3 ASC 210 BALANCE SHEET

Form of the Statement of Financial Position

Example: Statement of financial position – highly aggregated

Example: Statement of financial position – highly detailed

PERSPECTIVE AND ISSUES

Subtopics

ASC 210, Balance Sheets, is divided into two Subtopics:

- ASC 210-10, Overall, which focuses on the presentation of the balance sheet, particularly the operating cycle and current assets and liabilities, and

- ASC 210-20, Offsetting, which offers guidance on offsetting amounts for certain contracts and repurchase and reverse repurchase agreements.

Scope and Scope Exceptions

The guidance in ASC 210-20 does not apply to:

“The derecognition or nonrecognition of assets and liabilities. Derecognition by sale of an asset or extinguishment of a liability results in removal of a recognized asset or liability and generally results in the recognition of gain or loss. Although conceptually different, offsetting that results in a net amount of zero and derecognition with no gain or loss are indistinguishable in their effects on the statement of financial position. Likewise, not recognizing assets and liabilities of the same amount in financial statements achieves similar reported results.” ASC 205-10-15-2

Overview

Statements of financial positions (formerly most commonly known as balance sheets, and also referred to as statements of financial condition) present information about assets, liabilities, and owners' equity and their relationships to each other. They reflect an entity's resources (assets) and its financing structure (liabilities and equity) in conformity with generally accepted accounting principles. The statement of financial position reports the aggregate effect of transactions at a point in time, whereas the statements of income, retained earnings, comprehensive income, and cash flows all report the effect of transactions occurring during a specified period of time such as a month, quarter, or year.

User's look at the statement of financial position in order to assess the entity's

- Liquidity, the extent to which it holds cash or cash equivalents in the normal course of operating its business

- Financial flexibility, ability to take effective actions to alter the amounts and timing of its cash flows so it can respond to unexpected needs and opportunities. Financial flexibility includes the ability to raise new equity capital or to borrow additional amounts by, for example, utilizing unused lines of credit.

- Ability to pay its debts when due, and

- Ability to distribute cash to its investors to provide an acceptable rate of return.

The rights of the shareholders and other suppliers of capital (bondholders and other creditors) of an entity are many and varied. The disclosure of these rights is an important objective in the presentation of financial statements. The rights of shareholders and creditors are mutually exclusive claims against the assets of the entity, and the rights of creditors (liabilities) take precedence over the rights of shareholders (equity). Both sources of capital are concerned with two basic rights: the right to share in the cash or property disbursements (interest and dividends) and the right to share in the assets in the event of liquidation.

Although a statement of financial position presents an entity's financial position, it does not purport to report its value. It cannot for reasons that include:

- The values of certain assets, such as human resources, secret processes, and competitive advantages are not included in a statement of financial position despite the fact that they have value and will generate future cash flows.

- The values of other assets are measured at historical cost, rather than market value, replacement cost, or specific value to the entity. For example, property and equipment are measured at original cost reduced by depreciation, but the underlying assets' value can significantly exceed that adjusted cost and the assets may continue to be productive even though fully depreciated in the accounting records.

- The values of most liabilities are measured at the present value of cash flows at the date the liability was incurred rather than at the current market rate. When market rates increase, the increase in value of a liability payable at a fixed interest rate that is below market is not recognized in the statement of financial position. Conversely, when interest rates decrease, the loss in value of a liability payable at a fixed rate in excess of the market rate is not recognized.

It is common for the statement of financial position to be divided into classifications based on the length of the entity's operating cycle. Assets are classified as current if they are reasonably expected to be converted into cash, sold, or consumed either within one year or within one operating cycle, whichever is longer. Liabilities are classified as current if they are expected to be liquidated through the use of current assets or incurring other current liabilities. The excess or deficiency of current assets over or under current liabilities, which is referred to as net working capital, identifies, if positive, the relatively liquid portion of the entity's capital that is potentially available to serve as a buffer for meeting unexpected obligations arising within the ordinary operating cycle of the business.

Technical Alerts

Beginning with annual reporting periods on or after January 1, 2013, and interim periods within those periods, entities must disclose offsetting and related arrangements. The requirements must be replied retrospectively. Both ASUs discussed below have the same effective dates.

ASU 2011-11. In December 2011, the FASB issued ASU 2011-11, Balance Sheet (Topic 210) Disclosures about Offsetting Assets and Liabilities. The purposes of the ASU were to

- increase the comparability of financial statements prepared in accordance with GAAP and IFRS financial statements and

- enhance disclosures of transactions eligible for offsetting.

