21 ASC 325 INVESTMENTS—OTHER

ASC 325-30, Investments in Insurance Contracts

Investments in Life Settlement Contracts

Presentation in the statement of financial position

Examples of presentation alternatives in the statement of financial position

Examples of income statement presentation alternatives

Cash flow statement presentation

Disclosure of accounting policy

Disclosures when using the investment method

Disclosures when using the fair value method

ASC 325-40, Beneficial Interests in Securitized Financial Assets

PERSPECTIVE AND ISSUES

Topics

The Codification contains several Topics on the various forms of investments:

- ASC 320, Investments – Debt and Equity Securities

- ASC 323, Investments – Equity Method and Joint Venures

- ASC 325, Investments – Other.

Subtopics

ASC 325 contains four subtopics:

- ASC 325-10, Overall, which merely identifies the other three topics

- ASC 325-20, Cost Method Investments, which offers guidance on stocks of entities not accounted for under the fair value method (ASC 320) or the equity method (ASC 323)

- ASC 325-30, Investments in Insurance Contracts, which provides guidance on investments, life insurance contracts in general, and life settle contracts

- ASC 325-40, Beneficial Interests in Securitized Financial Assets, which provides guidance on accounting for a transferor's interest in securitized transaction accounted for as sales and purchased beneficial interests.

Overview

ASC 325-30 provides guidance on investments in insurance contracts. A life settlement contract is an agreement executed between a third-party investor and the owner of a life insurance policy where (1) the investor does not have an insurable interest in the life of the insured, (2) the investor pays an amount in excess of this policy's cash surrender value to the policy owner, and (3) upon the death of the insured, the face value of the policy is paid to the investor. These investments may be facilitated by a broker or transacted directly between the investor and the policy owner.

ASC 325-40 provides guidance on another type of investment. When a reporting entity sells a portion of an asset that it owns, the portion retained becomes an asset separate from the portion sold and separate from the assets obtained in exchange. This is the situation when financial assets such as loans are securitized with certain interests being retained (e.g., a defined portion of the contractual cash flows). Management of the reporting entity must allocate the previous carrying amount of the assets sold based on the relative fair values of each component at the date of sale. In most cases, the initial carrying amount (i.e., the allocated cost) of the retained interest will be different from the fair value of the instrument. Furthermore, cash flows from those instruments may be delayed depending on the contractual provisions of the entire structure (for example, cash may be retained in a trust to fund a cash collateral account). The issue is addressed by ASC 325-40.

DEFINITIONS OF TERMS

Source: 325-20-20

Publicly Traded Company. A publicly traded company includes any company whose securities trade in a public market on either of the following:

- A stock exchange (domestic or foreign)

- In the over-the-counter market (including securities quoted only locally or regionally), or any company that is a conduit bond obligor for conduit debt securities that are traded in a public market (a domestic or foreign stock exchange or an over-the-counter market, including local or regional markets).

Additionally, when a company is required to file or furnish financial statements with the SEC or makes a filing with a regulatory agency in preparation for sale of its securities in a public market it is considered a publicly traded company for this purpose.

Conduit debt securities refers to certain limited-obligation revenue bonds, certificates of participation, or similar debt instruments issued by a state or local governmental entity for the express purpose of providing financing for a specific third party (the conduit bond obligor) that is not a part of the state or local government's financial reporting entity. Although conduit debt securities bear the name of the governmental entity that issues them, the governmental entity often has no obligation for such debt beyond the resources provided by a lease or loan agreement with the third party on whose behalf the securities are issued. Further, the conduit bond obligor is responsible for any future financial reporting requirements.

Source: ASC 325-30-20

Cash surrender value. The amount of cash that may be realized by the owner of a life insurance contract or annuity contract upon discontinuance and surrender of the contract before its maturity. The cash surrender value may be different from the policy account balance due to outstanding loans (including accrued interest) and surrender charges. (Note: The use of this glossary term is not consistent among legal contracts. When determining the applicability of this term, the economic substance of the item shall be taken into consideration.)

