47 ASC 810 CONSOLIDATIONS

Special-Purpose Entities and Variable Interest Entities

GAAP treatment of special-purpose entities

Example of expected variability of cash flows

Initial determination of VIE status

Determination and redetermination of whether an interest holder is the primary beneficiary

Related-party considerations in determining the primary beneficiary

Initial measurement with common control

Initial measurement absent common control

Example of consolidation of a VIE

Example of an implicit variable interest

Example of application of ASC 810-10-25 to a synthetic lease

Changing or eliminating differences in fiscal year-end

Partnerships and similar entities

Limited liability companies that maintain a specific ownership account for each investor

Limited liability companies that are functionally equivalent to corporations (“analogous entities”)

Display in the reporting entity's financial statements when the investee is not a corporation

PERSPECTIVE AND ISSUES

Subtopics

ASC 810, Consolidations, consists of three subtopics:

- ASC 810-10, Overall, which has three subsections:

- General

- Variable Interest Entities

- Consolidation of Entities Controlled by Contract

- ASC 810-20, Control of Partnerships and Similar Entities, which addresses the potential consolidation of those entities

- ASC 810-30, Research and Development Arrangements, which provides direction on whether and how those arrangements should be consolidated.

Scope and Scope Exceptions

ASC 810-10. The following are excluded from the scope of the subtopics and sections of ASC 810-10 governing variable interest entities (VIE) (ASC 810-10-15-17 et seq.):

- Not-for-profit organizations unless the organization was organized to avoid VIE status. It is important to note, however, that a not-for-profit organization can be a related party for the purpose of determining the primary beneficiary (parent) of a VIE by applying ASC paragraphs 810-10-25-42 through 44.

- Employers are not to consolidate an employee benefit plan subject to ASC 712, Nonretirement Postemployment Benefits) or to ASC 715, Retirement Benefits.

- Separate accounts of life insurance entities (ASC 944-80).

- A governmental organization.

- A nongovernmental financing entity, unless the financing entity meets both of the following conditions:

- It is not a governmental organization, and

- It is used by a business entity in a manner similar to a VIE to attempt to circumvent VIE accounting rules.

- Investments accounted for at fair value, as per ASC 946.

- An entity created prior to December 31, 2003, for which, after expending “exhaustive efforts,” management of the variable interest holder is unable to obtain information needed to determine whether the entity is a VIE, determine whether the holder is the primary beneficiary, or make the required consolidating/eliminating entries required by FIN 46(R).

- An entity that qualifies to be treated as a business, as defined in ASC 810-10-30-2, need not be evaluated by a variable interest holder to determine whether it is a VIE unless one or more of the following conditions exists:

- The variable interest holder and/or its related parties/de facto agents1 (de facto agents are discussed later in this chapter) participated significantly in the design or redesign of the entity. This factor is not considered when the entity is an operating joint venture jointly controlled by the variable interest holder, and either one or more independent parties, or a franchisee.

- The design of the entity results in substantially all of its activities either involving or being conducted on behalf of the variable interest holder and its related parties.

- Based on the relative fair values of interests in the entity, the variable interest holder and its related parties provide more than half of its total equity, subordinated debt, and other forms of subordinated financial support.

- The entity's activities relate primarily to one or both of the following:

- (1) Single-lessee leases

- (2) Securitizations or other forms of asset-backed financings.

ASC 810-20. An entity is in the scope of ASC 810-20 if the entity is required to apply the consolidation guidance in ASC 810-10 to its investment in a limited partnership. ASC 810-20 does not apply to:

- Limited partnerships or similar entities that are entities within the scope of the Variable Interest Entities Subsections of ASC 810-10.

- A general partner that carries its investment in the limited partnership at fair value with changes in fair value reported in a statement of operations or financial performance.

- Entities in industries in which it is appropriate for a general partner to use the pro rata method of consolidation for its investment in a limited partnership.

- Circumstances in which no single general partner in a group of general partners controls the limited partnership.

(ASC 810-20-15-2)

ASC 810-30. ASC 810-30 is limited to those research and development arrangements in which all of the funds for the research and development activities are provided by the sponsor of the research and development arrangement. It does not apply to either:

- Transactions in which the funds are provided by third parties, which would generally be within the scope of Subtopic 730-20.

- Special-purpose entities required to be consolidated under the guidance on variable interest entities.

Overview

The major accounting issues in business combinations and in the preparation and presentation of consolidated or combined financial statements are as follows:

- The proper accounting basis for the assets and liabilities of the combining entities

- The accounting for goodwill or negative goodwill (the gain from a bargain purchase), if any exists

- The elimination of intercompany balances and transactions in the preparation of consolidated or combined statements.

While the presentation of consolidated financial statements is required under GAAP, there is no parallel requirement to present combined financial statements for entities under common control (brother/sister entities). However, in certain cases, it is desirable that combined financial statements be prepared for such entities. This process is very similar to an accounting consolidation using the formerly permitted pooling accounting, except that the equity accounts for the combining entities are carried forward intact.

Consolidation of variable interest entities (VIEs) has increased substantially under the ASC 810 requirements, which were spurred on by the financial reporting scandals of the early 2000s.

The accounting for the assets and liabilities of entities acquired in a business combination is largely dependent on the fair values assigned to them at the transaction date. (The now-obsolete pooling method relied upon book values.) ASC 820, Fair Value Measurements, provides a framework for measuring fair value and important guidance when assigning values as part of a business combination. In essence, it favors valuations determined on the open market, but allows other methodologies if open market valuation is not practicable.

DEFINITIONS OF TERMS

Source: ASC 810

Business. An integrated set of activities and assets that is capable of being conducted and managed for the purpose of providing a return in the form of dividends, lower costs, or other economic benefits directly to investors or other owners, members, or participants. Additional guidance on what a business consists of is presented in paragraphs 805-10-55-4 through 55-9.

Business Combination. A transaction or other event in which an acquirer obtains control of one or more businesses. Transactions sometimes referred to as true mergers or mergers of equals also are business combinations. See also Acquisition by a Not-for-Profit Entity.

Combined Financial Statements. The financial statements of a combined group of commonly controlled entities or commonly managed entities presented as those of a single economic entity. The combined group does not include the parent.

Consolidated Financial Statements. The financial statements of a consolidated group of entities that include a parent and all its subsidiaries presented as those of a single economic entity.

Consolidated Group. A parent and all its subsidiaries.

Equity Interests. Used broadly to mean ownership interests of investor-owned entities; owner, member, or participant interests of mutual entities; and owner or member interests in the net assets of not-for-profit entities.

Expected Losses. A legal entity that has no history of net losses and expects to continue to be profitable in the foreseeable future can be a variable interest entity (VIE). A legal entity that expects to be profitable will have expected losses. A VIE's expected losses are the expected negative variability in the fair value of its net assets exclusive of variable interests and not the anticipated amount or variability of the net income or loss.

Expected Losses and Expected Residual Returns. Expected losses and expected residual returns refer to amounts derived from expected cash flows as described in FASB Concepts Statement No. 7, Using Cash Flow Information and Present Value in Accounting Measurements. However, expected losses and expected residual returns refer to amounts discounted and otherwise adjusted for market factors and assumptions rather than to undiscounted cash flow estimates. The definitions of expected losses and expected residual returns specify which amounts are to be considered in determining expected losses and expected residual returns of a variable interest entity (VIE).

Expected Residual Returns. A variable interest entity's (VIE's) expected residual returns are the expected positive variability in the fair value of its net assets exclusive of variable interests.

Expected Variability. Expected variability is the sum of the absolute values of the expected residual return and the expected loss. Expected variability in the fair value of net assets includes expected variability resulting from the operating results of the legal entity.

Fair Value. The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Foreign Entity. An operation (for example, subsidiary, division, branch, joint venture, and so forth) whose financial statements are both:

- Prepared in a currency other than the reporting currency of the reporting entity

- Combined or consolidated with or accounted for on the equity basis in the financial statements of the reporting entity.

Kick-Out Rights. The ability to remove the reporting entity with the power to direct the activities of a VIE that most significantly impact the VIE's economic performance.

Legal Entity. Any legal structure used to conduct activities or to hold assets. Some examples of such structures are corporations, partnerships, limited liability companies, grantor trusts, and other trusts.

