15. Reviewing Your Data

This book would not be complete without a few pages of instructions about what reports you should review for your business. These reports are not the only reports you will find useful in QuickBooks, but they are important for you to periodically review in your file.

These reports are only a subset of the many reports in QuickBooks, but accounting professionals typically use them to verify the accuracy of your data. This chapter is devoted to the business owner, helping you properly review your data for accuracy. Each section tells what the review accomplishes and what reports in QuickBooks help with these reviews.

Reviewing the Balance Sheet

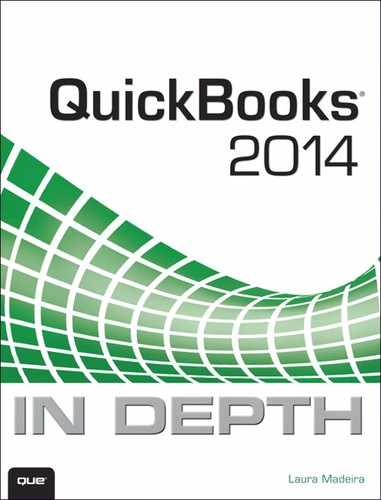

The report a business owner is least likely to look at is also one of the most important. To the business owner, the Balance Sheet report shows the balance of assets (what the business owns), liabilities (what the business owes others), and equity (what was put into the business or taken out of the business). Because these numbers are important, a business owner should first review this report.

This section details specific reports to use when reviewing your data. Each report is prepared on accrual basis unless otherwise mentioned. Begin by creating a Balance Sheet report of your data; this is the primary report we use for review.

From the menu bar, select Reports, Company & Financial, Balance Sheet Standard.

Leave the report with today’s date on it. You first review your data with today’s date before using any other date. In the following instructions, if a different date is needed, the step-by-step details state that. Verify that the top left of the report shows Accrual Basis. If not, click the Customize Report button on the report and select Accrual Basis from the Report Basis options.

Figure 15.1 shows a sample data Balance Sheet Standard report.

Figure 15.1. Review your Balance Sheet first, as in this example.

Account Types

Reviewing the account types assigned requires some basic knowledge of accounting. If you’re unsure of what to look for, ask your accountant to take a quick look at how your accounts are set up.

Review the names given to accounts. Do you see account names in the wrong place on the Balance Sheet? For example, does an Auto Loan account show up in the current asset section of the Balance Sheet?

To correct the category (account type) assigned, follow these steps:

