16.4 Cryptocurrencies

In this section, we give a general discussion of issues related to digital cash, using Bitcoin as an example.

The Brands digital cash system from Section 16.2 gives insight into how difficult it can be to re-create the benefits of cash using just cryptography and, even with all its cryptographic sophistry, the Brands scheme is still not able to allow for the cash to be transferred to others or for the digital money to be divided into smaller amounts. Up until the 2000s, almost all digital cash protocols faced many shortcomings when it came to creating digital objects that acted like real-world money. For example, in order to allow for anonymity and to prevent double spending, it was necessary to introduce significant complexity into the scheme. Some protocols were able to work only online (i.e., they required the ability to connect to an agent acting as a bank to verify the validity of the digital currency), some protocols like Brands’s system did not allow users to break cash into smaller denominations and thereby issue change in transactions. Beyond the technical challenges, some systems, like Chaum’s ECash, faced pragmatic hurdles in persuading banks and merchants to adopt their system. Of course, without merchants to buy things from, there won’t be users to make purchases, and this can be the death of a cryptocurrency.

One of the major, practical challenges that the early forms of cryptocurrencies faced was the valuation of their digital cash. For example, just because a digital coin is supposedly worth $100, what actually makes it worth that amount? Many early digital currencies attempted to tie themselves to real-world currencies or to real-world commodities (like gold). While this might seem like a good idea, it also introduced several practical challenges: it implicitly meant that the value of the entire cryptocurrency had to be backed by an equivalent amount of real-world cash or coins. And this was a problem – if these new, digital currencies wanted to exist and be used, then they had to acquire a lot of real-world money to back them.

This also meant that the new forms of digital cash weren’t actually their own currency, but actually just another way to spend an existing currency or commodity. Since needing real-world assets in order to get a cryptocurrency off the ground was a hurdle, it led many to ask “What if one could make the digital cash its own currency that was somehow valued independently from other currencies?”

It turns out that many of the technical solutions needed to overcome the various hurdles that we have outlined already existed in the early 2000s and what was needed was a different perspective. In 2008, Satoshi Nakamoto presented a landmark paper [Nakamoto], which launched the next generation of cryptocurrencies and introduced the well known cryptocurrency Bitcoin. These cryptocurrencies, which include Bitcoin, Ethereum, and many others, have been able to overcome many of the hurdles that stifled previous attempts such as ECash. Currently, currencies like Bitcoin and Ethereum are valid currencies that are traded internationally.

The new generation of cryptocurrencies were successful because they made practical compromises or, to put it another way, they did not try to force all of the properties of real-world cash onto digital currencies. For example, a digital currency like Bitcoin does not work offline, but it does cleverly use decentralization to provide robustness so that if parts of the system are offline, the rest of the system can continue to function. Another major paradigm shift was the realization that one did not need to create a digital object corresponding to a coin or to cash, but rather that the money could be virtual and one only needed to keep track of the trading and exchange of this virtual money. That is, bookkeeping was what was important, not the coin itself! And, once we stop trying to create a digital object that acts like cash, then it becomes a lot easier to achieve properties like preventing double spending and being able to divide coins into smaller parts. Another paradigm shift was the realization that, rather than tying the value of the currency to real-world currency, one could tie the value to solving a hard (but not impossible) computational problem and make the solution of that computational problem have value in the new currency.

In order to understand how these new cryptocurrencies work, let’s take a look at the basic structures being used in Bitcoin. Many of the other currencies use similar building blocks for their design.

As we just mentioned, one of the major changes between Bitcoin and older digital cash schemes is a move away from a digital object representing a coin and instead to the use of an imaginary or virtual currency that is kept track of in bookkeeping records. These ledgers, as they are known, record the creation and exchange of these virtual coins. The use of cryptography to form secure ledgers has become a growing trend that has impacted many applications beyond the support of cryptocurrencies.