Noncontrolling Interest. The portion of equity (net assets) in a subsidiary not attributable, directly or indirectly, to a parent. A noncontrolling interest is sometimes called a minority interest.

Owners. Used broadly to include holders of ownership interests (equity interests) of investor-owned entities, mutual entities, or not-for-profit entities. Owners include shareholders, partners, proprietors, or members or participants of mutual entities. Owners also include owner and member interests in the net assets of not-for-profit entities.

Parent. An entity that has a controlling financial interest in one or more subsidiaries. (Also, an entity that is the primary beneficiary of a variable interest entity.)

Participating Rights. The ability to block the actions through which a reporting entity exercises the power to direct the activities of a VIE that most significantly impact the VIE's economic performance. (ASC 810-10-20)

Participating Rights. Participating rights allow the limited partners to participate in certain financial and operating decisions of the limited partnership that are made in the ordinary course of business. (ASC 810-20-20)

Primary Beneficiary. An entity that consolidates a variable interest entity (VIE). See paragraphs 810-10-25-38 through 25-38G for guidance on determining the primary beneficiary.

Protective Rights. Rights designed to protect the interests of the party holding those rights without giving that party a controlling financial interest in the entity to which they relate. For example, they include any of the following:

- Approval or veto rights granted to other parties that do not affect the activities that most significantly impact the entity's economic performance. Protective rights often apply to fundamental changes in the activities of an entity or apply only in exceptional circumstances. Examples include both of the following:

- A lender might have rights that protect the lender from the risk that the entity will change its activities to the detriment of the lender, such as selling important assets or undertaking activities that change the credit risk of the entity.

- Other interests might have the right to approve a capital expenditure greater than a particular amount or the right to approve the issuance of equity or debt instruments.

- The ability to remove the reporting entity that has a controlling financial interest in the entity in circumstances such as bankruptcy or on breach of contract by that reporting entity.

- Limitations on the operating activities of an entity. For example, a franchise agreement for which the entity is the franchisee might restrict certain activities of the entity but may not give the franchisor a controlling financial interest in the franchisee. Such rights may only protect the brand of the franchisor.

Publicly Traded Entity under (or Public Entity). Any entity that does not meet the definition of a nonpublic entity.

Related Parties. Related parties include:

- Affiliates of the entity

- Entities for which investments in their equity securities would be required, absent the election of the fair value option under the Fair Value Option Subsection of Section 825-10-15, to be accounted for by the equity method by the investing entity

- Trusts for the benefit of employees, such as pension and profit-sharing trusts that are managed by or under the trusteeship of management

- Principal owners of the entity and members of their immediate families

- Management of the entity and members of their immediate families

- Other parties with which the entity may deal if one party controls or can significantly influence the management or operating policies of the other to an extent that one of the transacting parties might be prevented from fully pursuing its own separate interests

- Other parties that can significantly influence the management or operating policies of the transacting parties or that have an ownership interest in one of the transacting parties and can significantly influence the other to an extent that one or more of the transacting parties might be prevented from fully pursuing its own separate interests.

Sponsor. An entity that capitalizes a research and development arrangement.

Subordinated Financial Support. Variable interests that will absorb some or all of a variable interest entity's (VIE's) expected losses.

Subsidiary. An entity, including an unincorporated entity such as a partnership or trust, in which another entity, known as its parent, holds a controlling financial interest. (Also, a variable interest entity that is consolidated by a primary beneficiary.)

Variable Interest Entity. A legal entity subject to consolidation according to the provisions of the Variable Interest Entities Subsections of Subtopic 810-10.

Variable Interests. The investments or other interests that will absorb portions of a variable interest entity's (VIE's) expected losses or receive portions of the entity's expected residual returns are called variable interests. Variable interests in a VIE are contractual, ownership, or other pecuniary interests in a VIE that change with changes in the fair value of the VIE's net assets exclusive of variable interests. Equity interests with or without voting rights are considered variable interests if the legal entity is a VIE and to the extent that the investment is at risk as described in paragraph 810-10-15-14. Paragraph 810-10-25-55 explains how to determine whether a variable interest in specified assets of a legal entity is a variable interest in the entity. Paragraphs 810-10-55-16 through 55-41 describe various types of variable interests and explain in general how they may affect the determination of the primary beneficiary of a VIE.

CONCEPTS, RULES, AND EXAMPLES

Special-Purpose Entities and Variable Interest Entities

Introduction and background.

ASC 810 provides the primary authority for determining when presentation of consolidated financial statements is required. The rationale underlying ASC 810 is that consolidated financial statements are more informative to users when one enterprise directly or indirectly holds a controlling financial interest in one or more other enterprises. It further stipulates that the usual condition that best evidences which party holds a controlling financial interest is the party that holds a majority voting interest.

The foregoing discussion of consolidations and business combinations provided extensive guidance regarding parent/subsidiary relationships in the context of the parent holding a majority voting interest in the subsidiary. The subsidiary in this relationship is sometimes referred to as a voting interest entity.

Managers and their advisors have devised many new and creative types of ownership structures, financing arrangements, financial instruments, and business relationships. Many, if not most, of these arrangements were originated to accomplish legitimate business objectives. Some of the arrangements, however, were financially engineered with the express intent of establishing financial control over assets or operations while the sponsoring entity avoided obtaining the voting control that served as the determinant of the need for accounting consolidation.

Examples of such arrangements abound and have been discussed in the chapter on ASC 805. Perhaps no such type of financial arrangement or structure, however, has received the level of negative publicity as the special-purpose entity (SPE). An SPE is narrowly defined as a trust or other legal vehicle to which a transferor transfers a portfolio of financial assets, such as mortgage loans, commercial loans, credit card debt, automobile loans, and other groups of homogenous borrowings.

Commonly, SPEs have been organized as trusts or partnerships (flow-through entities, to avoid double incidence of corporate income taxation), and the outside equity participant was ultimately defined as having as little as 3% of the total assets of the SPE at risk. No authoritative GAAP ever established this 3% threshold, but nevertheless it evolved somewhat by default and had been subject to varying interpretations under different sets of conditions.

In a process called a securitization, the SPE typically issues and sells securities that represent beneficial interests in the cash flows from the portfolio. The proceeds the SPE receives from the sale of these securities are used to purchase the portfolio from the transferor. The cash flows received by the SPE from the dividends, interest, redemptions, principal repayments, and/or realized gains on the financial assets are used to pay a return to the investors in the SPE's securities. By transferring packages of such loans to an SPE, these assets can be legally isolated and made “bankruptcy proof” (and thus made more valuable as collateral for other borrowings); various types of debt instruments can thus be used, providing the sponsor with fresh resources to fund future lending activities.

GAAP treatment of special purpose entities.

SPEs had their origin in the rules for consolidation, which historically were based on the existence of majority ownership of one enterprise by another. While the substitution of control for ownership had been contemplated as a means of limiting the use of SPEs to evade consolidation requirements, practical difficulties in defining control had kept this project from fruition for many years.

The concept of a qualified SPE (QSPE) denotes that an SPE can participate in “true sales” of financial assets under ASC 860-20, to be accounted for as sales rather than as secured borrowings. QSPEs have been eliminated.

Importantly, for the sponsor to avoid consolidating the SPE, the outside equity participant was required to have control, which—although customarily not invoked under GAAP as the criterion for consolidation—was established as the key determinant for sponsor nonconsolidation of an SPE. Where an SPE was controlled by parties other than the sponsor, and there was significant at-risk capital invested by them, consolidation of the SPE in the sponsor's financial statements could be avoided.

Problems in past practice.

While ASC 810 requires the consolidation of VIEs engaged in leasing, and in a wide range of other transactions, its scope exceptions specifically permitted sponsors to avoid consolidating QSPEs. These structures were widely used by corporations and financial institutions, and at the time that these rules were originally issued, consolidation of QSPE was viewed as being potentially disruptive to the effective functioning of the capital markets.

With the benefit of hindsight, it is clear that the rules for SPEs evolved in a way that left too much to chance and to the influence of highly interested parties. As a result, notwithstanding the arguably important role that SPEs may have played in providing liquidity and lending capacity to the financial marketplace, SPEs came to be widely used to manipulate financial reporting. Thus, the “outside” equity participants often funded their “independent capital contributions” with debt obtained from lenders to the sponsor, or via debt indirectly guaranteed by the sponsor, some of whom evaded disclosure of their positions as guarantors by means of imaginative interpretations of GAAP, particularly of FAS 5, codified as ASC 450.

