3.

CASH FLOW: THE ESSENCE OF RENTAL REAL ESTATE

For a landlord, the need for positive cash flow—to have more money coming in than going out—is in many ways more important than month-to-month profit. As a rule, real estate investors do not mind a paper loss for tax purposes. In fact, the perfect situation is one in which you achieve positive cash flow and report a net tax loss. Is this possible? Yes, and in fact, it is the most likely scenario if you plan properly.

Ideally, positive cash flow should be generated from the properties themselves. This means that you do not need to invest more and more cash each year just to maintain your real estate investment. In some markets, achieving positive cash flow requires higher down payments than you would like; in some other markets—where property values are too high but market rents are too low—positive cash flow is simply not possible. In those situations, it doesn’t make sense to embark on a real estate investment plan. Only those who have owned property for many years can afford to rent out property because they bought the property before prices rose, because monthly mortgage payments are small, and because, in all likelihood, market rents are high enough to pay the mortgage.

The interaction between rental income and mortgage payments is the starting point in an analysis of cash flow. Your first goal should be to generate rent adequate to pay your monthly principal and interest, property taxes, insurance, and utilities. Even if you achieve this offset, it does not allow for unexpected repairs or vacancies, which are the unpleasant realities of real estate investing. When you calculate the tax benefit of investing in real estate, however, it is possible that your tax savings may be enough to cover maintenance and repairs.

ANALYZING CASH FLOW BEFORE INVESTING

How important is it to analyze the cash flow situation for your rental properties? It is the critical first step in the process—the very analysis that determines whether you should even proceed. If you invest in a property that does not produce enough income to cover your known expenses, you may create a financial hardship for yourself. At that point, you have two concerns. First, how can you afford to continue carrying the property indefinitely with negative cash flow? And, second, is the property value increasing beyond the monthly outflow of money? If it is not, then by design, you have created a losing situation.

DEFINING INVESTMENT VALUE

Investment value has to be defined for real estate in ways much different from other investments. With stocks, investment value may refer to long-term growth prospects, meaning today’s price per share is a good value and is likely to grow in the future. You can buy stock, collect dividends, and wait; there is no requirement to put more money into the investment each month. In real estate, investment value has to be defined in terms of (a) supply and demand and (b) cash flow. Supply and demand may be applied either to property values and their growth rates or to the separate demand for rental properties. Both tend to move in similar cycles, but not necessarily. You may find situations in which prices are rising but rental unit demand is relatively low, or vice versa.

The second way to define investment value is to evaluate cash flow. If your mortgage payment is significantly higher than what you can expect to collect in rents, you have to determine whether you can afford the extra payment each month. It makes sense to accept a negative cash flow situation only if and when you are convinced that property values are growing so quickly that they outpace the monthly negative cash flow.

COMPARING RENTS TO HOUSING PRICES

When you analyze the typical level of rent paid for housing in your area and compare that dollar amount to the typical price of housing, you can tell whether it makes sense to buy real estate, keeping the need for cash flow in mind.

EXAMPLE 1: In your city, the typical small home (two bedrooms, one bath, 1,400 square feet) can be purchased for $85,000. An 80 percent mortgage ($68,000) will cost you $325 per month, assuming a thirty-year loan at 4 percent. If rents for such homes run about $350 per month, then the rental income will cover your mortgage payment. (For the sake of simplicity, this example does not include an allowance for insurance, property taxes, utilities, and repairs.)

![]()

![]()

EXAMPLE 2: If the same house costs $150,000 in your city, your 80 percent mortgage of $120,000 would cost about $573 per month. If average rents run at $450 for such homes, it would not be practical to invest under these terms. You would begin with a negative cash flow of $123 per month, even before calculating taxes, insurance, and other expenses.

![]()

These two examples demonstrate that cash flow is a fairly straightforward test: If property values are so high that a mortgage payment will exceed the level of rents you can reasonably expect to earn, it will not be practical to buy rental property.

KEEPING CASH FLOW IN MIND

While rental levels tend to track property values, this is not always the case. In some situations, rental demand can be quite high while property values remain relatively low; in other cases, property values may outpace what you could expect to bring in through rents. For example, in a suburban town in the Midwest, where a large portion of the population consists of college students, rents may be relatively high due to demand, but property values relatively low—the ideal situation for rental investing with cash flow in mind. However, in areas such as New York City, San Francisco, or Los Angeles, property values are quite high, and although rents are high as well, cash flow simply won’t work out. If the typical starter home costs $300,000 (so that you would have to find a mortgage of $240,000 at the 80 percent level), mortgage payments would be $1,678 per month (based on a thirty-year term at 7.5 percent). If you could expect to get only $1,000 per month, then clearly it would not make sense to consider investing.

