6 ASC 225 INCOME STATEMENT

Format of Statements of Income and Comprehensive Income

Income from Continuing Operations

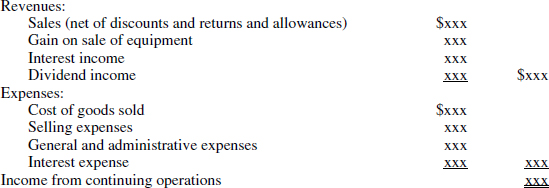

Example of a single-step format for income from continuing operations

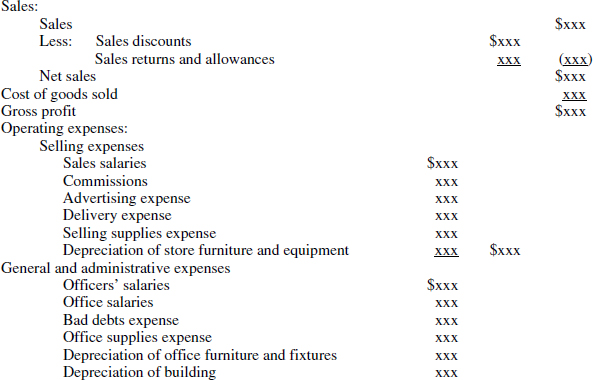

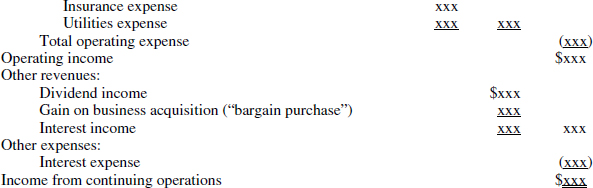

Example of a multiple-step format for income from continuing operations

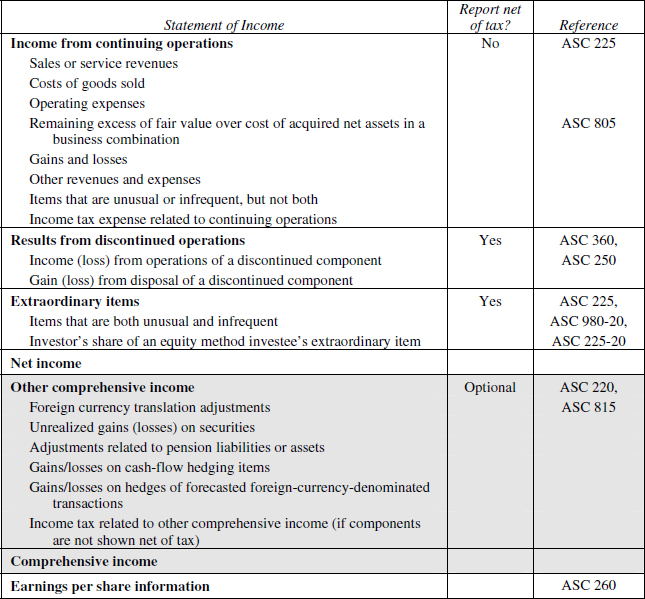

Examples of the format for presentation of various income statement items

ASC 225-20, Extraordinary and Unusual Items

Items specifically included or excluded from extraordinary items

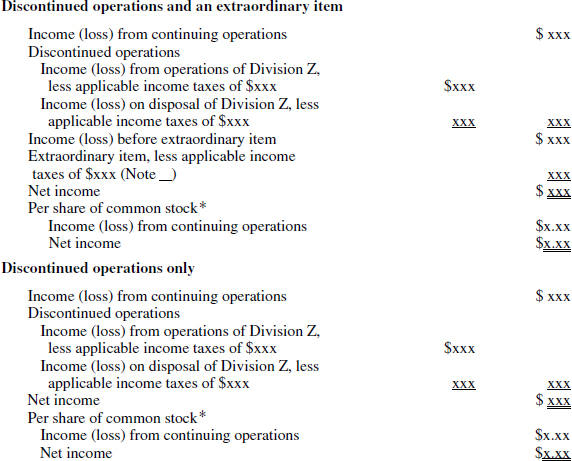

Example of the income statement presentation for extraordinary items

Statement of Income and Retained Earnings

Example of a statement of changes in equity

ASC 225-30, Business Interruption Insurance

PERSPECTIVE AND ISSUES

Subtopics

ASC, Income Statement, contains three subtopics:

- ASC 220-10, Overall, which provides general income statement guidance and on the structure of the Topic.

- ASC 220-20, Extraordinary Items, which addresses the classification, presentation and disclosure of extraordinary events and transactions and the presentation and disclosure of unusual and infrequently occurring items that do not meet the extraordinary criteria.

- ASC 220-30, Business Interruption Insurance, which provides presentation and disclosure requirements for business interruption insurance.

The three subtopics provide discrete information and are not interrelated.

Scope and Scope Exceptions

The guidance in ASC 225 applies to all entities.

ASC 225-20-15-2 specifically mandates that “The net effect of discontinuing the application of regulatory operations accounting addressed in Section 980-20-40 shall be recognized as an extraordinary item and thus shall be subject to the scope of this Subtopic regardless of whether the criteria discussed in paragraph 225-20-45-2 are met.”

Overview

The primary focus of financial reporting is to provide information about an entity's performance that is useful to present and potential investors, creditors, and others when they are making financial decisions. In financial reporting, performance is primarily measured by net income and its components, which are provided in the income statement.

In contrast to the statement of financial position, which provides information about an entity at a point in time, an income statement provides information about a period of time. It reflects information about the transactions and other events occurring within the period. Most of the weaknesses of an income statement are a result of its periodic nature. Entities are continually creating and selling goods and services, and at any single point in time some of those processes will be incomplete.

DEFINITIONS OF TERMS

Source: ASC 220-20-20

Extraordinary Items. Extraordinary items are events and transactions that are distinguished by their unusual nature and by the infrequency of their occurrence. Thus, both of the following criteria should be met to classify an event or transaction as an extraordinary item:

- Unusual nature. The underlying event or transaction should possess a high degree of abnormality and be of a type clearly unrelated to, or only incidentally related to, the ordinary and typical activities of the entity, taking into account the environment in which the entity operates (see paragraph 225-20-60-3).

- Infrequency of occurrence. The underlying event or transaction should be of a type that would not reasonably be expected to recur in the foreseeable future, taking into account the environment in which the entity operates (see paragraph 225-20-60-3).

Infrequency of Occurrence. See Extraordinary Items.

Unusual Nature. See Extraordinary Items

(Source ASC 220-30-20)

Business Interruption Insurance. Insurance that provides coverage if business operations are suspended due to the loss of use of property and equipment resulting from a covered cause of loss. Business interruption insurance coverage generally provides for reimbursement of certain costs and losses incurred during the reasonable period required to rebuild, repair, or replace the damaged property.

Gross Margin. The excess of sales over cost of goods sold. Gross margin does not consider all operating expenses.

CONCEPTS, RULES, AND EXAMPLES

Recognition and Measurement

Revenues.

Revenues represent actual or expected cash inflows that result from an entity's central operations. Revenues are generally recognized at the culmination of the earnings process—when the entity has substantially completed all it must do to be entitled to future cash inflows (or to retain cash already transferred). Most often, an exchange transaction indicates that revenues have been earned. Merchandise is delivered or services are rendered to a customer, resulting in the receipt of cash or the right to receive cash in the future. Revenues are generally measured by the values of the assets exchanged (or liabilities incurred).

