10.

TAX REPORTING FOR ANNUAL INCOME AND EXPENSE

As an investor in real estate, your tax-reporting requirements are more complex than for most other types of investments. For example, if you invest only in stocks and mutual funds, you report interest and dividends on Schedule B and capital gains on Schedule D of Form 1040. Beyond that, there are usually no special schedules to file.

For real estate transactions, you must also report the income and expense on Schedule E, along with depreciation, passive loss limitations, and like-kind exchanges on specialized schedules. This chapter provides blank copies and examples for each of the applicable forms.

HOW TO REPORT REAL ESTATE TRANSACTIONS USING FORM 1040

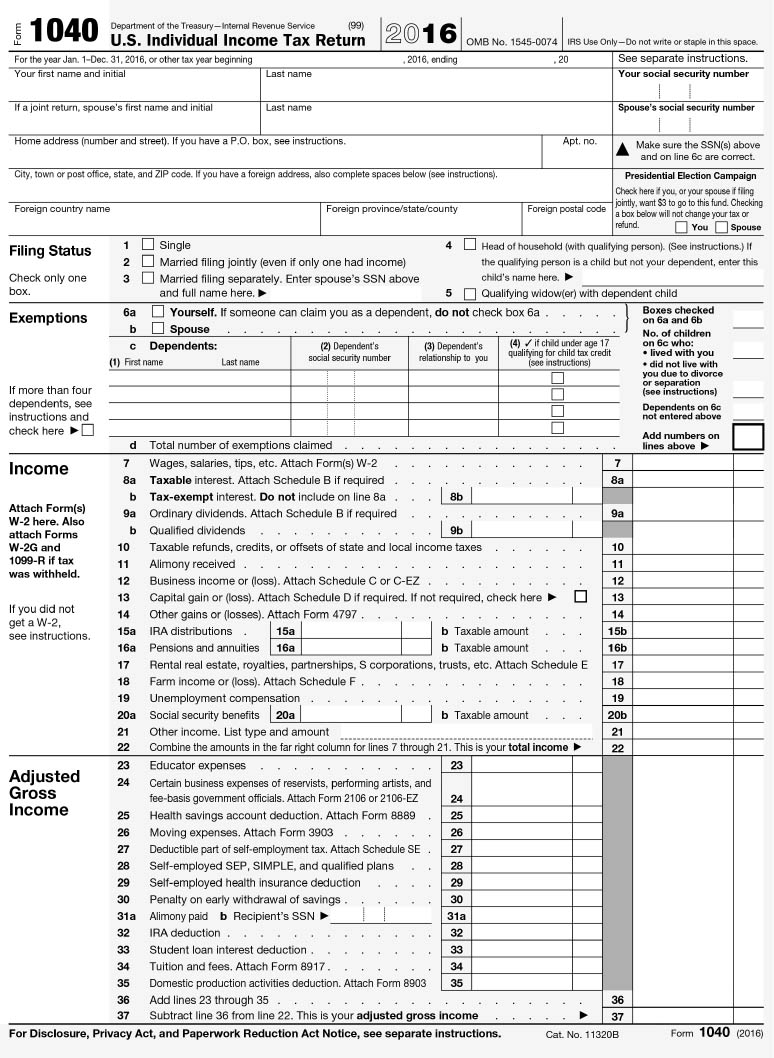

Everyone is familiar with IRS Form 1040, the summary page of every tax return. All schedules and forms that are a part of your tax return are summarized on the 1040. In the case of real estate investments, you have to transfer data from Schedule E, where income, expenses, and profit or loss are summarized. This is the primary schedule for your year-to-year real estate activity.

The two pages of Form 1040 are shown in Figures 10-1(a) and 10-1(b). The net profit or loss from real estate is reported on line 17, brought over from the bottom line from Schedule E. If you sold investment real estate during the year, you would also show an entry on line 13, capital gains and losses, the total of which is transferred over from Schedule D.