Furthermore, sponsors engaged in transactions with SPEs that often resulted in the sponsors recognizing large amounts of income. In some instances, complex sets of guarantees and option arrangements had the effect of causing these gains to potentially be reversible in the future, clearly not evidence of the economic substance intended by FASB to be present in order to justify off-balance-sheet treatment. In the most egregious transactions, sponsors were able to recoup reportable gains from economic events and transactions that could never have supported income recognition if engaged in directly by the entity, even extending to recognizing fair value changes in the sponsor's own capital stock.

It is clear that SPEs do serve various tax, legal, and strategic corporate objectives, but whether the exclusion of SPEs from their sponsor's consolidated financial statements had, under prior rules, any accounting legitimacy remains an unanswered question. In other words, in setting forth a representation of an entity's economic position and the results of its operations, the validity of excluding events or transactions that are in fact integral to the entity's current financial position and future prospects, merely because these have been “walled off” by a legal structure, was doubtful. Simply put, the issue is whether economic substance is to be presented, regardless of legal form.

FASB's response to Enron.

After the public revelations regarding Enron and its use of SPEs to conceal its true financial condition, FASB recognized the need to augment the existing consolidations model to take into account financial arrangements where parties other than the holders of a majority of the voting interests exercise financial control over another entity. Thus, it undertook a project to issue an interpretation of Accounting Research Bulletin (ARB) 51 to broaden its scope.

In its deliberations on these issues, FASB decided not to refer to entities within the scope of the eventual interpretation as SPEs. This decision underscores the fact that the type of entity to which the interpretation applies is more broadly defined than entities that qualify as SPEs involved in securitization transactions or even SPEs that hold nonfinancial assets.

FASB coined the term variable interest entity (VIE) to designate an entity that is financially controlled by one or more parties that do not hold a majority voting interest. A party that possesses the majority of this financial control, if there is one, is referred to as the VIE's primary beneficiary. This new language proved burdensome and confusing in practice, and FASB responded by amending the definition of “parent” to include a VIE's primary beneficiary and amended the definition of “subsidiary” to include a VIE that is consolidated by its primary beneficiary.

See the Scope and Scope Exceptions section at the beginning of this chapter for details on entities excluded from the ASC 810-10 guidance.

Terminology.

FIN 46(R), codified as part of the Consolidations Topic at ASC 810-10, substantially altered the US GAAP consolidations model to which accountants had long been accustomed. Under ASC 810-10, VIEs that have a primary beneficiary, as defined, must be consolidated in the general-purpose financial statements of that primary beneficiary, regardless of the extent of ownership (or lack of it) by that entity. The ASC introduced a number of new terms and concepts in the attempt to explain and operationalize the accounting for VIEs.

Variable interests. (See definition in Definition of Terms section.) Variable interests are identified by thoroughly analyzing the assets, liabilities, and contractual arrangements of an entity to determine whether each item being analyzed creates variability or absorbs/receives variability. Favorable changes in the fair value of the entity's net assets and contractual arrangements that create variability comprise expected residual returns which result from estimated outcomes in which the entity outperforms the probability-weighted expected results. Unfavorable changes in the fair value of the entity's net assets and contractual arrangements that create variability comprise expected losses which result from estimated outcomes in which the entity underperforms the probability-weighted expected results.

ASC 810-10-55-16, Identifying Variable Interests, provides examples of potential variable interests. Each of the items below is potentially an explicit or implicit variable interest in an entity or in specified assets of an entity. Upon analysis of the specific facts, circumstances, and contractual terms, the financial statement preparer is charged with determining whether a particular item either absorbs expected losses or receives expected residual returns (collectively referred to as expected variability) or both. The absorbing/receiving of variability is the sole determinant of whether an interest is a variable interest and, in analyzing specific situations, the degree of variability can differ widely for each item:

- At-risk equity investments in a VIE

- Investments in subordinated debt instruments issued by a VIE

- Investments in subordinated beneficial interests issued by a VIE

- Guarantees of the value of VIE assets or liabilities

- Written put options on the assets of a VIE or similar obligations that protect senior interests from suffering losses

- Forward contracts to sell assets owned by the entity at a fixed price

- Stand-alone or embedded derivative instruments, including total return swaps and similar arrangements

- Contracts or agreements for fees to be paid to a decision maker (These are generally deemed to absorb variability unless the relationship between the entity and the decision maker meets specified criteria to be considered an employee/employer relationship or a “hired service provider” relationship, in which case the arrangement would not be deemed to create a variable interest. In this case, the fees would be included in computations of expected variability.)

- Other service contracts with non-decision makers

- Operating leases that include residual value guarantees and/or lessee option to purchase the leased property at a specified price

- Variable interests of one VIE in another VIE

- Interests retained by a transferor of financial assets to a VIE.

As previously stated, although all of these examples potentially qualify as variable interests, they differ widely in terms of the extent of their variability, which has a direct effect on the likelihood of their causing their holders to be considered the primary beneficiary of the VIE. Note that an interest can qualify as a variable interest but the entity in which the interest is held may not qualify as a VIE.

Variable interest entities. VIEs include any entity that, by design, possesses one of the following characteristics:

- The total equity investment at risk is not sufficient to permit the entity to finance its activities without additional subordinated financial support from either the existing equity holders or other parties. That is, the equity investment at risk is not sufficient to absorb all of the expected losses of the entity. For this purpose, the total equity investment at risk

- Includes only equity investments in the entity that participate significantly in profits and losses even if those investments do not carry voting rights.

- Does not include equity interests that the entity issued in exchange for subordinated interests in other variable interest entities.

- Does not include amounts provided to the equity investor directly or indirectly by the entity or by other parties involved with the entity (for example, by fees, charitable contributions, or other payments), unless the provider is a parent, subsidiary, or affiliate of the investor that is required to be included in the same set of consolidated financial statements as the investor.

- Does not include amounts financed for the equity investor (for example, by loans or guarantees of loans) directly by the entity or by other parties involved with the entity, unless that party is a parent, subsidiary, or affiliate of the investor that is required to be included in the same set of consolidated financial statements as the investor.

or

- As a group, the holders of the equity investment at risk lack any one of the following three characteristics of a controlling financial interest:

- The direct or indirect ability through voting or similar rights to make decisions about an entity's activities that affect the entity's success. The investors do not have that ability through voting rights or similar rights if no owners hold voting rights or similar rights (such as those of a common stockholder in a corporation or a general partner in a partnership).

- The obligation to absorb the expected losses of the entity. The investor or investors do not have that obligation if they are directly or indirectly protected from absorbing the expected losses or are guaranteed a return by the entity itself or by other parties with whom the entity is involved.

- The right to receive the expected residual returns of the entity. The investors do not have that right if their return is limited to a specified maximum amount by the entity's governing documents or arrangements with other variable interest holders or with the entity.

The equity investors as a group also are considered to lack characteristic 2a if, upon consideration of those investors' at-risk equity investments and all other interests in the entity, (1) the voting rights of some investors are not proportional to their obligations to absorb the entity's expected losses, to receive the entity's expected residual returns, or both, and (2) substantially all of the entity's activities (for example, lending activities, or asset acquisitions) either involve or are conducted on behalf of an investor that has disproportionately few voting rights.

(ASC 810-10-15-14)

In other words, VIEs are generally thinly capitalized entities that carry risks of economic losses or possibilities of economic gains beyond what the nominal owner (the equity participant) could absorb or will be able to benefit from, respectively. If a party provides “subordinated financial support” to the entity that exposes it to absorbing the majority of the VIE's expected losses, or entitles it to receive the majority of the VIE's expected residual returns, or both, it is generally deemed to be the primary beneficiary of that VIE and will be required to consolidate the VIE as its subsidiary, irrespective of how much, if any, equity investment it has in the VIE.

