team, including your listing specialist, to use anything other than their designated company email (no personal emails). Once you let them go, they will be constantly getting emails and customers will be contacting them, as this is the email they have associated success and REOs with. This intellectual property belongs to you and you need to protect it. Besides, your name is on the line, so you need full control.

![]() INSIDER TIP

INSIDER TIP

Always make your team communicate to all parties in the REO transaction with their company email address. This includes instant messaging internally in the office as well. You will be creating a brand of your company and you want customers to associate your team’s wants with that brand.

![]() SHARE YOUR STORY

SHARE YOUR STORY

Do you have a success story you would like to share on how you implemented the REO Bootstrap Model or REO Plus Model? How about using OVM to bankroll your business? Please logon and submit it for your chance to be featured in the next revised edition of REO Boom:

POINTS TO REMEMBER

- The top three tech time savers that can give you an extra one to two hours a day are: folders, rules, and Quick Parts.

- OVM payables should be negotiated at a minimum of 120 days with three different vendors. Make sure you get what is promised in writing to avoid the three shady vendor tactics.

- You can start the REO business on a shoe-string budget with $1,000 or less.

- The REO Plus Model is the system of standardizing tasks and is lucrative after you achieve thirty active listings so you can spread your fixed costs over volume of properties.

- Use the REO Bootstrap Model when you first start and you have less than thirty active listings on the MLS. It saves you fixed costs (salary, rent), but you’re sharing your listing commission with your team.

- The bigger your network is, the more value you will provide to banks. Build a large pool of customers to attract more banks in your REO footprint.