Module 24: Federal Securities Acts

Overview

The bulk of the material tested on the exam from this area comes from the Securities Act of 1933, as amended, and the Securities Exchange Act of 1934, as amended. Topics included under the scope of the 1933 Act are registration requirements, exempt securities, and exempt transactions. The purposes of the 1933 Act are to provide investors with full and fair disclosure of a security offering and to prevent fraud. The basic prohibition of the 1933 Act is that no sale of a security shall occur in interstate commerce without registration and without furnishing a prospectus to prospective purchasers unless the security or the transaction is exempt from registration.

The purpose of the 1934 Act is the establishment of the Securities Exchange Commission to assure fairness in the trading of securities subsequent to their original issuance. The basic scope of the 1934 Act is to require periodic reports of financial and other information concerning registered securities, and to prohibit manipulative and deceptive devices in both the sale and purchase of securities.

A. Securities Act of 1933

B. Securities Exchange Act of 1934

C. The Sarbanes-Oxley Act of 2002

D. The Wall Street Reform and Consumer Protection (Dodd-Frank) Act of 2010

E. Exemptions for Smaller and Emerging Companies

F. Internet Securities Offering (ISO)

G. Electronic Signatures and Electronic Records

H. State “Blue-Sky” Laws

Key Terms

Multiple-Choice Questions

Multiple-Choice Answers and Explanations

Simulations

Simulation Solutions

The exam often tests on the Federal Securities Acts; however, this is sometimes combined with accountant’s liability or is included within questions concerning corporate or limited partnership law. You should also expect questions on the Sarbanes-Oxley Act of 2002 and the Dodd-Frank Act of 2010. Before beginning the reading you should review the key terms at the end of the module.

C. The Sarbanes-Oxley Act of 2002

D. The Wall Street Reform and Consumer Protection (Dodd-Frank) Act of 2010

E. Exemptions for Smaller and Emerging Companies

G. Electronic Signatures and Electronic Records

H. State “Blue-Sky” Laws

KEY TERMS

Insiders. Includes officers, directors, and owners of more than 10% of any class of an issuer’s equity securities.

Prospectus. Any notice, circular, advertisement, letter, or communication offering any security for sale (or merger).

Proxy. Grant of authority by a shareholder to someone else to vote the shareholder’s shares at a meeting.

Registration statement. The statement required to be filed with the SEC before the initial sale of securities can occur.

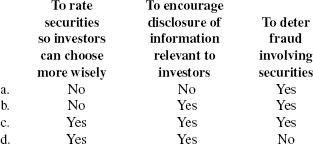

Security. Any debt or equity interest in a company including a note, stock, bond, certificate of interest, debenture, investment contract, etc.

Underwriter. Any person who has purchased from an issuer with a view to the public distribution of any security, or a party who participates in such an undertaking.

Multiple-Choice Questions (1–45)

A. Securities Act of 1933

1. A preliminary prospectus, permitted under SEC Regulations, is known as the

a. Unaudited prospectus.

b. Qualified prospectus.

c. “Blue-sky” prospectus.

d. “Red-herring” prospectus.

2. Under the Securities Exchange Act of 1934, which of the following types of instruments is excluded from the definition of “securities”?

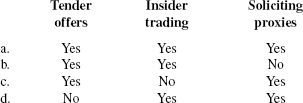

a. Investment contracts.

b. Convertible debentures.

c. Nonconvertible debentures.

d. Certificates of deposit.

3. A tombstone advertisement

a. May be substituted for the prospectus under certain circumstances.

b. May contain an offer to sell securities.

c. Notifies prospective investors that a previously-offered security has been withdrawn from the market and is therefore effectively “dead.”

d. Makes known the availability of a prospectus.

4. Under the Securities Act of 1933, which of the following statements most accurately reflects how securities registration affects an investor?

a. The investor is provided with information on the stockholders of the offering corporation.

b. The investor is provided with information on the principal purposes for which the offering’s proceeds will be used.

c. The investor is guaranteed by the SEC that the facts contained in the registration statement are accurate.

d. The investor is assured by the SEC against loss resulting from purchasing the security.

5. Which of the following statements concerning the prospectus required by the Securities Act of 1933 is correct?

a. The prospectus is a part of the registration statement.

b. The prospectus should enable the SEC to pass on the merits of the securities.

c. The prospectus must be filed after an offer to sell.

d. The prospectus is prohibited from being distributed to the public until the SEC approves the accuracy of the facts embodied therein.

Items 6 and 7 are based on the following facts:

Sandy Corporation is considering the following issuances:

I. Notes with maturities of three months to be used for commercial purposes and having a total aggregate value of $500,000.

II. Notes with maturities of two years to be used for investment purposes and having a total aggregate value of $300,000.

III. Notes with maturities of two years to be used for commercial purposes and having a total aggregate value of $200,000.

6. Which of the above notes is (are) exempt securities and need not be registered under the Securities Act of 1933?

a. I only.

b. II only.

c. I and III only.

d. I, II, and III.

7. Which of the above notes is (are) subject to the antifraud provisions of the Securities Act of 1933?

a. I only.

b. II only.

c. I and III only.

d. I, II, and III.

8. Which of the following is not a security under the definition for the Securities Act of 1933?

a. Any note.

b. Bond certificate of interest.

c. Debenture.

d. All of the above are securities under the Act.

9. Which of the following requirements must be met by an issuer of securities who wants to make an offering by using shelf registration?

| Original registration statement must be kept updated | The offer must be a first-time issuer of securities | |

| a. | Yes | Yes |

| b. | Yes | No |

| c. | No | Yes |

| d. | No | No |

10. Which of the following securities would be regulated by the provisions of the Securities Act of 1933?

a. Securities issued by not-for-profit, charitable organizations.

b. Securities guaranteed by domestic governmental organizations.

c. Securities issued by savings and loan associations.

d. Securities issued by insurance companies.

