5.

BOOKKEEPING BASICS FOR RENTAL PROPERTY

Some real estate investors make a dangerous assumption: The record-keeping part of the business is easy and can be done by a friend, a spouse, or an online system. These ideas are not bad ideas on their own merit, but if you lack the basic knowledge of how to keep records and why it is important, you could overlook some of the essentials. Many investors do not realize how complex real estate transactions can be, especially during times of repairs or working on fixer-upper properties.

MISTAKES WORTH AVOIDING

To start a discussion of basic bookkeeping, here are some useful guidelines:

1. If you don’t know anything about record keeping, hire someone who does.

2. Don’t make the mistake of thinking that software is a substitute for knowledge. If you don’t know how to keep books, admit it before you try to set up a system.

3. Don’t complicate matters; keep things simple. Complicated records inevitably become poorly kept records.

4. Set up a bank account only for real estate income and expenses. Do not keep records in which you mix business transactions with personal ones.

5. Back up your system with copies kept on a different drive.

6. Study the results, and make sure you understand the tax planning aspects of your transactions.

SPECIAL SITUATIONS

You must meet special requirements for tracking and reporting rental activity. This is not difficult. It just means that you need to set up your record keeping so that you are able to comply with tax reporting requirements.

A few special considerations make rental property bookkeeping different from most other types of business records. You need to allocate expenses between two or more rental properties and divide expenses when they apply partly to your personal residence and rental investments. In addition, some calculations do not apply to other types of investments (such as depreciation and a breakdown between mortgage principal and interest).

TYPES OF TRANSACTIONS

Most investors are aware of record-keeping requirements and tax reporting for capital gains, interest, or dividend income, and of limitations on claiming losses. When you also own real estate, you need to keep track of rental income as well as payments and expenses. Aside from the reporting rules, you also want to track cash flow and anticipate possible future problems. For example, if your rental property is financed with a variable-rate loan, an increase in your rate could mean a change from marginally positive cash flow to negative cash flow. Recognizing this problem, you are faced with the choice of raising rents or absorbing the negative number. The same problem can occur when your property taxes or utility bills are increased. Your rental agreement may provide that increases in property taxes will be automatically passed on to tenants, which will protect your cash flow. If utility expenses rise, you may either raise rents or pass on the utility burden directly to the tenant.

![]()

EXAMPLE: One landlord faced rising utility costs and higher property taxes. However, the rental agreement was month-to-month rather than a lease, so there was no provision for passing increased costs on to the tenant. As an alternative, the landlord advised the tenant that, effective two months later, he would be responsible for the water and sewer bill. The tenant agreed.

![]()

In this example, the landlord covered the increased costs by modifying the rental agreement. However, he did not increase the monthly rent. From the tenant’s point of view, the net result is the same, but accepting responsibility for a utility bill may be perceived differently. (Tenants may feel that they have more direct control over utility costs.)

WHAT TO RECORD

Record keeping helps you to anticipate changes in cash flow as well as to keep track of the required tax records. The transactions you should track include:

![]() Rental Income. You need to record rental income you receive and deposit that income in your bank account.

Rental Income. You need to record rental income you receive and deposit that income in your bank account.

![]() Mortgage Payments. Your monthly rental property mortgage payment consists of principal and interest and, in many cases, property taxes and insurance as well. The mortgage principal reduces your mortgage debt, but it is not deductible. You need to calculate monthly interest expense. Some lenders break this down each month for you, but others do not. Therefore, you should know how to calculate this cost (see Chapter 2). The impounds you pay each month for property taxes and your insurance payments are rental expenses and should be recorded in the proper account. If you pay property taxes and insurance separately and not as part of your mortgage payment, those payments are recorded as expenses.

Mortgage Payments. Your monthly rental property mortgage payment consists of principal and interest and, in many cases, property taxes and insurance as well. The mortgage principal reduces your mortgage debt, but it is not deductible. You need to calculate monthly interest expense. Some lenders break this down each month for you, but others do not. Therefore, you should know how to calculate this cost (see Chapter 2). The impounds you pay each month for property taxes and your insurance payments are rental expenses and should be recorded in the proper account. If you pay property taxes and insurance separately and not as part of your mortgage payment, those payments are recorded as expenses.

![]() Utilities. If you pay utilities yourself, these payments are deductible as rental expenses. If your property is used partly as a rental and partly as your residence, then only the rental portion is deductible. The portion you can deduct is calculated based on usage. For example, if you rent out 30 percent of your floor space, you can deduct 30 percent of the utilities. Or if you rent out your property for three months of the year, you can deduct 25 percent of utilities paid for the entire year.

Utilities. If you pay utilities yourself, these payments are deductible as rental expenses. If your property is used partly as a rental and partly as your residence, then only the rental portion is deductible. The portion you can deduct is calculated based on usage. For example, if you rent out 30 percent of your floor space, you can deduct 30 percent of the utilities. Or if you rent out your property for three months of the year, you can deduct 25 percent of utilities paid for the entire year.

![]() Advertising. Payments to advertise a property for rent are deductible.

Advertising. Payments to advertise a property for rent are deductible.

![]() Legal and Accounting Fees. You may need to consult an attorney regarding contract questions and tenant relations, and you may need help from an accountant or tax adviser to assist with your tax return and tax planning. These are deductible expenses when the consultation relates to your rental properties.

Legal and Accounting Fees. You may need to consult an attorney regarding contract questions and tenant relations, and you may need help from an accountant or tax adviser to assist with your tax return and tax planning. These are deductible expenses when the consultation relates to your rental properties.

![]() Auto Expenses. If you use a personal car or truck for rental activities, that portion of use is deductible as a rental expense. The most practical method for claiming a deduction for business use of your automobile is on a miles-used basis. Keep good records of mileage and actual use.

Auto Expenses. If you use a personal car or truck for rental activities, that portion of use is deductible as a rental expense. The most practical method for claiming a deduction for business use of your automobile is on a miles-used basis. Keep good records of mileage and actual use.

![]() Telephone. Like auto expenses, you can deduct business use of your telephone, but you need to keep thorough records to document that business use.

Telephone. Like auto expenses, you can deduct business use of your telephone, but you need to keep thorough records to document that business use.

![]() Office Expenses. You need to purchase record-keeping items such as accounting worksheets, binders, folders, and signs (to advertise properties for rent, for example). These expenses are deductible on your tax return as long as they relate specifically to rental property management activities.

Office Expenses. You need to purchase record-keeping items such as accounting worksheets, binders, folders, and signs (to advertise properties for rent, for example). These expenses are deductible on your tax return as long as they relate specifically to rental property management activities.

![]() Depreciation. The depreciation of properties is a noncash expense, which is calculated annually based on the cost of your property. You cannot depreciate the value of land, but all improvements in the building (e.g., any major additions and repairs) are depreciated annually.

Depreciation. The depreciation of properties is a noncash expense, which is calculated annually based on the cost of your property. You cannot depreciate the value of land, but all improvements in the building (e.g., any major additions and repairs) are depreciated annually.

![]() Amortization. If you pay loan fees (also called points) when you finance your rental property, you may not be allowed to deduct that expense in one year. Points often have to be amortized over the life of the loan. For example, if you pay $2,700 in total points and your loan is scheduled to be repaid over thirty years, you are allowed to deduct $90 per year.

Amortization. If you pay loan fees (also called points) when you finance your rental property, you may not be allowed to deduct that expense in one year. Points often have to be amortized over the life of the loan. For example, if you pay $2,700 in total points and your loan is scheduled to be repaid over thirty years, you are allowed to deduct $90 per year.

CASH ACCOUNTING

Most individuals report their income and pay taxes on a cash basis. That is, you report income and deduct expenses only in the period they are paid. So expenses such as property taxes can be deducted only when you pay them. If you are charged $400 in legal fees toward the end of December, but you do not pay the bill until January, the expense is deductible in the later year when you use the cash accounting basis.

