2.

GETTING STARTED IN RENTAL PROPERTY INVESTING

There is no single way to invest in real estate. Just as the stock market offers a rich variety of methods for the flexible investor, real estate can also be approached in a number of ways. You can distinguish between types of property, for example, with each having its own supply and demand features. In some cases, one type of property will have very strong demand whereas another may be soft. For example, a large portion of the local population might consist of college students (creating a strong demand for multiunit rental housing), but at the same time, there might be very little retail trade or manufacturing in the area (causing a soft market for commercial and industrial property).

Real estate, like the stock market, can be set up according to the type of investment you want and the level of risk you’re willing to accept. Every investment has attributes; these attributes define income opportunity as well as risk. Before deciding whether to invest in real estate, you should examine the positive and negative attributes in order to evaluate opportunity and risk—just as you would do with any form of investing.

LOCATION, LOGISTICS, AND LIMITATION

According to an old adage, the three most important attributes of real estate are location, location, and location. Actually, it might better be restated as location, logistics, and limitation. These are the three attributes that define whether real estate represents a sound investment.

1. Location, of course, is the central defining element of a “good” real estate investment. The vast difference in land values between 400 acres of Texas scrubland and a quarter acre in downtown Dallas makes this point. Whereas the scrubland is next to valueless, the location of the urban land creates a strong demand that drives up its value.

2. Logistics is the second defining attribute. It does not matter how desirable land is in terms of its size, topography, and vegetation if it is not logistically viable as an investment. This means that you need basic services—roads, utilities, and access—to ensure that the land will grow in value. You cannot build a house in the middle of an area that does not have access to needed services. The logistics dictate that such a property is not a practical investment.

3. Limitation is the third attribute that defines investment value. In areas such as Manhattan, San Francisco, and Tampa Bay, the proximity of land to water naturally limits how much development can occur. There is a finite amount of land. As a result, land becomes increasingly valuable as more demand for improvements comes into play. When the land has been fully developed, further construction has to move upward, or prices simply rise in response to the situation: The limitation of land means the supply is not enough to meet the demand, so land values rise.

OTHER CONSIDERATIONS There are many additional aspects to real estate investing, of course. You also need to consider tax advantages, limitations on capital to invest, and the unavoidable aspect of dealing with tenants, lenders, and local economic changes that could lead to vacancies. Real estate investment requires careful planning. In turn, planning demands that investors understand how to keep accurate records, plan ahead for taxes, and make the right decisions today to protect the value of their investments, possibly for many years to come.

FINANCIAL PLANNING

The decision to become a real estate investor is usually made as part of a larger personal financial plan. Many considerations are involved: available capital, family income, comfort levels with owning real estate and carrying a large dollar amount of debt, other assets (stocks, retirement accounts, and savings, for example), and long-term goals. Once you decide that you want to include investment real estate in your financial plan, you also accept the attributes that go along with your decision. The financial planning considerations include:

![]() Capital Limitations. If you have little or no money to invest, real estate will not be a serious prospective market for you. Because of the inherent risks of cash flow and debt financing, you will be in better shape when you have savings and adequate other investments available. Few people would seriously consider beginning a real estate investment plan without first establishing more liquid investments.

Capital Limitations. If you have little or no money to invest, real estate will not be a serious prospective market for you. Because of the inherent risks of cash flow and debt financing, you will be in better shape when you have savings and adequate other investments available. Few people would seriously consider beginning a real estate investment plan without first establishing more liquid investments.

As a practical matter, it is very difficult to begin a real estate investment plan before you have adequate capital resources. Whether those resources are acquired through inheritance, savings, sound investment strategies, or other means, they are essential. Some investors are unwilling to face the reality and to acknowledge the potential problems of getting into real estate before they are ready. The tendency is to limit the question to having enough cash for a down payment, but the problem of capital limitation is far more complex. If you don’t have any cash reserves or income available to cover a month or two of expenses when no rent is coming in, then the risks of rental real estate are too high. If you cannot qualify for a mortgage loan because you lack assets as well as a high enough level of income, then there is no point in pursuing creative alternatives to overcome the financial limitations. The risks are real. The best choice is to wait until you are better situated and put real estate aside for the moment.

![]() Family Income. You need to balance all investment programs with your personal income level. Of course, someone earning a very low monthly wage would not be able to qualify for the mortgage loans needed to begin a real estate investment program. Family income, if too low, would preclude your ability to qualify for loans. Of equal importance, when you live on a tight budget, you cannot afford to carry a large debt whose payments depend on rent payments by tenants. In that situation, two or three months’ vacancies could destroy the family budget.

Family Income. You need to balance all investment programs with your personal income level. Of course, someone earning a very low monthly wage would not be able to qualify for the mortgage loans needed to begin a real estate investment program. Family income, if too low, would preclude your ability to qualify for loans. Of equal importance, when you live on a tight budget, you cannot afford to carry a large debt whose payments depend on rent payments by tenants. In that situation, two or three months’ vacancies could destroy the family budget.

![]() Outside Factors. As an example, a community whose revenue is derived largely from tourism may suffer big losses in retail trade due to national economic conditions, political turmoil, and other outside causes. The effect on commercial values, even if temporary, is very real. It’s even possible that commercial values could be more volatile than comparable values in communities that are more self-sustained. For example, an antique store located in Niagara Falls is likely to be more vulnerable to economic change than one carrying the same items in Omaha, Nebraska, or Philadelphia.

Outside Factors. As an example, a community whose revenue is derived largely from tourism may suffer big losses in retail trade due to national economic conditions, political turmoil, and other outside causes. The effect on commercial values, even if temporary, is very real. It’s even possible that commercial values could be more volatile than comparable values in communities that are more self-sustained. For example, an antique store located in Niagara Falls is likely to be more vulnerable to economic change than one carrying the same items in Omaha, Nebraska, or Philadelphia.

![]() Basis for Valuation. Another important difference in valuation between residential and commercial properties is the basis for valuation itself. Appraisal of residential property is usually done on the replacement or cost basis. The appraiser finds comparably sized homes with similar features, located in similar neighborhoods, then makes needed adjustments to arrive at an approximation of value. However, commercial property valuation has to take different factors into account. A well-constructed building has little commercial value if a highway bypass keeps traffic away, whereas a poorly constructed, outdated building located right in the middle of vehicular and pedestrian traffic lanes will have a higher value than property located a few blocks away.

Basis for Valuation. Another important difference in valuation between residential and commercial properties is the basis for valuation itself. Appraisal of residential property is usually done on the replacement or cost basis. The appraiser finds comparably sized homes with similar features, located in similar neighborhoods, then makes needed adjustments to arrive at an approximation of value. However, commercial property valuation has to take different factors into account. A well-constructed building has little commercial value if a highway bypass keeps traffic away, whereas a poorly constructed, outdated building located right in the middle of vehicular and pedestrian traffic lanes will have a higher value than property located a few blocks away.

![]()

KEY POINT Investors in commercial property cannot depend on residential criteria for selection and valuation. They need to have, or to hire, expertise that can be used to set value based on income generation potential, local trends, and economic, political, or cyclical factors, if applicable, that will affect a property’s value.