The requirements apply to financial and derivative instruments that are either offset on the statement of financial position or subject to an enforceable netting arrangement or similar agreement. The disclosures must include both net and gross information for those assets and liabilities. Required disclosures also include amounts subject to an enforceable netting arrangement not included in the statement of financial position, instruments that management makes an election not to offset, and the amounts related to financial collateral. Unless another format is more appropriate, the disclosure must be presented in tabular format, separately by assets and liabilities. In addition to the quantitative information, management must present a description of the rights of setoff for recognized assets and liabilities subject to an enforceable master netting or similar arrangement. (ASC 210-20-50).

ASU 2013-01. In January 2013, the FASB issued ASU 2013-01, Balance Sheet (Topic 210): Clarifying the Scope of Disclosures about Offsetting Assets and Liabilities. The purpose of the ASU is to address stakeholder concerns about possible diversity in practice caused by lack of clarity in ASU 2011-11. As companies began to implement ASU 2011-11, management realized that many commercial contracts have provisions that would equate to master netting arrangements. To leave the FASB provisions as issued would have caused an undue burden for little benefit. The amendments clarify that the scope of ASU 2011-11 applies to derivatives accounted for in accordance with Topic 815, Derivatives and Hedging, including:

- Bifurcated embedded derivatives,

- Repurchase agreements and reverse repurchase agreements

- Securities borrowing and securities lending transactions that are either offset in accordance with Section 210-20-45 or Section 815-10-45 or subject to an enforceable master netting arrangement or similar agreement.

The ASU removes trade payables and receivables from the scope of the offsetting disclosure requirements. The ASU also makes clear that derivatives that fall within one of the scope exceptions in ASC 815 are outside the scope of the offsetting disclosure requirements.

The IASB was informed of FASB's decision to narrow the scope of the offsetting disclosures. The IASB has not indicated whether it will revisit this issue in the future.

Practice Alerts

Financial statement classification is a frequent topic of SEC comment letters. While SEC rules only apply to public entities, preparers of financial statements can benefit from the findings of SEC reviewers. The classification of current and noncurrent assets and liabilities, including debt have been a source of SEC staff comments. Preparers should look to the guidance in ASC 210-10-45 and the discussion in this chapter when preparing classified balance sheets to determine whether an item should be classified as current or noncurrent.

The SEC staff has also commented on the classification of investments as cash equivalents. Preparers should bear in mind that an investment does not meet the ASC 230-10-20 definition of a cash equivalent unless the security is purchased very near its stated maturity date. Unless the investments are purchased three months or less before their maturity date, investments with stated maturities greater than three months cannot be classified as cash equivalents. For further information, see the Definitions of Terms section below and discussion of cash classification later in this chapter.

DEFINITIONS OF TERMS

(Source: ASC 210-10-20)

Cash Equivalents. Cash equivalents are short-term, highly liquid investments that have both of the following characteristics:

- Readily convertible to known amounts of cash

- So near their maturity that they present insignificant risk of changes in value because of changes in interest rates.

Generally, only investments with original maturities of three months or less qualify under that definition. Original maturity means original maturity to the entity holding the investment. For example, both a three-month U.S. Treasury bill and a three-year U.S. Treasury note purchased three months from maturity qualify as cash equivalents. However, a Treasury note purchased three years ago does not become a cash equivalent when its remaining maturity is three months. Examples of items commonly considered to be cash equivalents are Treasury bills, commercial paper, money market funds, and federal funds sold (for an entity with banking operations).

Current Assets. Current assets is used to designate cash and other assets or resources commonly identified as those that are reasonably expected to be realized in cash or sold or consumed during the normal operating cycle of the business.

Current Liabilities. Current liabilities is used principally to designate obligations whose liquidation is reasonably expected to require the use of existing resources properly classifiable as current assets, or the creation of other current liabilities.

Operating Cycle. The average time intervening between the acquisition of materials or services and the final cash realization constitutes an operating cycle.

Short-Term Obligations. Short-term obligations are those that are scheduled to mature within one year after the date of an entity's balance sheet or, for those entities that use the operating cycle concept of working capital, within an entity's operating cycle that is longer than one year.

Working Capital. Working capital (also called net working capital) is represented by the excess of current assets over current liabilities and identifies the relatively liquid portion of total entity capital that constitutes a margin or buffer for meeting obligations within the ordinary operating cycle of the entity.