With rental properties, there are two exceptions to this rule:

1. Rental income is deducted in the year the rent is earned, even if payment is early or late. So if your tenant pays January’s rent on December 30, it still is assigned to the following year.

2. Interest works in the same way; you are allowed to deduct interest only in the period to which it applies. If you prepay your January mortgage payment hoping to get the additional interest expense into the current year, it will not work. It is deductible in the following year.

MATCHING RENTAL INCOME AND BANK DEPOSITS

Keeping track of rental income is a fairly simple process. The easiest way is to ensure that your bank deposits match your income. To keep your records as clear and as simple as possible, follow four rules:

1. Set up an account to be used only for rental income and payments. Because you will have a volume of rental-related income, expenses, and payments, your bookkeeping will be clarified significantly if you set up a special account and use it only for rental activity. Some real estate investors try to track their income and payments through their existing accounts, but that is difficult to do consistently. Even if it costs you money to set up a new account, it is the best way to keep things clear. The bank charges are going to average about $7 per month on average, and you may even be able to make arrangements for free checking.1

2. Deposit all rental income into the investment account. It is most important that your deposits match your reported rental activity. All income you receive, whether made by check or cash, should be deposited into your investment account. In this way, your record of deposits will match what you report on your tax return. The “source document” for rent is going to be the rental agreement you sign with a tenant, but the real documentation is going to exist in the records you keep of bank transactions. The rental income you deposit in your investment account will be used for mortgage payments and other expenses; use the checking account as a simple way to keep track of all of your rental activity.

3. Identify all nonrental deposits made. If your rental income falls short of your payment obligations, you will need to make additional deposits periodically. Be sure you identify those deposits specifically, in order to be able to explain the source of all deposits. Identify the deposit at the time you write it into your checking account. So when you deposit rental income, identify it as income (and if you have more than one rental property, you should also list the property address). When you transfer money from your personal account, identify it as a transfer. This will simplify your record keeping and reporting. A written record of changes in your account balance can be maintained in a traditional checking register, a journal like the one in Figure 5-1, or online in various formats. Today, many investors use software to track and maintain their books, for example.

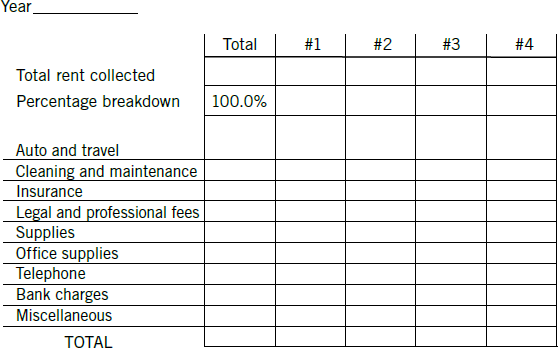

4. Set up a simple receipts journal, and keep it current. Your checking account is an excellent convenience for capturing all of your investment-related activity. (Incidentally, you can also use the same account to track investment activity in stocks and mutual funds by expanding the breakdown of deposits and payments. In this manner, all of your investment activity can be reported in a single record, and it is isolated from your personal records. This makes it easier to document what you report on your tax return, including rental income and payments, dividend and interest income, capital gains and losses, and transfers of capital in and out of other investments.) A comprehensive receipts journal that includes space for tracking all of your investment activity is shown in Figure 5-1. Note that in this sample journal, rental income is identified by specific property; space has been allowed for up to four properties. You need this breakdown for your federal income tax return.

Software like Quickbooks and similar products are easy to use and have largely replaced the need for handwritten journals and ledgers. Books can also be maintained very simply on Excel and other spreadsheet programs.

IMPORTANT The total column should match your bank deposits without exception. It should also balance with the sum of all other columns, which is an additional procedure for double-checking your figures and keeping your receipts journal in balance.

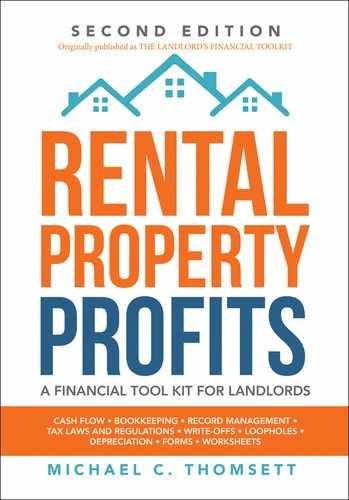

FIGURE 5-1. INVESTMENT RECEIPTS JOURNAL

Investment receipts journal

Month, year _____________________

GOOD BOOKKEEPING

This procedure—keeping track of rental income through (a) your checking account and (b) the receipts journal—allows you to fully document all of your investment income throughout the year. The secret to effective bookkeeping is uniformity. If you have income from a number of different investments, you need to consolidate it in some manner. When it comes time to prepare your tax return, you do not want to have to scramble to figure out rental income for each property—and interest, dividends, and capital gains—while also trying to ensure that you don’t count a transfer as income by mistake. The simplified receipts journal ties your deposits to specific sources and makes the record uniform. A double-check is also available from your monthly bank statement, whether received in paper form on paperless and online. Make sure that the total reported by your bank agrees with the “total” column on your receipts journal. Any differences should be corrected. So, if you forget to write down a deposit halfway through the month, you’ll be able to find the error and fix it.

BREAKING DOWN MORTGAGE PAYMENTS

Keeping track of income is not a complicated matter. You need to put a little more effort into tracking payments, however. The largest payment you make each month is going to be the mortgage payment. Your monthly payment may consist of up to four different elements: mortgage principal (which reduces your debt balance), interest, and—if impounds are included—additional amounts for property taxes and insurance. It is important to be able to break out these various segments of the mortgage payment in order to track both cash flow and profit and loss. Some lenders provide breakdowns of these payments each month; others do not.

If your lenders do not provide you with a breakdown of each month’s payment, use a worksheet such as the one shown in Figure 5-2. This worksheet allows room for not only interest and principal but also for the impounds you may need to pay each month. As you write each month’s check for your mortgage payment, break it down so that your payments record can be kept up-to-date with accurate information.

![]()

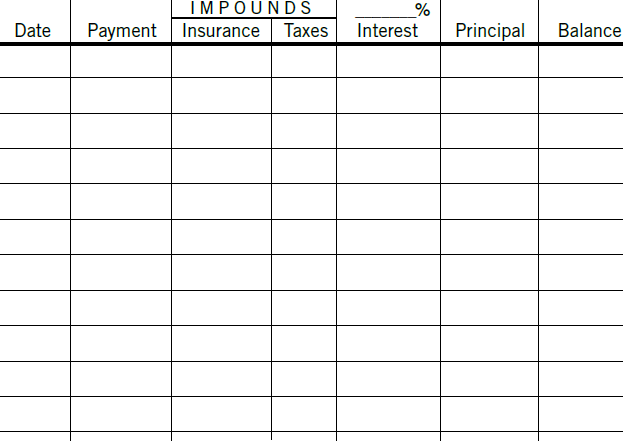

EXAMPLE: Your loan balance is $96,000 at the beginning of the year, and your monthly payment consists of $458.32 (for principal and interest) plus $135.00 for insurance and taxes, for a total of $593.32. The breakdown during the first year is summarized in Table 5-1.

![]()

TABLE 5-1. MORTGAGE AMORTIZATION TABLE ($)

BALANCING OUT IMPOUNDS

Each month’s loan payment has to be broken down in your books according to the type of transaction involved. Impounds are collected by the lender and paid according to the due dates. For example, you may be required to make two payments a year on your property taxes and quarterly payments on your insurance policy. So the lender collects impounds and then makes timely payments for you. Using the previous example, the collection of impounds and payments may resemble the breakdown in Table 5-2.