One way to overcome this problem is to make a larger down payment, thereby lowering your monthly payments. However, many would-be real estate investors cannot afford to make down payments of 30 percent, 40 percent, or more. While that would go a long way toward easing the cash flow problem, it is simply not a viable solution for most people.

![]()

KEY POINT The very first step in determining whether to consider real estate investing is to go through this preliminary analysis. What is the cost of the property? What level of rental demand exists? And finally, do the numbers work out?

CALCULATING RENTAL PROPERTY CASH FLOW

The next step involves making comparisons between the current market value of likely rental properties and the rent you are likely to receive—based on your analysis of the market. You want to be able to estimate the most likely cash flow experience you will have in real estate. This process includes calculating monthly rental income, property taxes, insurance, utilities, and other expenses; the mortgage payment; an amount to have in reserve for repairs or vacancies; and the tax benefit you will gain from investing in rental property.

BREAKING DOWN MONTHLY PAYMENTS

To estimate cash flow, you must divide monthly payments into several categories. These are:

![]() Deductible Expenses That You Pay. Examples are payments for interest on your mortgage loan; property taxes, insurance, and utilities; applicable other expenses, such as accounting or legal fees, office supplies, or car and truck expenses; and the cost of supplies you need for small repairs.

Deductible Expenses That You Pay. Examples are payments for interest on your mortgage loan; property taxes, insurance, and utilities; applicable other expenses, such as accounting or legal fees, office supplies, or car and truck expenses; and the cost of supplies you need for small repairs.

WHERE TO LOOK Free instructional manuals can be ordered on the Internal Revenue Service’s (IRS’s) Web site at https://www.irs.gov. Request Publication 527, “Residential Rental Property,” for more information about deductible expenses.

![]() Deductible Noncash Expenses. You can deduct depreciation on the value of the property but not the land; on the car or truck you use to conduct your real estate business; and on computer, landscaping, or other equipment required to do business. While you do not make actual payments for depreciation, you calculate the amount you are allowed to deduct and claim it as an expense (see Chapter 8). You also amortize points paid at closing if you are required to claim that expense over several years (see Chapter 11).

Deductible Noncash Expenses. You can deduct depreciation on the value of the property but not the land; on the car or truck you use to conduct your real estate business; and on computer, landscaping, or other equipment required to do business. While you do not make actual payments for depreciation, you calculate the amount you are allowed to deduct and claim it as an expense (see Chapter 8). You also amortize points paid at closing if you are required to claim that expense over several years (see Chapter 11).

![]() Payments That Are Not Deductible. You make monthly payments on your mortgage, and, while the interest portion of the payment is deductible, the portion that goes to principal cannot be deducted. You may also pay for equipment that you have to depreciate over many years; such payments are not deductible in the year you spend the money. For example, if you purchase a $600 lawn mower, you can depreciate it, but you cannot deduct the payment the year it is made.

Payments That Are Not Deductible. You make monthly payments on your mortgage, and, while the interest portion of the payment is deductible, the portion that goes to principal cannot be deducted. You may also pay for equipment that you have to depreciate over many years; such payments are not deductible in the year you spend the money. For example, if you purchase a $600 lawn mower, you can depreciate it, but you cannot deduct the payment the year it is made.

PLUGGING IN ACTUAL FIGURES

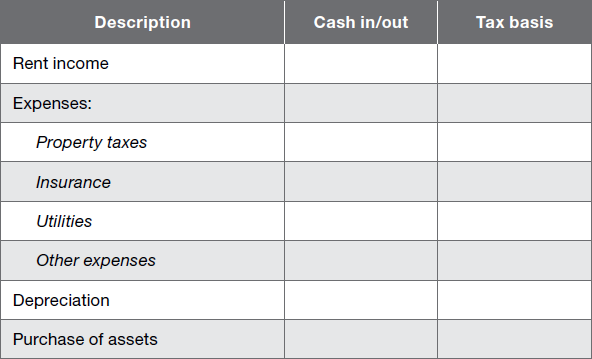

Each of these types of transactions has to be treated differently to calculate cash flow—not only because it involves a mix of cash and noncash but also because you want to calculate your tax benefits as well. For real estate investing, the tax benefits are part of the overall equation, so you need a worksheet to accurately determine the outcome. A cash flow calculation worksheet is shown in Table 3-1.

TABLE 3-1: WORKSHEET FOR CASH FLOW CALCULATION ($)

To fill in this worksheet, begin with a few assumptions:

![]() Rent of $700 per month is realistic.

Rent of $700 per month is realistic.

![]() Property taxes average $45 per month.

Property taxes average $45 per month.

