12. Managing Payroll

Many areas in QuickBooks deserve a thorough review. One, in particular, is payroll. Managing your payroll includes verifying that you are paying your employees properly and that you remain in compliance with state and federal regulations regarding your company’s payroll obligations.

If your company processes payroll for employees, this chapter can help you better manage the many facets of providing payroll.

Report Center Payroll Reports

Reporting on payroll activity is necessary to properly manage your business payroll activity. QuickBooks offers several payroll reports that you can customize to suit your needs. For more details on customizing reports, see Chapter 14, “Reporting in QuickBooks.” Whether you are new to QuickBooks or an expert, you will benefit from the payroll reports in the Report Center. To open the Report Center, from the menu bar, select Reports, Report Center. Select any of the icons on the top right to change the viewing method for the Report Center:

• Carousel View

• List View

• Grid View

By default, the Report Center opens with the Standard tab selected and displays several report categories. Click Employees & Payroll. To the right, you see sample payroll reports (see Figure 12.1) using Grid View.

Figure 12.1. Preview and prepare payroll reports in the Report Center.

Underneath each sample report, you can click the corresponding icons to prepare the report using your data and a date you select, get more information about the report, mark the report as a favorite, or access help information for the report. Icon descriptions display when you hover your cursor over a report.

The Report Center also offers these tabs:

• Memorized—From any displayed report, click Memorize to add the report to this tab in the Report Center.

• Favorites—Mark a report as a Favorite (or Fave) to include the report in this tab group.

• Recent—QuickBooks lists reports you have recently prepared here.

• Contributed—You can download custom reports created by Intuit or other QuickBooks users and use them with your data. You can also share reports you create with the community-at-large. When sharing a report, you are not sharing sensitive information—you share just the format of the report.

You can also type a descriptive search term into the search box in the Report Center to display a list of relevant reports. Additional payroll reports are available in QuickBooks using pivot tables in Microsoft Excel. The next section details these reports.

Excel Reports

If you did not find the report you needed in the Report Center, check out the many reports that use pivot tables in Microsoft Excel. Your QuickBooks software includes these reports.

To access these reports, follow these steps:

1. From the menu bar, select Reports, Employees & Payroll, Summarize Payroll Data in Excel. QuickBooks launches Excel and provides a dialog box that enables you to do the following:

• Select Date ranges for collecting payroll data.

• Select Options/Settings that include updating worksheet headers, changing column widths, and enabling drill-down on data and other useful settings.

• Select optional reports, including 8846 Worksheet, Effective Rates by Item, YTD Recap, and Deferred Compensation report.

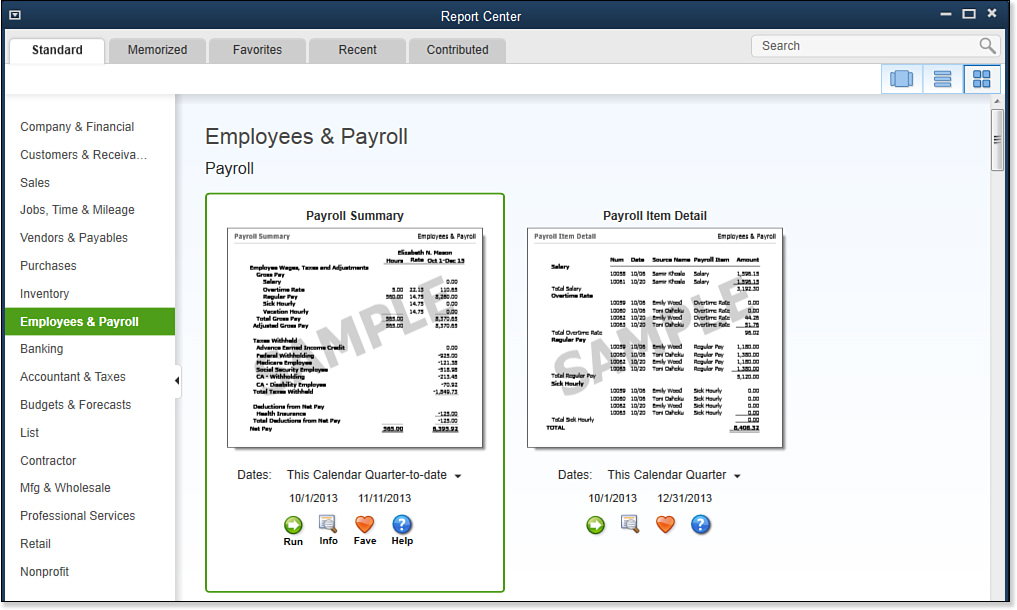

2. Click Get QuickBooks Data. Excel collects data for the selected date range and creates a workbook with several worksheets (see Figure 12.2), including the following:

• Employee Journal

• YTD Summary (two versions)

• Hours

• Rates & Hours by Job

• State Wage Listing

• Deferred Comp

• Quarterly details

• 8846 Worksheet

• Calculated % By Payroll Item and Employee

Figure 12.2. You can prepare this and many other payroll reports with your data using Excel spreadsheets.

You can save this report as an Excel worksheet for future reference. However, this report cannot be updated with more current data, unlike many other exported Excel reports.

In addition to these reports, there are other reports that QuickBooks creates using Excel.

From the menu bar, select Reports, Employees & Payroll, More Payroll Reports in Excel. Choose which specific report you want from the following:

• Payroll Summary by Tax Tracking Type

• Employee Time & Costs

• Employee Sick & Vacation History

• Employee Direct Deposit Listing

• Tax Form Worksheets

• New! Certified Payroll Report

As you can see, QuickBooks provides plenty of options for finding the right payroll report for your needs, either within QuickBooks or using the automatically generated Microsoft Excel reports.

Tax Forms and Filings

Up to this point, you have set up payroll, managed employees and payroll items, paid your employees and the state and federal liabilities, and prepared payroll reports. You now see how QuickBooks helps you comply with the required payroll reporting.

In Chapter 11, “Setting Up Payroll,” you learned about the many payroll subscription offerings you can choose from. If you want your QuickBooks software to automatically calculate your payroll transactions and prepare federal and state forms, you need to have the Intuit QuickBooks Payroll Enhanced subscription. For accounting professionals who prepare payroll for multiple clients, Intuit QuickBooks Payroll Enhanced for Accountants is the subscription most suitable.

QuickBooks can print required federal and state payroll forms or E-File them for you; completing your payroll reporting tasks is so easy.