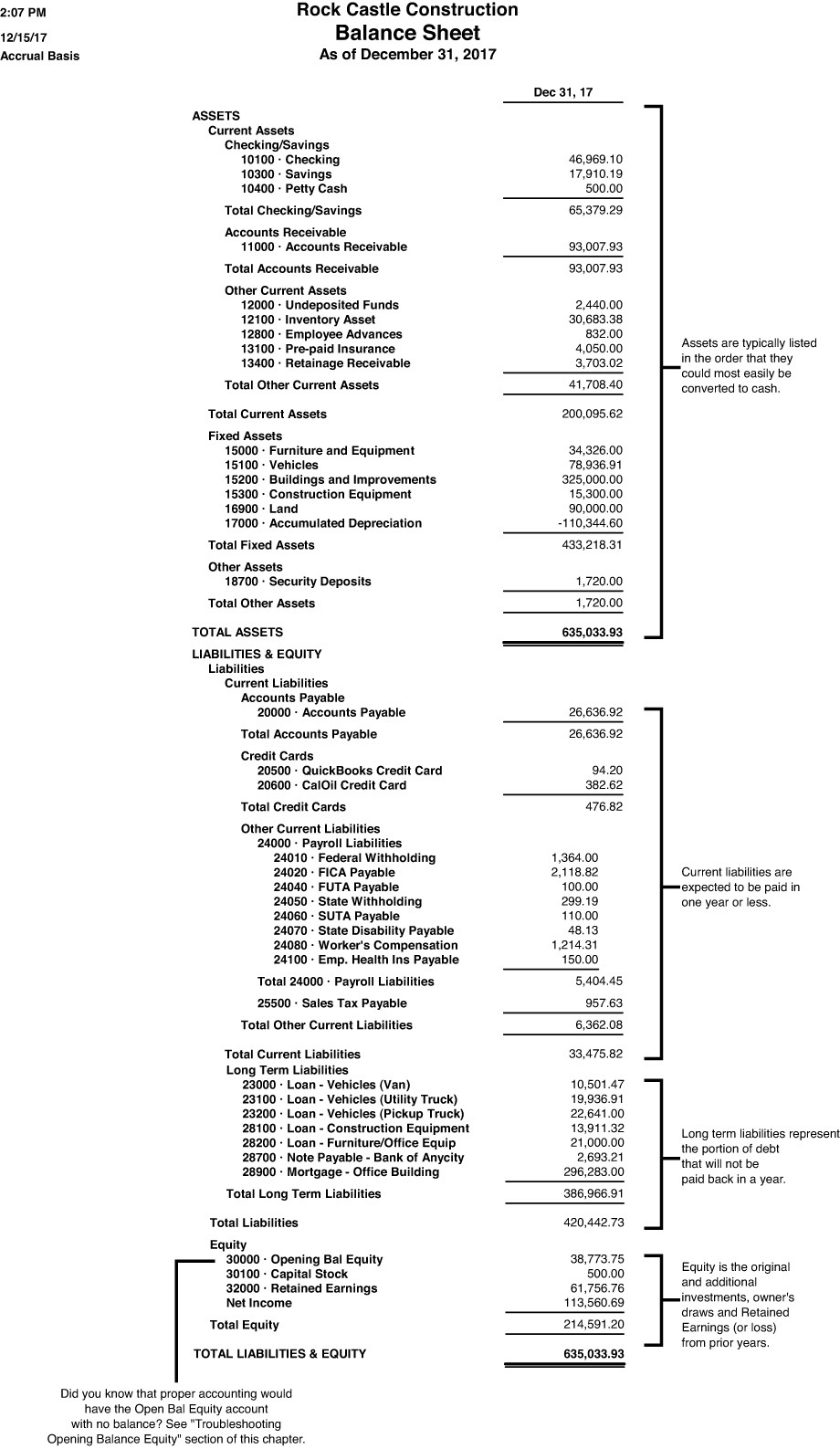

1. From the menu bar, select Lists, Chart of Accounts.

2. Select the account in question with one click. From the Account drop-down menu, select Edit. On the Edit Account dialog box (see Figure 15.2), you can select the drop-down menu for Account Type to change the currently assigned account type.

Figure 15.2. In the Edit or New Account dialog box, you assign the account type for proper placement of financial reports.

Prior Year Balances

You should give your accountant a copy of your Balance Sheet dated as of the last day of your prior tax year (or fiscal year) and request that he or she verify that the balances agree with the accounting records used to prepare your tax return. This is one of the most important steps to take in your review because Balance Sheet numbers are cumulative over the years you are in business.

→ For more information, see “Accrual Versus Cash Basis Reporting,” p. xxx.

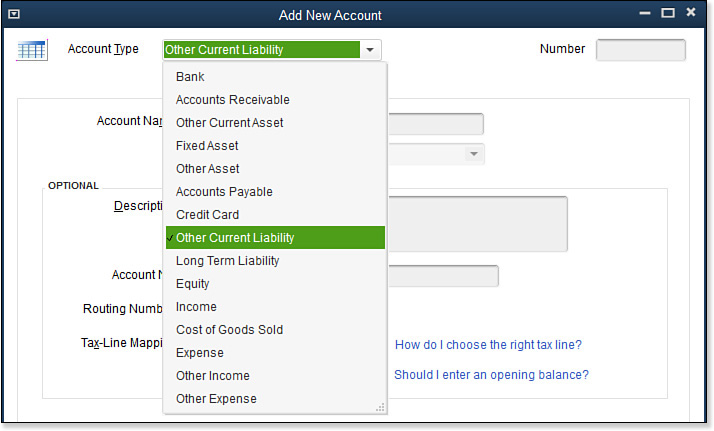

You can also create a two-year balance sheet to give to your accounting professional:

From the menu bar, select Reports, Company & Financial, Balance Sheet Prev Year Comparison (see the report in Figure 15.3). If necessary, click the Customize Report button to change the Report Basis.

Figure 15.3. The Balance Sheet Prev Year Comparison report is a useful report to give your accounting professional at tax time.

Tip

You might want to give the Balance Sheet Prev Year Comparison report to your accountant using both accrual and cash basis reporting. To change the basis of the report, click the Customize Report button and select the desired report basis on the Display tab.

Bank Account Balance(s)

Compare your reconciled bank account balances on the Balance Sheet report to the statement your bank sends you. Modify the date of the Balance Sheet to be the same as the ending statement date on your bank statement. Your QuickBooks Balance Sheet balance for your bank account should be equal to the bank’s ending statement balance plus or minus any uncleared deposits or checks/withdrawals dated on or before the statement ending date.

At tax time, give your last month’s bank statement and QuickBooks bank reconciliation report to your accounting professional.

