1.

THE NATURE OF REAL ESTATE INVESTING

Real estate, over time, has been the most consistently profitable investment choice you can make. As long as you research ahead of time, know your market, and pick specific properties carefully, your investment should grow over time. This is true even in light of the depressed market since 2008. This period of time has been among the worst markets for real estate in many years. However, the market inevitably recovers from its negative cycles and comes back as strongly as ever.

This is why right now is a great time for investors to look seriously at the possibility of becoming a real estate investor. For most investors, the first question to ask is how much risk is appropriate. The answer to this question will help in the decision as to whether to proceed as a real estate investor or to look elsewhere.

Most people start out investing in residential property. A single-family house or small multiunit property (two to four units) is manageable and affordable, and you can always step up from there to buy additional properties or exchange your initial investment for larger ones. To get started, you want to define what you hope to achieve by purchasing real estate. Property is far more expensive than most other investments, so you will be making a commitment in most cases to a mortgage. The majority of investment value will consist of borrowed money, so you will depend on rental income to make your investment affordable. Given the potential affordability of real estate (with tenants essentially covering your mortgage payment for you), the consistent historical growth of real estate values, and the exceptionally good tax advantages, the benefits of real estate investing are significant. However, “affordable” is not restricted to net profits but, much more significantly, extends to the cash flow generated by the investment—that is, the comparison between money coming in and money going out. You need positive cash flow or, at worst, a breakeven form of cash flow in a majority of cases. Most investors cannot—and should not—afford to carry negative cash flow from their investments.

AN OVERVIEW OF THE MARKET

Since residential property is, by far, the most common real estate investment, examples in this book focus on single-family housing. Other choices (such as raw land speculation, commercial, and industrial properties) are much more advanced and beyond the interest of most investors.

The residential housing market can be easily studied in any given area. You can readily find information about the local population, employment, rental occupancy and vacancy rates, and the level of new construction under way. These factors add up to the supply and demand for real estate in your city or town. This, then, is the logical starting point if you are thinking of investing in real estate.

![]()

KEY POINT Information about local supply and demand for rental property can be found through local real estate brokers, appraisers, and bankers. Multiple Listing Service (MLS) publications also provide detailed information about property pricing and trends.

VALUABLE RESOURCE To locate Multiple Listing Service (MLS) in your city or town, go to http://www.mls.com.

To find specific properties for sale in your area and to judge the market prices in great detail, even down to neighborhood or zip code, check the many online sources for current listings as well as for recent sales of homes similar to those you are targeting as potential investments.

VALUABLE RESOURCE For a local listing of real estate in your town, check these sites:

SUPPLY AND DEMAND

The supply and demand for residential property involves three distinct and separate markets. First is the market price trend of housing, the best known and understood market. In this market, buyers want to know, first and foremost, what a house will cost. The second market focuses on supply and demand for rental units. Third is the market for available sources of mortgage financing.

The first market can be evaluated in terms of how prices change over time. Are houses selling for more this year than last year? What is the percentage of growth? Housing prices have beaten inflation over many years, with the recent exception in this market beginning in late 2008. The longer-term trend places housing among the strongest of growth investments. Assuming, of course, that you’ve selected property on the basis of good research and sound market analysis, you can expect real estate to be less volatile than the stock market, consistent in its growth rate over time, and safer by far than other alternatives. In many regions, prices have remained flat or have declined, so using national averages is not a safe way to pick a market. You need to check the regional trend to ensure that real estate in your town represents a viable investment. In areas where employment is strong and the population is growing, real estate values tend to grow as well. The market value of property is only the first of three important “markets” in real estate.

The second market involves demand for rentals. What is the average vacancy level? A very low vacancy rate is a positive sign, but a fluctuating or high vacancy indicates that there is more supply than demand. If that is the case, then the timing would not be good for investment, at least not right in your city. The trend between 2008 and 2016 has been for housing prices to decline (over most regions), leading to more people renting than buying. This increased rental level has driven market rentals upward. So as housing costs fall and market rents rise, the market for real estate investors is ideal, consisting of low investment prices along with higher rents.