Let us look at a simple ledger. To start, assume that we have a central bank, which we call BigBank. Later we shall remove BigBank, but for now it is useful to have BigBank around in order to start the discussion. We suppose that BigBank can make new virtual coins, and that it wants to share them with Alice. To do so, it makes a ledger that records these events, something that looks like:

This ledger can be shared with Alice or anyone else, and after looking at it, one can easily figure out the sequence of events that happened. BigBank made 100 coins, and then these coins were given by BigBank to Alice. Assuming there have not been any other transactions, then one can conclude that Alice is now the owner of 100 virtual coins.

Of course, Alice should not just trust this ledger. Anyone could have made this ledger, pretending to be BigBank. As it is, there is nothing tying this ledger to its creator. To solve this problem, we must use digital signatures. Therefore, BigBank has a public–private key pair and has shared its public key with Alice and the rest of the world. There are many ways in which this could have been done, but it is simplest to think of some certificate authority issuing a certificate containing BigBank’s public key credentials. Now, rather than share only the Ledger, BigBank also shares .

This makes it harder for someone to pretend to be BigBank, but we still have some of the usual problems that we encountered in Chapter 15. For example, one problem that stands out is that it is possible to perform a replay attack. If Alice receives five separate copies of the signed Ledger, then she might conclude that she has 500 coins. Therefore, in order to fix this we need to use some form of unique transaction identifier or counter in Ledger before BigBank signs it, something like:

Now, the signed Ledger allows anyone to have some trust that BigBank has given Alice 100 coins.

Alice’s coins aren’t much use to her unless she can spend them. Suppose she goes to Sarah’s Store, which is known to accept BigBank’s coins, and wants to buy an item using BigBank’s coins. Alice could write another entry in the ledger by giving Sarah’s Store an update to the ledger that looks like

Now, Alice signs this update and sends Sarah’s Store . Sarah’s Store can indeed verify that Alice made this update, but a problem arises: How does Sarah’s Store know that Alice in fact had 100 coins to spend?

A simple way to take care of this is for Alice to attach a signed copy of BigBank’s original Ledger. Now Sarah’s Store can verify that Alice did get 100 coins from BigBank.

This works, but we come to classic double spending problem that all digital currencies must address. Right now, there is nothing preventing Alice from going to Vendor Veronica and spending those 100 coins again. Alice can simply make another version of Ledger 2, call it Ledger :

She can sign Ledger and send both it and BigBank’s signed copy of the original Ledger 1. But even with these, there is no way for Vendor Veronica to be assured that Alice did not spend her 100 coins elsewhere, which she in fact did.

What is needed is a way to solve the double spending problem. We can do this by slightly revising the purchasing protocol to place BigBank in a more central role. Rather than let Alice announce her transaction, we require Alice to contact BigBank when she makes purchases and BigBank to announce updates to the ledger. The ledger of transactions operates as an append-only ledger in that the original ledger with all of its updates contains the history of all transactions that have ever occurred using BigBank’s coins. Since it is not possible to remove transactions from the ledger, it is possible for everyone to see if double spending occurs simply by keeping track of the ledger announced by BigBank.

Ensuring that this append-only ledger is cryptographically protected requires that each update is somehow tied to previous versions of the ledger updates, otherwise it might be possible for transactions to be altered. The construction of the append-only ledger is built using a cryptographic data structure known as a blockchain, which we introduced in Section 12.7. A blockchain consists of two different forms of hash-based data structures. First, it uses hash pointers in a hash chain, and second it uses a Merkle tree to store transactions. The use of the hash chain in the blockchain makes the ledger tamper-proof. If an adversary attempts to tamper with data that is in block , then the hash contained in block , namely, the hash of the correct block , will not match the hash of the altered block . The use of the Merkle tree provides an efficient means of determining whether a transaction belongs to a block.

Now suppose that BigBank wants to keep track of all of the transactions that have taken place and publish it so that others can know these transactions. BigBank could periodically publish blocks, or it could gather an entire collection of blocks and publish them all at once. Ultimately, BigBank publishes all of the blocks of the blockchain along with a final hash pointer that certifies the entire collection of blocks in the blockchain. Each of the blocks in the blockchain, along with the final hash pointer, is signed by BigBank so that others know the identity of the entity publishing the ledger. Thus, the hash chaining in the blockchain provides data integrity, while the digital signatures applied to each block provide origin authentication.

