CHAPTER 17

INTEGRATION OF FINANCIAL STATEMENT ANALYSIS TECHNIQUES

After completing this chapter, you will be able to do the following:

- Demonstrate the use of a framework for the analysis of financial statements given a particular problem, question, or purpose (e.g., valuing equity based on comparables, critiquing a credit rating, obtaining a comprehensive picture of financial leverage, evaluating the perspectives given in management’s discussion of financial results).

- Identify financial reporting choices and biases that affect the quality and comparability of companies’ financial statements, and illustrate how such biases affect financial decisions.

- Evaluate the quality of a company’s financial data, and recommend appropriate adjustments to improve quality and comparability with similar companies, including adjustments for differences in accounting rules, methods, and assumptions.

- Predict the impact on financial statements and ratios, given a change in accounting rules, methods, or assumptions.

- Analyze and interpret the effects of balance sheet modifications, earnings normalization, and cash flow statement related modifications on a company’s financial statements, financial ratios, and overall financial condition.

The three case studies demonstrate the use of financial analysis in decision making. Each case is set in a different type of industry: manufacturing, service, and financial service. The different focus, purpose, and context for each analysis result in different techniques and tools being applied to the analysis. However, each case demonstrates the use of a common financial statement analysis framework. In each case, an economic decision is arrived at; this is consistent with the primary reason for performing financial analysis: to facilitate an economic decision.

The following information relates to Questions 1 through 8.

Sergei Leenid, CFA, is a long-only fixed income portfolio manager for the Parliament Funds. He has developed a quantitative model, based on financial statement data, to predict changes in the credit ratings assigned to corporate bond issues. Before applying the model, Leenid first performs a screening process to exclude bonds that fail to meet certain criteria relative to their credit rating. Existing holdings that fail to pass the initial screen are individually reviewed for potential disposition. Bonds that pass the screening process are evaluated using the quantitative model to identify potential rating changes.

Leenid is concerned that a pending change in accounting rules could affect the results of the initial screening process. One current screen excludes bonds when the financial leverage ratio (equity multiplier) exceeds a given level and/or the interest coverage ratio falls below a given level for a given bond rating. For example, any “A”-rated bond of a company with a financial leverage ratio exceeding 2.0 or an interest coverage ratio below 6.0 would fail the initial screening. The failing bonds are eliminated from further analysis using the quantitative model.

The new accounting rule would require substantially all leases to be capitalized on a company’s balance sheets. To test whether the change in accounting rules will affect the output of the screening process, Leenid collects a random sample of “A”-rated bonds issued by companies in the retail industry, which he believes will be among the industries most affected by the change.

Two of the companies, Silk Road Stores and Colorful Concepts, recently issued bonds with similar terms and interest rates. Leenid decides to thoroughly analyze the potential effects of the change on these two companies and begins by gathering information from their most recent annual financial statements (Exhibit A).

EXHIBIT A Selected Financial Data for Silk Road Stores and Colorful Concepts

| Silk Road | Colorful Concepts | |

| Revenue | 3,945 | 7,049 |

| EBIT | 318 | 865 |

| Interest expense | 21 | 35 |

| Income taxes | 121 | 302 |

| Net income | 176 | 528 |

| Average total assets | 2,075 | 3,844 |

| Average total equity | 1,156 | 2,562 |

| Lease expense | 213 | 406 |

After examining lease disclosures, Leenid estimates the average lease term for each company at eight years with a fairly consistent lease expense over that time. He believes the leases should be capitalized using 6.5%, the rate at which both companies recently issued bonds.

While examining the balance sheet for Colorful Concepts, Leenid also discovers that the company has a 204 ending asset balance (188 beginning) for investments in associates, primarily due to its 20% interest in the equity of Exotic Imports. Exotic Imports is a specialty retail chain and in the most recent year reported 1,230 in sales, 105 in net income, and had average total assets of 620.

1. If the accounting rules were to change, Silk Road’s assets would increase by approximately:

A. 1,297.

B. 1,576.

C. 1,704.

2. If the accounting rules were to change, Silk Road’s interest coverage ratio would be closest to:

A. 3.03.

B. 3.50.

C. 5.04.

3. If the accounting rules were to change, Silk Road’s financial leverage ratio would be closest to:

A. 1.37.

B. 1.79.

C. 2.92.

4. Will the change in accounting rules impact the result of the initial screening process for Colorful Concepts?

A. It passes the screens now, but will not pass if the accounting rules change.

B. It passes the screens now and will continue to pass if the accounting rules change.

C. It fails the screens now and will continue to fail if the accounting rules change.

5. Based on Leenid’s analysis of the results of the initial screening, relative to Colorful Concepts the bond rating of Silk Road should be:

A. lower.

B. higher.

C. the same.

6. Ignoring the potential impact of any accounting change and excluding the investment in associates, the net profit margin for Colorful Concepts would be closest to:

A. 6.0%.

B. 7.2%.

C. 7.5%.

7. Ignoring the impact of any accounting change, the asset turnover ratio for Colorful Concepts excluding the investments in associates would:

A. stay the same.

B. increase by 0.10.

C. decrease by 0.10.

8. Excluding the investments in associates would result in the interest coverage ratio for Colorful Concepts being:

A. lower.

B. higher.

C. the same.

The following information relates to Questions 9 through 15.

