42 ASC 720 OTHER EXPENSES

ASC 720-30, Real and Personal Property Taxes

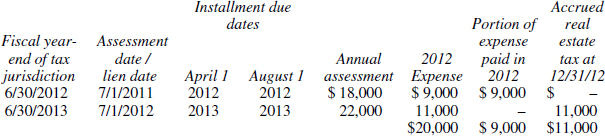

Example of accrued real estate taxes

PERSPECTIVE AND ISSUES

Subtopics

ASC 720, Other Expenses, contains nine subtopics:

- ASC 720-10, Overall, which merely lists the other subtopics

- ASC 720-15, Start-Up Costs

- ASC 720-20, Insurance Costs

- ASC 720-25, Contributions Made

- ASC 720-30, Real and Personal Property Taxes

- ASC 720-35, Advertising Costs

- ASC 720-40, Electronic Equipment Waste Obligations

- ASC 720-45, Business and Technology Reengineering

- ASC 720-50, Fees Paid to the Federal Government by Pharmaceutical Manufacturers and Health Insurers.

Scope and Scope Exceptions

ASC 720-15. ASC 720-15 applies to all nongovernmental entities. Routine ongoing efforts to improve existing quality of products, services, or facilities are not start-up costs. The subtopics lists specific activities that are not considered start-up costs and should be accounted for in accordance with other existing authoritative literature.

- Ongoing customer acquisition costs, such as policy acquisition costs (see Subtopic 944-30)

- Loan origination costs (see Subtopic 310-20)

- Activities related to routine, ongoing efforts to refine, enrich, or otherwise improve upon the qualities of an existing product, service, process, or facility

- Activities related to mergers or acquisitions

- Business process reengineering and information technology transformation costs addressed in Subtopic 720-45

- Costs of acquiring or constructing long-lived assets and getting them ready for their intended uses (however, the costs of using long-lived assets that are allocated to start-up activities [for example, depreciation of computers] are within the scope of this Subtopic)

- Costs of acquiring or producing inventory

- Costs of acquiring intangible assets (however, the costs of using intangible assets that are allocated to start-up activities [for example, amortization of a purchased patent] are within the scope of this Subtopic)

- Costs related to internally developed assets (for example, internal-use computer software costs) (however, the costs of using those assets that are allocated to start-up activities are within the scope of this Subtopic)

- Research and development costs that are within the scope of Section 730-10-15

- Regulatory costs that are within the scope of Section 980-10-15

- Costs of fundraising incurred by NFPs

- Costs of raising capital

- Costs of advertising

- Costs incurred in connection with existing contracts as stated in paragraph 605-35-25-41(d).

(ASC 720-15-15-4)

ASC 720-35. ASC 720-35 applies to all entities, but does not apply to the following transactions:

- Direct-response advertising (for guidance, see Subtopic 340-20).

- Advertising costs in interim periods (for guidance, see paragraph 270-10-45-7).

- Costs of advertising conducted for others under contractual arrangements.

- Indirect costs that are specifically reimbursable under the terms of a contract.

- Fundraising by NFPs (however, this Subtopic does apply to advertising activities of NFPs).

- Customer acquisition activities, other than advertising.

- The costs of premiums, contest prizes, gifts, and similar promotions, as well as discounts or rebates, including those resulting from the redemption of coupons. (Other costs of coupons and similar items, such as costs of newspaper advertising space, are considered advertising costs.)

(ASC 720-35-15-3)

ASC 720-35 may or may not apply to activities, such as product endorsements and sponsorships of events, which may be performed pursuant to executory contracts. (ASC 720-35-15-4)

DEFINITIONS OF TERMS

Source: ASC 720

Start-up Activities. Defined broadly as those one-time activities related to any of the following:

- Opening a new facility

- Introducing a new product or service

- Conducting business in a new territory

- Conducting business with an entirely new class of customers (for example, a manufacturer who does all of business with retailers attempts to sell merchandise directly to the public) or beneficiary

- Initiating a new process in an existing facility

- Commencing some new operation.

CONCEPTS, RULES, AND EXAMPLES

ASC 720-15, Start-Up Costs

ASC 720-15 provides guidance on financial reporting of start-up costs and organization costs and requires such costs to be expensed as incurred. Start-up costs are defined as onetime activities related to opening a new facility, introducing a new product or service, conducting activities in a new territory, pursuing a new class of customer, initiating a new process in an existing facility, or some new operation. Those costs are variously referred to as preopening costs, preoperating costs, organization costs, and start-up costs.

ASC 720-30, Real and Personal Property Taxes

Accrued real estate and personal property taxes represent the unpaid portion of an entity's obligation to a state, county, or other taxing authority that arises from the ownership of real or personal property, respectively. ASC 720-30 indicates that the most acceptable method of accounting for property taxes is a monthly accrual of property tax expense during the fiscal period of the taxing authority for which the taxes are levied. The fiscal period of the taxing authority is the fiscal period that includes the assessment or lien date.

A liability for property taxes payable arises when the fiscal year of the taxing authority and the fiscal year of the entity do not coincide or when the assessment or lien date and the actual payment date do not fall within the same fiscal year.

Rohlfs Corporation is a calendar-year corporation that owns real estate in a state that operates on a June 30 fiscal year. In this state, real estate taxes are assessed and become a lien against real property on July 1. These taxes, however, are payable in arrears in two installments due on April 1 and August 1 of the next calendar year. Real estate taxes assessed were $18,000 and $22,000 for the years ended 6/30/2012 and 6/30/13, respectively. Rohlfs computes its accrued real estate taxes at December 31, 2011, as follows:

Proof of the accrual computation is as follows:

Annual assessment—year-end 6/30/13 of $22,000 ÷ 12 = $1,833/month × 6 months $11,000

ASC 730-35, Advertising Costs

The costs of advertising are expensed either as costs are incurred or the first time the advertising takes place (e.g., when the television advertisement is aired or printed copy is published), if later (720-35-25). However, there are two exceptions:

- Direct-response advertising

- Whose primary purpose is to elicit sales to customers who could be shown to have responded specifically to the advertising, and

- That results in probable future economic benefits; and

- Expenditures for advertising costs that are made subsequent to recognizing revenues related to those costs.

Expenditures for direct-response advertising are deferred if both of the conditions listed above are met. The future benefits to be received are the future revenues arising as a direct result of the advertising. The company is required to provide entity-specific persuasive evidence that there is a linkage between the direct-response advertising and these future benefits. These costs are then amortized over the period in which the future benefits are expected to be received.

Advertising expenditures are sometimes made subsequent to the recognition of revenue (such as in “cooperative advertising” arrangements with customers). In order to achieve proper matching, these costs are to be estimated, accrued, and charged to expense when the related revenues are recognized.