(Source: ASC 210-20)

Cash. Consistent with common usage, cash includes not only currency on hand but demand deposits with banks or other financial institutions. Cash also includes other kinds of accounts that have the general characteristics of demand deposits in that the customer may deposit additional funds at any time and also effectively may withdraw funds at any time without prior notice or penalty. All charges and credits to those accounts are cash receipts or payments to both the entity owning the account and the bank holding it. For example, a bank's granting of a loan by crediting the proceeds to a customer's demand deposit account is a cash payment by the bank and a cash receipt of the customer when the entry is made.

Daylight Overdraft. Daylight overdraft or other intraday credit refers to the accommodation in the banking arrangements that allows transactions to be completed even if there is insufficient cash on deposit during the day provided there is sufficient cash to cover the net cash requirement at the end of the day. That accommodation may be through a credit facility, including a credit facility for which a fee is charged, or from a deposit of collateral.

Repurchase Agreement. A repurchase agreement (repo) refers to a transaction that is accounted for as a collateralized borrowing in which a seller-borrower of securities sells those securities to a buyer-lender with an agreement to repurchase them at a stated price plus interest at a specified date or in specified circumstances. The payable under a repurchase agreement refers to the amount of the seller-borrower's obligation recognized for the future repurchase of the securities from the buyer-lender. In certain industries, the terminology is reversed; that is, entities in those industries refer to this type of agreement as a reverse repo.

Reverse Repurchase Agreement. A reverse repurchase agreement (also known as a reverse repo) refers to a transaction that is accounted for as a collateralized lending in which a buyer-lender buys securities with an agreement to resell them to the seller-borrower at a stated price plus interest at a specified date or in specified circumstances. The receivable under a reverse repurchase agreement refers to the amount due from the seller-borrower for the repurchase of the securities from the buyer-lender. In certain industries, the terminology is reversed; that is, entities in those industries refer to this type of agreement as a repo.

Right of Setoff. A right of setoff is a debtor's legal right, by contract or otherwise, to discharge all or a portion of the debt owed to another party by applying against the debt an amount that the other party owes to the debtor.

Securities Custodian. The securities custodian for a securities transfer system may be the bank or financial institution that executes securities transfers over the securities transfer system, and book entry securities exist only in electronic form on the records of the transfer system operator for each entity that has a security account with the transfer system operator.

CONCEPTS, RULES, AND EXAMPLES

Form of the Statement of Financial Position

The format of a statement of financial position is not specified by any authoritative pronouncement. Instead, formats and titles have developed as a matter of tradition and, in some cases, through industry practice.

Two basic formats are used.

- The balanced format, in which the sum of the amounts for liabilities and equity are added together on the face of the statement to illustrate that assets equal liabilities plus equity

- The less frequently presented equity format, which shows totals for assets, liabilities, and equity, but no sums illustrating that assets less liabilities equal equity.

Those two formats can take one of two forms.

- The account form, presenting assets on the left-hand side of the page and liabilities and equity on the right-hand side

- The report form, which is a top-to-bottom or running presentation.

The three elements customarily displayed in the heading of a statement of financial position are:

- The legal name of the entity whose financial position is being presented

- The title of the statement (e.g., statement of financial position or balance sheet)

- The date of the statement (or statements, if multiple dates are presented for comparative purposes).

The entity's legal name appears in the heading exactly as specified in the document that created it (e.g., the certificate of incorporation, partnership agreement, LLC operating agreement, etc.). The legal form of the entity is often evident from its name when the name includes such designations as “incorporated,” “LLP,” or “LLC.” Otherwise, the legal form is either captioned as part of the heading or disclosed in the notes to the financial statements. A few examples are as follows:

ABC Company

(a general partnership)

ABC Company

(a sole proprietorship)

ABC Company

(a division of DEF, Inc.)

The use of the titles “statement of financial position,” “balance sheet,” or “statement of financial condition” infers that the statement is presented using generally accepted accounting principles. If, instead, some other comprehensive basis of accounting, such as income tax basis or cash basis is used, the financial statement title must be revised to reflect this variation. The use of a title such as “Statements of Assets and Liabilities—Income Tax Basis” is necessary to differentiate the financial statement being presented from a GAAP statement of financial position.

The last day of the fiscal period is used as the statement date. Usually, this is a month-end date unless the entity uses a fiscal reporting period always ending on a particular day of the week such as Friday or Sunday. In these cases, the statement of financial position would be dated accordingly (i.e., December 26, October 1, etc.).

