CHAPTER 15

MULTINATIONAL OPERATIONS

1. B is correct. IAS 21 requires that the financial statements of the foreign entity first be restated for local inflation using the procedures outlined in IAS 29, “Financial Reporting in Hyperinflationary Economies.” Then, the inflation-restated foreign currency financial statements are translated into the parent’s presentation currency using the current exchange rate. Under U.S. GAAP, the temporal method would be used with no restatement.

2. C is correct. Ruiz expects the euro to appreciate against the hryvnia (UAH) and expects some inflation in the Ukraine. In an inflationary environment, FIFO will generate a higher gross profit than weighted average cost. For either inventory choice, the current rate method will give higher gross profit to the parent company if the subsidiary’s currency is depreciating. Thus, using FIFO and translating using the current rate method will generate a higher gross profit for the parent company, Eurexim SA, than any other combination of choices.

3. B is correct. If the parent’s currency is chosen as the functional currency, the temporal method must be used. Under the temporal method, fixed assets are translated using the rate in effect at the time they were acquired.

4. C is correct. Monetary assets and liabilities such as accounts receivable are translated at current (end-of-period) rates regardless of whether the temporal or current rate method is being used.

5. B is correct. When the foreign currency is chosen as the functional currency, the current rate method is used. All assets and liabilities are translated at the current (end-of-period) rate.

6. B is correct. When the foreign currency is chosen as the functional currency, the current rate method must be used and all gains or losses from translation are reported as a cumulative translation adjustment to shareholder equity. When the foreign currency decreases in value (weakens), the current rate method results in a negative translation adjustment in stockholders’ equity.

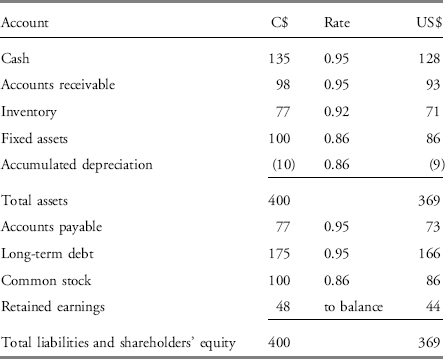

7. B is correct. When the parent’s currency is used as the functional currency, the temporal method must be used to translate the subsidiary’s accounts. Under the temporal method, monetary assets and liabilities (e.g., debt) are translated at the current (year-end) rate, nonmonetary assets and liabilities measured at historical cost (e.g., inventory) are translated at historical exchange rates, and nonmonetary assets and liabilities measured at current value are translated at the exchange rate at the date when the current value was determined. Because beginning inventory was sold first and sales and purchases were evenly acquired, the average rate is most appropriate for translating inventory and $77 × 0.92=$71. Long-term debt is translated at the year-end rate of $0.95. $175 × 0.95=$166.

8. B is correct. Translating the 2007 balance sheet using the temporal method, as is required here, results in assets of $369 million. The translated liabilities and common stock amount to $325 million, meaning that the value for 2007 retained earnings is: $369 million − $325 million=$44 million.

Temporal Method (2007)

9. C is correct. The Canadian dollar would be the appropriate reporting currency when substantially all operating, financing, and investing decisions are based on the local currency. The parent country’s inflation rate is never relevant. Earnings manipulation is not justified, and at any rate, changing the functional currency would take the gains off of the income statement.

10. C is correct. If the functional currency was changed from the parent currency (U.S. dollar) to the local currency (Canadian dollar), the current rate method would replace the temporal method. The temporal method ignores unrealized gains and losses on nonmonetary assets and liabilities, but the current rate method does not.

11. B is correct. If the Canadian currency is chosen as the functional currency, the current rate method will be used and the current exchange rate will be the rate used to translate all assets and liabilities. Currently, only monetary assets and liabilities are translated at the current rate. Sales are translated at the average rate during the year under either method. Fixed assets are translated using the historical rate under the temporal method but would switch to current rates under the current rate method. Therefore, there will most likely be an effect on sales/fixed assets. Because the cash ratio involves only monetary assets and liabilities it is unaffected by the translation method. Receivables turnover pairs a monetary asset with sales and is thus also unaffected.