The third market is that for mortgage money. In 2016, rates were lower than they had been for many years, in the range of 3 percent. This is an extraordinary opportunity for investors, with the cost of borrowed money lower than it has been for many years. However, the rate is not the entire story. Qualifying for a mortgage involves a combination of lending rules and standards, your personal credit history, and the level of equity (your down payment) versus the percentage you would like to borrow. If you do not have money for a down payment or if your credit score is poor, you will face difficulties in getting a mortgage at a desirable rate.

![]()

KEY POINT The combined supply and demand features of the three forms of real estate markets are going to vary from one location to the next, often drastically. The next town over may have vastly different real estate features, and even within one city, the supply and demand can (and does) vary from one area to the next. It is essential to understand the population, employment, market value, and vacancy trends—in advance of committing money.

THE BASIC EQUATION

More details on these essential ideas are covered in later chapters. As an overview, however, a basic equation is an important starting point. The short-term market attributes of rental property are going to affect how well you can afford to invest money now. The whole market is likely to look different in a few years, but you want to make sure you have a reasonable expectation of keeping tenants in the property each month. The equation worth keeping in mind is a balance between how much money you receive (in rent) and how much you have to pay out (in mortgage payments and expenses). For that equation to work, you want to keep the property occupied as consistently as possible. Any time the property is vacant represents lost income, but your mortgage payment continues from month to month.

AN INVESTOR’S POINT OF VIEW

The market for residential real estate is not difficult for most people to understand. If you own a home, you know all about mortgage payments and the importance of being able to afford the payment each month. Anyone who has not yet bought a home knows that landlords expect rent to be paid on time. So the basic economics of real estate are familiar to everyone and are not as mysterious as the market forces at work in other markets, such as the stock market.

In evaluating investments, though, you need to look at properties from a different perspective. When you shop for your primary residence, you are interested in the comfort features, condition, and size of the property. As a real estate investor, you might be willing to buy property that would not interest you as a primary residence but that is ideally suited for rental purposes.

EXAMPLE: You have a growing family and need a house with several bedrooms for your own use. However, you have discovered that relatively small houses make excellent rentals. A two-bedroom house in modest condition is relatively inexpensive compared to other types of properties and is easy to keep occupied. A married couple or single person is drawn to such rentals and can afford what you will need to ask in rent, so such properties are easier to keep occupied than more expensive, larger homes would be.

![]()

In this example, your revaluation of the market would be made with rental income and payments in mind, rather than from the point of view of a homeowner. The investment attributes of your decision are going to be far different from your personal requirements.

![]()

KEY POINT When you search for investment properties, your criteria are far different than what they are for your primary residence—a primary distinction to keep in mind.

The real estate market has grown in value over time, even though recent trends have been negative. This is a national average, of course, and all real estate is local. This means that it is essential to understand the local features of supply and demand before investing. You cannot depend on national averages or even on local trends for the long term. If local property grows in value over fifteen or twenty years in the future, that is a promising feature. At the same time, you need to ensure that rental demand is strong right now, in order to cover your mortgage payments. As you look for potential rental investments, try to locate properties that are affordable, most likely to maintain value (and grow in value), and appealing to likely tenants.

REASONS TO INVEST IN REAL ESTATE

There are many good reasons to buy real estate. Among the most important reasons—assuming the local market conditions make it a viable choice—are the following:

![]() Diversification and Asset Allocation. Sound investment requires spreading capital over dissimilar investments. You would not want to put all of your capital into a low-yielding savings account, or into a single stock, or into real estate. You are better off diversifying your capital. You may wonder: If real estate is sure to grow over time, why not put all of your money into rentals? Diversification is important because different investments have different attributes. The stock market is volatile and you can make or lose money quickly; however, your money can be invested or taken out quickly. Savings accounts are safe but yield very little. Well-selected real estate is going to increase in value over time, but it is very difficult to get your money out if you need it for an emergency. You need to diversify your capital so that you have some funds available as you need them, some funds in very safe investments, and some in investments likely to grow over time.

