CHAPTER 6

UNDERSTANDING CASH FLOW STATEMENTS

After completing this chapter, you will be able to do the following:

- Compare cash flows from operating, investing, and financing activities and classify cash flow items as relating to one of those three categories given a description of the items.

- Describe how noncash investing and financing activities are reported.

- Contrast cash flow statements prepared under International Financial Reporting Standards (IFRS) and U.S. generally accepted accounting principles (U.S. GAAP).

- Distinguish between the direct and indirect methods of presenting cash from operating activities and describe the arguments in favor of each method.

- Describe how the cash flow statement is linked to the income statement and the balance sheet.

- Describe the steps in the preparation of direct and indirect cash flow statements, including how cash flows can be computed using income statement and balance sheet data.

- Convert cash flows from the indirect to direct method.

- Analyze and interpret both reported and common-size cash flow statements.

- Calculate and interpret free cash flow to the firm, free cash flow to equity, and performance and coverage cash flow ratios.

- Cash flow activities are classified into three categories: operating activities, investing activities, and financing activities. Significant noncash transaction activities (if present) are reported by using a supplemental disclosure note to the cash flow statement.

- Cash flow statements under IFRS and U.S. GAAP are similar; however, IFRS provide companies with more choices in classifying some cash flow items as operating, investing, or financing activities.

- Companies can use either the direct or the indirect method for reporting their operating cash flow:

- The direct method discloses operating cash inflows by source (e.g., cash received from customers, cash received from investment income) and operating cash outflows by use (e.g., cash paid to suppliers, cash paid for interest) in the operating activities section of the cash flow statement.

- The indirect method reconciles net income to operating cash flow by adjusting net income for all noncash items and the net changes in the operating working capital accounts.

- The cash flow statement is linked to a company’s income statement and comparative balance sheets and to data on those statements.

- Although the indirect method is most commonly used by companies, an analyst can generally convert it to an approximation of the direct format by following a simple three-step process.

- An evaluation of a cash flow statement should involve an assessment of the sources and uses of cash and the main drivers of cash flow within each category of activities.

- The analyst can use common-size statement analysis for the cash flow statement. Two approaches to developing the common-size statements are the total cash inflows/total cash outflows method and the percentage of net revenues method.

- The cash flow statement can be used to determine free cash flow to the firm (FCFF) and free cash flow to equity (FCFE).

- The cash flow statement may also be used in financial ratios that measure a company’s profitability, performance, and financial strength.

1. The three major classifications of activities in a cash flow statement are

A. inflows, outflows, and net flows.

B. operating, investing, and financing.

C. revenues, expenses, and net income.

2. The sale of a building for cash would be classified as what type of activity on the cash flow statement?

A. Operating

B. Investing

C. Financing

3. Which of the following is an example of a financing activity on the cash flow statement under U.S. GAAP?

A. Payment of interest

B. Receipt of dividends

C. Payment of dividends

4. A conversion of a face value $1 million convertible bond for $1 million of common stock would most likely be

A. reported as a $1 million investing cash inflow and outflow.

B. reported as a $1 million financing cash outflow and inflow.

C. reported as supplementary information to the cash flow statement.

5. Interest paid is classified as an operating cash flow

A. under U.S. GAAP but may be classified as either operating or investing cash flows under IFRS.

B. under IFRS but may be classified as either operating or investing cash flows under U.S. GAAP.

C. under U.S. GAAP but may be classified as either operating or financing cash flows under IFRS.

6. Cash flows from taxes on income

A. must be separately disclosed under IFRS only.

B. must be separately disclosed under U.S. GAAP only.

C. must be separately disclosed under both IFRS and U.S GAAP.

7. Which of the following components of the cash flow statement may be prepared under the indirect method under both IFRS and U.S. GAAP?

A. Operating

B. Investing

C. Financing

8. Which of the following is most likely to appear in the operating section of a cash flow statement under the indirect method?

A. Net income

B. Cash paid to suppliers

C. Cash received from customers

9. Red Road Company, a consulting company, reported total revenues of $100 million, total expenses of $80 million, and net income of $20 million in the most recent year. If accounts receivable increased by $10 million, how much cash did the company receive from customers?

A. $90 million

B. $100 million

C. $110 million

10. Green Glory Corp., a garden supply wholesaler, reported cost of goods sold for the year of $80 million. Total assets increased by $55 million, including an increase of $5 million in inventory. Total liabilities increased by $45 million, including an increase of $2 million in accounts payable. The cash paid by the company to its suppliers is most likely closest to:

A. $73 million.

B. $77 million.

C. $83 million.

11. Purple Fleur S.A., a retailer of floral products, reported cost of goods sold for the year of $75 million. Total assets increased by $55 million, but inventory declined by $6 million. Total liabilities increased by $45 million, and accounts payable increased by $2 million. The cash paid by the company to its suppliers is most likely closest to:

A. $67 million.

B. $79 million.

C. $83 million.

12. White Flag, a women’s clothing manufacturer, reported salaries expense of $20 million. The beginning balance of salaries payable was $3 million, and the ending balance of salaries payable was $1 million. How much cash did the company pay in salaries?