Accounts Receivable

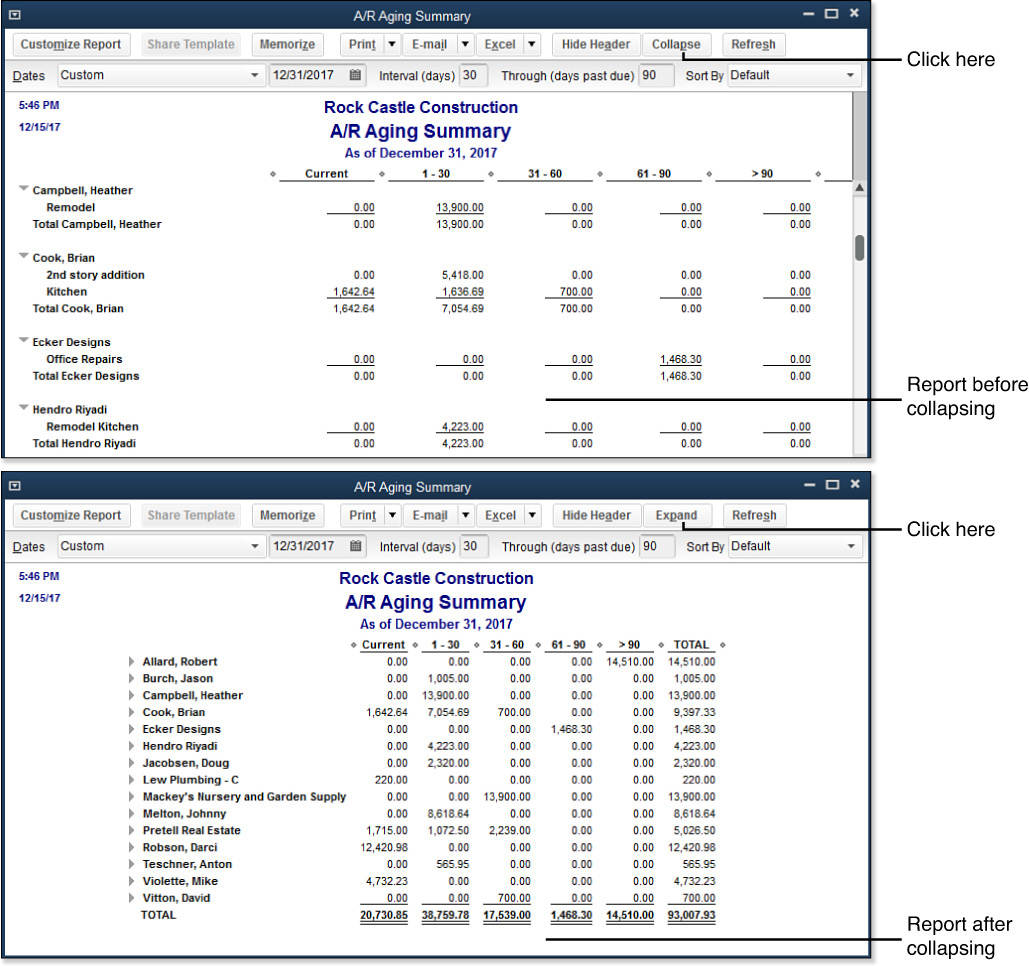

The Accounts Receivable balance on your Balance Sheet report should agree with the A/R Aging Summary Report total (see Figure 15.4).

Figure 15.4. Use Expand or Collapse at the top of the report to change the level of detail displayed.

To create the A/R Aging Summary report, from the menu bar, select Reports, Customers & Receivables, A/R Aging Summary or A/R Aging Detail. On the top of the report, click Collapse to minimize (remove from view) the line detail, making the report easier to view at a glance. The total should match the Accounts Receivable balance on the Balance Sheet report (see Figure 15.1).

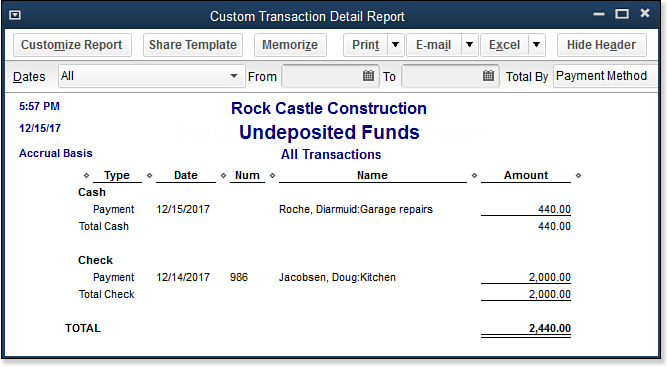

Undeposited Funds

The Undeposited Funds amount should agree with funds not yet deposited into your bank account, as shown in the custom report in Figure 15.5 (use today’s date on your Balance Sheet report).

Figure 15.5. The amount of funds this report shows should agree with the amount of funds you have not yet taken to the bank.

Create the following custom report to review the Undeposited Funds detail sorted by payment method:

1. From the menu bar, select Reports, Custom Reports, Transaction Detail. The Modify Report dialog box opens.

2. In the Report Date Range box, select All (type an a to change the date range to All).

3. In the Columns box, select the data fields you want to view on the report; in the Total By drop-down menu, select Payment Method.

4. Click the Filters tab; Account is already highlighted in the Choose Filter box. In the Account drop-down menu to the right, choose Undeposited Funds.

5. Also in the Choose Filter box, scroll down to select Cleared; on the right, select Cleared No.

6. (Optional) Click the Header/Footer tab and change the report title to Undeposited Funds. Click OK to view the report.

