50 Section 3

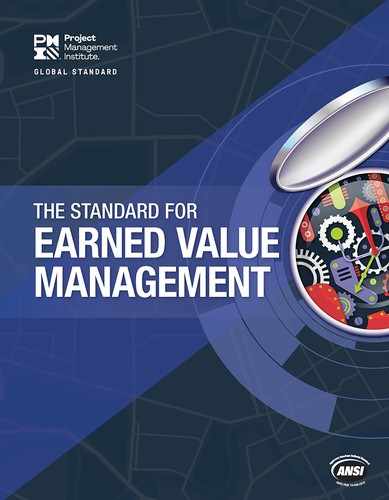

Figure 3-7. Project Schedule Presentation—Example

Calendar

Units

Days

1st

Quarter

1st

Quarter

4th

Quarter

3rd

Quarter

2nd

Quarter

Control

Account

Activity Description

CA-001

WP--01

WP-02

WP-03

CA-002

WP-04

WP-05

WP-06

CA-003

PP-02

PP-01

CA-004

PP-03

PP-04

PP-05

CA-005

PP-06

332

332

67

248

20

50

25

25

25

175

175

120

75

30

30

5

20

20

SAMPLE PROJECT

Project Management

Conception

Manage Product Realization

Close Project

Smart Building Planning Phase (Definition)

Architecture/Engineering and IT Planning

Architectural and Engineering Designs

Information System Requirements

Building Construction

Building Construction Work

Building Contingency Reserve

Smart Building Information System

Release 1

Release 2

Software Installation

Handover

Handover

Project Schedule Timeframe

3.3.4.4 SCHEDULE EVOLUTION

Project budgeting and scheduling are iterative processes involving the negotiation of project constraints until

consensus estimates are achieved among the stakeholders. Therefore, the schedule continues to evolve until the

project manager establishes the PMB.

A properly structured schedule model depicts the project team’s plan for work accomplishment by CA with WPs.

The planning package should be planned in detail and broken down into WPs before the work is executed. The CA

work package provides the underlying logic for the PMB, against which accomplishments are measured and expected

future outcomes are forecasted.

51

Enhancements to the schedule model may include:

Logic-driven schedule, networked at the work package or activity level,

Resource-loaded WP and/or activities,

Risk trigger milestones and potential risk responses incorporated as alternative paths, and

Schedule risk analysis data incorporated into the schedule model.

Inclusion of probabilistic considerations based on complexity awareness and risk analysis (striking a balance

between various risks and objectives) enhances the usefulness of the schedule model as a management tool.

3.3.5 COST BASELINE

The cost baseline for EVM is the approved budget for each control account with work and planning packages and the

appropriate contingency reserve (when required, depending on EEFs/OPAs). For EVM, the cost for each work package

or planning package (i.e., the approved budget) needs to be time-phased and aligned with the schedule baseline.

The cost baseline is developed as a summation of the approved budgets for the different CAs that have scheduled

work or planning packages. The basis for cost data within each CA is outlined during planning for each CA. The

cost should be based on cost estimates. The cost estimates are often broken out between direct and indirect costs.

Whether indirect costs are in the project estimate and, therefore, in the project budget depends on EEFs and OPAs.

EVM does not require any specific handling of indirect costs; however, indirect cost variances could impact variance

analysis. When the project and the enterprise want to include indirect costs, these should be incorporated in the cost

estimating process and included at the activity level or at higher levels (see Section 7.2.3.1 of the PMBOK

®

Guide).

Within EVM, when allocated at high levels, indirect costs can be apportioned to control accounts, work packages,

activities, or resources, as appropriate. It is important for users of EVM to understand which costs are included within

the PMB and which are not; this is dependent on organizational rules. EVM requires the cost estimate to be aligned

with the CAs at a minimum, but the cost estimate can be aligned down to the activity level.

The cost estimate provides the basis for establishing the budget. Typically, estimates should be developed for

each work package or planning package. The estimates for each work package should be robust enough to assist

the project team in planning the needed resources, while budget estimates for planning packages may have a lower

level of detail until enough information is available to support the conversion to work packages. All cost estimates

within the CAs should be developed within the timeframes established for that work in the schedule baseline. Further

guidance for developing a cost estimate can be found in the Practice Standard for Project Estimating [9].

52 Section 3

Once the cost estimates for work packages and planning packages within a control account are completed, the

project manager and the control account manager review them. The project manager may decide to authorize budget

for an amount more, less, or equal to the cost estimate as follows:

More budget may be authorized if the project manager is aware of likely future events, such as changes in

rates, processes, or customers. This extra budget is often put into contingency reserves at the work/planning

package level or within the CA.

Less budget may be authorized if the project manager is giving the control account manager a stretch goal or

holding back reserve. Less budget may also be authorized if some of the assumptions in initial estimates are

proven wrong or more information on scope is available before execution than when it was estimated. Often

the budget below the cost estimate is placed in reserves outside the CA.

Budget equal to the cost estimate may be authorized, particularly when risk analysis and reserves are handled

outside of the control account.

The most universal and broad measurement unit used to value both budget and actual resource consumption is

the monetary unit or appropriate currency, which is also the most widely used and original measure within the EVM

method. On multicurrency projects, the management of exchange rates should be addressed, which can be done

similarly to labor rate or other indirect and direct cost changes that have impacts on projects. This is not surprising since

cost data answer the basic question of any project sponsor: How much is the project really costing the organization?

However, it is possible to use other units for budget and cost, such as labor hours (i.e., human effort). These

alternatives often focus on a specific resource or cost element of the overall organizational effort, which is considered

more relevant for management purposes. All other cost elements are either converted to this unit or simply not

considered in EVM. The measure used depends on the nature and scope of the EVM being implemented and should

be documented within the project management plan.

Alternative measures should be consistent with the boundaries of the cost elements being controlled by the project.

For example, in some environments (e.g., in small software projects), the project manager is not responsible for

measuring the full project cost but only the direct human effort. In these scenarios, labor hours are used as the measure

of value—a more defined and less granular substitute for monetary units. In this example, nonhuman effort costs, such

as travel costs, are outside of the PMB. As a result, the different costs of the hourly efforts are not captured within the

PMB. In some cases, this may simplify the EVMS significantly while having little impact on the management value.

When alternative substitutes for monetary value are used, it is essential to ensure that the cost data used are the

chosen measure of organizational effort (in the form of resource consumption) incurred to execute the project; such a

measure, even if similar, should not be mistaken with the measures of scope accomplishment (e.g., scope data) like

physical measures (e.g. drawings complete).

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.