CHAPTER 13

EMPLOYEE COMPENSATION: POSTEMPLOYMENT AND SHARE-BASED

After completing this chapter, you will be able to do the following:

- Describe the types of postemployment benefit plans and the implications for financial reports.

- Explain and calculate measures of a defined benefit pension obligation (i.e., present value of the defined benefit obligation and projected benefit obligation) and net pension liability (or asset).

- Describe the components of a company’s defined benefit pension expense.

- Explain and calculate the impact of a defined benefit plan’s assumptions on the defined benefit obligation and periodic expense.

- Calculate and explain the effects on financial statements of adjusting for items of pension and other postemployment benefits that are reported in the notes to the financial statements.

- Interpret pension plan note disclosures including cash flow related information.

- Evaluate the underlying economic liability (or asset) of a company’s pension and other postemployment benefits.

- Calculate the underlying economic pension expense (income) and other postemployment expense (income) based on disclosures.

- Explain issues involved in accounting for share-based compensation.

- Explain the impact on financial statements of the accounting for stock grants and stock options, and the importance of companies’ assumptions in valuing these grants and options.

- Defined contribution pension plans specify (define) only the amount of contribution to the plan; the eventual amount of the pension benefit to the employee will depend on the value of an employee’s plan assets at the time of retirement.

- Balance sheet reporting is less analytically relevant for defined contribution plans because companies make contributions to defined contribution plans as the expense arises and thus no liabilities accrue for that type of plan.

- Defined benefit pension plans specify (define) the amount of the pension benefit, often determined by a plan formula, under which the eventual amount of the benefit to the employee is a function of length of service and final salary.

- Accounting for a defined benefit pension plan entails:

- Estimating the defined benefit obligation (the amount of future benefits) using actuarial assumptions and demographic variables;

- Estimating the present value of the defined benefit obligation and the related current service costs using the project unit credit method;

- Determining the actuarial gains and losses and the amount of these actuarial gains and losses to be recognized;

- Estimating any past service costs; and

- Determining the fair value of plan assets.

- Defined benefit pension plan obligations are funded by the sponsoring company contributing assets to a pension trust, a separate legal entity. Differences exist in countries’ regulatory requirements for companies to fund defined benefit pension plan obligations.

- IFRS requires companies to report on their balance sheet a pension liability or asset equal to the defined benefit obligation minus the fair value of plan assets, with optional adjustments for unrecognized actuarial gains or losses and required adjustments for any past service costs. However, IFRS restricts the amount of a pension asset that can be reported.

- U.S. GAAP requires companies to report on their balance sheet a pension liability or asset equal to the projected benefit obligation minus the fair value of plan assets, with no additional adjustments. There is no limit on the amount of a pension asset that can be reported.

- Pension expense includes the following components: current service costs, interest expense, past service costs, actuarial gains and losses, and expected return on plan assets (which reduces pension expense). IFRS does not require companies to present the various components of pension expense as a net amount (i.e., one line item) on the income statement. Instead, companies may disclose portions of net pension expense within different line items on the income statement. U.S. GAAP, however, requires all components of net periodic pension expense to be aggregated and presented as a net amount (a single line item) on the income statement.

- Estimates of the future obligation under defined benefit pension plans and other postemployment benefits are sensitive to numerous assumptions, including discount rates, assumed annual compensation increases, expected return on plan assets, and assumed health care cost inflation.

- Employee compensation packages are structured to fulfill varied objectives including satisfying employees’ needs for liquidity, retaining employees, and providing incentives to employees.

- Common components of employee compensation packages are salary, bonuses, and share-based compensation.

- Share-based compensation serves to align employees’ interest with those of the shareholders. It includes stocks and stock options.

- Share-based compensation has the advantage of requiring no current-period cash outlays.

- Share-based compensation expense is reported at fair value under IFRS and U.S. GAAP.

- The valuation technique, or option pricing model, that a company uses is an important choice in determining fair value and is disclosed.

- Key assumptions and input into option pricing models include items such as exercise price, stock price volatility, estimated life of each award, estimated number of options that will be forfeited, dividend yield, and the risk-free rate of interest. Certain assumptions are highly subjective, such as stock price volatility or the expected life of stock options, and can greatly change the estimated fair value and thus compensation expense.

The following information relates to Questions 1 through 6.