11. Which of the following securities is exempt from registration under the Securities Act of 1933?

a. Shares of nonvoting common stock, provided their par value is less than $1.00.

b. A class of stock given in exchange for another class by the issuer to its existing stockholders without the issuer paying a commission.

c. Limited partnership interests sold for the purpose of acquiring funds to invest in bonds issued by the United States.

d. Corporate debentures that were previously subject to an effective registration statement, provided they are convertible into shares of common stock.

12. Universal Corp. intends to sell its common stock to the public in an interstate offering that will be registered under the Securities Act of 1933. Under the Act,

a. Universal can make offers to sell its stock before filing a registration statement, provided that it does not actually issue stock certificates until after the registration is effective.

b. Universal’s registration statement becomes effective at the time it is filed, assuming the SEC does not object within twenty days thereafter.

c. A prospectus must be delivered to each purchaser of Universal’s common stock unless the purchaser qualifies as an accredited investor.

d. Universal’s filing of a registration statement with the SEC does not automatically result in compliance with the “blue-sky” laws of the states in which the offering will be made.

13. If securities are exempt from the registration provisions of the Securities Act of 1933, any fraud committed in the course of selling such securities can be challenged by

| SEC | Person defrauded | |

| a. | Yes | Yes |

| b. | Yes | No |

| c. | No | Yes |

| d. | No | No |

14. Issuers of securities are normally required under the Securities Act of 1933 to file a registration statement with the Securities Exchange Commission before these securities are either offered or sold to the general public. Which of the following is a reason why the SEC adopted the registration statement forms called Form S-2 and Form S-3?

a. To require more extensive reporting.

b. To be filed along with Form S-1.

c. To reduce the burden that issuers have under the securities laws.

d. To reduce the burden of disclosure that issuers have for intrastate issues of securities.

A.5. Exempt Transactions or Offerings

15. Regulation D provides for important exemptions to registration of securities under the Securities Act of 1933. Which of the following would be exempt?

I. Issuance of $500,000 of securities sold in a 12-month period to forty investors.

II. Issuance of $2,000,000 of securities sold in a 12-month period to 10 investors. The issuer restricts the right of the purchasers to resell for two years.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

16. Pix Corp. is making a $6,000,000 stock offering. Pix wants the offering exempt from registration under the Securities Act of 1933. Which of the following provisions of the Act would Pix have to comply with for the offering to be exempt?

a. Regulation A.

b. Regulation D, Rule 504.

c. Regulation D, Rule 505.

d. Regulation D, Rule 506.

17. Eldridge Corporation is seeking to offer $7,000,000 of securities under Regulation D of the Securities Act of 1933. Which of the following is (are) true if Eldridge wants an exemption from registration under the Securities Act of 1933?

I. Eldridge must comply with Rule 506 of Regulation D.

II. These securities could be debentures.

III. These securities could be investment contracts.

a. I only.

b. I and II only.

c. II and III only.

d. I, II, and III.

18. An offering made under the provisions of Regulation A of the Securities Act of 1933 requires that the issuer

a. File an offering circular with the SEC.

b. Sell only to accredited investors.

c. Provide investors with the prior four years’ audited financial statements.

d. Provide investors with a proxy registration statement.

19. Which of the following facts will result in an offering of securities being exempt from registration under the Securities Act of 1933?

a. The securities are nonvoting preferred stock.

b. The issuing corporation was closely held prior to the offering.

c. The sale or offer to sell the securities is made by a person other than an issuer, underwriter, or dealer.

d. The securities are AAA-rated debentures that are collateralized by first mortgages on property that has a market value of 200% of the offering price.

20. Regulation D of the Securities Act of 1933

a. Restricts the number of purchasers of an offering to 35.

b. Permits an exempt offering to be sold to both accredited and nonaccredited investors.

c. Is limited to offers and sales of common stock that do not exceed $1.5 million.

d. Is exclusively available to small business corporations as defined by Regulation D.

21. Frey, Inc. intends to make a $2,000,000 common stock offering under Rule 505 of Regulation D of the Securities Act of 1933. Frey

a. May sell the stock to an unlimited number of investors.

b. May make the offering through a general advertising.

c. Must notify the SEC within 15 days after the first sale of the offering.

d. Must provide all investors with a prospectus.

22. Under Regulation D of the Securities Act of 1933, which of the following conditions apply to private placement offerings? The securities

a. Cannot be sold for longer than a six-month period.

b. Cannot be the subject of an immediate unregistered reoffering to the public.

c. Must be sold to accredited institutional investors.

d. Must be sold to fewer than twenty nonaccredited investors.

23. Which of the following statements concerning an initial intrastate securities offering made by an issuer residing in and doing business in that state is correct?

a. The offering would be exempt from the registration requirements of the Securities Act of 1933.

b. The offering would be subject to the registration requirements of the Securities Exchange Act of 1934.

c. The offering would be regulated by the SEC.

d. The shares of the offering could not be resold to investors outside the state for at least one year.

24. Pix Corp. is making a $6,000,000 stock offering. Pix wants the offering exempt from registration under the Securities Act of 1933. Which of the following requirements would Pix have to comply with when selling the securities?

a. No more than 35 investors.

b. No more than 35 nonaccredited investors.

c. Accredited investors only.

d. Nonaccredited investors only.

25. Which of the following transactions will be exempt from the full registration requirements of the Securities Act of 1933?

a. All intrastate offerings.

b. All offerings made under Regulation A.

c. Any resale of a security purchased under a Regulation D offering.

d. Any stockbroker transaction.