THE RESIDENTIAL PROPERTY MARKET

Residential property is usually the preferred starting point for investors. The commercial market, valuation of property, and demand features may be too complex (and the risk factors too high) for the beginning real estate investor. Most people more easily understand residential property. Buying a house or duplex as a starting point is often a more comfortable choice.

IMPORTANT Assessing the demand features of real estate in terms of the need for rentals (versus the separate market controlling price trends in housing) is the key to selecting properties in the right place.

Demand may vary within a single community, as well as from one area to another. Many tenants need to be close to public transportation and shopping. Students prefer to be close to their college or university. Elderly or low-income families prefer housing close to public facilities and local assistance offices. Consequently, properties in more remote areas of town may experience greater vacancies than those closer to the conveniences that the mix of tenants finds desirable.

THE MANY ASPECTS OF LOCATION

Location is not limited to the city or town alone; it may also vary by proximity within a city or even within a fairly small town. Most experienced real estate investors have discovered that it is easier to pick properties wisely if they are intimately familiar with these subtle but important distinctions. Demand can be lower than average just because a specific property is a mile away from the closest bus line, school, or shopping center. A property that is well located in terms of conveniences is likely to remain occupied at a higher rate; when markets begin to soften, the better situated properties tend to stay occupied longer. In addition, location will also affect market rent levels, so that property will produce better cash flow as well. The point is that you may think of “location” as having several aspects.

Regional. In the broadest sense, location refers to the region of the country—a specific city, town, or even a state. In fact, national statistics break down trends in residential real estate values by regions in that manner: Northeast, Midwest, Northwest, and so on. The broadly defined location is of little value in picking properties. Just as stock indexes reveal overall trends in the stock market, national and regional real estate trends provide an average view, but averages consist of strong and weak markets, collectively.

City to City. When we get down to more localized definitions of location, we can study real estate from city to city. If you have studied the market at all, you already know that values can and do vary significantly from town to town. Two cities, one next to the other, may have vastly different markets. One city may have consistently strong growth and property value trends, whereas the other is stagnant. Subtle differences in economic conditions or the political environment can make a big difference even when geography is not great. One city may be governed by a council that encourages employment and new housing, and its real estate market is likely to be robust. Another city may not encourage new employment or building, so that people move away and there is no reason to expect real estate prices to grow. A lack of demand—generated from employment growth and the related population growth—means there is no real market for housing, so there is no reason to expect growth at any time in the near future, either.

Neighborhoods. Location can be even more finely defined. Within one city or town, certain areas are thought to be more desirable than others. Older, more established neighborhoods, those with their own grocery stores and other outlets, on quiet streets, will bring higher prices, and their market value will outpace the local averages. Homes located near highways, in high-crime neighborhoods, or close to downtown congestion or noise are going to grow at a slower pace.

Individual Houses. In addition, you can look at two houses in the same neighborhood and see considerable differences in value. Consider two houses only one block apart: One house is on a very busy thoroughfare and directly across the street from a school. Every morning and afternoon, dozens of buses and cars fill the street. During the recess and lunch periods, you can hear the sounds of children playing. The older children walk by the house, so lawns often are littered. The second house is one block away from the school, as well as the noise, congestion, and littering problem. While both of these houses are identical, the second house—because it is one block removed from the problems—will grow in value faster than the one on the busy street in the school zone.

Other Houses in the Area. The houses next to the house you’re thinking of buying also affect value. If they are well maintained and the neighborhood has a consistently high level of cosmetic maintenance, then your house will benefit. By the same argument, if neighbors do not care for their properties, they will hold down value in your investment property.

Owner-occupied housing tends to increase in value more than rental properties. With this in mind, it is strategically wise to invest in single-family properties in largely owner-occupied areas. That factor, a subtle interpretation of “location,” will help maintain your property’s value in line with the larger neighborhood trend. As long as you keep your property in good shape, it is likely to grow in conformity with other homes. In comparison, if you buy a property in an area characterized by other rentals, market growth is likely to be lower than it would be in neighborhoods with a majority of owner-occupied houses.

![]()

KEY POINT The location factor cannot be overlooked in the property study. It determines the ultimate value of the investment. Just as one stock will outperform other stocks in the same business sector for a variety of specific reasons, one house will perform better for you because of its location, condition, and neighborhood.

These observations are general rules of thumb. They do not dictate all markets, and you will find that every situation is unique. Real estate is truly a local investment that is affected not by national averages but by what is going on right there in town: employment, population demographics and trends, crime levels, transportation, shopping, and condition of the property and neighborhood. All of these factors affect long-term investment value, rental demand, and the likely occupancy and vacancy rates.

DIRECT OWNERSHIP OF RENTAL PROPERTY

The best known and most popular form of real estate investment is direct ownership. This normally involves financing the major portion of the purchase and paying the mortgage with rental income. This traditional approach is appealing to most investors—as long as rents continue to cover the cash flow demands—because it also involves favorable tax benefits (see Chapter 9).

Lenders are likely to apply much higher standards when you invest than when you buy a home and occupy it yourself. These standards apply to credit history, income, down payment requirements, and debt-to-value ratio. When you buy your own home, you can normally finance 90 percent of the purchase price and sometimes even more. Veteran’s Administration (VA) and Federal Housing Administration (FHA) loans, for example, often allow you to finance practically the entire purchase price. For nonoccupied housing or for commercial property, you may be required to pay a higher interest rate and come up with a higher down payment as well.

ADVANTAGES OF DIRECT CONTROL

While there are other ways to invest money in real estate, direct ownership has the greatest appeal. Stockholders own equity in a public company, but they have no real control. The ownership of a small fraction of stock provides the potential for appreciation in market value and dividend income, and stockholders have the right to vote on certain decisions, but they have no say in the day-to-day operations of the corporation. In comparison, when you own rental property, you do have direct control. You maintain the house by keeping the roof, landscaping, and internal systems in good repair; by selecting and paying for responsible homeowner’s insurance; and by keeping an eye on the property itself. You determine whether to paint the house a different color, add structural improvements, or refinance the mortgage to take out equity. In other words, the management of the investment is in your hands. For the purpose of market value, appreciation depends to an extent on local supply and demand as well as on the three Ls (location, logistics, limitations). Yet, to an equal degree, the value of the investment also depends on your individual effort in keeping the property in good shape, well maintained, and properly cared for.

HANDLING PROBLEMS

For a real estate investor, direct control also means that you need to deal with both expected and unexpected problems as they arise. The mortgage payment has to be made on time every month, even if your tenant does not pay rent or, equally troubling, if your property is vacant. The heating system breaks down, the roof begins to leak, or you discover an infestation of termites or ants. All of these expensive problems—none of which will be covered by your insurance—cannot be planned for, but they all occur. If you own your own home, you already know that maintenance never ends; it only pauses for a few months.

BUILD A RESERVE When you invest in rental property, you want rental income to be consistent and adequate to cover your mortgage payment—and it is wise also to establish a reserve fund for repairs.