Diversification and Asset Allocation. Sound investment requires spreading capital over dissimilar investments. You would not want to put all of your capital into a low-yielding savings account, or into a single stock, or into real estate. You are better off diversifying your capital. You may wonder: If real estate is sure to grow over time, why not put all of your money into rentals? Diversification is important because different investments have different attributes. The stock market is volatile and you can make or lose money quickly; however, your money can be invested or taken out quickly. Savings accounts are safe but yield very little. Well-selected real estate is going to increase in value over time, but it is very difficult to get your money out if you need it for an emergency. You need to diversify your capital so that you have some funds available as you need them, some funds in very safe investments, and some in investments likely to grow over time.

A more sophisticated view of diversification is called asset allocation. This is a strategic planning technique in which a portfolio is spread among many different markets or segments. While diversification usually refers to spreading risks within one market (buying many different stocks), asset allocation is broader. For example, you may want to have some money in ready-cash accounts as an emergency reserve fund; other capital invested in stocks, whether owned directly or purchased through a mutual fund; and yet more of your capital invested in real estate. These three markets represent completely different levels of risk and opportunity, and each is going to perform according to very different market forces.

Real estate is a superb market for asset allocation because of its strong historic attributes. Your ability to allocate capital among dissimilar markets protects your capital from cyclical changes. In times when the stock market is weak or falling, real estate may be strong. In fact, it is likely. Offsetting profit and loss effects of stocks and real estate occur time and again.

Diversification within a single market and asset allocation among many different markets are sensible portfolio management techniques. Real estate is a good fit for strategic asset allocation. It is different from the stock market, however. Investors wanting to get out of stocks for the moment but who plan to go back in a few months later have to decide where to place capital, either in other stocks or in different markets. Real estate is a longer-term investment, though. So if you plan to employ real estate in your asset allocation plan, it should be treated as a longer-term decision. You do not want to buy real estate in March and then look to sell it in June in order to put capital back into the stock market. That would be an expensive and, given closing-cost levels, a difficult move to make profitably.

![]() Cash Flow. With most investments, you place cash in someone else’s care, then you receive dividends, interest, or capital gains. You are 100 percent invested, and there is little or no question of cash flow. With real estate, you usually make a down payment and finance the lion’s share of the investment; so cash flow becomes critical. Most real estate investors depend on rental income to cover their mortgage payment. The bad news: If you do not keep the property rented every month, you have to make the mortgage payment from your other funds. The good news: If you keep the property occupied, then tenants’ rental payments are used to make those mortgage payments. In this situation—and given no unexpected extra expenses—the property pays for itself. When you purchase properties at the right price for your local market and when rents are high enough to cover your mortgage payment, you will have a positive cash flow. When you consider the tax benefits of reporting losses (which are created because you are also allowed to depreciate your rental property), it is possible to have positive cash flow and, at the same time, a net tax loss. This seemingly contradictory situation is quite common. When the tax benefits from net losses with depreciation create monthly tax savings, you can enjoy the best of both worlds: having tax losses to deduct while you collect more cash than you pay out.

Cash Flow. With most investments, you place cash in someone else’s care, then you receive dividends, interest, or capital gains. You are 100 percent invested, and there is little or no question of cash flow. With real estate, you usually make a down payment and finance the lion’s share of the investment; so cash flow becomes critical. Most real estate investors depend on rental income to cover their mortgage payment. The bad news: If you do not keep the property rented every month, you have to make the mortgage payment from your other funds. The good news: If you keep the property occupied, then tenants’ rental payments are used to make those mortgage payments. In this situation—and given no unexpected extra expenses—the property pays for itself. When you purchase properties at the right price for your local market and when rents are high enough to cover your mortgage payment, you will have a positive cash flow. When you consider the tax benefits of reporting losses (which are created because you are also allowed to depreciate your rental property), it is possible to have positive cash flow and, at the same time, a net tax loss. This seemingly contradictory situation is quite common. When the tax benefits from net losses with depreciation create monthly tax savings, you can enjoy the best of both worlds: having tax losses to deduct while you collect more cash than you pay out.

