CHAPTER 10

LONG-LIVED ASSETS

1. B is correct. Only costs necessary for the machine to be ready to use can be capitalized. Therefore, Total capitalized costs=12,980+1,200+700+100=$14,980.

2. A is correct. Borrowing costs can be capitalized under IFRS until the tangible asset is ready for use. Also, under IFRS, income earned on temporarily investing the borrowed monies decreases the amount of borrowing costs eligible for capitalization. Therefore, Total capitalized interest=(500 million×14%×2 years) − 10 million=130 million.

3. B is correct. A product patent with a defined expiration date is an intangible asset with a finite useful life. A copyright with no expiration date is an intangible asset with an indefinite useful life. Goodwill is no longer considered an intangible asset under IFRS and is considered to have an indefinite useful life.

4. C is correct. An intangible asset with a finite useful life is amortized, whereas an intangible asset with an indefinite useful life is not.

5. A is correct. If the company uses the straight-line method, the depreciation expense will be one-fifth (20 percent) of the depreciable cost in Year 1. If it uses the units-of-production method, the depreciation expense will be 19 percent (2,000/10,500) of the depreciable cost in Year 1. Therefore, if the company uses the straight-line method, its depreciation expense will be higher and its net income will be lower.

6. C is correct. If Martinez wants to minimize tax payments in the first year of the machine’s life, he should use an accelerated method, such as the double-declining balance method.

7. A is correct. Using the straight-line method, depreciation expense amounts to

![]()

8. B is correct. Using the units-of-production method, depreciation expense amounts to

![]()

9. A is correct. The straight-line method is the method that evenly distributes the cost of an asset over its useful life because amortization is the same amount every year.

10. A is correct. A higher residual value results in a lower total depreciable cost and, therefore, a lower amount of amortization in the first year after acquisition (and every year after that).

11. B is correct. Using the straight-line method, accumulated amortization amounts to

![]()

12. B is correct. Using the units-of-production method, depreciation expense amounts to

![]()

13. B is correct. In this case, the value increase brought about by the revaluation should be recorded directly in equity. The reason is that under IFRS, an increase in value brought about by a revaluation can only be recognized as a profit to the extent that it reverses a revaluation decrease of the same asset previously recognized in the income statement.

14. B is correct. The impairment loss equals £3,100,000.

15. B is correct. The result on the sale of the vehicle equals

16. A is correct. Gain or loss on the sale = Sale proceeds − Carrying amount. Rearranging this equation, Sale proceeds=Carrying amount+Gain or loss on sale. Thus, Sale price=(12 million − 2 million)+(–3.2 million)=6.8 million.

17. B is correct. IFRS do not require acquisition dates to be disclosed.

18. A is correct. IFRS do not require fair value of intangible assets to be disclosed.

19. B is correct. Investment property earns rent. Investment property and property, plant, and equipment are tangible and long-lived.

20. C is correct. When a company uses the fair value model to value investment property, changes in the fair value of the property are reported in the income statement—not in other comprehensive income.

21. A is correct. Investment property earns rent. Inventory is held for resale, and property, plant, and equipment are used in the production of goods and services.

22. C is correct. A company will change from the fair value model to either the cost model or revaluation model when the company transfers investment property to property, plant, and equipment.

23. C is correct. Expensing rather than capitalizing an investment in long-term assets will result in higher expenses and lower net income and net profit margin in the current year. Future years’ incomes will not include depreciation expense related to these expenditures. Consequently, year-to-year growth in profitability will be higher. If the expenses had been capitalized, the carrying amount of the assets would have been higher and the 2009 total asset turnover would have been lower.

24. C is correct. In 2010, switching to an accelerated depreciation method would increase depreciation expense and decrease income before taxes, taxes payable, and net income. Cash flow from operating activities would increase because of the resulting tax savings.

25. B is correct. 2009 net income and net profit margin are lower because of the impairment loss. Consequently, net profit margins in subsequent years are likely to be higher. An impairment loss suggests that insufficient depreciation expense was recognized in prior years, and net income was overstated in prior years. The impairment loss is a noncash item and will not affect operating cash flows.