MINIMIZING MAINTENANCE

If you purchase a newly built home to use as an income property, you should not experience any expensive repairs for several years. Properties go through maintenance cycles, and the first cycle tends to arrive about seven years after a house is built. To avoid the more expensive repairs, then, you could buy new homes and sell them after six years. Of course, this is not always a practical strategy. It may not be possible to afford new homes for investment, especially if older homes in your area are available for less money. You also cannot control the real estate cycle. Demand for housing could be low in six years when you would like to sell. You cannot control supply and demand, so the plan of timing investments to avoid unexpected maintenance costs is probably not practical.

CHOOSING PROPERTIES CAREFULLY

On balance, the advantages of direct control outweigh the problems if you select properties carefully. This requires that you inspect the properties and critically check their condition. For older homes especially, it is worth requiring an independent home inspection as part of the buying process. A qualified and independent inspector prepares a written report and has to disclose the condition of all systems in the property. If maintenance is needed, you can require it to be performed as a condition of buying the property. This protects you from the shock of unknown and expensive repairs you’d otherwise need to perform only a few months after you buy the property.

VALUABLE RESOURCE The American Society of Home Inspectors (ASHI) licenses individuals to perform professional home inspections and to guarantee their findings. To locate a licensed inspector, contact ASHI online at http://www.homeinspector.org.

Once you have ensured that properties do not have any hidden flaws, you are able to eliminate the potential problem of buying properties only to discover too late that they need extensive and costly repairs. A home inspection reduces your risk, at least in the immediate future. However, properties need ongoing maintenance, and this fact should be considered in evaluating the entire idea of investing in rental properties, especially for the long term.

FINANCING YOUR RENTAL INVESTMENT

Few people have enough cash available to buy properties outright, so they have to borrow the money, which means they purchase rental real estate with a mortgage. The selection of a competitive mortgage and terms will determine the long-term cost because a fractional change in interest adds up over the years. Here are some guidelines worth remembering when you finance or refinance your investment property, as compared to the same rules for your residence:

![]() Lenders apply a different standard to investor qualification. Homeowners with excellent credit and strong income can usually find attractive terms—low rates and low down payments. However, when you buy investment property, you are expected to pay a higher interest rate. Since the property will not be owner occupied, lenders will view the mortgage loan as having greater risks.

Lenders apply a different standard to investor qualification. Homeowners with excellent credit and strong income can usually find attractive terms—low rates and low down payments. However, when you buy investment property, you are expected to pay a higher interest rate. Since the property will not be owner occupied, lenders will view the mortgage loan as having greater risks.

![]() Down payment requirements may be higher. Lenders usually expect investors to put more down for their properties than they would ask of homeowners. For example, you might be able to locate an 80 percent or 90 percent loan for your own home (and sometimes even 100 percent). With rental property, some lenders are going to demand 30 percent as a down payment. As a general rule, if lenders will grant a mortgage for less down, they will also expect a higher interest rate.

Down payment requirements may be higher. Lenders usually expect investors to put more down for their properties than they would ask of homeowners. For example, you might be able to locate an 80 percent or 90 percent loan for your own home (and sometimes even 100 percent). With rental property, some lenders are going to demand 30 percent as a down payment. As a general rule, if lenders will grant a mortgage for less down, they will also expect a higher interest rate.

![]() You may need to seek nonconventional financing sources. You may find the best rates by shopping online for a mortgage. A simple Internet search under “mortgage” will reveal dozens of sources for mortgage loans, with competitive rates. You can narrow down the market for nonowner-occupied financing, but even then you will find that the traditional sources often exclude you if you want to borrow money for rental investments. You may consider private sources or even look for seller financing. (Be careful, however. A seller who offers to carry the loan could mean the property has defects that need to be fixed. Such defects would become your problem if you buy the property.)

You may need to seek nonconventional financing sources. You may find the best rates by shopping online for a mortgage. A simple Internet search under “mortgage” will reveal dozens of sources for mortgage loans, with competitive rates. You can narrow down the market for nonowner-occupied financing, but even then you will find that the traditional sources often exclude you if you want to borrow money for rental investments. You may consider private sources or even look for seller financing. (Be careful, however. A seller who offers to carry the loan could mean the property has defects that need to be fixed. Such defects would become your problem if you buy the property.)

![]() You may not be allowed to remove cash upon refinancing. Typically, homeowners can refinance their loans when rates go down and even take out cash because their equity has increased. With rental real estate, many lenders will not allow you to remove cash upon refinancing, even if the equity is there. This more conservative policy reflects the perception that nonowner-occupied property presents greater risks for lenders.

You may not be allowed to remove cash upon refinancing. Typically, homeowners can refinance their loans when rates go down and even take out cash because their equity has increased. With rental real estate, many lenders will not allow you to remove cash upon refinancing, even if the equity is there. This more conservative policy reflects the perception that nonowner-occupied property presents greater risks for lenders.

![]() It will be more difficult to find lines of credit. Homeowners can find equity lines of credit, which are excellent alternatives to refinancing. They can draw on the credit when they need to, borrowing only as much as they need and then paying down the debt when they can afford to. In fact, some lenders allow homeowners to take out an equity line of credit up to 100 percent of their equity and, in some instances, even more. For investors, however, it is more difficult. Most conventional lenders restrict their lines of credit only to owner-occupied housing. You may be able to find such a line of credit, but it will require some research.

It will be more difficult to find lines of credit. Homeowners can find equity lines of credit, which are excellent alternatives to refinancing. They can draw on the credit when they need to, borrowing only as much as they need and then paying down the debt when they can afford to. In fact, some lenders allow homeowners to take out an equity line of credit up to 100 percent of their equity and, in some instances, even more. For investors, however, it is more difficult. Most conventional lenders restrict their lines of credit only to owner-occupied housing. You may be able to find such a line of credit, but it will require some research.

COMPARING OWNER-OCCUPIED AND INVESTMENT FINANCING

Qualifying for a mortgage, even for an owner-occupied primary residence, is not always well understood. When considering the same questions for investment property, the confusion tends to increase.

Credit is a primary consideration for any type of mortgage. As a basic requirement to qualify for a loan, your credit history is normally the first issue a would-be lender is going to tackle. It’s logical. A lender wants to analyze the probability of getting paid on time every month, and credit history reflects the borrower’s level of credit responsibility. It is fair to say that an excellent credit history is essential for a real estate investor and that a poor credit history makes the venture impractical. Most lenders want to see a positive credit score, perhaps above 725 to 750; any score above 800 is excellent. A score below 600 presents problems for lenders and, as a consequence, for investors as well.

The credit score is developed from the history of on-time or late payments; outstanding judgments and items that have gone to collection; past defaults on loans; and any negative items reported. A single late payment, for example, can be explained away or seen as an exception. Two or more late payments indicates a more serious problem.

Down payment is a second item the lender wants to consider. For owner-occupied houses, the down payment for an FHA loan is 3.5 percent in most cases; a VA loan may be obtained with zero down. However, the lower the down payment, the higher monthly payments will be, so borrowers with a large down payment are better risks for lenders. Conventional loans may require as much as 10 percent down.

For investment property, expect to be required to come up with a 20 percent down payment. So a house priced at $150,000 will require a down payment of $30,000.