Preparing and Printing Tax Forms

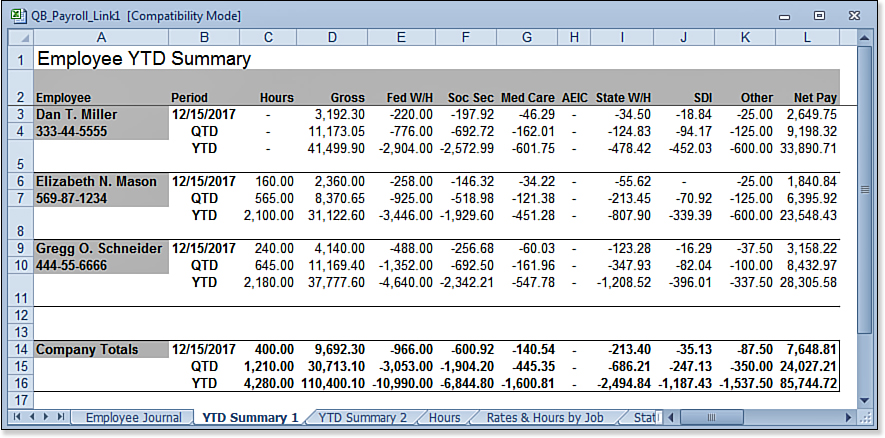

Before preparing your first payroll tax form, complete the Payroll Contact information in the Company Information window. To do so, from the menu bar, select Company, My Company. In the top-right corner, click the Edit icon. Select the Payroll Tax Form Information and confirm the Contact Name, Title, and Phone No. that will be included on the prepared payroll tax forms (see Figure 12.3).

Figure 12.3. QuickBooks prefills payroll tax forms with specified contact information.

To prepare your federal or state forms, follow these steps:

1. On the Home page, click the Process Payroll Forms icon.

2. QuickBooks opens the File Forms tab of the Payroll Center.

3. If a Payroll Subscription Alert message displays, informing you to update your tax tables, go to step 4; otherwise, go to step 6.

4. Click Get Updates or Skip. I recommend that you select Get Updates to ensure that you have the latest tax tables and forms.

5. Click OK to close the Payroll Update message.

6. After you update the payroll taxes, if the Payroll Center does not display, on the Home page, click the Process Payroll Forms icon.

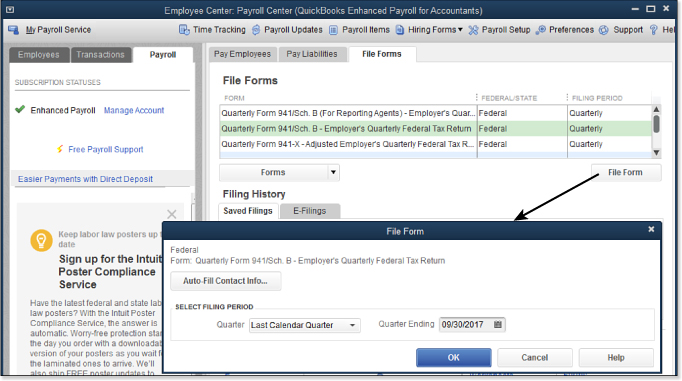

7. Select the appropriate form. Click the File Form button (see Figure 12.4).

Figure 12.4. With the Enhanced Payroll Subscription, QuickBooks can prepare all your federal forms and many state forms.

8. (Optional) Click Auto-Fill Contact Info and complete.

9. Select Filing Period, Quarter, and Quarter Ending date. Click OK.

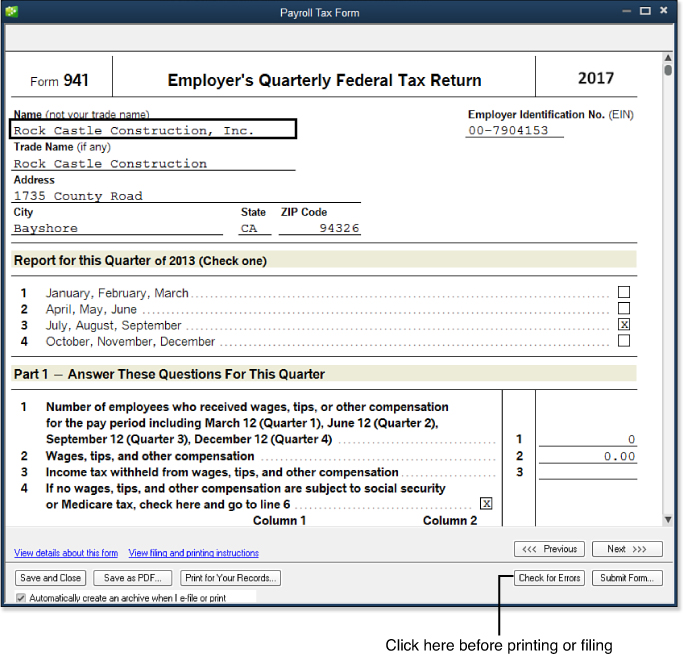

10. Complete any required fields on the displayed form. If you have questions about the form details, click the provided links. When you have completed the form, click the Check for Errors button (see Figure 12.5). If any errors display, click the error; QuickBooks advances to that section of the form for you to complete or correct.

Figure 12.5. Save time and prepare accurate payroll tax forms using the Enhanced Payroll subscription.

11. Click Next to advance to the next form page.

12. Click Save & Close if you need to return later to your saved work.

13. Click Save as PDF to save a PDF for your records, click Print for Your Records to prepare a paper copy, or click Submit Form if you have signed up for E-File of your payroll forms (discussed in the next section).

E-Filing Tax Payments and Forms

If you selected the Intuit QuickBooks Payroll Enhanced subscription or the Intuit QuickBooks Payroll Enhanced for Accountant’s subscription for your business, you can sign up for the E-File and E-Pay service.

With E-File and E-Pay, you prepare your payroll liability payments in QuickBooks and select E-Pay. Intuit debits your bank account for the funds and remits them directly to the IRS or appropriate state(s) on your behalf.

With E-File of your payroll forms, you can select Submit Form and have QuickBooks process your payroll form and send it to the IRS. You will receive email notification that the form was accepted (or rejected) by the IRS or state(s). To take advantage of the E-File and E-Pay service, you need the following:

• An active Enhanced Payroll subscription.

• A supported version of QuickBooks (typically not older than three years from the current calendar year).

• An Internet connection.

• The most recent payroll tax update.

• Enrollment with the Electronic Federal Tax Payment System (EFTPS), which the IRS uses for employer or individual payments. For more information, visit www.eftps.gov.

You can get more detailed information by clicking the Electronic Payment link at the bottom of the Pay Liabilities tab of the Payroll Center. As your business E-Pays and E-Files, you can click the E-Payments tab, which displays documentation that the payments and forms were successfully transmitted to the IRS.

Troubleshooting Payroll

Using the QuickBooks Run Payroll Checkup diagnostic tool is a recommended way to review and validate the accuracy of your payroll data. You can also review your data setup and accuracy manually by reviewing the reports detailed in this section.

