5 Cost and Economic Evaluation

5.1 INTRODUCTION

As was stated previously, reliability and service quality are very important, but “cost is king” in almost all-electric distribution decisions, both those made by consumers and by utilities. Every decision contains or implies certain costs: equipment, installation labor, operating, maintenance, losses, and many others. Regardless what type of paradigm is being used, and whether traditional or new technologies are being considered, planners and decisionmakers must deal with cost as a major element of their evaluation.

Many planning decisions revolve around selecting from alternatives on the basis of when they call for money to be spent. Two plans might be equal with respect to capacity and reliability, but different in both when and how much they require to be spent: one might eventually spend a lot, but only in the long run; the other might spend less, but call for more initial investment. At what point is the planner justified in picking the larger total expense because most of it lies far into the future?

This chapter provides a brief tutorial on engineering economics for planning to provide a basis for the methods applied later in the book. Section 5.2 reviews the major elements of cost. Section 5.3 looks at the time value of money and future-cost discount methods. Benefit cost analysis is covered in Section 5.4, and marginal benefit cost analysis, a cornerstone of aging infrastructure planning, in Section 5.5. Only a quick review is given here. More comprehensive treatment is available in books listed at the end of this chapter.

5.2 COSTS

“Cost” is the total sacrifice that must be expended or traded in order to gain some desired product or end result. It can include money, labor, materials, resources, real estate, effort, lost opportunity, and anything else that is given up to gain the desired end. Usually, the costs of these many different resources and commodities are measured on a common basis - money - by converting materials, equipment, land, labor, taxes and permits, maintenance, insurance, pollution, and lost opportunity costs to dollars, pounds, marks, yen, or whatever currency is most appropriate.

In those cases where all these elements can be put on a common basis, the subsequent planning can be done in a single-attribute manner. The goal being to achieve the planner’s goals while minimizing the total cost by trading the cost of one item against the others to find the best overall mix. However in some cases, one or more types of cost cannot be converted to money, for example, aesthetic impact or other “intangibles.” In such cases, multi-attribute planning and cost minimization must be done, involving more complicated evaluation methods (D. Atanackovic et al, 1997).

Types of Cost

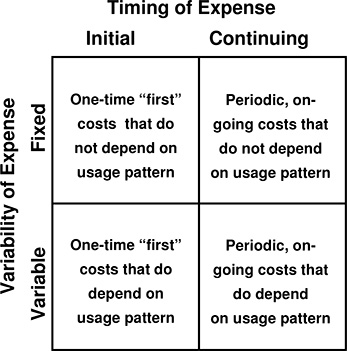

Initial cost is what must first be spent to obtain the facility or resource. It includes everything needed to put the facility in place, and is usually a single cost, or it can be treated as a single cost in planning studies if a series of costs over a period of time lead up to completion of the facility.

Continuing costs are those required to keep the facility operational and functioning the way its owner wants it to do. They include inspection and maintenance, fuel, supplies, replacement parts, taxes, insurance, electrical losses, and perhaps other expenditures. They persist as long as the facility is in use. Usually, continuing costs are studied on a periodic basis - daily, monthly, or annually.

Fixed costs are those that do not vary as a function of any possible variable element of the planning analysis or engineering study being carried out. For example, the annual costs of taxes, insurance, inspection, scheduled maintenance, testing, re-certification, and so forth, required to keep a 500 kW DG unit in service, do not vary depending on how often or heavily it is run. They are fixed costs.

By contrast, the DG unit’s fuel costs do vary with usage - the more it is run the higher the fuel costs. These are variable costs, a function in some manner of the amount of load served. Some types of maintenance and service costs may be variable, too. Highly used DG units need to be inspected and stress-caused wear and tear repaired more often than in units run for fewer hours.

Figure 5.1 Two characterizations, one based on when costs occur and the other on how they vary with usage, result in four categories of costs.

Figure 5.1 shows how these two sets of categorizations – initial, continuing, fixed, and variable - can be combined. This two by two matrix allows planners to identify fixed initial costs, variable initial costs, fixed continuing costs, and variable continuing costs. In this way, costs in studies can be characterized simultaneously by both their relationships to time and how they respond to assumptions about usage.

Sunk Cost

Once a cost has been incurred, even if not entirely paid, it is a “sunk cost.” For example, once a facility has been constructed and is in operation, it is a sunk cost, even if ten years later the company still has its capital depreciation on its books as a cost.

Embedded, Marginal, and Incremental Cost

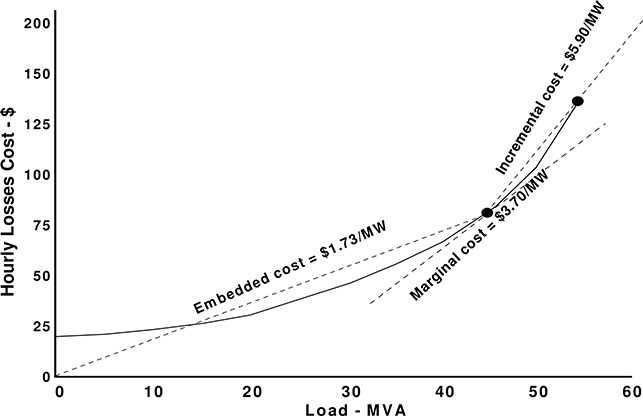

Embedded cost is that portion of the cost that exists in the current system, configuration, or level of use. Depending on the application, this can include all or portions of the initial fixed cost, and all or parts of the variable costs.

Figure 5.2 Hourly cost of losses for power shipped through a substation transformer as a function of the load. Currently loaded to 45 MVA, it has an “embedded” loss cost of $1.73/MVA, and a marginal cost of losses at that same point of $3.70/MVA. The incremental cost of losses for an increase in load to 55 MVA load is $5.90/MVA.

Often, the “embedded” cost is treated as a fixed cost in subsequent analysis about how cost varies from the current operating point. Marginal cost is the slope (cost per unit) of the cost function at the current operating point (Figure 5.2). This point is usually (but not always) the point at which current embedded cost is defined.

Incremental cost is the cost per unit of a specific jump or increment - for example, the incremental cost of serving an additional 17 MVA from a certain substation or the incremental cost of losses when load on a feeder decreases from 5.3 to 5.0 MVA. Marginal and incremental costs both expresses the rate of change of cost with respect to the base variable, but they can differ because of the inconsistencies and variances in the cost relationships.

In the example shown in Figure 5.2, the marginal cost has a slope (cost per unit change) and an operating point (e.g., 45 MW in Figure 5.2). Incremental cost has a slope and both “from” and “to” operating points (e.g., 45 MVA to 55 MVA in Figure 5.2) or an operating point and an increment (e.g., 45 MW plus 10 MVA increase).

5.3 TIME VALUE OF MONEY

Expenses Now and Then

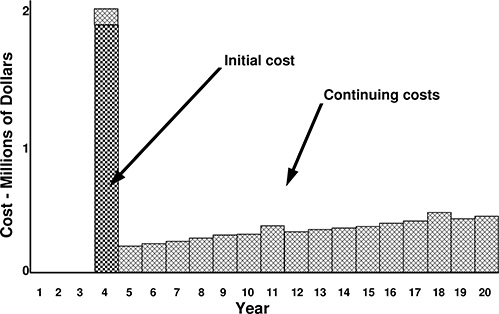

Almost any electrical project has both initial and continuing costs. Figure 5.3 shows the costs for a new distribution substation, planned to serve 65 MW of residential load on the outskirts of a large city. It has a high initial cost that includes the equipment, land, labor, licenses and permits, and everything else required in building the substation. Thereafter, it has taxes, inspection, maintenance, electrical losses, and other continuing costs on an annual basis. Figure 5.4 shows the initial and continuing costs identified with respect to fixed and variable categories, too. Typical of most electrical planning situations, the initial cost is almost entirely fixed, and the continuing costs are mostly variable.

Decisions Based on When and How Much is Spent

Any utility planner must deal with two types of time versus money decisions. The first involves deciding whether a present expense is justified because it cancels the need for some future expense(s). For example, suppose it has been determined that a new substation must be built in an area of a utility’s service territory where there is much new customer growth. Present needs can be met by completing this new substation with only one 25 MVA transformer, at a total initial cost of $1,000,000. Alternatively, it could be built with two 25 MVA transformers installed, at a cost of $1,400,000. Although not needed immediately, this second transformer will be required within four more years because of continuing growth. If added at that time, it will cost $642,000 extra - $242,000 more than if it is included at the time the substation is first built. The higher cost to add it later is a common fact of life in T&D systems’ planning and operation. It’s also a reflection of the additional start-up cost for a new project and of the higher labor and safety costs required for installing a transformer at an already-energized substation, rather than when the site is cold.

Which plan is best? Should planners recommend that the utility spend $400,000 now to avoid a $642,000 expense four years from now?

