Appendix Disclosure Checklist for Commercial Businesses

The disclosure checklist presented below provides a quick reference to those disclosures that are common to the financial statements of most commercial business enterprises. This checklist does not purport to be suitable for use as a comprehensive SEC disclosure checklist, nor is it designed to be used for reporting entities that are not-for-profit organizations, state or local governments, or that are engaged in other industries that are subject to specialized accounting and reporting rules. Readers are advised to access the FASB Codification for additional details on requirements.

Numbers preceding the topics refer to the relevant FASB ASC Topic. For each Topic, the related chapter in Wiley GAAP 2014 offers more information about implementing the requirements and gives examples.

CONTENTS

205 Presentation of Financial Statements

205-20 Discontinued Operations

205-30 Liquidation Basis of Accounting

225-20 Extraordinary and Unusual Items

235 Notes to Financial Statements

250 Accounting Changes and Error Corrections

270 Interim Financial Statements

310-20 Nonrefundable Fees and Other Costs

310-30 Loans and Debt Securities Acquired with Deteriorated Credit Quality

310-40 Troubled Debt Restructurings by Creditors

320 Investments—Debt and Equity

323 Investments—Equity Method and Joint Ventures

340 Other Assets and Deferred Costs

340-20 Capitalized Advertising Costs

340-30 Insurance Contracts That Do Not Transfer Insurance Risk

350 Intangibles—Goodwill and Other

350-30 General Intangibles Other than Goodwill

360 Property, Plant, and Equipment

405-40 Obligations Resulting from Joint and Several Liability Arrangements

410 Asset Retirement and Environmental Obligations

420 Exit or Disposal Cost Obligations

470-20 Debt with Conversion and Other Options

470-30 Participating Mortgage Loans

470-60 Troubled Debt Restructurings by Debtors

480 Distinguishing Liabilities from Equity

505-20 Stock Dividends and Stock Splits

505-50 Equity-Based Payments to Non-Employees

605-25 Multiple Element Arrangements

605-35 Construction-Type and Production-Type Contracts

605-45 Principal Agent Considerations

605-50 Customer Payments and Incentives

712 Compensation—Nonretirement Postemployment Benefits

715 Compensation—Retirement Benefits

715-20 Defined Benefit Plans—General

715-60 Defined Benefit Plans—Other Postretirement

715-70 Defined Contribution Plans

718 Compensation—Stock Compensation

718-40 Employee Stock Ownership Plans (ESOP)

720-20 Other Expenses—Insurance Costs

720-35 Other Expenses—Advertising Costs

740-30 Income Taxes—Other Considerations or Special Areas

740-270 Income Taxes—Interim Reporting

805-20 Identifiable Assets and Liabilities and Any Noncontrolling Interest

805-30 Goodwill or Gain from Bargain Purchase

805-50 Business Combinations—Related Issues

808 Collaborative Arrangements

815-40 Contracts in Entity's Own Entity

830-20 Foreign Currency Transactions

830-30 Translation of Financial Statements

835 Interest—Capitalization of Interest

840-40 Sale-Leaseback Transactions

852-20 Reorganization—Quasi Reorganizations

860 Transfers and Servicing of Financial Assets

860-20 Sales of Financial Assets

860-30 Secured Borrowing and Collateral

860-50 Servicing Assets and Liabilities

915 Development Stage Entities

PRESENTATION

205 Presentation of Financial Statements

1. Full set of financial statements consists of:

| a. Financial position | _____ |

| b. Earnings for the period as a separate statement or within a continuous statement of comprehensive income | _____ |

| c. Comprehensive income | _____ |

| d. Cash flows | _____ |

| e. Investments by and distributions to owners during this period. | _____ |

(FASB ASC 205-10-45-1A)

| 2. Comparative statements of financial position, income, and changes in equity are preferable. | _____ |

(FASB ASC 205-10-45-2)

(FASB ASC 205-10-45-4)

| 8. Differences between “economic” entity and legal entity being presented should be noted (e.g., consolidated or not? subsidiaries included and excluded, combined statements?, etc.) Disclose summarized financial information for previously unconsolidated subsidiaries. | _____ |

| 9. Identify new accounting principles not yet adopted and expected impact of adoption. | _____ |

| 10. For reclassifications or other reasons, changes have occurred in the manner or basis of presenting corresponding items in two or more periods, disclose the explanation of the change. | _____ |

(FASB ASC 205-10-50-1)

205-20 Discontinued Operations

Assets Sold or Held for Sale

1. For assets (or disposal groups) either sold or reclassified from held-and-used to held-for-sale during the period

| a. The facts and circumstances leading to the expected disposal, the expected manner and timing of the disposal, and if not separately presented on the face of the statement of financial position, the carrying amounts of the major classes of assets and liabilities included as part of the disposal group. | _____ |

| b. Gain or loss recognized for initial or subsequent write-downs to fair value less cost to sell, and, if not separately stated, the income statement caption in which included. | _____ |

| c. Amounts of revenue and pretax profit or loss reported as discontinued operations, if applicable. | _____ |

| d. If applicable, the segment in which the long-lived asset (disposal group) is reported under Topic 280. | _____ |

(FASB ASC 205-20-50-1)

Long-Lived Asset of Disposal Group Classified as Held for Sale

| 2. In the period of disposal, the major classes of assets and liabilities classified as held for disposal (either on the face of the income statement or in the notes to the financial statements). | _____ |

(FASB ASC 205-20-50-2)

3. For assets (or groups) reclassified from held-for-sale to held-and-used during the period, including the removal of individual assets or liabilities from a disposal group to be sold,

| a. The facts and circumstances leading to the decision to change the plan to sell the long-lived asset (disposal group). | _____ |

| b. The effect of the changed decision on the results of operations for the period in which the decision was made and any prior periods presented. | _____ |

(FASB ASC 205-20-50-3)

Continuing Cash Flows

4. For each discontinued operation that generates continuing cash flows:

| a. The nature of the activities that give rise to continuing cash flows. | _____ |

| b. The period of time continuing cash flows are expected to be generated. | _____ |

| c. The principal factors used to conclude that the expected continuing cash flows are not direct cash flows of the disposed component. | _____ |

(FASB ASC 205-20-50-4)

Adjustments to Previously Reported Amounts

| 5. The nature and amount of adjustments to amounts previously reported in discontinued operations that are directly related to the disposal of a component of an entity in a prior period. | _____ |

(FASB ASC 205-20-50-5)

Continuing Involvement by Ongoing Entity

| 6. In the period in which the discontinued operations are initially classified and for each discontinued operation in which the ongoing entity will engage in a continuation of activities after disposal and for which revenues and expenses that were intra-entity transactions are included in revenue, disclose those intra-entity amounts and the types of continuing involvement. | _____ |

(FASB ASC 205-20-50-6)

205-30 Liquidation Basis of Accounting

Note: The requirements of 205-30 are effective for December 15, 2013

| 1. Disclose information requited by other Topics relevant to understanding the statement of net assets in liquidation and statement of changes in net assets in liquidation, informing readers about the amount of cash or other consideration that the entity expects to collect and the amount that the entity is obligated or expects to be obligated to pay during the course of liquidation. | _____ |

(FASB ASC 205-30-50-1)

2. Disclose all of the following when for financial statements using the liquidation basis of accounting:

(FASB ASC 205-30-50-2)

210 Balance Sheet

The amounts at which current assets supplemented by information that reveals, for the various classifications of inventory items, the basis upon which their amounts are stated and, where practicable, indication of the method of determining the cost—for example, average cost, first-in first-out (FIFO), last-in first-out (LIFO), and so forth.

