CASH COLLECTION PROCESSES (STUDY OBJECTIVE 4)

Company-to-company sales are typically made on account, and a time span is given for the customer to pay. An example of the credit terms of sale would be net 30. This means the customer has 30 days after the invoice date to pay. Therefore, the timing of a cash collection is such that there will be some number of days between invoice date and collection of the cash. The actual number of days depends on the credit terms of the sale and the diligence of the customer in paying on time. When the customer sends a check, the company must have processes in place to properly handle the receipt. The appropriate employees should match the check with the related sales invoice, deposit the funds in a timely manner, and update customer and cash records. Exhibit 8-12 is a process map of a cash collection process. Exhibit 8-13 shows a document flowchart of cash collection processes, and Exhibit 8-14 shows the cash collection processes in a data flow diagram (DFD).

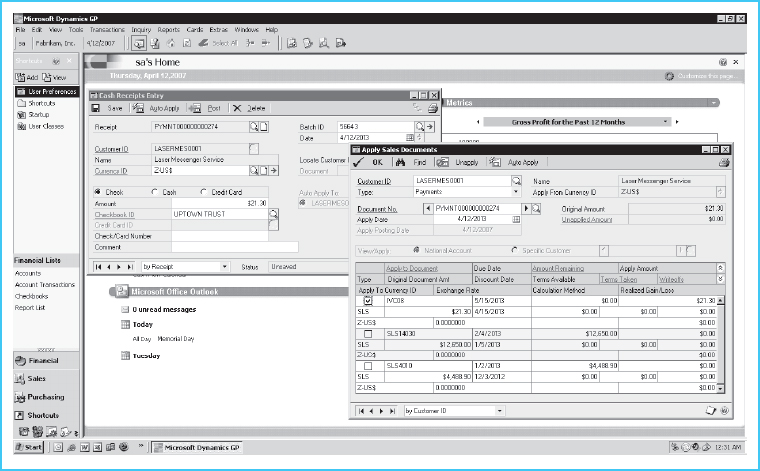

Collections from customers typically include a remittance advice, which is the documentation accompanying payment that identifies the customer account number and invoice to which the payment applies. An example of a remittance advice in your personal life is on your credit card statement. Part of your statement is meant to be detached and mailed with your payment. This remittance that you return enables the company to properly apply your payment to your account. In the case of company-to-company sales, a remittance advice identifies the invoice and customer account number to which the payment should be applied. Exhibit 8-15 shows the application of a payment to the appropriate invoice. In Exhibit 8-15, a check mark is placed in the IVC08 invoice box to apply the payment to that invoice.

For each check received, the payment must be matched with the appropriate invoice or invoices. A list of all cash collections is prepared, and the checks received are recorded in the cash receipts journal. A cash receipts journal is a special journal that records all cash collections. The listing of collections is to be forwarded, along with the payments received, to a cashier who prepares the bank deposit. The payments are deposited in the company account, and customer records and cash records must be updated.

Exhibit 8-12 Cash Receipts Process Map

Exhibit 8-13 Document Flowchart of a Cash Receipts Process

Exhibit 8-14 Cash Receipts Processes Data Flow Diagram

At the end of the month, an updated statement of account will be prepared and sent to the customer. This statement reflects the invoices that have been paid and the decrease in the customer's balance owed as a result of these collections. Also, the bank will send a monthly statement to the company so that the cash records of the company can be reconciled to the bank records.

Exhibit 8-15 Applying a Payment to an Invoice in Microsoft Dynamics®