As long as your impound balances zero out during a single year, the easiest treatment is to simply assign them directly to the appropriate expense category—in this example, insurance and taxes. Two important notes concerning year-end adjustments: First, the impounds are approximations, so you probably need to adjust your year-end expense to reflect the actual total.

TABLE 5-2. IMPOUNDS ACCUMULATED AND PAID ($)

Second, if impounds include balances collected but not yet paid out, you need to defer the amounts collected to be applied to the following year.

![]()

EXAMPLE: As of December 31, your lender collected $72.00 in insurance impound and another $297.00 for taxes. However, the actual payments for those expenses were not made and are not due until the following year. You should consult with your lender to reduce your insurance and property tax impounds throughout the coming year by those amounts, since the actual amount being claimed includes impounds not yet due.

![]()

BREAKING DOWN EACH MONTH’S PAYMENTS

Adjustments to impounds should be made at the end of the year to keep monthly entries as simple as possible. As you make each mortgage payment, break it down and classify each portion of the expense based on either the summary your lender provides or your own worksheet. For example, the first month’s mortgage payment of $593.32 would be broken down among the various accounts for the specific property as shown on Table 5-3.

TABLE 5-3. MONTHLY BREAKDOWN OF PAYMENT ($)

Category |

Amount |

Insurance |

36.00 |

Taxes |

99.00 |

Principal |

320.00 |

Interest |

138.32 |

Total |

593.32 |

IMPORTANT The record of mortgage payments has to be further distinguished by property. If you own more than one rental property, you need to break down each expense by property because you are required to summarize it in that manner on your income tax return. It is also important to track cash flow for each property because you may have some positive and some negative cash flow properties.

RECORDING EXPENSES FOR RENTAL PROPERTIES

The complication for rental properties is not only separating payments by type of expense but the additional requirement that you track expenses for each property. As long as expenses can be identified by the property itself (e.g., interest, taxes, utilities), this is easy to do. However, some expenses (such as office supplies, legal and accounting fees, auto and truck expenses, and telephone) cannot be as easily broken down by property. You need to use a formula that makes sense on some basis. Allocating nonspecific expenses among two or more properties is explained later in this chapter.

The process of recording expenses can become complex for multiple properties. A set of records can be maintained by hand in a series of journals and ledgers. These include books of original entry, known as journals, with summaries posted into a book of final entry, known as a general ledger. For multiple properties, the journals have to be maintained with separation between properties.

To simplify this process, check one of the several bookkeeping systems you can find online.

VALUABLE RESOURCE Online bookkeeping and accounting systems include:

Quickbooks |

|

Sage |

|

Xero |

|

Freshbooks |

SIMPLIFIED RECORD KEEPING

For those expenses easily identified for each property, the record-keeping rules can be simplified. Remember, you need two forms of distinction: (1) by type of expense and (2) by specific property. It makes sense to set up your records by type of expense and post payments to those expense accounts as they are made. Such a system can be set up within an automated accounting system or on a simple Excel worksheet. You need to also track expenses by property, so each expense account has to be subdivided by property address.

Figure 5-3 shows a simplified bookkeeping format that allows you to segregate each expense and break it down by rental property.

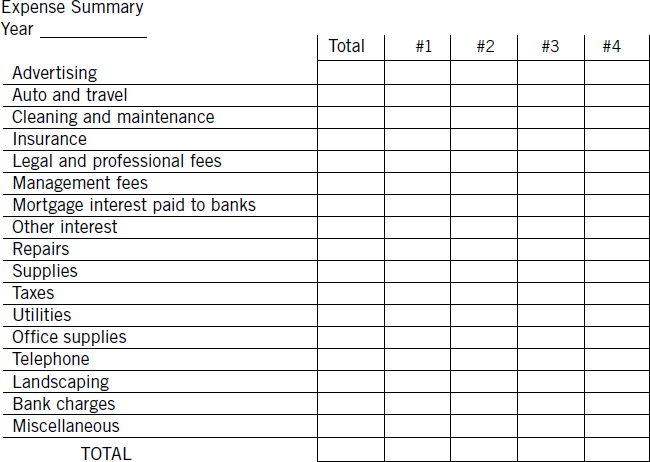

YEAR-END SUMMARY

The year-end summary is completed for each month. On an automated spreadsheet program, you could set up one “sheet” for each month, with one worksheet for each account, and track entries in that way. The year-end totals could then be transferred into a worksheet such as the one shown in Figure 5-4. This worksheet provides a summary that you can use to complete the expense portion of your federal tax return, Schedule E. (See Chapter 10 for more details.)

SIMPLE METHODS FOR TRACKING CASH PAYMENTS

A chronic problem for those operating their own businesses is the handling of cash transactions. Real estate investors are no exception. A potentially significant dollar amount of deductible expenses may be forgotten each year because the transaction takes place in cash. For example, when doing small repairs on a rental property, you make several trips to the hardware store to buy small tools, hardware, or parts. Each purchase runs $5 or less, and so you pay in cash, losing the receipt along the way. By the end of the job, you may have spent $50, collectively. If you do a repair job like that once a month, you lose track of $600 per year. This example may be only part of a larger problem. If you have several rental properties, it is all too easy to lose track of small expenses, so you need to devise a consistent but simple procedure.

SAVING RECEIPTS

In more formalized settings, like a business office, you would set up a petty cash fund, placing a set sum of money in a cash box and reimbursing cash expenses for receipts. Considering that the goal is to keep things simple, it should not be necessary to set up a petty cash fund. Instead, you can use a less formal procedure. Since you will normally use your car, van, or truck while out on real estate business, your cash transaction system can be operated out of your vehicle. The following four-point checklist is a suggestion for how the simplified cash system can work:

1. Place a large mailing envelope (e.g., 9 ×12-inch in size) in your vehicle.

2. Whenever you buy something related to your real estate investments, place the receipt in the envelope. Write on the receipt the type of expense and the property name.

3. Once a month (or more frequently, if the volume is high), gather together the receipts, subtotal each expense classification, and reimburse yourself from your business checking account. In this way, the cash expenses go through your checking account and into your books.

4. Document expenses immediately as they occur. Otherwise, you risk forgetting the specifics.

This simplified system gets you into the habit of filing receipts in the same place each time you spend money. Remembering to properly label each receipt also helps you assign each expense to the correct expense category and for the right property.

SETTING UP A CASH FUND

If you spend a large amount of cash, you could also place a small cash fund in the envelope. While this increases the chances for petty theft, it also makes it convenient to manage cash transactions. Most people find it easier to simply keep more cash in their pocket for such expenses. In general, though, you should work to minimize cash transactions because, even with a simple system like the one proposed, it is cleaner and easier to run as much as possible through your checking account.

OPENING AN ACCOUNT

To help improve the situation, you can charge your purchases rather than pay cash. In this way, you pay for your purchases with one monthly check (when you pay your credit card bill) instead of making a higher volume of small purchases throughout the month. As you sign for each purchase, be sure to write down the property address on the voucher so that you will be able to break down your monthly bill by rental property.

Use one credit card exclusively for your rental business expenses. Do not mix this with personal charges. Just as you need to set up a separate checking account, you also need to keep credit cards separate. Using the business credit card for small purchases solves the problem of cash transactions—as long as you keep daily records of what the expense is for and which property or properties to apply it to. To summarize the guidelines for the use of a credit card:

![]() Use one card exclusively for investment expenses. If you have two or more credit cards, use only one for your investment-related expenses. When you put gas in your car, purchase landscaping supplies, or shop at the hardware store, use the same card. Don’t use this card for any other purposes, except in emergencies. In this way, your monthly payment on the credit card is consistent, and you can easily keep track of business expenses as they occur.

