CHAPTER 14

INTERCORPORATE INVESTMENTS

After completing this chapter, you will be able to do the following:

- Describe the classification, measurement, and disclosure under International Financial Reporting Standards (IFRS) for (1) investments in financial assets, (2) investments in associates, (3) joint ventures, (4) business combinations, and (5) special purpose and variable interest entities.

- Distinguish between IFRS and U.S. GAAP in the classification, measurement, and disclosure of investments in financial assets, investments in associates, joint ventures, business combinations, and special purpose and variable interest entities.

- Analyze effects on financial statements and ratios of different methods used to account for intercorporate investments.

- Investments in financial assets are those in which the investor has no significant influence. They can be designated as held-to-maturity investments, held for trading securities, or available-for-sale securities. IFRS and U.S. GAAP treat investments in financial assets in a similar manner.

- Held-to-maturity investments are carried at cost.

- Held for trading securities are carried at fair value; unrealized gains and losses are reported on the profit or loss (income) statement.

- Available-for-sale securities are carried at fair value; unrealized gains and losses are reported in other comprehensive income in the equity section of the balance sheet.

- Gains or losses on investments designated as fair value are reported on the profit and loss (income) statement.

- Both IFRS and U.S. GAAP allow investments that would be classified as either held-to-maturity or available-for-sale to be carried at fair value, with unrealized losses reported in profit or loss (income statement).

- Investments in associates are those in which the investor has significant influence, but not control, over the investee’s business activities. Because the investor can exert significant influence over financial and operating policy decisions, IFRS and U.S. GAAP require the equity method of accounting because it provides a more objective basis for reporting investment income.

- The equity method requires the investor to recognize income as earned rather than when dividends are received.

- The equity investment is carried at cost, plus its share of postacquisition income (after adjustments) less dividends received.

- The equity investment is reported as a single line item on the balance sheet and on the income statement.

- Joint ventures are entities owned and operated by a small group of investors with shared common control. IFRS and U.S. GAAP apply different standards to joint ventures. IFRS favor proportionate consolidation, which requires the venturer’s share of the assets, liabilities, income, and expenses of the joint venture to be combined on a line-by-line basis with similar items in the venturer’s financial statements. However, IFRS does allow the use of the equity method to account for jointly controlled entities. U.S. GAAP requires the equity method accounting for joint ventures.

- Business combinations can be structured as mergers, acquisitions, or consolidations under U.S. GAAP. IFRS makes no such distinction among business combinations.

- An acquisition allows for the legal continuity for each of the combining companies. Both companies continue as separate entities through a parent–subsidiary relationship.

- If the acquiring company acquires less than 100 percent, noncontrolling (minority) shareholders’ interests are reported on the consolidated financial statements.

- Consolidated financial statements are prepared in each reporting period.

- Current IFRS and U.S. GAAP accounting standards require the use of the acquisition method to account for business combinations. Fair value is the appropriate measurement for identifiable assets and liabilities acquired in the business combination. If the acquisition is less than 100 percent, IFRS allow the noncontrolling interest to be measured at either its fair value (full goodwill) or at the noncontrolling interest’s proportionate share of the acquiree’s identifiable net assets (partial goodwill). U.S. GAAP requires the noncontrolling interest to be measured at fair value (full goodwill).

- Goodwill is the difference between the acquisition value and the fair value of the target’s identifiable net tangible and intangible assets. Because it is considered to have an indefinite life, it is not amortized. Instead, it is evaluated at least annually for impairment. Impairment losses are reported on the income statement. IFRS use a one-step approach to determine and measure the impairment loss, whereas U.S. GAAP use a two-step approach.

- Special purpose (SPEs) and variable interest entities (VIEs) are required to be consolidated by the entity which is expected to absorb the majority of the expected losses or receive the majority of expected residual benefits.

- U.S. GAAP has eliminated the use of qualified special purpose entities resulting in a convergence with IFRS over the accounting treatment of SPEs.