Let us return to the story of BigBank and all of the various participants who might want to use or acquire some of BigBank’s digital coins. Everyone wishing to use some of their BigBank coins must tell BigBank how many coins or how much value is being transferred for a purchase and whom the coins will be given to. BigBank does not need to know what is being purchased, or why there is a transaction occurring; it just needs to know the value of the exchange and the recipient. BigBank will then gather several of these individual transactions into a single block, and publish that block as an update to the blockchain that represents BigBank’s ledger.

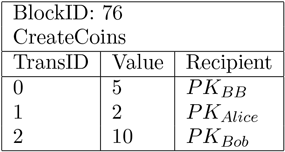

To do this, though, BigBank needs a way to describe the transactions in the ledger, and this means that there needs to be a set of basic transaction types that are allowed. It turns out that we don’t need very many to have a useful system. For example, it is useful for an entity like BigBank to create coins, where each coin has a value, a serial number, and a recipient. BigBank can, in fact, create as many coins as it wants during the time before it publishes the next block in the blockchain. For example, suppose BigBank creates three coins with different recipients, and that it publishes the creation of these coins in the data portion of a block that looks like:

When this block is published, it informs the rest of the world that BigBank created several coins of different values. First, in transaction 0 for block 76, a coin worth 5 units was created and given to (which, as will be explained shortly, stands for BigBank’s Public Key). This coin will be referred to as coin 76(0) since it was made in block 76, transaction 0. Similarly, a coin was created in transaction 1 of Block 76 for , which will be referred to as coin 76(1). Lastly, a coin was created in transaction 2 for , and will be referred to as coin 76(2). Who or what are , , and ? This is an example of something clever that Bitcoin borrowed from other applications of cryptography. In [HIP], it was recognized that the notion of one’s identity is best tied to something that only that entity should possess. This is precisely what a private key provides in public key cryptography, and so if someone wants to send something to Alice or Bob, then they can use Alice or Bob’s public key (which they know because the public key is public) as the name of the recipient.

In order to support purchases made by Alice and others, we need to allow for the users of BigBank currency to consume coins in exchange for goods, and to receive change for their transactions. It was realized that it was easier to simply destroy the original coin and issue new coins as payment to the vendors and new coins as change to those making purchases than it was to break a coin down into smaller denominations, which had proven difficult to accomplish for previous digital coin schemes. So, if Bob has a coin 76(2) worth 10 units, and he wants to buy something worth 7 units, BigBank destroys 76(2), issues a new coin to the vendor worth 7 units, and issues a new coin to Bob worth 3 units.

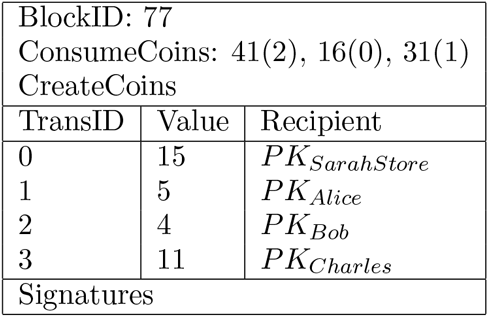

Of course, BigBank is big and might need to handle many transactions during the time it takes to form a block. Therefore, BigBank needs to hear from all of its customers about their purchases, and it needs to make certain that the coins that its customers are spending are valid and not previously spent. It also needs to create new coins and give the new coins to those who are selling to BigBank’s customers, while also issuing new coins as change. Let us look at how this could work. Suppose Alice has a coin 41(2) that is worth 20 units, and that she wants to buy a widget from Sarah’s Store for 15 units. Then, the first step that BigBank takes is to destroy Alice’s coin worth 20 units, then issue a new coin to Sarah’s Store worth 15 units and a new coin to Alice worth 5 units, which corresponds to Alice’s change from her purchase. Thus, one coin was consumed and two were created, but the total value of the coins being consumed is equal to the total value of the coins being created from the transaction. Lastly, before BigBank can publish its update to the ledger, it needs to get all of the owners of the coins that were consumed to sign the transaction, thereby ensuring that they knowingly spent their coins. Any good cryptographic signature scheme would work. Bitcoin uses the Elliptic Curve Digital Signature Algorithm (ECDSA), which we will see in Exercise 24 in Chapter 21.