A second and related type of time-vs.-money decision is determining if a present expense is justified because it will reduce future operating expenses by some amount. Suppose two types of distributed generators are candidates for installation at a high-reliability customer site. The first, Type A, costs $437,000 installed. It fully satisfies all loading, voltage regulation, and other criteria. On the other hand, the higher efficiency type B unit will also meet these same requirements and criteria and lower annual fuel costs by an estimated $27,000 per year. However, it has an initial cost of $597,000. Are the planners justified in recommending that $160,000 be spent, based on the long-term fuel savings?

Figure 5.3 A new substation’s costs are broken into two categories here, the initial cost, a one-time cost of creating the new substation, and its continuing annual costs which are required to maintain it in operation.

Figure 5.4 The new substation’s costs can also be viewed as composed of both fixed costs - those that are constant regardless of loading and conditions of its use, and variable costs. Those costs change depending on load, conditions, or other factors in its application as part of the power system. In this example, the variable costs increase nearly every year, reflecting higher losses’ costs as the load served gradually increases due to load growth.

These decisions, and many others in utility planning, involve comparing present costs to future costs, or comparing plans in which a major difference is when money is scheduled to be spent. To make the correct decision, the planner must compare these different costs in time on a sound, balanced basis, consistent with the electric utility’s or DG owner’s goals and financial structure.

Common Sense: Future Money Is Not Worth As Much As Present Money

Few people would happily trade $100 today for a reliable promise of only $100 returned to them a year from now. The fact is that $100 a year from now is not worth as much to them as $100 today. This “deal” would require them to give up the use of their money for a year. Even if they do not believe they will need to spend their $100 in the next year, conditions might change and they might discover later that they do need that money. Then too, there is a risk that they will not be re-paid, no matter how reliable the debtor.

Present Worth Analysis

Present worth analysis is a method of measuring and comparing costs and savings that occur at different times on a consistent and equitable basis for decision-making. It is based on the present worth factor, P, which represents the value of money a year from now in today’s terms. The value of money at any time in the future can be converted to its equivalent present worth as:

Value today of X dollars t years ahead = X × Pt (5.1)

Where P is the present worth factor

And t indexes the year ahead

For example, suppose that P = .90; then $100 a year from now is considered equal in value to today’s money of

100 × (.90) = $90

and $100 five years from now is worth only

$100 × (.90)5 = $59.05

Present worth dollars are often indicated with the letters PW. Today’s $100 has a value of $100 PW, $100 a year from now is $90 PW, $100 five years from now is $59.05 PW, and so forth.

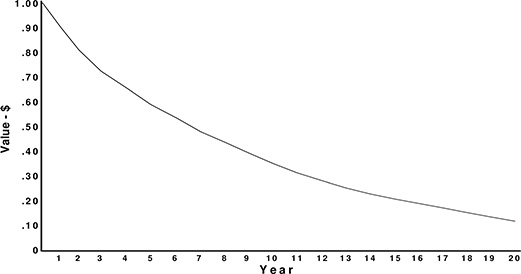

Figure 5.5 Present Worth Analysis discounts the value, or worth, of a dollar the further it lies in the future. Shown here is the value of one dollar as a function of future year, evaluated at a .90 present worth factor (11.1% discount rate).

Alternatively, the present worth factor can be used to determine how much future money equals any amount of current funds. For example, to equal $100 present worth, one year from now a person would need

$100/.90 = $111.11

Two years from now, one would need $100/(.90)2 = $123.46 to equal $100 PW.

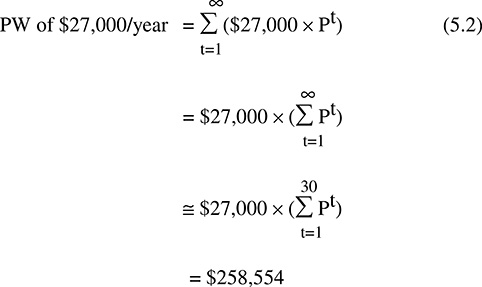

A continuing annual future cost (or savings) can be converted to a present worth by adding together the PW values for all future years. For example, the present worth of the $27,000 in annual fuel savings discussed for the type B DG unit earlier in this chapter can be found by adding together the present worth of $27,000 next year, $27,000 the year after, and so forth

Discount rate

Present Worth Analysis essentially discounts the value of future costs and savings just because they lie in the future, as shown in Figure 5.5. The discount rate used in an analysis, d, is the perceived rate of reduction in value of money from year to year. The present worth factor is related to this discount rate

P(t) = 1/(1+d)t (5.3)

Where d = discount rate

And t = future year

If d is 11.11%, it means that a year ahead dollar is discounted 11.11% with respect to today’s dollar, equivalent to a present worth factor of P = (1/1.111) = .90. Therefore, $111.11 a year from now is worth $111.11/1.1111 = $100 today. A decision-making process based on the values of d = 11.11% and PWF = .90 would conclude that spending $90 to save $100 a year from now was a break-even proposition (i.e., there is no compelling reason to do it). While if the same $100 savings can be had for only $88, the “deal” has a positive value.

A higher discount rate, corresponding to a lower present worth factor, renders the decision-making process less willing to trade today’s costs for future costs. If the discount rate is doubled, to 22.2%, P drops to .82. Now, $88 spent today to obtain a $100 cost reduction a year from now is no longer viewed as a good investment: that $88 must yield at least $88/1.222 = $108 a year from now to be viewed as merely break even.

Present worth analysis does not say “no” to truly essential elements of a plan

Power system planners with a commitment to see that service is always maintained often fall into a trap of wanting to build everything as early as practical in order to have plenty of capacity margin and to allow for unexpectedly high load growth. As a result, they come to view present worth analysis, and any other aspect of planning that might say “delay,” as negative.

But this is not the case. If applied correctly, present worth analysis never says “no” to essential expenses, for additions or changes that must be done now. For example, if a hurricane has knocked down ten miles of critically needed lines; there is no question about the timing of the expense in putting it back up. That must be done as soon as conditions permit, and present worth analysis is not even appropriate to apply to the decision.

Present Worth Analysis should be used to evaluate and rank alternatives only when there is a difference in the timing of expenses (the substation could be built this year or next year), or when costs and savings that occur at different times must be balanced (more spent today will lower cost tomorrow). Present worth analysis is an essential element of keeping costs as low as possible, and it should be applied in all situations where alternatives differ with respect to when expenses will be incurred.

How Are Present Worth Factors and Discount Rates Determined?

There is no one rule or set of guidelines that rigorously defines what contributes to the present worth factor (PWF), or its companion, the discount rate. Likewise, there is no inviolate formula like Ohm’s law or Schroedinger’s equation that lays out completely and with no exceptions exactly how to compute PWF from those factors that are deemed relevant. Quite simply, PWF is merely a number, a decision-making tool that allows planners to compare future expenses to present ones. The present worth factor is often arrived at through careful analysis and computation, but sometimes it is an empirical estimate “that just works well.”

The present worth factor is simply a value that sums up all the reasons why an organization would prefer to spend money tomorrow rather than today.

There can be many reasons why a person may wish to limit spending today in favor of spending tomorrow. These reasons all influence the selection of a value for the present worth factor. Priorities vary greatly from one company to another and also change with time. Among them is one-reason planners often finding difficult to accept: “We just don’t have the money, period.” In most electric utilities, present worth factors and discount rates are determined by a utility’s financial planners and based on the company’s regulatory requirements for financing and use of money. The methods applied to fix these requirements quantitatively and their relation to PWF are beyond the scope of this discussion, and available in other texts (e.g., IEEE Tutorial on Engineering Economics). However, it is worth looking at some of the primary influences on the present worth factor and how and why they influence it.

Interest rate

The fact that it takes more future dollars to equal a dollar today is often attributed to interest rate: a person who has $100 today can invest it at the prevailing interest rate, i.e., so that a year from now it will be (1+i) times as much. Thus, $100 invested today at an annual rate of 5% interest will be worth $105 a year from now and $128 five years from now. If the prevailing interest rate is 5%, then it is cost-effective to spend $100 only if it will save or return a value a year from now that exceeds $105. Otherwise, it would be better simply to leave the money invested and drawing interest. A PWF of .952 can be applied in a present worth analysis as described earlier, and will lead to decisions that reflect this concern.

But, in practice, present worth factor clearly represents something more than just interest rate, because the present worth factor as applied by most electric utilities is nearly always greater than what corresponds to the prevailing interest rate. For example, at the time of this writing, the inflation-adjusted interest rate on safe, long-term investments is about 5%, yet most utilities are using a present worth factor of about .11, equivalent to a 12.4% interest rate.

The difference, 12.4% versus 5.5% in this case, is attributable to other factors, although it may prove difficult or impossible for a distribution planner to determine and quantify all of them.