26. Under Rule 504 of Regulation D of the Securities Act of 1933, which of the following is (are) required?

I. No general offering or solicitation is permitted.

II. The issuer must restrict the purchasers’ right to resell the securities.

a. I only.

b. II only.

c. Both I and II.

d. Neither I nor II.

B. Securities Exchange Act of 1934

27. Dean, Inc., a publicly traded corporation, paid a $10,000 bribe to a local zoning official. The bribe was recorded in Dean’s financial statements as a consulting fee. Dean’s unaudited financial statements were submitted to the SEC as part of a quarterly filing. Which of the following federal statutes did Dean violate?

a. Federal Trade Commission Act.

b. Securities Act of 1933.

c. Securities Exchange Act of 1934.

d. North American Free Trade Act.

28. The Securities Exchange Commission promulgated Rule 10b-5 under Section 10(b) of the Securities Exchange Act of 1934. Which of the following is (are) purpose(s) of the Act?

29. Integral Corp. has assets in excess of $4 million, has 350 stockholders, and has issued common and preferred stock. Integral is subject to the reporting provisions of the Securities Exchange Act of 1934. For its 2008 fiscal year, Integral filed the following with the SEC: quarterly reports, an annual report, and a periodic report listing newly appointed officers of the corporation. Integral did not notify the SEC of stockholder “short swing” profits; did not report that a competitor made a tender offer to Integral’s stockholders; and did not report changes in the price of its stock as sold on the New York Stock Exchange. Under SEC reporting requirements, which of the following was Integral required to do?

a. Report the tender offer to the SEC.

b. Notify the SEC of stockholder “short swing” profits.

c. File the periodic report listing newly appointed officers.

d. Report the changes in the market price of its stock.

30. Which of the following factors, by itself, requires a corporation to comply with the reporting requirements of the Securities Exchange Act of 1934?

a. Six hundred employees.

b. Shares listed on a national securities exchange.

c. Total assets of $2 million.

d. Four hundred holders of equity securities.

31. The registration provisions of the Securities Exchange Act of 1934 require disclosure of all of the following information except the

a. Names of owners of at least 5% of any class of nonexempt equity security.

b. Bonus and profit-sharing arrangements.

c. Financial structure and nature of the business.

d. Names of officers and directors.

32. Under the Securities Act of 1933, which of the following statements is correct concerning a public issuer of securities who has made a registered offering?

a. The issuer is required to distribute an annual report to its stockholders.

b. The issuer is subject to the proxy rules of the SEC.

c. The issuer must file an annual report (Form 10-K) with the SEC.

d. The issuer is not required to file a quarterly report (Form 10-Q) with the SEC, unless a material event occurs.

33. Which of the following persons is not an insider of a corporation subject to the Securities Exchange Act of 1934 registration and reporting requirements?

a. An attorney for the corporation.

b. An owner of 5% of the corporation’s outstanding debentures.

c. A member of the board of directors.

d. A stockholder who owns 10% of the outstanding common stock.

34. The Securities Exchange Commission promulgated Rule 10b-5 from power it was given the Securities Exchange Act of 1934. Under this rule, it is unlawful for any person to use a scheme to defraud another in connection with the

| Purchase of any security | Sale of any security | |

| a. | Yes | Yes |

| b. | Yes | No |

| c. | No | Yes |

| d. | No | No |

35. The antifraud provisions of Rule 10b-5 of the Securities Exchange Act of 1934

a. Apply only if the securities involved were registered under either the Securities Act of 1933 or the Securities Exchange Act of 1934.

b. Require that the plaintiff show negligence on the part of the defendant in misstating facts.

c. Require that the wrongful act must be accomplished through the mail, any other use of interstate commerce, or through a national securities exchange.

d. Apply only if the defendant acted with intent to defraud.

Items 36 through 38 are based on the following:

Link Corp. is subject to the reporting provisions of the Securities Exchange Act of 1934.

36. Which of the following situations would require Link to be subject to the reporting provisions of the 1934 Act?

| Shares listed on a national securities exchange | More than one class of stock | |

| a. | Yes | Yes |

| b. | Yes | No |

| c. | No | Yes |

| d. | No | No |

37. Which of the following documents must Link file with the SEC?

| Quarterly reports (Form 10-Q) | Proxy Statements | |

| a. | Yes | Yes |

| b. | Yes | No |

| c. | No | Yes |

| d. | No | No |

38. Which of the following reports must also be submitted to the SEC?

| Report by any party making a tender offer to purchase Link’s stock | Report of proxy solicitations by Link stockholders | |

| a. | Yes | Yes |

| b. | Yes | No |

| c. | No | Yes |

| d. | No | No |

39. Which of the following events must be reported to the SEC under the reporting provisions of the Securities Exchange Act of 1934?

40. Adler, Inc. is a reporting company under the Securities Exchange Act of 1934. The only security it has issued is voting common stock. Which of the following statements is correct?

a. Because Adler is a reporting company, it is not required to file a registration statement under the Securities Act of 1933 for any future offerings of its common stock.

b. Adler need not file its proxy statements with the SEC because it has only one class of stock outstanding.

c. Any person who owns more than 10% of Adler’s common stock must file a report with the SEC.

d. It is unnecessary for the required annual report (Form 10-K) to include audited financial statements.

41. Which of the following is correct concerning financial statements in annual reports (Form 10-K) and quarterly reports (Form 10-Q)?

a. Both Form 10-K and Form 10-Q must be audited by independent public accountants and both must be filed with the SEC.

b. Both Form 10-K and Form 10-Q must be audited by independent public accountants but neither need be filed with the SEC.

c. Although both Form 10-K and Form 10-Q must be filed with the SEC, only Form 10-K need be audited by independent public accountants.

d. Form 10-K must be audited by independent public accountants and must also be filed with the SEC; however, Form 10-Q need not be audited by independent public accountants nor filed with the SEC.