![]() Insurance averages $13 per month.

Insurance averages $13 per month.

![]() Utilities that you, as landlord, will pay average $12 per month. (This figure may seem low, but remember that tenants usually pay most of the utilities, including gas and electric, water, and cable TV. As a landlord, you will probably pay very little, if any, utility bills.)

Utilities that you, as landlord, will pay average $12 per month. (This figure may seem low, but remember that tenants usually pay most of the utilities, including gas and electric, water, and cable TV. As a landlord, you will probably pay very little, if any, utility bills.)

![]() You estimate “other” expenses at $30 per month.

You estimate “other” expenses at $30 per month.

![]() Your property can be purchased for $120,000. Of this, $30,000 is the estimated value of land and $90,000 is for improvements; you are allowed to deduct $273 per month for depreciation.

Your property can be purchased for $120,000. Of this, $30,000 is the estimated value of land and $90,000 is for improvements; you are allowed to deduct $273 per month for depreciation.

![]() You do not plan to buy any equipment during the first year, so the estimated additional asset cost is zero.

You do not plan to buy any equipment during the first year, so the estimated additional asset cost is zero.

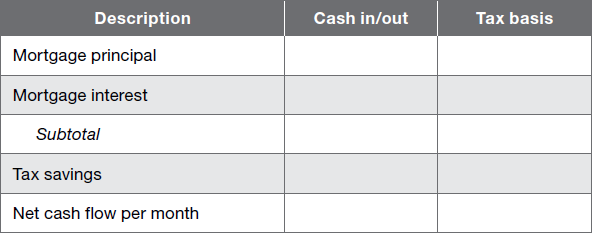

![]() Your mortgage payment is based on 80 percent financing ($96,000) and a 4 percent rate. Payments will be $458 per month (assuming a thirty-year amortization).

Your mortgage payment is based on 80 percent financing ($96,000) and a 4 percent rate. Payments will be $458 per month (assuming a thirty-year amortization).

![]() Your tax rate (federal and state combined) is 40 percent, based on a 33 percent federal and 7 percent state tax. (Of course, this figure will vary by state, as well as by your taxable income each year.)

Your tax rate (federal and state combined) is 40 percent, based on a 33 percent federal and 7 percent state tax. (Of course, this figure will vary by state, as well as by your taxable income each year.)

With all of these assumptions, you can complete the worksheet using monthly averages. An example follows in Table 3-2.

TABLE 3-2: FILLED-IN WORKSHEET FOR CASH FLOW CALCULATION ($)

In this example, the after-tax cash flow is negative. This occurs because the net for tax purposes of $7 per month translates to a $3 per month increase in your overall tax liability (at the 40 percent tax rate). So, in the example, you report a small net profit but have positive cash flow of $142 per month. This improves over time as the mortgage interest declines. This cash flow sets up a buffer for unexpected expenses.

In cases of marginal or negative cash flow, there is no cushion for unexpected expenses or vacancies. That represents a worst case scenario in which you would not be able to affordany unexpected surprises. In assessing the risk, you should want to perform a preliminary cash flow analysis before buying property. Solutions include looking at lower-priced homes, putting more money down, or waiting until the market becomes more favorable on a cash flow basis.

Depreciation is listed as part of the tax calculation but not cash in/out because this is a calculated expense and not a cash outlay. Principal on the mortgage is a cash outlay but not deductible for tax purposes; thus, it is listed in the first column but not in the second.

RISK FACTORS If you believe that rental demand is quite strong and that you are not likely to suffer vacancies in your rental property, the overall assumption shown in this exercise is reasonable. However, as a landlord, you have to live with the risks of possible vacancies, unexpected repairs, and tenants who fail to pay rent every month. The higher your down payment (and the lower your mortgage payments), the better your cash flow, which also translates to lower risks.

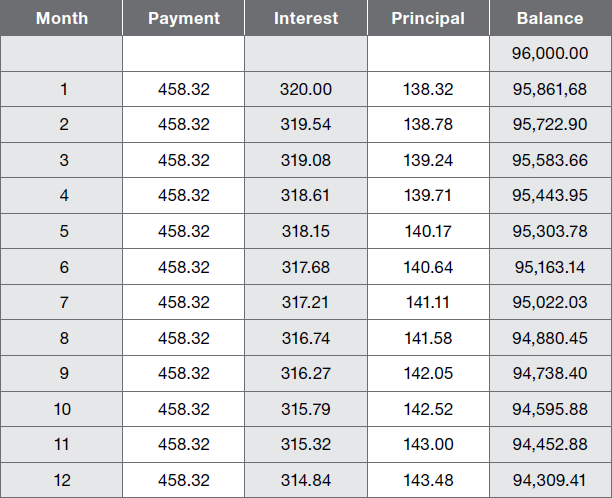

DETERMINING INTEREST AND PRINCIPAL

In the previous example, average interest and principal payments were applied on a typical monthly basis. How do you know what your interest and principal will be? Some lenders break down the monthly payment for you, which gives you the current month’s division. Other lenders provide no details, except an annual summary of interest for tax-reporting purposes. You may need to calculate monthly interest and principal payments on your own to be able to estimate cash flow. The calculation is not difficult.