Inflation

Inflation is not one of the factors normally taken into account by the present worth factor, although this is often misunderstood, and new planners often assume it is a part of the analysis. Inflation means that what costs a dollar today will cost more tomorrow - 3% annual inflation would mean an item costing a dollar today will be priced at $1.03 a year from now. While inflation needs to be considered by a utility’s financial planners, distribution planners can usually plan with constant dollars, by assuming that there is no inflation.

The reason is that inflation raises the cost of everything involved in distribution planning cost analysis. If inflation is 3%, and then on average a year from now equipment will cost 3% more, labor will cost 3% more, as will paperwork and filing fees and legal fees and taxes and replacement parts and transportation and everything else. More than that, over time inflation will call for similar adjustments in the utility’s rates, in the value of its stock, its dividends, and everything associated with its expenses and financing (including hopefully the planners’ salaries). It affects nearly every cost equally, at least to the extent that costs can be predicted in advance.1 From the standpoint of planning, since inflation makes no impact on the relative costs of various components, it can be ignored, making the planning process just a bit easier.

Some utilities do include inflation in their planning and in their present worth analysis. In such cases, an increment to account for inflation is added to the discount rate. Given a 5% interest rate and a 3% inflation rate discussed above, this would mean that the planners’ present worth factor might be

P = 1/(1+5%+3%) = .926

Present worth analysis would now compare today’s investment measured in today’s dollars against tomorrow’s investment measured in tomorrow’s inflated dollars. This type of accounting of future costs must sometimes be done for budgeting and finance estimation purposes.2

1 In actuality, utility and business planners and executives all realize that inflation will not impact every cost equally, but small variations in individual economic sectors have proven impossible to predict. In cases where there is a clear indication that certain costs will rise faster or slower than the general inflation rate, that difference should be taken into account.

Inflation must be included in the analysis, but all planning can be done with “constant dollars”

However, while an “inflated dollars” present worth analysis sometimes has to be done to estimate budgets, it is rarely an effective planning tool. Planning and decision making are facilitated when expenses and benefits are computed on a common basis - by measuring costs from all years in constant dollars. Is plan A, which calls for $1.35 million in expenses today, worth more than plan B, which costs $1.43 million three years from now? If both plans have been calculated using their respective present worth measured in constant dollars, then it is clear that plan A is the less costly of the two. But if inflation were a factor in the present worth analysis, then one has to do further adjustment of those numbers to determine which is best. (At 3% inflation, $1.35 million in three years will equal $1.48 million in then inflated dollars, making plan B, which costs $1.43 million three-year ahead inflated dollars, the better plan). Beyond this, errors or unreasonable cost estimates for future projects are more readily caught when expressed in non-constant dollars. For these reasons, present worth analysis in constant dollars is often used for planning, but an initial analysis, which accounts for inflation, may occasionally be needed for other purposes.

Earnings targets

The present worth factor for a dollar under the utility’s control should be higher than 1/(1 + interest rate), because the utility must be able to do better with its earnings than the prevailing interest rate. If a utility cannot better the prevailing interest rate with its own investment, then it should liquidate its assets and invest the results in earning that interest rate. Frankly, it won’t get the chance to do so: long before that, its shareholders will sell their stock and invest their money elsewhere, in companies that can beat the prevailing interest rate through their investment of the stockholder’s money.3 Therefore, a goal must be to use the company’s money to earn more than it could by other safe means.

2 For example, when estimating a future budget, the costs often do have to be put in dollars for the years being estimated, and those are inflated dollars.

3 Planners from municipal utilities may argue that this does not apply to them, but that is not necessarily true. If a municipal electric department cannot “earn” more from its investments than other businesses could, it is costing the city money to design and operate a system that needs to be subsidized by taxpayer money. Such subsidized operation may be the policy of the city government (some city governments deliberately subsidize commercial electric rates, using the low rates as a tool to attract employers to their region). Regardless, its planners should try to get as sound a return as possible.

As a result, while the prevailing interest rate may be 5%, the utility’s financial planners may have determined that a 12% earnings potential on all new expenditures is desirable. Rather than a PWF of .952 (5% interest) the utility would use a PWF of .892 (12%) to interject into the decision-making process its unwillingness to part with a dollar today unless it returns at least $1.12 a year from now. This is one tenet of many corporate plans, that all investments must return a suitable earning.

Risk

One hundred dollars invested with the promise of $108 payback a year from now may look good, but only if there is a very small chance that the investment will go wrong, with the loss of the interest and the $100 itself. Such cases are very rare, particularly if investments are made wisely, but there are other types of risks that a utility faces. For example, suppose that shortly after spending $100 to save $108 a year from now, a company gets hit by an unexpected catastrophe (e.g., an earthquake) that damages much of its equipment. It may desperately wish it had that $100 to pay for repairs, work that it simply has to have done to re-establish production. It now has no choice but to borrow the money it needs at short-term interest rates, which might be 12%. In retrospect, its expenditure of $100 to save $108 a year later would look unwise.

In practice, a present worth factor often includes a bias or margin to account for this type of “bird in the hand” value. By raising the PWF from 8% to 10%, the utility would be stating that yes: perhaps $108 is the year-ahead earnings goal. Simply breaking even with that goal is not enough to justify committing the company’s resources: today’s money will be committed only when there are very sound reasons to expect a better than minimum return.

Planning errors

In addition, the present worth factor often implicitly reflects a sobering reality of planning - mistakes cannot be avoided entirely. Under the very best circumstances, even the finest planning methods average about 1% “planning error” for every year the plan is extended into the future. Distribution expansion projects that must be committed a full five years ahead will turn out to spend about 5% more than if the planner could somehow go back and do things over again, knowing with hindsight exactly what the minimum expenditure is needed just to get by.

Adding 1% - or whatever is appropriate based on analysis of the uncertainty and the planning method being used - to the PWF biases all planning decisions so that they reflect this imperfection of planning. This makes the resulting decision-making process slower to spend money today on what appears to be a good investment for tomorrow, unless the predicted savings include enough margin over the element of risk to account for the fact that the planning method could be wrong.

Present Worth Factor Is a Decision-Making Tool, Not a Financial Factor

Thus, the present worth factor and discount rates are merely tools. Present worth analysis is a decision-making method to determine when money should be spent. It can embrace some or all of the factors discussed above, as well as others. Two equally prudent planners might pick very different present worth factors, depending on their circumstances, as summarized in Table 5.1 with the inputs that determined the PWFs used in the mid-1990s by a large investor-owned utility (IOU) in the northwestern United States and a municipality in the southwestern United States.

But while the present worth factor can be affected by many factors, the simple fact is that such determinations are irrelevant to the electric service planner. Present worth factor is used to evaluate and rank alternatives based on when they call for expenditures. It is just a tool, part of the analysis, period.

A relatively low PW factor means that the planning process will be more likely to select projects and plans that spend today in order to reduce costs tomorrow. As the PWF is decreased, the planning process becomes increasingly unwilling to spend any earlier than absolutely necessary unless the potential savings are very great. A very low PW factor will select plans that wait “until the last moment” regardless of future costs.

Table 5.1 Discount Rate “Computation” for Two Utilities

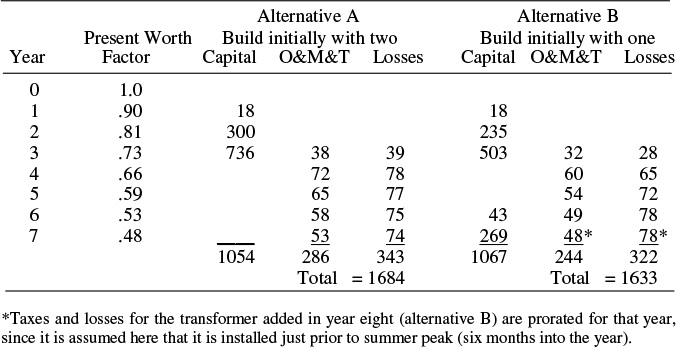

Table 5.2 Comparison of Yearly Expenses by Category for an Eight-Year Period

*Taxes and losses for the transformer added in year eight (alternative B) are prorated for that year, since it is assumed here that it is installed just prior to summer peak (six months into the year).

Comprehensive Present Worth Example

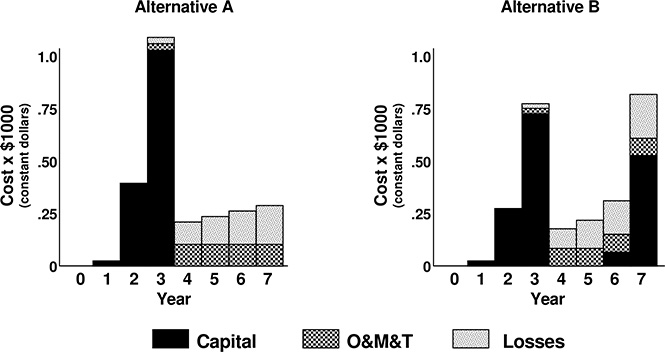

Table 5.2 and Figure 5.6 show more cost details on the two-versus-one substation transformer decision mentioned at the beginning of this section. In the case shown, the decision is being made now (in year zero), even though the substation will actually be built three years from now - the decision must be made now due to lead time considerations. Alternative A calls for building the new substation with two 25 MVA transformers at a total cost of $1,400,000 initially. Alternative B defers the second transformer four years (to year 7), reducing the initial cost to $1,000,000. And again, the addition of the second transformer four years later is estimated to cost $642,000 because of project start-up costs, separate filing and regulatory fees, and the fact that the work will have to be done at what will then be an energized site.