Statements of financial position generally are uniform in appearance from one period to the next with consistently followed form, terminology, captions, and patterns of combining insignificant items. If changes in the manner of presentation are made when comparative statements are presented, the prior year's information must be restated to conform to the current year's presentation.

ASC 205-10, Overall

Assets, liabilities, and shareholders' equity are separated in the statement of financial position so that important relationships can be shown and attention can be focused on significant subtotals.

Current assets.

Current assets are cash and other assets that are reasonably expected to be realized in cash or sold or consumed during the normal operating cycle of the business (ASC 201-10-05-4). When the normal operating cycle is less than one year, a one-year period is used to distinguish current assets from noncurrent assets. When the operating cycle exceeds one year, the operating cycle will serve as the proper period for purposes of current asset classification. When the operating cycle is very long, the usefulness of the concept of current assets diminishes. The following items are classified as current assets:

- Cash and cash equivalents include cash on hand consisting of coins, currency, undeposited checks; money orders and drafts; demand deposits in banks; and certain short-term, highly liquid investments. Any type of instrument accepted by a bank for deposit would be considered to be cash. Cash must be available for withdrawal on demand. Cash that is restricted as to withdrawal, such as certificates of deposit, would not be included with cash because of the time restrictions. Also, cash must be available for current use in order to be classified as a current asset. Cash that is restricted in use would not be included in cash unless its restrictions will expire within the operating cycle. Cash restricted for a noncurrent use, such as cash designated for the purchase of property or equipment, would not be included in current assets. Cash equivalents include short-term, highly liquid investments that

- are readily convertible to known amounts of cash and

- are so near their maturity (maturities of three months or less from the date of purchase by the entity) that they present negligible risk of changes in value because of changes in interest rates.

US Treasury bills, commercial paper, and money market funds are all examples of cash equivalents. Only instruments with original maturity dates of three months or less qualify as cash equivalents (ASC 205-10-45-1).

- Short-term investments are readily marketable securities acquired through the use of temporarily idle cash. To be classified as current assets, management must be willing and able to sell the security to meet current cash needs, or the investment must mature within one year (or the operating cycle, if longer). These securities are accounted for under ASC 320. Securities classified as trading securities must be reported as current assets. Securities classified as held-to-maturity or available-for-sale are reported as either current or noncurrent depending upon management's intended holding period, the security's maturity date (if any), or both. It is not necessary to show the ASC 320 classification on the face of the statement of financial position. Short-term investments can be combined into a single line if the classification details appear in the notes to the financial statements. The statement of financial position presentation might be as follows:

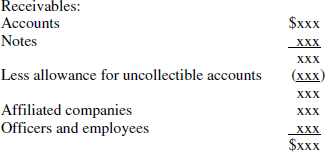

Marketable securities $xxx - Receivables include accounts and notes receivable, receivables from affiliated entities, and officer and employee receivables. The term “accounts receivable” is generally understood to represent amounts due from customers arising from transactions in the ordinary course of business (sometimes referred to as “trade receivables”). Valuation allowances, if any, are to be clearly stated. Estimates of needed allowances for uncollectibility may be based on historical correlations of bad debt experience as a percentage of sales or based on a direct credit quality analysis of the receivables. Valuation allowances to reflect the time value of money (discounts) are reported with the related receivable. If material, the different components that comprise receivables are to be separately stated. Receivables pledged as collateral are to be disclosed in the notes to the financial statements. The receivables section of a statement of financial position might be presented as follows:

- Inventories are goods on hand and available for sale. The basis of valuation and the method of pricing are to be disclosed. One form of presentation is as follows:

In the case of a manufacturing concern, raw materials, work in process, and finished goods must be stated separately on the statement of financial position or disclosed in the notes to the financial statements. Customarily, the components of manufacturing inventories are stated in order of their readiness for sale and ultimate conversion to cash—that is, finished goods are ready for sale, work in process is closer to being finished than raw materials and, of course, raw materials have not yet been placed into production. The disclosures must also include the basis upon which the amounts are stated and where practical the method of determining cost. A sample form of presentation is as follows:

- Prepaid expenses are amounts paid in advance to secure the use of assets or the receipt of services at a future date. Prepaid expenses will not be converted to cash, but they are classified as current assets because, if not prepaid, they would have required the use of current assets during the coming year or operating cycle, if longer (ASC 205-10-45-2). Prepaid rent and prepaid insurance are the most common examples of prepaid expenses.