Certificates. An insurance entity issues to each individual in a group contract a certificate of insurance for each person insured under the group contract. The certificate is merely a summary of the rights, duties, and benefits available under a group policy. If there is any conflict between the certificate and a group policy, the group policy is the controlling document. (Note: The use of this glossary term is not consistent among legal contracts. When determining the applicability of this term, the economic substance of the item shall be taken into consideration.)

Claims stabilization reserve. The claims stabilization reserve is established through deductions from the policy account balance through the cost of insurance charge and is sometimes held in a general account (that is, an account that is intermingled with the insurance entity's assets) as opposed to a legally segregated account (sometimes referred to as a separate account). The amounts are accumulated in this account until a death benefit is paid. The death benefit represents a combination of the policy account balance and the claims stabilization reserve based on the contractual terms. The cost of insurance is recalculated periodically based on actual experience of the insured class. Annually, the claims stabilization reserve is reviewed and an experience credit may be issued back to the policyholder if the experience has been favorable. The balance in the claims stabilization reserve will be reviewed annually and to the extent the balance is greater than the forecasted or expected amount, an experience refund would get credited to the entity's policy account balance. An entity's claims stabilization reserve will generally be realized through the collection of death benefits or an experience refund that gets credited to the policyholder's policy account balance or upon surrender of the group policy. A claims stabilization reserve is included in a policy as a mechanism for the policyholder and the insurance entity to share in the mortality risk, which in this case is the risk that the deaths will occur sooner than originally expected. Absent a claims stabilization reserve, the policyholder's net cost of insurance would typically be higher than in a policy without a claims stabilization reserve. The claims stabilization reserve is sometimes referred to as a mortality reserve or a mortality retention reserve. (Note: The use of this glossary term is not consistent among legal contracts. When determining the applicability of this term, the economic substance of the item shall be taken into consideration.)

Deferred acquisition costs tax. Section 848 of the Internal Revenue Code requires insurance entities to capitalize certain policy acquisition costs and defer deducting them in determining the insurer's tax liability. These costs are known as the deferred acquisition costs tax and are based on a percentage of the premium received as specified by the Internal Revenue Code. The initial deferred acquisition costs tax is deducted from a policyholder's policy account balance when the premium is paid. The deferred acquisition costs tax is credited back to the policyholder's policy account balance as the tax deduction is recognized in the insurer's tax return. (Note: The use of this glossary term is not consistent among legal contracts. When determining the applicability of this term, the economic substance of the item shall be taken into consideration.)

Insurance policy. The legal agreement between the policyholder and the insurance entity that states the terms of the arrangement. The term insurance policy includes all riders, attachments, side agreements, and other related documents that are either directly or indirectly part of the contractual arrangement. (Note: The use of this glossary term is not consistent among legal contracts. When determining the applicability of this term, the economic substance of the item shall be taken into consideration.)

Life settlement contract. A life settlement contract is a contract between the owner of a life insurance policy (the policy owner) and a third-party investor (investor), and has all of the following characteristics:

- The investor does not have an insurable interest (an interest in the survival of the insured, which is required to support the issuance of an insurance policy).

- The investor provides consideration to the policy owner of an amount to excess of the current cash surrender value of this life insurance policy.

- The contract pays the face value of the life insurance policy to an investor when the insured dies.

Policy account balance. At any point in time, this is the amount held by the insurance entity on behalf of the policyholder. This balance may be held in a general account, a separate account (a legally segregated account), or a combination of both on the insurance entity's balance sheet. This account includes premiums received from the policyholder, plus any credited income, less any relevant charges (acquisition costs, cost of insurance, and so forth). (Note: The use of this glossary term is not consistent among legal contracts. When determining the applicability of this term, the economic substance of the item shall be taken into consideration.)

Probable. The future event or events are likely to occur.