Kensington plc is based in the United Kingdom and offers its employees a defined benefit pension plan. Kensington complies with IFRS. The company’s effective tax rate for 2009 is 28 percent. Excerpts from a financial statement note on Kensington’s retirement plans are presented in Exhibit A.

EXHIBIT A Kensington Plc Defined Benefit Pension Plan

| (£ in millions) | 2009 |

| Components of net periodic benefit cost | |

| Service cost | £96 |

| Interest cost | 1,557 |

| Expected return plan assets | –1,874 |

| Recognized past service cost | 169 |

| Recognized net actuarial loss | 95 |

| Net periodic pension cost | £43 |

| Change in benefit obligation | |

| Benefit obligations at beginning of year | £28,416 |

| Service cost | 96 |

| Interest cost | 1,557 |

| Actuarial (gains) losses | –306 |

| Past service costs | 132 |

| Foreign exchange impact | –42 |

| Benefits paid | –1,322 |

| Benefit obligations at end of year | £28,531 |

| Change in plan assets | |

| Fair value of plan assets at beginning of year | £23,432 |

| Expected return plan assets | 1,874 |

| Actuarial loss | –572 |

| Employer contributions | 693 |

| Benefits paid | –1,322 |

| Fair value of plan assets at end of year | £24,105 |

| Funded Status | –£4,426 |

| Unrecognized past service cost | 185 |

| Unrecognized actuarial gain | –318 |

| Net asset (liability) in the balance sheet | –£4,559 |

1. At year-end 2009, £28,531 million represents:

A. the funded status of the plan.

B. the defined benefit obligation.

C. the fair value of the plan’s assets.

2. The economic pension expense for Kensington’s defined benefit plan is closest to:

A. £135 million.

B. £1,251 million.

C. £2,509 million.

3. The difference between Kensington’s estimated economic pension expense for the period and its reported net periodic pension cost is closest to:

A. £92 million.

B. £1,208 million.

C. £1,302 million.

4. To adjust Kensington’s reported net income to reflect the company’s underlying economic pension expense, the decrease in net income would be closest to:

A. £26 million.

B. £66 million.

C. £92 million.

5. To reflect the funded status of Kensington’s defined benefit pension plan, Kensington’s 2009 reported balance sheet liabilities would be decreased by an amount closest to:

A. £104 million.

B. £133 million.

C. £639 million.

6. An adjustment to Kensington’s statement of cash flows to reclassify the company’s excess contribution for 2009 would most likely entail reclassifying £558 million (excluding income tax effects) as an outflow related to:

A. investing activities rather than operating activities.

B. financing activities rather than operating activities.

C. operating activities rather than financing activities.

The following information relates to Questions 7 through 12.

Passaic Industries is based in France and offers its employees both a defined benefit pension plan and stock options. Passaic prepares its financial statements in accordance with IFRS. Several of the disclosures related to these plans are presented in Exhibits B, C, and D.

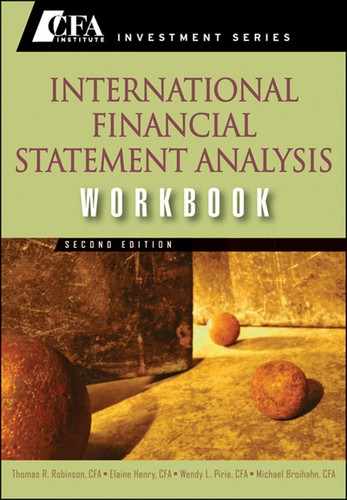

EXHIBIT B Components of Pension Cost (Income)

