12 ASC 270 INTERIM REPORTING

Integral/Discrete Pros and Cons

Differentiation between Public and Nonpublic Companies

Part I—Requirements Applicable to All Reporting Entities

Product Costs and Direct Costs

Example of interim reporting of product costs

Example of interim reporting of other expenses

Fair Value of Financial Instruments

Discontinued Operations and Extraordinary Items

Example of discontinued operations and extraordinary items

Example of interim reporting of contingencies

Change in accounting principle

Part II—Requirements Applicable to Public Reporting Entities

Quarterly Reporting to the SEC

Summarized interim financial data

Changes in accounting principle

Accelerated reporting requirements

PERSPECTIVE AND ISSUES

Subtopic

ASC 270, Interim Reporting, contains one subtopic:

- ASC 270-10, Overall, that provides guidance on

- Accounting and disclosure issues for reporting on periods less than one year and

- Minimum disclosure requirements for interim reporting for publicly traded companies.

Overview

The term “interim reporting” refers to financial reporting for periods of less than a year. GAAP does not mandate interim reporting. However, in the United States the Securities and Exchange Commission (SEC) requires public companies to file quarterly summarized interim financial data on its Form 10-Q. The level of detail of the information required in those interim reports is substantially less than is specified under GAAP for annual financial statements.

Objective.

The objective of interim reporting is to provide current information regarding enterprise performance to existing and prospective investors, lenders, and other financial statement users. This enables users to act upon relevant information in making informed decisions in a timely manner. SEC filings on Form 10-Q are due in no greater than 45 days after period end. Filings on Form 10-K are due, depending on entity size, from 75 to 90 days after year-end. The demand for timely information means that interim data will often be more heavily impacted by estimates and assumptions.

Integral Approach.

Historically, there have been two competing views of interim reporting. Under the integral view, the interim period is considered an integral part of the annual accounting period. It thus follows that annual operating expenses are to be estimated and allocated to the interim periods based on forecasted annual activity levels such as sales volume. The results of subsequent interim periods are adjusted to reflect the effect of estimation errors in earlier interim periods of the same fiscal year. ASC 270-10-45-1 prefers the integral view.

Discrete Approach.

Under the discrete view, each interim period is considered a discrete accounting period. Thus, estimations and allocations are made using the same methods used for annual reporting. It follows that the same expense recognition rules apply as under annual reporting, and no special interim accruals or deferrals would be necessary or permissible. Annual operating expenses are recognized in the interim period incurred, irrespective of the number of interim periods benefited (i.e., no special deferral rules would apply to interim periods).

Integral/Discrete Pros and Cons.

Proponents of the integral view argue that unique interim expense recognition procedures are necessary to avoid fluctuations in period-to-period results that might be misleading to financial statement users. Applying the integral view results in interim earnings which are indicative of annual earnings and, thus, arguably more useful for predictive purposes. Proponents of the discrete view argue that the smoothing of interim results for purposes of forecasting annual earnings has undesirable effects. For example, a turning point during the year in an earnings trend could be obscured if smoothing techniques implied by the integral view were to be employed.

The debate between integral and discrete views of interim reporting can result in very different interim measures of results of operations. This can occur, for example, because certain annual expenses may be concentrated in one interim period, yet benefit the entire year's operations. Examples include advertising expenses and major repairs and maintenance of equipment. Also, in the United States (and many other jurisdictions) progressive (graduated) income tax rates are applied to total annual income and various income tax credits may arise, all of which are computed on annual pretax earnings, often adding complexity to the determination of quarterly income tax expense.

Other Issues.

Interim reporting is problematic for reasons other than the choice of an underlying measurement philosophy. As reporting periods are shortened, the effects of errors in estimation and allocation are magnified, and randomly occurring events which might not be material in the context of a full fiscal year could create major distortions in short interim period summaries of reporting entity performance. The effects of seasonal fluctuations and temporary market conditions further limit the reliability, comparability, and predictive value of interim reports.

Technical Alert

ASU 2013-03. In February 2013, the FASB issued ASU 2013-03, Clarifying the Scope and Applicability of a Particular Disclosure to Nonpublic Entities. In its meetings related to ASU 2011-04, the Board had decided that nonpublic entities would not be required to disclose “the level in which a fair value measurement would be categorized within the fair value hierarchy for assets and liabilities not recognized at fair value but for which disclosure of fair value is required” After issuance of ASU 2011-04, some constituents noticed an inconsistency between what the Board intended and the actual changes to the codification. With ASU 2013-03, the board clarified that it did exempt nonpublic entities of any size from that disclosure in annual and interim financial statements.