Surrender charge. A contractual fee imposed by the insurance entity when a policyholder surrenders the insurance policy that typically decreases over the life of the policy. The surrender charge represents a recovery of costs incurred by the insurance entity in originating the policy. It may or may not be explicitly called a surrender charge and can be embedded in other agreements besides the insurance contract. (Note: The use of this glossary term is not consistent among legal contracts. When determining the applicability of this term, the economic substance of the item shall be taken into consideration.)

Source: ASC 323-40-20 Glossary

Beneficial interests. Rights to receive all or portions of specified cash inflows received by a trust or other entity, including, but not limited to, all of the following:

- Senior and subordinated shares of interest, principal, or other cash inflows to be passed-through

- Premiums due to guarantors

- Commercial paper obligations

- Residual interests, whether in the form of debt or equity.

Debt security. Any security representing a creditor relationship with an entity. The term debt security also includes all of the following:

- Preferred stock that by its terms either must be redeemed by the issuing entity or is redeemable at the option of the investor

- A collateralized mortgage obligation (or other instrument) that is issued in equity form but is required to be accounted for as a nonequity instrument regardless of how that instrument is classified (that is, whether equity or debt) in the issuer's statement of financial position

- US Treasury securities

- US government agency securities

- Municipal securities

- Corporate bonds

- Convertible debt

- Commercial paper

- All securitized debt instruments, such as collateralized mortgage obligations and real estate mortgage investment conduits

- Interest-only and principal-only strips.

The term debt security excludes all of the following:

- Option contracts

- Financial futures contracts

- Forward contracts

- Lease contracts

- Receivables that do not meet the definition of security and, so, are not debt securities (unless they have been securitized, in which case they would meet the definition of a security), for example:

- Trade accounts receivable arising from sales on credit by industrial or commercial entities

- Loans receivable arising from consumer, commercial, and real estate lending activities of financial institutions.

CONCEPTS, RULES, AND EXAMPLES

Cost Method Investments

An entity may hold stock in entities other than subsidiaries. The entity should account for these investments by one of three methods—

- The cost method (addressed in this Subtopic),

- The fair value method (Topic 320), or

- The equity method (Topic 323).

The cost method is generally followed for most investments

- In noncontrolled corporations,

- In some corporate joint ventures, and

- To a lesser extent in unconsolidated subsidiaries, particularly foreign.

For investments using the cost method, the investor recognizes, initially at cost, investments in stock of investees as assets on the statement of financial position.

Dividends.

Dividends are the vehicle for an investor to recognize earnings from an investment under the cost method. From the date of the investment entities recognize dividends received from an investee in one of two ways:

- If the dividends are distributed from net accumulated earnings, the investor recognizes them as income.

- If the dividends are in excess of earnings, they are considered a return on investment and the investor records them as reductions in the cost of the investment.

Impairment.

The value of the investment in stock accounted for under the cost method may lose its value because of a series of operating losses or other factors. If the impairment is considered other than temporary, investors should look to ASC 320-10-35-17 through 35-35. Those paragraphs discuss the methodology for determining impairment and evaluating whether the impairment is other than temporary and, therefore, must be recognized.

Changes in Accounting Method.

The level of ownership in stock of an investee may change An investor may lose the ability to influence policy or gain the ability to influence policy. These circumstances call for a change to or from the equity method of accounting. In those cases, preparers should look to ASC 323-10-35 for guidance.

Other Accounting Issues.

ASC 325-20 provides guidance on Accounting for a Cost Method Investment in Affordable Housing Projects with Allocated Tax Credits. Disclosures required by ASC 325 may be found in the disclosure checklist included with this volume.

Other Sources.

For guidance on the use of the cost method by real estate investment trusts with related service corporations, see Topic 974. (ASC 325-20-60)

ASC 325-30, Investments in Insurance Contracts

Investments in Life Settlement Contracts.

For a life settlement contract, ASC 325-30 requires the investor to elect to account for these investments using either the “investment method” or the “fair value method.” This irrevocable election is made in one of two ways:

- On an instrument-by-instrument basis supported by documentation prepared concurrently with acquisition of the investment, or

- Based on a preestablished, documented policy that automatically applies to all such investments.