Reviewing the Payroll Item Listing can also be helpful when you need to troubleshoot payroll issues.

→ For more information, see “Reporting About Payroll Items,” p. xxx.

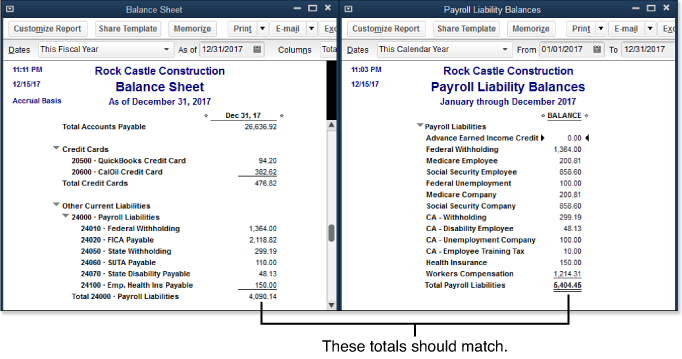

Comparing Payroll Liability Balances to the Balance Sheet

Periodically comparing your Balance Sheet payroll liabilities account balance to the amount on the Payroll Liabilities Balances report is important. To do so, follow these steps:

1. From the menu bar, select Reports, Company & Financial, Balance Sheet Standard.

2. Select the As Of date for the period you are reviewing.

3. From the menu bar, select Reports, Employees & Payroll, Payroll Liability Balances.

4. From the Dates drop-down list, select All from the top of the list. Leave the From date box empty. In the To date box, enter the same date that was used on the Balance Sheet Standard report. Doing so ensures that you are picking up all transactions for this account, including any unpaid balances from prior years. Click Print if you want to have a copy of this report to compare to your Balance Sheet payroll liabilities balance.

These two reports should have matching totals. In the examples in Figure 12.6, the Balance Sheet and Payroll Liabilities reports do not match.

Figure 12.6. Compare the Balance Sheet payroll liabilities amount to the Payroll Liability Balances report.

The totals might not match because nonpayroll transactions are used to record adjustments or payments to payroll liabilities using nonpayroll transactions, including the Make Journal Entry, Enter Bill, or Write Check transaction types.

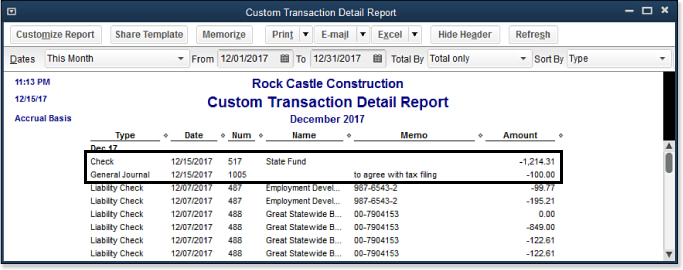

To troubleshoot payroll liabilities differences, you can use the Custom Transaction Detail report. To access the report, follow these steps:

1. From the menu bar, select Reports, Custom Reports, Transaction Detail. The Modify Report dialog box opens.

2. In the From date box, leave the field blank; in the To date box, enter the date you used on the Balance Sheet Standard report.

3. Select the same Report Basis as the Balance Sheet report.

4. In the Columns box, remove or add a checkmark for the information you want to display on the report. Be sure to include Type.

5. In the Sort By drop-down list, select Type.

6. Click the Filters tab; in the Choose Filters box, the Accounts filter is already selected. From the Accounts drop-down list to the right, select the Payroll Liabilities account.

7. Click OK to create the report.

QuickBooks creates a useful and telling report (see Figure 12.7). When this report is sorted by type of transaction, you can easily see what non-payroll-related transactions are affecting your Balance Sheet Standard report Payroll Liability balance and are not affecting your Payroll Liability Balances report.

Figure 12.7. Use the Custom Transaction Detail report to easily identify nonpayroll transactions that are recorded to the Payroll Liabilities account.

If you are an accounting professional working with the Client Data Review feature, you can also select the Find Incorrectly Paid Payroll Liabilities custom report from the menu bar by selecting Accountant, Client Data Review, Find Incorrectly Paid Payroll Liabilities.

→ For more information, see “Find Incorrectly Paid Payroll Liabilities,” p. xxx.

You can double-click any of the listed transactions to see more detail about the transaction that was used to create the adjustment to the Balance Sheet. If the Balance Sheet is correct and the Payroll Liability Balances report is not, you can choose between the following options:

• If there are only a few nonpayroll transactions, you might consider voiding them and re-creating them with the correct payroll liability payment transaction. However, if the transactions have been included in bank reconciliations, you have other factors to consider and should consider the next option.

• Create an Adjust Payroll Liabilities transaction.

→ For more information see, “Preparing Payroll Liability Payments,” p. xxx.

Comparing the Payroll Summary Report to Filed Payroll Returns

Has your company ever received a notice from the IRS indicating that your year-end payroll documents do not agree with your quarterly payroll return totals, or have you received a similar notice from your state payroll tax agency?

Listed in this section are some basic comparisons you should do both before filing a payroll return and afterward, if you allow users to make changes to transactions from previous payroll quarters.

→ For more information about preventing these changes, see “Set a Closing Date,” p. xxx.

Compare the following items routinely while doing payroll in QuickBooks and ensure that all apply:

• Each calendar quarter QuickBooks payroll totals agree with your filed payroll return totals. Look at these specific totals when reviewing the Payroll Summary:

• Total Adjusted Gross Pay in QuickBooks agrees with the Federal 941 Form, Wages, Tips, and Other Compensation.

• Federal Withholding in QuickBooks agrees with the Federal 941 Form, Total Income Tax Withheld from Wages, and so on.

• Employee and Company Social Security and Medicare in QuickBooks agrees with the computed Total Taxable Social Security and Medicare on the Federal 941 Form.

• Total payroll tax deposits for the quarter in QuickBooks agrees with your paper trail. Whether you pay online or use a coupon that you take to the bank, make sure you recorded the correct calendar quarter with the IRS for your payments.

• Total Adjusted Gross Pay for the calendar year in QuickBooks agrees with the reported Gross Wage total on the annual Federal Form W-3, Transmittal of Wage, and Tax Statements.

• Total Adjusted Gross Pay for the calendar quarter in QuickBooks agrees with the Total Gross Wage reported to your state payroll agency.

• Total Payroll expense from the Profit & Loss report agrees with total Adjusted Gross Pay on the Payroll Summary report. This will be possible if you have set up a separate chart of accounts for the payroll taxes expense of payroll.

Comparing these critical reports with your federal and state tax filings ensures that your data agrees with the payroll tax agency records.