The following information relates to Questions 1 through 6.

Cinnamon, Inc. is a diversified manufacturing company headquartered in the United Kingdom. It complies with IFRS. In 2009, Cinnamon held a 19 percent passive equity ownership interest in Cambridge Processing that was classified as available-for-sale. During the year, the value of this investment rose by £2 million. In December 2009, Cinnamon announced that it would be increasing its ownership interest to 50 percent effective 1 January 2010 through a cash purchase. Cinnamon and Cambridge have no intercompany transactions.

Peter Lubbock, an analyst following both Cinnamon and Cambridge, is curious how the increased stake will affect Cinnamon’s consolidated financial statements. He asks Cinnamon’s CFO how the company will account for the investment, and is told that the decision has not yet been made. Lubbock decides to use his existing forecasts for both companies’ financial statements to compare the outcomes of alternative accounting treatments.

Lubbock assembles abbreviated financial statement data for Cinnamon (Exhibit A) and Cambridge (Exhibit B) for this purpose.

EXHIBIT A Selected Financial Statement Information for Cinnamon, Inc. (£ in millions)

| Year Ending 31 December | 2009 | 2010* |

| Revenue | 1,400 | 1,575 |

| Operating income | 126 | 142 |

| Net income | 62 | 69 |

| 31 December | 2009 | 2010* |

| Total assets | 1,170 | 1,317 |

| Shareholders’ equity | 616 | 685 |

* Estimates made prior to announcement of increased stake in Cambridge.

EXHIBIT B Selected Financial Statement Information for Cambridge Processing (£ in millions)

| Year Ending 31 December | 2009 | 2010* |

| Revenue | 1,000 | 1,100 |

| Operating income | 80 | 88 |

| Net income | 40 | 44 |

| Dividends paid | 20 | 22 |

| 31 December | 2009 | 2010 |

| Total assets | 800 | 836 |

| Shareholders’ equity | 440 | 462 |

* Estimates made prior to announcement of increased stake by Cinnamon.

1. In 2009, Cinnamon’s earnings before taxes includes a contribution (in £ millions) from its investment in Cambridge Processing that is closest to:

A. £3.8.

B. £5.8.

C. £7.6.

2. In 2010, if Cinnamon is deemed to have control over Cambridge, it will most likely account for its investment in Cambridge using:

A. the equity method.

B. the acquisition method.

C. proportionate consolidation.

3. At 31 December 2010, Cinnamon’s shareholders’ equity on its balance sheet would most likely be:

A. highest if Cinnamon is deemed to have control of Cambridge.

B. independent of the accounting method used for the investment in Cambridge.

C. highest if Cinnamon is deemed to have significant influence over Cambridge.

4. In 2010, Cinnamon’s net profit margin would be highest if:

A. it is deemed to have control of Cambridge.

B. it had not increased its stake in Cambridge.

C. it is deemed to have significant influence over Cambridge.

5. At 31 December 2010, assuming control and recognition of goodwill, Cinnamon’s reported debt to equity ratio will most likely be highest if it accounts for its investment in Cambridge using the:

A. equity method.

B. full goodwill method.

C. partial goodwill method.

6. Compared to Cinnamon’s operating margin in 2009, if it is deemed to have control of Cambridge, its operating margin in 2010 will most likely be:

A. lower.

B. higher.

C. the same.

The following information relates to Questions 7 through 12.

Zimt, AG is a consumer products manufacturer headquartered in Austria. It complies with IFRS. In 2009, Zimt held a 10 percent passive stake in Oxbow Limited that was classified as held for trading securities. During the year, the value of this stake declined by €3 million. In December 2009, Zimt announced that it would be increasing its ownership to 50 percent effective 1 January 2010.

Franz Gelblum, an analyst following both Zimt and Oxbow, is curious how the increased stake will affect Zimt’s consolidated financial statements. Because Gelblum is uncertain how the company will account for the increased stake, he uses his existing forecasts for both companies’ financial statements to compare various alternative outcomes.