42. Burk Corporation has issued securities that must be registered with the Securities Exchange Commission under the Securities Exchange Act of 1934. A material event took place yesterday, that is, there was a change in the control of Burk Corporation. Which of the following statements is correct?

a. Because of this material event, Burk Corporation is required to file with the SEC, Forms 10-K and 10-Q.

b. Because of this material event, Burk Corporation is required to file Form 8-K.

c. Burk Corporation need not file any forms with the SEC concerning this material event if the relevant facts are fully disclosed in the audited financial statements.

d. Burk Corporation need not file any form concerning the material event if Burk Corporation has an exemption under Rules 504, 505, or 506 of Regulation D.

C. The Sarbanes-Oxley Act of 2002

43. Under the Sarbanes-Oxley Act which of the following officers must periodically certify that reports comply fully with relevant securities laws and also fairly present the financial condition of company in all material aspects?

a. The chairman of the board and the chief executive officer.

b. The secretary and the chief executive officer.

c. The chief financial officer and the chief executive officer.

d. The chief risk officer and the chief executive officer.

D. The Wall Street Reform and Consumer Protection (Dodd-Frank) Act of 2010

44. Which of the following is not an aspect of the Wall Street Reform and Consumer Protection (Dodd-Frank) Act of 2010?

a. The act increased the regulation of insurance companies.

b. The act prohibits banks from engaging in proprietary trading.

c. The act puts limits on the compensation of corporate chief executive officers.

d. The act requires mortgage originators to retain an economic interest in a portion of the credit risk of any securitized asset that they create and sell.

45. The Wall Street Reform and Consumer Protection (Dodd-Frank) Act of 2010 requires

a. All members of the compensation committee of the board of directors to be independent.

b. All members of the corporate governance committee of the board of directors to be independent.

c. All voting members of the board of directors to be independent.

d. All members of the risk management committee of the board of directors to be independent.

Multiple-Choice Answers and Explanations

Answers

Explanations

1. (d) A preliminary prospectus is usually called a “red-herring” prospectus. The preliminary prospectus indicates that a registration statement has been filed but has not become effective.

2. (d) Securities include debentures, stocks, bonds, some notes, and investment contracts. The main idea is that the investor intends to make a profit on the investment through the efforts of others. A certificate of deposit is a type of commercial paper, not a security.

3. (d) A tombstone advertisement is allowed to inform potential investors that a prospectus for the given company is available. It is not an offer to sell or the solicitation of an offer to buy the securities. Answer (a) is incorrect because the tombstone ad informs potential purchasers of the prospectus and cannot be used as a substitute for the prospectus. Answer (b) is incorrect because it informs of the availability of the prospectus and cannot be construed as an offer to sell securities. Answer (c) is incorrect because the tombstone ad notifies potential purchasers of the prospectus. It does not notify that the securities have been withdrawn from the market.

4. (b) The registration of securities under the Securities Act of 1933 has as its purpose to provide potential investors with full and fair disclosure of all material information relating to the issuance of securities, including such information as the principal purposes for which the offering’s proceeds will be used. Answer (a) is incorrect because information on the stockholders of the offering corporation is not required to be reported. Answer (c) is incorrect because the SEC does not guarantee the accuracy of the registration statements. Answer (d) is incorrect because although the SEC does seek to compel full and fair disclosure, it does not evaluate the securities on merit or value, or give any assurances against loss.

5. (a) If no exemption is applicable under the Securities Act of 1933, public offerings must be registered with the SEC accompanied by a prospectus. Answer (b) is incorrect because the SEC does not pass on nor rate the securities. Answer (c) is incorrect because the prospectus is given to prospective purchasers of the securities. Answer (d) is incorrect because the SEC does not pass on the merits or accuracy of the prospectus.

6. (a) Notes are exempt securities under the Securities Act of 1933 if they have a maturity of nine months or less and if they are also used for commercial purposes rather than investments. The actual dollar amounts in the question are not a factor. The notes described in II are not exempt for two reasons; they have a maturity of two years and are used for investment purposes. The notes in III are not exempt because the maturity is two years even though they are for commercial purposes.

7. (d) Whether the securities are exempt from registration or not, they are still subject to the antifraud provisions of the Securities Act of 1933.

8. (d) The definition of a security is very broad under the Securities Act of 1933. The basic idea is that the investor intends to make a profit through the efforts of others rather than through his/her own efforts. Notes, bond certificates of interest, and debentures are all considered securities.

9. (b) If an issuer of securities wants to make an offering by using shelf registration, the actual issuance takes place over potentially a long period of time. Therefore, s/he must keep the original registration statement updated. There is no requirement that the offeror must be a first-time issuer of securities.

10. (d) Under the 1933 Act, certain securities are exempt. Although insurance and annuity contracts are exempt, securities issued by the insurance companies are not. Answer (a) is incorrect because securities of nonprofit organizations are exempt. Answer (b) is incorrect because securities issued by or guaranteed by domestic government organizations are exempt. Answer (c) is incorrect because securities issued by savings and loan associations are exempt.

11. (b) Securities exchanged for other securities by the issuer exclusively with its existing shareholders are exempt from registration under the 1933 Act as long as no commission is paid and both sets of securities are issued by the same issuer. Answer (a) is incorrect because nonvoting common stock is not exempted under the Act. The amount of the par value is irrelevant. Answer (c) is incorrect because although the securities of governments are themselves exempt, the limited partnership interests are not. Answer (d) is incorrect because no such exemption is allowed.

