RISKS AND CONTROLS IN SALES PROCESSES (STUDY OBJECTIVE 2, continued)

Management should strive to achieve a system of internal controls, using both manual and programmed procedures to minimize the chance of error or fraud. Unfortunately, the existence of good internal controls is not necessarily related to financial success in terms of a company's ability to make money; internal controls do not ensure high sales and profits. However, effective and efficient internal controls may relieve managers of valuable time that might otherwise be spent on accounting or operational problems, thus making it possible for them to devote more attention to revenue growth and cost reduction.

In terms of the five internal control activities described in Chapter 3, following are common procedures associated with the sales process:

AUTHORIZATION OF TRANSACTIONS

Specific individuals within the company should have authoritative responsibility for establishing sales prices, payment terms, credit limits, and guidelines for accepting new customers. Only designated employees should perform these authorization functions. These specific people should have a recognized method of communicating when sales transactions have been authorized. For example, approval is often documented by a signature or initials on a sales order or shipping document. Such a signature indicates that a designated employee has verified that the sale is to an accepted customer, the customer's credit has been approved (i.e., it has not exceeded its credit limit), and the price is correct. Once a sales order has been filled, established procedures should be in place for verifying that the shipment represents items ordered. Thus, proper sales authorization control includes obtaining approval prior to processing an order and again before the order is shipped.

SEGREGATION OF DUTIES

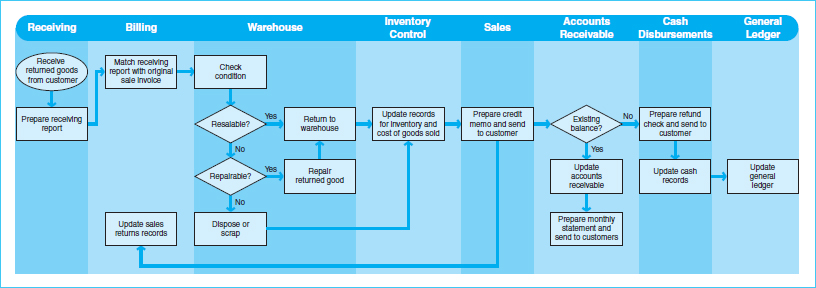

Within the sales process, the accounting duties related to order entry, credit approval, shipping, billing, information systems, and general accounting need to be separated in order to meet the objectives of internal controls. Recall that individuals with authoritative responsibilities should not also have access to the related records or custody of the related assets. In addition to the authorization responsibilities just described, certain information systems duties are included in the sales process, such as data entry, programming, IT operations, and security. The recording function includes the preparation of sales orders, shipping logs, and sales invoices, as well as that of general accounting reports such as the sales journal, accounts receivable subsidiary records and customer statements, the general ledger, and financial statements. Finally, the custody function includes product handling and preparing goods for shipment.

Ideally, good internal controls within the sales process require that accounting for inventory is completely separate from product handling. Also, any person who maintains detailed accounts receivable records should not also be responsible for maintaining the general ledger for or handling cash.

ADEQUATE RECORDS AND DOCUMENTS

Those responsible for recording sales should ensure that supporting documentation is retained and organized. As records are prepared, they should be compared with supporting information to make sure they are accurate and to prevent duplication. Sales orders, shipping logs, invoices, customer account statements, and other related documents should be saved and filed. Record files are often organized by customer name or by the numerical sequence of the documents. When companies account for the numerical sequence of their documents, it is possible to review the list to determine whether omissions have occurred. In addition, if accounting personnel compare the different documents that make up each transaction, they can find out whether the transaction has been carried out properly. For example, when the customer order, packing list, shipping records, and invoice for a single transaction are properly retained, personnel can verify that the records reflect the correct quantities, prices, customer, timing, etc. Maintaining good records also facilitates the performance of independent checks and reconciliations, which will be discussed later.

SECURITY OF ASSETS AND DOCUMENTS

A company's inventory of products should be protected by physical controls in the warehouse. Some examples of physical controls are surveillance cameras, security guards, and alarm systems. Likewise, data files, production programs, and accounting records should each be protected from unauthorized access. Passwords, backup copies, and physical controls (such as locked file cabinets) can protect a company's records.

INDEPENDENT CHECKS AND RECONCILIATION

In order to promote accountability for the sales process, companies should implement procedures whereby independent checks and record reconciliations are performed on a regular basis. These procedures are most effective when they are conducted by someone independent of the related authority, recording, and custody functions. Within the sales process, the most common types of independent checks include the verification of information in the sales journal and on sales invoices, the reconciliation of accounts receivable detail with invoices and with the general ledger, and the reconciliation of inventory records with actual (counted) quantities of products on hand.

COST–BENEFIT CONSIDERATIONS

Companies tend to implement internal controls only if they view the benefits of the control as being greater than the costs of carrying out the task. The extent to which a company implements controls depends upon many factors, including the type of products sold, business or industry factors, and the overall control consciousness of management. Following are some examples of characteristics indicating that a company may be more risky with respect to its sales processes:

- Frequent changes are made to sales prices or customers.

- The pricing structure is complex or based on estimates.

- A large volume of transactions is carried out.

- The company depends on a single or very few key customers.

- Shipments are made by consignees or are under other arrangements not controlled directly by the company.

- The product mix is difficult to differentiate.

- Shipping and/or recordkeeping are performed at multiple locations.

When any of these types of conditions exist, management should be especially mindful of the internal controls that are in place to make sure its system is well controlled.

As mentioned earlier, the effectiveness of internal controls is measured by their ability to prevent or detect errors and fraud. In determining the likelihood of errors or fraud, accountants must consider the risks that exist within the company's business processes. Exhibit 8-7 presents a summary of the relationship between controls and risks for the revenue processes. This exhibit does not include all the possible controls and risks surrounding the revenues process, but presents controls used to correct some common problems that may be encountered.

Exhibit 8-7 Sales Process Controls and Risks