![]() Leverage. Most individuals cannot afford to buy property outright and pay cash, just as most homeowners cannot afford to pay for their own homes all at once. One attribute of real estate investing is the need, in most cases, to finance 70 percent or more of the purchase price. As a strategic approach to investing, leverage is recognized as an important and advantageous method to use. Leverage means employing a limited amount of capital to purchase and control a greater value in investment. You would not be likely to borrow money to buy stocks because the stock market is an uncertain and risky place. However, properly selected and researched real estate is far less likely to lose market value. Not only does real estate tend to grow in value over time when other economic factors are positive; it is also insured through a fire insurance policy, and investors have direct control over the investment. Ownership in stock is uncertain and less tangible, but, given the features of locally owned and managed real estate, leverage makes a lot of sense.

Leverage. Most individuals cannot afford to buy property outright and pay cash, just as most homeowners cannot afford to pay for their own homes all at once. One attribute of real estate investing is the need, in most cases, to finance 70 percent or more of the purchase price. As a strategic approach to investing, leverage is recognized as an important and advantageous method to use. Leverage means employing a limited amount of capital to purchase and control a greater value in investment. You would not be likely to borrow money to buy stocks because the stock market is an uncertain and risky place. However, properly selected and researched real estate is far less likely to lose market value. Not only does real estate tend to grow in value over time when other economic factors are positive; it is also insured through a fire insurance policy, and investors have direct control over the investment. Ownership in stock is uncertain and less tangible, but, given the features of locally owned and managed real estate, leverage makes a lot of sense.

WEIGHING THE PROS AND CONS

The overall benefits of investing in real estate—combining growth, safety, and tax features—make it a choice worthy of serious consideration. You cannot expect this beneficial combination from any other investment. While cash invested in real estate is difficult to take out (because it can be removed only through refinancing or selling in most cases), the overall benefits of real estate make it worthwhile, especially if you balance your capital between real estate and other areas.

Even with all of the long-term benefits of real estate investing, however, you should expect to face some problems as a real estate investor. The need to borrow money to buy property is a significant risk, so you must be prepared to live with debt. There can be unanticipated expenses, such as for repairs, property tax hikes, or utility rate increases. Neighborhoods can change for the worse, the local economy can fall apart, or a large employer may close down or move away.

Another potential problem area involves dealing with tenants. The landlord–tenant relationship is usually amiable and fair. It is occasionally emotional or illogical. As a landlord, you accept the risk that some tenants will not be pleasant to work with. This is one feature of real estate that discourages many people from proceeding. If your temperament is inappropriate for dealing with tenants, then you should not buy real estate. At the same time, if the risk of problems can be mitigated by checking references, and if you are willing to go through those steps, then you will increase your chances for a positive, enjoyable, and profitable experience.

![]()

KEY POINT You should be aware of these potential problems, large and small, before you get into real estate investing, but many people find that the positives far outweigh the negatives.

THE IMPORTANCE OF TAX PLANNING

The benefits of real estate are difficult to ignore, and they make a strong case in support of including real estate in your portfolio. Equally important, tax planning requires serious thought and continually looking ahead. Anticipating potential tax-related problems in the future is always a necessary move, not only in managing your investments but generally as well. Real estate investors need to plan. The obvious reason—to reduce current-year tax liabilities—is only one part of the larger picture. Of course, you want to time decisions as much as possible to minimize taxes. The second part has to be kept in mind as well: the limitation on annual deductions. This comes in two forms: dollar amount and your income level.

ANNUAL DOLLAR LIMIT

The dollar amount is set at $25,000. You can deduct that much per year as long as your family income is at or below $100,000. If you are married but separated, or if you are single, the dollar amount may be lower, or it could even disappear completely. So married couples living apart and contemplating divorce need to plan carefully to minimize the tax consequences of divorce when real estate investments are involved.

In situations where you believe your tax losses will exceed $25,000, you will have to carry the excess over to future years or to the time you sell your investment property. This requires planning. For example, you can defer current-year expenses to next year to avoid spending money for deductions you do not need. You can also extend the time you use to depreciate assets, to reduce current-year expenses, and to move deductions to future years.

INCOME LEVEL

The second consideration is your overall income. If your annual adjusted gross income, as calculated for real estate tax purposes, exceeds $100,000, you lose 50 cents in deduction for each dollar above. For example, if your income this year will be $110,000, your ceiling will be reduced by one-half of the income above $100,000. So half of $10,000, or $5,000, is applied against the ceiling of $25,000, and your maximum loss will be reduced to $20,000 for the year.