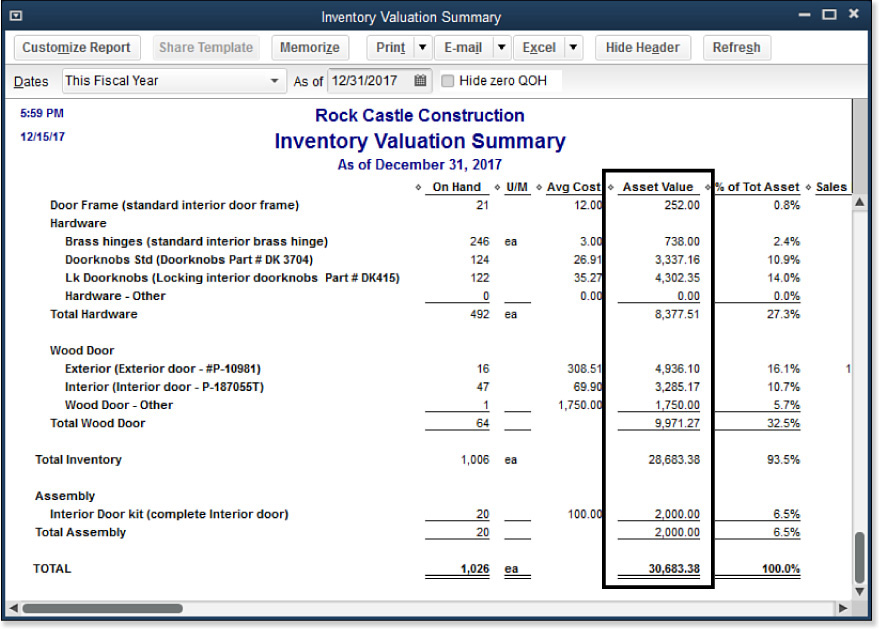

Inventory

The Inventory balance on the Balance Sheet report (refer to Figure 15.1) should agree with the Inventory Valuation Summary Asset Value report total (see Figure 15.6). The ending dates of both reports need to be the same.

Figure 15.6. The total of the Asset Value column should agree with the Inventory balance on the Balance Sheet report.

To create the Inventory Valuation Summary report, from the menu bar, select Reports, Inventory, Inventory Valuation Summary. Chapter 6, “Managing Inventory,” has more details on working with inventory reporting.

Other Current Assets

The Other Current Asset accounts can differ widely by company. If you have employee advances, make sure your employees concur with your records. For any other accounts in the Other Current Asset category, look to documentation within QuickBooks to verify the reported balances.

Do you need an easy report to sort the detail in these Other Current Asset accounts by a list name? In this example, I created a detail report of the Employee Advances account, sorted and subtotaled by payee (see Figure 15.7). You can create this same report for any of your accounts, sorting in a way that improves the detail for your review.

Figure 15.7. Create a custom report to review balances in an Employee Advances account or any other asset account.

To create a detail report of your Other Current Asset accounts (in addition to other types of accounts), follow these steps:

1. From the menu bar, select Reports, Custom Reports, Transaction Detail. The Modify Report dialog box displays.

2. On the Date Range drop-down menu, select All.

3. In the Columns box, select the specific data you want to see in the report.

Tip

Reconciling accounts like these can be useful. An example is when an employee pays back the loan in full. Complete the reconciliation for this account when the total of the loans matches the total of the payments, marking each transaction for this employee as Cleared. You can then filter the report for Uncleared only, limiting the amount of information that displays. This results in a beginning and ending balance of net $0.00.

4. Also in the Columns box, in the Total By drop-down menu, select Payee.

5. Click the Filters tab.

6. The Choose Filter box already has selected the Account filter. At the right, in the Account drop-down menu, select the Employee Advances account (or select the specific account for which you want to see detail).

7. (Optional) Click the Header/Footer tab and provide a unique report title. Click OK to create the modified report.

Verify the balances reported here with either the employees or outside source documents. If you do reconcile the account, you can filter for those transactions with a cleared status of No. This streamlines the amount of information the report displays.

Fixed Assets

Fixed assets are purchases that have a long-term life and, for tax purposes, cannot be expensed all at once. Instead, they must be depreciated over the expected life of the asset.

Accountants can advise business owners on how to classify assets. If the account balances have changed from year to year, you might want to review what transactions were posted, to make sure they are fixed-asset purchases and not expenses that should be reported on the Profit & Loss report.

If you have properly recorded a fixed-asset purchase to this account category, give your accountant the purchase receipt and any supporting purchase documents for their depreciation schedule records.

If you see a change in the totals from one year to the next, you can review the individual transactions in the account register by clicking Banking, Use Register, and selecting the account you want to review. Figure 15.8 shows the register for Fixed Assets—Furniture and Equipment. If a transaction was incorrectly posted here, you can edit the transaction by double-clicking the line detail and correcting the assigned account category.

Figure 15.8. Use registers for certain accounts to see the transactions that affect the balances.

Accounts Payable

The Accounts Payable balance on the Balance Sheet report should agree with the A/P Aging Summary report total (see Figure 15.9).

Figure 15.9. The A/P Aging Summary report total should agree with your Balance Sheet, Accounts Payable balance.

To create the A/P Aging Summary or Detail report, from the menu bar, select Reports, Vendors & Payables, A/P Aging Summary or Detail. For more information, see Chapter 8, “Managing Vendors.”

Credit Cards

Your credit card account balances should reconcile with the balances from your credit card statement(s). You might have to adjust your Balance Sheet report date to match your credit card vendor’s statement date, or you can request that your credit card company provide you with a statement cut-off at the end of a month.