12. (d) Even though the issuer may comply with the Federal Securities Act of 1933, it must also comply with any applicable state “blue-sky” laws that regulate the securities at the state level. Answer (a) is incorrect because it is unlawful for the company to offer or sell the securities prior to the effective registration date. Answer (b) is incorrect because registration becomes effective on the twentieth day after filing unless the SEC issues a stop order. Answer (c) is incorrect because a prospectus is any notice, circular, advertisement, letter, or communication offering the security for sale. No general offering or solicitation is allowed under Rules 505 or 506 of Regulation D whether the purchaser is accredited or not.

13. (a) Even if the securities are exempt under the Securities Act of 1933, they are still subject to the antifraud provisions. Both the person defrauded and the SEC can challenge the fraud committed in the course of selling the securities.

14. (c) The SEC adopted the Forms S-2 and S-3 to decrease the work that issuers have in preparing registration statements by permitting them to give less detailed disclosure under certain conditions than Form S-1 which is the basic long form. Answer (a) is incorrect because these forms decrease, not increase, reporting required. Answer (b) is incorrect because when permitted, these forms are used instead of Form S-1 which is the standard long-form registration statement. Answer (d) is incorrect because the purpose of the forms was not directed at intrastate issues.

15. (c) The issuance described in I is exempt because Rule 504 exempts an issuance of securities up to $1,000,000 sold in a 12-month period to any number of investors. The issuer is not required to restrict the purchasers’ resale. The issuance described in II is also exempt because Rule 505 exempts an issuance up to $5,000,000 sold in a 12-month period. It permits sales to 35 unaccredited investors and to any number of accredited investors. Since there were only 10 investors, this is met. The issuer also restricted the purchasers’ right to resell for two years as required.

16. (d) Under Regulation D, Rule 504 exempts an issuance of securities up to $1,000,000 sold in a 12-month period. Rule 505 exempts an issuance of up to $5,000,000 in a 12-month period. So Rule 506 has to be resorted to for amounts over $5,000,000. Regulation A can be used only for issuances up to $1,500,000.

17. (d) When more than $5,000,000 in securities are being offered, an exemption from the registration requirements of the Securities Act of 1933 is available under Rule 506 of Regulation D. Securities under the Act include debentures and investment contracts.

18. (a) Under Regulation A of the 1933 Act, the issuer must file an offering circular with the SEC. Answer (b) is incorrect because the rules involving sales to unaccredited and accredited investors are in Regulation D, not Regulation A. Answer (c) is incorrect because although financial information about the corporation must be provided to offerees, the financial statements in the offering circular need not be audited. Answer (d) is incorrect because the issuer is not required to provide investors with a proxy registration statement under Regulation A.

19. (c) Sales or offers to sell by any person other than an issuer, underwriter, or dealer are exempt under the 1933 Act. Answer (a) is incorrect because the Act covers all types of securities including preferred stock. Answer (b) is incorrect because closely held corporations are not automatically exempt. Answer (d) is incorrect because debentures, as debt securities, are covered under the Act even if they are highly rated or backed by collateral.

20. (b) Regulation D of the Securities Act of 1933 establishes three important exemptions in Rules 504, 505, and 506. Although Rules 505 and 506 have some restrictions on sales to nonaccredited investors, all three rules under Regulation D allow sales to both nonaccredited and accredited investors with varying restrictions. Answer (a) is incorrect because although Rules 505 and 506 allow sales to up to 35 nonaccredited investors, all three rules allow sales to an unlimited number of accredited investors. Answer (c) is incorrect because Rule 506 has no dollar limitation. Rule 505 has a $5,000,000 limitation in a 12-month period and Rule 504 has a $1,000,000 limitation in a 12-month period. Answer (d) is incorrect because Regulation D is not restricted to only small corporations.

21. (c) Under Rule 505 of Regulation D, the issuer must notify the SEC of the offering within 15 days after the first sale of the securities. Answer (a) is incorrect because under Rule 505, the issuer may sell to an unlimited number of accredited investors and to 35 unaccredited investors. Answer (b) is incorrect because no general offering or solicitation is permitted. Answer (d) is incorrect because the accredited investors need not receive any formal information. The unaccredited investors, however, must receive a formal registration statement that gives a description of the offering.

22. (b) The private placement exemption permits sales of an unlimited number of securities for any dollar amount when sold to accredited investors. This exemption also allows sales to up to 35 nonaccredited investors if they are also sophisticated investors under the Act. Resales of these securities are restricted for two years after the date that the issuer sells the last of the securities. Answer (a) is incorrect because there is no such restriction of sale. Answer (c) is incorrect because sales may be made to an unlimited number of accredited investors and up to 35 nonaccredited investors. Answer (d) is incorrect because sales can be made to up to 35 nonaccredited investors.

23. (a) When the issuer is a resident of that state, doing 80% of its business in that state, and only sells or offers the securities to residents of the same state, the offering qualifies for an exemption under the 1933 Act as an intrastate issue. Answer (b) is incorrect as the offering also qualifies for an exemption under the 1934 Act. Therefore, as the offering is exempted from both the 1933 and 1934 Acts, it would not be regulated by the SEC. Answer (d) is incorrect because resales can only be made to residents of that state nine months after the issuer’s last sale.

24. (b) Rule 506 permits sales to 35 unaccredited investors and to an unlimited number of accredited investors. The unaccredited investors must also be sophisticated investors (i.e., individuals with knowledge and experience in financial matters).

25. (b) Under Regulation A, an offering statement is required instead of the more costly disclosure requirements of full registration under the Securities Act of 1933. Answer (a) is incorrect because not all intrastate offerings are exempt. They must meet specified requirements to be exempt. Answer (c) is incorrect because many securities sold under Regulation D cannot be resold for two years. Answer (d) is incorrect because there is no such exemption for stockbroker transactions.

26. (d) Under Rule 504 of Regulation D, general offerings and solicitations are permitted. Also, the issuer need not restrict the purchasers’ right to resell. Note that both I and II are requirements of Rules 505 and 506 of Regulation D.