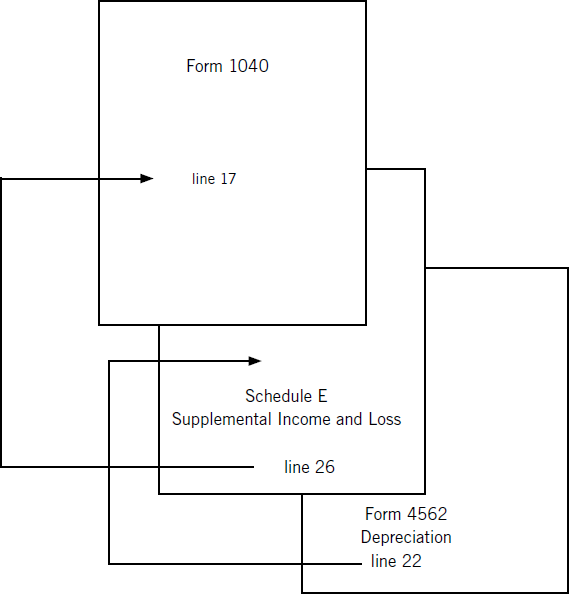

Real estate transactions are reported in a manner similar to business income, which would be reported on Schedule C (for sole proprietorships), with additional information provided on other tax schedules or by supplementary schedules. The depreciation form, number 4562, is filled in to supply further information for one line on Schedule E. The net profit or loss reported on Schedule E is then carried over and reported on Form 1040, line 17.

Figure 10-2 shows the flow of information for the typical year-to-year reporting of real estate profit and loss.

SCHEDULE A—ITEMIZED DEDUCTIONS

You also need to use Schedule A if you own your own home. If you rent out a portion of your home, the interest and property tax expenses are split between itemized deductions and rental investment expenses. Figure 10-3 shows an example of Schedule A.

ITEMIZING VS. THE STANDARD DEDUCTION

The determination of the proper division of interest and taxes raises an interesting strategic point concerning Schedule A. For example, for 2003, a married couple had a choice between itemizing or taking $9,500 as a standard deduction. Your combined interest and taxes (and other deductions) may exceed $9,500; however, if a portion of that total is properly assigned to rental investment expense, your remaining Schedule A deductions could be below the maximum standard deduction level. In that case, it would be advantageous for you to claim the standard deduction, since it would lower your taxable income and the total tax due.

![]()

EXAMPLE: You and your spouse own a home with a separate in-law unit that you rented out last year. According to your measurement of the square footage, the rental is 30 percent of the total. You record 30 percent of mortgage interest and property taxes as rental expense on Schedule E and 70 percent as itemized deductions on Schedule A. You have no other itemized deductions to claim.

![]()

Last year, your total mortgage interest was $9,618 and your property taxes were $705. The sum of these two expenses was clearly above the standard deduction of $9,500 for a married couple in 2003. However, when you record only 70 percent as itemized deductions, you end up with $6,733 interest and $494 in property taxes, or a total of $7,227.

In this case, you will reduce your total taxes by claiming the standard deduction of $9,500. Even if your tax rate is only 10 percent overall, claiming the standard deduction based on the previous example will reduce your taxes by more than $200 for the year. Is the proposed 10 percent rate realistic? It is, in fact, because the depreciation and other deductions that real estate investors are allowed to claim reduce taxable income significantly. The 10 percent rate can be achieved for many people in the middle-income range.

In the decision to itemize or use the standard deduction, you need to select the method that provides you with the greater advantage. In the previous example, it’s to your advantage to take the standard deduction. But you’re better off itemizing if the total of itemized deductions is higher than the amount allowed using the standard deduction. If your itemized deductions exceed the standard deduction even after assigning a portion of your interest and taxes to investment expense, then you would be better off itemizing.

PLANNING POINT What if itemized deductions and the standard deduction are very close? If you have numerous itemized deductions for interest and points, gifts to charity, and miscellaneous other deductions, you are entitled to list and claim them. But if the total is within a few hundred dollars of the standard deduction, it could be wise to simply forego itemizing. That reduces your exposure to audit and also simplifies your tax return.