Gelblum gathers abbreviated financial statement data for Zimt (Exhibit C) and Oxbow (Exhibit D) for this purpose.

EXHIBIT C Selected Financial Statement Estimates for Zimt AG (€ in millions)

| Year Ending 31 December | 2009 | 2010* |

| Revenue | 1,500 | 1,700 |

| Operating income | 135 | 153 |

| Net income | 66 | 75 |

| 31 December | 2009 | 2010 |

| Total assets | 1,254 | 1,421 |

| Shareholders’ equity | 660 | 735 |

* Estimates made prior to announcement of increased stake in Oxbow.

EXHIBIT D Selected Financial Statement Estimates for Oxbow Limited (€ in millions)

| Year Ending 31 December | 2009 | 2010* |

| Revenue | 1,200 | 1,350 |

| Operating income | 120 | 135 |

| Net income | 60 | 68 |

| Dividends paid | 20 | 22 |

| 31 December | 2009 | 2010 |

| Total assets | 1,200 | 1,283 |

| Shareholders’ equity | 660 | 706 |

* Estimates made prior to announcement of increased stake by Zimt.

7. In 2009, Zimt’s earnings before taxes includes a contribution (in € millions) from its investment in Oxbow Limited closest to:

A. (€0.6).

B. (€1.0).

C. €2.0.

8. At 31 December 2010, Zimt’s total assets balance would most likely be:

A. highest if Zimt is deemed to have control of Oxbow.

B. highest if Zimt is deemed to have significant influence over Oxbow.

C. unaffected by the accounting method used for the investment in Oxbow.

9. Based on Gelblum’s estimates, if Zimt is deemed to have significant influence over Oxbow, its 2010 net income (in € millions) would be closest to:

A. €75.

B. €109.

C. €143.

10. Based on Gelblum’s estimates, if Zimt is deemed to have joint control of Oxbow, and Zimt uses the proportionate consolidation method, its 31 December 2010 total liabilities (in € millions) will most likely be closest to:

A. €686.

B. €975.

C. €1,263.

11. Based on Gelblum’s estimates, if Zimt is deemed to have control over Oxbow, its 2010 consolidated sales (in € millions) will be closest to:

A. €1,700.

B. €2,375.

C. €3,050.

12. Based on Gelblum’s estimates, Zimt’s net income in 2010 will most likely be:

A. highest if Zimt is deemed to have control of Oxbow.

B. highest if Zimt is deemed to have significant influence over Oxbow.

C. independent of the accounting method used for the investment in Oxbow.

The following information relates to Questions 13 through 18.

Burton Howard, CFA, is an equity analyst with Maplewood Securities. Howard is preparing a research report on Confabulated Materials, SA, a publicly traded company based in France that complies with IFRS. As part of his analysis, Howard has assembled data gathered from the financial statement footnotes of Confabulated’s 2009 Annual Report and from discussions with company management. Howard is concerned about the effect of this information on Confabulated’s future earnings.

Information about Confabulated’s investment portfolio for the years ended 31 December 2008 and 2009 is presented in Exhibit E. As part of his research, Howard is considering the possible effect on reported income of Confabulated’s accounting classification for fixed income investments.

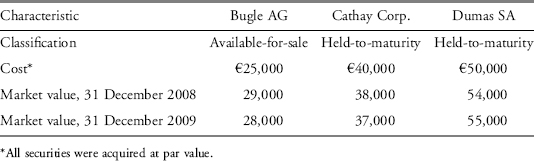

EXHIBIT E Confabulated’s Investment Portfolio (€ thousands)

In addition, Confabulated’s annual report discusses a transaction under which receivables were securitized through a special purpose entity (SPE) for Confabulated’s benefit.

13. The balance sheet carrying value of Confabulated’s investment portfolio (in € thousands) at 31 December 2009 is closest to:

A. 112,000.

B. 115,000.

C. 118,000.

14. The balance sheet carrying value of Confabulated’s investment portfolio at 31 December 2009 would have been higher if which of the securities had been reclassified as a held for trading security?