12. B is correct. If the functional currency were changed, then Consol-Can would use the current rate method and the balance sheet exposure would be equal to net assets (total assets − total liabilities). In this case, 400 − 77 − 175=148.

13. B is correct. Julius is using the current rate method, which is most appropriate when it is operating with a high degree of autonomy.

14. A is correct. If the current rate method is being used (as it is for Julius), the local currency (euro) is the functional currency. When the temporal method is being used (as it is for Augustus), the parent currency (U.S. dollar) is the functional currency.

15. C is correct. When the current rate method is being used, all currency gains and losses are recorded as a cumulative translation adjustment to shareholder equity.

16. C is correct. Under the current rate method, all assets are translated using the year-end 2008 (current) rate of $1.61/€1.00. €2,300 × 1.61=$3,703.

17. A is correct. Under the current rate method, both sales and cost of goods sold would be translated at the 2008 average exchange rate. The ratio would be the same as reported under the euro. €2,300 − €1,400=€900, €900/€2300=39.1 percent. Or, $3,542 − $2,156=$1,386, $1,386/$3,542=39.1 percent.

18. C is correct. Augustus is using the temporal method in conjunction with FIFO inventory accounting. If FIFO is used, ending inventory is assumed to be composed of the most recently acquired items and thus inventory will be translated at relatively recent exchange rates. To the extent that the average weight used to translate sales differs from the historical rate used to translate inventories, the gross margin will be distorted when translated into U.S. dollars.

19. C is correct. If the U.S. dollar is the functional currency, the temporal method must be used. Revenues and receivables (monetary asset) would be the same under either accounting method. Inventory and fixed assets were purchased when the U.S. dollar was stronger, so at historical rates (temporal method), translated they would be lower. Identical revenues/lower fixed assets would result in higher fixed asset turnover.

20. A is correct. If the U.S. dollar is the functional currency, the temporal method must be used, and the balance sheet exposure will be the net monetary assets of 125 + 230 −185 − 200 = −30 or a net monetary liability of $30. This net monetary liability would be eliminated if fixed assets (nonmonetary) were sold to increase cash. Issuing debt, either short-term or long-term, would increase the net monetary liability.

21. A is correct. Because the U.S. dollar has been consistently weakening against the Singapore dollar, cost of sales will be lower and gross profit higher when an earlier exchange rate is used to translate inventory, compared to using current exchange rates. If the Singapore dollar is the functional currency, current rates would be used. Therefore, the combination of the U.S. dollar (temporal method) and FIFO will result in the highest gross profit margin.

22. A is correct. Under the current rate method, revenue is translated at the average rate for the year, SGD 4,800 × 0.662=$3,178. Debt should be translated at the current rate, SGD 200 × 0.671=$134. Under the current rate method, Acceletron would have a net asset balance sheet exposure. Since the SGD has been strengthening against the USD, the translation adjustment would be positive rather than negative.

23. B is correct. Under the temporal method, inventory and fixed assets would be translated using historic rates. Accounts receivable is a monetary asset and would be translated at year-end (current) rates. Fixed assets are found as (1,000 × 0.568)+(640 × 0.606)=$956.

24. B is correct. $0.671/SGD is the current exchange rate. That rate would be used regardless of whether Acceletron uses the current rate or temporal method. $0.654 was the weighted average rate when inventory was acquired. That rate would be used if the company translated its statements under the temporal method, but not the current rate method. $0.588/SGD was the exchange rate in effect when long-term debt was issued. As a monetary liability, long-term debt is always translated using current exchange rates. Consequently, that rate is not applicable, regardless of how Acceletron translates its financial statements.