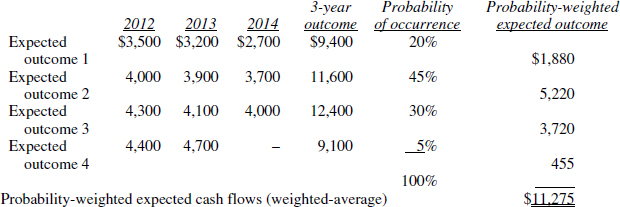

Expected variability. When estimating an entity's expected future cash flows in accordance with CON 7, Using Cash Flow Information and Present Value in Accounting Measurements, a range of probability-weighted expected outcomes is used. Mathematically, this is simply a weighted-average calculation. The following example illustrates the mathematical concept of expected variability:

Mided Mining Company is computing the probability-weighted expected future cash flows from operating and disposing of a tunnel boring machine that has a remaining estimated useful life of three years. This estimate was necessitated by ASC 360, which requires an evaluation, when certain events or circumstances occur, of whether the future cash flows associated with the use and disposal of long-lived assets are sufficient to recover their carrying value over their estimated remaining depreciable lives. Because of uncertainty regarding the amounts and timing of the cash flows, Mided's management used the CON 7 probability-weighted expected cash flow model with the following results:

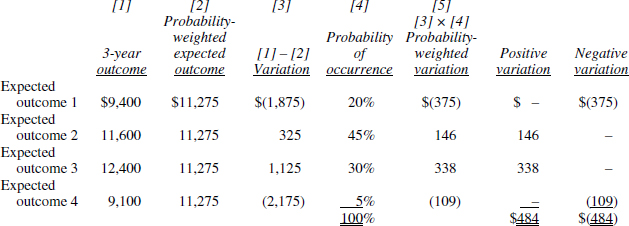

The $11,275 weighted-average, undiscounted, is compared to the carrying value of the tunnel boring machine to determine whether or not the carrying value is fully recoverable. The weighted-average consists of four different outcomes, each with its own estimated probability of occurrence. Since these amounts represent management's best estimates, management deems it possible that, at the end of the three-year period, any one of these outcomes could actually occur. When management considers the individual probability of occurrence for each of the four outcomes estimated above, the analysis yields the following results:

Careful examination of the above analysis yields the following conclusions:

- Variations naturally occur between expected outcomes and actual outcomes.

- Because the expected outcome is calculated as an average, some of the amounts used to compute it will be higher than the average and some will be lower than the average.

- When the individual variations are computed and each is multiplied by its probability of occurrence, the absolute value of the sum of the positive variations will exactly equal the absolute value of the sum of the negative variations.

- When these two absolute values are summed ($484 + $484 = $968 in the example above), the result, the total variability in both directions is called the expected variability of the cash flows.

- The higher the expected variability of a set of cash flow estimates, the higher the level of risk and uncertainty associated with the estimate.

The analysis of expected variability is based on the following two-step approach: (1) Determine the nature of an entity's risks, which shall at least include the areas of credit, interest rates, foreign currency exchange, commodity prices, equity prices, and operations, and then (2) determine the extent of the variability the entity was designed to pass through to its interest holders by reviewing its activities, contract terms, terms of issued interests, how those interests were negotiated, and the parties participating in the entity's design.

Expected losses and expected residual returns. Expected losses represent the expected negative variability in the fair value of an enterprise's net assets exclusive of variable interests. Expected residual returns represent the expected positive variability in the fair value of an enterprise's net assets exclusive of variable interests. The expected variability in an enterprise's net income or loss is included in the determination of its expected losses and expected residual returns.

Parents and subsidiaries. As discussed previously, the definitions of parent and subsidiary have been broadened to encompass variable interest entities and their primary beneficiaries. Thus, the primary beneficiary of a VIE is now referred to as its parent, and the VIE itself is considered a subsidiary of its primary beneficiary/parent.

Noncontrolling interests. A noncontrolling interest represents the portion of equity (or net assets) in a subsidiary (VIE) that is not directly or indirectly attributable to the parent (primary beneficiary). Thus parent companies of subsidiaries that are VIEs will be required to fully record the noncontrolling interest's share of VIE losses even if recording these losses results in a deficit in noncontrolling interest. ASC 810-10-45 settles the controversial issue of how the noncontrolling interest is classified in the consolidated statement of financial position by requiring that it be reported within the equity section, separately from the equity of the parent company, and clearly identified with a caption such as “noncontrolling interest in subsidiaries.” Should there be noncontrolling interests attributable to more than one consolidated subsidiary, the amounts may be aggregated in the consolidated statement of financial position.

Only equity-classified instruments issued by the subsidiary may be classified as equity in this manner. If, for example, the subsidiary had issued a financial instrument that, under applicable GAAP, was classified as a liability in the subsidiary's financial statements, that instrument would not be classified as a noncontrolling interest since it does not represent an ownership interest.

Initial determination of VIE status.

Whether or not an entity qualifies as a VIE is initially determined when an entity obtains its variable interest in that entity. This determination is based on the circumstances existing at that date, taking into account future changes that are required in existing governing documents and contractual arrangements. It is not necessary, however, for an interest holder to make this determination if both of the following conditions exist:

- It is apparent that the holder's interest would not be a significant variable interest, and

- The holder, its related parties, and its de facto agents (as specified later in this chapter in the section entitled “Related-party considerations in determining the primary beneficiary”) were not significant participants in the design or redesign of the entity.

Determination and redetermination of whether an interest holder is the primary beneficiary.

A holder of a variable interest initially determines whether it is the primary beneficiary of a VIE in conjunction with the initial determination that the entity is a VIE, that is, when the holder initially obtains its interest in the entity. This initial determination of whether an interest holder is the primary beneficiary (irrespective of whether the holder is or is not considered to be the primary beneficiary) needs to be reconsidered when the changes are made to the entity's governing documents or contractual arrangements that result in a reallocation of the obligation to absorb expected losses or the right to receive expected residual returns of the VIE between the existing primary beneficiary and other unrelated parties. A variable interest holder that had previously determined that it was the VIE's primary beneficiary is required to reconsider its initial decision to consolidate that VIE if (1) it sells or otherwise disposes of all or part of its variable interest to unrelated parties, or (2) if the VIE issues new variable interests to parties other than the primary beneficiary or the primary beneficiary's related parties.

If a variable interest holder had, upon obtaining its interest, determined that it was not the primary beneficiary of a VIE, it is to reconsider this determination it if obtains additional variable interests in the VIE.

Related-party considerations in determining the primary beneficiary.

Many SPE structures made use of related-party relationships, which did not, however, automatically necessitate consolidation (although disclosures were required under GAAP). For the purpose of a variable interest holder determining whether it is the primary beneficiary of a VIE, the definition of related parties is expanded from the definition set forth in ASC 850, Related-Party Disclosures, to include additional parties that act as “de facto agents” or “de facto principals” of the variable interest holder. The following table sets forth the related parties as prescribed by ASC 850 as well as additional related parties designated for this purpose in ASC 810-10-25-42 and 43:

| Related parties | De facto principals/agents |

|

|

These related-party attribution rules require consolidation of many of the currently popular SPE structures, unless the VIE is well capitalized and such subordinated support vehicles as loan guarantees are dispensed with.

If two or more related parties (including de facto principals/agents specified above) hold variable interests in the same VIE, and the aggregate variable interests held by those parties would, if held by a single party, identify that party as the primary beneficiary, then the member of the related-party group that is most closely associated with the VIE is the primary beneficiary that is required to consolidate the VIE as a subsidiary in its financial statements. In determining which party is most closely associated with the VIE, all relevant facts and circumstances are to be considered, including:

- Whether there is a principal/agent relationship between parties within the related-party group

- The relationship of the activities of the VIE to each of the parties in the related-party group

- The significance of the VIE's activities to each of the parties in the related-party group

- The extent of a party's exposure to the expected losses of the VIE

- The structure of the VIE.

Reconsideration of VIE status.

Once an initial determination is made as to whether an entity is a variable interest entity (as opposed to a voting interest entity), that initial determination need not be reconsidered unless one or more of the following circumstances occurs:

- A change is made to the VIE's governing documents or contractual arrangements that results in changes in either the characteristics or sufficiency of the at-risk equity investment in the VIE.

- As a result of a return of some or all of the equity investment to the equity investors, other interests become exposed to the VIE's expected losses.

- There is an increase in the VIE's expected losses that results from the entity engaging in activities or acquiring assets that were not anticipated at either the inception of the entity or a later reconsideration date.