Revenues are commonly distinguished from gains for three reasons. See the table below.

| Revenues | Gains |

| Result from an entity's central operations | Result from incidental or peripheral activities of the entity |

| Are usually earned | Result from nonreciprocal transactions (such as winning a lawsuit or receiving a gift) or other economic events for which there is no earnings process |

| Are reported gross | Are reported net |

The existence of an exchange transaction generally is critical to the accounting recognition of revenue. However, an exchange transaction is viewed in a broader sense than the legal concept of a sale. Whenever an exchange of rights and privileges takes place, an exchange transaction is deemed to have occurred. For example, interest revenue and interest expense are earned or incurred ratably over a period without a discrete transaction taking place. Accruals are recorded periodically in order to reflect the interest realized by the passage of time. In a like manner, the percentage-of-completion method recognizes revenue based upon the measure of progress on a long-term construction project. The earnings process is considered to occur simultaneously with the measure of progress (e.g., the incurrence of costs).

The timing of revenue recognition also varies based on the realizability of the future cash flows. For example, the production of certain commodities takes place in an environment in which the ultimate realization of revenue is so assured that revenue can be recognized upon the completion of the production process. At the opposite extreme is the situation in which an exchange transaction has taken place, but significant uncertainty exists as to the ultimate collectibility of the amount. For example, in certain sales of real estate, where the down payment percentage is extremely small and the security for the buyer's notes is minimal, revenue is often not recognized until the time collections are actually received.

Expenses.

Expenses represent actual or expected cash outflows that result from an entity's central operations. Expenses are generally recognized when an asset either is consumed in an entity's central operations or is no longer expected to provide the level of future benefits expected when that asset was recognized.

Expenses are commonly distinguished from losses for three reasons:

| Expenses | Losses |

| Result from an entity's central operations | Result from incidental or peripheral activities of the entity |

| Often incurred during the earnings process | Often result from nonreciprocal transactions (such as thefts or fines) or other economic events unrelated to an earnings process |

| Reported gross | Reported net |

- Expenses result from an entity's central operations; losses result from incidental or peripheral activities of the entity.

- Although many cash outflows are recognized directly as expenses, this accounting is often done for expediency since most expenses are first assets, if only for a brief moment. Measuring the consumption of assets is done by one of three pervasive measurement principles:

- Associating cause and effect,

- Systematic and rational allocation, or

- Immediate recognition.

The general approach for recognizing expenses is first to attempt to match costs with the related revenues. Next, a method of systematic and rational allocation should be attempted. If both of those measurement principles are inappropriate, the cost should be immediately expensed.

Some costs, such as materials and direct labor consumed in the manufacturing process, are relatively easy to identify with the related revenue elements. The matching principle requires that all expenses incurred in the generation of revenue should be recognized in the same accounting period as the related revenues are recognized. Thus, those cost elements are included in inventory and expensed as cost of sales when a product is sold and revenue from the sale is recognized. That process is associating cause and effect.

Other costs are more closely associated with specific accounting periods. In the absence of a cause and effect relationship, the asset's cost should be allocated to the accounting periods benefited in a systematic and rational manner. This form of expense recognition involves assumptions about the expected length of benefit and the relationship between benefit and cost of each period. Depreciation of plant, property, and equipment, amortization of intangibles, and allocation of rent and insurance are examples of costs that are recognized by the use of a systematic and rational method.

All other costs are normally expensed in the period in which they are incurred. This includes costs for which no clear-cut future benefits can be identified, costs that were recorded as assets in prior periods but for which no remaining future benefits can be identified, and costs for which no rational allocation scheme can be devised.

Expenses do not include distributions to owners. Expenses of a corporation are easily identified and separated from distributions to stockholders. In both the sole proprietorship and partnership form of entity, the identification process can be more difficult. Items such as interest or salaries paid to partners or owners may be thought of as distributions of profits rather than expenses. However, many entities adopt the philosophy that financial reporting should be the same regardless of legal form (economic substance takes precedence over legal form). Under the corporate form of business, interest on stockholder loans and salaries paid to stockholders are clearly classified as expenses and not as distributions. Accordingly, these items may be treated as expenses for both partnerships and sole proprietorships. However, full disclosure and consistency of financial reporting treatment would be required. Circumstances may involve treating certain payments, such as guaranteed salaries, as expenses while classifying other “salaries” as profit distributions.