You should give your accountant a copy of the most recent credit card statement so that he or she can verify the accuracy of your credit card balance.

For more information on working with reconciliation tasks, see Chapter 13, “Working with Bank and Credit Card Accounts.”

Payroll Liabilities

The Payroll Liabilities balance on the Balance Sheet report should agree with your Payroll Liability Balances report total. Be careful with the dates here. If you have unpaid back payroll taxes, select a date range of All for the Payroll Liability Balances report. See Figure 15.10.

Figure 15.10. The Payroll Liability Balances report total should agree with the same total on the Balance Sheet report.

To create the Payroll Liability Balances report, from the menu bar, select Reports, Employees & Payroll, Payroll Liability Balances. Totals on this report should match your Balance Sheet report for the Payroll Liabilities account.

Sales Tax Payable

The Sales Tax Payable balance on the Balance Sheet report should agree with the Sales Tax Liability report balance. You might need to change the Sales Tax Payable report date and basis to match that of your Balance Sheet.

Caution

If you have set up your Sales Tax Preference as Cash Basis, you cannot compare this balance to an Accrual Basis Balance Sheet report.

To create the Sales Tax Liability report, from the menu bar, select Reports, Vendors & Payables, Sales Tax Liability.

Make sure the To date matches that of the Balance Sheet report date. The total should match the Sales Tax Payable total on your Balance Sheet report (see Figure 15.11).

Figure 15.11. The Sales Tax Liability report total should match the Sales Tax Payable balance on your Balance Sheet report.

Other Current Liabilities and Long-Term Liabilities

Compare any other accounts you have in the Other Current Liabilities and Long-Term Liabilities account types with outside documents from your lending institutions.

Reconcile these accounts the same as you reconcile your bank account, to verify that your balances agree with the lending institution’s records.

Note

If you have an account named Opening Balance Equity that has a balance, this account should have a zero balance after data file setup is completed. For more information, see “Closing Opening Balance Equity to Retained Earnings,” p. xxx.

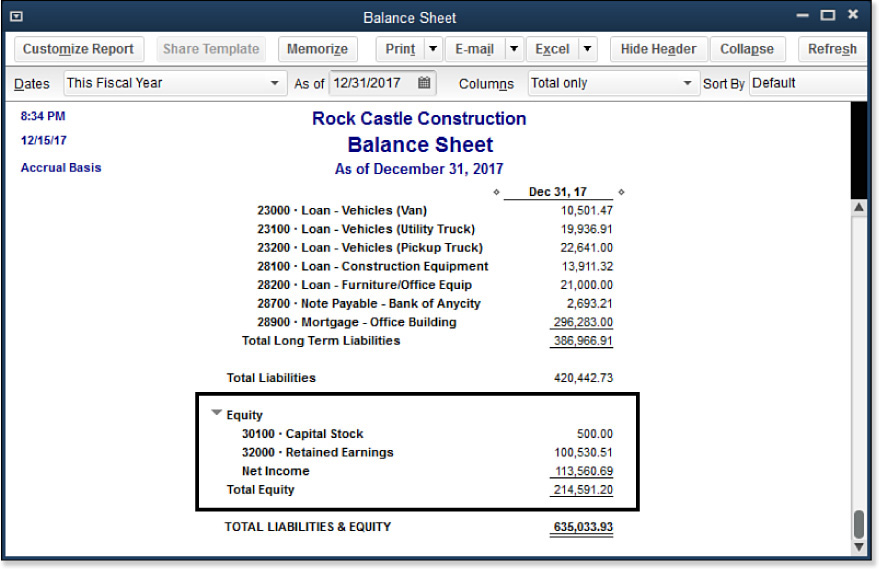

Equity

Equity accounts differ for each company. Your accountant should review these account balances and make any necessary tax adjustments at year-end or tax time.

The reports this chapter discusses do not make up an exhaustive, end-all list for reviewing your Balance Sheet, but they are a great start when reviewing your own data or your client’s data.

Reviewing the Profit & Loss Report

My experience over the years has been that business owners do not look at the Balance Sheet report often, if at all. However, nearly every business owner I have worked with has reviewed the Profit & Loss Standard report for the business. The reason might be that the Profit & Loss report is easier to interpret than the Balance Sheet report.

Even with simple organization (money in, money out), a careful review of the Profit & Loss report is prudent for the business owner who wants to track how well the business is doing financially. To create a Profit & Loss Standard report, from the menu bar, select Reports, Company & Financial, Profit & Loss Standard (or Profit & Loss Detail).

You can review your Profit & Loss report using two methods:

• Cash Basis—Income is recognized when received. Expenses are recognized when paid.

• Accrual Basis—Income is recognized as of the date of the customer’s invoice. Expenses are recognized as of the date of the vendor’s bill.

Cash basis reporting offers an incomplete snapshot in time because it shows what cash has changed hands but doesn’t show unpaid bills from vendors or uncollected invoices from customers. Additionally, many companies file their annual tax returns using cash basis reports. Nothing is wrong with looking at reports prepared with cash basis accounting. However, I encourage all my clients to consider reviewing the Profit & Loss Standard report in accrual basis.