(FASB ASC 210-10-50-1)

210-20 Offsetting

1. The following disclosures for 210-20 are effective January 1, 2013. They apply to both of the following:

| a. Recognized derivative instruments that are offset in accordance with either Section 210-20-45 or Section 815-10-45. | _____ |

| b. Recognized derivative instruments that are subject to an enforceable master netting arrangement or similar agreement, irrespective of whether they are offset in accordance with either Section 210-20-45 or Section 815-10-45. | _____ |

(FASB ASC 210-20-50-1)

| 2. Information to enable financial statements users to evaluate the effect or potential effect of netting arrangements on its financial position. This includes the effect or potential effect of rights of setoff associated with an entity's recognized assets and recognized liabilities that are in the scope of ASC 210-20-50-1. | _____ |

(FASB ASC 210-20-50-2)

3. At the end of the reporting period the following quantitative information separately for assets and liabilities that are within the scope of paragraph 210-20-50-1:

| a. The gross amounts of those recognized assets and those recognized liabilities | _____ |

| b. The amounts offset in accordance with the guidance in Sections 210-20-45 and 815-10-45 to determine the net amounts presented in the statement of financial position | _____ |

| c. The net amounts presented in the statement of financial position | _____ |

| d. The amounts subject to an enforceable master netting arrangement or similar agreement not otherwise included in (b):

|

|

| e. The net amount after deducting the amounts in (d) from the amounts in (c). | _____ |

(FASB ASC 210-20-50-3)

| 4. Presented the information required above in a tabular format, separately for assets and liabilities, unless another format is more appropriate. The total amount disclosed in accordance with paragraph 210-20-50-3(d) for an instrument should not exceed the amount disclosed in accordance with paragraph 210-20-50-3(c) for that instrument. | _____ |

(FASB ASC 210-20-50-4)

5. A description of the rights of setoff associated with an entity's recognized assets and recognized liabilities subject to an enforceable master netting arrangement or similar agreement disclosed in accordance with paragraph 210-20-50-3(d), including the nature of those rights.

(FASB ASC 210-20-50-5)

225 Income Statement

225-20 Extraordinary and Unusual Items

1. Present descriptive captions and the amounts for individual extraordinary events or transactions, preferably on the face of the income statement, if practicable; otherwise disclosure in related notes is acceptable. Describe the nature of an extraordinary event or transaction and the principal items entering into the determination of an extraordinary gain or loss. Disclose the income taxes applicable to extraordinary items on the face of the income statement; alternatively, disclosure in the related notes is acceptable.

(FASB 225-20-45-11)

2. Present earnings per share information related to extraordinary items either on the face of the income statement or in the notes.

(FASB ASC 225-20-45-12)

3. Each adjustment in the current period of an element of an extraordinary item that was reported in a prior period shall be separately disclosed as to year of origin, nature, and amount.

(FASB ASC 225-20-50-2)

Unusual or Infrequent Items

4. Disclose the nature and financial effects of each event or transaction on the face of the income statement or, alternatively, in notes to financial statements.

(FASB ASC 225-20-50-3)

230 Statement of Cash Flows

| 1. Policy for determining which items are treated as cash equivalents | _____ |

(FASB ASC 230-10-50-1)

| 2. Disclose both interest and income taxes paid in a schedule following the statement or in the notes, if the indirect method of reporting net cash flows from operating activities is used. | _____ |

(FASB ASC 230-10-50-2)

| 3. Information about all investing and financing activities of an entity during a period that affect recognized assets or liabilities but that do not result in cash receipts or cash payments in the period shall be disclosed. Those disclosures may be either narrative or summarized in a schedule, and they shall clearly relate the cash and noncash aspects of transactions involving similar items. | _____ |

(FASB ASC 230-10-50-3)

| 4. Examples of noncash investing and financing transactions are converting debt to equity; acquiring assets by assuming directly related liabilities, such as purchasing a building by incurring a mortgage to the seller; obtaining an asset by entering into a capital lease; obtaining a building or investment asset by receiving a gift; and exchanging noncash assets or liabilities for other noncash assets or liabilities. | _____ |

(FASB ASC 230-10-50-4)

| 5. Some transactions are part cash and part noncash; only the cash portion shall be reported in the statement of cash flows. | _____ |

(FASB ASC 230-10-50-5)

| 6. If there are only a few such noncash transactions, it may be convenient to include them on the same page as the statement of cash flows. Otherwise, the transactions may be reported elsewhere in the financial statements, clearly referenced to the statement of cash flows. | _____ |

(FASB ASC 230-10-50-6)

235 Notes to Financial Statements

1. Identify and describe significant accounting principles followed and methods of applying them that materially affect statements; disclosures should include principles and methods that involve

| a. Selection from acceptable alternatives. | _____ |

| b. Principles and methods peculiar to the company's industry. | _____ |

| c. Unusual or innovative applications of generally accepted accounting principles. | _____ |

(FASB ASC 235-10-50-3)

2. Among others, common accounting policies are:

| a. Basis of consolidation | _____ |

| b. Depreciation methods | _____ |

| c. Amortization of intangibles | _____ |

| d. Inventory pricing | _____ |

| e. Accounting for recognition of profit on long-term construction-type contracts | _____ |

| f. Recognition of revenue from franchising and leasing operation | _____ |

| g. Use of estimates | _____ |

| h. Cash equivalents | _____ |

| i. Impairment | _____ |

| j. Property | _____ |

| k. Interperiod tax allocation. | _____ |

(FASB ASC 235-10-50-4)

| 3. Accounting policies disclosures do not duplicate details presented elsewhere. It may be appropriate to refer to related details presented elsewhere in the financial statements. | _____ |

(FASB ASC 235-10-50-5)

| 4. Location of accounting policies may be flexible, but it is preferable to disclose significant accounting policies in a separate summary preceding the notes to financial statements, or as the initial note, under the same or a similar title. | _____ |

(FASB ASC 235-10-50-6)

250 Accounting Changes and Error Corrections

Change in Accounting Principle

1. Nature and justification of change in accounting principle

| a. The nature of and reasons for making the change, addressing preferability of the newly adopted principle. | _____ |

| b. Descriptions of prior period items that have been restated. | _____ |

| c. The effects of the change for both current period and prior period(s) being presented; specific quantification of the effects on income from continuing operations, net income, any other financial statement caption materially affected, and corresponding per-share amounts for each. | _____ |

| d. The cumulative effect on retained earnings at the beginning of the earliest period's financial statements presented. | _____ |

| e. As of the beginning of the earliest statement presented, the cumulative effect of the change in retained earnings or other components of equity or net assets in the statement of financial position. | _____ |

| f. If ASC 250 requirement to restate prior periods is not adhered to, based on impracticability criterion, explain and provide details regarding method of accounting applied. | _____ |

| g. When indirect effects of change in accounting principle are included, describe these effects and state the amounts recognized in the current reporting period, together with per-share amounts. If possible, also state the indirect effects of the change in each of the prior periods being presented. | _____ |

(FASB ASC 250-10-50-1)

| 2. For interim reports after the date of adoption of a new accounting principle, the effect of the change on income from continuing operations, net income (or other appropriate captions of changes in the applicable net assets or performance indicator), and related per-share amounts, if applicable, for those post-change interim periods. | _____ |

(FASB ASC 250-10-50-3)

Change in Accounting Estimate

| 3. For a change in accounting estimate, if the change affects several future periods (e.g., for change in useful lives of fixed assets), disclose the effect on income from continuing operations and net income of current period (and related per-share amounts). For a change in estimate not having material effect in the current period, but which is deemed likely to have material effects on later periods, describe the change. | _____ |

(FASB ASC 250-10-50-4)

| 4. For change in reporting entity, nature of change and reason for it; also, effect of change on income before extraordinary items, net income, and comprehensive income for all periods presented (also per-share amounts). For a change in entity not having material effect currently but anticipated to have such effect in later periods, the nature of the change and reason the change was made. | _____ |

(FASB ASC 250-10-50-6)

Correction of an Error in Previously Issued Financial Statements

| 5. For the correction of an error, disclose that the previously issued statements have been reissued and the nature of the error in previously issued statements and the effect of its correction on each financial statement line item (only in period of discovery and correction), with per-share equivalents. Also, the cumulative effect on retained earnings or other appropriate components of equity or net assets. | _____ |

(FASB ASC 250-10-50-7)

| 6. The effects (both gross and net of applicable income tax) of prior period adjustments on the net income of prior periods in the annual report for the year in which the adjustments are made and in interim reports issued during that year after the date of recording the adjustments. | _____ |

(FASB ASC 250-10-50-8)

| 7. For single period only financial statements, indicate the effects of such restatement on the balance of retained earnings at the beginning of the period and on the net income of the immediately preceding period. For financial statements for more than one period are presented, the effects for each of the periods included in the statements. Include the amounts of income tax applicable to the prior period adjustments. Disclosure of restatements in annual reports issued after the first such post-revision disclosure would ordinarily not be required. | _____ |

(FASB ASC 250-10-50-9)