Use one card exclusively for investment expenses. If you have two or more credit cards, use only one for your investment-related expenses. When you put gas in your car, purchase landscaping supplies, or shop at the hardware store, use the same card. Don’t use this card for any other purposes, except in emergencies. In this way, your monthly payment on the credit card is consistent, and you can easily keep track of business expenses as they occur.

![]() Keep receipts even when using your card, and match all purchases to your monthly statements. Just because you are charging your purchases does not mean you should throw away your receipt, for several reasons. First, you should always check your receipts against what gets charged to your account in order to make sure all of those charges are legitimate. Second, the receipt documents what you purchased and is necessary to complete your record keeping. Third, the receipt may be necessary to allocate expenses among properties. For example, you may make a purchase at one store, but the items are allocated to two different properties.

Keep receipts even when using your card, and match all purchases to your monthly statements. Just because you are charging your purchases does not mean you should throw away your receipt, for several reasons. First, you should always check your receipts against what gets charged to your account in order to make sure all of those charges are legitimate. Second, the receipt documents what you purchased and is necessary to complete your record keeping. Third, the receipt may be necessary to allocate expenses among properties. For example, you may make a purchase at one store, but the items are allocated to two different properties.

![]() As an alternative, use a debit card on your business account. Some people don’t want to use their credit cards. Perhaps they don’t have an adequate line of credit, or they find it too much trouble to remember which credit card to use. In this case, you can use a debit card associated with your investment expense. The debit card is as convenient as writing a check, and the cash comes out immediately. Remember, though, you still need to keep the receipt to make the record of your transaction complete.

As an alternative, use a debit card on your business account. Some people don’t want to use their credit cards. Perhaps they don’t have an adequate line of credit, or they find it too much trouble to remember which credit card to use. In this case, you can use a debit card associated with your investment expense. The debit card is as convenient as writing a check, and the cash comes out immediately. Remember, though, you still need to keep the receipt to make the record of your transaction complete.

![]() Pay off the balance each month. Don’t let your investment credit card debt get out of control. Pay off the entire balance each month unless an exceptional situation arises (such as an unexpected, expensive repair). Having credit available is one way to manage cash flow, but you can use your card in that way only if you keep the balance under control. Paying off the entire balance is the same as if you were writing checks for each and every transaction. Don’t allow your balance to inch upward so that you end up with no credit available when you need it.

Pay off the balance each month. Don’t let your investment credit card debt get out of control. Pay off the entire balance each month unless an exceptional situation arises (such as an unexpected, expensive repair). Having credit available is one way to manage cash flow, but you can use your card in that way only if you keep the balance under control. Paying off the entire balance is the same as if you were writing checks for each and every transaction. Don’t allow your balance to inch upward so that you end up with no credit available when you need it.

ALLOCATING EXPENSES AMONG PROPERTIES

Certain expenses cannot be identified by property. The larger expenses—interest, property taxes, utilities, and insurance—are easily and specifically tied to the property itself. However, legal and professional fees, office supplies, auto and truck expenses, and telephone charges are far more difficult to deal with.

YEAR-END ALLOCATION

You are required to break down your rental expense by property, so you need to devise a method that makes sense and is also consistent for allocating nonspecific expenses. The most reliable method is to make allocations at the end of the year based on the level of rents collected. Performing allocations during the year is not advised; this makes more work and confuses the bookkeeping process. Keep it simple and straightforward month to month, and prepare a worksheet at the end of the year, such as the one in Figure 5-5, as part of your tax return, to allocate expenses.

Note that insurance is included on this form. The insurance expense that belongs to each property can be easily allocated, of course. The purpose for including insurance on the allocation worksheet is for forms of insurance that cannot be broken down by property, such as insurance on a vehicle that you use only for managing your rentals.

The distinction between “supplies” and “office supplies” can be confusing as well. The type of items you would list under supplies includes hardware, drywall compound, paintbrushes, and small tools. The office supplies category includes the usual paper and pens, as well as letterhead, envelopes, stamps, printed checks and deposit slips, and other paper goods.

COMPUTING THE ALLOCATION

The allocation is not difficult to compute. You just break down each year’s total in each expense classification using the same percentages as rents.

![]()

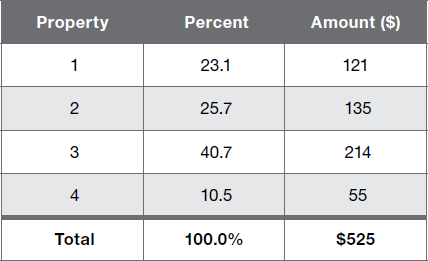

EXAMPLE: You owned four properties during the most recent year. Rental income was $3,400, $3,785, $6,010, and $1,554. To arrive at a percentage breakdown, divide each rental total by the overall total ($14,749):

$3,400 ÷ $14,749 = 23.1%

$3,785 ÷ $14,749 = 25.7%

$6,010 ÷ $14,749 = 40.7%

$1,554 ÷ $14,749 = 10.5%

APPLYING THE ALLOCATION

To apply these breakdowns for each expense, multiply the total by the applicable percentage. For example, if your legal and professional fees totaled $525 for the year, using the breakdown, you would assign the expense to each property as shown on Table 5-4.

TABLE 5-4. ANNUAL EXPENSE ALLOCATION

What if you own a property for only part of the year? The allocation method is still reasonable because it shows a smaller rental total for the property and, as a result, a smaller dollar value as well. However, if you had an unusually large expense in the early part of the year and did not purchase an additional property until later, you could calculate two separate allocations: one for the period you owned three properties and another for the period of time you owned all four. Because the difference is probably going to be insignificant in most cases, it is a lot of extra work to calculate separate allocations, and it may even confuse rather than clarify the issue. The most reasonable approach is to apply an allocation for the entire year, consistently. The overall result will not change, so your tax liability is going to be the same no matter how you break down the allocation.

USING THE NONALLOCATION METHOD

An alternative is not to allocate these expenses at all but rather to show them in a separate column. On the Schedule E used to report rental income, you are asked to show each property’s results in its own column. You could include a column for nonallocated expenses. Using this method, you would report rental income, expenses, and profit or loss for each property, and then a last column, “unallocated expenses,” would have a total for each expense and a net loss. The columns are added together to summarize the net profit or loss.

![]()

KEY POINT The unallocated expense method keeps the books simple because no expenses are divided or assigned to specific properties. However, the process of evaluating cash flow for each property is more difficult. You need to perform your cash flow on all properties, but that is the method you probably use each month anyway.

A suggestion: Evaluate cash flow each month based on a worksheet allocation of expenses, which allows you to look at each property objectively. But don’t make allocations in your books. Then at the end of the year when you prepare your taxes, you can consult with your tax adviser as to whether or not to allocate expenses. That allocation can be done on a worksheet, without complicating your bookkeeping.

Nonallocation is easier than breaking down expenses. You should continue to assign expenses to specific properties as long as you can break them down easily. Therefore, utilities, interest, and property taxes should be assigned to their respective properties as payments are being made.

SIMPLIFYING DEPRECIATION WITH NONALLOCATION

The nonallocation method also clarifies the treatment of depreciation for assets that are not unique to a particular property. Under the allocation method, you need to break out a portion of depreciation for each property. Expenses that may be nonspecific to property (for your auto or truck expenses, the costs of landscaping equipment and tools, for example) have to be allocated to each property individually. This complicates the question of depreciation significantly. When you sell a rental property, you are supposed to “recapture” the depreciation expenses you have claimed while you owned it. (This means the amount of depreciation claimed over the time you owned property is taxed upon sale of the property.) If you have claimed a portion of depreciation for nonspecific items, it confuses the calculation of recaptured depreciation expense.