Financial tests of income and debt are the third and equally important test for qualification. Lenders look at the debt-to-income (DTI) ratio. This is calculated as your monthly expenses, including the proposed mortgage, as a percentage of your gross monthly income. If your DTI is higher than 50 percent, you probably will not qualify for the loan.

UNDERSTANDING LENDING RULE RESTRICTIONS

Rules for conventional financing are restrictive because lenders themselves have to meet specific rules. Most loans are not kept by the original lender but are resold to the secondary market. Even if lenders continue to service a loan (i.e., collecting payments and impounds, the periodic increments taken for property taxes and insurance), the debt itself usually ends up being sold to an organization such as the Government National Mortgage Association (GNMA), also known as Ginnie Mae, or the Federal National Mortgage Association (FNMA), or Fannie Mae. Mortgages are pooled, and shares are then sold to investors.

With this secondary market dictating terms for mortgage loans, it is not always up to the lender whether to grant your loan. If the lender intends to sell your mortgage debt on the secondary market (which commonly occurs), the specific terms imposed by that market have to be met. These terms relate to credit rating, interest rate, down payment, type of property, and DTI.

![]()

KEY POINT The lowest risk—from a lender’s point of view—is a loan granted on an owner-occupied house, with a large down payment, and with a borrower whose credit is excellent. Not everyone meets all of these conditions, so varying degrees of approval are possible. The higher the risk, the higher the interest rate will be, and the more down payment you’ll be required to deposit.

Investors will have more difficulty than for owner-occupied housing. Whenever your equity in the property is less than 20 percent, you are going to be required to carry a form of mortgage insurance designed to pay the lender in case you default. So, even though you are required to make a larger down payment, you also escape having to pay expensive insurance in addition to the fire and casualty insurance you have to carry on the property.

STARTING WITH YOUR PRIMARY RESIDENCE

Some investors have figured out that they can simplify the approval process by getting loans on their primary residence rather than trying to meet the higher standards of investment property. For example, if you currently live in a house and you’d like to begin an investment program, one solution is to locate a new primary residence and go for financing based on your plans to move into the new property. As soon as the transaction is complete, you move into the new home and convert your current residence into a rental. You will be able to continue making the same mortgage payments on your current home (which was financed originally based on your occupying the property as your primary residence) and rent the property out.

It is possible to accumulate a series of rental properties by simply moving into a series of new owner-occupied homes as the timing and your own financial situation dictate. The only requirement on the part of conventional lenders is that the property being financed must be your primary residence at the time the loan is approved. In theory, you could change your mind the day after the loan was approved and convert the new property to a rental. But this could be interpreted as making a false claim on your loan application. It is safer and wiser to move into the new home and convert your current primary residence to a rental as a bona fide change of status, even if only for a few months.

The decision to treat a specific property as a rental or as your primary residence should be based on practical considerations. If you ask your family to move to a property that is poorly located, too small for your needs, or too uncomfortable, then you are risking personal dissatisfaction and conflict at home. One advantage of moving to a series of acquired new homes is that you apply the same standards to rentals that you apply to your own home. If you have maintained your current primary residence well, it will be a pleasant place to live; a tenant will be willing to pay a reasonable level of rent based on how well you have cared for the property.

IMPORTANT The suggestion that investors can perpetually finance properties as primary residences and move from one property to another should be viewed cautiously. You should plan to actually move into the new property in order to avoid being accused of misleading your lender. Once you have completed the transaction, the lender will be satisfied, especially if you continue making timely mortgage payments. When you are established in the new property and you convert your previous residence to a rental, the lender on that home will not care whether you live there—as long as you keep the property insured and as long as the payments continue to arrive on time.

GETTING THE BEST DEAL

As a general rule, expect to do more work and meet a higher standard to finance your real estate investment. At the same time, also shop for the best possible deal. Look for a loan with the lowest possible up-front costs. Loan origination fees (points) are charged as an alternative to higher interest rates. A point is equal to 1 percent of the loan.

For example, if you are borrowing $100,000, each point will cost you $1,000. That can add up and makes a comparison between two loans more difficult. If one lender charges 6 percent and no points, and another charges 5 percent and three points, which is cheaper? The only way to make a valid comparison is to calculate the overall interest payments over the terms of the loan, plus points. This is an easy calculation involving three steps:

1. Multiply the monthly payment by the number of months in the loan term.

2. Subtract the amount being borrowed. (The remaining dollar amount is total interest.)

3. Add the points the lender wants to charge you.

The result is overall interest. Once it is calculated, you can determine whether one loan is going to be a better—or worse—deal than another.

When you study the overall interest expense of mortgaging a property, you realize that the cost of investment is not limited to the sales price. You will pay far more in interest over thirty years than the original price of the property. So investigating beforehand and finding the best deal is more important than finding a house that costs a few thousand dollars less. Basing the comparison on overall costs, you can save more money by finding the best interest rate deal than you would in trying to save a few dollars on the purchase price. If you get a “good deal” in your price but pay too much for interest, you will spend more in the long run.

![]()

KEY POINT You must make your mortgage payments whether you have paying tenants or not. You can readily see that vacancies—especially long-term vacancies—could be a big problem. The “cash flow risk” of real estate is significant unless you are able to locate a market in which vacancies are extremely low (less than 5 percent on average). Before deciding to become a real estate investor, research the local market in terms of prices, rental demand, and the current pattern of value appreciation.

INVESTING IN RESIDENTIAL REAL ESTATE

Why is residential property the most popular form of real estate investment? There is more demand for this type of property than for any other as an investment. Of course, the American Dream is home ownership, so the majority of today’s tenants would like to buy a home one day.

SINGLE-FAMILY HOMES

This desire for home ownership helps to strengthen the market value of single-family rental investments. The home you rent out today will be someone else’s primary residence at some point in the future.

The single-family home is also desirable because tenants who can afford the rent can have a yard and garden; it is a better environment for children than apartment living; and if the landlord allows it, they can have a pet.

NOTE If rental demand is relatively low in your area, allowing tenants with a cat or a small dog could push your property to the top of the list—especially if the majority of housing forbids pets.

Real estate has increased consistently in market value over many years, with the notable exception between 2009 and 2011 when property values declined. Since then, prices have come back strongly. The challenge for a real estate investor is to judge both cash flow and the likely bottoming out in market values. National averages show the long-term trends in prices of new homes. Figure 2-1 summarizes the growth rates since 1989.

FIGURE 2-1. AVERAGE SALES PRICES, NEW HOMES.

Source: U.S. Bureau of the Census https:www.census.gov/construction/nrs/pdf/uspriceann.pdf

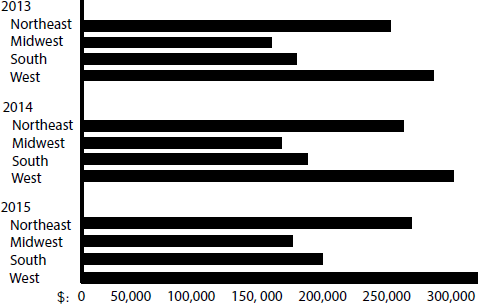

Note that these are averages. There is no guarantee that prices are going to go up everywhere or at the same rate. But if you (a) research the market before you buy, (b) conclude that the market is strong and growing, and (c) select properties carefully, the odds are vastly improved that the investment will be sensible and well timed. Real estate value increases over time even with cyclical declines, and it combines the best features of taxation, risk, and market value. Since all real estate is local (meaning national averages don’t apply everywhere), it is instructive to compare housing trends by region. Figure 2-2 shows the average sales price of existing homes in four major regions. This chart reveals how broadly defined regions are different from one another. Every region’s prices grew over the three years between 2013 and 2015, but average prices were quite dissimilar.