- There is a decrease in the VIE's expected losses due to the entity modifying or curtailing its activities.

- Additional at-risk equity is invested in the VIE.

- The equity investors, as a group, lose the power to direct the activities of the VIE that most significantly impact its economic performance.

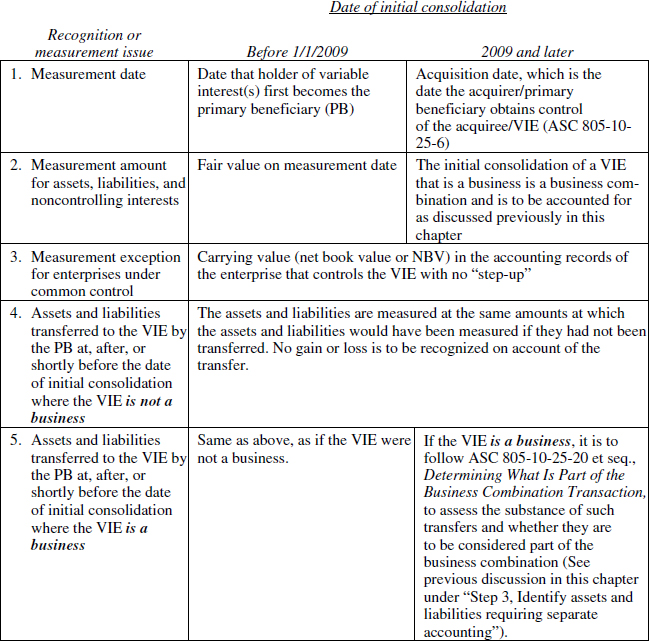

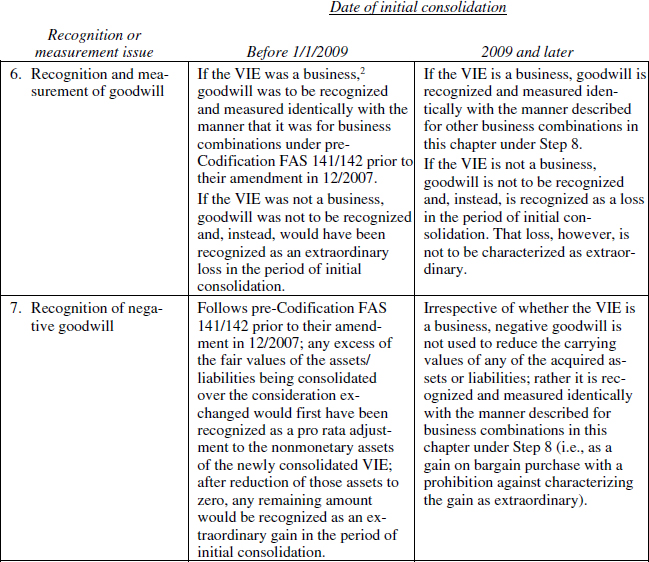

Initial measurement provisions. The initial measurement provisions of ASC 810 provide that:

- When the primary beneficiary of the VIE and the VIE are under common control, the primary beneficiary is to initially measure the assets, liabilities, and noncontrolling interests of the VIE at their carrying amounts in the accounting records of the entity that controls the VIE, or the amounts at which they would be carried by the controlling entity if that entity issued GAAP financial statements.

- When the primary beneficiary of the VIE and the VIE are not under common control:

- The initial consolidation of a VIE that is a business, discussed above, is a business combination transaction and, accordingly, is to be accounted for in accordance with the provisions of ASC 805.

- If an entity becomes the primary beneficiary of a VIE that is not a business:

- (1) The primary beneficiary is to initially measure and recognize the assets and liabilities of the VIE, except for goodwill, in accordance with ASC 805. However, any assets and liabilities transferred to the VIE by the primary beneficiary at, after, or shortly before the date the entity became the primary beneficiary are to be initially measured at the same amounts at which the assets and liabilities would have been measured if they had not been transferred. No gain or loss is to be recognized as a result of such transfers.

- (2) The primary beneficiary is to recognize a gain or loss for the difference between (a) the fair value of any consideration paid, the fair value of any noncontrolling interests, and the reported amount of any previously held interests and (b) the net amount of the VIE's identifiable assets and liabilities recognized and measured under the provisions of ASC 805. Goodwill is not to be recognized if the VIE is not a business.

Consolidation requirements.

An entity must consolidate a VIE of which it is the primary beneficiary. The variable interest holder that is the primary beneficiary of a VIE must have both 1) the power to direct those activities of the VIE most significantly impacting its economic performance, and 2) the obligation to absorb VIE losses that could potentially be significant to the VIE, or the right to receive benefits from the VIE that could potentially be significant to the VIE. Only one enterprise should be identified as the primary beneficiary, with the determining factor being the power to direct those activities of the VIE most significantly impacting its economic performance. It is possible that no primary beneficiary can be identified.

If there are other (noncontrolling) interests, these are shown in the consolidated balance sheet just as minority interests are under GAAP, and likewise a share of the operating results of the VIE are allocated to the noncontrolling interests in the consolidated statements of income (operations).

ASC 810-10-25-45 et seq. provides a 10% equity threshold test, which in practice is confusing and unworkable. The interpretation indicates that an at-risk equity investment of less than 10% of the entity's total assets is presumptively not considered sufficient to permit the entity to finance its activities without obtaining additional subordinated financial support but then goes on to provide that the presumption of insufficiency can be overcome by either quantitative analysis, qualitative analysis, or both. Consequently, financial statement preparers could mistakenly rely on the 10% presumption to conclude that an entity with less than 10% at-risk equity is a VIE, when in fact, further analysis would contradict that conclusion. Conversely, the interpretation indicates that it is also possible that an entity can require at-risk equity of more than 10% in order to sufficiently finance its activities. Consequently, the financial statement preparer also cannot rely on meeting or exceeding the 10% threshold as conclusive proof that the entity is sufficiently capitalized to avoid being characterized as a VIE.

The VIE provisions of ASC 810 greatly changed past practice. Previously, enterprises generally had been consolidated in financial statements because one enterprise controlled the other through a majority of voting interests. ASC 810-10-25 requires existing unconsolidated variable interest entities to be consolidated by their primary beneficiaries if the entities do not effectively disperse risks among the parties involved. Variable interest entities that effectively disperse risks will not be consolidated unless a single party holds an interest or combination of interests that effectively recombines risks that were previously dispersed.

Initial measurement with common control.

If the primary beneficiary of a VIE and the VIE itself are under common control, the primary beneficiary (parent) is to initially measure the assets, liabilities, and noncontrolling interests of the newly consolidated reporting entity at their preexisting carrying amounts.

Initial measurement absent common control.

The rules governing the initial measurement of the assets and liabilities of a newly consolidated VIE differ depending on the date on which the VIE is initially consolidated. These differing rules are attributable to amendments made in December 2007 to the original VIE rules to conform them more closely to the rules governing other business combinations. The following table compares the two sets of rules:

Accounting by a Primary Beneficiary (Parent)

for Initial Consolidation of a Variable Interest Entity

After initial measurement, the assets, liabilities, and noncontrolling interests of a consolidated variable interest entity will be accounted for as if the entity were consolidated based on majority voting interests.

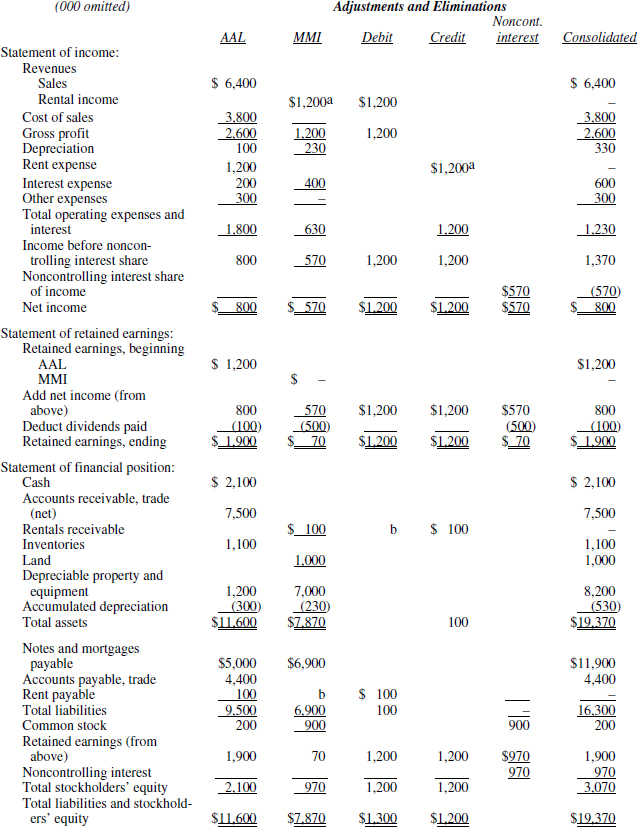

In practice, the most common situations requiring consolidation of a VIE will involve related-party leases. Consequently, this example uses a structured related-party lease to illustrate application of the consolidation provisions of ASC 810-10-30.