The investment method.

The investor recognizes the initial investment at the transaction price plus all initial direct external costs. Continuing costs (payments of policy premiums and direct external costs, if any) necessary to keep the policy in force are capitalized. Gain recognition is deferred until the death of the insured. At that time the investor recognizes in net income (or other applicable performance indicator) the difference between the carrying amount of the investment and the policy proceeds.

The investor is required to test the investment for impairment upon the availability of new or updated information that indicates that, upon the death of the insured, the expected proceeds from the insurance policy may not be sufficient for the investor to recover the carrying amount of the investment plus anticipated gross future premiums (undiscounted for the time value of money) and capitalizable external direct costs, if any. Indicators to be considered include, but are not limited to:

- A change in the life expectancy of the insured

- A change in the credit standing of the insurer.

As a result of performing an impairment test, if the undiscounted expected cash inflows (the expected proceeds from the policy) are less than the carrying amount of the investment plus the undiscounted anticipated gross future premiums and capitalizable external direct costs, an impairment loss is recognized. The loss is recorded by reducing the carrying value of the investment to its fair value. The fair value computation is to employ current interest rates. Note that a change in interest rates would not by itself require an impairment test.

The fair value method.

The initial investment is recorded at the transaction price. Each subsequent reporting period, the investor remeasures the investment at fair value and recognizes changes in fair value in current period net income (or other relevant performance indicators for reporting entities that do not report net income). Cash outflows for policy premiums and inflows for policy proceeds are to be included in the same financial statement line item as the changes in fair value are reported.

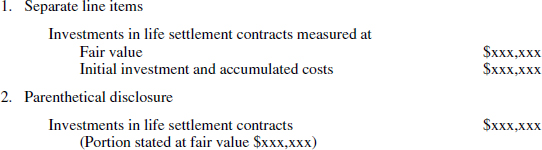

Presentation in the statement of financial position.

On the face of its statement of financial position, the investor is required to differentiate between investments remeasured at fair value and those accounted for using the investment method. This may be accomplished by either:

- Presenting separate line items for each type of investment, or

- Parenthetical disclosure.

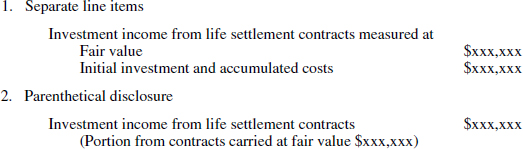

Income statement presentation.

Investment income attributable to fair value remeasurements is presented on the face of the income statement separately from investment income attributable to contracts accounted for using the investment method. This may be accomplished by either:

- Presenting separate line items for investment income attributable to each type of investment, or

- Parenthetical disclosure.

Cash flow statement presentation.

Cash inflows and outflows attributable to investments in life settlement contracts are to be classified based on the nature and purpose for which the contracts were acquired.

Disclosure of accounting policy.

In addition to other applicable GAAP disclosures, the investor is to disclose the policy it follows to account for life settlement contracts, including the classification in the cash flow statement of cash inflows and outflows associated with these contracts.

Disclosures when using the investment method.

For life settlement contracts accounted for under the investment method, the investor is required to disclose the following information based on the remaining life expectancy of the insured individuals:

- By year, for each of the first five fiscal years ending after the date of the statement of financial position, in total for the years succeeding those first five years, and in the aggregate:

- The number of life settlement contracts in which it has invested

- The carrying value of those contracts

- The face value (death benefits) of the life insurance policies covered by those contracts

- By year, for each of the first five fiscal years ending after the date of the most recent statement of financial position presented, the life insurance premiums expected to be paid in order to keep the life insurance policies related to the life settlement contracts in force.

- If management becomes aware of new or updated information that causes it to change its estimates of the expected timing of its receipt of the proceeds from the investments, it is to disclose the nature of the information and its related effect on the timing of the expected receipt of the policy proceeds. This disclosure is to include significant effects of the change in estimate on the disclosure described in item 1.1

Disclosures when using the fair value method.