![]()

KEY POINT Deferring payment of expenses or extending depreciation until later years makes sense if you cannot take full advantage of those deductions this year. Planning for tax purposes is an essential and important feature of investing in real estate. If you are not thoroughly versed in tax law (including the laws in your state), you should consult with a qualified tax expert and get assistance in planning ahead for tax benefits or for the consequences of decisions you make throughout the year.

YOUR CREDIT APPLIED TO REAL ESTATE INVESTING

One important consideration for every real estate investor is often overlooked or not mentioned at all. That is the quality of your personal credit. Because you will be borrowing money to buy rental properties, lenders will be keenly interested in your credit standing.

Homeowners—even those with poor credit—may be able to find a lender willing to carry a loan. This is because owner-occupied property is very low risk, and lenders recognize this fact. In comparison, investment property loans are more likely to be foreclosed. If the demand for rentals falls and investors cannot meet their mortgage obligations, it is possible that the investor will simply walk away from the investment. So lenders are sensitive to the possibility of default on investment property mortgage loans. If an investor’s credit is not impeccable, it will be more difficult to find loans. With the higher-risk levels in mind, lenders require higher down payments for investment property; lenders may also require higher loan points and other fees, just to offset their higher risks. The standards are higher, and for good reason.

WHAT THE LENDER MIGHT REQUIRE

If your credit rating is less than perfect, you may have to meet a series of extra requirements. These could include:

![]() Higher down payment requirements, so that you have more invested capital at stake, which in turn reduces the likelihood that you will just walk away from the loan obligation if the costs of keeping the property get too high

Higher down payment requirements, so that you have more invested capital at stake, which in turn reduces the likelihood that you will just walk away from the loan obligation if the costs of keeping the property get too high

![]() Higher loan origination and other fees, charged to reduce the lender’s risk of default on your part

Higher loan origination and other fees, charged to reduce the lender’s risk of default on your part

![]() Closer scrutiny of financial information and more reporting than usual, so that loan underwriters will be confident that the information you provide is accurate and complete

Closer scrutiny of financial information and more reporting than usual, so that loan underwriters will be confident that the information you provide is accurate and complete

![]() More appraisal, inspection, and other outside fees, to ensure that the property being financed does not have hidden maintenance costs or is not overvalued

More appraisal, inspection, and other outside fees, to ensure that the property being financed does not have hidden maintenance costs or is not overvalued

![]() A higher interest rate on the loan itself, due to the higher level of risk to the lender

A higher interest rate on the loan itself, due to the higher level of risk to the lender

INCOME VS. OBLIGATIONS

If your income is too low to qualify for the loan you seek, you will have to put more money down or simply wait until your income level rises. You may also need to start out with a less expensive property so that your income will qualify you for the investment. Although different lenders employ many variations of the basic strategy, they all look at the numbers in the same way. They calculate your net monthly income (your take-home pay) and then take a percentage of that as the maximum obligation they will accept for your mortgage payment. (The “obligation” usually includes mortgage principal and interest, property taxes, and insurance.) If the payment goes over that level, the loan will be rejected in its present form. You may need to reduce the obligation by making a larger down payment, for example.

When you fill out a loan application, you are required to estimate monthly obligations as well as monthly rental income. A lender is probably going to reduce the estimated income you report to allow for possible vacancies. The degree of adjustment will depend on recent vacancy levels in the area, a statistic that the lender will know or have access to. So your total net income will include your take-home pay, any other income (from dividends and interest, for example), and rentals (adjusted downward for the vacancy factor). The net total of this calculation is then multiplied by a specific percentage that the lender uses to qualify investment property mortgage loans. If the total obligation exceeds the predetermined percentage of total income, the lender will not approve the loan.

![]()

KEY POINT The review of your loan application will be much easier if your credit is excellent. The better your credit, the easier it will be to find acceptable financing. For anyone with poor credit, the flexibility of being able to finance properties, without concern for being rejected, is going to be curtailed. That does not mean it will be impossible to find a loan, but the loan is going to be more expensive, and review time is likely to be greater as well.