SCHEDULE E—INCOME AND EXPENSE

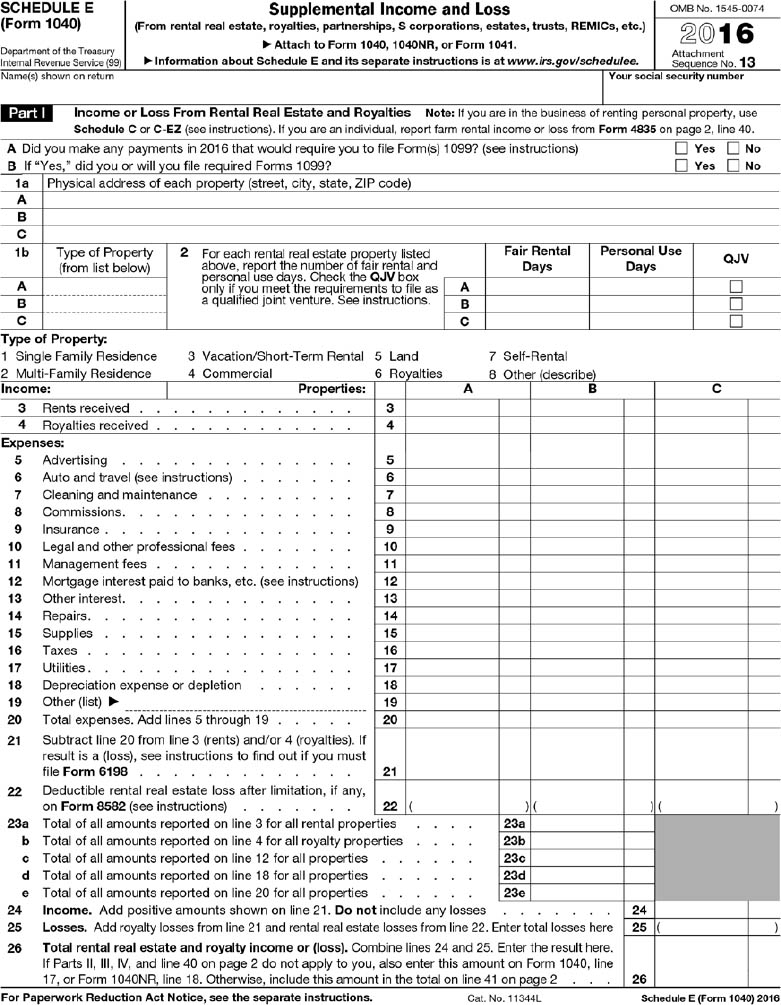

Schedule E is used to summarize income and expenses for each property. If you carry over unused losses, you can deduct them in future years when you sell a specific property or when you report passive gains. Therefore, keeping accurate records by property is essential. Figures 10-4(a) and 10-4(b) show the two pages of Schedule E. (Note: The second page of Schedule E does not relate specifically to real estate investment activities.)

FILLING OUT SCHEDULE E

For a single property, the reporting of income and expenses is straightforward. The items in your checking account, plus any cash expenses and other transactions not shown in your account, are categorized and listed on the form. You need to adjust for interest expenses and impound payments based on the information supplied by your lender.

Income. The easiest reporting occurs when you have a single rental property that is rented out full-time and is not used at all as a primary residence. To keep your records as clear as possible, it is desirable to run all rental income through a checking account established specifically for rental activity. In this way, your bank deposits will agree with the total of rental receipts plus any additional funds you transfer from your other accounts.

Payments. The record of transactions is also made easier when all of your rental-related payments are made from the same rental-specific checking account. The larger payments will be made for monthly mortgage payments, insurance, and property taxes. The interest portion of your mortgage payments is fully deductible as an expense on Schedule E. Your lender will provide you with a tax form at the end of each year, listing the total interest you paid. Insurance you pay for hazard and mortgage coverage is also fully deductible as long as the property was used exclusively as a rental. Property taxes, if paid directly, are made twice a year to your local county tax authority.

Impounds. If your lender impounds a monthly amount for property taxes and insurance, you need to report the correct amount in these two categories. That is not the total of impounds withheld but the specific payments made by your lender from the impounds it collected each month. The lender will send you a summary of impound activity each year, which will include identification of insurance and tax payments.

Additional Expenses. Other expenses are reported on the applicable line on the first page of Schedule E. Some expenses do not have a specific line and have to be added in via the spaces provided at the end of the printed list. So payments for office supplies and expenses such as telephone and landscaping, for example, will be reported on those lines.

Net Income (or Loss). Cash expenses are added up, a subtotal is shown, and below that, the total of depreciation expenses is recorded. The net income is shown on line 24 or net loss on line 25; the total is then carried over to be reported on the first page of your tax return, Form 1040, on line 17. As explained in Chapter 9, you have two limitations in claiming expenses for rental activity:

1. One is the maximum loss you can claim per year, which is $25,000.

2. The other is the reduction in that loss level when your modified adjusted gross income is higher than $100,000. For every dollar above $100,000, you lose 50 cents in deductible losses; if your adjusted gross income is $150,000 or more, you cannot claim any loss from real estate activity.