DEFINITIONS OF TERMS

Source: ASC 270-10-20

Acquiree. The business or businesses that the acquirer obtains control of in a business combination. This term also includes a nonprofit activity or business that a not-for-profit acquirer obtains control of in an acquisition by a not-for-profit entity.

Acquirer. The entity that obtains control of the acquiree. However, in a business combination in which a variable interest entity (VIE) is acquired, the primary beneficiary of that entity always is the acquirer.

Acquisition by a Not-for-Profit Entity. A transaction or other event in which a not-for-profit acquirer obtains control of one or more nonprofit activities or businesses and initially recognizes their assets and liabilities in the acquirer's financial statements. When applicable guidance in Topic 805 is applied by a not-for-profit entity, the term business combination has the same meaning as this term has for a not-for-profit entity. Likewise, a reference to business combinations in guidance that links to Topic 805 has the same meaning as a reference to acquisitions by not-for-profit entities.

Business. An integrated set of activities and assets that is capable of being conducted and managed for the purpose of providing a return in the form of dividends, lower costs, or other economic benefits directly to investors or other owners, members, or participants. Additional guidance on what a business consists of is presented in paragraphs 805-10-55-4 through 55-9.

Business Combination. A transaction or other event in which an acquirer obtains control of one or more businesses. Transactions sometimes referred to as true mergers or mergers of equals also are business combinations. See also Acquisition by a Not-for-Profit Entity.

Financing Receivable. A financing arrangement that has both of the following characteristics:

- It represents a contractual right to receive money in either of the following ways:

- On demand

- On fixed or determinable dates.

- It is recognized as an asset in the entity's statement of financial position.

See paragraphs 310-10-55-13 through 55-15 for more information on the definition of financing receivable, including a list of items that are excluded from the definition (for example, debt securities).

Legal Entity. Any legal structure used to conduct activities or to hold assets. Some examples of such structures are corporations, partnerships, limited liability companies, grantor trusts, and other trusts.

Not-for-Profit Entity. An entity that possesses the following characteristics, in varying degrees, that distinguish it from a business entity:

- Contributions of significant amounts of resources from resource providers who do not expect commensurate or proportionate pecuniary return

- Operating purposes other than to provide goods or services at a profit

- Absence of ownership interests like those of business entities.

Entities that clearly fall outside this definition include the following:

- All investor-owned entities

- Entities that provide dividends, lower costs, or other economic benefits directly and proportionately to their owners, members, or participants, such as mutual insurance entities, credit unions, farm and rural electric cooperatives, and employee benefit plans.

Publicly Traded Company. A publicly traded company includes any company whose securities trade in a public market on either of the following:

- A stock exchange (domestic or foreign)

- In the over-the-counter market (including securities quoted only locally or regionally), or any company that is a conduit bond obligor for conduit debt securities that are traded in a public market (a domestic or foreign stock exchange or an over-the-counter market, including local or regional markets).

Additionally, when a company is required to file or furnish financial statements with the SEC or makes a filing with a regulatory agency in preparation for sale of its securities in a public market it is considered a publicly traded company for this purpose.

Conduit debt securities refers to certain limited-obligation revenue bonds, certificates of participation, or similar debt instruments issued by a state or local governmental entity for the express purpose of providing financing for a specific third party (the conduit bond obligor) that is not a part of the state or local government's financial reporting entity. Although conduit debt securities bear the name of the governmental entity that issues them, the governmental entity often has no obligation for such debt beyond the resources provided by a lease or loan agreement with the third party on whose behalf the securities are issued. Further, the conduit bond obligor is responsible for any future financial reporting requirements.

Variable Interest Entity. A legal entity subject to consolidation according to the provisions of the Variable Interest Entities Subsections of Subtopic 810-10.

CONCEPTS, RULES, AND EXAMPLES

Differentiation between Public and Nonpublic Companies

The explanations and interpretations in this chapter have been divided into two sections. Part I discusses issues applicable to both public and nonpublic reporting entities (including, where applicable, not-for-profit organizations). Part II discusses issues applicable only to publicly traded companies.