GETTING PREAPPROVAL FOR YOUR LOAN

Prospective first-time homeowners can find a lender to prequalify them. Based on income level and credit history, the borrower can find out what level of investment the lender can and will approve. The lender reveals the maximum loan it will grant based on the borrower’s financial information. The preapproval is conditional because the lender also wants to ensure that the property being purchased is worth what the homeowner intends to pay and that its condition is acceptable for lending purposes.

The preapproval of a mortgage loan for investment purposes is not quite as easy. Because the equation includes rental income, it will be impossible for the lender to assess the borrower’s overall income and obligation without the specific property in mind.

You may be able to obtain conditional preapproval from a lender. The qualifications will include the usual appraisal and condition standards but will also go beyond that to require acceptable rental income after deducting an estimated vacancy factor. Assuming that the lender would qualify you on the basis of a comparison between total income and mortgage obligation, you may receive a type of preapproval even when your credit is not perfect. At least a lender may be willing to stipulate that your application will be given serious consideration. Some lenders won’t go that far, making it clear that they will not approve loans if your credit is poor, regardless of property value and condition.

Poor credit is also the reason lenders are less likely to approve an equity line of credit. Most lenders limit lines of credit to primary residences, although some allow borrowers to take Home Equity Line of Credit (HELOC) contracts on rental properties—but as a rule, this exception is allowed only if the borrower’s credit is exceptional.

MAINTAINING INVESTMENT PERSPECTIVE

In every type of investment, you are wise to keep your perspective. For example, if you buy shares of stock because a stranger on an investment chat room tells you its price will go through the roof, you have no one but yourself to blame if you lose money. If you invest because a stockbroker tells you it’s a “good” investment and that turns out not to be true, then it means your trust was misplaced.

The same caution applies to real estate. Success in investing is the result of thorough research; the identification of sound, sensible investments in strong markets; and ongoing maintenance. (In the case of stocks, you want to hold shares as long as value is rising and the fundamental strength is high and then sell when conditions change. In the case of real estate, maintenance means finding the best tenants and then keeping an eye on the property.)

There are no easy ways to accumulate wealth. Yes, some people have made fortunes in real estate by buying in the right place at the right time, but it is also true that they took risks and worked to acquire and maintain their properties. If you discover that you are simply not satisfied with your investments, you should sell and get out. For a stock investor, this means selling the shares if you spend your nights lying awake and worrying. For a real estate investor, you should not have to dread your telephone ringing, fearing it is a tenant calling with a complaint. If you have to fight every month to get your rent or if you even worry about the possibility of such problems, then real estate is not right for you.

RISK TOLERANCE

Maintaining your perspective also has to include an ongoing evaluation of long-term goals and your personal risk tolerance. Keeping real estate for the long term should be coordinated with a specific idea that you have about your reasons for wealth accumulation, matched with your expectations for growth in real estate values (all on an after-tax basis, of course, because real estate tax benefits are significant). Risk tolerance has three major aspects when real estate is involved. These are:

1. Tenant Issues. The most important level of risk involves your relationship with tenants. This is far more important than investment value or cash flow. Even if your investment works well on paper, tenants can affect your quality of life directly—especially if they are giving you trouble. If your experiences are negative, then you have exceeded your risk tolerance. The problem has to be fixed (which may be as easy as replacing a poor tenant with a good one); otherwise, it makes no sense to keep the properties. In the end, the whole experience has to be enjoyable for you.

Many investors have problem-free relations with tenants; others have not had universally positive experiences. The potential problems vary by area, due to the relative strength of landlord–tenant laws. In some states, tenants have very strong rights, which may lead to the abuse of landlords. In those states, you could have great difficulty if you end up with a tenant who does not pay rent, and it could take many months to evict a problem tenant. In other states, the laws are less complex or are even favorable to landlords.

2. Market Value. The best known form of investment risk is the change in market value. Is your property value growing? On a month-to-month basis, tenants are expected to pay rent adequate to make your mortgage payment; so over the long term, you should be able to accumulate equity through rents. However, the risk exposure is worthwhile only if property values are rising as well. If market value is not growing, you might consider selling the property and investing in one with more potential.