Reconciling Payroll Reports to Business Financials

When applying for a business loan from your bank, your company might be required to produce compiled, reviewed, or audited financials. One of the many items that will be reviewed is the comparison of payroll costs included in the business financials to those in the payroll returns filed with federal or state governments.

If you are uncertain about which accounts within your chart of accounts to review, refer to the account you assigned to the payroll item. Here are a few selected comparisons you can do yourself as a business owner:

• Compare Federal Form 941 Wages, Tips, and Other Compensation (Box 2) to the expense accounts used to report salaries and wages. You might need to add multiple accounts to match the total in Box 2.

• Compare the company portion of the payroll taxes reported to federal or state governments. If you are uncertain about the amount, ask your accountant or view information about payroll taxes on the www.irs.gov website.

This section has given you several critical comparisons to make and reports to review. No matter how proficient you are with QuickBooks, review these reports often. The next section of this chapter provides instructions on handling unique payroll transactions.

Recording Unique Payroll Transactions

The following sections detail several common payroll transactions you might need in your business.

Employee Loan Payment and Repayment

Your business might offer a loan to an employee in advance of payroll earnings. This amount should not be taxed at the time of payment if you expect the loan to be paid back to the company.

Paying an Employee Paycheck Advance

When you offer to pay employees an advance on their earnings, you are creating a loan payment check. If this is a loan to be paid back to the company, follow these steps:

1. From the menu bar, select Employees, Pay Employees, Unscheduled Payroll. The Enter Payroll Information dialog box opens.

2. Place a checkmark next to the employee you are creating the loan check for.

3. QuickBooks might warn that a paycheck for that period already exists. Click Continue if you want to create the loan payment check. You return to the Enter Payroll Information dialog box.

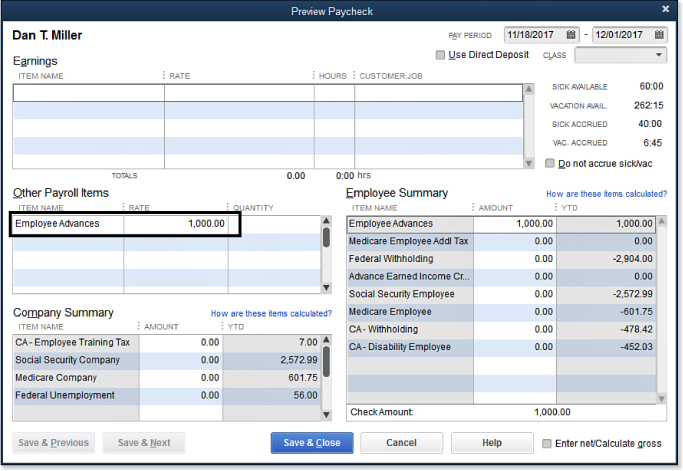

4. To modify the check to be an employee loan check, click the Open Paycheck Detail button.

5. In the Preview Paycheck dialog box, remove any amounts from the Earnings box (if you expect to be repaid this amount, the amount is not considered taxable earnings).

6. In the Other Payroll Items drop-down list, select the Employee Advances (in this example, it was an Addition type payroll item), as in Figure 12.8, and skip to step 15.

Figure 12.8. Use an Addition type payroll item when preparing a nontaxable loan (advance) to an employee.

If you do not have an employee advance payroll item, you can easily create one right from the Preview Paycheck dialog box. In the Other Payroll Items box drop-down list, click Add New.

7. In the Add New Payroll Item dialog box, select the button for the Addition type and click Next.

8. The Add New Payroll Item (Addition) dialog box opens. Name the item Employee Advances (if displayed, do not select the Track Expenses by Job box). Click Next.

9. In the Expense Account drop-down list, select Employee Advances, Other Current Asset account. You can also scroll to the top of this list and click Add New in this dialog box to create the Other Current Asset account, if needed. Click Next.

10. On the Tax Tracking Type screen, select None (at the top of the list) and click Next.

Caution

Carefully consider what option you choose when selecting the Tax Tracking type for a new payroll item or editing an existing payroll item. The selection you choose here affects how QuickBooks taxes or doesn’t tax the payroll item on paychecks and how QuickBooks handles reporting the payroll item on forms, such as the W-2 form given to employees at the end of a calendar year.

When you select each Tax Tracking type, QuickBooks provides detailed information about how it will be treated for tax calculations and form preparation. Be sure to take the time to read these. If you are unsure of the proper tax tracking type, consult your accounting professional.

11. Do not place a checkmark next to any of the Taxes options. Click Next.

12. The Calculate Based on Quantity screen opens. Leave the default of Neither selected and click Next.

13. On the Gross vs. Net screen, leave the default of Gross. This setting has no impact because you are setting it up with a tax tracking type of None. Click Next.

14. The Default Rate and Limit screen opens. Leave it blank because you define the limit amounts individually for each employee. Click Finish to close the Add New Payroll Item (Addition) dialog box.

15. You return to the Preview Paycheck dialog box. From the Other Payroll Items box, in the Item Name column, select the Employee Advance payroll addition item from the drop-down list. Enter the dollar amount of the loan you are providing the employee in the Rate column. QuickBooks creates a payroll advance check without deducting any payroll taxes (see Figure 12.8 shown previously). Note that you do not need to enter anything in the Quantity column.

Note

You can also record the employee loan portion using a Write Check transaction type. Make sure the payee listed on the check is the employee’s name (not a vendor or other name). Record the loan payment to the Employee Advances other current asset account on the Expense tab.

This type of transaction will not report on the Payroll Summary report, one of the reasons I choose to use a Paycheck and Payroll Items to record the initial payroll loan.

QuickBooks now has on record a loan paid to the employee. If you have defined payment terms with the employee, you need to edit the employee’s record so that the agreed-to amount is deducted from future payroll checks. Learn more about this task in the following section.

Automatically Deducting the Employee Loan Repayments

When a company provides an advance to an employee that is to be paid back in installments, you can have QuickBooks automatically calculate this amount and even stop the deductions when the total of the loan has been completely paid back to the company. QuickBooks automatically deducts the loan repayments from future payroll checks. Follow these steps to record a payroll deduction on the employee’s setup:

1. From the menu bar, select Employees, Employee Center.

2. Select the employee who was given a payroll advance or loan. Click the Edit icon in the top right. The Edit Employee dialog box opens.

3. At the right, select the Payroll Info tab.

4. In the Item Name column of the Additions, Deductions, and Company Contributions box, select your Employee Loan Repay deduction item (and skip to step 14), or click Add New to open the Add New Payroll Item dialog box.