The next block of transactions in the blockchain thus looks like:

BigBank’s approach to managing its ledger of transactions seems to work well, but it has one major problem, and that is the fact that BigBank has to be involved in every transaction. Not only does this mean a lot of work for BigBank, but it also leads to several security concerns, such as the risk of a denial of service to the system if BigBank becomes disconnected from the rest of the network, or the risk that BigBank might use its influence as the central entity in the economy to extract extortion from its members. Although BigBank cannot create false transactions, it could ask for large service fees in order to carry out a transaction.

Bitcoin gets around the problem of a central bank vetting each and every transaction by making the blockchain protocol decentralized. In other words, rather than having a single entity check the transactions, Bitcoin uses the notion of community consensus to check that the transactions are correct. Also, rather than have a single entity maintain and update the ledger of transactions, Bitcoin allows the members of the community to form the next block in the blockchain and thereby update the ledger themselves. In fact, Bitcoin went further in that it did not trust banks to mint coins themselves. Instead, Bitcoin devised a means by which coins get created periodically and are awarded to those who do work to keep the Bitcoin system moving smoothly.

In order to understand this, we need to set the stage for how life in the Bitcoin universe works. Every units of time (in Bitcoin, ), the users in the Bitcoin network must agree on which transactions were broadcast by the users making purchases and trading in bitcoins. Also, the nodes must agree on the order of the transactions, which is particularly important when money is being exchanged for payments. Bitcoin then proceeds in rounds, with a new update to the ledger being published each round.

Every user in the Bitcoin network keeps track of a ledger that contains all of the blocks that they’ve agreed upon. Every user also keeps a list of transactions that they have heard about but have not yet been added to the blockchain. In particular each user might have slightly different versions of this list, and this might happen for a variety of reasons. For example, one user might have heard about a transaction because it is located near that transaction, while another user might be further away and the announcement of the transaction might not have made it across the network to that user yet. Or, there might be malicious users that have announced incorrect transactions and are trying to put wrong transactions into the blockchain.

Bitcoin uses a consensus protocol to work out which transactions are most likely correct and which ones are invalid. A consensus protocol is essentially a way to tally up how many users have seen and believe in a transaction. In each round of the consensus protocol, new transactions are broadcast to all of the users in the Bitcoin network. These transactions must be signed by those spending the coins involved. Each user collects new transactions and puts the transactions it believes into a new block. In each round, a random user will get to announce its block to all of the other users. Bitcoin uses a clever way to determine which user will be this random user, as we shall soon discuss. All of the users that get this new block then check it over and, if they accept it, they include its hash in the next block that they create. Bitcoin uses the SHA-256 hash function for hashing the block and forming the hash pointer.

Before we proceed to discuss how Bitcoin randomly chooses which user will be chosen to announce its block, we look at some security concerns with this protocol. First is the concern that Alice could attempt to double spend a coin. In each round, coins are being created and destroyed, and this is being logged into the ledger. Since the ledger is being announced to the broader community, other users know which coins have been spent previously and thus they will not accept a transaction where Alice tries to spend a coin she already used. Much of the trustworthiness of Bitcoin’s system is derived from the fact that a consensus protocol will arrive at what most users believe is correct and, as long as most users are honest, things will work as they should with false transactions being filtered before they get into the blockchain.

Another concern is that Alice could write transactions to give herself coins from someone else. This is not possible because, in order to do so, Alice would have to write a transaction as if she was another user, and this would require her to create a valid signature for another user, which she is unable to do.

A different concern is whether Alice could prevent a transaction from Bob from being added to the ledger. Although she could choose not to include Bob’s transaction in a block she is creating, there is a good chance that one of the other users in the network will announce a block with Bob’s transaction because the user that is chosen to announce its block is randomly chosen. Additionally, even if she is chosen to announce her block, a different honest user will likely be chosen during the next round and will simply include Bob’s transaction. In Bitcoin, there isn’t any problem with a transaction taking a few rounds to get into the blockchain.