3. Cash Flow. Of course, you want rental income to cover your mortgage payment and other expenses. An after-tax positive cash flow is desirable, and a prolonged period of negative cash flow can destroy your family’s budget. This form of risk tolerance has to be well managed in order for your investment to work.

Managing each of these potential forms of risk requires planning on your part.

DEALING WITH TENANTS

You reduce the risk involved in having to deal with tenants through proper selection and by checking credit and personal references. The majority of problems faced by landlords can be traced to lax procedures in checking references or misplaced trust.

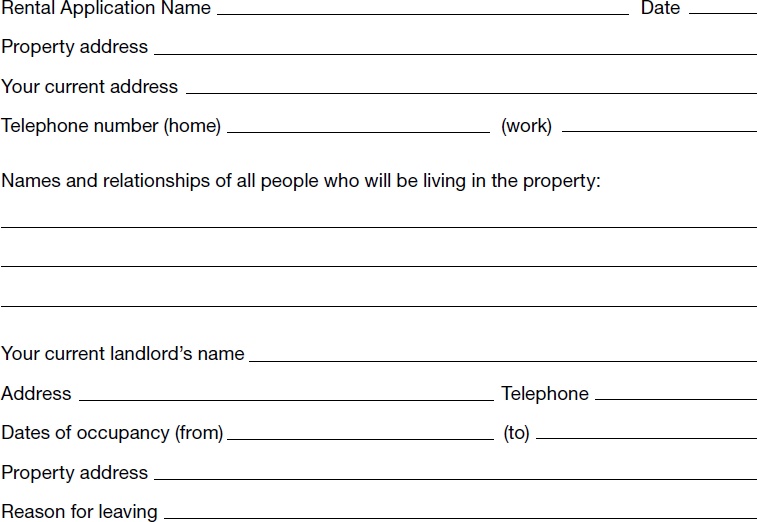

Screening Tenants. If rental demand is high and stable, you will be able to select from among many applicants. When vacancies are low—5 percent or less—you may receive more than a hundred responses to a single newspaper ad. You need to get a written application from tenants. This is the first step in checking whether tenants can provide the basic information you need—employment verification, current landlord’s name, a bank account reference, and monthly salary verified with copies of recent pay stubs. Use a form such as the one shown in Figure 1-1, and require all applicants to complete it.

Some applicants will fail to fill out the form, meaning that they know they cannot refer you to their previous landlord, that they do not have a bank account, or that they have no income. Any of these problems disqualify the person based on even a cursory review. Therefore, simply requiring a written application is a necessary first step.

![]()

KEY POINT Look for applicants who have jobs, a current bank account, a local address, and a record of no evictions. You will discover that people lacking these important features will apply for your vacant rental, even though they have no reasonable expectation of making rent payments. Verification (including calling the person’s employer to confirm income) is essential.

Checking References. The second step is checking all references. The importance of checking references—even when your instincts tell you that all is well—cannot be emphasized too much. Confirm the bank account to make sure it exists and is not currently overdrawn. Call both current and past landlords to determine whether they will provide positive recommendations. If the applicant does not provide you with both landlord references, or if they simply don’t have references to give you, that should disqualify them. For example, if an applicant claims to have been living with his parents, you have no reliable way to determine what kind of tenant he will be. Another potential problem is that the current landlord might be so motivated to get rid of the tenant that the reference will not be objective or accurate. This is why you also need to talk to a past landlord.

Also talk to the employer. Are the reported salary level and dates of employment accurate? You also want to make sure that the individual does in fact have the job and is in good standing. At this stage, you simply want to verify the information the applicant has provided to you. There is no way to ensure that employment will continue into the future, and this step is intended only for initial fact-checking.

If the applicant is self-employed, you cannot verify income in the same manner. You will need to get a copy of the person’s bank statement for the past two or three months to ensure that deposits are going into the bank. There is no reason to reject an application just because the applicant is self-employed, but, as with all forms of information, you need to be able to verify what you’re told on the application.

Reviewing Credit History. You may want to collect a small fee from the applicant to run a credit check. The cost is usually about $15, although you will need to subscribe to a service and obtain written permission from the tenant applicant. If the would-be tenant does not provide all the information you need or is unable to give you verifiable references, look elsewhere.