27. (c) Under the Securities Exchange Act of 1934, issuers of securities registered under this Act must file quarterly reports (Form 10-Q) for the first three quarters of each fiscal year. The financial data in these may be unaudited; however, material misinformation is a violation of the 1934 Act. Answer (a) is incorrect—the Federal Trade Commission Act does not apply to this action. Answer (b) is incorrect because the Securities Act of 1933 applies to the initial issuance of securities and not to the secondary market of publicly traded securities. Answer (d) is incorrect because NAFTA is an agreement designed to promote free trade between the US, Mexico, and Canada.

28. (b) Purposes of Section 10(b) of the Securities Exchange Act of 1934 include deterring fraud in the securities industry and encouraging disclosure of relevant information so investors can make better decisions. The SEC does not rate the securities.

29. (c) Under the Securities Exchange Act of 1934, issuers of securities registered under this Act must file annual and quarterly reports with the SEC. The company must also file current reports covering certain material events such as a change in the amount of issued securities, a change in corporate control, or a change in newly appointed officers. Answer (a) is incorrect because a competitor’s making a tender offer need not be reported to the SEC. Answer (b) is incorrect because Integral Corp. need not notify the SEC of stockholder “short swing profits.” Answer (d) is incorrect because the company need not report information on the market price of its stock to the SEC. This market price information is already public information because the stock is traded on the New York Stock Exchange.

30. (b) Securities must be registered with the SEC if they are traded on any national securities exchange. Securities must also be registered if they are traded in interstate commerce where the corporation has more than $10 million in assets and 500 or more shareholders.

31. (a) The Securities Exchange Act of 1934 has registration provisions that require specified disclosures including bonus and profit-sharing arrangements, the financial structure and nature of this business, and names of officers and directors.

32. (c) Under the Federal Securities Act of 1933, which incorporates the filing requirements of the Federal Securities Exchange Act of 1934, the issuer must file with the SEC an annual report on Form 10-K. Answer (a) is incorrect because the issuer must file the annual report with the SEC but is not required to distribute it to its stockholders. Answer (b) is incorrect because the solicitation of proxies triggers certain proxy solicitation rules. Answer (d) is incorrect because it is the current report on Form 8-K that is filed when material events occur. The Form 10-Q is filed each of the first three quarters of each year and is known as the quarterly report.

33. (b) Under the 1934 Act, insiders include officers and directors of the corporation as well as owners of 10% or more of the stock of the corporation. Accountants, attorneys, and consultants can also be insiders subject to further regulation under the 1934 Act. Creditors, that is, owners of debentures are not considered to be insiders.

34. (a) Under Rule 10b-5, it is unlawful to use schemes to defraud in connection with the purchase or sale of any security. Note that this rule was made from powers given the SEC under the Securities Exchange Act of 1934, which applies to purchases in addition to sales of securities.

35. (c) For the Securities Exchange Act of 1934 to apply, including the antifraud provisions of Rule 10b-5, there must be shown a federal constitutional basis such as use of the mail, interstate commerce, or a national securities exchange. Answer (a) is incorrect because the antifraud provisions apply whether or not the securities had to be registered under either the 1933 Act or the 1934 Act. Answer (b) is incorrect because under Rule 10b-5, the plaintiff must prove more than negligence (i.e., either knowledge of falsity or reckless disregard for the truth in misstating facts). Answer (d) is incorrect because the plaintiff could recover if the defendant acted with reckless disregard for the truth.

36. (b) If the shares are listed on a national securities exchange, they are subject to the reporting provisions of the 1934 Act. There is no provision concerning a corporation owning more than one class of stock that by itself requires that it be subject to the reporting provisions of the 1934 Act.

37. (a) Under the 1934 Act, Link must file with the SEC annual reports (Form 10-K), quarterly reports (Form 10-Q), current reports (Form 8-K) of certain material events, and proxy statements when proxy solicitations exist.

38. (a) When there is a proxy solicitation, Link must make a report of this to the SEC. Also, reports of tender offers to purchase securities need to be submitted to the SEC.

39. (a) A tender offer is a request to the shareholders of a given company to tender their shares for a stated price. If the tender offer was unsolicited, the corporation must report this to the SEC under the reporting provisions of the Securities Exchange Act of 1934. Also, trading by insiders such as officers, directors, or shareholders owning at least 10% of the stock of a corporation registered with the SEC must also be reported to the SEC under the 1934 Act. Likewise, solicitation of proxies must be reported to the SEC.

40. (c) Under the Securities Exchange Act of 1934 which applies if interstate commerce or the mail is used, any purchaser of more than 5% of a class of equity securities must file a report with the SEC. Answer (d) is incorrect because the required annual report (Form 10-K) must be certified by independent public accountants. Answer (a) is incorrect because each company must also comply with the filing requirements under the Securities Act of 1933. Answer (b) is incorrect because there is no exemption from filing proxy statements simply because the company has only one class of stock.

41. (c) Forms 10-K (annual reports) and 10-Q (quarterly reports) must be filed with the SEC. Forms 10-K containing financial statements must be audited by independent public accountants. However, this is not true of Forms 10-Q which cover the first three fiscal quarters of each fiscal year of the issuer. The financial statements in 10-Qs must be reviewed by public accountants.

42. (b) When certain material events take place, such as a change in corporate control, the corporation covered under the 1934 Act must file Form 8-K, a current report, with the SEC within four days after the material event occurs. Answer (a) is incorrect because Burk Corporation must file Forms 10-K, annual reports, and Forms 10-Q, quarterly reports, whether or not a material event has taken place. Answer (c) is incorrect because there is no such exception provided. Answer (d) is incorrect because Rules 504, 505, and 506 under Regulation D apply to the initial issuance of securities under the Securities Act of 1933 and do not relieve Burk Corporation from the filing requirements with the SEC under the 1934 Act.

