RISKS AND CONTROLS IN THE CASH COLLECTION PROCESSES (STUDY OBJECTIVE 4, continued)

We now turn our attention to specific internal controls and related risks associated with cash collections from sales revenues. Some internal controls present within a cash receipts process are as follows.

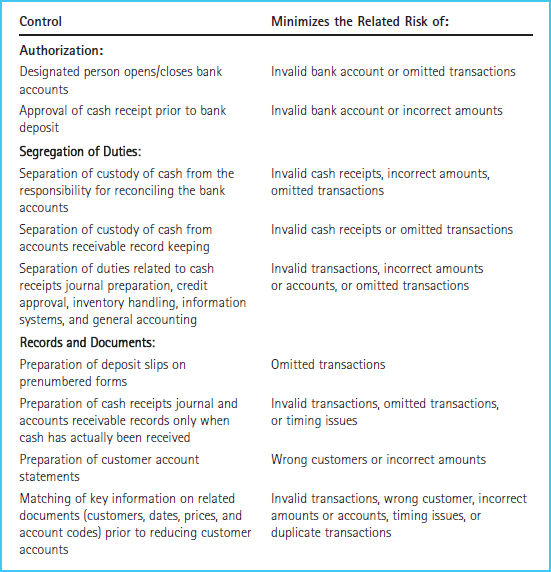

AUTHORIZATION OF TRANSACTIONS

Appropriate individuals should be assigned responsibility for opening and closing all bank accounts and approving bank deposits or electronic transfers of funds. This ensures that records are updated only for authorized transactions.

SEGREGATION OF DUTIES

As you know, authorization duties (described previously) need to be kept separate from recording and custody duties. Recording responsibilities include maintaining a cash receipts journal, updating accounts receivable records for individual customers, and posting subsidiary ledger totals to the general ledger. Custody responsibilities include opening mail, preparing a list of collections, handling receipts of currency and checks, and preparing bank deposits. At minimum, those who handle cash should not have the authority to access the company's cash or accounting records or reconcile the bank account. In addition, those with responsibility for information systems programming or control should not also have access to the cash or accounting records. Furthermore, anyone responsible for maintaining detailed records for daily cash receipts or accounts receivable subsidiary accounts should not also have access to the general ledger.

ADEQUATE RECORDS AND DOCUMENTS

Cash receipts listings should be prepared on a daily basis, so the daily activity of collections should be reconciled to supporting documentation from the bank deposit. Bank deposit receipts should be retained and filed chronologically, and regular, timely bank reconciliations should be prepared and retained. Detailed customer accounts should also be maintained and reconciled with customer statements regularly.

SECURITY OF ASSETS AND DOCUMENTS

Access to cash collections needs to be limited to those who are expressly authorized to handle cash. Controls over cash collections are likely the most important control procedure, because cash is the asset most susceptible to theft or misappropriation. Because of the universal appeal of cash and the difficulty of proving ownership, a company must take extra precautions to protect this asset. Cash collections should be deposited in the bank in a timely manner to prevent the risk of theft. Also, related computerized data files and programs must be protected from unauthorized use.

INDEPENDENT CHECKS AND RECONCILIATION

A physical count of cash needs to be conducted from time to time in order to compare actual cash on hand with the amounts in the accounting records. To maximize effectiveness, cash counts should occur on a surprise basis and be conducted by someone not otherwise responsible for any cash receipts functions. Daily bank deposits should also be compared with the detail on the related remittance advice and in the cash receipts journal.

In addition, it is important that companies regularly reconcile their cash accounts with the respective bank statements. Like cash counting procedures, a bank reconciliation should be performed by someone who has no other responsibility for handling cash or accounting for cash transactions. The bank statements should be received directly by the person who prepares the reconciliation, to make sure it is not altered by other company personnel. Among the bank reconciliation tasks are procedures to ensure that deposits are examined for proper dates and that all reconciling items are reviewed and explained.

COST-BENEFIT CONSIDERATIONS

In addition to the need for tight controls over cash due to its susceptibility to theft, the following circumstances may indicate risks related to cash collections:

- High volume of cash collections

- Decentralized cash collections

- Lack of consistency in the volume or source of collections

- Presence of cash collections denominated in foreign currencies

Companies often find that maximum internal controls are beneficial with respect to cash collections, due to the great temptation that exists for those in a position to steal cash and the high (and unrecoverable) cost of errors. Even a small company will tend to find ways to segregate duties and implement a variety of internal controls in order to protect its valuable cash. Exhibit 8-16 presents typical procedures used to control cash receipts and the risks that they help to reduce.

Exhibit 8-16 Cash Receipts Controls and Risks

In wrapping up the discussion of revenue-related accounting processes, it is important to mention an additional issue that may impact the accounting records related to cash collections for sales transactions. Namely, most companies have occasional problems with customers who fail to pay, leading to the write-off of accounts receivable and the recording of an allowance for uncollectible accounts. Companies should ensure that proper controls are in place to reduce risks related to transactions involving uncollectible accounts. Specifically, responsibilities should be segregated such that no one has the opportunity to write off customer accounts as a cover-up for stolen cash or inventory. In addition, since determining the amount of an allowance for uncollectible accounts is very subjective, it is important that thorough guidelines be established for this process. In order to properly monitor customer payments and determine the amount of an allowance for uncollectible accounts, an accounts receivable aging report should be generated to analyze all customer balances and the respective lengths of time that have elapsed since payments were due.