REPORTING LOSSES

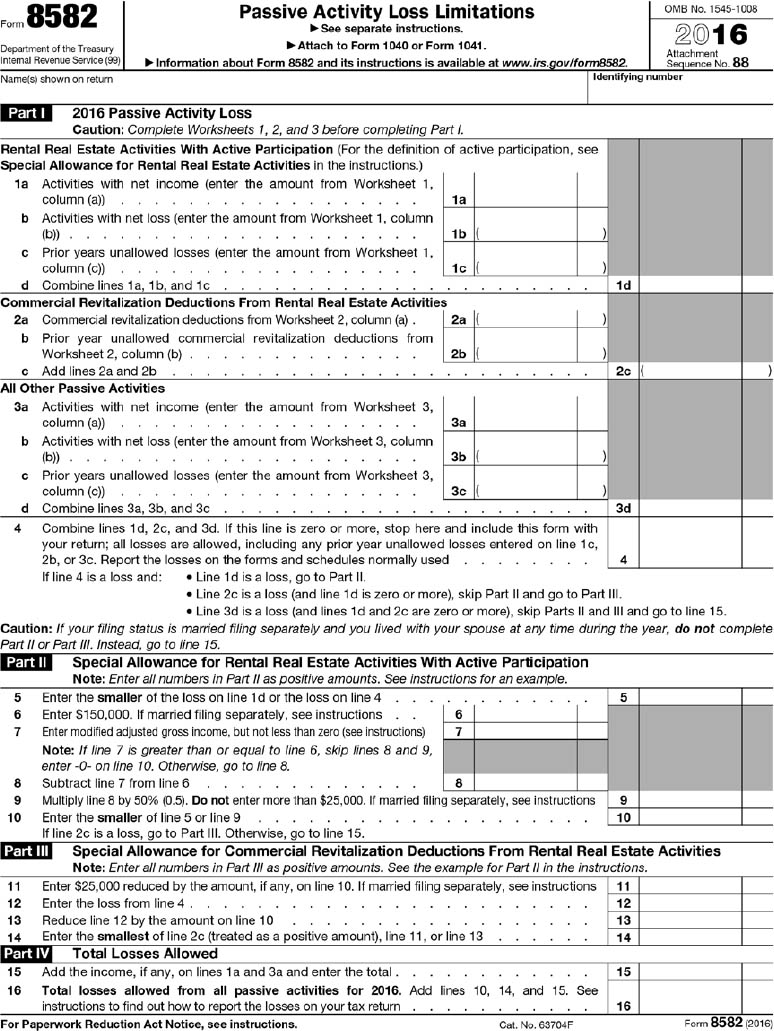

If the total is a loss, you have two possible restrictions. If the loss exceeds $25,000, the excess has to be carried forward to be used in the future. And if your modified adjusted gross income is greater than $100,000, your deductible loss will be further reduced. In either of these cases, you are required to complete Form 8582, Passive Activity Loss Limitations. This three-page form is shown in Figures 10-5(a), 10-5(b), and 10-5(c) on pages 215–217.

Record the amount of loss from real estate activities on line 1b of Form 8582. If you have any prior years’ unused losses, they are recorded on line 1c. The total of 1b and 1c is then entered on line 1d. The total is also recorded on line 4.

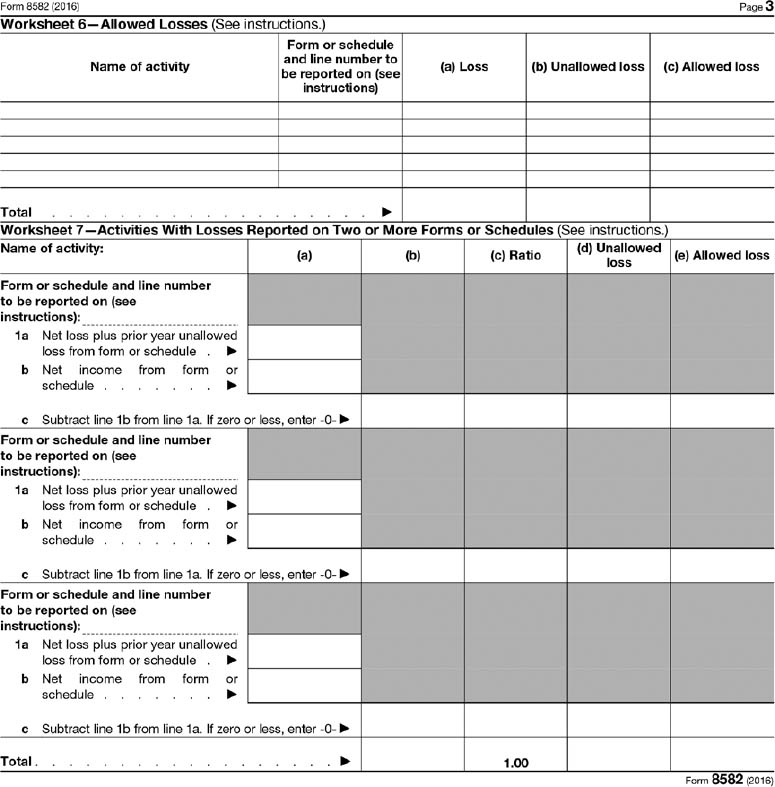

Part II of the form is used to calculate reductions in the allowed maximum loss deduction when your modified adjusted gross income is greater than $100,000. The total allowed maximum loss is recorded on lines 10 and 16. The second page of Form 8582 contains a series of worksheets that identify overall gain or loss, unallowed losses to be carried forward, and allocation of losses by property. This exercise is not only used as part of your tax return; it also provides a useful record for writing off future unused losses when you sell a specific property. The worksheets continue on page 3 of the form.