Step 1. Multiply the beginning balance by the interest rate. In the example in the previous section, the original loan balance was $96,000, and the interest rate was 4 percent. We further assumed a thirty-year amortization rate, so that monthly payments would be $458.32. (Amortization tables showing monthly payments can be found in interest rate books or online, by searching for “mortgage amortization tables.”) In our example, the first year’s calculation would be:

$96,000.00 × 0.04 = $3,840.00

Step 2. Divide the annual interest by twelve (months) to calculate the current month’s interest expense:

$3,840.00 ÷ 12 = $320.00

Step 3. Subtract the current month’s interest expense from the total payment to calculate the current month’s principal payment:

$458.32 − $320.00 = $138.32

Step 4. Subtract the principal payment from the loan balance to calculate the new loan balance:

$96,000.00 − $138.32 = $95,861.68

These calculations can be carried forward twelve times to determine the full year’s total payments, interest, principal, and ending balance. This calculation is shown in Table 3-3.

TABLE 3-3: MORTGAGE AMORTIZATION TABLE ($)

Although amortization tables are available online, you might want to set up your own calculator on an Excel worksheet. Table 3.4 contains the values that have to be entered to create one.

Table 3-5 shows the outcome of these Excel calculations.

TABLE 3-5: EXCEL WORKSHEET RESULTS

THE DIFFERENCE BETWEEN CASH FLOW AND PROFIT

Any business—whether real estate owned for profit or a retail shop—demands planning and carefully detailed management. At first glance, it would seem that cash flow and profits are the same thing: Cash comes in and cash goes out. But in practice, the two are vastly different. In real estate, as the previous section demonstrated, just determining an estimated tax benefit requires considerable calculation. So it is commonly the case that cash flow and tax-based net profit are quite different. The principal paid on your mortgage and money paid for capital improvements decrease cash flow because money is paid out without being deductible. Depreciation expense, on the other hand, is possibly your largest annual deduction after interest, but it does not involve payments in cash.

COMPARING DIFFERENT PROPERTIES

Since cash flow and net profits (or losses) are different, why even make the comparison? Because as a method for measuring the cash flow and tax benefits, a property-to-property test reveals the benefit of holding onto a specific investment for the long term.

![]()

EXAMPLE: You own two properties. Property A produces positive cash flow of $588 per year and also provides you with a tax loss of $3,600. The combination of the two is $4,188 per year. Property B provides an annual net loss of $1,020 (an $85 loss per month) but produces annual tax losses of $4,410.

![]()

That adds up to $3,390 (after deducting the negative cash flow from the tax loss). Compare the two properties in Table 3-6.

TABLE 3-6. PROPERTY COMPARISONS ($)

Clearly, property A is more advantageous because it provides positive cash flow. In comparison, property B suffers a negative cash flow each year. You may justify holding onto the second investment if property values are increasing at a rate greater than the negative cash flow, assuming that you can afford to carry the excess each month. It makes no sense, though, to keep a property whose market value is being outpaced by negative cash flow. The tax benefits are not worth the loss. (Remember, monthly cash flow has already included a calculation of the tax benefit.)

BEST OF BOTH WORLDS

If you are able to limit your investments to only those properties that produce both positive cash flow and tax-based losses, you get the best of both worlds. The level of comparison between profit (or loss) and cash flow and tax loss is a goal worth striving for, and one that can be achieved in the right markets.

IMPORTANT There are limitations to annual losses you can claim under the law. The maximum net loss you are allowed to claim each year is $25,000, and that goes down if your taxable income exceeds $100,000 (see Chapter 9).

The point worth making in regard to cash flow is that monthly net losses can add up to a substantial reduction of your tax liability. The calculations also demonstrate that the difference between cash flow and profits can be large, so you need to keep these differences in mind when planning ahead.

SHOULD YOU INVEST IN MORE THAN ONE RENTAL PROPERTY?