We now return to the question of how nodes are randomly selected. Remember that we needed to remove the role of a central entity like BigBank, and this means that we cannot rely on a central entity to determine which user will be randomly selected. Bitcoin needed a way to choose a user randomly without anyone controlling who that user would be. At the same time, we can’t just allow users to decide selfishly that they are the one chosen to announce the next block – that could lead to situations where a malicious user purposely leaves another user’s transactions out of the blockchain.

Bitcoin also needed a way to encourage users to want to participate by being the random node that announces a new block. The design of Bitcoin allows users who create blocks to be given a reward for making a block. This reward is known as a block reward, and is a fixed amount defined by the Bitcoin system. Additionally, when a user engages in a transaction that it wants logged into the blockchain ledger, it can set aside a small amount of value from the transaction (taking a little bit from the change it might issue itself, for example), and give this amount as a service charge to the user that creates and adds the block containing the transaction into the blockchain.

Together, these two incentives encourage users to want to make the block, so the challenge then is ensuring that random users are selected. Bitcoin achieves this by requiring that users perform a task where it isn’t guaranteed which user will be the first to complete the task. The first user to complete the task will have performed the proof of work needed to be randomly selected. Users compete with each other using their computing power, and the likelihood that a user will be selected ”randomly” depends on how much computing power they have. This means that if Alice has twice the computing power that Bob has, then she will be twice as likely to be the first to complete the computing task. But, even with this advantage, Alice does not control whether she will finish the task first, and so Bob and other users have a chance to publish the block before she does.

Bitcoin’s proof of work requires that users solve a hash puzzle in order to be able to announce a block to be added to the blockchain. Specifically, a user who wishes to propose a block for adding the community’s ledger is required to find a nonce such that

where is the nonce to be found, is the hash of the previous block in the blockchain, are the transactions that the user is proposing to add to the ledger, and is a threshold value for the hash puzzle. What this means is the hash value is interpreted as an integer in binary and there must be a certain number of 0s at the beginning of this binary expansion. The value of is chosen so that it will take roughly units of time for some user to solve the puzzle. In Bitcoin, , and every two weeks the Bitcoin protocol adjusts so that the average time needed to solve a hash puzzle remains around . Bitcoin uses the SHA-256 hashing algorithm twice for the proof of work cryptopuzzle, once for the hash of the previous ledger and once for obtaining the desired small hash value. In practice, the user does a massive computation using numerous nonces, hoping to be the first to find an appropriate hash value.

Once a user finds this nonce, it forms the new block, which includes , the previous hash, and the transactions it has included. Then the user announces the block to the entire community. The reward for completing this task first is that the user will receive the block reward, which is several bitcoins, as well as transaction fees. The process of solving the hash puzzle and announcing a block is called Bitcoin mining, and has become a popular activity with many companies devoting large amounts of computing (and electrical power) to solving puzzles and reaping the Bitcoin rewards.

Let’s now put everything together and describe what a typical Bitcoin blockchain looks like. A block in Bitcoin’s blockchain consists of a header followed by a collection of transactions that have been organized as a Merkle tree. The header itself contains several different pieces of information: the hash pointer to the previous block in the blockchain, a timestamp, the root of the Merkle tree, and the nonce. In actual implementation of Bitcoin, it is only the hash of the header that must satisfy the conditions of the cryptographic puzzle, rather than the hash of the full block of information. This makes it easier to verify a chain of blocks since one only needs to examine the hash of the headers, and not the hashes of many, many transactions. We may therefore visualize the Bitcoin blockchain as illustrated in Figure 16.1.

Figure 16.1 Each block in Bitcoin’s blockchain consists of a header and a Merkle tree of transactions

Our description of Bitcoin is meant to convey the ideas behind cryptocurrencies in general and thus greatly simplifies the details of the actual Bitcoin protocol. We have avoided describing many practical matters, such as the formal specification of the language used by Bitcoin to specify transactions, the data structures and housekeeping that are needed to keep track of transactions, as well as the details behind the use of the hash of a public key for addressing users. The reader can look at [Bitcoin] or [Narayanan et al.] to find the details behind Bitcoin and its protocols.