EXHIBIT C Funded Status of Plan

| At 31 December | ||

| (in millions) | 2009 | 2008 |

| Change in benefit obligation | ||

| Beginning balance | €45,183 | €42,781 |

| Service cost | 908 | 910 |

| Interest cost | 2,497 | 2,457 |

| Plan participants’ contributions | 9 | 12 |

| Amendments | 156 | 270 |

| Actuarial (gain) loss | (925) | 2,778 |

| Settlement/curtailment/acquisitions/dispositions, net | 85 | (1,774) |

| Benefits paid | (2,331) | (2,251) |

| Ending balance | €45,582 | €45,183 |

| Change in plan assets | ||

| Beginning balance at fair value | €43,484 | €38,977 |

| Expected return on plan assets | 3,455 | 3,515 |

| Actuarial gain | 784 | 1,945 |

| Company contribution | 526 | 2,604 |

| Plan participants’ contributions | 9 | 12 |

| Settlement/curtailment/acquisitions/dispositions, net | 216 | (1,393) |

| Benefits paid | (2,286) | (2,208) |

| Exchange rate adjustment | 15 | 32 |

| Ending balance at fair value | €46,203 | €43,484 |

| Funded Status | €621 | (€1,699) |

| Unrecognized past service cost | 104 | 218 |

| Unrecognized actuarial loss (gain) | 237 | (115) |

| Net asset (liability) in the balance sheet | €962 | (€1,596) |

EXHIBIT D Volatility Assumptions Used to Value Stock Option Grants

| Grant Year | Weighted Average Expected Volatility |

| 2009 valuation assumptions | |

| 2005–2009 | 21.50% |

| 2008 valuation assumptions | |

| 2004–2008 | 23.00% |

7. If Passaic had reported under U.S. GAAP, with regard to its defined benefit pension plan, Passaic’s year-end 2009 balance sheet most likely would report a:

A. €621 million asset.

B. €962 million asset.

C. €621 million liability.

8. The net periodic pension cost reported on the Passaic Industries income statement for the year ending 31 December 2009 is closest to:

A. €908 million.

B. €1,050 million.

C. €2,331 million.

9. The Passaic Industries statement of cash flows for the year ended 31 December 2009 shows the reconciliation of net income to cash flows from operating activities for the period. The associated net adjustment to net income related to the defined benefit pension plan is closest to:

A. €524 million.

B. €526 million.

C. €1,050 million.

10. The estimated increase in the pension obligation due to benefits earned by current employees in 2009 is closest to:

A. €908 million.

B. €1,050 million.

C. €2,331 million.

11. In 2009, the actual return on Passaic’s plan assets is closest to:

A. −€1,760 million.

B. €3,445 million.

C. €4,239 million.

12. Compared to 2009 net income as reported, if Passaic Industries had used the same expected volatility assumption for its 2009 option grants that it had used in 2008, its 2009 net income would have been:

A. lower.

B. higher.

C. the same.

The following information relates to Questions 13 through 18.

Stereo Warehouse is an Australian retailer that offers employees a defined benefit pension plan and stock options as part of its compensation package. Stereo Warehouse prepares its financial statements in accordance with International Financial Reporting Standards (IFRS).

Peter Friedland, CFA, is an equity analyst concerned with earnings quality. He is particularly interested in whether the discretionary assumptions the company is making regarding compensation plans are contributing to the recent earnings growth at Stereo Warehouse. He gathers information from the company’s regulatory filings regarding the pension plan assumptions in Exhibit E and the assumptions related to option valuation in Exhibit F.

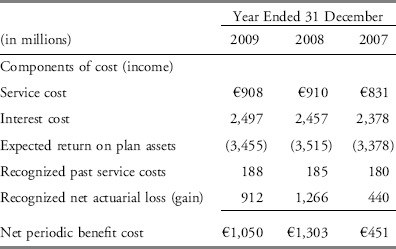

EXHIBIT E Assumptions Used for Stereo Warehouse Defined Benefit Plan

EXHIBIT F Option Valuation Assumptions

13. Compared to the 2009 reported financial statements, if Stereo Warehouse had used the same expected long-term rate of return on plan assets assumption in 2009 as it used in 2007, its year-end 2009 pension obligation would most likely have been:

A. lower.

B. higher.

C. the same.

14. Compared to the reported 2009 financial statements, if Stereo Warehouse had used the same discount rate as it used in 2007, it would have most likely reported lower:

A. net income.

B. total liabilities.

C. cash flow from operating activities.

15. Compared to the assumptions Stereo Warehouse used to compute its net periodic pension cost in 2008, earnings in 2009 were most favorably impacted by the change in the:

A. discount rate.

B. estimated future salary increases.

C. expected long-term rate of return on plan assets.

16. Compared to the pension assumptions Stereo Warehouse used in 2008, which of the following pair of assumptions used in 2009 are most likely internally inconsistent?