A. $18 million

B. $21 million

C. $22 million

13. An analyst gathered the following information from a company’s 2010 financial statements (in $ millions):

| Year Ended 31 December | 2009 | 2010 |

| Net sales | 245.8 | 254.6 |

| Cost of goods sold | 168.3 | 175.9 |

| Accounts receivable | 73.2 | 68.3 |

| Inventory | 39.0 | 47.8 |

| Accounts payable | 20.3 | 22.9 |

Based only on the information given here, the company’s 2010 statement of cash flows in the direct format would include amounts (in $ millions) for cash received from customers and cash paid to suppliers, respectively, that are closest to:

| Cash Received from Customers | Cash Paid to Suppliers | |

| A. | 249.7 | 169.7 |

| B. | 259.5 | 174.5 |

| C. | 259.5 | 182.1 |

14. Golden Cumulus Corp., a commodities trading company, reported interest expense of $19 million and taxes of $6 million. Interest payable increased by $3 million, and taxes payable decreased by $4 million over the period. How much cash did the company pay for interest and taxes?

A. $22 million for interest and $10 million for taxes

B. $16 million for interest and $2 million for taxes

C. $16 million for interest and $10 million for taxes

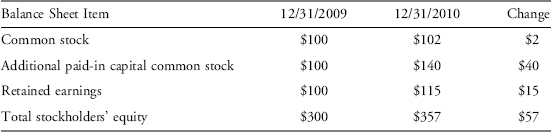

15. An analyst gathered the following information from a company’s 2010 financial statements (in $ millions):

| Balances as of Year Ended 31 December | 2009 | 2010 |

| Retained earnings | 120 | 145 |

| Accounts receivable | 38 | 43 |

| Inventory | 45 | 48 |

| Accounts payable | 36 | 29 |

In 2010, the company declared and paid cash dividends of $10 million and recorded depreciation expense in the amount of $25 million. The company considers dividends paid a financing activity. The company’s 2010 cash flow from operations (in $ millions) was closest to

A. 25.

B. 45.

C. 75.

16. Silverago Incorporated, an international metals company, reported a loss on the sale of equipment of $2 million in 2010. In addition, the company’s income statement shows depreciation expense of $8 million and the cash flow statement shows capital expenditure of $10 million, all of which was for the purchase of new equipment. Using the following information from the comparative balance sheets, how much cash did the company receive from the equipment sale?

A. $1 million

B. $2 million

C. $3 million

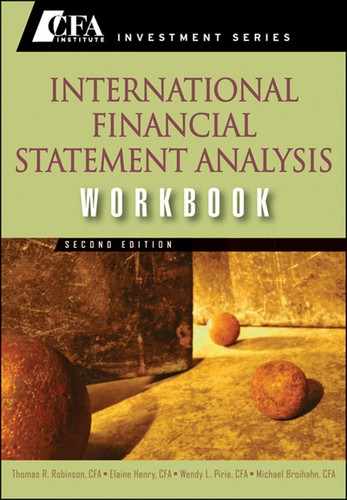

17. Jaderong Plinkett Stores reported net income of $25 million. The company has no outstanding debt. Using the following information from the comparative balance sheets (in millions), what should the company report in the financing section of the statement of cash flows in 2010?

A. Issuance of common stock of $42 million; dividends paid of $10 million

B. Issuance of common stock of $38 million; dividends paid of $10 million

C. Issuance of common stock of $42 million; dividends paid of $40 million

18. Based on the following information for Star Inc., what are the total net adjustments that the company would make to net income in order to derive operating cash flow?

A. Add $2 million

B. Add $6 million

C. Subtract $6 million

19. The first step in cash flow statement analysis should be to

A. evaluate consistency of cash flows.

B. determine operating cash flow drivers.

C. identify the major sources and uses of cash.

20. Which of the following would be valid conclusions from an analysis of the cash flow statement for Telefónica Group presented in Exhibit 6-3 in the text?

A. The primary use of cash is financing activities.

B. The primary source of cash is operating activities.

C. Telefónica classifies interest received as an operating activity.

21. Which is an appropriate method of preparing a common-size cash flow statement?

A. Show each item of revenue and expense as a percentage of net revenue.

B. Show each line item on the cash flow statement as a percentage of net revenue.

C. Show each line item on the cash flow statement as a percentage of total cash outflows.

22. Which of the following is an appropriate method of computing free cash flow to the firm?

A. Add operating cash flows to capital expenditures and deduct after-tax interest payments.

B. Add operating cash flows to after-tax interest payments and deduct capital expenditures.

C. Deduct both after-tax interest payments and capital expenditures from operating cash flows.

23. An analyst has calculated a ratio using as the numerator the sum of operating cash flow, interest, and taxes and as the denominator the amount of interest. What is this ratio, what does it measure, and what does it indicate?

A. This ratio is an interest coverage ratio, measuring a company’s ability to meet its interest obligations and indicating a company’s solvency.

B. This ratio is an effective tax ratio, measuring the amount of a company’s operating cash flow used for taxes and indicating a company’s efficiency in tax management.

C. This ratio is an operating profitability ratio, measuring the operating cash flow generated accounting for taxes and interest and indicating a company’s liquidity.