The usefulness of interim reports rests on the relationship to annual reports. Therefore, ASC 270-10-45-1 states that “each interim period should be viewed primarily as an integral part of an annual period,” and the accounting should be based on the principles and practices used in the entity's annual reporting. The exception to this is if the entity has adopted a change in accounting in the interim period. Certain principles and practices may also have to be modified so that the interim reporting better relates to the annual results. The modifications are detailed in ASC 270-10-45-4 through 45-11 and are detailed in the sections below.

PART I—REQUIREMENTS APPLICABLE TO ALL REPORTING ENTITIES

Revenues

Revenues are recognized as earned during an interim period using the same principles followed in annual reports (ASC 270-10-45-3). This rule applies to both product sales and service revenues. For example, product sales cutoff procedures are applied at the end of each interim period in the same manner that they are applied at year-end, and revenue from long-term construction contracts is recognized at interim dates using the same method used at year-end.

Product Costs and Direct Costs

Product costs and costs directly associated with service revenues are treated in interim reports in the same manner as in annual reports. ASC 270-1-45 provides for four integral view exceptions:

- The gross profit method may be used to estimate cost of goods sold and ending inventory for interim periods.

- When inventory consists of LIFO layers, and a portion of the base period layer is liquidated at an interim date, and it is expected that this inventory will be replaced by year-end, the anticipated cost of replacing the liquidated inventory is included in cost of sales of the interim period.

- An inventory market decline reasonably expected to reverse by year-end (i.e., a decline deemed to be temporary in nature) need not be recognized in the interim period. ASC 330-10-55 states that there must be substantial evidence available to support the contention that the market value will recover before the inventory is sold, which generally limits this interim exception to seasonal price fluctuations. If an inventory loss from a market decline that is recognized in one period is followed by a market price recovery, the reversal is recognized as a gain in the subsequent interim period. Recognition of this gain in the later interim period is limited to the extent of loss previously recognized. This is in marked contrast to lower of cost or market write-downs in annual financial statements, which are not permitted to be restored in a later period.

- Entities using standard cost accounting systems ordinarily report purchase price, wage rate, and usage or efficiency variances in the same manner as year-end. Planned purchase price and volume variances are deferred if expected to be absorbed by year-end.

The first exception above eliminates the need for a physical inventory count at the interim date. The other three exceptions attempt to synchronize the quarterly financial statements with the annual report. For example, consider the LIFO liquidation exception. Without this exception, interim cost of goods sold could include low earlier year or base-period costs, while annual cost of goods sold would include only current year costs.

Several questions arise when using LIFO for interim reporting.

- What is the best approach to estimate interim LIFO cost of sales?

- As noted above, when an interim liquidation occurs that is expected to be replaced by year-end, cost of sales includes the expected cost of replacement. How is this adjustment treated on the interim statement of financial position?

- How is an interim liquidation that is not expected to be replaced by year-end recorded?

These problems are not addressed in ASC 270. The only literature related to these problems is a 1984 American Institute of Certified Public Accounts (AICPA) Task Force LIFO Issues Paper.1

The Issues Paper describes two acceptable approaches to measuring interim LIFO cost of sales. The first approach makes specific quarterly computations of the effect of using LIFO based on year-to-date amounts. This is accomplished by reviewing quarterly price level changes and inventory levels. The second approach projects the expected annual effect of using LIFO and then allocates the results of that projection to the individual quarters. The allocation can be made equally to each quarter or can be made in relation to certain operating criteria per quarter.

The Issues Paper also describes two acceptable approaches to treating the interim liquidation replacement on the statement of financial position. The first approach is to record the adjustment for the effect on pretax income of the replacement as a deferred credit in the current liabilities section. The second approach is to record the adjustment as a credit to an inventory valuation allowance.

When an interim LIFO liquidation occurs that is not expected to be reinstated by year-end, the effect of the liquidation is recognized in the period in which it occurs to the extent that it can be reasonably determined. A reporting entity using dollar-value LIFO may allocate the expected effect of the liquidation to the quarters affected.