This question ultimately comes up. Does it make sense to invest in four or five properties—or even more? If you can finance an infinite number of properties, and mortgage payments are covered by rents, why not? Many promotions offering to show you how to get rich in real estate depend on the highly leveraged approach, but in practice it does not always work out. In planning cash flow, be aware of the potential effects of:

![]() Vacancies. If your area has a very low vacancy rate, you probably do not need to be concerned with chronic vacancy problems. (If you do experience high vacancies, the cause may be the condition of the property.) In markets with higher vacancy rates or seasonal changes in demand for rental housing, you need to plan ahead carefully. In projecting your cash flow through the year, you must determine whether it is feasible to work with more than one property, given the possibility of the vacancy factor. You may be able to get through a month or two with one property vacant, but what about five? Can you afford to continue making mortgage payments with no rental income?

Vacancies. If your area has a very low vacancy rate, you probably do not need to be concerned with chronic vacancy problems. (If you do experience high vacancies, the cause may be the condition of the property.) In markets with higher vacancy rates or seasonal changes in demand for rental housing, you need to plan ahead carefully. In projecting your cash flow through the year, you must determine whether it is feasible to work with more than one property, given the possibility of the vacancy factor. You may be able to get through a month or two with one property vacant, but what about five? Can you afford to continue making mortgage payments with no rental income?

![]() Tenant Problems. Even when your properties are occupied throughout the year, another risk is that your tenants will fall behind in the rent. In the worst situation, a tenant simply does not pay rent at all, and you have to begin eviction proceedings. That can be expensive and stressful and takes time as well. Depending on the rules in your state, you would have to expect to lose between one and three months’ rent to complete an eviction. If you select tenants with great care, you can minimize this problem, but it is a very real possibility, and the more properties you own, the higher your exposure.

Tenant Problems. Even when your properties are occupied throughout the year, another risk is that your tenants will fall behind in the rent. In the worst situation, a tenant simply does not pay rent at all, and you have to begin eviction proceedings. That can be expensive and stressful and takes time as well. Depending on the rules in your state, you would have to expect to lose between one and three months’ rent to complete an eviction. If you select tenants with great care, you can minimize this problem, but it is a very real possibility, and the more properties you own, the higher your exposure.

![]() Unexpected Repairs. There is never a good time to discover that you need to spend money to repair a heating system, a roof, or burst water pipes. Even with the best maintained property, unexpected repairs are going to arise and cost you money. With a single rental, you may have the financial reserves to get through the experience. With multiple properties, the potential strain on your personal budget could escalate.

Unexpected Repairs. There is never a good time to discover that you need to spend money to repair a heating system, a roof, or burst water pipes. Even with the best maintained property, unexpected repairs are going to arise and cost you money. With a single rental, you may have the financial reserves to get through the experience. With multiple properties, the potential strain on your personal budget could escalate.

![]() Tax Loss Limitations. As discussed previously, you are allowed to deduct up to $25,000 in losses on real estate investments each year, and other limitations may apply as well, depending on your overall income. So from the tax point of view, there is no advantage to owning so many properties that your losses exceed the $25,000 annual level. Because tax benefits often make the difference between positive and negative cash flow, your advance planning should also take into account the tax aspects of owning several properties.

Tax Loss Limitations. As discussed previously, you are allowed to deduct up to $25,000 in losses on real estate investments each year, and other limitations may apply as well, depending on your overall income. So from the tax point of view, there is no advantage to owning so many properties that your losses exceed the $25,000 annual level. Because tax benefits often make the difference between positive and negative cash flow, your advance planning should also take into account the tax aspects of owning several properties.

![]() Lending Restrictions. The secondary market for real estate financing imposes rules and limits on how many rentals you can finance through conventional lenders, based on your income, credit, and down payment requirements. Other restrictions include the level of debt you are allowed to finance. While homeowners are allowed to mortgage up to 90 percent of a home’s value, real estate investors may be limited to 80 percent or even 70 percent, depending on the program. So if you purchase a $100,000 rental property, you are likely to need to make a $20,000 or $30,000 down payment. Of course, the more properties you own, the more cash you need to make these payments.

Lending Restrictions. The secondary market for real estate financing imposes rules and limits on how many rentals you can finance through conventional lenders, based on your income, credit, and down payment requirements. Other restrictions include the level of debt you are allowed to finance. While homeowners are allowed to mortgage up to 90 percent of a home’s value, real estate investors may be limited to 80 percent or even 70 percent, depending on the program. So if you purchase a $100,000 rental property, you are likely to need to make a $20,000 or $30,000 down payment. Of course, the more properties you own, the more cash you need to make these payments.

![]() Time and Effort. Finally, as a practical matter, you need to determine how much time you want to spend managing real estate. When you own stocks or mutual fund shares, you do not have to spend much time at all to manage your holdings. With real estate, you must put in time for a variety of demands, and the more properties you own, the more time you will need to devote.