43. (c) The requirement is to identify the officers that must certify to financial reports under the Sarbanes-Oxley Act. Answer (c) is correct because the chief financial officer and the chief executive officer must certify.

44. (c) The requirement is to identify the item that is not an aspect of the Wall Street Reform and Consumer Protection Act of 2010. Answer (c) is correct because the act does not put limits on CEO compensation. Answers (a), (b), and (d) are incorrect because they are all aspects of the Dodd-Frank Act.

45. (a) The requirement is to identify the requirement of the Dodd-Frank Act of 2010. Answer (a) is correct because the Dodd-Frank Act requires all members of the compensation committee to be independent. Answers (b), (c), and (d) are incorrect because they are not requirements of the Act.

Simulations

Task-Based Simulation 1

Situation

You will have 15 questions based on the following information:

Butler Manufacturing Corp. planned to raise capital for a plant expansion by borrowing from banks and making several stock offerings. Butler engaged Weaver, CPA, to audit its December 31, 2009 financial statements. Butler told Weaver that the financial statements would be given to certain named banks and included in the prospectuses for the stock offerings.

In performing the audit, Weaver did not confirm accounts receivable and, as a result, failed to discover a material overstatement of accounts receivable. Also, Weaver was aware of a pending class action product liability lawsuit that was not disclosed in Butler’s financial statements. Despite being advised by Butler’s legal counsel that Butler’s potential liability under the lawsuit would result in material losses, Weaver issued an unqualified opinion on Butler’s financial statements.

In May 2010, Union Bank, one of the named banks, relied on the financial statements and Weaver’s opinion in giving Butler a $500,000 loan.

Butler raised an additional $16,450,000 through the following stock offerings, which were sold completely:

- June 2010—Butler made a $450,000 unregistered offering of Class B nonvoting common stock under Rule 504 of Regulation D of the Securities Act of 1933. This offering was sold over one year to 20 accredited investors by general solicitation. The SEC was notified eight days after the first sale of this offering.

- September 2010—Butler made a $10,000,000 unregistered offering of Class A voting common stock under Rule 506 of Regulation D of the Securities Act of 1933. This offering was sold over one year to 200 accredited investors and 30 nonaccredited investors through a private placement. The SEC was notified 14 days after the first sale of this offering.

- November 2010—Butler made a $6,000,000 unregistered offering of preferred stock under Rule 505 of Regulation D of the Securities Act of 1933. This offering was sold during a one-year period to forty nonaccredited investors by private placement. The SEC was notified 18 days after the first sale of this offering.

Shortly after obtaining the Union loan, Butler began experiencing financial problems but was able to stay in business because of the money raised by the offerings. Butler was found liable in the product liability suit. This resulted in a judgment Butler could not pay. Butler also defaulted on the Union loan and was involuntarily petitioned into bankruptcy. This caused Union to sustain a loss and Butler’s stockholders to lose their investments. As a result

- The SEC claimed that all three of Butler’s offerings were made improperly and were not exempt from registration.

- Union sued Weaver for

- Negligence

- Common Law Fraud

- The stockholders who purchased Butler’s stock through the offerings sued Weaver, alleging fraud under Section 10(b) and Rule 10b-5 of the Securities Exchange Act of 1934.

These transactions took place in a jurisdiction providing for accountant’s liability for negligence to known and intended users of financial statements.

Items 1 through 5 are questions related to the June 2010 offering made under Rule 504 of Regulation D of the Securities Act of 1933. For each item, indicate your answer by choosing either Yes or No.

| Yes | No | |

| 1. Did the offering comply with the dollar limitation of Rule 504? | ||

| 2. Did the offering comply with the method of sale restrictions? | ||

| 3. Was the offering sold during the applicable time limit? | ||

| 4. Was the SEC notified timely of the first sale of the securities? | ||

| 5. Was the SEC correct in claiming that this offering was not exempt from registration? |

Items 6 through 10 are questions related to the September 2010 offering made under Rule 506 of Regulation D of the Securities Act of 1933. For each item, indicate your answer by choosing either Yes or No.

| Yes | No | |

| 6. Did the offering comply with the dollar limitation of Rule 506? | ||

| 7. Did the offering comply with the method of sale restrictions? | ||

| 8. Was the offering sold to the correct number of investors? | ||

| 9. Was the SEC notified timely of the first sale of the securities? | ||

| 10. Was the SEC correct in claiming that this offering was not exempt from registration? | ||

| 10. Was the SEC correct in claiming that this offering was not exempt from registration? |

Items 11 through 15 are questions related to the November 2010 offering made under Rule 505 of Regulation D of the Securities Act of 1933. For each item, indicate your answer by choosing either Yes or No.

| Yes | No | |

| 11. Did the offering comply with the dollar limitation of Rule 505? | ||

| 12. Was the offering sold during the applicable time limit? | ||

| 13. Was the offering sold to the correct number of investors? | ||

| 14. Was the SEC notified timely of the first sale of the securities? | ||

| 15. Was the SEC correct in claiming that this offering was not exempt from registration? |