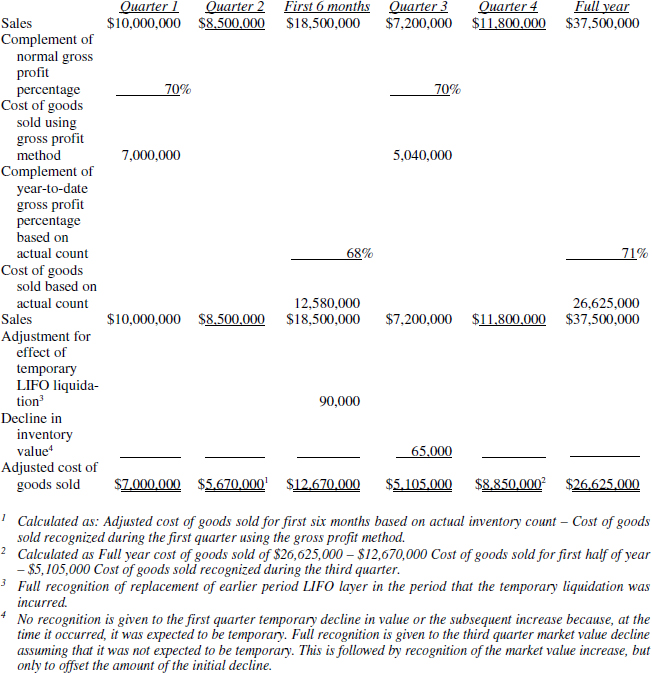

Dakota Corporation encounters the following product cost situations as part of its quarterly reporting:

- It takes physical inventory counts at the end of the second quarter and end of the fiscal year. Its typical gross profit is 30% of sales. The actual gross profit applicable to the first six months of the year is 32%. The actual full-year gross profit is 29%.

- It carries one type of its inventory at LIFO and the remaining inventory at first-in, first-out (FIFO).

- It suffers a clearly temporary decline of $10,000 in the market value of a specific part of its FIFO inventory in the first quarter, which it recovers in the second quarter.

- It liquidates earlier-period, lower-cost LIFO inventories during the second quarter. The liquidation results in second quarter cost of goods sold being $90,000 less (and, of course, second quarter gross profit being $90,000 more) than it would have been absent the LIFO liquidation. Dakota expects to, and does, restore these inventory levels by year-end.

- It suffers a decline of $65,000 in the market value of its FIFO inventory during the third quarter. The inventory value increases by $75,000 in the fourth quarter.

Dakota computes interim cost of goods sold to reflect the effect of these situations as follows:

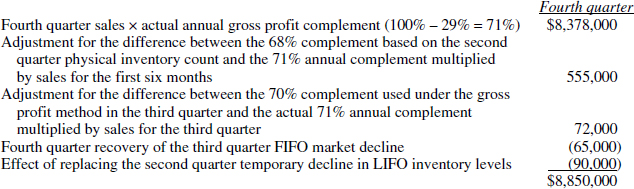

To illustrate that the fourth quarter is appropriately adjusted for the effects of applying the interim costing rules to the other quarters, the fourth quarter cost of goods sold is proved as follows:

Other Costs and Expenses

The integral view is evident in how current US GAAP treats costs incurred in interim periods. Most costs and expenses are recognized in interim periods as incurred. However, a cost that clearly benefits more than one interim period (e.g., annual repairs or property taxes) is allocated among the periods benefited (ASC 270-10-45-8). The allocation is based on

- Estimates of time expired,

- Benefit received, or

- Activity related to the specific periods.

Allocation procedures are to be consistent with those used at year-end reporting dates. However, if a cost incurred during an interim period cannot be readily associated with other interim periods, it is not arbitrarily assigned to those periods. The following parameters (ASC 270-45-10-9) are used in interim periods to account for certain types of expenses incurred in those periods:

- Costs that benefit two or more interim periods (e.g., annual major repairs) are assigned to interim periods through the use of deferrals or accruals.

- Quantity discounts given to customers based on annual sales volume are allocated to interim periods on the basis of sales to customers during the interim period relative to estimated annual sales.

- Property taxes (and like costs) are deferred or accrued at a year-end date to reflect a full year's charge to operations. Charges to interim periods follow similar procedures.

- Advertising costs are permitted to be deferred to subsequent interim periods within the same fiscal year if the costs clearly benefit those later periods. Prior to actually receiving advertising services, advertising costs may be accrued and allocated to interim periods on the basis of sales if the sales arrangement implicitly includes the advertising program. See Chapter 3 for a discussion of the specialized accounting for direct-response advertising prescribed by ASC 340-20. Those rules apply to both interim and annual reporting periods.