Accrual basis, although more complex, provides so much more information about the business:

• Matching Principle—Revenue (customer invoice) is recorded in the same accounting period as the expenses (vendor bills, paychecks, and the like) associated with services or products sold on the customer’s invoice.

• Seasonal Variations—Track how your business performs financially—for example, by comparing the same month across multiple years.

• Tracking Receivables and Payables—This information helps with both short-term and long-term forecast planning.

Tip

To review recurring monthly charges, preparing your Profit & Loss by the month is useful. In the Profit & Loss report, from the Columns drop-down menu at the top of the report, select Month.

With QuickBooks, you can easily change the report from cash to accrual basis by clicking the Customize Report button and manually selecting Cash or Accrual Basis on the Display tab of the Modify Report dialog box.

When reviewing the details of your Profit & Loss Detail report, you might want to look for these types of transactions:

• Monthly charges, such as rent, utility, equipment lease expenses, or other recurring expenses. Verify that the correct number of these charges is recorded, such as 12 monthly payments for rent.

• Credit card expenses reported to the proper expense accounts.

• Nonpayroll payments to owners, which normally are recorded to draw or equity type accounts.

• Purchase of equipment with a significant cost, which should have been recorded to an asset account.

• The principal portion of loan payments for vehicles or equipment; these should have been recorded to liability accounts.

A business owner who takes the time to review the Profit & Loss Detail report can feel more confident that business decisions founded on financials are as accurate as possible.

Other Reviews

You have completed the basic Balance Sheet and Profit & Loss Report reviews. These are important, and you are well on your way to being more confident about the information. This section details other equally important reviews.

Tracking Changes to Closed Accounting Periods

You can “lock” your QuickBooks data and prevent users from making changes to prior accounting periods. (Accountants call this process a soft close.) If you then need to add or modify a transaction in a prior period, the Admin user (or someone with security rights) can return and “unlock” the accounting period.

To have QuickBooks track information for the Closing Date Exception report, you have to set a closing date and, optionally, set specific users’ access to adding or modifying transactions on or before this date.

If you have compared your own or your clients’ data to prior-year financials or tax returns and the ending balances prior to the closing date have changed, you should view the Closing Date Exception report (available with QuickBooks Premier or Enterprise) to see exactly who made the change and what specific transactions were affected. For more information on working with clients’ files, see Chapter 16, “Sharing QuickBooks Data with Your Accountant.”

Caution

Exceptions, additions, and changes are not tracked unless a closing date has been set for a QuickBooks file.

To create the Closing Date Exception report (see Figure 15.12), from the menu bar, select Reports, Accountant & Taxes, Closing Date Exception. If you have not set a closing date, a warning prompt displays.

Figure 15.12. Review the Closing Date Exception report for changes made to transactions dated on or before a closing date.

This report enables you to identify changes that were made to transactions dated on or before the closing date. For modified transactions, the report details both the latest version of a transaction and the earlier version (as of the closing date). If your QuickBooks access rights allow you to change closed period transactions, you can then re-create the original transaction or change the date of added transactions so that you again agree with the ending balance from the previously closed period.

Accounting professionals can consult Appendix A, “Client Data Review,” for details on using the Troubleshoot Beginning Balances feature in QuickBooks Accountant.

Using the Audit Trail Report

The Audit Trail report provides details of additions and changes made to transactions, grouping the changes by username. The detail on this report shows the earlier and latest version of the transaction, if it was edited. You can filter the report to show a specific date range to narrow the amount of detail.

The Audit Trail report is available in all desktop versions of QuickBooks. To create the Audit Trail report in Figure 15.13, from the menu bar, select Reports, Accountant & Taxes, Audit Trail.

Figure 15.13. The QuickBooks Audit Trail report helps identify what changes were made to transactions and by which user.

If you find undesired transaction changes, consider setting a closing date password and limiting user security privileges.

→ For more information, see “Set a Closing Date,” p. xxx.

Using the Credit Card Audit Trail Report

QuickBooks users can stay in compliance with credit card industry security requirements by enabling security around who can view, add, or edit customers’ credit card numbers.

You can include or exclude individual users’ access to customers’ sensitive credit card information. The company accountant also can take advantage of a user type called External Accountant. When this type is assigned to your accountant, he or she cannot view these sensitive customer credit card numbers.

Additionally, when the Credit Card Audit Trail report is enabled, you can track which user viewed, edited, added, or removed a customer’s credit card number.

These three steps provide an overview of how to use this feature correctly:

1. Enable the customer credit card protection feature.

2. Select which users are given security rights to view the credit card numbers and which users are not given this privilege.

3. View the new Credit Card Audit Trail report to track viewing, editing, adding, and deleting activity with your customers’ credit cards.

The first step to viewing details on the Credit Card Audit Trail report is to enable Customer Credit Card Protection in QuickBooks. To do so, follow these steps:

1. Log in to the data file as the Admin user. From the menu bar, select Company, Customer Credit Card Protection.

2. Click the Enable button to open the Customer Credit Card Protection Setup dialog box. Type a complex password that is at least seven characters, including one number and one uppercase character. For example, coMp1ex is a complex password. This complex password now replaces the previous Admin password.