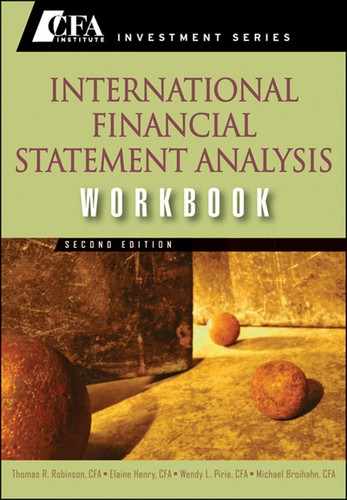

26. A is correct. The estimated average remaining useful life is 20.75 years.

27. A is correct. When leases are classified as finance leases, the lessee initially reports an asset and liability at a carrying amount equal to the lower of the fair value of the leased asset or the present value of the future lease payments. Under an operating lease, the lessee does not report an asset or liability. Therefore, total asset turnover (Total revenue÷Average total assets) would be lower if the leases were classified as finance leases.

28. C is correct. Total liabilities-to-assets would be higher. When leases are classified as finance leases, the lessee initially reports an asset and liability at a carrying amount equal to the lower of the fair value of the leased asset or the present value of the future lease payments. Both the numerator and denominator would increase by an equal amount, but the proportional increase in the numerator is higher and the ratio would be higher. The following exhibit shows what would happen to 2009 total liabilities, assets, and total liabilities-to-assets if €200 million, the fair value of the leased equipment, is added to AMRC’s total liabilities and assets. This simple example ignores the impact of accounting for the 2009 lease payment.

| 2009 Actual Under Operating Lease | 2009 Hypothetical Under Finance Lease | |

| Total liabilities | €2,750 | €2,950 |

| Total assets | €5,350 | €5,550 |

| Total liabilities-to-assets | 51.4% | 53.2% |

The depreciation and interest expense under a finance lease tends to be higher than the operating lease payment in the early years of the lease. The finance lease would result in lower net income and net profit margin. Long-lived (fixed) assets are higher under a finance lease and fixed asset turnover is lower.

29. C is correct. The decision to capitalize the costs of the new computer system results in higher cash flow from operating activities; the expenditure is reported as an outflow of investing activities. The company allocates the capitalized amount over the asset’s useful life as depreciation or amortization expense rather than expensing it in the year of expenditure. Net income and total assets are higher in the current fiscal year.

30. B is correct. Alpha’s fixed asset turnover will be lower because the capitalized interest will appear on the balance sheet as part of the asset being constructed. Therefore, fixed assets will be higher and the fixed asset turnover ratio (Total revenue/Average net fixed assets) will be lower than if it had expensed these costs. Capitalized interest appears on the balance sheet as part of the asset being constructed instead of being reported as interest expense in the period incurred. However, the interest coverage ratio should be based on interest payments, not interest expense (Earnings before interest and taxes/Interest Payments), and should be unchanged. To provide a true picture of a company’s interest coverage, the entire amount of interest expenditure, both the capitalized portion and the expensed portion, should be used in calculating interest coverage ratios.

31. C is correct. The cash flow from operating activities will be lower, not higher, because the full lease payment is treated as an operating cash outflow. With a finance lease, only the portion of the lease payment relating to interest expense potentially reduces operating cash outflows. A company reporting a lease as an operating lease will typically show higher profits in early years, because the lease expense is less than the sum of the interest and depreciation expense. The company reporting the lease as an operating lease will typically report stronger solvency and activity ratios.

32. A is correct. Accelerated depreciation will result in an improving, not declining, net profit margin over time, because the amount of depreciation expense declines each year. Under straight-line depreciation, the amount of depreciation expense will remain the same each year. Under the units-of-production method, the amount of depreciation expense reported each year varies with the number of units produced.

33. B is correct. The estimated average total useful life of a company’s assets is calculated by adding the estimates of the average remaining useful life and the average age of the assets. The average age of the assets is estimated by dividing accumulated depreciation by depreciation expense. The average remaining useful life of the asset base is estimated by dividing net property, plant, and equipment by annual depreciation expense.

34. C is correct. The impairment loss is a noncash charge and will not affect cash flow from operating activities. The debt to total assets and fixed asset turnover ratios will increase, because the impairment loss will reduce the carrying amount of fixed assets and therefore total assets.

35. A is correct. In an asset revaluation, the carrying amount of the assets increases. The increase in the asset’s carrying amount bypasses the income statement and is reported as other comprehensive income and appears in equity under the heading of revaluation surplus. Therefore, shareholders’ equity will increase but net income will not be affected, so return on equity will decline. Return on assets and debt to capital ratios will also decrease.