Costs and expenses subject to year-end determination, such as discretionary bonuses and profit-sharing contributions, are assigned to interim periods in a reasonable and consistent manner to the extent they can be reasonably estimated (ASC 270-10-45-10).

Application of interim expense reporting principles is illustrated in the following examples.

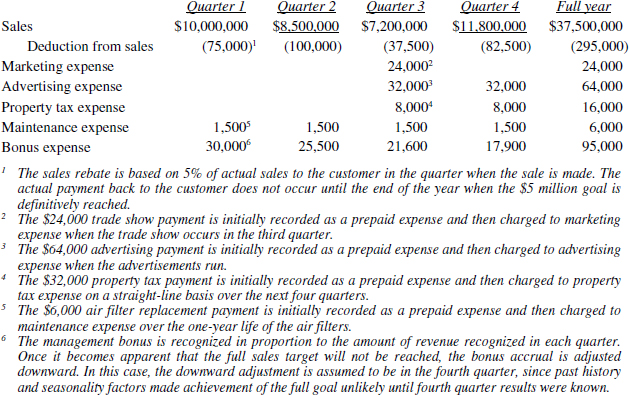

Dakota Corporation encounters the following expense scenarios as part of its quarterly reporting (for illustrative purposes, all amounts are considered to be material):

- Its largest customer, Floor-Mart, placed firm orders for the year that will result in sales of $1,500,000 in the first quarter, $2,000,000 in the second quarter, $750,000 in the third quarter, and $1,650,000 in the fourth quarter. Dakota gives Floor-Mart a 5% rebate if Floor-Mart buys at least $5 million of goods each year. Floor-Mart exceeded the $5 million goal in the preceding year and is expected to do so again in the current year.

- It incurs $24,000 of trade show fees in the first quarter for a trade show that will occur in the third quarter.

- It pays $64,000 in advance in the second quarter for a series of advertisements that will run during the third and fourth quarters.

- It receives a $32,000 property tax bill in the second quarter that applies to the following twelve-month period (July 1 to June 30).

- It incurs annual air filter replacement costs of $6,000 in the first quarter.

- Its management team is entitled to a year-end cash bonus of $120,000 if it meets an annual sales target of $40 million, prior to any sales rebates, with the bonus dropping by $10,000 for every million dollars of sales not achieved.

Dakota used the following calculations to record these scenarios:

Income Taxes

At each interim date, the reporting entity is required to make its best estimate of the effective income tax rate expected to apply to the full fiscal year. This estimate reflects expected federal, state, local, and foreign income tax rates, income tax credits, and the effects of applying income tax planning techniques. However, changes in income tax legislation are reflected in interim periods only after the enactment date of the legislation. This process is necessary to avoid distortions that would result if early interim periods reflected the entire effect of lower income tax brackets, while later periods suffered from having all income taxed at higher bracket rates. Since income taxes apply to annual income, not to interim periods on stand-alone bases, an integral approach is clearly warranted.

Fair Value of Financial Instruments

ASC 825-10-50 requires disclosures about the fair value of financial instruments in interim reporting periods, as well as in annual financial statements. Specifically, an entity should disclose the fair value of all financial instruments for which it is practicable to create such an estimate, alongside their carrying values. The format of this presentation should clarify whether these items are assets or liabilities. The entity should also disclose the methods and significant assumptions that it used to estimate the fair value of the financial instruments, as well as note any changes in these methods and assumptions from the preceding period.

Discontinued Operations and Extraordinary Items

Extraordinary items and the effects of the disposal of a component of the entity (ASC 270-10-45-11A) are reported separately in the interim period in which they occur. The same treatment is given to other unusual or infrequently occurring events. No attempt is made to allocate the effects of these items over the entire fiscal year in which they occur.

Materiality is evaluated by relating the item to the expected annual results of operations. Thus, an item to be reported in an early interim period may be judged material but later, when estimated results for the full fiscal year are known with greater precision, be judged immaterial; the opposite pattern may also occur, with a presumed immaterial item being later found material to full-year results of operations. Either of such eventualities is inherent in the interim reporting process and would not be deemed an error requiring restatement.