Error Corrections Related to Prior Interim Periods of the Current Fiscal Year

| 8. The effect on income from continuing operations, net income, and related per-share amounts for each prior interim period of the current fiscal year and income from continuing operations, net income, and related per-share amounts for each prior interim period restated in accordance with paragraph 250-10-45-26. | _____ |

(FASB ASC 250-10-50-11)

260 Earnings per Share

| 1. Earnings per-share amounts for income from continuing operations and net income, shown on the face of income statement for all periods presented. | _____ |

(FASB ASC 260-10-45-2)

| 2. If applicable, per-share amounts for discontinued operations, extraordinary items, and cumulative effect of an accounting change, presented either on face of income statement or in notes to financial statements. | _____ |

(FASB ASC 260-10-45-3)

3. For each income statement presented

| a. Reconciliation of the numerators and the denominators of the basic and diluted per-share computations for income from continuing operations. | _____ |

| b. Effect that has been given to preferred dividends in arriving at income available to common stockholders in computing basic EPS. | _____ |

| c. Securities (including those issuable pursuant to contingent stock agreements) that could potentially dilute basic EPS in the future that were not included in the computation of diluted EPS because to do so would have been antidilutive for the period(s) presented. | _____ |

(FASB ASC 260-10-50-1)

| 4. Amounts should be restated when stock dividends, splits, or reverses occur after close of period but before statements are issued with appropriate disclosure. | _____ |

(FASB ASC 260-10-50-2)

270 Interim Financial Information

1. Provide, at a minimum, the captions and disclosures required when publicly traded entities report summarized interim financial information. These required disclosures are

j. The following information regarding defined benefit pension plans and other defined benefit postretirement benefit plans, disclosed for interim statements that include an income statement:

| k. Information about the use of fair value to measure assets and liabilities recognized in the statement of financial position as required by ASC 820-10-50. | _____ |

| l. Information about derivative instruments required by ASC 815-10-50, 815-2050, 815-30-50, and 815-35-50. | _____ |

| m. The information about fair value of financial instruments as required by Section 825-10-50. | _____ |

| n. The information about certain investments in debt and equity securities as required by Sections 320-10-50 and 942-320-50. | _____ |

| o. The information about other-than-temporary impairments as required by Sections 320-10-50, 325-20-50, and 958-320-50. | _____ |

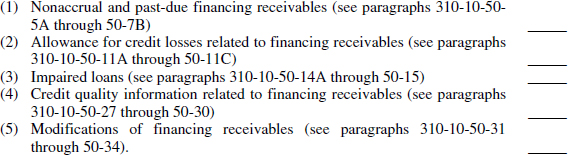

| p. All of the following information about the credit quality of financing receivables and the allowance for credit losses determined in accordance with the provisions of Topic 310:

|

|

| q. The gross information and net information required by paragraphs 210-20-50-1 through 50-6. | _____ |

r. The information about changes in accumulated other comprehensive income required by ASC 220-10-45-14A and ASC 220-10-45-17 through 45-17B.

If summarized financial data are regularly reported on a quarterly basis, the foregoing information with respect to the current quarter and the current year to date or the last 12 months to date should be furnished together with comparable data for the preceding year.

(FASB ASC 270-10-50-1)

| 2. In the absence of a separate fourth quarter report or disclosure of the results (as outlined in the preceding paragraph) for that quarter in the annual report, disclose disposals of components of an entity and extraordinary, unusual, or infrequently occurring items recognized in the fourth quarter, as well as the aggregate effect of year-end adjustments that are material to the results of that quarter (see paragraphs 270-10-05-2 and 270-10-45-10) in the annual report in a note to the annual financial statements. If a publicly traded company that regularly reports interim information makes an accounting change during the fourth quarter of its fiscal year and does not report the data specified by the preceding paragraph in a separate fourth quarter report or in its annual report, make the disclosures about the effect of the accounting change on interim periods that are required by paragraphs 270-10-45-12 through 4514 or by paragraph 250-10-45-15, as appropriate, in a note to the annual financial statements for the fiscal year in which the change is made. | _____ |

(FASB ASC 270-10-50-2)

| 3. Disclosure of the impact of the financial results for interim periods of the matters discussed in paragraphs 270-10-45-12 through 45-16 and 270-10-50-5 through 50-6 is desirable for as many subsequent periods as necessary to keep the reader fully informed. There is a presumption that users of summarized interim financial data will have read the latest published annual report, including the financial disclosures required by generally accepted accounting principles (GAAP) and management's commentary concerning the annual financial results, and that the summarized interim data will be viewed in that context. In this connection, management is encouraged to provide commentary relating to the effects of significant events upon the interim financial results. | _____ |

(FASB ASC 270-10-50-3)

| 4. Publicly traded companies are encouraged to publish balance sheet and cash flow data at interim dates since these data often assist users of the interim financial information in their understanding and interpretation of the income data reported. If condensed interim balance sheet information or cash flow data are not presented at interim reporting dates, significant changes since the last reporting period with respect to liquid assets, net working capital, long-term liabilities, or stockholders' equity shall be disclosed. | _____ |

(FASB ASC 270-10-50-4)

| 5. Extraordinary items shall be disclosed separately and included in the determination of net income for the interim period in which they occur. In determining materiality, extraordinary items shall be related to the estimated income for the full fiscal year. In addition, matters such as unusual seasonal results, business combinations, and acquisitions by not-for-profit entities shall be disclosed to provide information needed for a proper understanding of interim financial reports. | _____ |

(FASB ASC 270-10-50-5)

| 6. Contingencies and other uncertainties that could be expected to affect the fairness of presentation of financial data at an interim date shall be disclosed in interim reports in the same manner required for annual reports. Such disclosures shall be repeated in interim and annual reports until the contingencies have been removed, resolved, or have become immaterial. The significance of a contingency or uncertainty should be judged in relation to annual financial statements. Disclosures of such items shall include, but not be limited to, those matters that form the basis of a qualification of an independent auditor's report. | _____ |

(FASB ASC 270-10-50-6)

7. The following may not represent all references to interim disclosure:

| a. For business combinations and combinations accounted for by not-for-profit entities, see Sections 805-10-50, 805-20-50, 805-30-50, 805-740-50, and 958-805-50. | _____ |

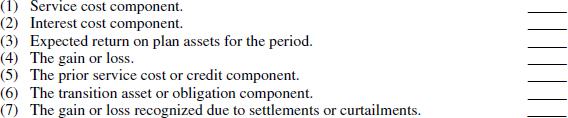

| b. For compensation-related costs, see paragraphs 715-60-50-3 and 715-60-50-6 | _____ |

| c. For disclosures required for entities with oil- and gas-producing activities, see paragraph 932-270-50-1. | _____ |

| d. For disclosures related to prior interim periods of the current fiscal year, see paragraph 250-10-50-11. | _____ |

| e. For fair value requirements, see Section 820-10-50. | _____ |

| f. For guarantors, see Section 460-10-50. | _____ |

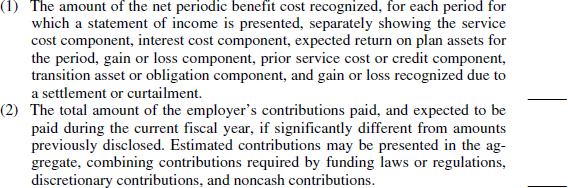

| g. For pensions and other postretirement benefits, see paragraphs 715-20-50-6 through 50-7. | _____ |

| h. For reportable segments, see paragraphs 280-10-50-39 and 280-10-55-16. | _____ |

| i. For suspended well costs and interim reporting, see Section 932-235-50. | _____ |

| j. For applicability of disclosure requirements related to risks and uncertainties, see paragraph 275-10-15-3. | _____ |

(FASB ASC 270-10-50-7)

275 Risks and Uncertainties

| 1. Nature of operations including description of major products, services, principal markets served locations, and relative importance of operations in various businesses and basis for determination of relative importance (e.g., sales volume, profits, etc.). Convey relative importance, but disclosures need not be quantified. | _____ |

(FASB ASC 275-10-50-2)

| 2. Explanation that the preparation of financial statements requires the use of management's estimates. | _____ |