5. If you are creating a new item, select type Deduction and click Next.

6. Type a name for the item, such as Employee Loan Repay, and click Next.

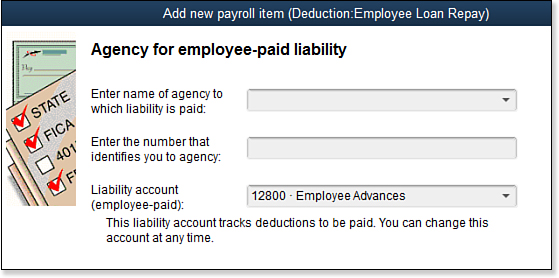

7. The Add New Payroll Item (Deduction) dialog box opens. Leave the agency name and number fields blank. For the Liability Account, select the drop-down list and select your Employee Advances, Other Current Asset account created when you made the employee advance check. (See Figure 12.9.) Click Next.

Figure 12.9. Assign the Other Current Asset Employee Advances as the liability account for the paycheck deduction.

8. The Tax Tracking type screen displays. Leave the default for Tax Tracking type of None and click Next.

9. The Taxes screen displays. Accept the default of no taxes selected and click Next.

10. The Calculate Based on Quantity screen displays. Leave the default of Neither selected and click Next.

11. The Gross vs. Net screen displays. Leave the default of Gross Pay selected. This setting has no impact because you are setting it up with a Tax Tracking type of None. Click Next.

12. The Default Rate and Limit screen displays. Leave it blank because you define the limit amounts individually for each employee. Click Finish to return to the New Employee dialog box or Edit Employee dialog box.

13. In the Item Name column of the Additions, Deductions, and Company Contributions box, select the Employee Loan Repay deduction item you just created.

14. In the Amount column, enter the per-pay-period amount you want to deduct.

15. In the Limit column, enter the amount of the total loan. QuickBooks stops deducting the loan when it reaches the limit. Click OK to record your changes to the employee setup.

QuickBooks is now properly set up to deduct the stated amount on each paycheck until the employee loan has been fully repaid. If you provide additional employee loans, do not forget to go back to step 15 to add the new amount to the previous loan total.

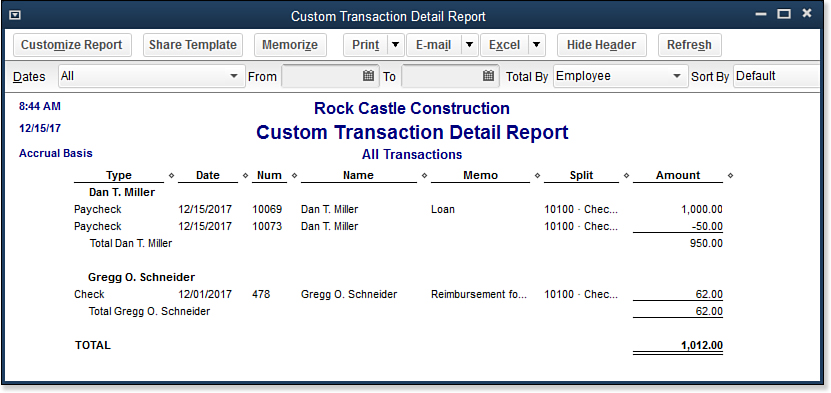

Reporting Employee Loan Details

Tracking the actual details of the employee loan is equally important. To open a modified version of my favorite report, the Transaction Detail report (in Figure 12.10), follow these steps:

Figure 12.10. Create a report to track your employee loan details.

1. From the menu bar, select Reports, Custom Reports, Transaction Detail. The Modify Report dialog box displays.

2. In the Report Date Range drop-down list, select the date range you are reviewing, or choose All to view all dates.

3. In the Columns box, select or deselect the detail you want to see displayed on the report.

4. In the Total By drop-down list, select Employee.

5. Click the Filters tab; Account is already selected in the Choose Filters box. In the Account drop-down list to the right, select the Employee Advances, Other Current Asset account.

6. In the Choose Filters box, select the Amount filter and, optionally, select an amount greater than or equal to .01. Doing so provides a report of only employees with nonzero balances.

7. If you want to change the report title, click the Header/Footer tab and customize the report title.

8. Click OK to view the modified report.

9. If you want to use this report again, click Memorize to save the report for later use.

You are now prepared to advance money to an employee and track the employee’s payments against the loan accurately. Don’t forget to review the balances and to increase the limit when new loans are paid out.

Reprinting a Lost Paycheck

When any other check in QuickBooks is lost, you typically void the check in QuickBooks and issue a stop payment request to your bank so it cannot be cashed.

With payroll, you need to be a bit more cautious about voiding the transaction because, when you void a payroll transaction and then reissue it, payroll taxes can be calculated differently on the replacement check compared to the original paycheck.

Certain payroll taxes are based on limits; for example, Social Security, Federal Unemployment, and State Unemployment taxes are examples of taxes that are charged to employees or to the company, up to a certain wage limit. When you void a previously issued check, QuickBooks recalculates these taxes for the current replacement check, and these amounts might differ from the original check, potentially affecting the net amount of the check.

Proper control is to issue a stop payment request for the missing check to your bank so it cannot be cashed. In QuickBooks, instead of voiding the payroll check and then re-creating it, print a new payroll check (from the same original payroll check details), record the new check number, and then separately create a voided check for the lost check.

To record these transactions, follow these steps:

1. Locate the lost check in your checking register from the menu bar by selecting Banking, Use Register.

2. In the Select Account drop-down list, select the bank account that has the missing check and click OK to open the bank register.

3. Find the check in the register that was reported missing. Double-click the specific check to open the Paycheck dialog box (see Figure 12.11). Make a note of the check number, date, and payee.

Figure 12.11. Do not re-create a lost paycheck; instead, select Print Later on the original paycheck.

4. In the open Paycheck dialog box, on the Main tab of the ribbon toolbar at the top of the transaction, select the Print Later checkbox.

5. Print the paycheck singly or with others by clicking the Print button at the top of the check on the Main tab of the ribbon toolbar.

6. Enter the Printed Check Number. After printing the check, QuickBooks assigns the new check number and uses the check date and totals assigned to the original check.

7. To keep track of the lost check in your accounting, from the menu bar, select Banking, Write Checks. Using the original check number, date, and payee, record the check with a zero amount to an account of your choosing. You might get a message warning not to pay employees with a check, but because you are recording a zero transaction, you can ignore this warning.

8. With the lost check created in step 7 still open, from the menu bar, select Edit, Void Check. QuickBooks prefills with a 0 amount and adds Void to the Memo line of the check. This now shows this check as voided in your register, just in case the employee was able to cash the check. You would notice when reconciling that you marked it as voided.

Using this method for printing a lost payroll check ensures that you do not inadvertently change any prior-period payroll amounts and reported payroll totals; at the same time, recording the lost check helps keep a record of each check issued from your bank account.