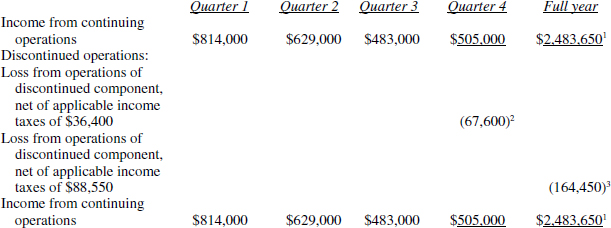

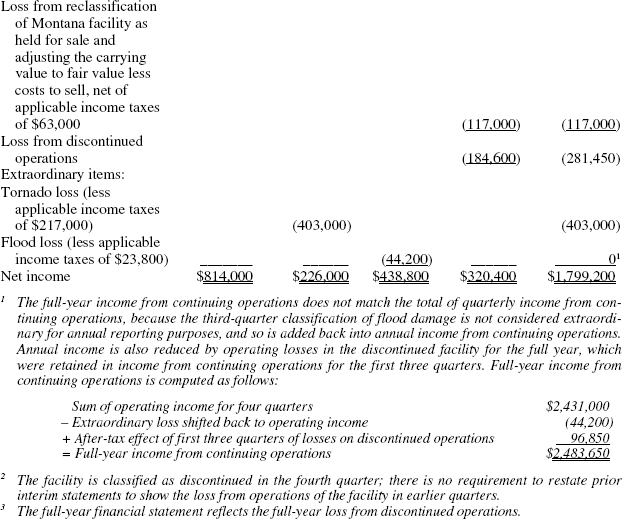

Dakota Corporation's Helena, Montana, facility suffers a direct hit from a tornado during the second quarter. Dakota's management believes the loss warrants treatment as an extraordinary item since the state of Montana does not typically experience tornadoes. Dakota's insurance does not cover tornados, and the loss resulting from cleanup costs and writing down the net book value of the damaged portion of the building is $620,000, or $403,000 net of applicable income taxes computed at a flat 35% rate. As required by ASC 360-10-35, Dakota's management estimates the expected future cash flows from the use and ultimate disposition of the property and determines that the building does not require any further write-down for impairment.

In the third quarter, before the tornado repairs are completed, this unfortunate facility is subjected to a flood; however, the unreimbursed damage is only $68,000, or $44,200 net of applicable income taxes. The flood damage is considered material in the third quarter, but subsequently, during the fourth quarter, is determined to be immaterial for annual reporting purposes.

Finally, in the fourth quarter, management declares the facility too damaged to repair, and reclassifies it as held-for-sale. The facility meets the criteria of ASC 360-10-35 to be classified as a component of the entity since its operations and cash flows are clearly distinguishable from the rest of Dakota Corporation. Activities conducted at the facility generated income from operations of $82,000 in the first quarter, followed by losses of $102,000, $129,000, and $104,000 in the succeeding quarters, prior to 35% income taxes. Upon classification of the facility as held for sale, the carrying value is written down to its fair value less cost to sell resulting in a further loss of $117,000, which is net of $63,000 in applicable income taxes.

Dakota includes these circumstances in its quarterly and annual financial statement in the following manner:

Note that classification as an extraordinary item is based on facts and circumstances, given the requirement under GAAP that the event be both infrequent in occurrence and unusual in nature. If the plant were located in Kansas, for example, and tornado damage did not qualify under both criteria given its location, then this would not have been presented as an extraordinary item.

Contingencies

In general, contingencies and uncertainties that exist at an interim date are accrued or disclosed in the same manner required for annual financial statements. For example, contingent liabilities that are probable and subject to reasonable estimation are to be accrued. The materiality of the contingency is evaluated in relation to the expected annual results. Disclosures regarding material contingencies and uncertainties are to be repeated in all interim and annual financial statements until they have been settled, adjudicated, transferred, or judged to be immaterial.

The following adjustments or settlements are accorded special treatment in interim reports if they relate to prior interim periods of the current fiscal year:

- Litigation or similar claims

- Income taxes (except for the effects of retroactive tax legislation enacted during an interim period)

- Renegotiation proceedings associated with government contracts

- Utility revenue under rate-making processes.

If the item is material, directly related to prior interim periods of the current fiscal year in full or in part, and becomes reasonably estimable in the current interim period, it is reported as follows:

- The portion directly related to the current interim period is included in that period.

- Prior interim periods are restated to reflect the portions directly related to those periods.