If you have a number of assets that cannot be assigned to each property, using the nonallocation method makes the most sense. Even if this is not a problem today, if you expect to own several properties in the future, you may want to establish a policy now that you will not allocate expenses to each property. This keeps everything much easier to track.

YEAR-END TAX REPORTING

One problem with nonallocation is that it does not allow you to show a net profit or loss on your tax return for each property. This does not affect your overall outcome because the net total of all properties is the profit or loss number that gets transferred to Form 1040 and on which tax is computed. Whether or not you allocate expenses, it is not wise to try to perform the allocation every month. The means for determining the breakdown—usually rental receipts—is likely to change throughout the year, so you would have to continually adjust the breakdown. Allocation should be a year-end calculation, done only once. This also keeps your books simple.

![]()

EXAMPLE: You have three rental properties, and you are summarizing transactions as part of your year-end tax reporting. You do not want to allocate certain expenses. A summary of your annual rental income and expenses would look like the summary in Table 5-5.

![]()

TABLE 5-5. SUMMARY, ANNUAL INCOME AND EXPENSE ($)

In this example, nonallocated expenses were kept separate. While it would be a fairly simple matter to allocate these expenses, this method is clearer and cleaner. Because the net profit or loss on a capital gain is going to be based on the depreciated value of the property, depreciation expenses have to be divided among properties. However, any nonspecific depreciation can be kept in the nonallocated category and treated the same as other nonallocated expenses.

SHOWING NONALLOCATED EXPENSES ON YOUR TAX FORM

Nonallocation is not a preferred method for reporting taxes because it does not comply with the columns and format of the tax form. Even so, the net profit or loss continues to be reported, so there is no harm done by the nonallocation of certain expenses. And, even though the method does not exactly match the requirements of the tax form, it does comply with the provisions of the tax laws. You are required to report the net profit or loss from the activity and to show a breakdown by property of all revenue and expenses. Because nonallocated expenses cannot be directly assigned, they are treated as though they represent a separate property but only in the sense that they are given their own special column for reporting purposes.

In the previous example, four columns are shown, plus a total column. The tax form where this information is reported (Schedule E of Form 1040) has only three columns. That doesn’t mean that all of the information has to be forced into three columns. When the information exceeds the capacity of the form, it is summarized on a supplementary schedule, and the totals are reported in the far-right column of the form.

GETTING HELP—FINDING A QUALIFIED BOOKKEEPER

Even if you are comfortable doing most of your own record-keeping chores, you may find it necessary to hire someone to formalize your books. You may already know how to record transactions and balance the books, but you may be one of the thousands of people who simply don’t enjoy bookkeeping, so it’s a bargain to pay someone else to do it for you.

What guidelines should you follow in finding the right bookkeeper? Here are a few ideas:

![]() Check references. Any time you hire someone to work for you, it is essential to check references. Some people are not trustworthy, qualified, or competent, and it is expensive to discover that for yourself, after you have hired them. Ask for professional references, including the two latest jobs, and check them thoroughly. If an applicant is not willing or able to provide references, don’t hire them. People are not always completely honest in what they tell you when applying for a job, so you must ensure that the person you are interviewing has experience. Ask them questions about bookkeeping: What have they done in the past? Have they worked with accountants in the area? (If so, that gives you more references to check.) Are they full-charge bookkeepers? (A full-charge bookkeeper is supposed to be qualified to do all the bookkeeping entries, including the final entries at the end of each month.)

Check references. Any time you hire someone to work for you, it is essential to check references. Some people are not trustworthy, qualified, or competent, and it is expensive to discover that for yourself, after you have hired them. Ask for professional references, including the two latest jobs, and check them thoroughly. If an applicant is not willing or able to provide references, don’t hire them. People are not always completely honest in what they tell you when applying for a job, so you must ensure that the person you are interviewing has experience. Ask them questions about bookkeeping: What have they done in the past? Have they worked with accountants in the area? (If so, that gives you more references to check.) Are they full-charge bookkeepers? (A full-charge bookkeeper is supposed to be qualified to do all the bookkeeping entries, including the final entries at the end of each month.)

![]() Find someone with experience in real estate. When it comes to recording transactions, keeping records, and breaking down expenses, the rules for real estate are different from most other types of businesses. You need someone with experience in rental bookkeeping. While this is not absolutely essential, it is an advantage. A person who understands how to allocate real estate expenses and why it is so important will have an advantage over someone you will have to train.

Find someone with experience in real estate. When it comes to recording transactions, keeping records, and breaking down expenses, the rules for real estate are different from most other types of businesses. You need someone with experience in rental bookkeeping. While this is not absolutely essential, it is an advantage. A person who understands how to allocate real estate expenses and why it is so important will have an advantage over someone you will have to train.

![]() Consider using a management company’s services. If you cannot find a qualified bookkeeper in your area, you may want to check with a local real estate management company. These companies handle all of the details of rentals—from bookkeeping to filling vacancies and fielding tenant problems—for landlords who don’t want to deal with these matters themselves or who live far away and cannot. Some of these companies may be willing to quote you a price for keeping your books. They usually charge between 8 percent and 12 percent of rents collected for complete services, including finding tenants, collecting rents, and keeping the books.

Consider using a management company’s services. If you cannot find a qualified bookkeeper in your area, you may want to check with a local real estate management company. These companies handle all of the details of rentals—from bookkeeping to filling vacancies and fielding tenant problems—for landlords who don’t want to deal with these matters themselves or who live far away and cannot. Some of these companies may be willing to quote you a price for keeping your books. They usually charge between 8 percent and 12 percent of rents collected for complete services, including finding tenants, collecting rents, and keeping the books.

![]() Coordinate the bookkeeping routines with your tax adviser. Your tax adviser should not be someone whom you see only once a year. You may also need midyear tax-planning advice, so make an appointment to plan ahead. In the course of managing your taxes, you can also ask your tax professional where you can find a qualified bookkeeper. The tax adviser may know someone or, if a member of a large firm, may have an in-house bookkeeping service. This can save you a lot of time and trouble. Your tax adviser won’t have to depend on an outsider’s bookkeeping to determine what is going on; the same adviser can supervise how the books are set up and how month-end and year-end summaries are recorded.

Coordinate the bookkeeping routines with your tax adviser. Your tax adviser should not be someone whom you see only once a year. You may also need midyear tax-planning advice, so make an appointment to plan ahead. In the course of managing your taxes, you can also ask your tax professional where you can find a qualified bookkeeper. The tax adviser may know someone or, if a member of a large firm, may have an in-house bookkeeping service. This can save you a lot of time and trouble. Your tax adviser won’t have to depend on an outsider’s bookkeeping to determine what is going on; the same adviser can supervise how the books are set up and how month-end and year-end summaries are recorded.

![]() Be aware of employment rules. Make sure the individual you hire understands that the arrangement is not an employment agreement. That means they are responsible for their own insurance and taxes. In some situations, you could get into a lot of trouble if you don’t have a specific agreement and the person complains to the tax authorities that you did not withhold taxes, worker’s compensation, or unemployment insurance. Therefore, get your agreement in writing, specifying that the individual’s status is as an independent contractor and that the agreement is not an employment contract.

Be aware of employment rules. Make sure the individual you hire understands that the arrangement is not an employment agreement. That means they are responsible for their own insurance and taxes. In some situations, you could get into a lot of trouble if you don’t have a specific agreement and the person complains to the tax authorities that you did not withhold taxes, worker’s compensation, or unemployment insurance. Therefore, get your agreement in writing, specifying that the individual’s status is as an independent contractor and that the agreement is not an employment contract.

If you decide to hire someone as an employee, you should first check into record-keeping and reporting requirements. Having an employee is a complex administrative and bookkeeping challenge. You must make periodic deposits for payroll taxes and pay approximately 12 percent of payroll for federal and state insurance and Social Security. You must also pay workers’ compensation insurance. For all of these reasons, it is far more efficient and cheaper to hire a bookkeeping service and not an employee.