For real estate investors, the implications are clear. As the first illustration revealed, the average decline in housing prices was quite short-term, and prices continued rising soon after the decline from 2008 to 2011, to even higher historical price levels. The second illustration shows that average prices vary considerably, depending on where you live. When the analysis is taken down to the local level (city or county), the differences are likely to be even more noticeable.

FIGURE 2-2 AVERAGE SALES PRICES, EXISTING HOMES

Source: National Association of Realtors: http://www.realtor.org/sites/default/files/reports/embargoes/ehs-7-21/ehs-06-2016-overview-2016-07-21.pdf

At the same time that prices declined and then rose once again, the trend in average market rents presented an interesting contrast to housing costs. See Figure 2-3. Average rents followed the direction of the overall housing markets by declining between 2008 and 2011 but rose strongly from 2011 onward.

The underlying causes for rental increases occurred for reasons different from the reasons for the growth in housing values. Since 2008, a growing number of people who would have been likely home buyers in the past chose to rent, out of concern about the possibility of home prices continuing to decline. This wait-and-see attitude placed increased demand for rentals, as shown in Figure 2-4.

FIGURE 2-3. AVERAGE MONTHLY RENT, U.S., 10 YEARS.

Source: U.S. Bureau of the Census, retrieved from http://www.deptofnumbers.com/rent/us

FIGURE 2-4. HOME OWNERSHIP RATES, 2005–2014.

Source: U.S. Census Bureau, Current Population Survey/Housing Vacancy Survey retrieved at http://www.census.gov/housing/hvs/files/currenthvspress.pdf

This summary reveals a steady decline in the percentage of home ownership. The longer-term trend showed the opposite—home ownership rates growing steadily between 1995 and 2005. If you are considering entering the real estate rental market, these statistics demonstrate that the timing is ideal. The market value of property is rising, and at the same time, market rents are also on the rise even as home ownership rates have been declining for over a decade.

MORTGAGES FOR REAL ESTATE INVESTMENT

Another factor encouraging for real estate investment is the historically low rate of interest. Unlike the double-digit rates of the past, today’s housing interest rate is in the low single digits as of 2016. However, credit has also been tightened.

Today, investors have to be prepared to put down 20 percent or more to ensure that a mortgage will be granted. This also removes the requirement for expensive mortgage insurance and often will result in a lower interest rate.

A significant down payment is virtually a requirement, along with a strong credit history. Loans can be looked for in many places, and large banks often are the worst place to start. A local or regional bank is likely to be more flexible and have less red tape, even though they work in the same system with a majority of loans sold to the secondary market.

If you have poor credit or lack enough cash for a 20 percent or higher down payment, consider seeking owner financing. There is the possibility that a current owner who is motivated enough to find a new buyer may carry some or all of the debt. This is not always easy because most sellers would prefer to cash out. But if you seek finance from a traditional lender, getting the current owner to carry a second mortgage lowers the lender’s risk and makes the overall deal more feasible, even if your credit history is not perfect.

A restriction on mortgages for investors also relates to the number of rentals you are allowed to finance. As a general rule, you cannot have more than four rental properties with mortgages. Most lenders draw the line at that level. Two qualifications may enable you to mortgage a fifth or sixth investment property. First, look for houses costing less than you can afford. Having a cushion helps you to get approval beyond four properties. Second, it means a lot if you have owned your four properties for more than one year, especially if your mortgage payments have all been made on time.

Some investors will be interested in properties other than single-family homes, even though this is by far the most popular choice. However, some alternatives deserve consideration as well.

Mobile Homes. Mobile homes are an alternative form of investment. However, they are not really comparable to permanent housing. Mobile homes, by definition, are personal property and not real property. If you invest in a mobile home, its value is going to decline over the time you own it, just as a car’s value declines. If you buy the land where the mobile home is situated, it is possible that land values will grow. Some investors have discovered this as an alternative to buying more expensive houses. They buy the land and then place a mobile home on it, renting it out. Over a period of years, the payments for both land and mobile home are covered by rent. Ultimately, the investor owns the land free and clear and can either continue renting out the mobile home or sell it and use the land for other purposes—to build a permanent home or sell the land at a profit, for example.

Condominiums. Another way to go is to purchase a condominium unit and rent it out. A condo might seem cheaper at first glance, but it could end up being more expensive than direct ownership. When monthly association fees are added to your mortgage payment, the overall expense adds up to much more than it would be to simply buy a home. Using a loan payment table, find the total payment, and you will see what you could have afforded if you had purchased a single-family home. The total of payments would buy much more house than you could afford paying mortgage plus fees for the condo.

Co-ops. Finally, a cooperative unit might be convertible to a rental. However, co-op owner associations tend to be more restrictive than typical condo or planned-unit associations. The rules of the co-op housing association might prevent you from renting out your unit. So you need to check the sublet policy before buying a co-op.

![]()

KEY POINT Condos and co-ops have historically grown in value, but they have not kept pace with the rate of growth in single-family housing. For most first-time investors, the single-family home is by far the best and safest method for getting into real estate investing for the first time.

MULTIPLE-UNIT HOUSING

A two- or three-unit building is similar to a single-family house because it may also have a yard and other homelike features. At the same time, it shares features with apartments, such as lower rents than single-family housing, shared utility costs, and less privacy. So there are trade-offs among the different types of housing.

From the investment point of view, a duplex or triplex is likely to produce far better cash flow than single-family housing yet still attract tenants who want some of the features associated with a house as opposed to an apartment. Many tenants express a desire to have a garden, for example. (Some never get around to planting anything, but if they have been living in an apartment, they see houses or duplexes as providing them more flexibility.)

For people who cannot afford to buy a house, renting a duplex or triplex is a reasonable compromise. These units are affordable (rents are usually more than for an apartment but less than a house) yet offer many features of home ownership. In a market with varying or weakening demand, duplex or triplex units are likely to have less vacancy than apartments (because of the desirable features they provide) or single-family housing (because of the higher cost of renting the entire house).

TWO ESSENTIAL FACTORS TO CONSIDER

When you begin comparing one type of housing to another, you need to keep two separate investment considerations in mind. First is the long-term market value of the investment itself, and second is the more immediate rental demand and cash flow question.

LONG-TERM PROPERTY VALUES

How will your rental increase in value over time? Based on historical averages, single-family housing tends to increase in value more than multifamily units and other types of rental properties. Single-family houses are likely to be the most profitable long-term investment based on the averages.

If properties are growing in value in your area, buying single-family rentals makes sense. You pay your costs by collecting rents, and you can wait out the market. When values are far higher than they are today, you can sell at a profit. Whereas rents tend to increase over time due to local cost-of-living trends, your mortgage cost is fixed (if you obtain a fixed-rate loan) or the costs are limited (in a variable-rate loan, the rate cap will limit the interest rate increases over time). So as a long-term investment, single-family houses are likely to increase in value more favorably than other properties.

