CHAPTER 11

INCOME TAXES

After completing this chapter, you will be able to do the following:

- Describe the differences between accounting profit and taxable income, and define key terms, including deferred tax assets, deferred tax liabilities, valuation allowance, taxes payable, and income tax expense.

- Explain how deferred tax liabilities and assets are created and the factors that determine how a company’s deferred tax liabilities and assets should be treated for the purposes of financial analysis.

- Determine the tax base of a company’s assets and liabilities.

- Calculate income tax expense, income taxes payable, deferred tax assets, and deferred tax liabilities, and calculate and interpret the adjustment to the financial statements related to a change in the income tax rate.

- Evaluate the impact of tax rate changes on a company’s financial statements and ratios.

- Distinguish between temporary and permanent differences in pretax accounting income and taxable income.

- Describe the valuation allowance for deferred tax assets—when it is required and what impact it has on financial statements.

- Compare a company’s deferred tax items.

- Analyze disclosures relating to deferred tax items and the effective tax rate reconciliation, and explain how information included in these disclosures affects a company’s financial statements and financial ratios.

- Identify the key provisions of and differences between income tax accounting under IFRS and U.S. GAAP.

- Differences between the recognition of revenue and expenses for tax and accounting purposes may result in taxable income differing from accounting profit. The discrepancy is a result of different treatments of certain income and expenditure items.

- The tax base of an asset is the amount that will be deductible for tax purposes as an expense in the calculation of taxable income as the company expenses the tax basis of the asset. If the economic benefit will not be taxable, the tax base of the asset will be equal to the carrying amount of the asset.

- The tax base of a liability is the carrying amount of the liability less any amounts that will be deductible for tax purposes in the future. With respect to revenue received in advance, the tax base of such a liability is the carrying amount less any amount of the revenue that will not be taxable in the future.

- Temporary differences arise from recognition of differences in the tax base and carrying amount of assets and liabilities. The creation of a deferred tax asset or liability as a result of a temporary difference will only be allowed if the difference reverses itself at some future date and to the extent that it is expected that the balance sheet item will create future economic benefits for the company.

- Permanent differences result in a difference in tax and financial reporting of revenue (expenses) that will not be reversed at some future date. Because it will not be reversed at a future date, these differences do not constitute temporary differences and do not give rise to a deferred tax asset or liability.

- Current taxes payable or recoverable are based on the applicable tax rates on the balance sheet date of an entity; in contrast, deferred taxes should be measured at the tax rate that is expected to apply when the asset is realized or the liability settled.

- All unrecognized deferred tax assets and liabilities must be reassessed on the appropriate balance sheet date and measured against their probable future economic benefit.

- Deferred tax assets must be assessed for their prospective recoverability. If it is probable that they will not be recovered at all or partly, the carrying amount should be reduced. Under U.S. GAAP, this is done through the use of a valuation allowance.

1. Using the straight-line method of depreciation for reporting purposes and accelerated depreciation for tax purposes would most likely result in a:

A. valuation allowance.

B. deferred tax asset.

C. temporary difference.

2. In early 2009 Sanborn Company must pay the tax authority €37,000 on the income it earned in 2008. This amount was recorded on the company’s 31 December 2008 financial statements as:

A. taxes payable.

B. income tax expense.

C. a deferred tax liability.

3. Income tax expense reported on a company’s income statement equals taxes payable, plus the net increase in:

A. deferred tax assets and deferred tax liabilities.

B. deferred tax assets, less the net increase in deferred tax liabilities.

C. deferred tax liabilities, less the net increase in deferred tax assets.

4. Analysts should treat deferred tax liabilities that are expected to reverse as:

A. equity.

B. liabilities.

C. neither liabilities nor equity.

5. Deferred tax liabilities should be treated as equity when:

A. they are not expected to reverse.

B. the timing of tax payments is uncertain.

C. the amount of tax payments is uncertain.

6. When both the timing and amount of tax payments are uncertain, analysts should treat deferred tax liabilities as:

A. equity.

B. liabilities.

C. neither liabilities nor equity.

7. When accounting standards require recognition of an expense that is not permitted under tax laws, the result is a:

A. deferred tax liability.

B. temporary difference.

C. permanent difference.

8. When certain expenditures result in tax credits that directly reduce taxes, the company will most likely record:

A. a deferred tax asset.

B. a deferred tax liability.

C. no deferred tax asset or liability.

9. When accounting standards require an asset to be expensed immediately but tax rules require the item to be capitalized and amortized, the company will most likely record:

A. a deferred tax asset.

B. a deferred tax liability.

C. no deferred tax asset or liability.

10. A company incurs a capital expenditure that may be amortized over five years for accounting purposes, but over four years for tax purposes. The company will most likely record:

A. a deferred tax asset.

B. a deferred tax liability.

C. no deferred tax asset or liability.

11. A company receives advance payments from customers that are immediately taxable but will not be recognized for accounting purposes until the company fulfills its obligation. The company will most likely record:

A. a deferred tax asset.

B. a deferred tax liability.

C. no deferred tax asset or liability.

The following information relates to Questions 12 through 14.