ASC 205-10-45-4 excludes the following from current assets:

- Cash and claims to cash that are restricted as to withdrawal or use for other than current operations, are designated for expenditure in the acquisition or construction of noncurrent assets, or are segregated for the liquidation of long-term debts. Even though not actually set aside in special accounts, funds that are clearly to be used in the near future for the liquidation of long-term debts, payments to sinking funds, or for similar purposes shall also, under this concept, be excluded from current assets. However, if such funds are considered to offset maturing debt that has properly been set up as a current liability, they may be included within the current asset classification.

- Investments in securities (whether marketable or not) or advances that have been made for the purposes of control, affiliation, or other continuing business advantage.

- Receivables arising from unusual transactions (such as the sale of capital assets, or loans or advances to affiliates, officers, or employees) that are not expected to be collected within 12 months.

- Cash surrender value of life insurance policies.

- Land and other natural resources.

- Depreciable assets.

- Long-term prepayments that are fairly chargeable to the operations of several years, or deferred charges such as bonus payments under a long-term lease, costs of rearrangement of factory layout or removal to a new location.

Noncurrent assets.

Excluded from the classification of current assets are assets that will not be realized in cash during the next year (or operating cycle, if longer). The following assets would be classified as noncurrent assets:

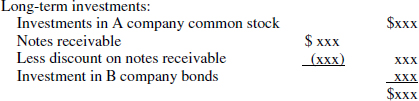

- Long-term investments are investments that are intended to be held for an extended period of time (longer than one operating cycle). The following are the three major types of long-term investments:

- Debt and equity securities are stocks, bonds, and long-term notes receivable. Securities that are classified as available-for-sale or held-to-maturity investments under ASC 320 would be classified as long-term if management intended to hold them for more than one year. Under ASC 320, the categories of these securities (held-to-maturity versus available-for-sale) need not be reported on the face of the statement of financial position if they are reported in the notes to the financial statements. The securities section of the statement of financial position could be presented as follows:

- Tangible assets not currently used in operations (e.g., land purchased as an investment and held for sale).

- Investments held in special funds (e.g., sinking funds, pension funds, amounts held for plant expansion, and cash surrender values of life insurance policies).

- Debt and equity securities are stocks, bonds, and long-term notes receivable. Securities that are classified as available-for-sale or held-to-maturity investments under ASC 320 would be classified as long-term if management intended to hold them for more than one year. Under ASC 320, the categories of these securities (held-to-maturity versus available-for-sale) need not be reported on the face of the statement of financial position if they are reported in the notes to the financial statements. The securities section of the statement of financial position could be presented as follows:

- Property, plant, and equipment are assets of a durable nature that are used in the production or sale of goods, sale of other assets, or rendering of services rather than being held for sale (e.g., machinery and equipment, buildings, furniture and fixtures, natural resources, and land). These are disclosed with related accumulated depreciation/depletion as follows:

Accumulated depreciation may be shown in total or by major classes of depreciable assets. In addition to showing this amount on the statement of financial position, the notes to the financial statements are to disclose the amounts of major classes of depreciable assets, by nature or function, at the date of the statement of financial position. Assets under capital leases are separately disclosed. A general description of the method or methods used in computing depreciation with respect to major classes of depreciable assets (ASC 360-10-50) is also to be included in the notes to financial statements.

- Intangible assets include legal and/or contractual rights that are expected to provide future economic benefits and purchased goodwill. The technical definition of goodwill is that it represents the excess of the cost of an acquired entity over the net of the fair values assigned to its identifiable assets and liabilities. Practically, goodwill represents the amount by which the acquirer believes the acquiree entity's fair value as a whole exceeds the net fair value of its assets and liabilities. Goodwill is only recognized as an asset when acquired in a business combination; internally generated goodwill is not explicitly recognized, although it may in fact be implicitly given recognition as a replacement for impaired purchased goodwill due to the mechanical workings of the goodwill impairment assessment process under GAAP. Patents, copyrights, logos, and trademarks are examples of rights that are recognized as intangible assets. Intangible assets with finite useful lives are amortized to expense over those lives. Generally, the amortization of an intangible asset is credited directly to the recorded amount of the asset although it is acceptable to use an accumulated amortization valuation allowance. Intangible assets with indefinite economic useful lives are tested for impairment at least annually.