Most of the payments in a mortgage go to interest in the early years. A thirty-year mortgage, for example, is only half paid by the twenty-fourth year; the other half gets paid off more rapidly in the last six years. At first glance, this looks like bad news. How can your investment appreciate if you are paying so little to decrease the mortgage debt?

As a homeowner, the argument does apply. You gain very little in equity from paying down your loan during the first few years you own your home. The average homeowner moves within five years from the time of purchasing a first home, so almost no equity is accumulated through payments. As an investor, you have to keep three points in mind:

1. You claim interest expense as a deduction on your tax return. As an investor, you are allowed to deduct all of your interest as an expense—in addition to property taxes, utilities, depreciation, and other expenses. So payments of interest shelter rental income and produce net losses rather than taxable gains. The deduction of interest is an attractive benefit, effectively reducing your “real cost” of the mortgage. For example, if your combined federal and state effective tax rate is 40 percent, then an $800 monthly interest expense is reduced to $480 after taxes (because you reduce your personal tax liability by $320, or 40 percent of the total interest expense).

2. Mortgage payments are made for you by tenants. Even though you collect rents and then make your own mortgage payment, you can look at the situation a little differently: Rent receipts are used to pay your mortgage payment. In this regard, the fact that most of your payment goes to interest does not really matter because it is paid for you. In practical terms, you are always better off paying less interest, meaning your loan gets paid down more rapidly and your cash flow improves. However, with the offset between interest expense and rental income, the high cost of borrowing money is not as much of an issue as it would be without that income.

3. Appreciation occurs from market price changes. It is a mistake to assume that you accumulate equity only by paying down your mortgage loan. In fact, there is far more appreciation potential in market value growth. In some areas, that growth has been extraordinary, with multiple-year, double-digit growth in market prices of homes. In other areas, prices move more slowly or, in some cases, fall. Well-selected real estate is going to grow in value as long as the local economy is vibrant and jobs are available so that people are moving in instead of moving out. The longer you hold investment property in these circumstances, the greater the market appreciation is likely to be.

VACANCIES IN RENTALS

Growth in market value has been impressive historically. However, the second investment consideration—rental demand—could be far more important in the month-to-month evaluation of your investment properties. You want to acquire properties that will pay for themselves in terms of rental income versus mortgage payments, property taxes, insurance, utilities, and other expenses. If you cannot make cash flow work, you will have an unending cash flow problem. A vacancy for a few months will have a similar negative impact on your personal finances, so cash flow risk is a serious matter for every real estate investor. This is why the question of cash flow (see Chapter 3) should be more important than long-term market value.

Vacancy Rates. Real estate investors are keenly aware that vacancy rates affect their ability to make the investment program work. If you have chronic vacancies, it means that you are asking too much in rent or that the area has more supply than demand. This is a troubling problem because it makes real estate investing far less practical. Unless you can afford to carry the mortgage debt without a full year’s rental income, you could be in big trouble. The more properties you own, the more severe the vacancy problem would become.

![]()

KEY POINT Before beginning your investment plan, investigate vacancy trends. Also look at current and planned new construction. If hundreds of new apartment or modest housing units are going to be built during the next year or two, what does that mean for the prospect of vacancies? The threat has to be taken seriously, especially if vacancies are already high in your city or town.

To investigate trends in vacancy, check with a real estate broker or loan officer at your bank. Both have access to updated information about housing and should know the current vacancy rates. More important, they have statistics on rental and vacancy trends, including average rents, for housing of certain sizes and features, often broken down by neighborhood. The trend is important because you can track how the situation is changing over time.

For example, if vacancy rates have been low but have increased lately, what is the cause? Are more units being built, or are people moving away? How does the vacancy rate compare with the local employment rate? These are critical questions that define whether the timing for starting a real estate investment plan is good or bad. The real estate agent, whether using local Multiple Listing Service (MLS) data or consulting with an in-house rental specialist, should be able to advise you on the significance of the trend.

What if vacancy rates are low or decreasing? At first glance, this would seem to indicate a positive environment for you to begin buying rental housing. However, it is wise to check with your planning department and local economic or community groups and investigate the situation a little further. Are new construction plans going to change the picture? Are new employers coming to town, or are established employers closing up shop and going elsewhere? A sudden, large layoff and resulting unemployment can turn a good historical vacancy trend into a disaster. So while you need to have a grasp on what is occurring in local building, you also need to be informed about employment and population statistics.

Additional help in getting statistics for real estate vacancy trends can be found in a local landlords’ association, if there is one in your community. Also, check with the chamber of commerce and any local tenants’ organizations or rental referral services. (Incidentally, if you register with referral services, you will get many free tenant referrals, as an alternative to paying for an ad in your local paper.) The tenant referral service makes its money by charging people a fee in exchange for a list of local apartments and houses available for rent. These agencies have a very good idea of vacancy levels because they experience both supply and demand and are aware when one side or the other moves.

Cash Flow vs. Investment Value. Cash flow is definitely affected by the vacancy rate. The “market” is not a singular concept. It includes the housing value market, or the prices people pay for homes. It also includes the demand for housing units, which operates on separate assumptions and does not always move in the same direction as housing prices. With this in mind, the compromise of investing in a duplex or triplex could make sense. Even though the long-term market value for these multiunit properties may not be as healthy as that for single-family houses, the cash flow will be far more favorable. You also spread your cash flow risk. For example, if a triplex has one vacancy this month, you continue to collect rent on the remaining two units. Depending on the relationship between rent and cost, this can make a huge difference in your cash flow. A vacancy in a single-family house is always a 100 percent vacancy. In a duplex, a single vacancy takes 50 percent of your monthly rental income, and in a triplex, a single vacancy is only one-third of total income.

The balance between long-term investment value and immediate cash flow requirements has to be considered before you buy a property. While both of these issues are important, they often contradict one another. If you believe you can afford to live with the risk of vacancies in a single-family home, you can create a more profitable long-term investment. But if that risk would be too much for your monthly budget, you are better off compromising by accepting a potentially more modest long-term profit in exchange for more certainty in immediate cash flow.

PART-YEAR RENTALS AND VACATION HOMES

Many people who own two properties rent out their homes while they live in their secondary location. From a record-keeping perspective, this situation presents some potential problems. These issues can be solved with careful and thorough documentation based on a logical division between personal use and rental use. The records need to reflect how you make these divisions, so that you can support what you report on your tax return. Because many expenses that are deductible for investment properties are not deductible for your home, you need to be able to divide those expenses between rental and personal use. Even expenses that are deductible—such as mortgage interest and property taxes—are reported separately. For the time you use a property as a rental, these expenses are reported as part of your investment income or loss. For the time you use the property as your home, the expenses are reported as itemized deductions.

DIVIDING YOUR EXPENSES

The most reliable and accurate way to divide these expenses is on the basis of the number of days a property is used during the year for each purpose. The exact number of days you live in a property would count as residential. The remainder of the year would be assigned to treatment as a rental property.