Checking Legal History. It is also easy in most states and counties to check legal history, since that information is a matter of public record. You can go to the clerk of a municipal or superior court and provide a name to be searched. From this search, you can discover—usually for no fee—whether a person has ever been evicted in that county or convicted of any crimes.

Being Alert to Warning Signs. Some tenants cannot afford the rent you are asking. They may try to barter with you for part of the rent by “doing work around the place,” or by performing landscaping chores (which is their responsibility already in most cases), or by offering to paint the house. These are warning signals. You are probably not going to have a positive experience in hiring tenants in exchange for rent for any purpose. If the tenant cannot afford to pay the full amount of rent, the application should be rejected.

Renting Month to Month. If you are unsure of how long you wish to rent to a specific tenant, offer a month-to-month arrangement rather than a lease. The month-to-month option protects you; if the tenant does not pay rent, it is easier to give notice under a month-to-month arrangement. Having a lease gives you a legal contract, but if the tenant is a deadbeat, it is unlikely that you will be able to collect what the person owes you. The month-to-month idea may make more sense.

Using a Management Company. You could also hire a management company to deal with tenants directly. This service will cost you a percentage of rents collected, and some management companies are better than others. So, even if you hire a company, you need to check it out beforehand as well. Join a local landlords’ association, if there is one, and ask other members for referrals to local management companies.

KEEPING AN EYE ON MARKET VALUE

The best way to reduce the risk of stagnation in market value is with advance research. You should know your local market before you buy. That market includes the recent historical price trends for housing, as well as occupancy trends and market rent levels in rental housing. While current trends are not going to continue forever, you can certainly determine whether current conditions are strong or weak. You want to buy in a market where properties are available for attractive prices, but rental demand is high. This is the best of all conditions, especially if the cyclical supply and demand factors are timed in your favor. If real estate prices rise during the time you own the property, you benefit in several ways: from year-to-year tax benefits, tenant-paid mortgages, and positive cash flow.

What should you do if and when the market softens? The property value itself may go through many cycles over the long term, so you may need to be patient and wait out the cycles. If employment in your city or town is strong and people are moving in instead of leaving the area, demand will continue to grow for real estate. If current building trends are exceeding demand but economic trends support long-term holding of your real estate, you may need to wait out the market. The situation is far different when the market for rental units goes soft. If there are more rentals in town than there are people wanting them, you could face a more immediate problem: the loss of rental income. If you believe your investment is not growing quickly enough, or if you experience higher than expected vacancies, you should keep open the possibility of selling. There is no sense in remaining invested in real estate or any other market if you are not experiencing strong cash flow and market value growth.

MANAGING CASH FLOW

The real test of real estate investments is cash flow. You need to break even at the very least, when you take tax benefits into account. If you have high vacancies, you have to pay mortgage, insurance, taxes, utilities, and maintenance out of pocket, since these expenses are not being covered by rental income. With the tax benefits in place with fully occupied properties, you don’t need the tax write-off you get when properties are vacant. The solution to cash flow problems is based in careful research before you buy. Be sure you know the demand market for rentals, and pick properties whose mortgage payment, taxes, and interest can be covered through rental receipts. Also make sure that vacancies for rental properties are consistently low before you put money into rental investments. Negative cash flow is never a good thing, so you need to take steps to avoid finding yourself paying out more than you are bringing in.

RESEARCH AND ADVANCE PLANNING

The nature of real estate investing includes many benefits as well as risk. Dealing with tenants, keeping an eye on market value, and managing cash flow are all easily handled when you select properties and tenants well. In each case, research and investigation will reduce or eliminate surprises, which you do not want once you have committed yourself to an investment. Always begin by selecting properties in strong, healthy markets—that is the essence of all types of investments. Stockbrokers should help you to pick stocks that rise consistently year after year. Similarly, real estate investors seek to invest in areas where market demand is strong, not only among potential buyers but also among prospective tenants.

Doing research ahead of time is a key first step if you are contemplating entering the real estate market. By avoiding problems before they arise, your experience will be both positive and profitable.