- Other assets is an all-inclusive heading which incorporates assets that do not fit neatly into any of the other asset categories (e.g., long-term prepaid expenses, deposits made to purchase equipment, deferred income tax assets (net of any required valuation allowance), bond issue costs, noncurrent receivables, and restricted cash).

Liabilities

Liabilities are displayed on the statement of financial position in the order of expected payment.

Current liabilities.

Obligations are classified as current if their liquidation is reasonably expected to require the use of existing resources properly classifiable as current assets or to create other current obligations (ASC 210-45-5). Current liabilities also includes obligations that are due on demand or that are callable at any time by the lender are classified as current regardless of the intent of the entity or lender. ASC 470-10-45 includes more guidance on those and on short-term debt expected to be refinanced (ASC 205-10-45-7). The following items are classified as current liabilities:

- Accounts payable. Accounts payable is normally comprised of amounts due to suppliers (vendors) for the purchase of goods and services used in the ordinary course of running a business.

- Trade notes payable are also obligations that arise from the purchase of goods and services. They differ from accounts payable because the supplier or vendor finances the purchase on terms longer than the customary period for trade payables. The supplier or vendor generally charges interest for this privilege. If interest is not charged, it is imputed in accordance with ASC 835.

A valuation allowance is used to reduce the carrying amount of the note for the resulting discount as follows:

- Accrued expenses represent estimates of expenses incurred on or before the date of the statement of financial position that have not yet been paid and that are not payable until a succeeding period within the next year. Examples of accrued expenses include salaries, vacation pay, interest, and retirement plan contributions.

- Dividends payable are obligations to distribute cash or other assets to shareholders that arise from the declaration of dividends by the entity's board of directors.

- Advances and deposits are collections of cash or other assets received in advance to ensure the future delivery of goods or services. Advances and deposits are classified as current liabilities if the goods and services are to be delivered within the next year (or the operating cycle, if longer). Advances and deposits include such items as advance rentals and customer deposits. Certain advances and deposits are sometimes captioned as deferred or unearned revenues.

- Agency collections and withholdings are liabilities that arise because the entity acts as an agent for another party. Employee tax withholdings, sales taxes, and wage garnishments are examples of agency collections.

- Current portion of long-term debt is the portion of a long-term obligation that will be settled during the next year (or operating cycle, if longer) by using current assets. Generally, this amount includes only the payments due within the next year under the terms of the underlying agreement. However, if the entity has violated a covenant in a long-term debt agreement and, as a result, the investor is legally entitled to demand payment, the entire debt amount is classified as current unless the lender formally (in writing) waives the right to demand repayment of the debt for a period in excess of one year (or one operating cycle, if longer). In two cases, obligations to be paid in the next year are not classified as current liabilities. Debt expected to be refinanced through another long-term issue and debt that will be retired through the use of noncurrent assets, such as a bond sinking fund, are treated as noncurrent liabilities because the liquidation does not require the use of current assets or the creation of other current liabilities.

Noncurrent liabilities.

Obligations that are not expected to be liquidated within one year (or the current operating cycle, if longer) are classified as noncurrent. The following items would be classified as noncurrent:

- Notes and bonds payable are obligations that will be paid in more than one year (or one operating cycle, if longer).

- Capital lease obligations are contractual obligations that arise from obtaining the use of property or equipment via a capital lease contract.

- Written put options on the option writer's (issuer's) equity shares and forward contracts to purchase an issuer's equity shares that require physical or net cash settlement are classified as liabilities on the issuer's statement of financial position. The obligation is classified as noncurrent unless the date at which the contract will be settled is within the next year (or operating cycle, if longer).

- Certain financial instruments that embody an unconditional obligation to issue a variable number of equity shares and financial instruments other than outstanding shares that embody a conditional obligation to issue a variable number of equity shares are classified as a liability in the issuer's statement of financial position. The obligation is classified as noncurrent unless the date at which the financial instrument will be settled is within the next year (or operating cycle, if longer).

- Contingent obligations are recorded when it is probable that an obligation will occur as the result of a past event. In most cases, a future event will eventually confirm the amount payable, the payee, or the date payable. The classification of a contingent liability as current or noncurrent depends on when the confirming event will occur and how soon afterwards payment must be made.

- Mandatorily redeemable shares are recorded as liabilities per ASC 480. A mandatory redemption clause requires common or preferred stock to be redeemed (retired) at a specific date(s) or upon occurrence of an event which is uncertain as to timing although ultimately certain to occur. The obligation is classified as noncurrent unless the date at which the shares must be redeemed is within the next year (or operating cycle, if longer).