Gains and losses.

Gains are increases in equity resulting from transactions and economic events other than those that generate revenues or are investments from owners. Losses are decreases in equity resulting from transactions and economic events other than those that generate expenses or are distributions to owners. Gains and losses result from an entity's peripheral transactions (e.g., sale of used equipment), from economic events outside of the control of management (e.g., holding gains on securities), or from nonreciprocal transactions (e.g., lawsuit settlements, fines, and thefts).

Gains and losses are often described in financial statements by their sources, for example, realized gains (losses) on sale of securities or earthquake loss. They are usually measured at net amounts. For example, gains (losses) from sales of assets are measured by subtracting the unexpired cost of the asset from the proceeds, and holding gains (losses) are measured by subtracting the value at the beginning of the period from the value at the end of the period.

Gains often result from transactions and other events that involve no earnings process. In terms of recognition, it is more significant that the gain be realized or realizable than earned. Losses are recognized when it becomes evident that future economic benefits of a previously recognized asset have been reduced or eliminated, or that a liability has been incurred without associated economic benefits.

Format of Statements of Income and Comprehensive Income

The basic order of presentation of information in an income statement (or statement of income and comprehensive income) is defined by a series of accounting pronouncements, as shown by the diagram below. Other than in the section “income from continuing operations,” the display of revenues, expenses, gains, losses, and other comprehensive income is predetermined by authoritative pronouncement. Only within income from continuing operations does tradition and industry practice determine the presentation.

The three items that are shown in the heading of an income statement are

- The name of the entity whose results of operations is being presented

- The title of the statement

- The period of time covered by the statement.

The entity's legal name should be used and supplemental information could be added to disclose the entity's legal form as a corporation, partnership, sole proprietorship, or other form if that information is not apparent from the entity's name. The use of the titles “Income Statement,” “Statement of Income and Comprehensive Income,” “Statement of Operations,” or “Statement of Earnings” denotes preparation in accordance with GAAP. If another comprehensive basis of accounting were used, such as the cash or income tax basis, the title of the statement would be modified accordingly. “Statement of Revenue and Expenses—Income Tax Basis” or “Statement of Revenue and Expenses—Modified Cash Basis” are examples of such titles.

The date of an income statement must clearly identify the time period involved, such as “Year Ending March 31, 2013.” That dating informs the reader of the length of the period covered by the statement and both the starting and ending dates. Dating such as “The Period Ending March 31, 2013” or “Through March 31, 2013” is not useful because of the lack of precision in those titles. Income statements are rarely presented for periods in excess of one year but are frequently seen for shorter periods such as a month or a quarter. Entities whose operations form a natural cycle may have a reporting period end on a specific day (e.g., the last Friday of the month). These entities should head the income statement “For the 52 Weeks Ended March 29, 2013” (each week containing seven days, beginning on a Saturday and ending on a Friday). Although that fiscal period includes only 364 days (except for leap years), it is still considered an annual reporting period.

Income statements generally should be uniform in appearance from one period to the next. The form, terminology, captions, and pattern of combining insignificant items should be consistent. If comparative statements are presented, the prior year's information should be restated to conform to the current year's presentation if changes in presentation are made.

Aggregation of items should not serve to conceal significant information, such as netting revenues against expenses or combining dissimilar types of resources, expenses, gains, or losses. The category “other or miscellaneous expense” should contain, at maximum, an immaterial total amount of aggregated insignificant items. Once this total approaches a material amount of total expenses, some other aggregations with explanatory titles should be selected.

Income from Continuing Operations

The section “income from continuing operations” includes all revenues, expenses, gains, and losses that are not required to be reported in other sections of an income statement.