Time and Effort. Finally, as a practical matter, you need to determine how much time you want to spend managing real estate. When you own stocks or mutual fund shares, you do not have to spend much time at all to manage your holdings. With real estate, you must put in time for a variety of demands, and the more properties you own, the more time you will need to devote.

![]()

KEY POINT With these inhibiting factors in mind, you need to be aware of not only the financial and practical limitations but also the level of risk involved with purchasing rental properties. If you wish to own multiple houses, the cash flow risk increases proportionately. While a single rental contains an element of cash flow risk, it increases with each additional property that you buy. This doesn’t mean you should avoid investing in more than one property, just that you should carefully evaluate each situation and plan ahead for potential problems.

CONTINGENCY PLANNING FOR CASH FLOW

While these example showed that it is possible to experience positive cash flow and a net tax loss at the same time, real-life situations do not always work out that way. Other factors concerning cash flow require contingency planning on your part. Due to the nature of unexpected expenses and costs, vacancies, or tenant problems, it is impossible to build in absolute certainty in your real estate investment program. You can mitigate your risks by doing careful and thorough tenant screening, picking the best locations for your rental properties, diligently monitoring your property, investing only when the economic conditions indicate a strong demand, and limiting your exposure by not overbuying in the market.

Even in the best markets and after the most diligent research on your part, there are going to be unknown and unexpected surprises. How do you plan for these? Here are some general guidelines:

![]() Make sure you have an adequate cash reserve. You need to limit your risk exposure by matching up property investments with cash reserves. If your family income is adequate to cover what you consider a realistic level of risk on two properties, then buying three or four properties may be taking excessive risk. You may justify exceeding that level by reasoning that it is unlikely you will face vacancies or unexpected repairs on all of your properties at the same time. That is a reasonable evaluation, as long as you enter the situation with an awareness of the cash flow risks. Your cash flow reserves are literally the amount of money you can afford out of your personal budget to cover unexpected losses, whether they are repairs, vacancies, or other problems.

Make sure you have an adequate cash reserve. You need to limit your risk exposure by matching up property investments with cash reserves. If your family income is adequate to cover what you consider a realistic level of risk on two properties, then buying three or four properties may be taking excessive risk. You may justify exceeding that level by reasoning that it is unlikely you will face vacancies or unexpected repairs on all of your properties at the same time. That is a reasonable evaluation, as long as you enter the situation with an awareness of the cash flow risks. Your cash flow reserves are literally the amount of money you can afford out of your personal budget to cover unexpected losses, whether they are repairs, vacancies, or other problems.

![]() Take your time in acquiring properties. Do thorough research, and don’t allow anyone to pressure you into making a fast decision. Good bargains are plentiful in most markets, and if you lose out on one today, another one will show up tomorrow. Take the time you need to research the prices of properties, vacancy rates, and rental demand trends; to find the best neighborhoods; and to analyze likely after-tax cash flow—all before you commit yourself.

Take your time in acquiring properties. Do thorough research, and don’t allow anyone to pressure you into making a fast decision. Good bargains are plentiful in most markets, and if you lose out on one today, another one will show up tomorrow. Take the time you need to research the prices of properties, vacancy rates, and rental demand trends; to find the best neighborhoods; and to analyze likely after-tax cash flow—all before you commit yourself.

![]() Require inspection of a property as a condition for closing. The worst outcome for any real estate investor is to discover that they have unwittingly bought a “money pit”—a property that demands never-ending maintenance. Never trade your right to require inspections in exchange for other concessions. As a contingency, require that the seller agree to an independent inspection, and reserve the right to cancel the whole deal if that inspection uncovers hidden flaws in the property. You may wish to pay the $200 to $300 fee for the inspection, just to make sure that you get a qualified and independent report. If you ask the seller to pay for the inspection, you lose the right to ensure the independence of the inspector.

Require inspection of a property as a condition for closing. The worst outcome for any real estate investor is to discover that they have unwittingly bought a “money pit”—a property that demands never-ending maintenance. Never trade your right to require inspections in exchange for other concessions. As a contingency, require that the seller agree to an independent inspection, and reserve the right to cancel the whole deal if that inspection uncovers hidden flaws in the property. You may wish to pay the $200 to $300 fee for the inspection, just to make sure that you get a qualified and independent report. If you ask the seller to pay for the inspection, you lose the right to ensure the independence of the inspector.

![]() Avoid buying properties that don’t qualify for conventional financing. Some first-time investors have gotten around the need to qualify for financing by working mainly with sellers who agree to carry a loan for them. As attractive as this might seem, you should ask why they are willing to finance your purchase. Chances are that the house’s condition prevents it from qualifying for conventional financing. If that’s the case, you need to know what those conditions are before you buy. If you simply proceed without finding out why the seller is willing to carry a loan, you could be buying someone else’s problems. The day will come when you wish to sell; if the house has a serious deficiency, you won’t be able to move it to a new buyer, who will probably also need financing. Proceed cautiously when a seller offers to carry a loan for you; it could be a red flag.