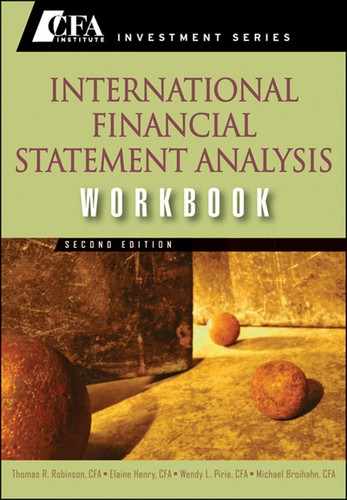

Quentin Abay, CFA, is an analyst for a private equity firm interested in purchasing Bickchip Enterprises, a conglomerate. His first task is to determine the trends in ROE and the main drivers of the trends using DuPont analysis. To do so he gathers the data in Exhibit B.

EXHIBIT B Selected Financial Data for Bickchip Enterprises

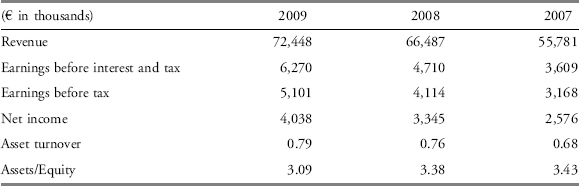

After conducting the DuPont analysis, Abay believes that his firm could increase the ROE without operational changes. Further, Abay thinks that ROE could improve if the company divested segments that were generating the lowest returns on capital employed (total assets less noninterest-bearing liabilities). Segment EBIT margins in 2009 were 11% for Automation Equipment, 5% for Power and Industrial, and 8% for Medical Equipment. Other relevant segment information is presented in Exhibit C.

EXHIBIT C Segment Data for Bickchip Enterprises (€ thousands)

Abay is also concerned with earnings quality, so he intends to calculate Bickchip’s cash-flow-based accruals ratio and the ratio of operating cash flow before interest and taxes to operating income. To do so, he prepares the information in Exhibit D.

EXHIBIT D Earnings Quality Data for Bickchip Enterprises (€ in thousands)

9. Over the three-year period presented in Exhibit B, Bickchip’s return on equity is best described as:

A. stable.

B. trending lower.

C. trending higher.

10. Based on the DuPont analysis, Abay’s belief regarding ROE is most likely based on:

A. leverage.

B. profit margins.

C. asset turnover.

11. Based on Abay’s criteria, the business segment best suited for divestiture is:

A. medical equipment.

B. power and industrial.

C. automation equipment.

12. Bickchip’s cash-flow-based accruals ratio in 2009 is closest to:

A. 9.9%.

B. 13.4%.

C. 23.3%.

13. The cash-flow-based accruals ratios from 2007 to 2009:

A. indicate improving earnings quality.

B. indicate deteriorating earnings quality.

C. indicate no change in earnings quality.

14. The ratio of operating cash flow before interest and taxes to operating income for Bickchip for 2009 is closest to:

A. 1.6.

B. 1.9.

C. 2.1.

15. Based on the ratios for operating cash flow before interest and taxes to operating income, Abay should conclude that:

A. Bickchip’s earnings are backed by cash flow.

B. Bickchip’s earnings are not backed by cash flow.

C. Abay can draw no conclusion due to the changes in the ratios over time.

The following information relates to Questions 16 through 21.

Michael Wetstone is an equity analyst covering the software industry for a public pension fund. Prior to comparing the financial results of Software Services Inc. and PDQ GmbH, Wetstone discovers the need to make adjustments to their respective financial statements. The issues preventing comparability, using the financial statements as reported, are the sale of receivables and the impact of minority interests.

Software Services sold $267.5 million of finance receivables to a special purpose entity. PDQ does not securitize finance receivables. An abbreviated balance sheet for Software Services is presented in Exhibit E.

EXHIBIT E Abbreviated Balance Sheet for Software Services ($ 000)

| Year Ending | 31 December 2009 |

| Total Current Assets | $1,412,900 |

| Total Assets | $3,610,600 |

| Total Current Liabilities | $1,276,300 |

| Total Liabilities | $2,634,100 |

| Total Equity | $976,500 |

A significant portion of PDQ’s net income is explained by its 20% minority interest in Astana Systems. Wetstone collects certain data (Exhibit F) related to both PDQ and Astana in order to estimate the financials of PDQ on a stand-alone basis.

EXHIBIT F Selected Financial Data Related to PDQ and Astana Systems

| PDQ (€ in 000) | Astana ($ in 000) | |

| Earnings before tax (2009) | €41,730 | $15,300 |

| Income taxes (2009) | 13,562 | 5,355 |

| Net income (2009) | 28,168 | 9,945 |

| Market capitalization (recent) | 563,355 | 298,350 |

| Average $/€ exchange rate in 2009 | 1.55 | |

| Current $/€ exchange rate | 1.62 |

16. Compared to holding securitized finance receivables on the balance sheet, treating them as sold had the effect of reducing Software Services’ reported financial leverage by:

A. 6.8%.

B. 7.4%.

C. 9.2%.

17. Had the securitized finance receivables been held on the balance sheet, Software Services’ ratio of liabilities to total capital would have been closest to:

A. 73.0%.

B. 74.8%.

C. 80.4%.

18. How much of PDQ’s value can be explained by its equity stake in Astana?

A. 6.5%.

B. 10.6%.

C. 20.0%.

19. On a “solo” basis, PDQ’s P/E ratio is closest to:

A. 19.6.

B. 21.0.

C. 24.5.

20. The adjusted financial statements were created during which phase of the financial analysis process?

A. Data collection.

B. Data processing.

C. Data interpretation.

21. The estimate of PDQ’s solo value is crude because of:

A. the potential differences in accounting standards used by PDQ and Astana.

B. the differing risk characteristics of PDQ and Astana.

C. differences in liquidity and market efficiency where PDQ and Astana trade.