GETTING THE MOST OUT OF YOUR DEDUCTIONS

This brings up an interesting planning consideration for those who do rent out a portion of their primary residence. If you will not be able to claim a loss because your income exceeds $150,000 (or if your loss is restricted because your adjusted gross income is between $100,000 and $150,000), you have every incentive to claim as little as possible in rental expense for interest and taxes. In this situation, you want to use a method that provides the smallest rental expense and the largest itemized deduction. You can base the division of expenses on square feet, number of people living on the premises, or percentage of market rent levels, for example. If your deductions for rental expenses cannot be fully claimed, it becomes desirable and economical to assign as much as possible of your interest and property tax expense to Schedule A.

![]()

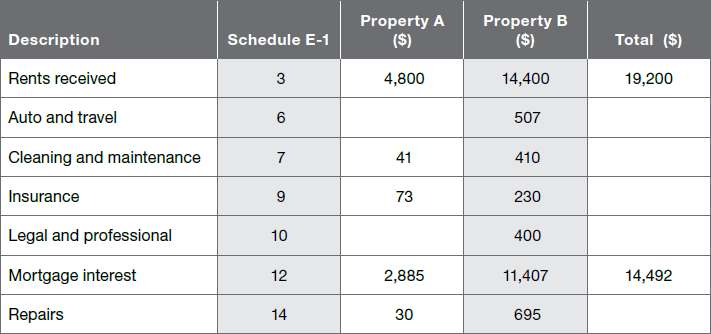

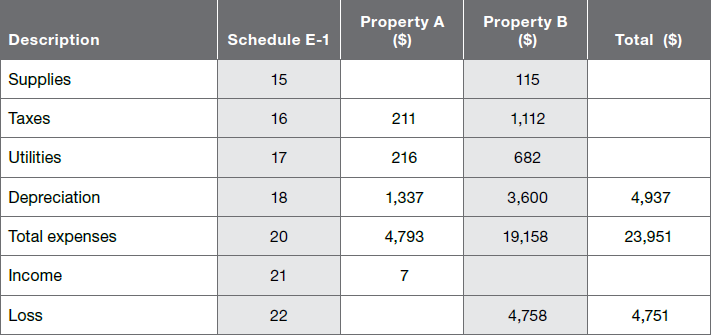

EXAMPLE: Last year you rented out 30 percent of your primary residence and received $4,800 in rents. You also owned a rental for the entire year and received $14,400. A summary of rental income and expense on each of these properties is shown in Table 10-1. Expenses for cleaning, insurance, mortgage interest, taxes, and utilities for Property A were calculated as 30 percent of the total, with the other 70 percent assigned to your personal use. Mortgage interest and taxes were assigned 30 percent to this schedule and 70 percent to itemized deductions on Schedule A.

![]()

TABLE 10-1. SUMMARY, RENTAL INCOME AND EXPENSE

If you compare Table 10-1 to Figure 10-4, you can see how these details fit into Schedule E. The table includes references to each line on Schedule E. The “total” column corresponds to those columns on the schedule that require a total: rents received, mortgage interest, total expenses and depreciation, and net income or loss.

DEPRECIATION AND AMORTIZATION

In addition to reporting any excess passive losses that are to be carried forward, you need to fill out Form 4562, Depreciation and Amortization. This form summarizes your claimed expense for each year; in addition, you may need to add a supplementary schedule showing the breakdown of depreciation. A sample of Form 4562 (two pages) is shown in Figures 10-6(a) and 10-6(b).

![]()

EXAMPLE: Last year you claimed depreciation for two properties. You depreciated 30 percent of your primary residence based on your calculation of applicable square feet; you also claimed depreciation for a rental property you owned for the entire year.

![]()

In this example, you owned both properties for the entire year, so all depreciation should be reported on line 17 and also on line 22 of Form 4562. Table 10-2 shows a typical supplementary schedule that would be attached to your tax return to provide more details on claimed depreciation.

TABLE 10-2. SUPPLEMENTARY SCHEDULE, DEPRECIATION EXPENSE: STRAIGHT-LINE (SL) METHOD (deductible portion in italic)

Any amortization claimed is listed on lines 42 and 44 on the second page of Form 4562.

DOCUMENTING LARGE EXPENSES

Reporting real estate transactions can involve some large numbers, notably for interest and property taxes. How do you document these expenses?