(FASB ASC 275-10-50-4)

| 3. Significant estimates used in the determination of the carrying amounts of assets or liabilities or in the disclosure of gain or loss contingencies when, based on information known to management prior to issuance of the financial statements, it is at least reasonably possible that the effect on the financial statements of a condition or situation existing at the statement of financial position date for which an estimate has been made will change in the near term due to one or more future confirming events. (If the estimate involves a loss contingency covered by ASC 450, include an estimate of the possible loss or range of loss, or state such estimate cannot be made.) Indicate the nature of the uncertainty and that it is at least reasonably possible that a change in estimate may occur in the near term. | _____ |

(FASB ASC 275-10-50-6 through 9)

| 4. Vulnerability because of concentrations in the volume of business with a particular customer, supplier, or lender; revenue from particular products or services; available sources of supply of materials, labor, or other inputs; and market or geographic area. (For concentrations of labor subject to collective bargaining agreements, disclose both the percentage of the labor force covered by a collective bargaining agreement and the percentage of the labor force covered by a collective bargaining agreement that will expire within one year. For concentrations of operations located outside of the entity's home country, disclose the carrying amounts of net assets and the geographic areas in which they are located.) | _____ |

(FASB ASC 275-10-50-16 through 21)

280 Segment Reporting

1. General information on segments including

| a. Factors used to identify the enterprise's reportable segments, including the basis of organization (e.g., whether management has chosen to organize the enterprise around differences in products and services, geographic areas, regulatory environments, or a combination of factors and whether operating segments have been aggregated). | _____ |

| b. Types of products and services from which each reportable segment derives its revenues. | _____ |

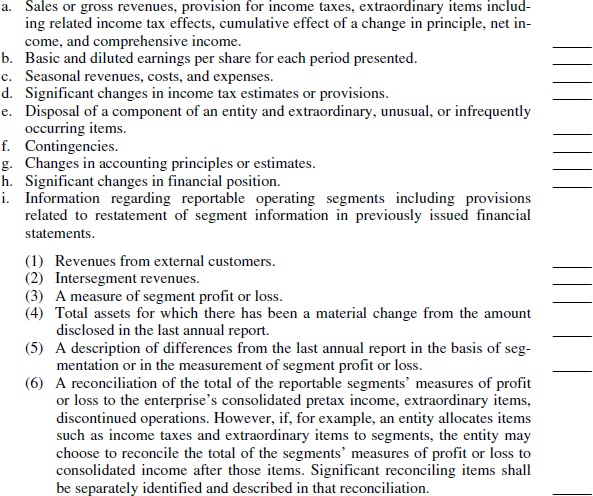

(FASB ASC 280-10-50-21)

2. The following about each reportable segment if the specified amounts are included in the measure of segment profit or loss reviewed by the chief operating decision maker:

| a. Revenues from external customers. | _____ |

| b. Revenues from transactions with other operating segments of the same enterprise. | _____ |

| c. Interest revenue. | _____ |

| d. Interest expense. | _____ |

| e. Depreciation, depletion, and amortization expense. | _____ |

| f. Unusual items. | _____ |

| g. Equity in the net income of investees accounted for by the equity method. | _____ |

| h. Income tax expense or benefit. | _____ |

| i. Extraordinary items. | _____ |

| j. Significant noncash items other than depreciation, depletion, and amortization expense. | _____ |

(FASB ASC 280-10-50-22)

| 3. Interest revenue and interest expense included in reported segment profit or loss is intended to provide information about the financing activities of a segment. | _____ |

(FASB ASC 280-10-50-23)

| 4. If a segment has no or only immaterial financial operations, no information about interest is required. For segments that are primarily a financial operation where interest revenue probably constitutes most of segment revenues and interest expense constitutes most of the difference between reported segment revenues and reported segment profit or loss, disclose interest revenue separately from interest expense. | _____ |

(FASB ASC 280-10-50-24)

5. Disclose the following about each reportable segment if the specific amounts are included in the determination of segment assets reviewed by the chief operating decision maker:

| a. The amount of investment in equity method investees. | _____ |

| b. Total expenditures for additions to long-lived assets other than financial instruments, long-term customer relationships of a financial institution, mortgage and other servicing rights, deferred policy acquisition costs, and deferred tax assets. | _____ |

(FASB ASC 280-10-50-25)

| 6. If no asset information is provided for a reportable segment, disclose that fact and the reason. | _____ |

(FASB ASC 280-10-50-26)

7. An explanation should be provided of the measurements of segment profit or loss and segment assets for each reportable segment; at a minimum, these shall include the following:

| a. The basis of accounting for any transactions between reportable segments. | _____ |

| b. The nature of any differences between the measurements of the reportable segments' profits or losses and the company's consolidated income before income taxes, extraordinary items, discontinued operations, and the cumulative effect of changes in accounting principles (if not apparent from the reconciliations); for example, accounting policies and policies for allocation of centrally incurred costs that are necessary for an understanding of the reported segment information. | _____ |

| c. The nature of any differences between the measurements of the reportable segments' assets and the company's consolidated assets (if not apparent from the reconciliations); for example, accounting policies and policies for allocation of jointly used assets that are necessary for an understanding of the reported segment information. | _____ |

| d. The nature of any changes from prior periods in the measurement methods used to determine reported segment profit or loss and the effect, if any, of those changes on the measure of segment profit or loss. | _____ |

| e. The nature and effect of any asymmetrical allocations to segments; for example, an enterprise might allocate depreciation expense to a segment without allocating the related depreciable assets to that segment. | _____ |

(FASB ASC 280-10-50-29)

8. Reconciliations of the totals of segment revenues, reported profit or loss, assets, and other significant items to corresponding company amounts, as follows:

| a. The total of the reportable segments' revenues to the enterprise's consolidated revenues. | _____ |

| b. The total of the reportable segments' measures of profit or loss to the company's consolidated income before income taxes, extraordinary items, discontinued operations, and the cumulative effect of changes in accounting principles. | _____ |

| c. The total of the reportable segments' assets to the company's consolidated assets. | _____ |

| d. The total of the reportable segments' amounts for every other significant item of information disclosed to the corresponding consolidated amount. | _____ |

(FASB ASC 280-10-50-30)

| 9. Identify and describe separately all significant reconciling items. | _____ |

(FASB ASC 280-10-50-31)

10. For a public entity disclose all of the following about each reportable segment in condensed financial statements of interim periods:

| a. Revenues from external customers | _____ |

| b. Intersegment revenues | _____ |

| c. A measure of segment profit or loss | _____ |

| d. Total assets for which there has been a material change from the amount disclosed in the last annual report | _____ |

| e. A description of differences from the last annual report in the basis of segmentation or in the basis of measurement of segment profit or loss | _____ |

| f. A reconciliation of the total of the reportable segments' measures of profit or loss to the public entity's consolidated income before income taxes, extraordinary items, and discontinued operations. However, if a public entity allocates items such as income taxes and extraordinary items to segments, the public entity may choose to reconcile the total of the segments' measures of profit or loss to consolidated income after those items. Significant reconciling items shall be separately identified and described in that reconciliation. | _____ |

(FASB ASC 280-10-50-32)

| 11. Interim disclosures are required for the current quarter and year-to-date amounts. Paragraph 270-10-50-1 states that when summarized financial data are regularly reported on a quarterly basis, the information in the previous paragraph with respect to the current quarter and the current year to date or the last 12 months to date should be furnished together with comparable data for the preceding year. | _____ |

(FASB ASC 280-10-50-33)

| 12. If revenues from transaction with a single external customer amount to ten percent or more of an enterprise's revenues, disclose that fact, the total amount of revenues from each such customer, and the identity of the segment or segments reporting the revenues. | _____ |

(FASB ASC 280-10-50-42)

| 13. Depreciation and amortization expense for each reportable segment, when the chief operating decision maker evaluates the performance of its segments based on earnings before interest, taxes, depreciation, and amortization. | _____ |

ASSETS

310 Receivables

| 1. Basis of accounting for loans and trade receivables | _____ |

| 2. Method used in determining the lower of cost or fair value of nonmortgage bonds held for sale | _____ |

| 3. Classification and method of accounting for interest-only strips, loans, other receivables or retained interests in securitizations that can contractually be prepaid or otherwise settled in a way that the holder would not recover substantially all of its recorded investment | _____ |

| 4. Methods for recognizing interest income on load and trade receivables. | _____ |

(FASB ASC 310-10-50-2)

For loans and trade receivables:

| 5. Separately report each major category of loans and trade receivables either on the face of the statement of financial position or in the notes. | _____ |