![]() Hire someone you are comfortable with. No matter how qualified a bookkeeper might be, you should be comfortable with the person. You want to be able to talk about your books and ask questions. The bookkeeper, too, must be comfortable working with you. If there is tension in the relationship, you will not enjoy meeting with your bookkeeper. You also will not be able to get the information you need and deserve.

Hire someone you are comfortable with. No matter how qualified a bookkeeper might be, you should be comfortable with the person. You want to be able to talk about your books and ask questions. The bookkeeper, too, must be comfortable working with you. If there is tension in the relationship, you will not enjoy meeting with your bookkeeper. You also will not be able to get the information you need and deserve.

![]() Pay attention to what is being done. One of the greatest mistakes any investor or small business owner can make is letting someone else do the books without paying attention. You should ask questions, review work, and make sure you understand exactly what is going on with your books. You are responsible for keeping records even if you hire someone else, so you need to ensure that the information is being recorded accurately and properly.

Pay attention to what is being done. One of the greatest mistakes any investor or small business owner can make is letting someone else do the books without paying attention. You should ask questions, review work, and make sure you understand exactly what is going on with your books. You are responsible for keeping records even if you hire someone else, so you need to ensure that the information is being recorded accurately and properly.

WATCH THIS Some investors think it is efficient to let their bookkeeper sign checks. This is not a smart idea. You invite trouble when you give someone else unlimited access to your funds. Signing the checks is a good control point, where you can ask questions if you’re unsure about anything—or want to know what is being paid, for example. Not everyone will embezzle just because they have the opportunity, but why invite trouble? Sign your own checks, and supervise the entire bookkeeping operation regularly.

THE RENTAL AGREEMENT

In thinking about various types of documentation (receipts, invoices, statements), it is common to view investment activities in terms of the usual tax rules. You need a document to verify the expense. For rental activity, you also need to document the fact that an agreement existed for the period you claim deductions.

You can verify expenses to a degree with utility records that show where you and your tenants receive mail. Going beyond this, though, you also need to enter a written agreement with your tenant that defines what you have agreed upon. Your rental contract defines the beginning date of your rental, the amount of rent the tenant is supposed to pay, any deposits given to you and what they are for, which utilities the tenant pays, and other important terms. In addition to being an important legal document, the rental contract is also a form of documentation for tax purposes. It establishes that a contract existed between landlord and tenant.

CONFORMING TO THE LAW

Laws vary from one state to another. The specific terms you put in your rental agreement should be reviewed by a real estate attorney to ensure that your requirements conform with local laws. For example, some states require twenty days’ notice if you or your tenant want to terminate the agreement; other states require thirty days. You cannot waive the legal requirement. Even if you and your tenant agree to twenty days’ notice, but your state requires thirty days, that is the rule. If one side or the other makes a thirty-day notice, that conforms with the law.

A typical rental agreement for a month-to-month rental is shown in Figure 5-6. Remember, though, that the specific rules in your state may require modification to some of the terms listed.

SOME PROBLEMS TO WATCH FOR

The rental agreement is a contract. Of course, it is designed to cover most of the common problems that can arise between landlord and tenant, but it cannot possibly cover everything. Disagreements can and do arise, and some areas of conflict seem to be more common than others—no matter how carefully the rental agreement is worded. These common problem areas include:

This is a rental agreement for a month-to-month rental between _____________________________ _________________________________ (tenant) and _______________________________ (landlord), for property located at ________________________________ in the city of _____________________________ _____________________________. The rental terms begin on ____________________ and will continue until one side provides written notice to terminate the agreement. Such notice will be provided no less than __________ days before the intended date of moving. The landlord agrees to refund all deposits due to the tenant as specified below within __________ days after the property has been vacated.

The monthly rent is payable on the __________ day of each month in the amount of $__________ per month. The security and cleaning deposit is payable on the date this agreement is signed in the amount of $__________. This deposit will be returned upon completion of this agreement and subject to the tenant’s returning of keys and completion of a walk-through inspection by the landlord and a return of property condition to its original condition. Any cost of cleaning or repair will be deducted from this deposit, explained, and the remaining balance refunded. No portion of this deposit may be applied to rents remaining due upon termination of this agreement.

Residents of the property are limited to the following persons:

No additional persons may reside at this address under the terms of this agreement, without written permission from the landlord and renegotiation of a new rental agreement. No pets are allowed at this address unless preapproved by the landlord and subject to an additional pet deposit.

The tenant also agrees to the following rules:

a. The outside areas will be maintained in current condition, including lawn and yard maintenance. No personal property will be left in the yard or on the porch area.

b. The tenant will not paint or perform other repairs or modifications to the property without prior written consent from the landlord.

c. The landlord has the right to inspect the property, make repairs, or show the property to prospective buyers in the event a sale is pending, or to new prospective tenants if this agreement is in the process of ending, provided that the landlord will provide _______ days’ notice in advance and make an appointment to have access to the property.

d. Rents will be submitted by mail or in person on the due date and at the owner’s address.

e. No motor vehicles in excess of _______ vehicles will be kept at the property. All vehicles kept at the property will be currently licensed and registered. No repairs of motor vehicles are allowed at the property.

f. The tenant will pay for all repairs for damages caused by the tenants, their children, or guests. If the landlord pays for such repairs, the tenant agrees to reimburse the landlord by payments on a schedule agreed upon by the landlord and tenant.

g. The tenant will not change locks without prior written permission from the landlord. Upon termination of this agreement, the tenant agrees to provide the landlord with two key sets for the changed locks.

h. Other: Violation of any of the terms of this contract may result in the landlord beginning eviction proceedings. The tenant has read this agreement, understands its terms, and has been given a copy of the agreement. This agreement also represents a deposit receipt according to the terms above. Other agreements that are part of this contract include a Statement of Condition and ______________________________________________________________________.

![]() Due Date of Rent. Tenants may have a relaxed attitude about the date the rent is actually due. From your point of view, the mortgage payment is usually due on the first, so it would be nice to collect rents on the same day. If you do not specify the due date with the tenant, the payment may slip. If you do not enforce the agreed-upon due date each month, the tenant may fall so far behind that it will be impossible to catch up.

Due Date of Rent. Tenants may have a relaxed attitude about the date the rent is actually due. From your point of view, the mortgage payment is usually due on the first, so it would be nice to collect rents on the same day. If you do not specify the due date with the tenant, the payment may slip. If you do not enforce the agreed-upon due date each month, the tenant may fall so far behind that it will be impossible to catch up.

![]() Residents Allowed in the Property. Every house has a limited amount of space. A very small property will be appropriate for a limited number of people, so the rental agreement is designed specifically to limit the number of people who are allowed to live on the premises. Some tenants with large families will initially represent that there are only two people, only to move three or four more people in later. The problem with this is that there will be more wear and tear on the property; in addition, it is not fair to you when tenants deceive you about the number of people living in your property. This is why the contract includes space to list everyone. It allows you to enforce the terms later if more people move into the property. You need to be sure that you don’t violate local laws when limiting the number of people who can live in your property. Some states’ rules forbid discriminating against families with children, for example, so you cannot reject an application solely because your tenant has children. The criteria must include a reasonable argument about the size of the property and the number of people who can live within that space with that many bedrooms and baths.

Residents Allowed in the Property. Every house has a limited amount of space. A very small property will be appropriate for a limited number of people, so the rental agreement is designed specifically to limit the number of people who are allowed to live on the premises. Some tenants with large families will initially represent that there are only two people, only to move three or four more people in later. The problem with this is that there will be more wear and tear on the property; in addition, it is not fair to you when tenants deceive you about the number of people living in your property. This is why the contract includes space to list everyone. It allows you to enforce the terms later if more people move into the property. You need to be sure that you don’t violate local laws when limiting the number of people who can live in your property. Some states’ rules forbid discriminating against families with children, for example, so you cannot reject an application solely because your tenant has children. The criteria must include a reasonable argument about the size of the property and the number of people who can live within that space with that many bedrooms and baths.