A. Bugle.

B. Cathay.

C. Dumas.

15. Compared to Confabulated’s reported interest income in 2009, if Dumas had been classified as available-for-sale, the interest income would have been:

A. lower.

B. the same.

C. higher.

16. Compared to Confabulated’s reported earnings before taxes in 2009, if Bugle had been classified as a held for trading security, the earnings before taxes (in € thousands) would have been:

A. the same.

B. €1,000 lower.

C. €3,000 higher.

17. Confabulated’s reported interest income would be lower if the cost was the same but the par value (in € thousands) of:

A. Bugle was €28,000.

B. Cathay was €37,000.

C. Dumas was €55,000.

18. Confabulated’s special purpose entity is most likely to be:

A. held off-balance sheet.

B. consolidated on Confabulated’s financial statements.

C. consolidated on Confabulated’s financial statements only if it is a “qualifying SPE.”

The following information relates to Questions 19 through 24.

BetterCare Hospitals, Inc. operates a chain of hospitals throughout the United States. The company has been expanding by acquiring local hospitals. Its largest acquisition, that of Statewide Medical, was made in 2001 under the pooling of interests method. BetterCare complies with U.S. GAAP.

BetterCare is currently forming a 50/50 joint venture with Supreme Healthcare under which the companies will share control of several hospitals. BetterCare plans to use the equity method to account for the joint venture. Supreme Healthcare complies with IFRS and will use the proportionate consolidation method to account for the joint venture.

Erik Ohalin is an equity analyst who covers both companies. He has estimated the joint venture’s financial information for 2010 in order to prepare his estimates of each company’s earnings and financial performance. This information is presented in Exhibit F.

EXHIBIT F Selected Financial Statement Forecasts for Joint Venture ($ in millions)

| Year Ending 31 December | 2010 |

| Revenue | 1,430 |

| Operating income | 128 |

| Net income | 62 |

| 31 December | 2010 |

| Total assets | 1,500 |

| Shareholders’ equity | 740 |

Supreme Healthcare recently announced it had formed a special purpose entity through which it plans to sell up to $100 million of its accounts receivable. Supreme Healthcare has no voting interest in the SPE, but it is expected to absorb any losses that it may incur. Ohalin wants to estimate the impact this will have on Supreme Healthcare’s consolidated financial statements.

19. Compared to accounting principles currently in use, the pooling method BetterCare used for its Statewide Medical acquisition has most likely caused its reported:

A. revenue to be higher.

B. total equity to be lower.

C. total assets to be higher.

20. Based on Ohalin’s estimates, the amount of joint venture revenue (in $ millions) included on BetterCare’s consolidated 2010 financial statements should be closest to:

A. $0.

B. $715.

C. $1,430.

21. Based on Ohalin’s estimates, the amount of joint venture net income included on the consolidated financial statements of each venturer will most likely be:

A. higher for BetterCare.

B. higher for Supreme Healthcare.

C. the same for both BetterCare and Supreme Healthcare.

22. Based on Ohalin’s estimates, the amount of the joint venture’s 31 December 2010 total assets (in $ millions) that will be included on Supreme Healthcare’s consolidated financial statements will be closest to:

A. $0.

B. $750.

C. $1,500.

23. Based on Ohalin’s estimates, the amount of joint venture shareholders’ equity at 31 December 2010 included on the consolidated financial statements of each venturer will most likely be:

A. higher for BetterCare.

B. higher for Supreme Healthcare.

C. the same for both BetterCare and Supreme Healthcare.

24. If Supreme Healthcare sells its receivables to the SPE, its consolidated financial results will most likely show:

A. a higher revenue for 2010.

B. the same cash balance at 31 December 2010.

C. the same accounts receivable balance at 31 December 2010.

The following information relates to Questions 25 through 30.