However, this decision involves other costs, which while secondary in importance, should be considered in any complete analysis. For example, no-load losses, taxes, and O&M will be greater during the first four years in Alternative A than in Alternative B. Table 5.2 and Figure 5.6 compare the expenditure streams for the eight-year period for both alternatives, including capital; operations, maintenance, and taxes (O&M&T); and losses.4

4 The table and figure cover the only period during which there are differences that must be analyzed in the decision making. At the end of the eight-year period, the two alternatives are the same – either way the substation exists at that point with two 25 MVA transformers installed. Present worth thereafter is essentially the same.

Figure 5.6 Yearly expenses for the two alternative plans for the new substation (constant dollars).

Note also, that the capital for substation construction in either alternative is not spent entirely in the year the substation is completed. A small amount is spent two years earlier (for filing and preparing for the site), and the site, itself, and some equipment purchased a year earlier so that work can begin on schedule.

In comparing differences in the two alternatives, observe also that the second transformer in Alternative A increases O&M&T costs during the first four years of operation as compared to the other alternative, because taxes must be paid on its additional value, and it must be maintained and serviced.

The difference in losses’ costs is more complicated. Initially, losses are higher if two transformers are installed, because this means twice the no-load losses, and the twin transformers are initially very lightly loaded, so that there is no significant savings in load-related losses over having just one transformer. But by year six the two-transformer configuration’s lower impedance (the load is split between both transformers) produces noticeable savings due to reduced losses as compared to the other alternative.

Overall, Alternative A spends fewer dollars in the period examined $142,000 less. It has the lower amount of long-term spending.

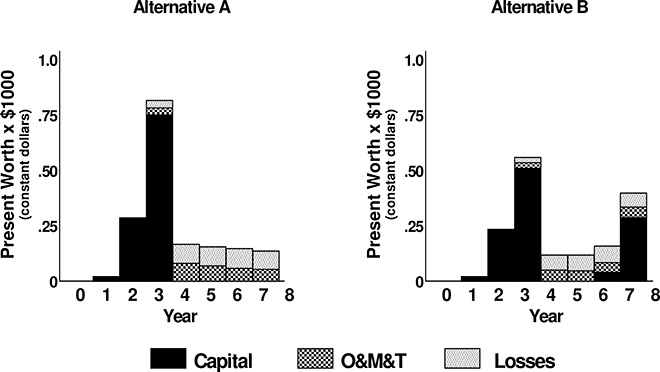

Table 5.3 and Figure 5.7 show the various cost streams for both alternatives converted to PW dollars using a present worth factor of .90 (equivalent to p = 11.11%). Note that dollar amounts have dropped– discounted future dollars just aren’t as valuable as the undercounted dollar figures. More important, is the present worth evaluation reverses the order of cost preference for the two options. Even though its total spending is less, Alternative A is rated a higher present worth by $51,000 PW, because many of its expenses are closer to the present.

The total difference in PW is slightly more than 3% of the average PW value of the alternative. Considering the straightforward nature of this analysis, and the high proportion of the various cost elements common to both alternatives, it is very unlikely that the analysis is in error by 3%. Therefore, this is very likely a dependable evaluation: Alternative B is the recommended “low-cost” option. Alternative A would cost more.

Looking at the sensitivity of this decision to present worth factor, the two alternatives would be considered equal if the evaluation had used a present worth factor of .937, equal to a discount rate of 6.77%. Present worth factor would have to be higher (i.e., the discount rate lower) to have reversed the determination that Alternative B is, in fact, the low-cost option.

Again, considering that nominal PWF values less than .92 are extremely uncommon, the recommendation that Alternative B is the preferred option seems quite sound. Therefore, the planner’s recommendation should be to build the substation with one transformer initially, and add the other at a later time, as needed.

Levelized Value

Often, it is useful to compare projects or plans on the basis of their levelized annual cost, even if their actual costs change greatly from one year to the next. This involves finding a constant annual cost whose present worth equals the total present worth of the plan, as illustrated by Figure 5.7. Leveled cost analysis is a particularly useful way of comparing plans when actual costs within each plan vary greatly from year to year over a lengthy period of time, or when the lifetimes of the options being considered are far different. It also has applications in regulated rate determination and financial analysis. In general, the present worth, Q, leveled over the next “n” years is

Leveled value of Q over n years = Q (d × (1+d)n )/((1+d)n - 1) (5.4)

Thus, the steps to find the leveled cost of a project are: 1) Find the present worth of the project and, 2) Apply equation 5.2 to the present worth. As an example here, using Alternative A’s calculated total present worth of $1,684,000 from Table 5.3, that value can be levelized over the seven-year period in the table as

= $1,684,000 (.1111(1.1111)7/(1.11117 - 1)

= $358,641

Table 5.3 Comparison of Yearly Present Worth by Category for an Eight-Year Period

Figure 5.7 Present worth of expenses associated with the two alternative substation plans given in Table 5.2 and Figure 5.6.

By contrast, Alternative B has a levelized cost over the same period of $347,780. If the utility planned to pay for alternative A or B over the course of that seven-year period, the “payments” it would have to make would differ by a little more than $10,800 per year.

Lifetime levelized analysis

Rather than analyze planning alternatives over a short-term construction period planners or budget administrators often wish to look at a new addition to the system over the period in which it will be in service or be financed.

For example, in the two-or-one transformer substation planning problem presented above, the substation would be planned on the basis of providing a minimum of 30 years of service, and it would be depreciated on the company books for 30 years or more. Therefore, planners should analyze cost over 30 years and compare alternative plans, A and B, on that same basis.

Figure 5.8 shows projected costs for Alternative A over a 32-year period, which includes the first through thirtieth years of service for the substation. The total present worth of the substation’s costs over the period is just over $3 million (construction plus 30 years of O&M&T plus losses), which represents a leveled cost of $348,500/year. By contrast, Alternative B (the less expensive of the two construction schedules, as determined earlier) has a leveled cost of $342,200/year. It saves an average of $5,900/year or about $500/month in terms of a 30-year budget perspective.

Figure 5.8 Cost of Alternative A from Figure 5.7 over a 32-year period that includes its first 30 years of service. Present worth of all cost comes to slightly more than $3,000,000. Leveled over years three through 30, those in which the substation is planned to be in service, this represents an annual cost of nearly $350,000 per year, which can be viewed as the annual cost of providing the substation service.

Table 5.4 Lifetime Analysis of Illumination

Comparing cost over different equipment lifetimes

Very often the lifetimes or periods of cost being considered for two or more options are not equivalent, and yet it is desired to compare their costs on a valid basis. Leveled lifetime cost is a good way to do so. Table 5.4 compares the annual costs of providing 1,000 lumens of illumination (about the equivalent of a standard 75 watt incandescent light bulb) for 2,500 hours per year, using incandescent, halogen, or compact fluorescent lamps, which have expected lives of three, five, and six years respectively. The initial costs, the annual operating costs, and the lifetimes of these three options all differ substantially. In each case, initial and continuing annual energy costs are evaluated on a present worth basis over the lifetime of the particular lamp; then the leveled cost over that period is determined. This permits a comparison that identifies the compact fluorescent as having less than half the annual cost of the incandescent.

In this example, each alternative was evaluated over a different period of time - its lifetime - yet the results are directly comparable. The results are identical to those that would have been obtained from analysis of all over any much longer period, taking replacement costs and other factors into account.

For example, suppose that the analysis in Table 5.4 had compared all three options over a 30-year period. That would have required a series of ten incandescent bulbs, one every three years, six-halogen, and five-compact fluorescent lamps. Each of the sections of Table 5.4 would have extended for 30 years with appropriate PWF, computations, and sums, but the analysis would have reached the same conclusion about which of the three lamps was best.

5.4 DECISION BASES AND COST-EFFECTIVENESS EVALUATION

How does a planner know that a particular project is “best”? In many cases this is determined once present worth analysis has adjusted all costs and savings with respect to equipment lifetime, schedule, and other time-value-of-money considerations. Such decisions are straightforward - in many cases trivial. But determining what to do is not always merely a matter of just identifying the option with the lowest cost. Selection may be based on the relative merits of costs versus savings, the benefits versus cost or the relative gain per dollar invested. In integrated resource planning (IRP) situations, the decision may also depend on the applicable philosophy about what constitutes savings and who should benefit most from a public utility’s investment in the system.