(FASB ASC 310-10-50-3)

| 6. State the allowance for doubtful accounts or credit losses and any unearned income, unamortized premiums or discounts, and any net unamortized deferred fees and costs. | _____ |

(FASB ASC 310-10-50-4)

| 7. Except for credit card receivables, disclose the policy for charging off uncollectible trade accounts receivable that have a contractual maturity of one year or less and that arose from the sale of goods or services. | _____ |

(FASB ASC 310-10-50-4A)

| 8. The carrying amount of financial instruments that serve as collateral for borrowings. (See also 860-30-50-1A) | _____ |

(FASB ASC 310-10-50-5)

| 9. By class of financing receivable, with some exceptions (FASB ASC 310-10-50-5b) accounting policies for financing receivables, including policies related to nonaccrual status, for recording payments received on nonaccrual financing receivables, for resuming accrual of interest, and for determining past due or delinquent status. | _____ |

(FASB ASC 310-10-50-6)

10. For nonaccrual and past due financing receivables as of each balance sheet date:

| a. State the recorded investment in loans (and trade receivables, if applicable on nonaccrual status) | _____ |

| b. State the recorded investment in financing receivables past due 90 days or more and still accruing. | _____ |

(FASB ASC 310-10-50-7)

| 11. Present an analysis of the age of the recorded investment in financing receivables. | _____ |

(FASB ASC 310-10-50-7a)

12. Policies and methodology used to estimate liability for off-balance-sheet credit exposures and related charges for those credit exposures.

(FASB ASC 310-10-50-9)

| 13. The amount of foreclosed or repossessed assets, which can be included in the other assets category if the notes to the financial statements disclose the amount. | _____ |

(FASB ASC 310-10-50-11)

14. All of the following by portfolio segment:

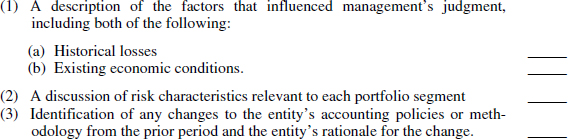

a. A description of the entity's accounting policies and methodology used to estimate the allowance for credit losses, including all of the following:

| b. A description of the policy for charging off uncollectible financing receivables | _____ |

| c. The activity in the allowance for credit losses for each period, including all of the following:

|

|

| d. The quantitative effect of changes identified in item (a)(3) on item (c)(2) | _____ |

| e. The amount of any significant purchases of financing receivables during each reporting period | _____ |

| f. The amount of any significant sales of financing receivables or reclassifications of financing receivables to held for sale during each reporting period | _____ |

| g. The balance in the allowance for credit losses at the end of each period disaggregated on the basis of the entity's impairment method | _____ |

| h. The recorded investment in financing receivables at the end of each period related to each balance in the allowance for credit losses, disaggregated on the basis of the entity's impairment methodology in the same manner as the disclosure in item (g). | _____ |

(FASB ASC 310-50-11B)

15. To disaggregate the information required by items (g) and (h) above on the basis of the impairment methodology, separately disclose:

| a. Amounts collectively evaluated for impairment (determined under Subtopic 450-20) | _____ |

| b. Amounts individually evaluated for impairment (determined under Section 310-10-35) | _____ |

| c. Amounts related to loans acquired with deteriorated credit quality (determined under Subtopic 310-30). | _____ |

(FASB ASC 310-10-50-11C)

| 16. For each class of financing receivable, for loans that are impaired, disclose the accounting for and the amount of impaired loans. | _____ |

(FASB ASC 310-10-50-14A)

17. For loans that meet the definition of an impaired loan by class of financing receivable:

| a. The recorded investment in the impaired loans and the amount for which there is a related allowance for credit losses, the amount of that allowance, and the amount of the investment for which there is no allowance for credit losses. | _____ |

| b. The total unpaid principal balance of the impaired loans. | _____ |

| c. The policy for recognizing interest income on impaired loans, including how cash receipts are recorded | _____ |

| d. The average recorded investment in the impaired loans | _____ |

| e. The related amount of interest income recognized during the time within that period that the loans were impaired | _____ |

| f. The amount of interest income recognized using a cash-basis method of accounting during the time within that period that the loans were impaired, if practicable. | _____ |

| g. The entity's policy for determining which loans the entity assesses for impairment | _____ |

| h. The factors considered in determining that the loan is impaired. | _____ |

(FASB ASC 310-10-50-15)

| 18. Disclose items in ASC 310-10-50-15 for impaired loans that have been charged off partially. | _____ |

(FASB ASC 310-10-50-16)

| 19. Information that enables financial statement users to understand how and to what extent management monitors the credit quality of its financing receivables in an ongoing manner assess the quantitative and qualitative risks arising from the credit quality of its financing receivables. | _____ |

(FASB ASC 310-10-50-28)

| 20. Provide quantitative and qualitative information by class about credit quality of financing receivables, including a description of the credit quality indicator, the recorded investment in financing receivables by credit quality indicator, and for each credit quality indicator, the date or range of dates in which the information was updated for that indicator. | _____ |

(FASB ASC 310-10-50-29)

| 21. If the entity discloses internal risk ratings, qualitative information on how those internal risk ratings relate to the likelihood of loss. | _____ |

(FASB ASC 310-10-50-30)

Modifications

22. For troubled debt restructurings of financing receivables that occurred during the period:

| a. By class of financing receivable, qualitative and quantitative information, including how the financing receivables were modified and the financial effects of the modifications | _____ |

| b. By portfolio segment, qualitative information about how such modifications are factored into the determination of the allowance for credit losses. | _____ |

(FASB ASC 310-10-50-33)

23. For financing receivables modified as troubled debt restructurings within the previous 12 months and for which there was a payment default during the period:

| a. By class of financing receivable, qualitative and quantitative information about those defaulted financing receivables, including types of financing receivables that defaulted and the amount that defaulted. | _____ |

| b. By portfolio segment, qualitative information about how such defaults are factored into the determination of the allowance for credit losses. | _____ |

(FASB ASC 310-10-50-34)

310-20 Nonrefundable Fees and Other Costs

| 1. The method for recognizing interest income on trade and loan receivables, including a statement about the entity's policy for treatment of related fees and costs, including the method of amortizing net deferred fees or costs. | _____ |

(FASB ASC 310-20-50-1)

| 2. If prepayments are anticipated in applying the interest method, the significant assumptions underlying the prepayment estimates. | _____ |

(FASB ASC 310-20-50-2)

| 3. The unamortized net fees and costs are reported as a part of each loan category. Additional disclosures such as unamortized net fees and costs may be included in the footnotes to the financial statements if the lender believes that such information is useful to the users of financial statements. | _____ |

(FASB ASC 310-20-50-3)

| 4. For credit card fees, the accounting policy for credit card fees, net amount capitalized at the balance sheet date, and the amortization period(s). | _____ |

(FASB ASC 310-20-50-4)

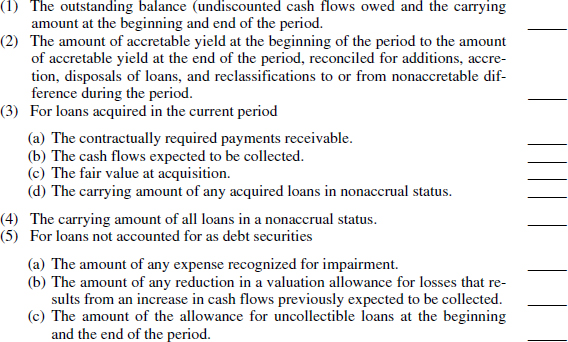

310-30 Loans and Debt Securities Acquired with Deteriorated Credit Quality

1. For certain loans or debt securities acquired with deteriorated credit quality, the following disclosures are required:

| a. How prepayments on loans receivable are considered in the determination of contractual cash flows and cash flows expected to be collected. | _____ |

(FASB ASC 310-30-50-1)

b. For loans acquired through purchase, including in a business combination, separately for loans accounted for as debt securities and for those not accounted for as debt securities

(FASB ASC 310-30-50-2)

310-40 Troubled Debt Restructurings by Creditors

| 1. In the body of the financial statements or in the accompanying notes, the amount of commitments, if any, to lend additional funds to debtors owing receivables whose terms have been modified in a troubled debt restructuring. | _____ |

(FASB ASC 310-40-50-1)