There are two generally accepted formats for the presentation of income from continuing operations: the single-step and the multiple-step formats.

In the single-step format, items are classified into two groups: revenues and expenses. The operating revenues and other revenues are itemized and summed to determine total revenues. The cost of goods sold, operating expenses, and other expenses are itemized and summed to determine total expenses. The total expenses (including income taxes) are deducted from the total revenues to arrive at income from continuing operations.

Some believe that a multiple-step format enhances the usefulness of information about an entity's performance by reporting the interrelationships of revenues and expenses, using subtotals to report significant amounts. In a multiple-step format, operating revenues and expenses are separated from nonoperating revenues and expenses to provide more information concerning the firm's primary activities. This format breaks the revenue and expense items into various intermediate income components so that important relationships can be shown and attention can be focused on significant subtotals. Some examples of common intermediate income components are as follows:

- Gross profit (margin)—The difference between net sales and cost of goods sold.

- Operating income—Gross profit less operating expenses.

- Income before income taxes—Operating income plus any other revenue items and less any other expense items.

The following items of revenue, expense, gains, and losses are included within income from continuing operations:

- Sales or service revenues are charges to customers for the goods and/or services provided during the period. This section should include information about discounts, allowances, and returns in order to determine net sales or net revenues.

- Cost of goods sold is the cost of the inventory items sold during the period. In the case of a merchandising firm, net purchases (purchases less discounts, returns, and allowances plus freight-in) are added to beginning inventory to obtain the cost of goods available for sale. From the cost of goods available for sale amount, the ending inventory is deducted to obtain the cost of goods sold.

- Operating expenses are primary recurring costs associated with central operations (other than cost of goods sold) that are incurred in order to generate sales. Operating expenses are normally reported in the following two categories:

- Selling expenses

- General and administrative expenses

Selling expenses are those expenses directly related to the company's efforts to generate sales (e.g., sales salaries, commissions, advertising, delivery expenses, depreciation of store furniture and equipment, and store supplies). General and administrative expenses are expenses related to the general administration of the company's operations (e.g., officers and office salaries, office supplies, depreciation of office furniture and fixtures, telephone, postage, accounting and legal services, and business licenses and fees).

- Gains and losses result from the peripheral transactions of the entity. If immaterial, they are usually combined and shown with the normal, recurring revenues and expenses. If they are individually material, they should be disclosed on a separate line. Examples are write-downs of inventories and receivables, effects of a strike, gains and losses on the disposal of equipment, and gains and losses from exchange or translation of foreign currencies. Holding gains on available-for-sale securities are included in other comprehensive income rather than income from continuing operations.

- Other revenues and expenses are revenues and expenses not related to the central operations of the company (e.g., interest revenues and expenses, and dividend revenues).

- Unusual or infrequent items should be reported as a separate component of income from continuing operations.

- Goodwill impairment losses are presented as a separate line item in the income from continuing operations section of the income statement.

- Exit or disposal activity costs are included in income from continuing operations before income taxes.

- Income tax expense related to continuing operations is that portion of the total income tax expense applicable to continuing operations.

The section ends in a subtotal that varies depending upon the existence of discontinued operations and extraordinary items. Net income reflects all items of profit and loss recognized during the period, except for error corrections. The effects of changes in accounting principles (under ASC 250) are dealt with by retrospective application to all prior periods being presented. For example, the subtotal is usually titled “income from continuing operations” only when there is a section for discontinued operations in one of the years presented. If there is only a section for extraordinary items, the subtotal is usually titled “income before extraordinary items.” The titles are adjusted accordingly if more than one of these additional sections are necessary. If there are no discontinued operations or extraordinary items, the subtotal is titled “net income.”

The requirement that net income be presented as one amount does not apply to those entities that have statements different in format from commercial enterprises:

- Investment companies

- Insurance entities

- Certain not-for-profit entities (NFPs).