Interest Paid. A bank or savings institution is required to send you and the IRS an annual report called Form 1098. It identifies the loan and the total interest you paid during the year. You should ensure that the amount you computed and reported on your tax return agrees with the total reported to you on Form 1098. You may also wish to attach a copy of this form to your tax return for each property in order to document the expense that you are claiming. If you divide your primary residence interest between Schedule A and Schedule E, you should also attach a summary of your calculation. You may show the calculation right on the copy of Form 1098 that you attach to your return. For example:

Total square feet in the property = 3,400

Total square feet in the rental unit = 1,020 = 30% × 3,400

Interest included on Schedule E = 30% × $9,618 = $2,885

Interest included as itemized deduction = 70% × $9,618 = $6,733

![]()

KEY POINT If you end up claiming a standard deduction instead of itemizing, it does not matter. This brief summary supports what you have claimed as applicable to rental activity, based on total square footage of your property.

Property Taxes. It may also be desirable to attach documentation of other major expenses, such as property taxes. This is especially worthwhile if you divide the expense between the two schedules. Attach a copy of the bill from your county, with the breakdown clearly shown. For example:

Total property taxes = $705

Total square feet in the property = 3,400

Total square feet in the rental unit = 1,020 = 30% × 3,400

Taxes included on Schedule E = 30% × $705 = $211

Taxes included as itemized deduction = 70% × $705 = $494

HOW MUCH DOCUMENTATION TO PROVIDE

Opinions vary on whether you should attach documentation to your tax return proving expenses or showing your breakdown. One school of thought states that you should not supply any information that is not specifically required. The other school of thought contends that by proving an expense up front, you anticipate and answer questions before they are asked. Both sides make valid points. The decision should be based on your exposure to a possible audit and on whether it is worthwhile to provide documentation with the idea of preventing an audit from happening.

Providing documentation along with your tax return may help ward off an audit. If a tax return is selected for audit and reviewed, having documentation attached will answer the big questions. For example, it may be that your return is pulled because you claim a very high expense for interest and taxes. If the IRS were to audit your return, they may also ask to see receipts for utilities, office expenses, legal fees, cleaning, and other items. However, if the major items have been explained, then auditing the other line items would not be necessary.

![]()

KEY POINT Maintaining complete, accurate records will enable you to successfully handle an audit in most cases. It’s up to you how much documentation to provide along with your return.

FORM 4797 AND SCHEDULE D—SALE OF RENTAL PROPERTY

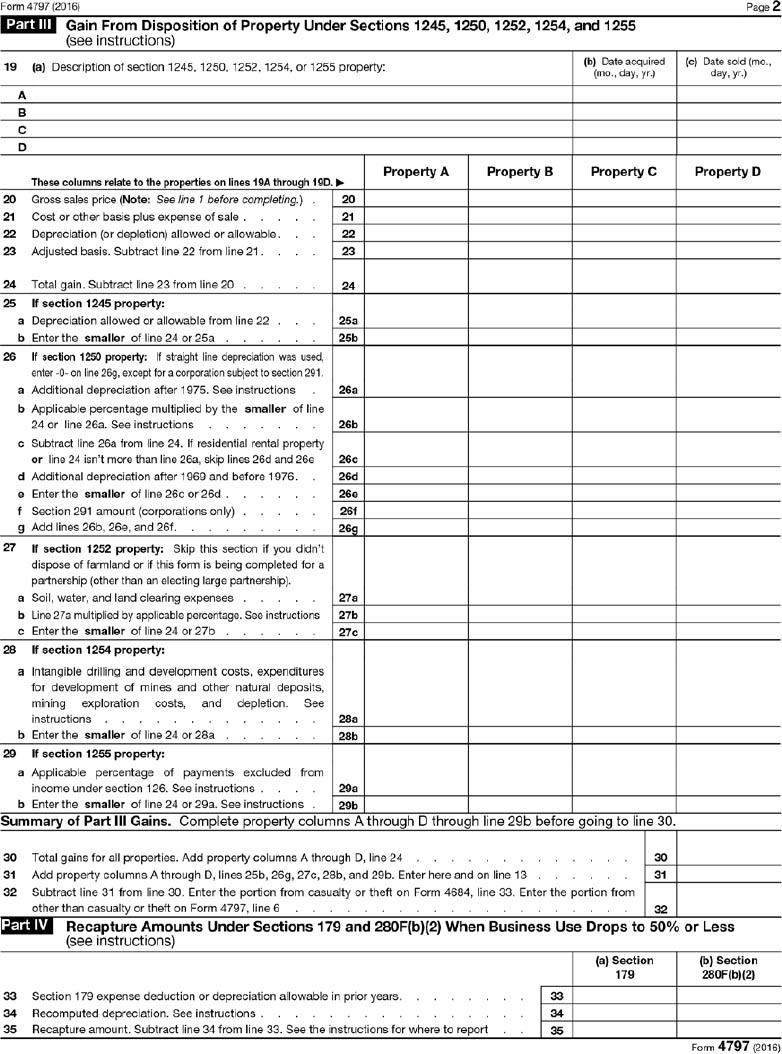

Beyond the year-to-year reporting of rental income and expense, you also need to fill in special forms to report capital gains on rental property for the year in which you sell. For this, you use Form 4797 and Schedule D. A sample of Form 4797 is shown in Figures 10-7(a) and 10-7(b).