This section briefly reviews cost-effectiveness concepts and methods. More comprehensive discussions of the concepts discussed here and the methods developed to apply them can be found in the references at the end of the chapter.

Lowest Cost Among Alternatives

In many cases and from many perspectives, the goal of planning is to identify an alternative with the lowest cost. If all pertinent costs (capital, losses, O&M&T, etc.) are considered, and the appropriate type of present worth adjustment is made for timing, lifetimes, and schedules, then the alternative with the lowest PW cost is the preferred option.

Payback Period

The period of time required for “long-term” savings to re-pay the initial investment is often used as a measure of the desirability of making an investment in a resource or other addition to the electric supply. Returning to the “type A versus type B DG unit” problem discussed earlier in this chapter, a fuel savings of $27,000 per year will require six years (6 × $27,000 = $162,000) to repay the $160,000 additional cost of the type B unit over type A. (If the break-even is computed based on PW dollars at a .90 PW factor, the payback of the original $160,000 takes ten years.)

“Payback period” analysis is most often used informally, to provide an additional perspective on plans and financing. Rarely is it part of the formal planning criteria or a specific cost-effectiveness test called for by regulatory authority or management. However, it does address one question that can be quite important to any investor - “When will I get my money back?”

Benefit/Cost Ratio Analysis

In many planning situations, one or all of the options being considered have both costs and benefits, and there are constraints or interrelated considerations with respect to both that impact the selection of the plan. In such cases, planning consists of more than simply ranking the alternatives by cost and selecting the one at the top of the list. Alternatives vary in benefit, too. This situation is particularly common in IRP situations, where options such as DSM have a cost, but also benefits accruing from their use.

Very often in such cases, the planning decisions are based on an evaluation of the expected gain versus the cost. Benefit-cost ratio is a simple concept: a ratio less than one indicates the project will lose more than it gains; the higher the benefit/cost ratio above 1.0, the greater the potential gain relative to its cost. For example, suppose that it has been determined that a particular project, with a PW cost of $160,000, would provide PW savings equal to $258,600. A planner could evaluate the benefit to cost ratio of this proposal as

Benefit/Cost = $258,600/$160,000 = 1.62

This alternative has more benefit than cost - 62% more.

Benefit-cost ratio is generally applied as a ranking method, to prioritize projects that are viewed as discretionary or optional, or in cases where there simply isn’t enough funding for all the projects that present worth analysis has indicated are worthwhile. It has drawbacks, however, as explained below.

5.5 BUDGET-CONSTRAINED PLANNING:

MARGINAL BENEFIT/COST ANALYSIS

Example Problem from an Aging Infrastructure System

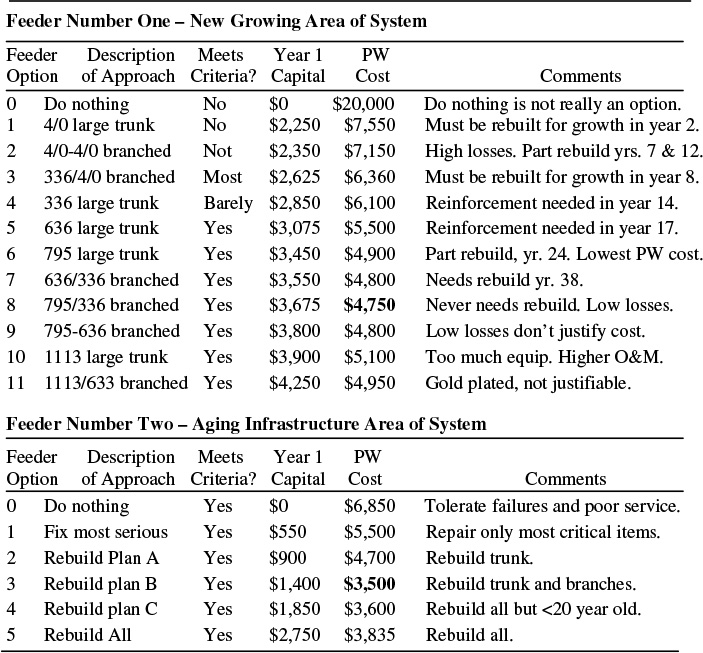

Table 5.5 shows the different planning options available for two feeders in a utility, which has aging infrastructure problems. Feeder 1 does not currently exist, it is being planned for a growing part of a utility service territory where new customers are developing, customers who must be served in order to meet the utility’s obligation to serve (or a wireco’s obligation to connection). This new distribution feeder can be built in any of several sizes and designs, as shown, using conductors and layouts of various types, all with advantages and disadvantages (including differences in cost). The details of exactly what each alternative is, and the differences in costs are unimportant to this discussion. What matters is that there are alternatives for the construction of this new feeder, and that they differ in both ability to handle future growth without further construction and service quality. Note that “do nothing” is listed as an option. This is not a feasible option for the utility, but for completeness sake it is given a PW cost of $20,000,000 – the consequences, at least in part, of not serving these new customers.

Feeder number 2 is an existing feeder with an average equipment age of 45 years, part of an aging infrastructure area of the system. Slow load growth (.3% per capita increase annually) has exacerbated the usual problems that aging causes, leading to below-average service quality. The table shows the capital costs for various rebuilding programs, along with their expected PW costs based on project O&M savings and restoration costs, calculated by analysis of age, equipment condition, load curves, and failure-likelihood. Again, “do nothing” is an option in this case.

Least-Cost Selection of Alternatives (Traditional Approach)

Traditionally, electric utilities have applied a planning paradigm that includes several fundamental assumptions:

1) All new customers will be connected to the system.

2) All new designs will meet standards.

3) Long-term (e.g., present worth) costs will be minimized.

4) Capital funding for any project that meets the above requirements will be forthcoming.

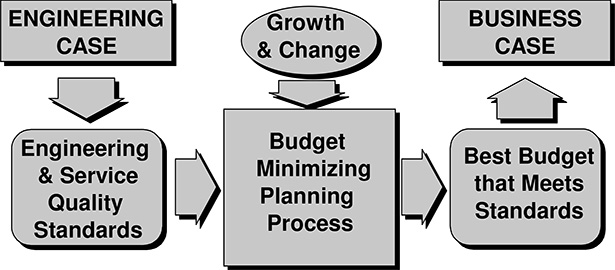

This paradigm can be labeled an engineering-driven paradigm, because engineering requirements (1 and 2 above) drive the decision-making process (3) and define the financial requirement (4). This is illustrated in Figure 5.9.

In this traditional approach, the two alternatives in Table 5.5 would be evaluated for total present worth cost over a long period (usually 30 years) or alternatively on a lifetime basis, adding together present worth costs for both initial and continuing operating costs over the period. If load projections and planning criteria showed that the feeder had to be upgraded during the period, the present worth cost of the future capital cost for that upgrade would typically be included.

Table 5.5 Two Feeder Project Alternatives Evaluated on the Basis of Least-Cost Present Worth Value System at 11% Discount Rate - $ × 1000

Figure 5.9 The traditional engineering-driven approach to prioritizing projects and determining utility budgets.

In each case, the alternative with the lowest PW cost would be selected. In the example shown in Table 5.5, this process would select option 8 for feeder 1 (the 795/336 branched feeder design) at a capital outlay of $3,695,000 and option 3 for feeder 2 (rebuild plan B) at a cost of $1,400,000. The utility would need a total of $5,075,000 in capital for the two projects, probably borrowing the money for this work, as is the typical financial method at most investor owned utilities.

Facing Budget Constraints

Suppose the utility that needed to do both projects listed in Table 5.5 was forced to reduce its capital budget by 30% in order to achieve financial targets for both rate and stock return reasons. This reduction would drop the $5,075,000 capital total for the two projects to an allowable $3,550,000.

One possible adjustment within the traditional paradigm to accommodate budget constraints is to change the time-value of money used in the PW analysis. The discount rate can be raised to 20%, 30%, or even higher, with the result that it “cuts” items from the approval list of projects. Each increase in discount rate reduces the perceived value of future savings from a project, and biases the decision-making process in favor of alternatives with lower initial costs, such as “doing nothing.”

To achieve the desired reduction to below, $3.55 million in this example, a discount rate 38% is necessary. This will force the selection process for the two example projects to $3,550,000 by selecting only option 7 for feeder 1, and selecting nothing for feeder 2. This provides a total cost of $3.55 million (just meeting the budget) and selects “do nothing” for the refurbishment project.

Using this approach, the capital budget required by the planning process is reduced. However, there are four practical problems with this approach:

1. It does not provide a mechanism to force the budget below any specific limit. By trial and error, the utility can find a discount rate that “works out” to the right budget, but it is not a simple process. More important, it is not a dependable process: next year the required discount could be different. This approach does not lead to a simple rule that can be “aimed” at a specific budget target.