2. If both of the following conditions exist, it is not necessary to disclose information about an impaired loan that has been restructured in a troubled debt restructuring involving a modification of terms need not be included in the disclosures required by paragraphs 310-10-50-15(a) and 310-10-50-15(c) in years after the restructuring:

| a. The restructuring agreement specifies an interest rate equal to or greater than the rate that the creditor was willing to accept at the time of the restructuring for a new loan with comparable risk. | _____ |

| b. The loan is not impaired based on the terms specified by the restructuring agreement. | _____ |

(FASB ASC 310-40-50-2)

| 3. Apply consistently the exception in ASC 310-40-50-2 for paragraph 310-10-50-15(a) and 310-10-50-15(c) to all loans restructured in a troubled debt restructuring that meet the criteria in that paragraph. | _____ |

(FASB ASC 310-40-50-3)

| 4. For a loan whose terms are modified in a troubled debt restructuring and is already written and the measure of the restructured loan is equal to or greater than the recorded investment, no impairment would be recognized under ASC 310-40. Disclose the amount of the write-down and the recorded investment in the year of the write-down, but not in later years if the two criteria of paragraph 310-40-50-2 are met. | _____ |

(FASB ASC 310-40-50-4)

| 5. For a loan restructured in a troubled debt restructuring into two (or more) loan agreements, consider the restructured loans separately when assessing the applicability of the disclosures in paragraph 310-10-50-15 in years after the restructuring. | _____ |

(FASB ASC 310-40-50-5)

320 Investments—Debt and Equity

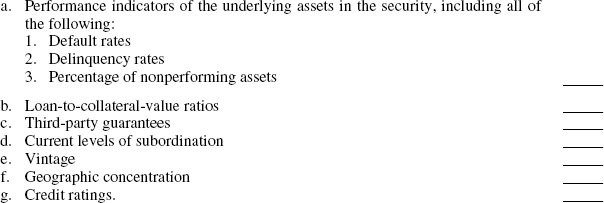

| 1. The disclosures for investments in debt and equity securities are required for all interim and annual periods. In determining whether disclosure for a particular security type is necessary and whether it is necessary to further separate a particular security type into greater detail, consider (shared) activity or business sector, vintage, geographic concentration, credit quality, and economic characteristic. | _____ |

(FASB ASC 320-10-50-1A and B)

2. For securities classified as available-for-sale, disclose by major security type as of each date for which a statement of financial position is presented.

| a. The amortized cost basis. | _____ |

| b. Aggregate fair value. | _____ |

| c. Total other-than-temporary impairment recognized in accumulated other comprehensive income. | _____ |

| d. Total gains for securities with net gains in accumulated other comprehensive income. | _____ |

| e. Total losses for securities with net losses in accumulated other comprehensive income. | _____ |

(FASB ASC 320-10-50-2)

3. Combined maturity information in appropriate groupings.

(FASB ASC 320-10-50-3)

4. For securities classified as held-to-maturity, by major security type as of each date for which a statement of financial position is presented

| a. Amortized cost basis. | _____ |

| b. Aggregate fair value. | _____ |

| c. Gross unrecognized holding gains. | _____ |

| d. Gross unrecognized holding losses. | _____ |

| e. Net carrying amount. | _____ |

| f. Total OTTI recognized in AOCI. | _____ |

| g. Gross gains and losses in AOCI for any derivatives that hedged the forecasted acquisition of the held-to-maturity securities. | _____ |

h. Information about the contractual maturities of those securities as of the date of the most recent statement of financial position presented. (Maturity information may be combined in appropriate groupings. In complying with this requirement, financial institutions [see paragraph 942-320-50-1] shall disclose the fair value and the net carrying amount (if different from fair value) of debt securities on the basis of at least the following four maturity groupings:

|

|

| May disclose separately securities not due at a single maturity date, such as mortgage-backed securities. If allocated, disclose the basis for allocation. | _____ |

(FASB ASC 320-10-50-5)

5. For SEC reporting—Substantial post-statement of financial position market decline.

Impairment of Securities

6. For all investments for which there is an unrealized loss where impairment has not been recognized because the loss is not considered “other than temporary”

| a. Quantitative disclosure in tabular form and aggregated by category of investment under ASC 320 and ASC 958-320, and cost-method investments, as of the date of each statement of financial position presented. | _____ |

NOTE: The disclosures in (1) and (2) below are to be segregated by those investments that have been in a continuous unrealized loss position for less than 12 months and those that have been in a continuous unrealized loss position for 12 months or longer.

![]()

| b. A narrative as of the date of the most recent statement of financial position that provides sufficient information to enable the reader of the financial statements to understand the disclosures in a. above, as well as both the positive and negative information that the investor considered in reaching the conclusion that the impairment is not other than temporary. | _____ |

NOTE: These disclosures may be aggregated by investment category; however, individually significant unrealized losses should not be aggregated.

Examples of relevant information that could be included in this narrative are

- The nature of the investments

- The causes(s) of the impairment(s)

- The number of investment positions in an unrealized loss position

- The severity and duration of the impairment(s)

| c. Other evidence considered by the investor in concluding that the impairment is not other than temporary (e.g., reports from industry analysts, sector credit ratings, volatility data regarding the fair value of the security, and/or any other relevant information that the investor considered). | _____ |

(FASB ASC 320-10-50-6 and 7)

7. The reference point for determining how long an investment has been in a continuous unrealized loss position is the balance sheet date of the reporting period in which the impairment is identified. For entities that do not prepare interim financial information, the reference point is the annual balance sheet date of the period during which the impairment was identified. The continuous unrealized loss position ceases upon either of the following:

| a. The recognition of the total amount by which amortized cost basis exceeds fair value as an other-than-temporary impairment in earnings | _____ |

| b. The investor becoming aware of a recovery of fair value up to (or beyond) the amortized cost basis of the investment during the period. | _____ |

(FASB ASC 320-10-5-8)

8. For interim and annual periods in which an other-than-temporary impairment of a debt security is recognized and only the amount related to a credit loss was recognized in earnings, an entity shall disclose by major security type, the methodology and significant inputs used to measure the amount related to credit loss. Examples of significant inputs include, but are not limited to, all of the following:

(FASB ASC 320-10-5-8A)

9. Disclose a tabular rollforward of the amount related to credit losses recognized in earnings in accordance with paragraph 320-10-35-34D, which including at a minimum:

| a. The beginning balance of the amount related to credit losses on debt securities held by the entity at the beginning of the period for which a portion of an other-than-temporary impairment was recognized in other comprehensive income | _____ |

| b. Additions for the amount related to the credit loss for which an other-than-temporary impairment was not previously recognized | _____ |

| c. Reductions for securities sold during the period (realized) | _____ |

| d. Reductions for securities for which the amount previously recognized in other comprehensive income was recognized in earnings because the entity intends to sell the security or more likely than not will be required to sell the security before recovery of its amortized cost basis | _____ |

| e. If the entity does not intend to sell the security and it is not more likely than not that the entity will be required to sell the security before recovery of its amortized cost basis, additional increases to the amount related to the credit loss for which an other-than-temporary impairment was previously recognized | _____ |

| f. Reductions for increases in cash flows expected to be collected that are recognized over the remaining life of the security (see paragraph 320-10-35-35) | _____ |

| g. The ending balance of the amount related to credit losses on debt securities held by the entity at the end of the period for which a portion of an other-than-temporary impairment was recognized in other comprehensive income. | _____ |

(FASB ASC 323-10-50-8B)

10. For sales, transfers, and related matters that occurred during the period:

| a. The proceeds from sales of available-for-sale securities and the gross realized gains and gross realized losses that have been included in earnings as a result of those sales. | _____ |

| b. The basis on which the cost of a security sold or the amount reclassified out of AOCI into earnings was determined. | _____ |

| c. The gross gains and gross losses included in earnings from transfers of securities from the available-for-sale category into the trading category. | _____ |

| d. The amount of the net unrealized holding gains or losses on available-for-sale securities for the period that are included in AOCI and the amount of gains and losses reclassified out of AOCI into earnings for the period. | _____ |

| e. The portion of trading gains and losses for the period that relates to trading securities still held at the reporting date. | _____ |

(FASB ASC 320-10-50-9)

