INTRODUCTION TO REVENUE PROCESSES (STUDY OBJECTIVE 1)

There are many kinds of companies selling many kinds of products and services. Because there is such a variety of types of companies and items for sale, and because there are so many methods of conducting revenue transactions, it is impossible to present an example of revenue and collection business processes that represents all possibilities. For instance, retailers may sell their products to consumers through company-owned department stores, using cash registers with bar coding systems called point of sale (POS) systems. These systems record the sale, collect cash, and update the inventory status all at the time of the sale. On the other hand, a manufacturer may sell products to other companies on 30-day credit terms, deliver the goods and bill the customer at a later date, and collect payment after the 30-day period.

The business processes for a company selling to other companies are likely to be different from a company selling products to consumers. An example of a company that sells to end consumers is Walmart, while an example of a company that sells to other companies is Procter & Gamble (P&G). P&G sells consumer products, such as Crest® toothpaste, to companies (like Walmart) who then resell to consumers. Walmart serves as the middle man who buys toothpaste from P&G and resells to consumers. The business processes that Walmart engages in to generate and collect revenue are much different from those of P&G. This chapter begins by describing a common set of revenue and cash collection processes for companies that sell goods to other companies. Business process maps, document flowcharts, and data flow diagrams are included as visual representations of the business activities. However, the processes illustrated and described in this chapter can focus only on common characteristics of such companies. Not all companies conduct business exactly as presented in this chapter.

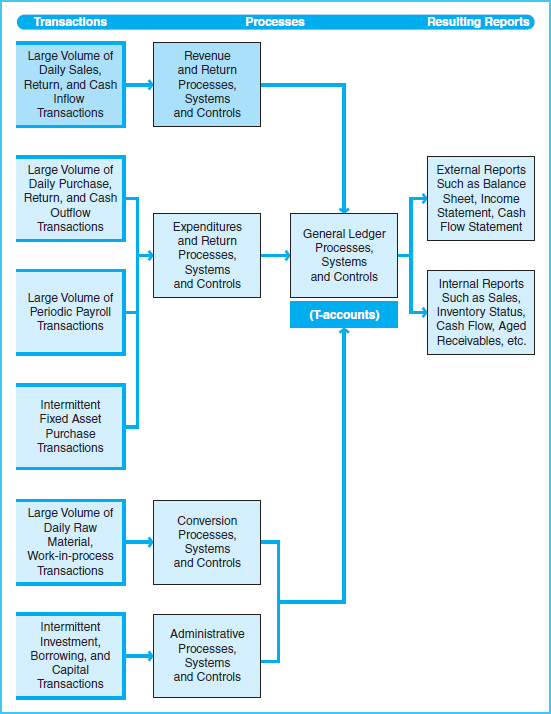

Exhibit 8-1 shows the revenue processes section of the overall accounting system that is the subject of this chapter. In a large company, there may be thousands or hundreds of thousands of sales transactions occurring each day. The company must have systems and processes in place to capture, record, summarize, and report the results of these transactions. The processes are the polices and procedures that employees follow in completing the sale, capturing customer data and sales quantities, and routing the resulting sales documents to the right departments within the company. The accounting system uses this flow of sales documents to various departments to record, summarize, and report the results of the sales transactions.

For example, when a sale occurs, the information resulting from that sale must flow into the sales recording systems, the accounts receivable and cash collection systems, and the inventory tracking systems. In IT accounting systems, these recording and processing systems are called transaction processing systems (TPS). Thus, there is a set of processes within the company to conduct sales transactions and handle the related sales information, and there is a TPS within the IT system to record, summarize, and report sales transactions.

Exhibit 8-1 Revenue Processes within the Overall System

Sales transactions that occur daily also generate other related transactions. Those transactions are the movement of inventory to customers, the recording of accounts receivable and the subsequent cash inflow, and sales returns from customers. Processes for each of these types of transactions must be in place for the company to carry out transactions on a daily basis. The business processes that are common in company-to-company sales transactions are as follows:

- Collect order data from the customer (another company, not the end-user consumer).

- Deliver goods, often via common carrier such as trucking company or rail carrier.

- Record the receivable and bill the customer.

- Handle any product returns from the customer and issue appropriate credit.

- Collect the cash.

- Update the records affected, such as accounts receivable, cash, inventory, revenue, and cost of goods sold.

These types of processes are divided into the following groups:

- Sales processes, including ordering, delivery, and billing

- Sales returns processes

- Cash collection processes

Although different companies conduct business differently, there tend to be similarities in the way they carry out related business processes. For instance, the sales processes generally involve receipt of a customer's order for products or services, delivery of the products or services, and billing the customer for those products or services. Sales processes also need supporting practices such as credit check and stock authorization. Most companies carry out these types of business transactions; however, the ways they do so are likely to differ. For instance, even though most companies collect order data from customers, the manner of receiving order data may vary. Orders may take the form of a mailed purchase order, a website order, or an EDI order.

Sales returns are an exception to the sales process; they are essentially a sale reversal that occurs when products are returned from customers. The sales return processes generally involve the receipt of goods and adjustment of customer accounts, inventory stock records, and other accounting reports.

Cash collections result from completed sales transactions. When cash is received from customers, it must be deposited in the bank. In addition, cash collection processes involve updating and reconciling cash and customer account balances.

The beginning part of this chapter describes common, simple methods of conducting business transactions within the revenue and cash collection processes. These descriptions are ordered according to the three categories explained earlier: sales, sales returns, and cash collections.

This chapter also considers the following risks that may affect the revenue and cash collection processes:

- Recorded transactions may not be valid or complete—that is, they may involve a fictitious customer, incorrect quantities or terms, or erroneous duplication.

- Transactions may be recorded in the wrong amount.

- Valid transactions may have been omitted from the records.

- Transactions may have been recorded in the wrong customer account.

- Transactions may not have been recorded in a timely manner.

- Transactions may not have been accumulated or transferred to the accounting records correctly.

The internal control procedures and IT controls that help lessen these risks are presented in exhibits following the discussion of each process category.

After describing the business processes for company-to-company transactions, the latter part of this chapter describes alternative business process models to generate and collect revenue. Examples include e-commerce or Web-based sales, EDI systems, and point of sale systems.