2. No ability to make really difficult cuts. As discussed in Chapter 6, PW analysis never says “no” to essential projects. In the face of severe budget cuts, the traditional paradigm still decrees that all new construction must be done, and work must be done to standards.

3. Using a high discount rate is inappropriate. High discount rates means future savings are unimportant, which is not true: The utility’s current financial situation precludes it from affording long-term savings, but this is not the same as saying it does not want them. (The importance of this distinction will become clear in several more pages.)

4. Customers in older areas of the system might legitimately complain that they are not getting the service and attention they deserve. New customers in outlying areas get shiny new service built to high standards. They get old equipment and lousy service.

Raising the discount rate to accommodate this budget reduction needs to change only the relative importance of the future savings against which present costs are evaluated: The planning method still assumes that the goal is to balance long- and short-term costs. Truly deep budget cuts need to be addressed by looking at how necessary the various projects are today, not at how today’s costs weigh against tomorrow’s savings, in any measure. (This will be discussed at length in a few paragraphs.)

Using Benefit/Cost Ratio to Make the Decisions

Ranking projects based on the benefit/cost ratio is often used to decide among project alternatives. This method can compare the present value of savings over the life of the project to today’s cost to implement. One can also evaluate projects based on their payback period. The two methods usually produce comparable results, selecting or rejecting the same sets of projects. With all proposed projects ranked in this manner, the utility can then determine how much capital it would need to finance all worthwhile projects. Alternatively, it can chose to find only those above any arbitrary benefit/cost limit.

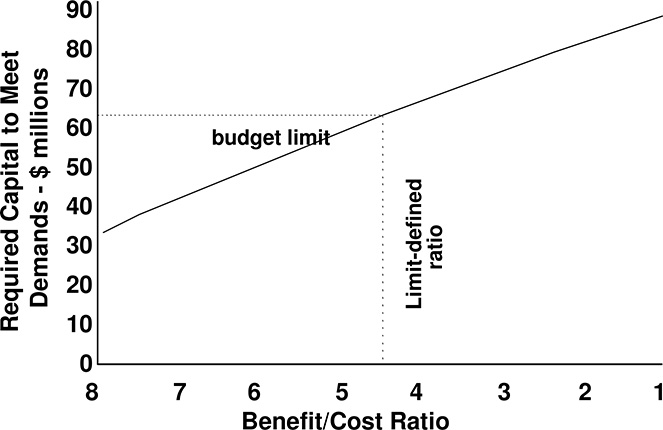

Figure 5.10 plots the results of such analysis for the two feeder projects from Table 5.5, and others that are in the present-year budget. This particular utility needs $88 million to finance all worthwhile projects, as determined by traditional (PW least cost) planning paradigms.

The utility could achieve a budget reduction of 30%, limiting capital spending to only $61.6 million, by approving only projects with a benefit-cost ratio of 4.4:1 or better.

Table 5.6 shows the impact of using benefit cost ratio as the arbiter in prioritizing the two example feeder projects. The benefit cost ratio selected for each option for both projects is shown in the rightmost column. For feeder 1, option 6 is selected (795 large trunk) at $3,450,000. For feeder 2, nothing is selected; all the options fall below the cutoff. The utility would have to have a budget of at least $77 million (only a 12.5% reduction) before any of these projects would be approved.

Figure 5.10 Cumulative capital requirements versus benefit/cost ratio for all “worthwhile” projects. The utility needs $88 million. Using B/C as the prioritization test, a reduction of 30% (to $61.6 million) means it can afford projects only up to 4.4:1, and only those with a B/C ratio above that limit should be approved. Benefit/cost ratio provides a way to limit spending to within a severe budget constraint, but it does not spend that budget most effectively (see text).

Table 5.6 The Two Feeder Projects From Table 5.5 Assessed By B/C Ratio

Results Still Not Completely Satisfactory

The use of B/C ratio as the prioritization for projects resulted in only slight real improvement over the use of a higher discount rate. Of the four objections listed earlier for that approach, there still exist numbers 1 and 4:

1. B/C ratio analysis does not provide a mechanism to force the budget below any specific limit. By trial and error, the utility can find a discount rate that “works out” to the right budget, but it is not a simple process. More importantly, it is not a dependable process: next year the required discount could be different. This approach does not lead to a simple rule that can be “aimed” at a specific budget target.

(Objections 2 and 3 were solved by the use of B/C analysis)

2. Customers in older areas of the system might legitimately complain that they are not getting the service and attention they deserve. New customers in outlying areas get shiny new service built to high standards. They get old equipment and lousy service.

Number 4 is a particularly damning objection in the long run, sure to get the utility into trouble with its customer base and regulators alike.

Budget Constrained Planning: Optimization Using Marginal Benefit Cost Ratio

A business rather than engineering-driven planning process

Even though many utilities may still operate within a regulatory framework, they may face limits on the amount of money they can borrow or other financial pressures that preclude as much capital spending as they would like. This constraint is completely incompatible with the fourth precept listed for the traditional paradigm earlier, which assumed that sufficient capital funding would be available for all projects that justify themselves on the basis of present worth economics.

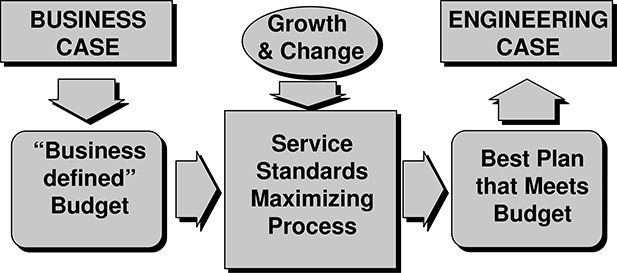

Since the constraints facing the utility are business-related (goals related to borrowing limitations, required rate reductions or caps, and targets for satisfactory stock dividend performance), it makes sense to adopt a “business driven” decision making basis for capital spending. Many utilities are forced, or chose to, shift to the business-driven structure shown in Figure 5.11, in order to plan to meet the pressures of a competitive marketplace and industry. In this paradigm, a survival and expansion plan, based on business necessities and goals, defines the available T&D budget for the utility. Good or bad, that’s all the budget there is, and unfortunately experience throughout the 1990s proved that in general the required reduction was on the order of 25%–35% less than traditional levels.

What went wrong with benefit/cost ratio prioritization?

There is, however, a problem with using the benefit/cost ratio as previously described. Consider the preceding example. The first option for feeder 1 had such a high benefit/cost ratio that all options that built on it also had high benefit/cost ratio. Each of the options for feeder 1 builds on the high B/C ratio of its option. For example, option 2 costs an additional $150,000 and lowers PW cost by $400,000. Those additional dollars spent over option 1 carry a benefit cost ratio of only 4:1, yet the option is ranked as having an overall B/C ratio of 5.5 to one because its costs and benefits include those of option 1 also. By contrast, all the options for feeder 2 are much lower in B/C ratio: feeder 2’s highest option is less than feeder 1’s lowest option.

As a more dramatic example of the “wrong” this method applies, consider adding an option to Table 5.6. Option 1b would be a variation of option 1 that costs $500,000 more in capital, but for which that additional cost contributes nothing in terms of improved PW benefit. At a cost of $2,850 and benefit of $12,450, this combination would still have a benefit/cost ratio of 4.5:1, so it would be still be approved under the budget-restricted guideline and over any spending on feeder 2 - a total waste of $500,000!

Marginal Benefit Cost Analysis

Table 5.7 shows the options for the two feeders evaluated on a marginal benefit/cost ratio basis. In each project, the additional present worth savings delivered by moving up from one option to the next is evaluated against that additional expense.

Given a budget constraint of $3,550, planners “buy” the most effective use of their dollars by taking the options whose marginal benefit cost ratios are shown in bold (final column) in Table 5.7. This is option 3 for feeder 1 and option 3 for feeder 2. A total of $3,525,000 in expenses for the two projects gains a total savings (over do nothing) of $15,790. No other combination of choices delivers so much “bang” for the buck.

Figure 5.12 shows the budget requirements when all projects the utility is considering are re-ranked on the basis of their marginal present worth/marginal capital ratio. There, the total for every marginal B/C ratio is determined, a plot analogous to that of Figure 5.10 in how it is used, but using marginal rather than just benefit cost ratio. As before, slightly more than $88 million is required to meet all projects with a ratio above zero. As indicated, when limited to $61.6 million, the utility must approve only projects with a MPW/C ratio of 1.5:1 or better. But, unlike the case where it was using benefit/cost ratio as the guiding rule, it will now always “buy” an equivalent ( and biggest overall) PW savings -the most it can afford.