For life settlement contracts accounted for under the fair value method, the investor is required to disclose the following information based on the remaining life expectancy of the insured individuals:

- The method(s) and significant assumptions used to estimate the fair value of the contracts, including any mortality assumptions

- By year, for each of the first five fiscal years ending after the date of the statement of financial position, in total for the years succeeding those first five years, and in the aggregate

- The number of life settlement contracts in which it has invested

- The carrying value of those contracts

- The face value (death benefits) of the life insurance policies covered by those contracts

- The reasons for changes in its estimates of the expected timing of its receipt of the proceeds from the investments including significant effects of the change in estimates on the information disclosed in item 2.

ASC 325-40, Beneficial Interests in Securitized Financial Assets

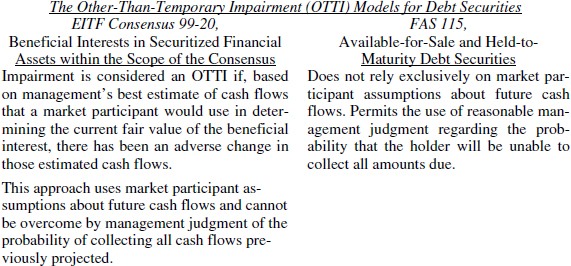

This subtopic, when initially issued, provided that the holder of the beneficial interest was to recognize the excess of all cash flows anticipated at the acquisition transaction date over the initial investment as interest income using the effective yield method. The holder would be required to update the estimate of cash flows over the life of the beneficial interest. If the estimated cash flows were to change (but there was still an excess over the carrying amount), the adjustment was to be accounted for as a change in estimate with the amount of the periodic accretion adjusted over the remaining life of the beneficial interest. If the fair value of the beneficial interest were to decline below its carrying amount, the reporting entity was to apply the impairment guidance in ASC 320. If it is not practicable for a holder/transferor to estimate the fair value of the beneficial interest at the securitization date, interest income was to be recognized using the cash basis rather than the effective yield method.

Impairment and interest income on purchased and retained beneficial interests in securitized financial assets.

If, based on current information and events that the reporting entity anticipates a market participant would use in determining the current fair value of the beneficial interest, there is a change in estimated cash flows, the amount of accretable yield is to be recalculated. If the change in estimated cash flows is adverse, an other-than-temporary impairment would be considered to have occurred.

This model differed from the model applied to AFS and HTM debt securities that were not beneficial interests. Thus, US GAAP contained two separate models to determine whether an impairment in the value of debt securities was considered to be “other-than-temporary” and, accordingly, to be written down through a charge to net income as summarized in the following table:

Amendments to impairment guidance in ASC 325-40. FSP EITF 99-20-1, Amendments to the Impairment Guidance of EITF Issue No. 99-20

The FSP applies to beneficial interests included in the scope of EITF Consensus 99-20 (ASC 325-40). These include beneficial interests that:

- Are either debt securities under ASC 320 or are required to be accounted for in a manner similar to debt securities classified as available for sale or trading by ASC 310-10-35-45, as amended by FAS 166. These include the following securities, unless the security is within the scope of ASC 815, Derivatives and Hedging:

- Interest-only strips,

- Other interests that continue to be held by a transferor in securitizations,

- Loans,

- Other receivables, or

- Other financial assets that can be contractually prepaid or otherwise settled in a manner that the holder would not recover substantially all of its recorded investment.

- Involve securitized financial assets with contractual cash flows including, but not limited to loans, receivables, debt securities, and guaranteed lease residuals.

- Do not result in consolidation of the entity issuing the beneficial interest by the holder of the beneficial interests.

- Are not in the scope of ASC 310-30, Loans and Debt Securities Acquired with Deteriorated Credit Quality.

- Are not beneficial interests in securitized financial assets that (a) are of high credit quality (e.g., guaranteed by the US government, its agencies, or other creditworthy guarantors, and loans or securities sufficiently collateralized to ensure that the possibility of credit loss is remote), and (b) cannot be contractually prepaid or otherwise settled in a manner that the holder would not recover substantially all of its recorded investment.