Arielle Aromatics Ltd. (AAL) is a manufacturer of aromatherapy products that is 100% owned by Arielle Stone. AAL's headquarters and manufacturing plant are leased pursuant to an operating lease with an S Corporation, Myles' Management, Inc. (MMI), owned by Arielle's brother, Myles.

AAL's headquarters building and the land on which it is built are the only assets owned by MMI. They have been pledged as collateral for a mortgage loan that is guaranteed by a corporate guarantee of AAL and a personal guarantee of Arielle.

MMI has been determined to be a variable interest entity (VIE) and AAL its primary beneficiary. The following is the consolidating worksheet at December 31, 2011:

Arielle Aromatics Ltd. and Subsidiary

Consolidating Worksheet

Year Ending December 31, 2011

The consolidating entries posted to the December 31, 2011 worksheet are as follows:

The consolidation process is relatively straightforward. The effects of the related-party lease, the rental income and expense and intercompany receivable and payable are eliminated so that, on a consolidated basis, the financial statements reflect the building, mortgage debt, depreciation, and interest expense.

The only difference between this consolidation of a VIE and a conventional consolidation of a voting interest entity in accordance with ASC 810-10-45 is the noncontrolling interest allocation. ASC 810-10-45-18 specifies that the elimination of intraentity profit or loss is not affected by the existence of a noncontrolling interest and that the elimination may be allocated between the parent (the controlling interest) and the noncontrolling interests.

In this example, however, the controlling interest holder, AAL, has no legal claim on the profit of MMI, since MMI's profit or loss is legally allocable to its equity owner. If this example had been a conventional consolidation of a voting interest entity, the effect of eliminating the rental income from MMI would be a remaining MMI loss of $630, computed as follows:

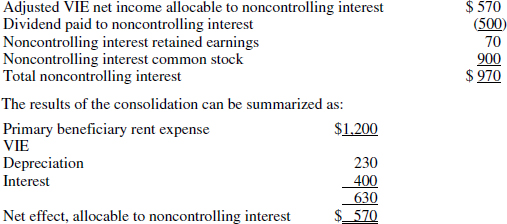

ASC 810-10-35-3 provides a special rule that the effect of eliminating fees or other sources of income or expense between the primary beneficiary and the consolidated VIE is to be attributed solely to the primary beneficiary and not to the noncontrolling interest computed as follows and illustrated above:

The net income allocation to the noncontrolling interest shown above is reduced by the dividends paid to the noncontrolling interest as follows:

Consolidated net income of $800 is the same as the primary beneficiary's net income since the entire $570 of VIE net income is allocated to the noncontrolling interest. The results, however, can have a profound effect on the way that the financial statements portray the leverage of the primary beneficiary to users, which might be the difference between AAL meeting or violating its loan covenants.

Certain practical matters require consideration in the case of consolidating VIEs.

- VIE without GAAP financial statements. Many VIEs structured as shown in this example had not previously prepared financial statements. Prior to consolidating the VIE with the primary beneficiary, the VIE's accounting records must be adjusted to eliminate any differences between GAAP and the basis on which the VIE reports for income tax purposes.

- Lack of prior independent CPA involvement with VIE. VIEs that had not been subject to financial reporting in the past obviously had not needed to engage an independent CPA to perform a compilation, review, or audit engagement. Upon consolidation, the consolidated financial statements, including the VIE's (subsidiary's) financial position and results of operations, will be subject to the same level of service as the financial statements of the primary beneficiary (parent).

- Interaction with ASC 460-10. ASC 460-10, Guarantor's Accounting and Disclosure Requirements for Guarantees, Including Indirect Guarantees of Indebtedness of Others, requires guarantors to recognize a liability at inception for the obligations embodied in the guarantee. In the example above, the guarantee of the VIE's mortgage by the primary beneficiary would be exempt from the initial recognition and measurement provision of ASC 460-10 because the guarantee is analogous to a parent guarantee of its subsidiary's debt to a third party, which is specifically exempted from the recognition and measurement provisions of ASC 460-10. However, the guarantee is not exempt from the disclosure requirements of ASC 460-10 and ASC 450-10.

- General-purpose financial statements. In the example, AAL is the “parent” company. It would be precluded by ASC 810-10-45-11 from issuing separate, general-purpose financial statements that exclude MMI, since this would be a GAAP departure; however, nothing precludes MMI from issuing separate subsidiary-only financial statements.

Implicit variable interests. One of the most misunderstood aspects of this area of the literature is referred to as an implicit variable interest. The FASB staff attempted to clarify this matter in FSP FIN 46(R)-5, codified as ASC 810-10-25-48 through 54 and ASC 810-10-55-88 through 89.

A party that did not explicitly issue a direct guarantee of another party's obligation can, nevertheless, be held to be an implicit guarantor of that obligation and thus, hold a variable interest in the party whose debt is implicitly guaranteed.

Consider the situation where the principal shareholder of a company personally guarantees a mortgage on the premises that the company occupies and leases from a related LLC whose sole member is the lessee's principal shareholder. Normally, the rent payments due under the related-party lease are structured to provide sufficient cash flow to the lessor to enable it to meet its debt service obligations under the mortgage. If the lessee were to become delinquent under its rent obligations to the lessor, the lessor would not have sufficient cash flow to enable it to make the payments due under its mortgage, which would cause a loan delinquency or default.

Should this occur, the following scenarios could occur:

- The lender could repossess the property and sell it to pay off the loan.

- The lender could enforce the guarantee and compel the shareholder to pay off the loan on behalf of the lessor or, at least to make the delinquent payments on behalf of the lessor to cure the default, or

- The lessee could sell off assets or borrow money from its stockholder or a third party to enable it to pay its delinquent rent, thereby enabling the lessor to make its delinquent mortgage payments.

Scenario 1 would not be a desirable outcome, as the lessor would lose title to its property and the lessee, in default on its rent, could end up without the premises in which it operates its business since, upon sale of the property, the successor owner would potentially terminate the lease for nonpayment.

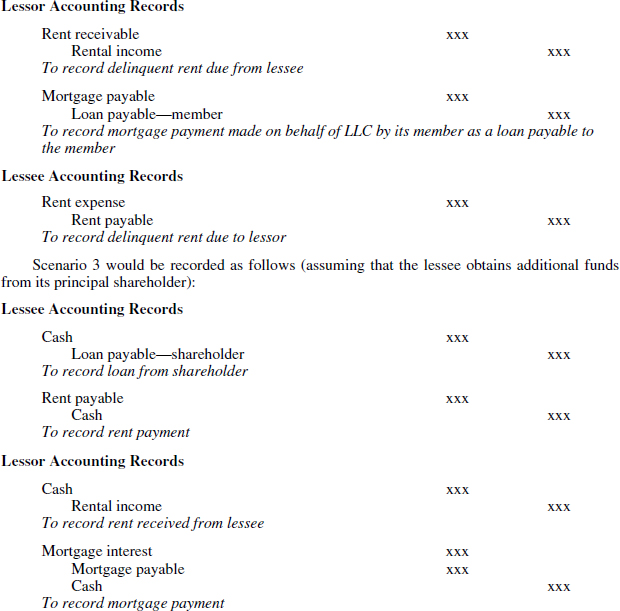

Under scenario 2 if the shareholder were to pay the delinquent mortgage payment on behalf of the lessor, the transactions would be recorded as follows:

The outcomes of scenarios 2 and 3 are very similar. Under scenario 2, the shareholder/member will have a loan receivable from the thinly capitalized LLC that depends solely on the delinquent corporation for its cash flow. In scenario 2, the lessee will have to raise cash in an amount sufficient to fund the LLC's repayment of its loan to the shareholder/member and keep the mortgage current. Since the LLC is dependent upon the lessee for its cash flow, the lessee has implicitly incurred an obligation to fund the LLC's loan repayment to the shareholder/member. It is, of course, in the best interest of the lessee to fund this, since it entitles the lessee to continue to benefit from the use of the leased property and, contractually, the lessee is already obligated to pay the delinquent rent.