Task-Based Simulation 2

Situation

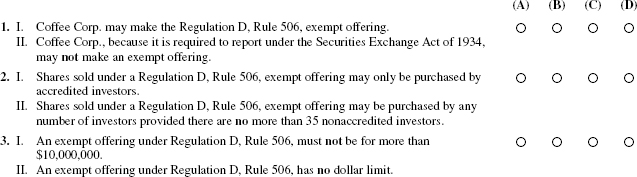

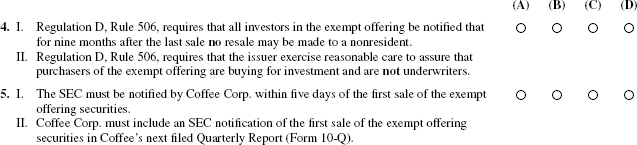

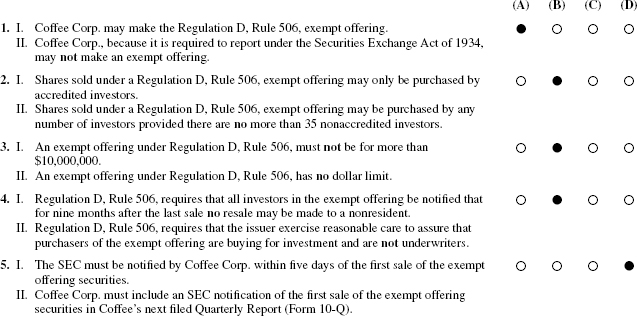

Coffee Corp., a publicly held corporation, wants to make an $8,000,000 exempt offering of its shares as a private placement offering under Regulation D, Rule 506, of the Securities Act of 1933. Coffee has more than 500 shareholders and assets in excess of $1 billion, and has its shares listed on a national securities exchange.

Items 1 through 5 relate to the application of the provisions of the Securities Act of 1933 and the Securities Exchange Act of 1934 to Coffee Corp. and the offering. For each item, select from List II whether only statement I is correct, whether only statement II is correct, whether both statements I and II are correct, or whether neither statement I nor II is correct.

List II

Simulation Solutions

Task-Based Simulation 1

| Yes | No | |

| 1. Did the offering comply with the dollar limitation of Rule 504? | ||

| 2. Did the offering comply with the method of sale restrictions? | ||

| 3. Was the offering sold during the applicable time limit? | ||

| 4. Was the SEC notified timely of the first sale of the securities? | ||

| 5. Was the SEC correct in claiming that this offering was not exempt from registration? |

Explanations

1. (Y) Rule 504 exempts an issuance of securities up to $1,000,000 sold in a 12-month period to any number of investors. Butler made the offering for $450,000.

2. (Y) This offering involved a general solicitation which is now allowed under Rule 504 providing the solicitation is to only accredited investors.

3. (Y) This offering was sold over the applicable 12-month period in Rule 504.

4. (Y) The SEC was sent notice of this offering eight days after the first sale. Under Rule 504, the SEC must be notified within 15 days of the first sale of the securities.

5. (N) Even though this stock was sold by general solicitation, this is allowed under Rule 504.

| Yes | No | |

| 6. Did the offering comply with the dollar limitation of Rule 506? | ||

| 7. Did the offering comply with the method of sale restrictions? | ||

| 8. Was the offering sold to the correct number of investors? | ||

| 9. Was the SEC notified timely of the first sale of the securities? | ||

| 10. Was the SEC correct in claiming that this offering was not exempt from registration? |

Explanations

6. (Y) Rule 506 allows private placement of an unlimited dollar amount of securities.

7. (Y) These securities were sold through private placement which is appropriate under Rule 506.

8. (Y) Rule 506 allows sales to up to 35 nonaccredited investors who are sophisticated investors with knowledge and experience in financial matters. It allows sales to an unlimited number of accredited investors.

9. (Y) The SEC was notified 14 days after the first sale of the offering which is within the 15-day rule.

10. (N) Since this offering met the requirements discussed in 6. through 9. above, the SEC was incorrect.

| Yes | No | |

| 11. Did the offering comply with the dollar limitation of Rule 505? | ||

| 12. Was the offering sold during the applicable time limit? | ||

| 13. Was the offering sold to the correct number of investors? | ||

| 14. Was the SEC notified timely of the first sale of the securities? | ||

| 15. Was the SEC correct in claiming that this offering was not exempt from registration? |

Explanations

11. (N) Rule 505 exempts an issuance of securities up to $5,000,000. Butler made a $6,000,000 unregistered offering of preferred stock.

12. (Y) The offering was sold during the applicable 12-month period.

13. (N) Rule 505 permits sales to 35 nonaccredited investors. Butler went over this limit by selling to 40 nonaccredited investors.

14. (N) The SEC was notified 18 days after the first sale of this offering which is over the 15-day requirement.

15. (Y) This offering was not exempt from registration because it went over the $5,000,000 limit and the stock was sold to more than 35 nonaccredited investors.

Task-Based Simulation 2

Explanations

1. (A) Statement I is correct because under Regulation D, Rule 506, the corporation may make a private placement of an unlimited amount of securities if it meets certain requirements. Statement II is incorrect. Coffee Corp. may still make an exempt offering under the Securities Act of 1933 even if it will be subject to the requirements of the Securities Exchange Act of 1934.

2. (B) Statement I is incorrect because up to 35 nonaccredited investors may purchase shares under Regulation D, Rule 506, if they are sophisticated investors. Statement II is correct because Rule 506 does allow sales to up to 35 nonaccredited investors assuming they are also sophisticated investors, that is, individuals with knowledge and experience in financial matters, or individuals represented by people with such knowledge and experience.

3. (B) Statement I is incorrect and Statement II is correct for the same reason. Regulation D, Rule 506, has no dollar limit on the placement of securities as long as other requirements are met.

4. (B) Statement I is incorrect because Regulation D has no requirements putting restrictions on resales to nonresidents. Statement II is correct because Regulation D requires that the issuer take reasonable steps to see that purchasers of the exempt offering are not underwriters and are buying for investment.

5. (D) Statement I is incorrect. Under Regulation D, the SEC must be notified within fifteen days of the first sale of the securities. Statement II is incorrect because the Quarterly Reports do not require SEC notification of the first sale of exempt securities.