3. You also must choose a Challenge Question from the drop-down menu and provide an answer to a question. This question helps you reset your password if you forget it. Click OK.

4. A message box opens, letting you know the next steps and telling you that you will be reminded in 90 days to change the password. Click OK.

5. QuickBooks notifies you that you have enabled Customer Credit Card Protection and details how to allow access by user to the credit card numbers (see step 6). Click OK. You then return to QuickBooks logged in as the Admin user.

6. To select which employees have access to view the full credit card numbers, or to add or change customer credit card numbers, from the menu bar, select Company, Set Up Users and Passwords, and select the Set Up Users option.

7. The QuickBooks login dialog box displays, requiring you to enter the Admin password to gain access to user security settings. Click OK to open the User List dialog box.

8. Select a username and click the Edit button. (Optional) Edit the username or password, or click Next to accept these fields as they are.

9. The Access window for the specific user opens. Choose the Selected Areas of QuickBooks option. Click Next.

10. The Sales and Accounts Receivable access options display. Choose either Full Access or Selective Access; either of these choices combined with a checkmark in the View Complete Credit Card Numbers box (see Figure 15.14) enables the user to view and add, delete, or modify the credit card number. If no checkmark is placed, the user sees only the last four digits of the customer’s credit card when recording transactions that use this sensitive information.

Figure 15.14. Option to limit user-specific access to viewing complete customer credit card numbers.

11. Click Finish if this is the only setting you want to modify, or click Next to advance through additional security settings.

Tip

When creating a login user for your accountant, select the user type External Accountant. By default, this user type cannot view your customers’ stored sensitive credit card numbers.

You have now properly enabled the customer credit card protection and granted or removed user access to these confidential credit card numbers.

With this feature enabled, your data file is now tracking critical user activity about your customers’ credit card numbers. QuickBooks records when the credit card security was enabled and maintains records of when a user enters a credit card number, modifies a credit card, or even views the Customer Credit Card Audit Trail report (see Figure 15.15).

Figure 15.15. The Customer Credit Card Audit Trail report cannot be modified, filtered, or purged.

This Customer Credit Card Audit Trail report is always tracking customer credit card activity, as long as the feature remains enabled. This report can be viewed only by logging into the file as the Admin user. However, you can use your mouse to select the entire report or part of it and then press Ctrl+C to copy the report to the Windows Clipboard. You can then paste the report into Excel or another program if you want to search or filter the report.

While not recommended, if you want to disable this setting, you must first log in to the data file as the Admin user and enter the complex password that you created when you enabled the protection. From the menu bar, select Company, Customer Credit Card Protection, and click the Disable Protection button. Click Yes to accept that customers’ credit card number viewing, editing, and deleting activity by QuickBooks users is no longer being tracked for audit purposes.

Reporting on Voided/Deleted Transactions

QuickBooks offers flexibility for handling changes to transactions. If you grant users rights to create transactions, they also have rights to void and delete transactions. Don’t worry—you can view these voided transaction changes in the Voided/Deleted Transactions Summary (see Figure 15.16) or Voided/Deleted Transactions Detail reports. You can use these reports to view transactions before and after the change, as well as to identify which user made the change.

Figure 15.16. The QuickBooks Voided/Deleted Transactions Summary report quickly identifies which transactions were either voided or deleted, making troubleshooting easy.

To create the Voided/Deleted Transactions Summary report, from the menu bar, select Reports, Accountant & Taxes, Voided/Deleted Transactions Summary (or Voided/Deleted Transactions Detail).

Viewing the Transactions List by Date Report

Although the title of Transaction List by Date report doesn’t imply as much “power” as the other reports discussed in this chapter, I use this report most often when reviewing a data file.

If you are new to QuickBooks, you will soon learn that the date you enter for each transaction is important. The year you assign to the transaction is the year QuickBooks reports the transaction in your financials. For example, if you record a transaction with the year 2071 instead of 2017, this date can cause your financials not to show the effect until the year 2071.

To create the Transaction List by Date report, shown in Figure 15.17, from the menu bar, select Reports, Accountant & Taxes, Transaction List by Date. In the Dates drop-down menu, select All.

Figure 15.17. The QuickBooks Transaction List by Date report can help identify any incorrectly dated transactions.

You can use this report to see both the oldest dated transaction (when the file was started) and the furthest-dated transaction (to identify whether date errors have been made). As with all other QuickBooks reports, you can double-click a specific transaction to change the date, if needed.

Fortunately, QuickBooks preferences help avoid transaction dating errors by enabling you to set a warning for date ranges. To open the date warning preference, follow these steps:

1. Log in to the QuickBooks data file as the Admin or External Accountant user.

2. From the menu bar, select Edit, Preferences. In the Preferences dialog box, select the Company Preferences tab and choose the Accounting preference on the left.

3. Type in the user-defined date warning range you want to work with for past-dated transactions and future-dated transactions. QuickBooks sets the default warnings at 90 days in the past and 30 days in the future. An attempt to enter transactions dated before or after this date range prompts QuickBooks to give the user a warning message (see Figure 15.18).