Avoid buying properties that don’t qualify for conventional financing. Some first-time investors have gotten around the need to qualify for financing by working mainly with sellers who agree to carry a loan for them. As attractive as this might seem, you should ask why they are willing to finance your purchase. Chances are that the house’s condition prevents it from qualifying for conventional financing. If that’s the case, you need to know what those conditions are before you buy. If you simply proceed without finding out why the seller is willing to carry a loan, you could be buying someone else’s problems. The day will come when you wish to sell; if the house has a serious deficiency, you won’t be able to move it to a new buyer, who will probably also need financing. Proceed cautiously when a seller offers to carry a loan for you; it could be a red flag.

![]() Perform preventive maintenance regularly. Plan to perform specific tasks as part of your annual cycle. If you own property in northern climates, wrap water pipes and replace heater filters at the beginning of winter; clean out gutters in the fall; maintain septic systems and wells in the spring; and have other expensive systems checked by an expert once a year. The money you spend making sure everything is in working order may prevent more expensive surprises later.

Perform preventive maintenance regularly. Plan to perform specific tasks as part of your annual cycle. If you own property in northern climates, wrap water pipes and replace heater filters at the beginning of winter; clean out gutters in the fall; maintain septic systems and wells in the spring; and have other expensive systems checked by an expert once a year. The money you spend making sure everything is in working order may prevent more expensive surprises later.

![]() If maintenance is a chronic problem, sell the property. Don’t make the mistake of keeping property that is costing more than it’s worth. Problem houses don’t get better; they tend to continue causing you problems. If you are continually facing unexpected expenses and losing money, cut your losses as soon as possible. Put the property on the market and escape the continuing burden.

If maintenance is a chronic problem, sell the property. Don’t make the mistake of keeping property that is costing more than it’s worth. Problem houses don’t get better; they tend to continue causing you problems. If you are continually facing unexpected expenses and losing money, cut your losses as soon as possible. Put the property on the market and escape the continuing burden.

![]() Cut losses when necessary. If you overbuy and realize that you are losing money or simply cannot afford to cover the cash flow problems you face, even if temporary, then the smart move is to sell some of your properties. If you own two or three properties and you come to the conclusion that you can only manage one, get rid of the excess. Keep the property that produces the best cash flow and presents the fewest problems. Don’t make the mistake of selling your best performing assets and keeping the problems. A cash flow difficulty is caused by the very properties you need to sell. Cutting losses is the smart move when you are overextended.

Cut losses when necessary. If you overbuy and realize that you are losing money or simply cannot afford to cover the cash flow problems you face, even if temporary, then the smart move is to sell some of your properties. If you own two or three properties and you come to the conclusion that you can only manage one, get rid of the excess. Keep the property that produces the best cash flow and presents the fewest problems. Don’t make the mistake of selling your best performing assets and keeping the problems. A cash flow difficulty is caused by the very properties you need to sell. Cutting losses is the smart move when you are overextended.

![]() Monitor the market, and be prepared to alter your strategy. Nothing remains the same forever. Just as stockholders need to watch for changing fundamentals of companies whose stock they buy, real estate investors have to do the same. Today’s strong demand market can soften next year. Your city may currently have a very low vacancy rate, but any number of factors could change the situation—for example, construction of a large apartment complex, closure of a major employer’s facility, seasonal factors, or a poor local economy. In areas near the Canadian border, changes in international exchange rates may affect the local retail market and, as a result, housing demand. You must continually monitor your local economy, demand for rental housing, and other factors that will affect that demand over time.

Monitor the market, and be prepared to alter your strategy. Nothing remains the same forever. Just as stockholders need to watch for changing fundamentals of companies whose stock they buy, real estate investors have to do the same. Today’s strong demand market can soften next year. Your city may currently have a very low vacancy rate, but any number of factors could change the situation—for example, construction of a large apartment complex, closure of a major employer’s facility, seasonal factors, or a poor local economy. In areas near the Canadian border, changes in international exchange rates may affect the local retail market and, as a result, housing demand. You must continually monitor your local economy, demand for rental housing, and other factors that will affect that demand over time.

GETTING BETTER CASH FLOW

You can take some steps to improve cash flow. For example, if you were planning to pay for water and garbage disposal while your tenants will be responsible for electric and gas, you can instead shift all of the utility costs to your tenants in addition to rent. By shopping for more desirable mortgage terms or making a larger down payment, you can reduce the cash flow gap further. If lower rates become available, you can refinance, lowering your interest expense and monthly payment.