Why two different forms for one transaction? Form 4797 is used to report sales of investment properties. The details are listed on this form, with the single-line profit or loss transferred to Schedule D, which summarizes capital gains or losses. The totals from Schedule D are then transferred to line 13 of Form 1040. The system is set up so that you can report all activity in the right place. For example, if you sell a property and also had capital gain distributions from mutual fund shares and, perhaps, a net loss from selling stock, all of your capital gains and losses end up on Schedule D.

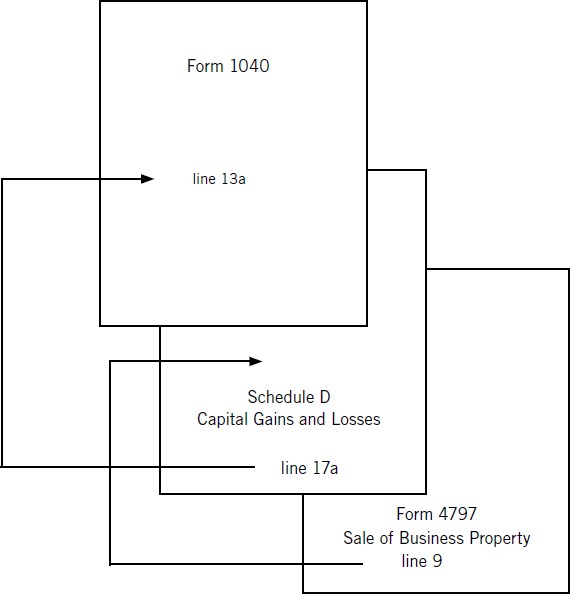

A summary of the flow of information between schedules is shown in Figure 10-8.

A sample of Form 4797 (two pages) is shown in Figures 10-9(a) and 10-9(b).

The flow of reporting information for rental property capital gains is shown in Figure 10-8. The reported gain or loss is transferred from Form 4797 to Schedule D and then onto Form 1040. This volume of forms is necessary. Schedule D is designed to report all capital gains and losses, including those reported on Form 4797 and those shown only on Schedule D. The need for several specialized forms comes from the need for uniformity.

![]()

EXAMPLE: You sold a property in 2015 that you bought two years before and realized a gain. The adjusted sales price was $147,366. You had claimed depreciation while you owned the property totaling $5,119; your original net purchase price was $119,417. Your net capital gain of $33,068 would be reported on Form 4797 as shown on Table 10-3.

![]()

TABLE 10-3, FORM 4797 REPORTING

Line |

Information |

2a |

Address |

2b |

1/15/13 |

2c |

4/13/13 |

2d |

$147,366 |

2e |

$ 5,119 |

2f |

$119,417 |

2g |

$ 33,068 |

7 & 9 |

$ 33,068 |

This information is transferred to Schedule D—the two-page form shown in Figures 10-9(a) and 10-9(b). The net capital gain of $33,068 is reported on that schedule on lines 11, 15, and in Part III, line 16.

![]()

KEY POINT The distinction between short-term and long-term capital gains is important because they are taxed differently. Taxes on long-term gains (i.e., assets held more than one year) are lower than those on short-term gains, which are taxed at the same rate as other taxable income.