Basic postamendment unified approach to OTTI evaluations. The objective of the analysis as to whether an impairment is other-than-temporary is to determine whether it is probable that the holder will realize some portion of the unrealized loss on an impaired security. Under US GAAP, a holder may ultimately realize an unrealized loss on the impaired security because, for example

- It is probable that the holder will not collect all of the contractual or estimated cash flows, considering both their amount and timing, or

- The holder of the security lacks the intent and ability to hold it until recovery of the loss.

It is inappropriate for management to automatically conclude that, because all of the scheduled payments to date have been received, a security has not incurred an OTTI.

Conversely, it is also inappropriate for management to automatically conclude that every decline in fair value of a security represents OTTI.

The longer and/or the more severe the decline in fair value, the more persuasive the evidence that would be needed to overcome the premise that it is probable that the holder will not collect all of the contractual or estimated cash flows from the security.

Further analysis and the exercise of judgment are required to assess whether a decline in fair value indicates that it is probable that the holder will not collect all of the contractual or estimated cash flows from the security.

In performing the assessment of OTTI and developing estimates of future cash flows, the holder is to consider all information available that is relevant to collectibility, including information about past events, current conditions, and forecasts that are reasonable and supportable. This information should generally include:

- The remaining payment terms of the security,

- Prepayment speeds,

- The issuer's financial condition,

- Expected defaults,

- The value of the underlying collateral,

- Information regarding whether any interests subordinated to those of the holder are sufficient to absorb any estimated losses on the loans underlying the security,

- The effect, if applicable, of any credit enhancements on the expected performance of the security, including consideration of the current financial condition of a guarantor of the security.

NOTE: This applies only if the guarantee is not a separate contract. Per ASC 320-10-35-23, the holder is not to combine separate contracts (such as a debt security and a guarantee or other credit enhancement) for the purpose of the determination of impairment or the determination of whether the debt security can be contractually prepaid or otherwise settled in a manner that would preclude the holder from recovering substantially all of its cost.

Some or all of the securitized loans that comprise many beneficial interests may be structured with payment streams that are not level over the life of the loan. Thus, the remaining payments expected to be received from the security could differ significantly from those received in prior periods. These so-called “nontraditional” loans may have features such as:

- Terms permitting principal payment deferral (interest-only)

- Interest accruals exceeding the required payments (negative amortization or reverse mortgages)

- A high loan-to-value ratio

- Collateral applying to multiple loans that, when considered together, result in a high loan-to-value ratio

- Option adjustable rate mortgages (Option ARMs) or similar products that may expose the borrower to future increases in required payments

- An initial interest rate (“teaser rate”) below the market rate of interest for the initial period of the term of the loan that will increase significantly at the end of that initial period

- Interest-only loans

- Loans requiring a “balloon” payment at maturity.

In achieving this objective, the holder considers information such as:

- Reports and forecasts from industry analysts

- Sector credit ratings

- Other market data relevant to the collectibility of the security.

The existence of these or other features necessitates consideration by the holder of whether a security backed by loans that are currently performing will continue to perform when the contractual provisions of those loans require increasing payments on the part of the borrowers. In addition, the holder is to consider how the value of any collateral would affect the expected performance of the security. Naturally, if the fair value of the collateral has declined, the holder must assess the effect of the decline on the ability of the borrower to make the balloon payment since the decline in value may preclude the borrower from obtaining sufficient funds from a potential refinancing of the debt.

Timing of recognition of an OTTI. If management of the entity both holds an available-for-sale beneficial interest whose fair value is less than its amortized cost basis and does not expect the fair value to recover prior to an expected sale shortly after the date of the statement of financial position, a write-down for other-than-temporary impairment is to be recognized as a charge to net income in the period in which the decision to sell the beneficial interest is made.

1 This disclosure requirement does not impose an obligation on management to actively seek out new or updated information in order to update the assumptions used in determining the remaining life expectancy of the life settlement contracts.