Percy Byron, CFA, is an equity analyst with a U.K.-based investment firm. One firm Byron follows is NinMount PLC, a U.K.-based company. On 31 December 2008, NinMount paid £320 million to purchase a 50 percent stake in Boswell Company. The excess of the purchase price over the fair value of Boswell’s net assets was attributable to previously unrecorded licenses. These licenses were estimated to have an economic life of six years. The fair value of Boswell’s assets and liabilities other than licenses was equal to their recorded book values. NinMount and Boswell both use the pound sterling as their reporting currency and prepare their financial statements in accordance with IFRS.

Byron is concerned whether the investment should affect his “buy” rating on NinMount common stock. He knows NinMount could choose one of several accounting methods to report the results of its investment, but NinMount has not announced which method it will use. Byron forecasts that both companies’ 2009 financial results (excluding any merger accounting adjustments) will be identical to those of 2008.

NinMount’s and Boswell’s condensed income statements for the year ended 31 December 2008, and condensed balance sheets at 31 December 2008, are presented in Exhibits G and H, respectively.

EXHIBIT G NinMount PLC and Boswell Company Income Statements for the Year Ended 31 December 2008 (£ in millions)

| NinMount | Boswell | |

| Net sales | 950 | 510 |

| Cost of goods sold | (495) | (305) |

| Selling expenses | (50) | (15) |

| Administrative expenses | (136) | (49) |

| Depreciation & amortization expense | (102) | (92) |

| Interest expense | (42) | (32) |

| Income before taxes | 125 | 17 |

| Income tax expense | (50) | (7) |

| Net income | 75 | 10 |

EXHIBIT H NinMount PLC and Boswell Company Balance Sheets at 31 December 2008 (£ in millions)

| NinMount | Boswell | |

| Cash | 50 | 20 |

| Receivables—net | 70 | 45 |

| Inventory | 130 | 75 |

| Total current assets | 250 | 140 |

| Property, plant, & equipment—net | 1,570 | 930 |

| Investment in Boswell | 320 | — |

| Total assets | 2,140 | 1,070 |

| Current liabilities | 110 | 90 |

| Long-term debt | 600 | 400 |

| Total liabilities | 710 | 490 |

| Common stock | 850 | 535 |

| Retained earnings | 580 | 45 |

| Total equity | 1,430 | 580 |

| Total liabilities and equity | 2,140 | 1,070 |

Note: Balance sheets reflect the purchase price paid by NinMount, but do not yet consider the impact of the accounting method choice.

25. NinMount’s current ratio on 31 December 2008 most likely will be highest if the results of the acquisition are reported using:

A. the equity method.

B. consolidation with full goodwill.

C. consolidation with partial goodwill.

26. NinMount’s long-term debt to equity ratio on 31 December 2008 most likely will be lowest if the results of the acquisition are reported using:

A. the equity method.

B. consolidation with full goodwill.

C. consolidation with partial goodwill.

27. Based on Byron’s forecast, if NinMount deems it has acquired control of Boswell, NinMount’s consolidated 2009 depreciation and amortization expense (in £ millions) will be closest to:

A. 102.

B. 148.

C. 204.

28. Based on Byron’s forecast, NinMount’s net profit margin for 2009 most likely will be highest if the results of the acquisition are reported using:

A. the equity method.

B. consolidation with full goodwill.

C. consolidation with partial goodwill.

29. Based on Byron’s forecast, NinMount’s 2009 return on beginning equity most likely will be the same under:

A. either of the consolidations, but different under the equity method.

B. the equity method, consolidation with full goodwill, and consolidation with partial goodwill.

C. none of the equity method, consolidation with full goodwill, or consolidation with partial goodwill.

30. Based on Byron’s forecast, NinMount’s 2009 total asset turnover ratio on beginning assets under the equity method is most likely:

A. lower than if the results are reported using consolidation.

B. the same as if the results are reported using consolidation.

C. higher than if the results are reported using consolidation.