Figure 15.18. Set the Date Warning preference so users are warned when dating a transaction outside an acceptable date range.

Caution

Be cautious when making changes to the dates, especially if the year in question has already had a tax return prepared on the existing information.

Troubleshooting Opening Balance Equity Account

QuickBooks automatically records the following transactions to the Opening Balance Equity account:

• Your opening balance transaction when you created a new bank account in the Express Start setup

• Opening balances for other Balance Sheet report accounts created in the Add New Account dialog box

• Inventory total value balances entered in the New Item dialog box

• Bank reconciliation adjustments for older versions of QuickBooks

Other common transactions that a user might assign to this account include the following:

• Accrual basis opening accounts payable transactions as of the start date

• Accrual basis opening accounts receivable transactions as of the start date

• Uncleared bank checks or deposits (accrual or cash basis) as of the start date

Caution

Although Intuit offers certain ready-made tools to convert other software to QuickBooks, some might not convert the data as expected. Be sure to verify that the information is correct after the conversion.

Closing Opening Balance Equity into Retained Earnings

The Opening Balance Equity account should have a zero balance when a file setup is complete and done correctly. When I refer to a completely and correctly set-up QuickBooks file, I assume the following:

• You are not converting your data from Quicken, Sage 50 (formerly Peachtree), Small Business Accounting, or Office Accounting. Each of these products has an automated conversion tool available free from Intuit, which eliminates the need to do startup transactions if you convert the data and not just lists.

• Your company did not have any transactions prior to the first use of QuickBooks. In this case, you simply enter typical QuickBooks transactions after your QuickBooks start date, with no need for unusual startup type entries.

• Your company did have transactions prior to the first use of QuickBooks. You have chosen to enter these transactions one by one as regular transactions. You do not need to record any transactions to the Opening Balance Equity account.

• Your company did have transactions prior to the first use of QuickBooks, but there are so many that it is not feasible to re-create them in QuickBooks. Instead, follow the directions in Chapter 3, “Setting Up a QuickBooks Data File for Accrual or Cash Basis Reporting,” p. xxx.

• You have entered each of your unpaid customer invoices, unpaid vendor bills, and uncleared bank transactions and dated them prior to your QuickBooks start date.

• You have entered and dated your trial balance one day before your QuickBooks start date. (You might need to request the trial balance numbers from your accountant if you are not converting from some other financial software that provides you with a trial balance.)

• When you create a Trial Balance report in QuickBooks dated one day before your QuickBooks start date, it agrees with your accountant’s trial balance or with the trial balance from your prior financial software, with the exception that you have a balance in the Opening Balance Equity account.

If you answered yes to each of these assumptions, I expect that your Opening Balance Equity account is equal to the Retained Earnings balance from your accountant’s financials or from your prior software, or I assume that the amount matches the Equity section balance if your entity is an LLC or partnership with no Retained Earnings. If it doesn’t agree, you need to continue to review the data to identify the errors. If it does agree, you are prepared to make the final entry in your startup process.

To create this closing entry using a General Journal Entries transaction, follow these steps:

1. From the menu bar, select Company, Make General Journal Entries.

2. Enter a Date (it should be one day before your QuickBooks start date).

3. Type an Entry No.

4. Leaving line 1 of the transaction blank, on line 2 of the Make General Journal Entries transaction (using the example shown in Figure 15.19), decrease (debit) Opening Balance Equity by $38,773.75 and increase (credit) Retained Earnings by the same amount. This action “closes” Opening Balance Equity to Retained Earnings. Click Save & Close.

Figure 15.19. Use a Make General Journal Entries transaction to close Opening Balance Equity to Retained Earnings.

Caution

Leave the first line of any Make General Journal Entries transaction blank because QuickBooks uses this line as the source line. Any list item in the name column on the first line (source line) of a General Journal Entries transaction also is associated in reports with the other lines of the same general journal entries transaction. For more information about working with multiple-line journal entries, see the caution on p. xxx of Chapter 10, “Managing Customers.”

5. Click OK to the QuickBooks warning that displays; QuickBooks saves the transaction. The warning advises you that you are posting to a Retained Earnings account and states that QuickBooks has a special purpose for this account. It is appropriate to post this entry to Retained Earnings. This warning is a result of a preference setting you can access from the menu bar by selecting Edit, Preferences, Accounting. Select the Company Preferences tab and choose the option to enable Warn when posting a transaction to Retained Earnings prompt. (You must be logged in as Admin or External Accountant user, and you must be in single-user mode to modify this preference.)

When the transaction is saved, create the Balance Sheet Standard report as explained earlier in this chapter and verify that your ending numbers are accurate—that is, they should match your accountant’s or your prior software trial balance for the same period. Figure 15.20 now shows the proper Retained Earnings balance, and you no longer have a balance in Opening Balance Equity.

Figure 15.20. The Balance Sheet viewed after “closing” Opening Balance Equity to Retained Earnings.

Reviewing your data file can help improve the accuracy of your tax filings and provide more reliable information for management decisions.