Figure 5.11 Many utilities have shifted to a business-driven structure, in which business needs define the available budget. The traditional planning paradigm has difficulty adjusting to this external change in cases where the reduction from traditional budget levels is significant. Although this paradigm stretches some traditionally rigid standards, it obtains both better reliability and better economy from the limited budget.

Application of Marginal Benefit-Cost Evaluation

Generally, the way one proceeds with the decision making on two or more projects using this approach is shown in Table 5.8. There, the options for the two feeder projects (from Table 5.7) have been merged and sorted into order based on marginal benefit cost ratio. Planners make their selections against a budget total by moving down the table, selecting options and adding their marginal cost (delta cost) into their total, stopping when they have the appropriate budget total (equal to the limit).

Given a budget limit to work within, ($3,550,000 in this example), planning begins by selecting feeder 1 option 1 ($2,250,000), the highest item on the table. It then proceeds to add feeder 1, option 2, for an additional $100,000, as well as option 3 for that same feeder, at $275,000, for a total so far of $2,625,000 in cost. The next item on the list is feeder 2 option 1 with a marginal cost of $550,000, bringing the total spent so far to $3,175. Finally, feeder 2 option 2 can be added, at an additional $350,000, bringing the total to $3,525, the best, with the options listed, totaling under $3,550.

Table 5.7 The Example Two Feeder Projects From Table 5.5 Assessed By Marginal B/C Ratio

Table 5.8 Options for Both Feeder Projects From Table 5.7 Merged Into One List, Ranked By Marginal B/C Ratio

Figure 5.12 Cumulative capital requirements for the utility, versus the marginal PW/capital ratio required for that level of requirement. The utility’s $61.6 million budget allows it to spend up to a 2.1:1 marginal benefit cost ratio. This approach provides a much better guiding rule for project approval and assures maximum overall “bang for the buck” using the limited capital budget.

New basic paradigm for T&D project decision making

Generally, this approach is applied in decision making with a portion of the future costs being the performance-based rate penalties, customer paybacks, or other monetary risk measures of poor customer service quality that might be incurred by the utility. More on this concept will be given throughout this book, as prioritization based on marginal benefit-cost ratio is one or the cornerstones of the results-driven management approach and a key factor in the procedures that will be outlined to balance and optimize spending over the entire utility. This approach represents two major shifts in the thinking pattern, or paradigm applied to evaluation of projects.

1. Zero-base planning. No project, even a new customer extension, is absolutely necessary. All planning is done on a “zero base” basis, by beginning with “do nothing” as the base assumption.

2. Service-quality rather than standards-driven planning. If the cost penalty due to poor reliability is high enough to justify “doing something,” then money will be spent. Otherwise nothing is approved no matter how far below standards the resulting design will be (excepting safety standards, which must be met).

Note that the method satisfies all of the four problems listed earlier with application of the higher discount rate for planning. In particular, customers in older areas of town now have the same cost per improvement of service quality directed at them as consumers in newer areas of the system.

Refurbishment alternatives receive a “marginal” advantage

The net effect of the changes made in prioritization due to use of this method is complicated. First, although this paradigm does not assume that new service extension will be done, it’s impossible to argue with the service contribution that doing something delivers in all new construction cases (building something avoids nearly 8,760 hours of interruption time, more “bang” than one can get with most other projects). As a result, from any practical perspective, this planning method will always decide to build something to serve new customers.

But there are substantial differences in what this process will decide to build. Taking into account the value of service, this approach will no longer build the new service extension project to a very high level meant to meet thirty-year needs, just because that is what meets standards. Instead, it adjusts both new customer construction and aging infrastructure refurbishment decisions toward equivalent levels of payback on money spent for customer service. Money is spent on making some refurbishment additions to raise poor service levels, and the capital is obtained by cutting what is built in new areas so that service levels there may be less than if built to traditional “lowest PW” levels.

The results indicate the types of sacrifices that are often spread around the system. Restricted by budget constraints to projects with a 2.5:1 marginal ratio, the feeder 1 project is built with only a limited design not meeting traditional standards, for a capital reduction of $1,000,000 over the unconstrained (lowest PW cost) situation. For the refurbishment project, its option 2 (plan A) is selected, a reduction from the recommendation that flowed out of unconstrained PW cost minimization, of $500,000.

The reductions are spread equitably over both projects: using higher discount rates or B/C ratio made all the cusps in the aging infrastructure area. Note that with this planning method both projects get some of the limited funds, though neither gets as much as in the unconstrained budget (minimize present worth).

From the perspective of the traditional approach, the decision made for the new feeder project in this situation makes no sense. It is built with a capacity and style so that it is stressed at peak conditions from the very day it is built. However, from this new paradigm’s standpoint, the service quality provided by the new feeder is no worse (in fact, it is slightly better) than the service quality delivered to customers in older areas of the system.

Interestingly, the ultimate result of this planning method is not a drop in overall reliability compared to continuing with the traditional paradigm. The new paradigm results in old and new areas being more balanced in capital spending and service quality results. Due to the non-linearities in reliability-versus-cost relationships, very often the utility’s service quality indices, such as SAIFI, actually improve slightly with this value system.

This planning method is recommended in situations where a distribution utility has capital budget limitations that must be addressed and there is a concern that inequities in service quality may become a real or perceived problem, particularly with allocation of funds for refurbishment of aging infrastructure areas. Its application in a comprehensive manner is called asset management.

5.6 ASSET MANAGEMENT AND PARETO ANALYSIS

Asset management is a way of making capital budget decisions throughout an organization that aligns all capital spending with strategic business objectives - of maximizing business performance while managing risk, budgets, resources, and key performance indicators. A key element of this approach is a recognition that:

a) The company has multiple objectives (things it wants to accomplish) such as reliability, working down average equipment age, profit margin, safety, etc.

b) A candidate project might contribute to many or several of these objectives, improving reliability and safety and efficiency.

c) There are often multiple ways a particular detail could be handled. A set of troublesome MV breakers could be replaced with new, or refurbished, or merely serviced, or ignored. Each option has benefits (or not) and costs (or not), and might be most preferable depending on if and what other projects are funded, or not.

Pareto Analysis

Pareto Analysis is the basic analytical and decision-support engine of asset management. It is a strengthened version of the budget-constrained approaches discussed in the previous sections. Suppose planners at Big State Electric (BSE) identify 100 major capital spending projects the company could do in the next year, each with a defined scope (what it involves and what it does), an estimated cost, and estimated impacts on corporate KPIs (key performance indicators) like SAIDI, safety, system losses, power quality, working down the age of critical yet old equipment, future profit margins, etc. Taken together, all 100 projects might cost $500 million. However, BSE would never fund all of them, for two reasons. First, it doesn’t have anywhere near $500 million – it is thinking of spending somewhere maybe up to $150 million and might be able to stretch to $200 million if pressed to the wall, but no further. Further, some combinations of these projects don’t make sense if done together. BSE would never refurbish the vaults in its downtown network and replace them, but planners have scoped out potential projects to do both, in order to comprehensively look at the company’s options: they’d like to see them replaced, but things are complicated, there are a lot of other important goals, too, and money is tight. Maybe refurbishment is all BSE can afford. Maybe it can’t even afford that. Asset management will help the planners decide what to recommend.

Portfolios

A portfolio is a combination of projects and programs the utility decides to approve and execute. Traditionally, the utility called the set of projects it approved each year “the capital budget,” a term that stressed what it was spending, or “the approved construction list,” a term that stressed that it was going to build. Calling it a portfolio instead stresses that these projects are investments, i.e., that the company expects something in return and in fact wants to maximize that return. Each circle in Figure 5.13 represents a different potential portfolio, some combination of projects and programs that the utility could decide to fund. The vertical axis is a measure of its contribution to success (how much the utility gets toward its KPI targets) while the horizontal axis is a measure of its cost (how much it spends) for that particular set of projects and programs. Each circle is plotted based on its total “bang” (what it provides in total towards the KPI goals the utility wants) versus “bucks” (what all of its projects cost when added together).

Figure 5.13 Potential portfolios (asset use and spending plans) can be plotted by their cost and performance results as shown here and explained in the text. Only the best portfolios lie on the efficient frontier, also called the Pareto curve, which denotes the maximum performance possible at every budget level. Optimization used in asset management finds only the portfolios on the efficient frontier and draws the curve for the utility planners.

Some of the potential portfolios in Figure 5.13 are inefficient portfolios (unshaded circles). BSE could buy any of these but never will, because it knows it can get more for its money. For example, why fund the combination of projects called portfolio B when one can fund A instead and get roughly 30% more “bang” for the same money? Or the company could fund portfolio C and get the same bang but for considerably less money. Portfolio B is inefficient, whereas A and C are efficient portfolios: if you want as much bang as C gives, you have to spend at least what C costs – no other portfolio can give you that much or more for less money. Similarly, if you want as much as B provides, it is the least costly way to get it.