- Other noncurrent liabilities include defined benefit pension obligations, postemployment obligations, and postretirement obligations. Deferred income taxes are liabilities to pay income taxes in the future that result from differences between the carrying amounts of assets and liabilities for income tax and financial reporting purposes.

Presentation

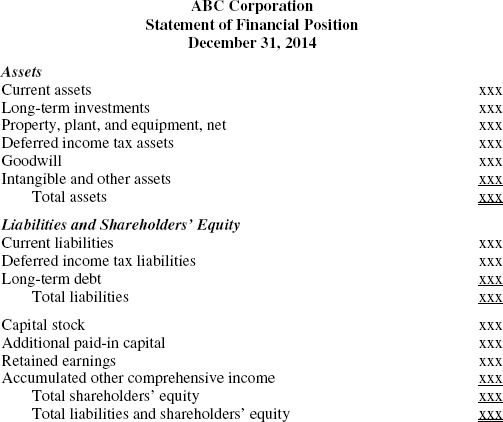

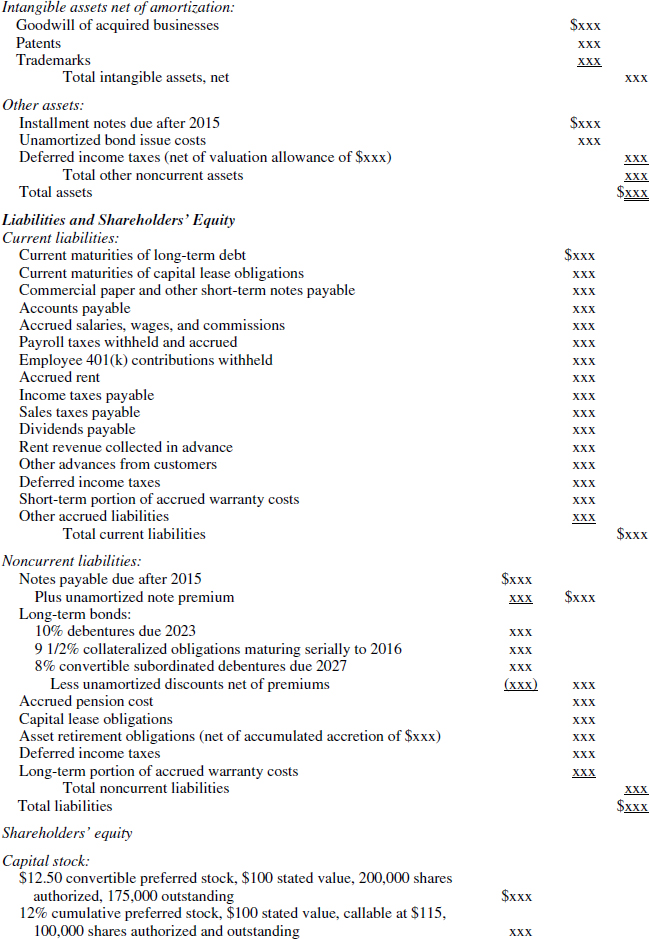

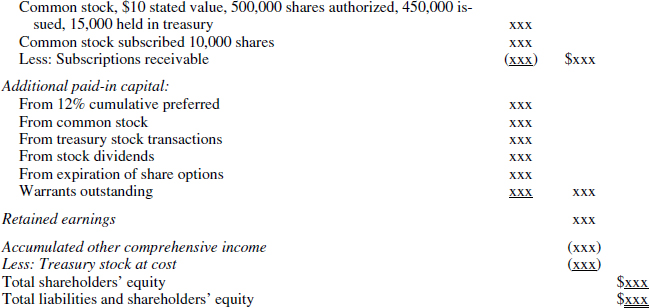

The classification and presentation of information in a statement of financial position may be highly aggregated, highly detailed, or anywhere in between. In general, highly aggregated statements of financial position are used in annual reports and other presentations provided to the public. Highly detailed statements of financial position are used internally by management. The following highly aggregated statement of financial position includes only a few line items. The additional details required by GAAP are found in the notes to the financial statements.