![]() Responsibility for Yard Maintenance and Provision of Tools. Tenants often want to occupy a house but do not own a lawn mower and other yard tools. As landlord, you probably don’t expect to provide these tools for your tenants, so this is one possible area of conflict. Some tenants might expect the landlord to buy a lawn mower for them. You need to clarify the fact that the tenant is responsible for yard maintenance, and this invariably includes mowing a lawn, weeding, trimming, and performing other yard routines. Logically, this also means having to buy the needed tools, renting them, or asking a friend for help. Some landlords gladly lend their mower to the tenant or leave a spare mower on the premises. But lacking these, the tenant has to assume responsibility for making arrangements necessary to maintain the yard areas.

Responsibility for Yard Maintenance and Provision of Tools. Tenants often want to occupy a house but do not own a lawn mower and other yard tools. As landlord, you probably don’t expect to provide these tools for your tenants, so this is one possible area of conflict. Some tenants might expect the landlord to buy a lawn mower for them. You need to clarify the fact that the tenant is responsible for yard maintenance, and this invariably includes mowing a lawn, weeding, trimming, and performing other yard routines. Logically, this also means having to buy the needed tools, renting them, or asking a friend for help. Some landlords gladly lend their mower to the tenant or leave a spare mower on the premises. But lacking these, the tenant has to assume responsibility for making arrangements necessary to maintain the yard areas.

![]() Rent Offsets. Some tenants think it is reasonable to barter for some of the rental obligation. This usually means they cannot afford the rent you are asking. If this comes up in the application phase, it is a warning sign. If it comes up later, it may be troubling, but you have to remain firm. The full amount of rent is due. None of that rent can be exchanged for performing work around the property or otherwise working for you. Chances are, you will never have enough work to keep the tenant busy, even if you wanted to. In addition, you already have a specific contract with your tenants; complicating that agreement with a working relationship raises all sorts of potential trouble. What if they injure themselves? Are you liable for providing insurance or withholding taxes? What if you’re unhappy with their work and want to fire them? Any number of conflicts can come up, so you are better off keeping the landlord–tenant relationship as simple as possible. The two most common areas that come up in the bartering offer are landscaping and painting. Since the tenant is already responsible for landscaping, there is no room for negotiation on that count. Most people who have never painted a house think it is an easy job, but they soon find out it is far more work than they think. Landlords should never give permission for tenants to paint inside or out, even if they want to perform the work for free. You need to maintain control over color choices, quality of work, and timing. Tenants may start out working for free, only to later decide they should be paid for their efforts—another potential conflict area worth avoiding.

Rent Offsets. Some tenants think it is reasonable to barter for some of the rental obligation. This usually means they cannot afford the rent you are asking. If this comes up in the application phase, it is a warning sign. If it comes up later, it may be troubling, but you have to remain firm. The full amount of rent is due. None of that rent can be exchanged for performing work around the property or otherwise working for you. Chances are, you will never have enough work to keep the tenant busy, even if you wanted to. In addition, you already have a specific contract with your tenants; complicating that agreement with a working relationship raises all sorts of potential trouble. What if they injure themselves? Are you liable for providing insurance or withholding taxes? What if you’re unhappy with their work and want to fire them? Any number of conflicts can come up, so you are better off keeping the landlord–tenant relationship as simple as possible. The two most common areas that come up in the bartering offer are landscaping and painting. Since the tenant is already responsible for landscaping, there is no room for negotiation on that count. Most people who have never painted a house think it is an easy job, but they soon find out it is far more work than they think. Landlords should never give permission for tenants to paint inside or out, even if they want to perform the work for free. You need to maintain control over color choices, quality of work, and timing. Tenants may start out working for free, only to later decide they should be paid for their efforts—another potential conflict area worth avoiding.

![]() Automobiles on the Premises. You want to restrict the number of cars that tenants are allowed to have parked on or near your property. This restriction should include a limitation on the number of vehicles, a rule that the vehicles have to be registered, and a ban on working on vehicles on the premises. Without these rules, it is too easy for tenants to make a mess of your property, not only visually but environmentally as well. Your neighbors will not appreciate the problems, and the conditions may also violate local zoning rules. Including vehicle restrictions in your rental contract is important, if only because the problem does arise from time to time.

Automobiles on the Premises. You want to restrict the number of cars that tenants are allowed to have parked on or near your property. This restriction should include a limitation on the number of vehicles, a rule that the vehicles have to be registered, and a ban on working on vehicles on the premises. Without these rules, it is too easy for tenants to make a mess of your property, not only visually but environmentally as well. Your neighbors will not appreciate the problems, and the conditions may also violate local zoning rules. Including vehicle restrictions in your rental contract is important, if only because the problem does arise from time to time.

![]() Application of Security Deposit to Rents. When they want to end their relationship with you, tenants may decide to apply their security deposit to the last month’s rent. This means that if they do not clean the property or if damage has been done, you have no recourse in collecting the costs from the security deposit. However, by the time the tenant has decided not to pay the last month’s rent, it is really too late to prevent this. By the time you would be able to take action to collect unpaid rent, the tenant will be gone and there would be no point in proceeding.

Application of Security Deposit to Rents. When they want to end their relationship with you, tenants may decide to apply their security deposit to the last month’s rent. This means that if they do not clean the property or if damage has been done, you have no recourse in collecting the costs from the security deposit. However, by the time the tenant has decided not to pay the last month’s rent, it is really too late to prevent this. By the time you would be able to take action to collect unpaid rent, the tenant will be gone and there would be no point in proceeding.

If the property is left damaged and no security deposit was collected, you can file a small claims action, but even with a judgment, collection will be a problem. Unless the damage is significant, the effort will not necessarily be justified by the dollar amount of damages. A far more sensible approach is to require tenants to prepay the last month’s rent as well as the security deposit, although this will create a hardship for many tenants. They will need to pay the first and last month’s rent plus a security deposit in order to move in. Depending on the condition and age of the property, the neighborhood, and the tenant’s references, you may be willing to forego the last month’s rent requirement. If this rule translates to having longer periods of vacancy (because fewer people can afford to put down that much money), it will not be worthwhile—especially if other landlords are not requiring the first and last months’ rent as part of their conditions for moving in.

![]() Conditions for Return of Security Deposit. The security deposit is intended as a fund to ensure that tenants do not damage your property, fail to return keys, or leave without cleaning. Even so, some tenants will cause considerable damage and fail to clean up and still expect to be given their security deposit. You may need to clarify the intent of the deposit. One solution to this potential problem is to advise tenants that when they are ready to vacate, you want to do a walk-through inspection with them. At this time, you can check conditions and let tenants know of any repairs or cleaning that still need to be done. You can also inform them that in order to get their security deposit back, those repairs and cleaning chores need to be completed. This step helps to improve communication and ensures that tenants know the terms of vacating the property.

Conditions for Return of Security Deposit. The security deposit is intended as a fund to ensure that tenants do not damage your property, fail to return keys, or leave without cleaning. Even so, some tenants will cause considerable damage and fail to clean up and still expect to be given their security deposit. You may need to clarify the intent of the deposit. One solution to this potential problem is to advise tenants that when they are ready to vacate, you want to do a walk-through inspection with them. At this time, you can check conditions and let tenants know of any repairs or cleaning that still need to be done. You can also inform them that in order to get their security deposit back, those repairs and cleaning chores need to be completed. This step helps to improve communication and ensures that tenants know the terms of vacating the property.