NOTE Even if the property is vacant for part of the remainder of the year, the applicable expenses (e.g., utilities, insurance, taxes, interest) are deductible as rental expenses—as long as the property is available to rent. The calculation should be based on the actual days you use the property as your residence versus the full year—and the time the property is available as a rental.

VACATION HOMES

Under federal rules, you are allowed to claim itemized deductions for your primary residence as well as for a second home. Besides applying to a home used partly as a residence and partly as a rental, the rule also extends to vacation homes. By definition, a vacation home is a second property that you use for only part of the year. If you do not rent out your vacation home at all, then the property taxes and interest are claimed as itemized deductions. However, if you rent out your vacation home, then you can claim deductions as rental expense for property taxes and interest, as well as for insurance, utilities, and other expenses.

TWO IMPORTANT QUALIFICATIONS First, any property taxes and interest claimed as rental expense have to be deducted from the amount you report as itemized deductions. Second, you can deduct rental expenses only for the portion of the year that your vacation home is available as a rental

MAKING THE HOUSE AVAILABLE FOR RENT

The period in which you are allowed to claim rental expenses is not automatically the whole time you do not use the house yourself. It has to be available as a rental in order for you to properly claim a rental expense. Even if you don’t have a tenant for the entire time, you must be able to show that the property was available. The best way to establish that it was available for rent is by keeping copies of online ads you place to try to find tenants. To document your claim that a rental was available, be sure to list in the ad the exact dates you want to rent out the property. As long as you can establish availability, and as long as you do not use the property during the same period, expenses for a vacation home can be deducted as rental expenses.

If you make the property available for rent only three months of the year and live in it for only three months, what happens to the remaining six months? Because it is available to rent for only three months, you would be allowed to claim a deduction of only one-fourth of total expenses (or actual expenses occurring during the period the property was available for rent). The remaining nine months would be assigned as personal expenses, so you would be allowed to claim three-fourths of property taxes and interest as itemized deductions.

These distinctions are important because you are allowed to deduct additional expenses while the property is available as a rental. Those expenses—which include utilities, insurance, and depreciation—are not deductible as itemized deductions. So, from a tax standpoint, the longer the period of time a second home is available as a rental, the greater the advantage.

THE LOGISTICS OF A PART-TIME RENTAL

Equally important, you should think about some of the logistics involved with the use of property as a part-time rental. Vacation homes often are located far from your primary residence, perhaps hundreds of miles away. As a general observation, the farther you live from your rental property, the more difficult it will be to manage it and to work with tenants. Even a relatively minor repair, for example, is easy to take care of if you live a few blocks from your rental; you may even choose to do the work yourself. But when the same repair has to be done on a house far from where you live, it is more complicated. You have to trust the tenant’s description of the problem. You also have to either hire someone you trust to perform the repair or allow the tenant to find someone. In other words, you have less control over the situation.

The timing of a changeover from rental to personal use is another potential problem area to keep in mind. For example, if you want to rent out the property from September through May but use it yourself for the months from June through August, you must find a tenant willing to agree to that schedule. This means there is a chance you won’t be able to keep the property occupied for all the months you want to rent it out. You might also discover that tenants don’t want to leave even if they have agreed to a month-to-month situation.

![]()

KEY POINT Potential logistics and timing problems don’t make it inadvisable to use properties for dual purposes. They only require more planning and, possibly, greater expense as well. If the alternative is to simply leave a property vacant most of the year, then you lose the rental income, which is not a practical alternative.

RENTING OUT PART OF YOUR HOUSE

If you rent out part of your house, you face different potential problems. Because you and your tenant will be sharing common areas, you will want to be compatible in order for the arrangement to work. A rental that is self-contained, with its own entrance but located on the same lot, simplifies the issue. However, many landlords discover that it is not advantageous to have tenants living so close by because they tend to require higher maintenance, another potential problem to consider. Even so, having a tenant residing in an in-law unit—or, as it is called in some places, an additional dwelling unit (ADU)—can make the difference between your home being affordable or not. Rental income relieves your mortgage burden while providing tax benefits.

![]()

KEY POINT The part-time rental or shared rental arrangement helps many people to afford their mortgage, reduce monthly home maintenance expenses, and ease into rental investments in an affordable and practical way. Planning ahead and thoroughly screening tenants are the keys to creating a positive experience.

REAL ESTATE SPECULATION

Most people who enter the real estate market are seeking the safety and advantages normally associated with this investment: direct control, positive after-tax cash flow, significant tax advantages, and steady appreciation in market value. These features make real estate one of the best investments available and present an excellent way to diversify your portfolio.

However, some people would prefer to speculate in real estate. For those with higher-than-average risk tolerance, there are several ways to become a speculator. One method is to buy rental properties in a market where prices are rising quickly. Some speculators are willing to take on negative cash flow in the belief that market price will outpace the monthly drain of cash. If they are right, they can make a lot of profit in a short period of time. However, if they are wrong, the market will top out and may even decline. In that case, they are stuck with inflated property and negative cash flow. This is a high-risk form of speculation.

![]()

KEY POINT With any form of speculation, the greater the potential for profits, the greater your risks. This is the basic investment equation: Risk and opportunity expand or contract together and are different attributes of the same tendency. Real estate speculation can lead to fantastic profits, but only if you are also willing to take significant risks. Most people are not well suited for the high-risk, high-reward aspects of speculation. The few who are will tell you stories of big profits but may be less likely to tell you about those times when they lost large sums of money.

Speculation is a form of gambling. To make a profit, you know you must beat the odds, so you take a chance and hope that luck is on your side. When combined with a degree of skill and experience, the luck factor can be reduced somewhat, but it cannot be eliminated entirely. Most real estate investors are impressed enough with the benefits of buying single-family housing, taking the tax advantages, and waiting out market appreciation. Those who are attracted to the roller-coaster ride of speculation should be willing to take the whole mix: fast and high profits, as well as fast and potentially high losses.

FIXER-UPPER PROPERTIES

One method of speculation that is usually less risky is buying fixer-upper properties for fast turnaround. This investor looks for run-down houses that need cosmetic care—painting, yard work, and minor repairs. By fixing up the property and then marketing it as soon as possible, a speculator can make a good profit, assuming that market values hold and there is a strong demand for housing.

If you go into the fixer-upper market, you need to become an expert at identifying what types of properties are the best candidates for a healthy profit and what types of repairs will produce the best return. Of course, you also need to be able to perform the work yourself or hire someone who can do the work for you. These three important qualifiers are at the heart of a successful fixer-upper investment and deserve to be discussed in more detail.

Finding the Best Properties. The most likely fixer-upper property is a single-family home that is structurally sound but that has been neglected. To make the investment worthwhile, the ideal candidate should be priced far enough below the typical market value for homes of the same type and located in the same neighborhood. Finding the worst house on a good block, in other words, is the primary guideline for locating a good fixer-upper. To determine whether it is going to be worth your time and effort, there has to be enough spread between the home’s cost and the cost of other houses; otherwise, you won’t be able to make a profit. How much is enough? That is going to depend on (a) the types of repairs that need to be done, (b) the time it is going to take, and (c) how much of the work you are able to do on your own.