- The portion directly related to prior years is recognized in the restated first interim period of the current year.

Dakota Corporation is sued over its alleged violation of a patent in one of its products. Dakota settles the litigation in the fourth quarter. Under the settlement terms, Dakota must retroactively pay a 3% royalty on all sales of the product to which the patent applies. Sales of the product are $150,000 in the first quarter, $82,000 in the second quarter, $109,000 in the third quarter, and $57,000 in the fourth quarter. In addition, the cumulative total of all sales of the product in prior years is $1,280,000. Dakota restates its quarterly financial results to include the following royalty expense:

Seasonality

The operations of many businesses are subject to recurring material seasonal variations. Such businesses are required to disclose the seasonality of their activities to avoid the possibility of misleading interim reports. ASC 270-10-45-11 also recommends that such businesses present results of operations for twelve-month periods ending at the interim date of the current and preceding year.

Accounting Changes

Change in accounting principle.

The discussion commencing at ASC 270-10-45-12 requires disclosure in interim financial statements of any changes in accounting principles or the methods of applying them from those that were followed in:

- The prior fiscal year,

- The comparable interim period of the prior fiscal year, and

- The preceding interim periods of the current fiscal year.

The information to be included in these disclosures is the same as is required to be included in annual financial statements and is to be provided in the interim period in which the change occurs, subsequent interim periods of that same fiscal year, and the annual financial statements that include the interim period of change.

ASC 250 requires changes in accounting principle to be adopted through retrospective application to all prior periods presented. This accounting treatment is the same in both interim and annual financial statements. The impracticability exception provided by ASC 250 is only applicable to annual financial statements and may not be invoked for prechange interim periods occurring in the same fiscal year as the change is made.

ASC 270-10-45-15 recommends making a change in accounting principle in the first interim report of a fiscal year wherever possible.

Change in accounting estimate.

ASC 250 requires that changes in accounting estimate be accounted for currently and prospectively. Retroactive restatement and presentation of pro forma amounts are not permitted. This accounting is the same whether the change occurs at the end of a year or during an interim reporting period.

Change in reporting entity.

When an accounting change results in the financial statements presenting a different reporting entity than was presented in the past, all prior periods presented in the new financial statements, including all previously issued interim financial information, are to be retroactively restated to present the financial statements of the new reporting entity. In restating the previously issued information, however, interest previously capitalized under ASC 835 with respect to equity-method investees that have not yet commenced their planned principal operations, is not to be changed.

Restatements.

The term “restatement” may only be used to describe a correction of an error from a prior period. Under ASC 250, when a restatement is made, the financial statements of each individual prior period presented (whether interim or annual) are to be adjusted to reflect correction of the effects of the error that relate to that period. Full disclosure of the restatement is to be provided in the financial statements of the:

- Interim period in which the restatement is first made,

- Subsequent interim periods during the same fiscal year that includes the interim period in which the restatement is first made, and

- Annual period that includes the interim period in which the restatement is first made.

PART II—REQUIREMENTS APPLICABLE TO PUBLIC REPORTING ENTITES

Quarterly Reporting to the SEC

Summarized interim financial data.

The SEC does not require registrants to file complete sets of quarterly financial statements. Rather, on a quarterly basis, condensed (summarized) unaudited interim financial statements are required to be filed with the SEC on its Form 10-Q (Regulation S-X, Rule 10-01—ASC 270-10-S99-1). The minimum captions and disclosures required to be included in these financial statements are summarized in the Disclosure Checklist in the Appendix. Although such financial statements are informational tools used by investors, creditors, and analysts, they are not presented in sufficient detail to constitute a fair presentation of the reporting entity's financial position and results of operations in accordance with US GAAP.

Changes in accounting principle.

In the interim period in which a new accounting principle is adopted, the SEC expects registrants to include in the quarterly condensed financial statements a complete set of the disclosures required to be included in annual financial statements. In addition, these complete disclosures are to be repeated in the interim condensed financial statements of each of the quarters immediately succeeding the quarter of adoption until an annual Form 10-K is filed that reflects the registrant's adoption of the new accounting principle.

Fourth quarter adjustments.

When, as is typical, the fourth quarter results are not reported separately, the annual financial statements of publicly traded companies are required to disclose the effects on the fourth quarter of accounting changes made during the quarter; disposals of components of the reporting entity; extraordinary, unusual, or infrequently occurring items; and the aggregate effect of year-end adjustments having a material effect on the quarter's results.