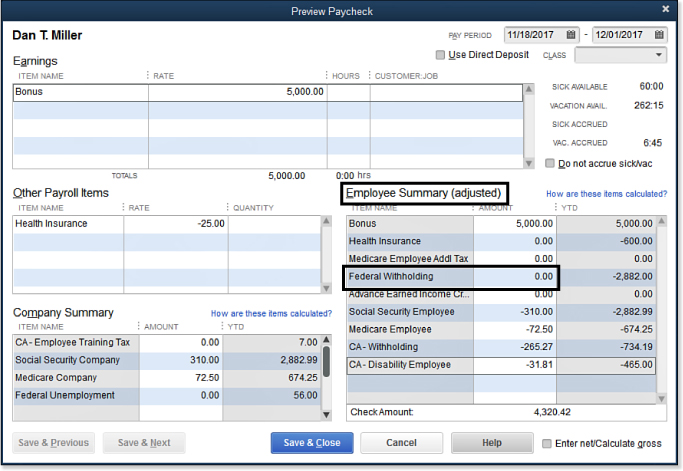

Paying a Taxable Bonus

Use an unscheduled payroll to issue bonuses to your employees. This payroll is included in the total taxable wages. To do so, follow these steps:

1. From the menu bar, select Employees, Pay Employees, Unscheduled Payroll. The Enter Payroll Information dialog box displays.

Note

When issuing a bonus paycheck, QuickBooks might display a warning that a paycheck already exists for the date you have selected. Click Continue to close the warning. You return to the Enter Payroll Information dialog box.

2. Place a checkmark next to the employee(s) receiving a bonus check.

3. If the employee is paid hourly, you can adjust the hours from the regular pay column.

4. Often you want to edit or remove the default Gross Earnings or Federal Taxes Withheld entries on a bonus check. To adjust this detail, click the Open Paycheck Detail button to modify the default amounts.

5. If you are using the Intuit Enhanced Payroll subscription, you can also select the checkbox for Enter Net/Calculate Gross on the paycheck detail. Selecting this option enables you to specify the net amount; QuickBooks then calculates the gross amount to cover taxes and withholdings.

6. QuickBooks might display a warning dialog box titled Special Calculation Situation to inform you that certain payroll items have reached their limits.

7. In the example in Figure 12.12, the Federal Withholding amount that was automatically calculated was removed. QuickBooks now shows that this paycheck was adjusted.

Figure 12.12. QuickBooks identifies when automatic payroll calculations have been manually adjusted.

Caution

Adjust paychecks cautiously, making sure you do not adjust items that have a predefined tax table amount, such as Social Security and Medicare. If you do and the adjustment causes the calculated totals to be incorrect for the year, QuickBooks self-corrects the taxes on the next payroll check you create for this employee. You should also obtain the advice of your tax accountant before adjusting taxes withheld on bonus payroll checks.

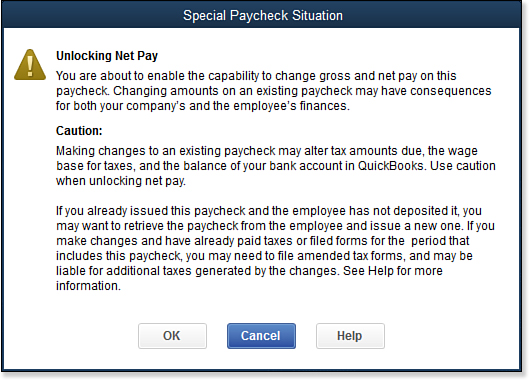

Adjusting an Employee Paycheck

You should rarely need to adjust a paycheck record in QuickBooks. One example is when you hand-prepare a check and later discover that QuickBooks calculated a different net pay amount.

In this example, the check amount the employee cashed differs from what QuickBooks computed, so adjusting the QuickBooks paycheck is acceptable.

To adjust a prepared employee check before it is printed, or to adjust a paycheck that had the wrong amount in QuickBooks from what was recorded on the actual check, follow these steps:

1. Locate the paycheck in your checking register by clicking the Check Register icon on the QuickBooks Home page.

2. If you have multiple checking accounts, select the account the paycheck was recorded to and click OK to open the bank register.

3. Find the check with the incorrect amount; open the paycheck transaction by double-clicking the check.

4. Click the Paycheck Detail button to display the detail of the check to be modified.

5. Click Unlock Net Pay and review the caution message QuickBooks provides about changing net pay on existing checks. Click OK to close the message (see Figure 12.13).

Figure 12.13. QuickBooks protects inadvertent changes by requiring you to unlock net pay before modifying a paycheck record.

6. Modify the check as needed, being careful not to modify the Social Security or Medicare taxes. Modify the check to reflect the actual check amount that cleared.

7. Click OK to close the dialog box.

8. Click Save & Close to save the changes to the paycheck.

Cautiously consider the effect of changes you make to existing paychecks on previously filed payroll tax returns.

Allocating Indirect Costs to Jobs Through Payroll

This section provides instructions for allocating “indirect” job costs, or costs that your company incurs but that cannot be easily associated with a job. The term allocating used here refers to distributing costs to jobs independent of the original cost record. Costs such as cell phones, automobile fuel, training fees, uniforms, and small tools are practically impossible to assign to jobs.

However, don’t confuse these costs with the general and administrative costs of the business. These costs are essential to your overall operations and are relatively stable.

Why do I mention this at all? If you review your Profit & Loss report and total the collective value of these costs, it can be significant—and when these costs are not associated with jobs, a job’s profitability is overstated.

To begin, make sure that you assign a customer or job to each line on expense transactions. Additionally, using the Items tab (see Figure 12.14) enables you to include these costs in a variety of Job Profitability reports that are item based. To access these reports, from the icon bar, select Reports, Jobs, Time & Mileage.

Figure 12.14. Properly record job costs using the Items tab, and assign a customer or job to the line.

If your company performs much of the labor associated with your service or product (instead of subcontracting the work to a vendor), you can use the payroll records to automatically allocate these costs to customers or jobs. This is easy using just a few steps, as the following sections illustrate.

Identify Costs and Allocation Rate

The first step in this process is to review your Profit & Loss report and identify which expense accounts you post your indirect job expenses to without assigning a customer or job. These costs are easy to identify; they increase when you have more jobs and decrease when you have fewer jobs.

Because this method uses payroll as the tool to automatically allocate the costs, you next need to estimate the number of payroll hours in the period you will be allocating expenses.

Following is an example that you should be able to replicate with your own data. After reviewing my company’s Profit & Loss report, I estimate the cost of paying for employee’s cellular phones yearly is $15,000.00. I also estimate the yearly labor hours to be 16,000 hours. To arrive at the overhead allocation rate as a per-hour cost, I divide the estimated cost by the estimated hours. In this example, the per-hour cost is rounded to 94 cents per hour.