It is quite difficult to find an appropriate fixer-upper property in areas that are kept up and in good shape. Because property values tend to be high in such areas, few if any properties are neglected. Another problem is that the difference between fixer-upper values and current market values of well-maintained homes could be too slim to justify the strategy. You are far more likely to find promising fixer-upper candidates in more run-down neighborhoods. In these areas, property values are going to be lower than in nicer neighborhoods, the market for housing is likely to be weaker, and the potential for the dollar amount of profits could be limited as well. However, the rate of return will be greater because the difference in market values will be more significant. So you may be able to trade fixer-upper properties in greater volume and realize a profit in poorer neighborhoods, given the varying market risk factors.

So there’s the dilemma. Better neighborhoods hold higher market value and represent lower-risk investments over time. Poorer neighborhoods offer naturally lower-priced homes but have greater potential for appreciation. Just as higher-priced homes make poorer candidates as rentals (because the mortgage payments may be far higher than market rental levels), the same higher-priced homes are far less likely to work as fixer-uppers.

Identifying the Best Yielding Repairs. The most profitable repairs are those that are strictly cosmetic. A house with overgrown weeds in the yard seems overwhelming, but landscaping is among the fastest and easiest of problems to fix. A house needing to be painted is also a good candidate, especially if you are willing to do the painting yourself. Properties requiring inside paint jobs and minor repairs are also good. Once you move beyond the range of cosmetic fixes, the question of affordability becomes more important. If you need to replace major plumbing and electrical systems, the roof, or other expensive features of the house, you are going to have difficulty making the fixer-upper plan work. The cost of hiring a plumber or an electrician is so high that your return would be too marginal to make the move a practical one. You are going to make the most profit working with fixer-upper properties if you have the skills and the time to do the work yourself.

Performing the Work Yourself. The more types of repairs and improvements you are able to perform, the more practical the fixer-upper market becomes as an alternative. Simple repairs (e.g., yard work, painting inside and outside) cost little and are easy to do. If you have carpentry and other skills, then you can take on more complicated repairs. If you are skilled at kitchen cabinetry, roofing, electrical work, or plumbing, the fixer-upper market available to you is far broader than for most people. But if you are going to need to hire experts to put the house back in working order, that will cut into your profit margin and may even offset your potential profits completely. By specializing in fixer-upper properties needing the types of work you can perform on your own, you will be able to earn far higher profits than an unskilled investor.

OTHER FACTORS TO KEEP IN MIND

![]() What about closing costs? An important consideration for fixer-upper investors is that of closing costs. You have to pay some costs when you buy and even more when you sell. In evaluating whether the idea makes sense, you must factor in the time involved and the estimated closing costs to ensure that you have a good chance of making a profit. Merely breaking even isn’t acceptable, considering all the work you have to do. Why place yourself at risk if you don’t have the likely outcome of a decent profit?

What about closing costs? An important consideration for fixer-upper investors is that of closing costs. You have to pay some costs when you buy and even more when you sell. In evaluating whether the idea makes sense, you must factor in the time involved and the estimated closing costs to ensure that you have a good chance of making a profit. Merely breaking even isn’t acceptable, considering all the work you have to do. Why place yourself at risk if you don’t have the likely outcome of a decent profit?

![]() Should you live in the fixer-upper? Some people like to move into the fixer-upper while they are working on it. The advantage to this approach is that you can continue paying on the mortgage while living in the property. Then, if it takes longer than you expect to resell the property, it is simply your primary residence and the pressure is off to sell quickly. The major disadvantage to living in the fixer-upper is the stress it may cause for your family. Moving frequently and living in homes that are continually being repaired and fixed can cause significant tension and adversely affect your personal quality of life. To succeed as a fixer-upper investor, you should also consider how your decision will affect your family. If you and your spouse are fairly young and don’t have children, and you both want to work on fixer-uppers, it is the best possible situation. But if you have small children and your spouse does not want to move from house to house—and won’t participate in the project—the whole venture will soon deteriorate into an ongoing argument over dust, noise, and disruption. No amount of profit can justify the stress that will result.

Should you live in the fixer-upper? Some people like to move into the fixer-upper while they are working on it. The advantage to this approach is that you can continue paying on the mortgage while living in the property. Then, if it takes longer than you expect to resell the property, it is simply your primary residence and the pressure is off to sell quickly. The major disadvantage to living in the fixer-upper is the stress it may cause for your family. Moving frequently and living in homes that are continually being repaired and fixed can cause significant tension and adversely affect your personal quality of life. To succeed as a fixer-upper investor, you should also consider how your decision will affect your family. If you and your spouse are fairly young and don’t have children, and you both want to work on fixer-uppers, it is the best possible situation. But if you have small children and your spouse does not want to move from house to house—and won’t participate in the project—the whole venture will soon deteriorate into an ongoing argument over dust, noise, and disruption. No amount of profit can justify the stress that will result.

![]() How long should you keep it? The fixer-upper investor also has to decide how long to keep a property, especially if it will be used as a primary residence. If you live in your home for two years or more, any profit you earn upon sale is tax free up to $500,000 for a married couple. You can execute as many tax-free sales as you want as long as you meet the two-year requirement. There also is no age restriction on the two-year rule. Homeowners of any age can take advantage of this tax rule. For the fixer-upper investor, though, there is a dilemma. Without the two-year rule, the goal would be to resell properties as quickly as possible, take the profit, and reinvest elsewhere. But if the profit is substantial, it could also make sense to use each property as a primary residence and wait out the two-year period so that the profit will be completely tax free. (Rules will vary by state, so even if you escape federal taxes, you could still be liable for state capital gains tax from selling your primary residence.)

How long should you keep it? The fixer-upper investor also has to decide how long to keep a property, especially if it will be used as a primary residence. If you live in your home for two years or more, any profit you earn upon sale is tax free up to $500,000 for a married couple. You can execute as many tax-free sales as you want as long as you meet the two-year requirement. There also is no age restriction on the two-year rule. Homeowners of any age can take advantage of this tax rule. For the fixer-upper investor, though, there is a dilemma. Without the two-year rule, the goal would be to resell properties as quickly as possible, take the profit, and reinvest elsewhere. But if the profit is substantial, it could also make sense to use each property as a primary residence and wait out the two-year period so that the profit will be completely tax free. (Rules will vary by state, so even if you escape federal taxes, you could still be liable for state capital gains tax from selling your primary residence.)

![]()

KEY POINT The potential conflict between tax breaks and quality of living needs to be resolved. If you make decisions based only on tax questions, your investments will become counterproductive. If you determine that quality of life is a priority and, as a result, you do not invest in real estate at all, then you lose potential profits and tax benefits. So there needs to be a balance between the two sides.

The attractive features of rental real estate include a wide variety of choices. Whichever way you decide to go—commercial property or residential, single-family house or multiunit buildings, part-year rentals or fixer-uppers—you must keep thorough records of your transactions. Record keeping is vital not only to track cash flow and profit or loss but also to document the expenses you claim as part of your tax return. Subsequent chapters will provide you with a wealth of practical guidance to help you understand the various financial aspects of investing in and managing rental real estate.