11. For any sales/transfers from held-to-maturity classification, disclose

| a. Net carrying amount. | _____ |

| b. Net gain or loss in AOCI for any derivative that hedged the forecasted acquisition of the held-to-maturity security. | _____ |

| c. Realized or unrealized gain or loss. | _____ |

| d. Circumstances leading to decision to sell or transfer the security. (These transfers should be rare. See ASC 320-10-25-14 for the conditions under which sales of debt securities may be considered as maturities.) | _____ |

(FASB ASC 320-10-50-10 and 11)

323 Investments—Equity Method and Joint Ventures

| 1. If the investor has more than one investment in common stock, disclosures wholly or partly on a combined basis may be appropriate. Consider the significance of an investment to the investor's financial position and results of operations. | _____ |

(FASB ASC 323-10-50-2)

| 2. Name of each investee and the percentage of ownership of common stock. | _____ |

| 3. Accounting policies with respect to each of the investments. | _____ |

| 4. Difference between the carrying amount for each investment and its underlying equity in the investee's net assets and the accounting treatment of the difference between these amounts. | _____ |

| 5. For those investments which have a quoted market price, the aggregate value of each investment. | _____ |

| 6. If investments in corporate joint ventures or other investments accounted for under the equity method are considered to have a material effect on the investor's financial position and operating results, summarized data for the investor's assets, liabilities, and results of operations. | _____ |

| 7. If potential conversion of convertible securities and exercise of options and warrants would have material effects on the investor's percentage of the investee. | _____ |

(FASB ASC 323-10-50-3)

325 Investments—Other

Cost Method Investments

1. For investments valued using the cost method, as of the date of each statement of financial position presented in the annual financial statements

| a. The aggregate carrying amount of all investments valued using the cost method. | _____ |

| b. The aggregate carrying amount of cost-method investments not evaluated for impairment by the investor. | _____ |

| c. The fact that the fair value of a cost-method investment is not estimated by management if no events or changes in circumstances have been identified that potentially would have a significant adverse effect on the investment's fair value, and any of the following

|

|

(FASB ASC 325-20-50-1)

Investments in Insurance Contracts

| 2. If a policyholder, contractual restrictions on the ability to surrender a policy. | _____ |

(FASB ASC 325-30-50-1)

| 3. Accounting policy for life settlement contracts. including the classification of cash receipts and cash disbursements in statement of cash flows. | _____ |

(FASB ASC 325-30-50-2)

| 4. All of the following for life settlement contracts accounted for under the investment method based on the remaining life expectancy for each of the first five succeeding years from the date of the statement of financial position and thereafter, as well as in the aggregate: the number of life settlement contracts and their carrying value and the face value of underlying life insurance policies. | _____ |

(FASB ASC 325-30-50-4)

| 5. As of the date of the most recent statement of financial position, the life insurance premiums anticipated to be paid for each of the five succeeding fiscal years in order to keep the life settlement contracts in force. | _____ |

(FASB ASC 325-30-50-5)

| 6. The nature of new or updated information that causes the investor to change its expectations on the timing of the realization of proceeds from the investments in life settlement contracts. Include the information and the related effect on the timing of the realization of proceeds from the life settlement contracts. | _____ |

(FASB ASC 325-30-50-6)

| 7. The method and significant assumptions used to estimate the fair value of investments in life settlement contracts, including any mortality assumptions. | _____ |

(FASB ASC 325-30-50-7)

| 8. For life settlement contracts accounted for under the fair value method based on remaining life expectancy for each of the first five succeeding years from the date of the statement of financial position and thereafter, as well as in the aggregate: the number and carrying value of life settlement contracts and the face value (death benefits) of the life insurance policies underlying the contracts. | _____ |

(FASB ASC 325-30-50-8)

| 9. The reasons for changes in its expectation of the timing of the realization of the investments in life settlement contracts. | _____ |

(FASB ASC 325-30-50-9)

| 10. For each reporting period presented in the income statement, the gains or losses recognized during the period on investments sold during the period and the unrealized gains or losses recognized during the period on investments that are still held at the date of the statement of financial position. | _____ |

(FASB ASC 325-30-50-10)

330 Inventory

| 1. Change in basis of stating inventories and its effect. | _____ |

(FASB ASC 330-10-50-1)

| 2. Lower of cost or market “losses,” if material. | _____ |

(FASB ASC 330-10-50-2)

| 3. Goods stated above cost. | _____ |

(FASB ASC 330-10-50-3)

| 4. Inventories stated at sales price. | _____ |

(FASB ASC 330-10-50-4)

| 5. Amount of net losses on firm purchase commitments accrued under 330-10-35-1. | _____ |

(FASB ASC 330-10-50-5)

340 Other Assets and Deferred Costs

340-20 Capitalized Advertising Costs

| 1. a. The accounting policy selected from the two alternatives in paragraph 720-35-25-1 for reporting advertising, indicating whether such costs are expensed as incurred or the first time the advertising takes place | _____ |

| b. A description of the direct-response advertising reported as assets (if any), the accounting policy for it, and the amortization method and period | _____ |

| c. The total amount charged to advertising expense for each income statement presented, with separate disclosure of amounts, if any, representing a write-down to net realizable value | _____ |

| d. The total amount of advertising reported as assets in each balance sheet presented. | _____ |

(FASB ASC 340-20-50-1)

340-30 Insurance Contracts That Do Not Transfer Insurance Risk

| 1. A description of the contracts accounted for as deposits and the separate amounts of total deposit assets and total deposit liabilities reported in the statement of financial position. | _____ |

(FASB ASC 340-30-50-1)

| 2. Insurance entities—the changes in the recorded amount of the deposit arising from an insurance or reinsurance contract that transfers only significant underwriting risk. | _____ |

(FASB ASC 340-30-50-2)

350 Intangibles—Goodwill and Other

350-20 Goodwill

1. For goodwill, a reconciliation of changes in the carrying amount during the period, showing separately

| a. The gross amount and accumulated impairment losses at the beginning of the period. | _____ |

| b. Additional goodwill recognized during the period, except goodwill that is included in a disposal group that, upon acquisition, meets the criteria in ASC 360 to be classified as held for sale. | _____ |

| c. Adjustments resulting from the subsequent recognition of deferred tax assets during the period in accordance with ASC 805-740. | _____ |

| d. Goodwill included in a disposal group classified as held for sale in accordance with 360-10-45-9 and goodwill derecognized during the period without having previously been reported in a disposal group classified as held for sale. | _____ |

| e. Impairment losses recognized during the period. | _____ |

| f. Net foreign exchange differences arising during the period. | _____ |

| g. Any other changes in carrying amounts during the period. | _____ |

| h. The gross amount and accumulated impairment losses at the end of the period. | _____ |

For entities that report segment information in accordance with Topic 280, provide the above information about goodwill in total and for each reportable segment and disclose any significant changes in the allocation of goodwill by reportable segment. If any portion of goodwill has not yet been allocated to a reporting unit at the date the financial statements are issued, disclose that unallocated amount and the reasons for not allocating that amount.

(FASB ASC 350-20-50-1)

2. Goodwill impairment losses recognized during the period

| a. The facts and circumstances causing the impairment. | _____ |

| b. The amount of the impairment loss and the method of determining fair value of the associated reporting unit (whether based on quoted market prices; prices of comparable businesses; or present value or other valuation techniques; or a combination of these methods). | _____ |

| c. If the amount recognized is an estimate that has not yet been finalized, that fact and the reasons why the estimate is not yet complete. | _____ |

(FASB ASC 350-20-50-2)

| 3. The quantitative disclosures about significant unobservable inputs used in fair value measurements categorized within Level 3 of the fair value hierarchy required by paragraph 820-10-50-2(bbb) are not required for fair value measurements related to the financial accounting and reporting for goodwill after its initial recognition in a business combination. | _____ |

(FASB ASC 350-20-50-3)

350-30 General Intangibles Other Than Goodwill

1. For each major class of intangible asset, for each period-end for which a statement of financial position is presented:

a. For intangible assets subject to amortization, all of the following:

| (1) The total amount assigned and the amount assigned to any major intangible asset class | _____ |

| (2) The amount of any significant residual value, in total and by major intangible asset class | _____ |

| (3) The weighted-average amortization period, in total and by major intangible asset class. | _____ |

(FASB ASC 350-30-50-1a)

| b. For intangible assets not subject to amortization, the total carrying amount and the carrying amount for each major intangible asset class. | _____ |