A. Estimated future salary increases, inflation

B. Discount rate, estimated future salary increases

C. Expected long-term rate of return on plan assets, discount rate

17. Compared to the reported 2009 financial statements, if Stereo Warehouse had used the 2007 expected volatility assumption to value its employee stock options, it would have most likely reported higher:

A. net income.

B. compensation expense.

C. deferred compensation liability.

18. Compared to the assumptions Stereo Warehouse used to value stock options in 2008, earnings in 2009 were most favorably impacted by the change in the:

A. expected life.

B. risk-free rate.

C. dividend yield.

The following information relates to Questions 19 through 24.

Andreas Kordt is an equity analyst examining the financial statements of Aero Euro. Aero Euro is based in Belgium and complies with IFRS. Kordt is concerned that the accounting guidelines for defined benefit pension plans do not reflect the underlying economic financial conditions and he intends to adjust Aero Euro’s financial statements accordingly. He also wants to compare the reported financial statements to those of a company that follows U.S. GAAP. As an initial step, he collected certain information relating to the plans, which is presented in Exhibits G and H.

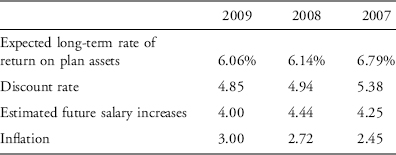

EXHIBIT G Pension Plan Assumptions for Aero Euro

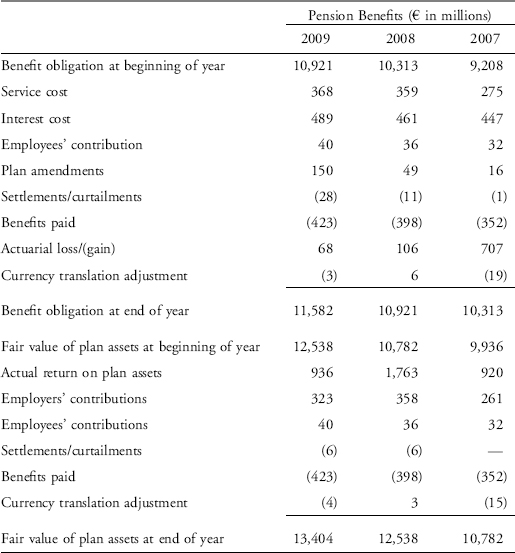

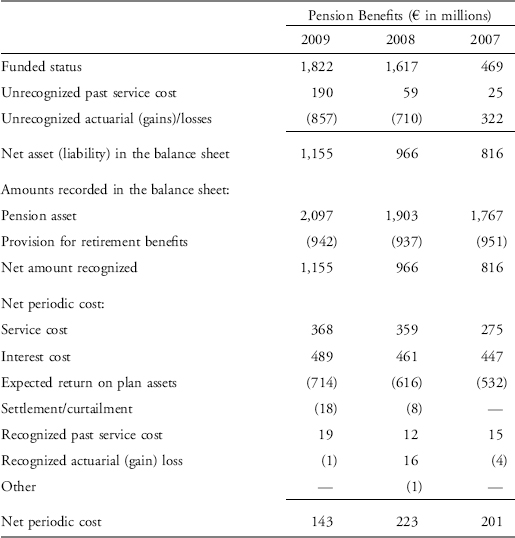

EXHIBIT H Information Related to Aero Euro’s Defined Benefit Plans

19. At year-end 2009, €11,582 million represents the total present value of benefits Aero Euro’s employees:

A. would receive if they left the company.

B. are expected to earn during their career.

C. have earned in the current and past periods.

20. Aero Euro’s underlying economic pension expense for 2009 is closest to:

A. €118 million.

B. €143 million.

C. €323 million.

21. The 2009 net periodic pension cost recognized in Aero Euro’s income statement is closest to:

A. €143 million.

B. €423 million.

C. €1,155 million.

22. Adjusting Aero Euro’s 2009 balance sheet to reflect the underlying economic position of the company’s defined benefit pension plan would result in a €667 increase in:

A. assets.

B. liabilities.

C. shareholders’ equity.

23. Compared to the reported 2009 financial statements, if Aero Euro used the 2007 expected rate of salary increase assumption in 2009 it would have most likely reported higher:

A. net income.

B. benefit obligation.

C. recognized past service costs.

24. Compared to the reported 2009 financial statements, if Aero Euro used the 2007 expected long-term rate of return on plan assets in 2009 it would have most likely reported higher:

A. net assets.

B. net income.

C. pension expense.