Create Payroll Items for Allocating

After identifying the indirect expenses and the per-hour allocation rate, you are ready to create list items. You need to create the following:

• Chart of Accounts Allocation Account—I recommend that you create a new chart of accounts specifically for the allocation amount (see Figure 12.15). Having a separate account helps you identify over time whether the allocation estimate is closely matched to the like expense being recorded. The normal balance for this type of account is a negative expense balance.

Figure 12.15. Creating a unique account for the allocated costs helps identify them when viewing reports.

• Company Contribution Payroll Item—This item does not affect the employee’s gross earnings or net pay. The newly created payroll item provides the means to automatically allocate the cost to a job through the payroll record. When creating this item, follow these guidelines:

• Select Track Expense by Job checkbox.

• In the Liability Account (Company-Paid) field, assign the newly created allocated expense account. This account is “credited” during the payroll process.

• In the Expense Account field, assign the Cost of Goods Sold account, or whatever account you want the allocated costs to record to.

• Select None for the Tax Tracking Type.

• Do not select any of the taxes (this is the default for this item).

• Select Calculate This Item Based on Hours. This is important because your allocation is based on hours.

• Enter Default Rate (this is your allocation rate). In the current example, the rate is .94.

→ To learn more about working with these lists, see “Chart of Accounts,” p. xxx, and “Setting Up Payroll Items,” p. xxx.

Allocating Through Payroll Records

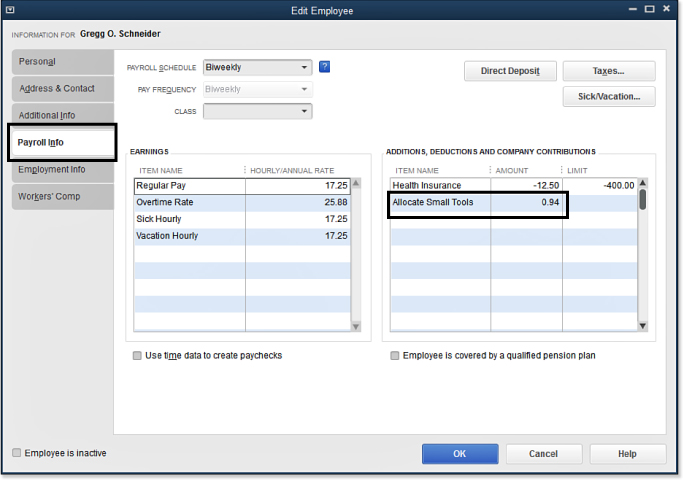

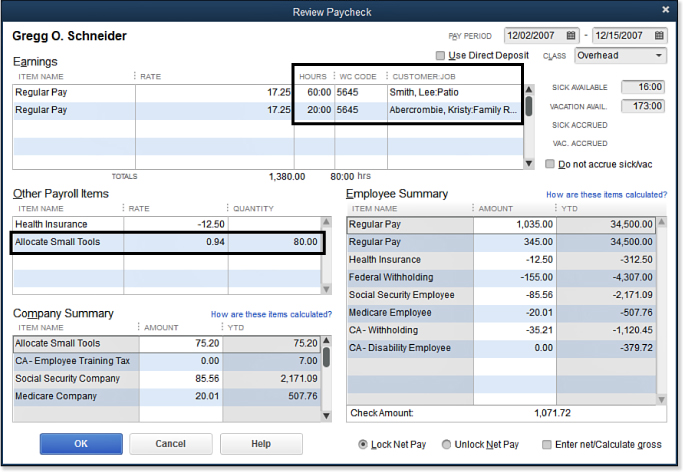

The method this section details presumes that your company performs the labor instead of hiring vendors to provide the labor for your product. For laborers you included in your estimated hours, add the newly created company contribution calculation to their employee record, on the Payroll Info tab. See Figure 12.16 and the added Allocate Small Tools calculation.

Figure 12.16. Using payroll calculations, you can allocate overhead expenses to jobs.

When you create a paycheck, QuickBooks uses this allocation payroll item in calculating the company’s costs. This payroll item had a tax tracking type of None and does not affect the employee’s gross or net wages.

Assigning the Calculate This Item Based on Hours option when you set up the payroll item distributes the estimated hourly cost of the small tools to the two jobs reported on the paycheck in Figure 12.17.

Figure 12.17. QuickBooks automatically uses the hours on the paycheck to allocate the estimated costs to the jobs.

Reporting on Actual and Allocated Costs

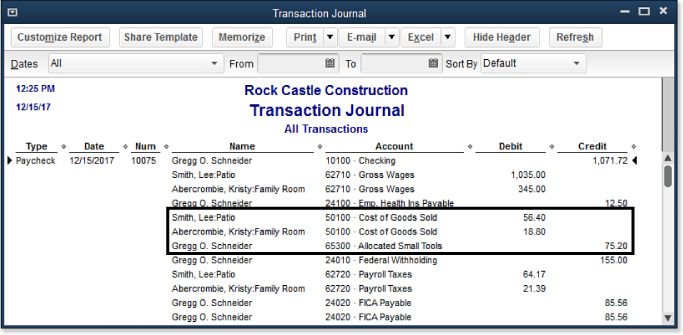

When you first begin using this method, you want to verify the payroll item provided for the desired accounting. I find the Transaction Journal report the easiest way to see the accounting that goes on behind the scenes with the payroll items.

From the checkbook register, select a paycheck record that used this newly created allocation item. From the ribbon toolbar at the top of the displayed check, select the Reports tab, Transaction Journal. The Transaction Journal report for the paycheck shown previously in Figure 12.17 displays in Figure 12.18.

Figure 12.18. Review the Transaction Journal report, verifying the accuracy of your payroll item setup for allocating overhead costs.

In this example, QuickBooks calculates 80 hours at the .94/hour allocation rate. The total amount is then distributed to the two jobs using a weighted average. The job with the most hours receives the highest allocated cost.

Allocating indirect job expenses takes just a few steps and results in more accurate job profitability reporting.

Depositing a Refund of Payroll Liabilities

If you received a refund from an overpayment of payroll taxes, you should not add it to a Make Deposits transaction (as with other deposits you create). If you do, the refunded amount will not correct your overpayment amount showing in the payroll liability reports and in certain payroll forms.

This type of payroll error rarely, if ever, occurs in current versions of QuickBooks, thanks to improved messaging and ease of creating payroll transactions from the Payroll Center.