The efficient frontier is the set of all efficient portfolios, and can be thought of as the upper boundary of this set of portfolios. The efficient frontier represents the set of efficient portfolio choices BSE has with regard to how much performance it wants to buy. This efficient frontier is also known as a Pareto curve, since it identifies a set of optimal solutions based on the same efficiency concepts used by the Italian economist Vilfredo Pareto when he examined issues related to social welfare (Pareto, 1906).

Efficient Choices

A key concept of asset management is efficient choice. The Pareto optimization determines the information shown in Figure 5.13 and identifies the frontier. This gives BSE a set of choices which are all optimum in the sense they maximizing what it gets for the money it spends. But the optimization does not chose or even identify a best plan. The utility executives must do that, deciding how much of one thing they want (money) versus the other (success).

Finding the Pareto curve is straightforward in concept even if technically intricate in practice. The major steps planners have to take to do so are:

1) Define all the projects, their costs, and KPI impacts.

2) Convert the KPI impacts to a single valued measure (benefit).

3) Rate each as to benefit/cost ratio (bang for the buck).

4) Sort them by benefit/cost ratio, highest to lowest.

5) Plot them cumulatively in a figure like that shown in Figure 5.13.

The result is the Pareto curve for this list of potential projects. At each point on the curve, no combination of projects taken from that list can provide more bang for the buck than the combination already plotted: the curve describes the efficient frontier for the utility. The curve has a decreasing slope: initially spending is very efficient, providing a lot of benefit for the money spent, but as more is spent each successive project is, at best, only as efficient as the one before it- the result of sorting them and putting them in order of bang for the buck.

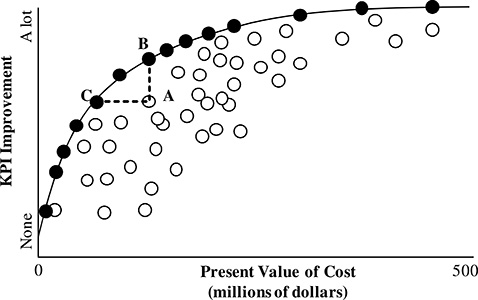

Figure 5.14 shows an actual set of 300 projects, taken from an asset management study for a large investor-owned electric utility in the central United States in 2004. Each project is a represented by a rectangle, of height equal to the benefit it provides and width equal to the project’s cost. The project at the lower left is that project, among all, that has the highest benefit cost ratio.

Figure 5.14 Pareto curve representing major capital projects for an electric utility. See text for details.

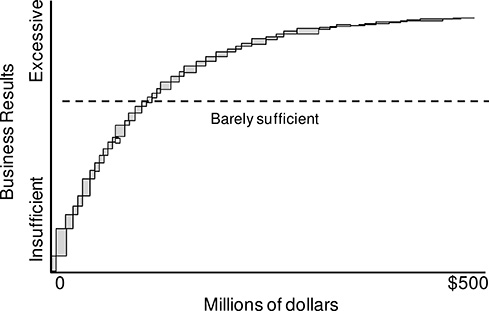

Realities of Asset Management

Figure 5.15 shows an actual Pareto curve from this same set of projects that includes consideration of several practical considerations that have to be included for the resulting plan to have any practical usefulness to the utility. These are:

Must do projects: a utility has to do some projects it must do. For example, it must do road widening projects to allow the state to build a new, wider highway, etc. It may have agreed to put certain existing lines underground when negotiating a new franchise agreement and rate schedule with a municipality in its service territory, etc. These projects are a given: they will be part of the portfolio.

Dependencies and other constraints. Some projects require another project be done first (Smart reclosers can’t be installed in the Eastwood division until a central control and communication hub is installed in an expanded Distribution Operations Center). Other projects are mutually exclusive (The utility can rebuild a set of breakers or replace them, but would never do both). Planners want both in the list of potential projects to be considered because they provide different amounts of long- and short-term benefit and have different costs. They want the optimization to decide which is best for their company.)

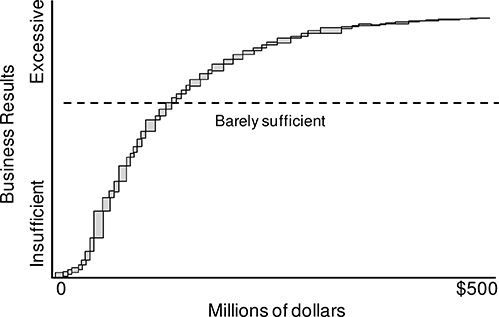

Figure 5.15 The same Pareto curve after practical issues like must-do projects and various practical constraints are considered. Achieving the minimum acceptable level of performance is about 20% more expensive than in Figure 5.14: the real world is just more expensive than theory sometimes estimates. On the other hand, the marginal benefit (slope of the curve = how much one gets for each additional dollar spent above the minimum) at the minimum point is about 25% more than in Figure 5.14. In the real world, the utility has a bit more incentive to spend more than the minimum necessary.

Goals are digital in many practical senses. As a optimization begins buying the best project first, every minute of SAIDI improvement is equally valuable up to the point where enough has been purchased to meet regulatory and business targets for reliability. After that it may not be valuable at all, particularly if other targets like working down equipment age, or reducing O&M costs, or meeting safety goals remain to be achieved.

As a result, the most effective Pareto optimizations never try to combine all the KPI impacts into a single-valued measure. Instead, a multi-target constrained optimization engine is used that is told to find the lowest cost portfolio that:

a) Meets all the minimum targets

b) Includes all must do projects

c) Includes a combination of projects that satisfies all constraints

Asset Management using Pareto Analysis driven by a MIP (mixed integer type) optimization is recommended for utility planning that includes both durability (lifetime and aging issues) and reliability (customer service) as well as other performance and business targets. For more information on utility asset management and optimization of methods see Willis and Brown (2010), which provides an accessible overview or Brown (2012), which gives a very detailed presentation on asset management and methods to implement it, in the References and Bibliography.

5.7 CONCLUSION

Planning involves the selection of the best alternative from among those at hand. In the power industry, that selection depends to a certain extent on the values of the group making the decision. All cost evaluations for power delivery planning are based in part upon economic evaluation that is consistent over the range of all alternatives. Usually, this means that present and future costs must be compared. Present worth analysis, levelized costing, or some similar method of putting present and future value on a comparable basis will be used.

Intra-Project, Marginal Benefit-Cost Alternatives Comparison

The foregoing method of maximizing benefit from a limited budget by comparing alternatives within each project (i.e., for each, several alternative ways of doing the project were evaluated) against alternatives from other projects, is called intra-project alternatives analysis. Methods that compare only a single alternative for each project (i.e., the method used in Table 5.5) are called inter-project comparisons. They compare each alternative based only on its ultimate “lowest cost” alternative. By contrast, intra-project comparison ranks the various alternatives for each project against one another.

It is the combination of comparing multiple alternatives in a project, against those of others, and the use of marginal benefit-cost analysis, that yields the additional savings. This method – intra-project comparison based on marginal benefit cost analysis – is called budget-constrained planning, of BCP for short.

BCP is more complicated to implement than traditional prioritization methods. However, the authors have helped several utilities implement it, where it has led to bottom line savings and reliability improvements as dramatic as the improvement shown in the foregoing examples. BCP delivers results. It will be used both in capital planning, and in maintenance and operations prioritization, later in this book. When applied uniformly over an entire utility (all regions, all functions), it is the basis for Results-Driven Management.

REFERENCES AND BIBLIOGRAPHY

D. Atanackovic, D. T. McGillis, and F. D. Galiana, “The Application of Multi-Criteria Analysis to a Substation Design,” paper presented at the 1997 IEEE Power Engineering Society Summer Meeting, Berlin.

T.W. Berrie, Electricity Economics and Planning, Peter Peregrinus Ltd., London, 1992.

R.E. Brown, Business Essentials for Utility Engineers, CRC Press, Boca Raton, 2010.

J.J. Burke, Power Distribution Engineering: Fundamentals and Applications, Marcel Dekker, New York, 1994.

V.D.F.Pareto, Manuale di economia politica, Centre d'Etudes Interdisciplinaires, Université de Lausanne, 1906.

H.L. Willis, Power Distribution Planning Reference Book- Second Edition, Marcel Dekker, New York, 2004.

H.L. Willis and R. W. Powell, “Load Forecasting for Transmission Planning,” IEEE Transactions on Power Apparatus and Systems, August 1985, p. 2550.

H.L. Willis and G. B. Rackliffe, Introduction to Integrated Resource T&D Planning, ABB Guidebooks, Raleigh, NC, 1994.

H.L. Willis and R. E. Brown, “Substation Asset Management,” Chapter 19 in Electric Power Substation Engineering Handbook – 3rd Edition, CRC Press Boca Raton, 2012.

World Bank, Guidelines for Marginal Cost Analysis of Power Systems, Energy Department paper number 18, 1984.