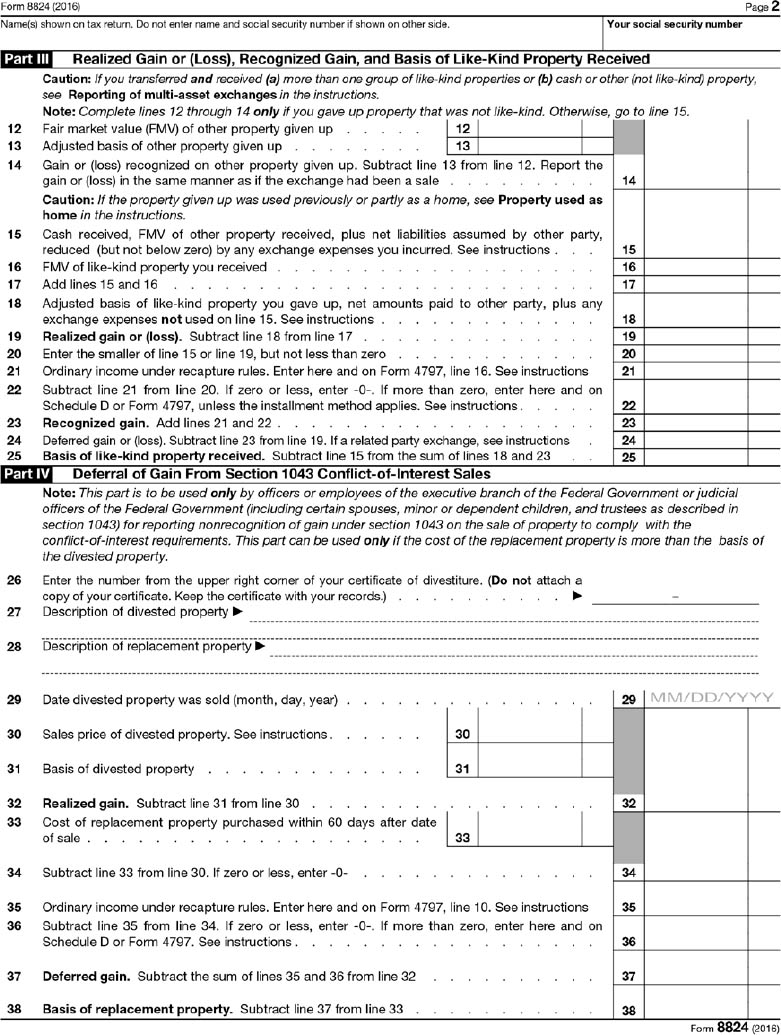

REPORTING LIKE-KIND EXCHANGES

As a real estate investor, a final form that you may need to complete is Form 8824, for reporting like-kind exchanges. These exchanges (1031 exchanges) allow you to defer taxes to a future sale. A sample of Form 8824 (four pages) is shown in Figures 10-10(a) and 10-10(b).

FOLLOWING THE SPECIFIC RULES

In a like-kind exchange, you are required to follow very precise rules for the timing of transactions and dollar amounts of replacement property. The purchase of replacement property has to be completed within 180 days of the sale of the original property. In a like-kind exchange, the gain on sale of investment property is deferred until you sell the replacement property, and this is achieved by reducing the basis in new property. For example, instead of reporting the current-year profit of $33,068 on Schedule D (see previous example), you may have been able to execute a like-kind exchange by purchasing another real estate investment.

![]()

EXAMPLE: You sold a rental property last year for $147,366 and replaced it with a like-kind exchange property. You bought the new property for an adjusted purchase price of $161,220 and closed the sale within the 180-day window.

![]()

In this example, your $33,068 profit reduces your basis in the new property. Although your adjusted purchase price was $161,220, your basis for tax purposes is calculated as shown in Table 10-4.

TABLE 10-4. ADJUSTED BASIS ($)

Adjusted purchase price |

161,220 |

Less: Deferred gain |

33,068 |

Adjusted basis |

128,152 |

![]()

KEY POINT When you eventually sell this newly acquired property, your gain will be reported not as the difference between purchase price and sale price but between basis and sale price. This is how gains are deferred in like-kind exchanges.

The rules for reporting real estate transactions can be quite complex. You may need to use the services of a qualified tax adviser, especially in those years when your transactions include capital gains or losses, like-kind exchanges, or adjustments in the passive losses you are allowed to deduct.

FIGURE 10-1(A). FORM 1040, PAGE 1.

FIGURE 10-1(B). FORM 1040, PAGE 2.

FIGURE 10-4(A). SCHEDULE E, PAGE 1.

FIGURE 10-4(B). SCHEDULE E, PAGE 2.

FIGURE 10-5(A). FORM 8582, PAGE 1.

FIGURE 10-5(B). FORM 8582, PAGE 2.

FIGURE 10-5(C). FORM 8582, PAGE 3.

FIGURE 10-6(A). FORM 4562, PAGE 1.

FIGURE 10-6(B). FORM 4562, PAGE 2.

FIGURE 10-7(A). FORM 4797, PAGE 1.

FIGURE 10-7(B). FORM 4797, PAGE 2.

FIGURE 10-9(A). SCHEDULE D, PAGE 1.

FIGURE 10-9(B). SCHEDULE D, PAGE 2.

FIGURE 10-10(A). FORM 8824, PAGE 1.

FIGURE 10-10(B). FORM 8824, PAGE 2.