Under scenario 3, the shareholder/member will have a loan receivable from a lessee that is experiencing difficulty in meeting its rent obligations. The lessee will have substituted a presumably interest-bearing loan payable to its shareholder for a noninterest-bearing rent payable obligation to the LLC and will, as in scenario 2, be obligated to raise cash sufficient to repay its shareholder and fund its rent obligations under the lease. In effect, the lessee will have used its available credit that it could have used for other operating purposes to help provide financial support to the LLC that would otherwise have insufficient capital to be self-sustaining. Again, implicitly, the lessee is functioning as a guarantor of the LLC's mortgage indebtedness by its willingness to provide the cash flow necessary for the LLC to meet its obligations.

Based on the foregoing analysis, in substance the lessee is the holder of an implicit variable interest in the lessor in the form of an implicit guarantee of the lessor's mortgage debt. Due to the fact that the implicit guarantee exposes the lessee/variable interest holder to the expected losses of the lessor, the lessor/LLC's sole member (and at-risk equity holder) is not the only party that potentially would absorb expected losses of the lessor.

Variable interests in “silos.”

A party may hold a variable interest in specific assets of a VIE (e.g., a guarantee or a subordinated residual interest). In computing expected losses and expected residual returns, a holder of a variable interest in specified assets of a VIE must determine if the interest it holds qualifies as an interest in the VIE itself. The variable interest is considered an interest in the VIE itself if either (1) the fair value of the specific assets is more than half of the total fair value of the VIE's assets or (2) the interest holder has another significant variable interest in the entity as a whole.

If the interests are deemed to be interests in the VIE itself, the expected losses and expected residual returns associated with the variable interest in the specified assets are treated as being associated with the VIE.

If the interests are not deemed to be interests in the VIE itself, the interests in the specified assets are treated as a separate VIE (referred to as a silo) if the expected cash flows from the specified assets (and any associated credit enhancements, if applicable) are essentially the sole source of payment for specified liabilities or specified other interests. Under this scenario, expected losses and expected residual returns associated with the silo assets are accounted for separately to the extent that the interest holder either absorbs the VIE's expected losses or is entitled to receive its expected residual returns. Any excess of expected losses or expected residual returns not borne by (received by) the variable interest holder is considered attributable to the entity as a whole.

If one interest holder is required to consolidate a silo of a VIE, other VIE interest holders are to exclude the silo from the remaining VIE.

Synthetic leases.

One of the more common SPE situations under prior GAAP is that of a synthetic lease. A synthetic lease is a financing transaction whereby an independent third-party lessor (i.e., unrelated to the lessee) constructs or acquires an existing single-tenant property and leases it to a lessee. The synthetic lease transaction is generally structured with a short lease term so that the lessee accounts for it as an operating lease under GAAP, not-withstanding the fact that, for federal income tax purposes, it is treated as a “financing,” which results in the lessee/taxpayer capitalizing the leased asset and deducting depreciation and interest.

When these arrangements were originally devised, prior to the establishment of consolidation rules for VIEs, they resulted in the lessee excluding the leased asset and related debt from its balance sheet. It also enabled creditworthy lessees to finance as much as 100% of the cost of the leased property, thus avoiding tying up precious working capital in a down-payment.

The lessee commits to a fixed schedule of rental payments, say for five years, so over that time there will only be a single amount of annual cash flows paid each year. The lease terms provide a purchase option to the lessee that can be exercised at any time during the lease term or upon the lease's expiration. Under the option, the lessee would pay the lessor a stipulated amount normally representing the lessor's original investment in the leased property augmented by a fixed rate of return. Thus, the lessor, to ensure it earns an acceptable return to its investors, is willing to sacrifice any appreciation of the property that exceeds the purchase price.

The lease will typically also provide, however, that if the fair value of the asset at lease expiration is less than the stipulated amount of the initial investment augmented by the agreed-upon fixed rate of return, the lessee agrees to pay the lessor for any shortfall.

In analyzing these two lease provisions, each represents a transfer of variability from one party to the other:

| Lessee purchase option that enables the lessee to benefit (obtain the expected residual rewards) from excess appreciation of the leased property | This option is a variable interest that entitles its holder, the lessee, to a portion of expected residual rewards associated with the leased asset that the lessor would otherwise be entitled to. Thus it transfers from lessor to lessee a portion of the favorable variability associated with the leased asset. |

| Lessee residual value guarantee | This guarantee is a variable interest that obligates its holder, the lessee, to absorb a stipulated portion of any unfavorable variability associated with the leased asset that would otherwise be absorbed by the lessor upon its disposition of the leased property. |

A synthetic lease is structured with a five-year term and an annual “rental” due at the end of each of those years of $50,000. The average (expected) cash flow each of those years will be that contractual amount. The fair value of the annual cash flow in any year will be the amount defined under CON 7, which is essentially the discounted present value of the annual lease payment.

Assume 6% is the relevant discount rate, and rents are paid annually in arrears. The fair value of the first year's rent is then $50,000 ÷ 1.06 = $47,170; the corresponding amount for year two's rent is $50,000 ÷ 1.062 = $44,500; and so on. Since this amount is fixed, there are no expected residual rewards or expected losses from the rental stream in each of the years one through five.

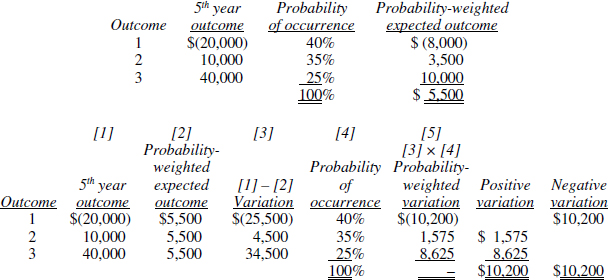

It is estimated that at the lease expiration date there may be a range of fair values for the asset. Also, the lessor is entitled to a cumulative return on its investment in the leased property. It is now necessary to compute, separately, the expected (i.e., probability-weighted) discounted fair values of the shortfall amount and the excess value amount. For simplicity, assume only three discrete outcomes are estimated to be possible:

- The asset is sold for an amount that falls short of the book value plus the promised rate of return, for a net shortfall of $20,000;

- The asset is sold for a net gain, after guaranteed return to the lessor, of $10,000; or

- The asset is sold for a net gain of $40,000.

These outcomes are summarized as follows:

Note that the expected loss equals the expected residual returns, as would always be the case, since the arithmetic average (mean) was used to compute the deviations of each projected outcome. Since the expected loss based on expected cash flow will be borne by the lessee if it occurs, and the expected residual return based on expected cash flows will benefit the lessee if one or the other occurs, the lessee is the primary beneficiary/parent of the VIE.

The actual computation would be based on the fair value of the expected cash flows. In this case, the expected fair value of the loss is given as $−10,200 ÷ (1.06)5 = $−7,622. The expected fair value of the expected residual rewards would correspondingly be $7,622.

The total expected variability of the lease arrangement is therefore $15,244 (all earlier years' rental streams had zero variability), and the lessee absorbs all of this.

Note that in real-life situations there may be many other complications, such as rentals based on variables such as sales of product and the like. In addition, many of these arrangements permit the lessee to exercise its purchase option at any time during the lease term rather than limiting exercise to the end of the lease term.

In such a situation, with a wider range of the amounts and timing of possible cash flows each period, the computations will be more challenging. Also, in some situations the VIE will have a range of assets and multiple parties with whom it is in contractual arrangements, which is a complication addressed somewhat by the standard, but which requires more analysis. However, it might be possible in many cases to immediately conclude qualitatively, based on analysis of the risks, rewards, and relationships, that the VIE is indeed to be consolidated, in which case these calculations will be unnecessary. The very existence of the purchase option and residual value guarantees provide qualitative evidence that, by design, the lessor is a VIE and the lessee is its primary beneficiary.