Even when the local conditions are not ideal for investing in real estate, you can improve your cash flow by picking properties carefully, altering your initial ideas about what types of rentals to buy, and increasing your down payment.

MULTIPLE-UNIT PROPERTIES

Your evaluation of likely cash flow may be interesting when you compare single-family housing to likely outcomes with multiunit housing. If you can purchase a single-family house for $120,000 and rent it out for $700 a month, you can make positive cash flow but only marginally. As an alternative, consider looking at multiple-unit investments. If you can find a duplex for the same $120,000 investment, you might also discover that each unit can be rented out for $500, increasing your cash flow by $300 per month—without a corresponding increase in expenses or in cash paid out. This is an example only, of course; the specific rent levels and prices of property vary by region. However, the point is that a duplex, triplex, or even a small apartment building may produce far better cash flow than a single-family home without requiring more investment or a higher mortgage payment.

A small apartment building is likely to require a greater investment and, perhaps, a higher down payment as well. However, if the cash flow justifies that as an alternative, it could make sense. Buying a five-unit apartment building would probably produce better cash flow than buying five single-family houses. It would also be easier and more economical to maintain, insure, and monitor a single property.

LARGER DOWN PAYMENT

In determining whether to make a higher down payment as a means for improving cash flow, the obvious limiting factor is availability of cash. However, a second level of analysis should be the use of available capital. If you can make cash flow work for a smaller down payment, that leaves more investment capital available for other purposes. The higher your down payment, the lower your cash flow risk, but more of your capital is tied up.

IMPROVED TAX BENEFITS

As your overall taxable income rises and you move into higher tax brackets, the tax advantages of owning real estate will be correspondingly higher as well. A relatively low overall (federal and state) tax bracket of 20–25 percent is not as advantageous, in terms of tax reduction, as an overall tax bracket of 40–50 percent or more. This, too, will create better cash flow down the road.

MANAGING CASH FLOW RISK

Because you need to make mortgage payments—even if you do not have a paying tenant in the property—there is a greater demand on your personal budget. This means that even if you have positive cash flow, a couple of months of vacancies could be a problem. For many first-time investors, the cash flow risk of real estate is invisible. You don’t think about it until you begin managing the property and repairs become necessary, vacancies occur, or your tenant is late with the rent one month. In these situations, the risk becomes all too apparent.

SPREADING THE RISK

One way to manage the cash flow risk is by spreading it. To many investors, this means buying more properties so that a negative situation in one is offset by positive cash flow in another. This may work most of the time but not all of the time. For example, if an increased vacancy rate is caused by changed local conditions, it is also likely that you will have higher vacancies on all of your properties. In that case, the intended diversification doesn’t achieve its intended result.

Another way to spread the risk is by investing in multiple-unit properties instead of single-family homes, as discussed previously. While the single-family property is likely to experience the best long-term market appreciation, you need to also consider how your financial life is going to be affected during the years that you own the property. Cash flow, in this respect, is more important than either long-term profits or year-to-year tax benefits. Remember these points:

1. You must be able to make monthly mortgage payments and pay for upkeep.

2. You need to ensure that you don’t overextend your budget by buying too many rental properties.

3. You need to consider your quality of life if you are managing a larger number of rentals. How much time are you willing to spend, and how much of your capital are you willing to tie up in illiquid, long-term investments?

These are the important questions that define cash flow risk and that, ultimately, determine how many properties you should purchase as investments and whether you want to directly manage those properties. If you believe that it makes sense to own several houses or one multiple-family property, you can also hire a professional management company. This insulates you from the day-to-day tenant contact that so many people find problematical.

WATCH THIS Using a property management company costs money, usually 10 percent of rents collected. For the marginal cash flow situation, such fees can be a big problem.

DO THE NUMBERS ADD UP?

Real estate cannot be economically bought and sold like stocks or mutual fund shares, so the market is far less liquid. For this reason, you need to determine the longer-term trends that affect both real estate values and likely long-term supply and demand for rentals. This can be achieved by studying employment statistics and knowing the number of rental units being built, the vacancy rates, and the prices of properties. Collectively, these factors also define whether or not you can make the cash flow work in your favor. If prices are too high, then mortgage payments will be higher, too.

It all comes down to a question of whether the numbers work out. As a real estate investor, you accept certain market risks, as you do in any form of investing. As long as you know those risks and can live with them, and the numbers work out to your satisfaction, you will better understand the finite nature of your own financial situation. Success in real estate investing is the result of initial research, a thorough awareness of risk, and the willingness to invest within your limits.