(ASC 225-10-45-1)

ASC 225-20, Extraordinary and Unusual Items

An event or transaction should be presumed to be an ordinary and usual activity (and thus, not to be described as extraordinary) unless the event or transaction is both of an unusual nature and infrequent in its occurrence.

Unusual nature.

To meet this criterion, the underlying event or transaction should

- Possess a high degree of abnormality and

- Be of a type clearly unrelated to, or only incidentally related to, the ordinary and typical activities of the reporting entity, taking into account the environment in which it operates.

In determining whether an event or transaction is of an unusual nature, the following special characteristics of the reporting entity are considered:

- Type and scope of operations

- Lines of business

- Operating policies

- Industry (or industries) in which the reporting entity operates

- Geographic locations of its operations

- Nature and extent of government regulation.

An event that is of an unusual nature for one reporting entity can be an ordinary and usual activity of another because of the above characteristics. Whether an event or transaction is beyond the control of management is irrelevant in the determination of whether it is of an unusual nature.

Infrequency of occurrence.

To satisfy this requirement, the underlying event or transaction should be of a type that would not reasonably be expected to recur in the foreseeable future, again taking into account the environment in which the reporting entity operates.

Items specifically included or excluded from extraordinary items.

Accounting pronouncements have specifically required the following items to be presented as extraordinary, irrespective of whether they meet the criteria stated above:

- The investor's share of an investee's extraordinary item when the investor uses the equity method of accounting for the investee (ASC 323-10-45).

- The net effect of adjustments relating to the discontinuation of the application of ASC 980 by a public utility or other reporting entity with regulated operations.

- The remaining excess of the fair value of acquired net assets over their cost pursuant to ASC 805.

- Estimated losses recognized due to obligations under the Coal Industry Retiree Health Benefit Act of 1992 (ASC 930-715-25).

Material gains and losses from the extinguishment of debt and gains from troubled debt restructurings previously were items specifically required to be classified as extraordinary. ASC 470-50-45 rescinded that requirement, so those gains and losses are now evaluated using the unusual and infrequent criteria described above. In addition, ASC 815-30-35 clarifies that, by analogy, these same criteria are to be used to evaluate the classification of gains or losses arising from adjustments to the carrying amount of debt required by the hedge accounting requirements of ASC 815.

The following items are, by definition, not extraordinary items:

- Write-down or write-off of receivables, inventories, equipment leased to others, or intangible assets

- Foreign currency gains and losses

- Gains and losses on the disposal of a segment of a business

- Gains and losses from sale or abandonment of property, plant, or equipment used in operations

- Effects of a strike

- Adjustments of accruals on long-term contracts.

(ASC 225-20-45-4)

Per ASC 225-20-55, neither the cost incurred by a company to defend itself from a takeover attempt nor the cost incurred as part of a “standstill” agreement meet the criteria for extraordinary classification as discussed in ASC 225-20.

Presentation.

Extraordinary items should be segregated from the results of ordinary operations and be shown net of taxes in a separate section of the income statement, following “discontinued operations.” If more than one extraordinary item occurs during a period, they should be reported separately or details should be included in the notes to the financial statements.

Statement of Income and Retained Earnings

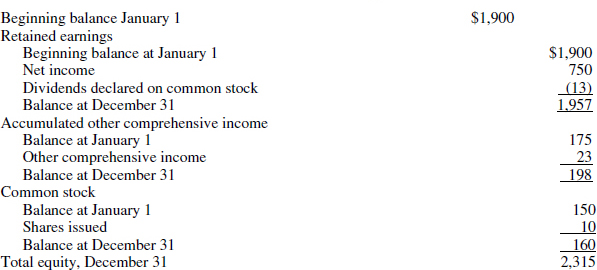

The example that follows illustrates the presentation of accumulated other comprehensive income in the statement of changes in equity.

Baker, Inc.