Changing or eliminating differences in fiscal year-end.

ASC 810-10-45 and ASC 810-10-50 state that the following scenarios constitute voluntary changes in accounting principle that are subject to the accounting and disclosure rules in ASC 250:

- A consolidated entity changes its fiscal year-end to alter or eliminate a difference between its year-end and the fiscal year-end of the entity that consolidates it in its financial statements (the parent or ASC 810 primary beneficiary).

- An investee that is accounted for by an investor using the equity method changes its fiscal year-end to alter or eliminate a difference between its year-end and the fiscal year-end of the equity method investor.

Retrospective application is not required if it is impracticable to do so. (See chapter in this volume on ASC 250.)

Partnerships and Similar Entities

General Partnerships.

Partners holding lesser interests may possess substantive participating rights (as that term is used in ASC 810-20-25-5) granted by a contract, lease, agreement with other partners, or court decree. When the other partners have such rights, the presumption of control by the general partner with the majority voting interest or majority financial interest is overcome. Under those circumstances, the controlling general partner would consolidate the partnership and the noncontrolling general partner would consolidate the partnership and the noncontrolling general partners would use the equity method (ASC 970-323; ASC 810-20-25-19).

Limited partnerships.

The structure of many limited partnerships consists of one investor serving as general partner and having only a small equity interest and the other investors holding limited partnership (or equivalent) interests. The proper accounting for such structures is ASC 970-323, Real Estate Investments—Equity Method and Joint Ventures, which formally deals only with certain real estate investments but has been applied by analogy to other investments. ASC 810-10-25 provides expanded guidance to the appropriate accounting in those circumstances where the majority owner lacks control due to the existence of “substantial participating rights” by minority owners.

If the investor/holder is an entity that is required under GAAP to measure its investment in the limited partnership (LP) at fair value with changes in fair value reported in the income statement, then it follows that applicable specialized guidance with respect to accounting for its investment.

If the investee entity is a variable interest entity (VIE) under the provisions of ASC 810, the holders of interests in the entity are to use the GAAP applicable to those interests. If the investor has a controlling financial interest in the VIE, the investor is deemed to be the entity's primary beneficiary (analogous to a parent company) and is required to consolidate the investee in its financial statements.

Noncontrolling interest holders in an LP that is a VIE are to account for their interests using the equity method or the cost method. Limited partner interests that are so minor that the limited partner has virtually no influence over operating and financial policies of the partnership would be accounted for using the cost method (ASC 970-323). To be considered to be this minor, the SEC staff has indicated that an interest would not be permitted to exceed 3–5% (ASC 323-30-S99). In practice, this benchmark is also generally accepted for non-SEC registrants, since it represents the most authoritative guidance currently available with respect to making this determination.

If the LP is not a VIE and the partners are not subject to specialized industry fair value accounting rules, a determination is made as to whether a single general partner or multiple general partners control the LP. If a single general partner controls the LP, that partner is to consolidate the LP, all other general partners are to apply the equity method of accounting to their investments, and the limited partners will use either the cost method (for minor investments) or the equity method, as previously discussed.

If more than one general partner controls the partnership, ASC 810-20 provides the framework for analyzing the respective legal and contractual rights and privileges associated with each owner/investor's interests to determine control. For the purpose of applying ASC 810-20, entities under common control are considered to be a single general partner. No guidance is offered, however, in ASC 810-20 as to how to determine which of several general partners is to consolidate the partnership.

ASC 810-20 integrates certain concepts from ASC 810 into what had been only fragmentary guidance. ASC 810 introduced the concept of “kick-out rights” which, when held by limited partners, gave them the right to eject the general partner(s) of the partnership, thereby (often) preventing the general partner(s) from exercising control. ASC 810-20 holds that there is a refutable presumption that general partners in a partnership have control, regardless of their actual ownership percentage, which can be overcome if the limited partners have certain defined abilities.

If the limited partners have the substantive ability to dissolve (liquidate) the limited partnership or otherwise remove the general partners without cause—which is referred to as “kick-out rights”—then the general partners will be deemed to lack control over the partnership. In such cases, consolidated financial reporting would not be appropriate, but equity method accounting would almost inevitably be warranted. To qualify, the kick-out rights must be exercisable by a single limited partner or a simple majority (or fewer) of limited partners. Thus, if a super-majority of limited partner votes is required to remove the general partner(s), this would not constitute a substantive ability to dissolve the partnership and would not thwart control by the general partner(s).

There is a range of possible qualifying requirements to exercise kick-out rights that could lead to the conclusion that nominal kick-out rights are ineffective in precluding the general partner(s) from exercising control. ASC 810-20 offers a series of illustrative examples to help the preparer interpret this guidance, and should be consulted to benchmark any real-world set of circumstances. Examples of barriers to the exercise of kick-out rights include:

- Conditions that make it unlikely the rights will be exercisable (e.g., conditions that narrowly limit the timing of the exercise)

- Financial penalties or operational barriers associated with dissolving (liquidating) the limited partnership or replacing the general partners that would act as a significant disincentive for dissolution (liquidation) or removal

- The absence of an adequate number of qualified replacements for the general partners or the lack of adequate compensation to attract a qualified replacement

- The absence of an explicit, reasonable mechanism in the limited partnership agreement or in the applicable laws or regulations, by which the limited partners holding the rights can call for and conduct a vote to exercise those rights

- The inability of the limited partners holding the rights to obtain the information necessary to exercise them.

A limited partner's unilateral right to withdraw is pointedly not equivalent to a kick-out right. However, if the partnership is contractually or statutorily bound to dissolve upon the withdrawal of one partner, that would equate to a kick-out right.

ASC 810-20 also addresses “participating rights” held by the limited partners, which it contrasts to “protective rights” as these were first defined in ASC 810. Limited partners' rights (whether granted by contract or by law) that would allow the limited partners to block selected limited partnership actions would be considered protective rights and would not overcome the presumption of control by the general partners(s). Among the actions cited by ASC 810-20 as illustrating protective (not participating) rights are:

- Amendments to the limited partnership agreement

- Pricing on transactions between the general partners and the limited partnership and related self-dealing transactions

- Liquidation of the limited partnership initiated by the general partners or a decision to cause the limited partnership to enter bankruptcy or other receivership

- Acquisitions and dispositions of assets that are not expected to be undertaken in the ordinary course of business (Note that limited partners' rights relating to acquisitions and dispositions expected to be made in the ordinary course of the limited partnership's business are participating rights.)

- Issuance or repurchase of limited partnership interests.

The presence of protective rights would not serve to overcome the presumption of control by the general partner(s). Substantive participating rights, on the other hand, do overcome the presumption of general partner control. Such rights could include:

- Selecting, terminating, and setting the compensation of management responsible for implementing the limited partnership's policies and procedures

- Establishing operating and capital decisions of the limited partnership, including budgets, in the ordinary course of business.

ASC 810-20 states that determination of whether the presumption of general partner control is overcome is a “facts and circumstances” assessment to be made in each unique situation. For example, depending on which decisions are required to be put to a full vote of the partnership (as opposed to being reserved for the general partner), the limited partners may be found to have substantive participating rights. Another important factor weighing on this determination: the relationships among limited and general partners (using ASC 850 related-party criteria).

The assessment of the extent of limited partners' rights and the impact those have on the presumption of general partner(s) control over the partnership (for consolidated financial reporting purposes) is to be made upon initial acquisition of the general partner's interest or formation of the partnership, and again at each financial reporting (i.e., statement of financial position) date.

Limited partnerships controlled by the general partners. As previously stated, the general partners are collectively presumed to be in control of the limited partnership and, if this is substantively the case, the accounting for the general partners depends on whether control of the entity rests with a single general partner. If a single general partner controls the limited partnership, that general partner consolidates the limited partnership in its financial statements. If no single general partner controls the limited partnership, each general partner applies the equity method to account for its interest (ASC 810-20).

Noncontrolling limited partners are to account for their interests using the equity method or by the cost method. As previously discussed, limited partner interests that are so minor (not to exceed 3–5%) that the limited partner has virtually no influence over operating and financial policies of the partnership would be accounted for using the cost method (ASC 970-323).