(FASB ASC 350-30-50-1b)

| c. The amount of research and development assets acquired in a transaction other than a business combination or an acquisition by a not-for-profit entity and written off in the period and the line item in the income statement in which the amounts written off are aggregated. | _____ |

(FASB ASC 350-30-50-1c)

| d. For intangible assets with renewal or extension terms, the weighted-average period before the next renewal or extension (both explicit and implicit), by major intangible asset class. | _____ |

(FASB ASC 350-30-50-1d)

2.

| a. Gross carrying amount and accumulated amortization, in total and by major class of intangible asset. | _____ |

| b. Amortization expense for the period. | _____ |

| c. Estimated aggregate amortization expenses for each of the five succeeding fiscal years as of the date of the latest statement of financial position presented. | _____ |

(FASB ASC 350-30-50-2a)

| 3. For intangible asset not subject to amortization, the total carrying amount and the carrying amount for each major intangible asset class. | _____ |

(FASB ASC 350-30-50-2b)

| 4. The entity's accounting policy on the treatment of costs incurred to renew or extend the term of a recognized intangible asset. | _____ |

(FASB ASC 350-30-50-2c)

| 5. The entity's accounting policy on the treatment of costs incurred to renew or extend the term of a recognized intangible asset. | _____ |

(FASB ASC 350-30-50-6)

6. For intangible assets that have been renewed or extended in the period for which the statement of financial position is presented

| (1) For entities that capitalize renewal or extension costs, the total amount of costs incurred in the period to renew or extend the term of a recognized intangible asset, by major intangible asset class. | _____ |

| (2) The weighted-average period prior to the next renewal or extension (both explicit and implicit), by major intangible asset class. | _____ |

(FASB ASC 350-30-50-2d)

7. For each impairment loss recognized related to an intangible asset, the following disclosures are to be made in financial statements that include the period the loss is recognized:

| a. A description of the impaired intangible asset and the facts and circumstances that caused the impairment. | _____ |

| b. The amount of the impairment loss and the method used to determine fair value. | _____ |

| c. The caption of the income statement in which it is included. | _____ |

| d. If applicable, the segment in which the impaired intangible asset is reported under Topic 280. | _____ |

(FASB ASC 350-30-50-3)

| 8. A nonpublic entity is not required to disclose the quantitative information about significant unobservable inputs used in fair value measurements categorized within Level 3 of the fair value hierarchy required by paragraph 820-10-50-2(bbb) that relate to the financial accounting and reporting for an indefinite-lived intangible asset after its initial recognition. | _____ |

(FASB ASC 350-30-50-3A)

| 9. For a recognized intangible asset, information that enables users of financial statements to assess the extent to which the expected future cash flows associated with the asset are affected by the entity's intent and/or ability to renew or extend the arrangement. | _____ |

(FASB ASC 350-30-50-4)

360 Property, Plant, and Equipment

| 1. Depreciation expense for the period | _____ |

| 2. Balances of major classes of depreciable assets, by nature or function, at the balance sheet date | _____ |

| 3. Accumulated depreciation, either by major classes of depreciable assets or in total, at the balance sheet date | _____ |

| 4. A general description of the method or methods used in computing depreciation with respect to major classes of depreciable assets. | _____ |

(FASB ASC 360-10-50-1)

5. In the period in which an impairment loss is incurred:

| a. A description of the impaired long-lived asset (asset group) and the facts and circumstances leading to the impairment | _____ |

| b. If not separately presented on the face of the statement, the amount of the impairment loss and the caption in the income statement or the statement of activities that includes that loss | _____ |

| c. The method or methods for determining fair value (whether based on a quoted market price, prices for similar assets, or another valuation technique) | _____ |

| d. If applicable, the segment in which the impaired long-lived asset (asset group) is reported under Topic 280. | _____ |

(FASB ASC 360-10-50-2)

LIABILITIES

405-40 Obligations Resulting from Joint and Several Liability Arrangements

| 1. About each obligation, or each group of similar obligations, resulting from joint and several liability arrangements for which the total amount under the arrangement is fixed at the reporting date, the nature of the arrangement (including how the liability arose, the relationship with other co-obligors, terms and conditions of the arrangement); the total outstanding amount under the arrangement (not reduced by the effect of any amounts that may be recoverable from other entities); the carrying amount of the liability and the carrying amount of any receivable recognized; the nature of any recourse provisions that would enable recovery from other entities of the amounts paid, including any limitations on the amounts that might be recovered; in the period the liability is initially recognized and measured or in a period the measurement changes significantly, the corresponding entry and where the entry was recorded in the financial statements. | _____ |

(FASB ASC 405-40-50-2)

| 2. The disclosure requirements in this Section are incremental to related party disclosures required. | _____ |

(FASB ASC 405-40-50-2)

410 Asset Retirement and Environmental Obligations

Asset Retirement Obligations

| 1. General description of asset retirement obligations and the related long-lived assets. | _____ |

| 2. Fair value of assets, if any, that are legally restricted to satisfy the liability. | _____ |

| 3. Reconciliation of the beginning and ending aggregate carrying amount of the liability separately, whenever there is a significant change in any of these components during the reporting period, showing the changes resulting from | _____ |

(FASB ASC 410-20-50-1)

| 4. If the fair value of an asset retirement obligation cannot be reasonably estimated, that fact and the reasons therefor shall be disclosed. | _____ |

(FASB ASC 410-20-50-2)

Environmental Obligations

| 5. Whether the accrual for environmental remediation liabilities is measured on a discounted basis. If an entity utilizes present-value measurement techniques, additional disclosures are appropriate. See ASC 410-30-50-7. | _____ |

(FASB ASC 410-30-50-4)

| 6. With respect to recorded accruals for environmental remediation loss contingencies and assets for third-party recoveries related to environmental remediation obligations, disclose if any portion of the accrued obligation is discounted, the undiscounted amount of the obligation, and the discount rate used in the present-value determinations. | _____ |

(FASB ASC 410-30-50-7)

| 7. May include a contingency conclusion that addresses the estimated total unrecognized exposure to environmental remediation and other loss contingencies. | _____ |

(FASB ASC 410-30-50-14)

| 8. Optionally, a description of the general applicability and impact of environmental laws and regulations upon the business and how the laws and regulations may give rise to loss contingencies for future environmental remediation. | _____ |

(FASB ASC 410-30-50-17)

420 Exit or Disposal Cost Obligations

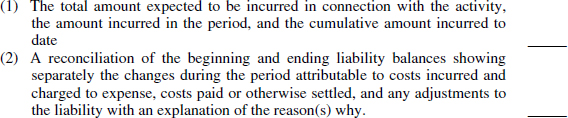

1. All of the following information shall be disclosed in notes to financial statements that include the period in which an exit or disposal activity is initiated and any subsequent period until the activity is completed:

| a. A description of the exit or disposal activity, including the facts and circumstances leading to the expected activity and the expected completion date | _____ |

| b. For each major type of cost associated with the activity (for example, one-time employee termination benefits, contract termination costs, and other associated costs), both of the following shall be disclosed:

|

|

| c. Line item(s) in the income statement or the statement of activities in which the costs in (b) are aggregated. | _____ |

| d. For each reportable segment, as defined in Subtopic 280-10, the total amount of costs expected to be incurred in connection with the activity, the amount incurred in the period, and the cumulative amount incurred to date, net of any adjustments to the liability with an explanation of the reason(s) why. | _____ |

| e. If a liability for a cost associated with the activity is not recognized because fair value cannot be reasonably estimated, that fact and the reasons why. | _____ |

(FASB ASC 420-10-50-1)

440 Commitments

1. All of the following:

| a. Unused letters of credit | _____ |

| b. Long-term leases | _____ |

| c. Assets pledged as security for loans | _____ |

| d. Pension plans | _____ |

| e. The existence of cumulative preferred stock dividends in arrears | _____ |

| f. Commitments, including a commitment for plant acquisition, and obligations to reduce debts, maintain working capital, and restrict dividends. | _____ |

(FASB ASC 440-10-50-1)

2. Unconditional purchase obligations are to be disclosed in accordance with FASB ASC 440-10-50-4 (if not recorded on the statement of financial position) or FASB ASC 440-10-50-6 (if recorded on the statement of financial position), if all the following criteria are met:

a. It is noncancelable, or cancelable only