THE STATEMENT OF CONDITION

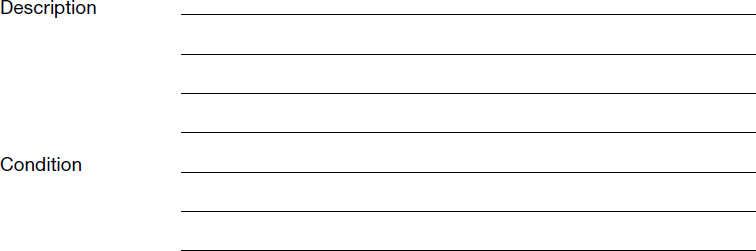

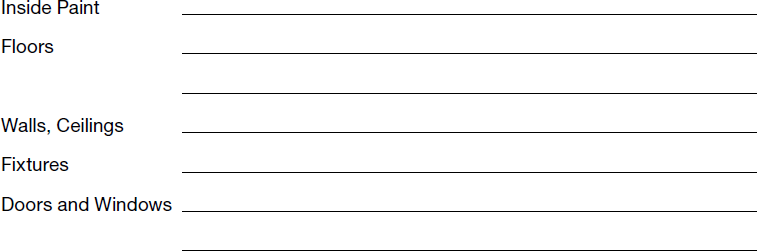

A second form, usually a part of the rental agreement, is the statement of condition. This is a listing of any and all defects and other conditions of the property, an inventory of any furniture or appliances included with the property, and other notes agreed to by both tenant and landlord. The form should be completed by the landlord as a walk-through of the property is performed with the tenant. This form could be multipage and list every possible condition, or it could be fairly simple, with only specific notations made. A sample of the simplified version of the Statement of Condition is shown in Figure 5-7.

PROTECTION FOR LANDLORD AND TENANT

The purpose of the Statement of Condition form is to document the exact condition of the property in order to protect both landlord and tenant. If there are any flaws in condition, these should be noted on the form. During the walk-through, the tenant has a chance to point out flaws that should be written down, such as chipped trim, holes in the walls, worn carpets, or missing and broken tiles. When the tenancy ends, the Statement of Condition can be referred to as the source of information about who is responsible for repairs. The same logic applies to appliances. If appliances are not clean when the tenant first sees them, this should be noted on the Statement of Condition. The landlord should deliver the property in clean condition. It would not be fair to turn over the property in less than clean condition and then expect the tenant to clean up upon vacancy.

Statement of Condition

Tenant and landlord have completed a walk-through of the property under the rental agreement signed on ___________ for the property located at _______________________

The following summary is agreed upon by both landlord and tenant.

The following furniture and appliances are located at the property:

Condition of the property is assumed to be without flaws, except as noted below:

The property and appliances are in acceptable working order and are clean, and tenant agrees that the property will be left in the same condition upon termination of the

The same protection works for the landlord. If the property is spotless and all fixtures are in clean and working order, this has to be noted on the Statement of Condition. If the tenant breaks anything or damages appliances or fixtures, you then have the right to deduct repairs and cleaning from the security deposit. There are some exceptions:

![]() Normal Wear and Tear. You expect carpets to wear out after a few years, and you also expect to need to repaint interior walls. These are examples of normal wear and tear. A tenant who has occupied the premises for many years should not be expected to pay for new carpeting that is several years old. You would expect a tenant to fill holes in the wall where they have hung paintings, but you would not expect them to pay for a new paint job in a room that hasn’t been painted for many years.

Normal Wear and Tear. You expect carpets to wear out after a few years, and you also expect to need to repaint interior walls. These are examples of normal wear and tear. A tenant who has occupied the premises for many years should not be expected to pay for new carpeting that is several years old. You would expect a tenant to fill holes in the wall where they have hung paintings, but you would not expect them to pay for a new paint job in a room that hasn’t been painted for many years.

![]() Appliance Breakdown. Landlords often put used appliances in their rentals. The cost of new appliances is prohibitive, and the number of appliances can be staggering. For example, if the typical house includes a refrigerator, dishwasher, washer, dryer, and range—a total of five appliances—that is a considerable investment. If you own four rental properties, that adds up to twenty appliances. Rather than paying for brand-new units, you will probably purchase used appliances, in which case you have to expect them to break down at some point.

Appliance Breakdown. Landlords often put used appliances in their rentals. The cost of new appliances is prohibitive, and the number of appliances can be staggering. For example, if the typical house includes a refrigerator, dishwasher, washer, dryer, and range—a total of five appliances—that is a considerable investment. If you own four rental properties, that adds up to twenty appliances. Rather than paying for brand-new units, you will probably purchase used appliances, in which case you have to expect them to break down at some point.

A broken appliance is often not worth fixing. More likely, you will place another used unit in the home if your tenant reports a breakdown. It would not be fair to expect the tenant to pay for repairs or replacements, considering that you are providing them with used appliances. You can find used appliances that are in good working order for far less than the prices you’d pay for new ones.

![]() Structural and System Flaws. You cannot expect your tenants to take responsibility for flaws in the building itself. Examples include maintenance of heating and air-conditioning systems, roofing and siding, outside paint, and electrical and plumbing systems. All of these are the landlord’s responsibility in most cases. If tenants were to break something by using systems other than as intended, they would be responsible. For example, if a tenant decides to rewire the house and your electrical system needs to be repaired as a result, the repair would be the tenant’s responsibility. However, normal problems and periodic maintenance, such as changing filters in your heating system, are your responsibility.

Structural and System Flaws. You cannot expect your tenants to take responsibility for flaws in the building itself. Examples include maintenance of heating and air-conditioning systems, roofing and siding, outside paint, and electrical and plumbing systems. All of these are the landlord’s responsibility in most cases. If tenants were to break something by using systems other than as intended, they would be responsible. For example, if a tenant decides to rewire the house and your electrical system needs to be repaired as a result, the repair would be the tenant’s responsibility. However, normal problems and periodic maintenance, such as changing filters in your heating system, are your responsibility.

KEEPING YOUR RECORDS SIMPLE BUT EFFECTIVE

The legal contracts you need are the beginning of documentation for the terms you and your tenant agree upon. Next, you want to create a method for keeping track of the money that changes hands each month. When you think about the purpose in setting up your books in a particular way, what is the real goal? You want an effective set of books that is easy to maintain, that is easy to track and explain, and that takes as little time as possible to update. Few real estate investors want to spend a lot of time maintaining their bookkeeping system. They would rather be doing other things.

If your bookkeeping and taxes are too complex, you may want to pay a bookkeeper to maintain your records and a tax expert to fill out your tax forms each year. However, by applying a few basic rules, you can probably keep your own books—at least when you first begin investing in real estate or own one property. Later on, if you own numerous properties and have many transactions each year, including the sale of properties, you may need to hire expert help.

![]()

SUMMARY OF KEY POINTS

• Set up a separate bank account, deposit all rental income, and run all payments and expenses through the account. This is the basis of keeping clear and accurate records.

• Keep all receipts, filed by type of expense or by vendor. This way, your records are kept in one place and—with relatively little time invested—you can keep the books simple but thorough.

• Handle cash expenses consistently, collecting receipts in an envelope you keep in your vehicle, and reimburse yourself periodically by writing a check from your investment account. This helps to keep your books consistent and minimizes the chances that you will overlook a legitimate deduction.

If your records are too much to handle, or if you are spending too much time struggling with your bookkeeping, ask for help. Hire a bookkeeping expert, either to do the work for you once a month or to show you how to improve your system so that it is easier to maintain. If you continually struggle with the process, you are better off paying for the help you need. If you understand the process but do not enjoy maintaining the records, consider automating your books, using an informal system like Excel worksheets or a flexible but easy-to-use accounting program you find online.