However, if you were paying your payroll liabilities outside the QuickBooks payroll menus and you had an overpayment that you requested and received a refund for, you can record the deposit to reflect receipt of the overpayment in your payroll reports. To do so, follow these steps:

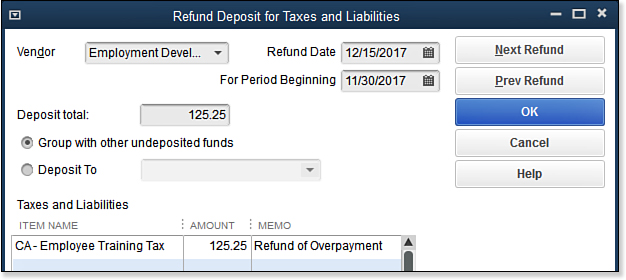

1. From the menu bar, select Employees, Payroll Taxes and Liabilities, Deposit Refund of Liabilities. The Refund Deposit for Taxes and Liabilities dialog box displays.

2. Select the name of the payroll tax liability vendor.

3. Enter the Refund Date (the date of your deposit).

4. Enter the For Period Beginning date (this should be the payroll month or quarter the overpayment was in).

5. Enter the Deposit Total of the refund.

6. Click the Group with Other Undeposited Funds button if this item is included on a bank deposit ticket with other deposit amounts; alternatively, select the Deposit To button to create a single deposit entry, and select the appropriate bank account from the drop-down list.

7. Select the Payroll Item that needs to be adjusted.

8. (Optional) Add a Memo so that you have a record of why this transaction occurred. Click OK.

See Figure 12.19 for a completed Refund Deposit for Taxes and Liabilities transaction.

Figure 12.19. Use the proper transaction when recording a refund of overpaid payroll liabilities.

Recording Payroll When Using an Outside Payroll Service

In Chapter 11, you learned about several Intuit-provided payroll subscription offerings that integrate with your QuickBooks software. If your company uses another payroll provider, you might find these instructions handy for recording the payroll activity in your QuickBooks file.

When using an outside payroll service, I encourage you to request comparative pricing for Intuit’s Assisted or Full Service Payroll offerings. One of the primary benefits of using an Intuit-provided payroll service is that you can track your employees’ time to jobs in QuickBooks and let Intuit take care of the rest of the payroll responsibility.

The method I recommend for recording this payroll makes the following assumptions:

• You want to track your employees’ time to customers or jobs.

• You value the customer or job profitability reports found by selecting Reports, Jobs, Time & Mileage from the menu bar including to name just a few:

• Job Profitability Summary or Detail

• Item Profitability

• Profit & Loss by Job

• You subscribe to one of Intuit’s payroll offerings.

• Your outside payroll vendor consolidates the charges to your bank account, usually two large debits. A typical payroll provider debits your bank account one lump sum for the net amount of the checks and another for payment of taxes to the IRS on your behalf.

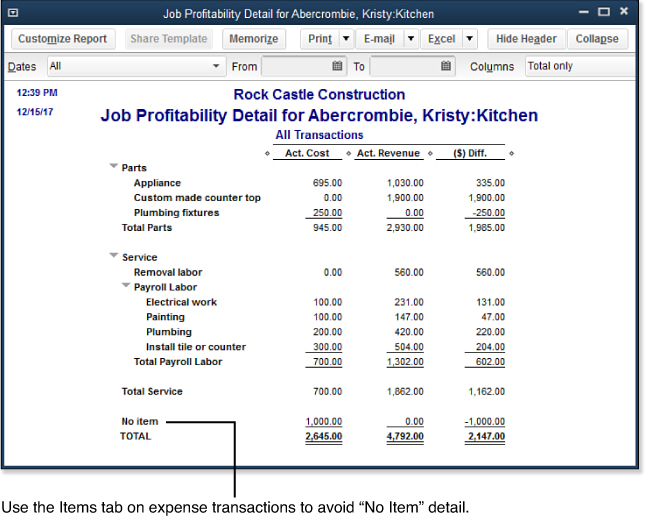

If your company does not need or want any of the previously listed items, you can continue recording the payroll using your current method. Be aware that, if you use a journal entry to record these payroll expenses, many of the Job Profitability reports will not reflect the information properly. Instead, use the Items tab on a check or vendor bill (refer to Figure 12.14) so that your Job Profitability reports provide complete details (see Figure 12.20).

Figure 12.20. Using paycheck transactions provides job profitability reports by labor type.

The following steps can help you track payroll costs to customers or jobs and record the company’s payroll expense. Chapter 11 has detailed instructions for each of these steps.

1. Create a bank account on the chart of accounts list and name it Payroll Clearing. The purpose of this account is to record individual net payroll checks. Many payroll vendors debit your bank account for the lump-sum total of the payroll checks, not individually.

2. Sign up for one of Intuit’s payroll subscriptions. If you don’t sign up for a subscription, you have to manually type the payroll calculation amounts that your payroll provider details for you. Your time is worth the expense!

3. Complete the payroll setup as detailed in Chapter 11. One exception: Because a payroll service is controlling your payroll, use a single Payroll Liabilities account for all taxes due.

4. Prepare timesheets, or record time directly on a paycheck transaction. QuickBooks calculates the expected additions or deductions for you based on your setup.

5. Assign the fictitious bank account named Payroll Clearing to each paycheck.

6. Compare your current payroll totals in QuickBooks to your vendor’s payroll reporting by selecting Reports, Employees & Payroll, Payroll Summary. Minor differences due to rounding are expected.

7. To record your vendor’s lump-sum debit to your bank account, select Banking, Transfer Funds from the menu bar.

8. Enter the date the vendor debits (charges) your bank account.

9. In the Transferred Funds From drop-down list, select the bank account that will be charged.

10. In the Transfer Funds To drop-down list, select the Payroll Clearing bank account.

11. Review the remaining balance in the Payroll Clearing account. From the menu bar, select Banking, Use Register, and select the Payroll Clearing bank account. Click OK.

12. If the balance is not zero, enter an adjusting entry in the next available row. Enter ADJ in the Number column; enter an amount in the Payment column to decrease or in the Deposit column to increase.

13. Assign an expense account of your choice for this small adjustment, and click Record. Your Payroll Clearing account should now have a net zero balance.

14. Record your vendor’s payment of the payroll taxes by selecting Banking, Write Checks from the menu bar.

15. From the Bank Account drop-down list, select the bank account from which your payroll taxes are withdrawn.

16. Enter the word Debit in the No. field, and select the date the charge is made to the bank account.

17. Select your payroll service vendor in the Pay to the Order Of drop-down list.

18. Enter the Amount in the field next to the payee name.

19. In the Account column on the Expenses tab, select your payroll liability account. I recommend simplicity here, using a single payroll liability account. You have a payroll service closely monitoring your payments; you might not need the same level of detail on your own balance sheet.

20. Click Save & Close to finish recording the payroll tax payment.

Check your work for accuracy. Your Payroll Clearing account should have a zero balance. The Payroll Liability account on your Balance Sheet should have a zero balance. Your job profitability reports accurately track payroll costs, and your bank register shows the debit transactions your payroll vendor made.