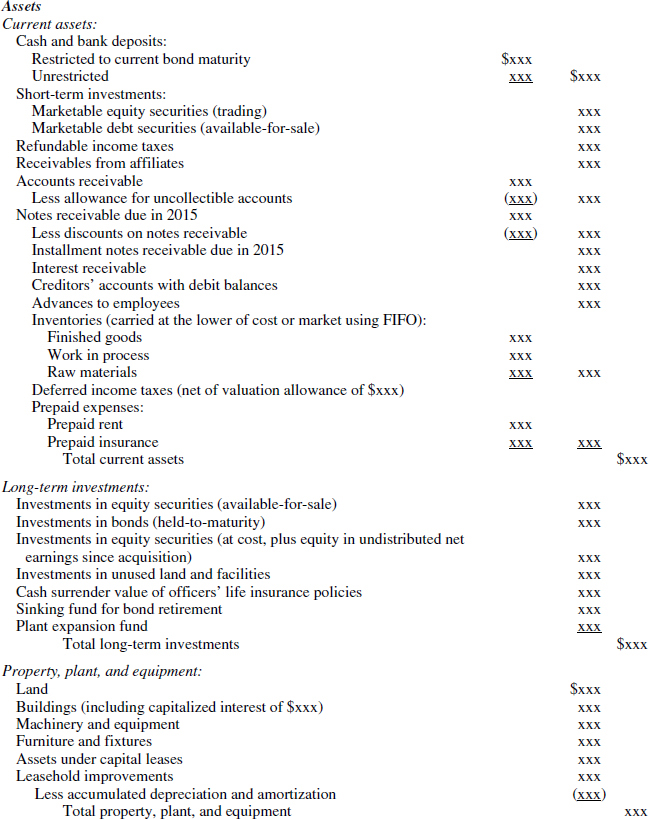

The following more-comprehensive statement of financial position includes more line items (for details about specific assets and liabilities) than are found in most statements of financial position.

ABC Corporation

Statement of Financial Position

December 31, 2014

ASC 210-20, Offsetting

(See also the Technical Alerts section at the beginning of this chapter for more information). In general, assets and liabilities are not permitted to be offset against each other unless certain specified criteria are met. ASC 210-20-45-1 permits offsetting only when all of the following conditions are met that constitute a right of setoff:

- Each of the two parties owes the other determinable amounts (although they may be in different currencies and bear different rates of interest).

- The reporting party has the right to set off the amount it owes against the amount owed to it by the other party.

- The reporting party intends to set off the two amounts.

- The right of setoff is legally enforceable.

In particular cases, state laws or bankruptcy laws may impose restrictions or prohibitions against the right of setoff (ASC 205-10-45-3).

The offsetting of cash or other assets against a tax liability or other amounts due to governmental bodies is acceptable only under limited circumstances (ASC 205-10-45-6). When it is clear that a purchase of securities is in substance an advance payment of taxes payable in the near future and the securities are acceptable for the payment of taxes, amounts may be offset. Primarily this occurs as an accommodation to governmental bodies that issue tax anticipation notes in order to accelerate the receipt of cash from future taxes (ASC 205-10-45-7).

Furthermore, when maturities differ, only the party with the nearest maturity can offset, because the party with the later maturity must settle in the manner determined by the party with the earlier maturity (ASC 205-10-45-8).

ASC 210-20-45-11 permits the offset of amounts recognized as payables in repurchase agreements against amounts recognized as receivables in reverse repurchase agreements with the same counterparty. If certain conditions are met, an entity may, but is not required to, offset the amounts recognized. The additional conditions are

- The repurchase agreements and the reverse repurchase agreements must have the same explicit settlement date.

- The repurchase agreements and the reverse repurchase agreements must be executed in accordance with a master netting agreement.

- The securities underlying the repurchase agreements and the reverse repurchase agreements exist in “book entry” form and can be transferred only by means of entries in the records of the transfer system operator or the security custodian

- The repurchase agreements and the reverse repurchase agreements will be settled on a securities transfer system that transfers ownership of “book entry” securities, and banking arrangements are in place so that the entity must only keep cash on deposit sufficient to cover the net payable.

- The same account at the clearing bank is used for the cash inflows of the settlement of the reverse repurchase agreements and the cash outflows in the settlement of the repurchase agreements.

Other Sources

| See ASC Location – Wiley GAAP Chapter... | For information on... |

| ASC 310-10-45-8 | The presentation of unearned discounts (other than cash or quantity discounts and the like), finance charges, and interest. |

| ASC 605-35-45-2 | The presentation of provisions for losses on contracts. |

| ASC 852-10-45-4 | The presentation of liabilities subject to compromise and those not subject to compromise during reorganization proceedings. |

| ASC 926-20-45-1 | The presentation of film costs in a classified balance sheet. |