Statement of Changes in Equity

For the Year Ended December 31, 2013

Pro Forma Earnings

Companies have increasingly made reference in press releases and published materials to an alternative measure of performance, referred to as “pro forma earnings.” This practice has generated confusion because there is no standard definition for “pro forma earnings.” Different reporting entities can, and have, defined pro forma earnings on a wide range of ad hoc bases, and sometimes a given entity fails even to consistently define this amount from period to period.

Often, even when GAAP-basis earnings are stated in the same announcement as the pro forma measure, it is the latter that receives most of the attention. In a number of instances, pro forma earnings have been based on very aggressive exclusions of operating costs and, sometimes, the inclusion of onetime gains. Such practices ultimately came to be widely recognized as being misleading and inappropriate, and popular sentiment turned against employment of such devices.

For reporting entities, part of the allure of pro forma earnings is that they can be defined to exclude some or all of a range of “unusual” items. Not surprisingly, most of the excluded items have been charges, such as those for worker layoffs, restructurings, assets impairments, and inventory obsolescence. Even if truly not expected to recur annually, many of these charges are quite normal and may be anticipated to recur at irregular intervals in the life of a given business. Furthermore, many such charges can be viewed as “catch-ups” for under-recognition of expenses in earlier periods, and since those charges would have been fully reflected in current earnings, the subsequent period's catch-up should, logically, also be included in the current period measure of operating results.

A further practice, which is improper but has not been uncommon, has been for reporting entities to opportunistically charge off an exaggerated loss in the current period, perhaps in connection with such randomly occurring events as discontinued operations. The loss is then excluded from pro forma earnings. The excess reserves then become available to be drawn down in future periods, as the provided-for expenses fail to materialize in the amounts reserved. The draw-downs of the excess reserves increase net income in future periods, but those draw-downs will not be excluded from pro forma earnings the way the original loss had been. The result will be to boost both GAAP-basis net income and pro forma earnings in future years.

The SEC adopted Regulation G to curtail the use of pro forma earnings statements. Regulation G states that a public company, or a person acting on its behalf, is not to make public a non-GAAP financial measure that, taken together with the information accompanying that measure, either contains an untrue statement of a material fact or omits a material fact that would be necessary to make the presentation of the non-GAAP financial measure not misleading. Further, Regulation G requires a public company that discloses or releases a non-GAAP financial measure to include in that disclosure or release a presentation of the most directly comparable GAAP financial measure and a reconciliation of the disclosed non-GAAP measure to that directly comparable GAAP financial measure.

The regulations also prohibit certain non-GAAP measures from inclusion in SEC filings. Public companies must not:

- Exclude from non-GAAP liquidity measures charges or liabilities that required, or will require, cash settlement, or would have required cash settlement absent an ability to settle in another manner. However, earnings before interest and taxes (EBIT) and earnings before interest, taxes, depreciation, and amortization (EBITDA) are permissible.

- Create a non-GAAP performance measure that eliminates items identified as nonrecurring, infrequent, or unusual if the nature of the excluded item is such that it is (a) reasonably likely to recur within two years or (b) similar to a charge or gain that occurred within the prior two years.

- Present non-GAAP financial measures on the face of the registrant's financial statements prepared in accordance with GAAP or in the accompanying notes.

- Present non-GAAP financial measures on the face of any pro forma financial information required to be disclosed by Article 11 of Regulation S-X (e.g., business combinations or disposals).

- Use titles or descriptions of non-GAAP financial measures that are the same as, or confusingly similar to, titles or descriptions used for GAAP measures.

The SEC's action has curbed the abuse of pro forma earnings measures, but it does little to standardize the measures in use.

ASC 225-30, Business Interruption Insurance

ASC 225-30 provides guidance on presentation and disclosure of business interruption insurance. This type of insurance may cover gross margin lost because of the suspension of normal operations, fixed charges, expenses related to gross margin, and expenses incurred to reduce the loss from business interruption, etc.

Entities may choose how to record proceeds from business interruption insurance as long as it does not conflict with other standards. Disclosure requirements can be found in the Appendix.