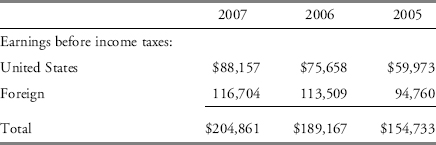

Note I: Income Taxes

The components of earnings before income taxes are as follows ($ thousands):

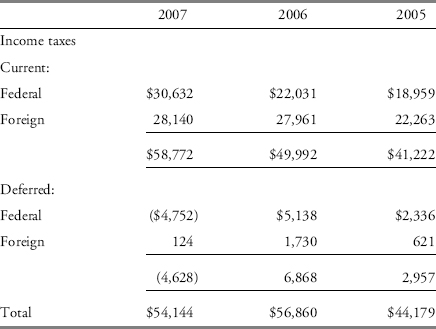

The components of the provision for income taxes are as follows ($ thousands):

12. In 2007, the company’s U.S. GAAP income statement recorded a provision for income taxes closest to:

A. $30,632.

B. $54,144.

C. $58,772.

13. The company’s effective tax rate was highest in:

A. 2005.

B. 2006.

C. 2007.

14. Compared to the company’s effective tax rate on U.S. income, its effective tax rate on foreign income was:

A. lower in each year presented.

B. higher in each year presented.

C. higher in some periods and lower in others.

15. Zimt AG presents its financial statements in accordance with U.S. GAAP. In 2007, Zimt discloses a valuation allowance of $1,101 against total deferred tax assets of $19,201. In 2006, Zimt disclosed a valuation allowance of $1,325 against total deferred tax assets of $17,325. The change in the valuation allowance most likely indicates that Zimt’s:

A. deferred tax liabilities were reduced in 2007.

B. expectations of future earning power has increased.

C. expectations of future earning power has decreased.

16. Cinnamon, Inc. recorded a total deferred tax asset in 2007 of $12,301, offset by a $12,301 valuation allowance. Cinnamon most likely:

A. fully utilized the deferred tax asset in 2007.

B. has an equal amount of deferred tax assets and deferred tax liabilities.

C. expects not to earn any taxable income before the deferred tax asset expires.

The following information relates to Questions 17 through 19.

The tax effects of temporary differences that give rise to deferred tax assets and liabilities are as follows ($ thousands):

| 2007 | 2006 | |

| Deferred tax assets: | ||

| Accrued expenses | $8,613 | $7,927 |

| Tax credit and net operating loss carry-forwards | 2,288 | 2,554 |

| LIFO and inventory reserves | 5,286 | 4,327 |

| Other | 2,664 | 2,109 |

| Deferred tax assets | 18,851 | 16,917 |

| Valuation allowance | (1,245) | (1,360) |

| Net deferred tax assets | $17,606 | $15,557 |

| Deferred tax liabilities: | ||

| Depreciation and amortization | $(27,338) | $(29,313) |

| Compensation and retirement plans | (3,831) | (8,963) |

| Other | (1,470) | (764) |

| Deferred tax liabilities | (32,639) | (39,040) |

| Net deferred tax liability | ($15,033) | ($23,483) |

17. A reduction in the statutory tax rate would most likely benefit the company’s:

A. income statement and balance sheet.

B. income statement but not the balance sheet.

C. balance sheet but not the income statement.

18. If the valuation allowance had been the same in 2007 as it was in 2006, the company would have reported $115 higher:

A. net income.

B. deferred tax assets.

C. income tax expense.

19. Compared to the provision for income taxes in 2007, the company’s cash tax payments were:

A. lower.

B. higher.

C. the same.

The following information relates to Questions 20 through 22.

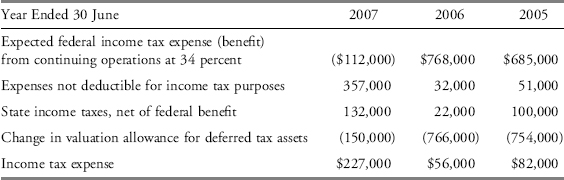

A company’s provision for income taxes resulted in effective tax rates attributable to loss from continuing operations before cumulative effect of change in accounting principles that varied from the statutory federal income tax rate of 34 percent, as summarized in the following table.

20. In 2007, the company’s net income (loss) was closest to:

A. ($217,000).

B. ($329,000).

C. ($556,000).

21. The $357,000 adjustment in 2007 most likely resulted in:

A. an increase in deferred tax assets.

B. an increase in deferred tax liabilities.

C. no change to deferred tax assets and liabilities.

22. Over the three years presented, changes in the valuation allowance for deferred tax assets were most likely indicative of:

A. decreased prospects for future profitability.

B. increased prospects for future profitability.

C. assets being carried at a higher value than their tax base.