Earnings per share.

The same procedures used at year-end are used for earnings per share computations and disclosures in interim reports. Note that annual earnings per share generally will not equal the sum of the interim earnings per share amounts, due to such factors as stock issuances during the year and market price changes. No reconciliation requirements exist for such disparities.

Accelerated reporting requirements.

To provide stakeholders with relevant, actionable information on a more timely basis, the SEC requires certain events that occur between regular quarterly reporting deadlines to be reported on its Form 8-K in accordance with an accelerated timetable. Events subject to accelerated reporting requirements are set forth below.

| Form 8-K item number | Event requiring disclosure |

| Section 1 – Registrant's Business and Operations | |

| 1.01 | Entry into or amendment of a “material definitive agreement” that provides for rights or obligations material to and enforceable by or against the registrant |

| 1.02 | Termination of material definitive agreement |

| 1.03 | Bankruptcy or receivership |

| 1.04 | Mine safety – reporting of shutdowns and patterns of violations Section 2 – Financial Information |

| 2.01 | Completion of acquisition or disposition of significant amounts of assets by registrant or any of its majority-owned subsidiaries (other than in the ordinary course of business) |

| 2.02 | Results of operations and financial condition—disclosure of material nonpublic information regarding a completed fiscal year or quarter included in a public announcement or release including an update of an earlier announcement or release |

| 2.03 | Creation of a direct financial obligation or an obligation under an off-balance- sheet arrangement |

| 2.04 | Triggering events that accelerate or increase a direct financial obligation or an obligation under an off-balance-sheet arrangement |

| 2.05 | Costs associated with exit or disposal activities |

| 2.06 | Material impairments

Section 3 – Securities and Trading Markets |

| 3.01 | Notice of delisting or failure to satisfy a continued listing rule or standard; transfer of listing |

| 3.02 | Unregistered sales of equity securities |

| 3.03 | Material modification to rights of security holders, including working capital restrictions and other limitations on the payment of dividends

Section 4 – Matters Related to Accountants and Financial Statements |

| 4.01 | Changes in registrant's certifying accountant |

| 4.02 | Nonreliance on previously issued financial statements or a related audit report or completed interim review

Section 5 – Corporate Governance and Management |

| 5.01 | Changes in control of the registrant |

| 5.02 | Departure of directors or principal officers; election of directors; appointment of certain officers; compensatory arrangements of certain officers |

| 5.03 | Amendments to articles of incorporation or bylaws; change in fiscal year |

| 5.04 | Temporary suspension of trading under registrants's employee benefit plans |

| 5.05 | Amendments to the Registrant's code of ethics, or waivers of a provision of the code of ethics |

| 5.06 | Change in shell company status |

| 5.07 | Submission of matters to a vote of security holders |

| Form 8-K item number | Event requiring disclosure |

| 5.08 | Shareholder director nominations

Section 6 – Asset-Backed Securities |

| 6.012 | Asset-backed securities' informational and computational material |

| 6.02 | Change of servicer or trustee |

| 6.03 | Change in credit enhancement or other external support for asset-backed securities |

| 6.04 | Failure to make a required distribution |

| 6.05 | Securities act updating disclosure

Section 7 – Regulation FD |

| 7.01 | Regulation FD disclosure—

Section 8 – Other Events |

| 8.01 | Other events that the registrant deems important to security holders that is not otherwise called for by the Form 8-K.

Section 9 – Financial Statements and Exhibits |

| 9.01 | Financial statements, pro forma information, and exhibits relative to business combinations described in item number 2.01 including certain shell-company transactions; or acquisitions of one or more real estate properties. |

Other Sources

| See ASC Location – Wiley GAAP Chapter | For information on... |

| 820-10-50 | For additional disclosure guidance on fair value measurements and disclosures for the reporting entity |

1 AICPA Accounting Standards Executive Committee Task Force on LIFO Inventory Problems, “Identification and Discussion of Certain Financial Accounting and Reporting Issues Concerning LIFO Inventories.” American Institute of Certified Public Accountants, November 30, 1984. The paper can be found at tinyurl.com/8i3f8t7.

2 For the purposes of items 6.nn, terms used are defined in Item 1101 of Regulation AB (17 CFR 229.1101)