CHAPTER 16

EVALUATING FINANCIAL REPORTING QUALITY

After completing this chapter, you will be able to do the following:

- Contrast cash-basis and accrual-basis accounting, and explain why accounting discretion exists in an accrual accounting system.

- Describe the relation between the level of accruals and the persistence of earnings and the relative multiples that the cash and accrual components of earnings should rationally receive in valuation.

- Explain opportunities and motivations for management to intervene in the external financial reporting process and mechanisms that discipline such intervention.

- Describe earnings quality and measures of earnings quality, and compare the earnings quality of peer companies.

- Explain mean reversion in earnings and how the accruals component of earnings affects the speed of mean reversion.

- Explain potential problems that affect the quality of financial reporting, including revenue recognition, expense recognition, balance sheet issues, and cash flow statement issues, and interpret warning signs of these potential problems.

- Financial reporting quality relates to the accuracy with which a company’s reported financial statements reflect its operating performance and to their usefulness for forecasting future cash flows. Understanding the properties of accruals is critical for understanding and evaluating financial reporting quality.

- The application of accrual accounting makes necessary use of judgment and discretion. On average, accrual accounting provides a superior picture to a cash basis accounting for forecasting future cash flows.

- Earnings can be decomposed into cash and accrual components. The accrual component has been found to have less persistence than the cash component and therefore (1) earnings with higher accrual components are less persistent than earnings with smaller accrual components, all else equal, and (2) the cash component of earnings should receive a higher weighting in evaluating company performance.

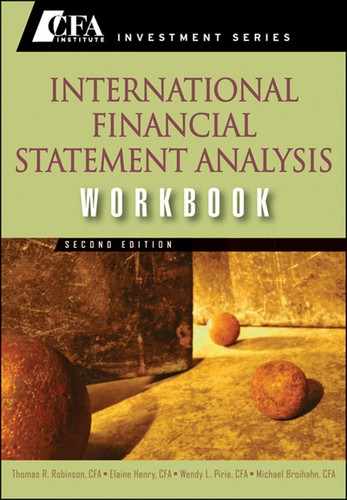

- Aggregate accruals=Accrual earnings−Cash earnings

- Defining net operating assets as NOAt=[(Total assetst−Casht)−(Total liabilitiest−Total debtt)] one can derive the following balance-sheet-based and cash-flow-statement-based measures of aggregate accruals/the accruals component of earnings:

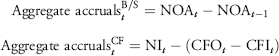

With corresponding scaled measures that can be used as simple measures of financial reporting quality:

- Aggregate accruals ratios are useful to rank companies for the purpose of evaluating earnings quality. Companies with high (low) accruals ratios are companies with low (high) earnings quality. Companies with low (high) earnings quality tend to experience lower (higher) accounting rates of return and relatively lower excess stock returns in future periods.

- Sources of accounting discretion include choices related to revenue recognition, depreciation choices, inventory choices, choices related to goodwill and other noncurrent assets, choices related to taxes, pension choices, financial asset/liability valuation, and stock option expense estimates.

- A framework for detecting financial reporting problems includes examining reported financials for revenue recognition issues and expense recognition issues.

- Revenue recognition issues include overstatement of revenue, acceleration of revenue, and classification of nonrecurring or nonoperating items as operating revenue.

- Expense recognition issues include understating expenses, deferring expenses, and the classification of ordinary expenses as nonrecurring or nonoperating expenses.

- Discretion related to off-balance sheet liabilities (e.g., in the accounting for leases) and the impairment of goodwill also can affect financial reporting quality.

1. Which of the following mechanisms is least likely to discourage management manipulation of earnings?

A. Debt covenants.

B. Securities regulators.

C. Class action lawsuits.

2. High earnings quality is most likely to:

A. result in steady earnings growth.

B. improve the ability to predict future earnings.

C. be based on conservative accounting choices.

3. The best justification for using accrual-based accounting is that it:

A. reflects the company’s underlying cash flows.

B. reflects the economic nature of a company’s transactions.

C. limits management’s discretion in reporting financial results.

4. The best justification for using cash-based accounting is that it:

A. is more conservative.

B. limits management’s discretion in reporting financial results.

C. matches the timing of revenue recognition with that of associated expenses.

5. Which of the following is not a measure of aggregate accruals?

A. The change in net operating assets.

B. The difference between operating income and net operating assets.

C. The difference between net income and operating and investing cash flows.

6. Consider the following balance sheet information for Profile, Inc.:

| Year Ended 31 December | 2007 | 2006 |

| Cash and short-term investments | 14,000 | 13,200 |

| Total current assets | 21,000 | 20,500 |

| Total assets | 97,250 | 88,000 |

| Current liabilities | 31,000 | 29,000 |

| Total debt | 50,000 | 45,000 |

| Total liabilities | 87,000 | 79,000 |

Profile’s balance-sheet-based accruals ratio in 2007 was closest to:

A. 12.5%.

B. 13.0%.

C. 16.2%.

7. Rodrigue SA reported the following financial statement data for the year ended 2007:

| Average net operating assets | 39,000 |

| Net income | 14,000 |

| Cash flow from operating activity | 17,300 |

| Cash flow from investing activity | (12,400) |

Rodrigue’s cash-flow-based accruals ratio in 2007 was closest to:

A. −8.5%.

B. −19.1%.

C. 23.3%.

8. Cash collected from customers is least likely to differ from sales due to changes in:

A. inventory.

B. deferred revenue.

C. accounts receivable.

9. Reported revenue is most likely to have been reduced by management’s discretionary estimate of:

A. warranty provisions.

B. inventory damage and theft.

C. interest to be earned on credit sales.

10. Zimt AG reports 2007 revenue of €14.3 billion. During 2007, its accounts receivable rose by €0.7 billion, accounts payable increased by €1.1 billion, and unearned revenue increased by €0.5 billion. Its cash collections from customers in 2007 were closest to:

A. €14.1 billion.

B. €14.5 billion.

C. €15.2 billion.

11. Cinnamon Corp. began the year with $12 million in accounts receivable and $31 million in deferred revenue. It ended the year with $15 million in accounts receivable and $27 million in deferred revenue. Based on this information, the accrual-basis earnings included in total revenue were closest to:

A. $1 million.

B. $7 million.

C. $12 million.

12. Which of the following is least likely to be a warning sign of low-quality revenue?

A. A large decrease in deferred revenue.

B. A large increase in accounts receivable.

C. A large increase in the allowance for doubtful accounts.

13. An unexpectedly large reduction in the unearned revenue account is most likely a sign that the company:

A. accelerated revenue recognition.

B. overstated revenue in prior periods.

C. adopted more conservative revenue recognition practices.

14. Canelle SA reported 2007 revenue of €137 million. Its accounts receivable balance began the year at €11 million and ended the year at €16 million. At year-end, €2 million of receivables had been securitized. Canelle’s cash collections from customers (in € millions) in 2007 were closest to:

A. €130.

B. €132.

C. €134.

15. In order to identify possible understatement of expenses with regard to noncurrent assets, an analyst would most likely beware management’s discretion to:

A. accelerate depreciation.

B. increase the residual value.

C. reduce the expected useful life.

16. A sudden rise in inventory balances is least likely to be a warning sign of:

A. understated expenses.

B. accelerated revenue recognition.

C. inefficient working capital management.

17. A warning sign that a company may be deferring expenses is sales revenue growing at a slower rate than:

A. unearned revenue.

B. noncurrent liabilities.

C. property, plant, and equipment.

18. An asset write-down is least likely to indicate understatement of expenses in:

A. prior years.

B. future years.

C. the current year.

19. Ranieri Corp. reported the following 2007 income statement:

| Sales | 93,000 |

| Cost of sales | 24,500 |

| SG&A | 32,400 |

| Interest expense | 800 |

| Other income | 1,400 |

| Income taxes | 14,680 |

| Net income | 22,020 |

Ranieri’s core operating margin in 2007 was closest to:

A. 23.7%.

B. 38.8%.

C. 73.7%.

20. Sebastiani AG reported the following financial results for the years ended 31 December:

| 2007 | 2006 | |

| Sales | 46,574 | 42,340 |

| Cost of sales | 14,000 | 13,000 |

| SGA | 13,720 | 12,200 |

| Operating income | 18,854 | 17,140 |

| Income taxes | 6,410 | 5,656 |

| Net income | 12,444 | 11,484 |

Compared to core operating margin in 2006, Sebastiani’s core operating margin in 2007 was:

A. lower.

B. higher.

C. unchanged.

21. A warning sign that ordinary expenses are now being classified as nonrecurring or nonoperating expenses is:

A. falling core operating margin followed by a spike in positive special items.

B. a spike in positive special items followed by falling core operating margin.

C. falling core operating margin followed by a spike in negative special items.

22. Which of the following obligations must be reported on a company’s balance sheet?

A. Capital leases.

B. Operating leases.

C. Purchase commitments.

23. The most accurate estimate for off-balance sheet financing related to operating leases consists of the sum of:

A. future payments.

B. future payments less a discount to reflect the related interest component.

C. future payments plus a premium to reflect the related interest component.

24. The intangible asset goodwill represents the value of an acquired company that cannot be attached to other tangible assets. This noncurrent asset account is charged to an expense:

A. as amortization.

B. when it becomes impaired.

C. at the time of the acquisition.

25. Total accruals measured using the balance sheet is most likely to differ from total accruals measured using the statement of cash flows when the company has made acquisitions:

A. financed by debt.

B. in exchange for cash.

C. in exchange for stock.