END OF CHAPTER MATERIAL

CONCEPT CHECK

- Manufacturing has changed in recent years as a result of each of the following factors except

- globalization

- technological advances

- increased competition

- lack of economic prosperity

- The term conversion processes is often used synonymously with

- operations

- production

- manufacturing

- all of the above

- Which of the following activities is not part of the planning component of the logistics function?

- Research and development

- Capital budgeting

- Human resource management

- Scheduling

- Which of the following activities is an inventory control activity?

- Engineering

- Maintenance

- Routing

- Quality control

- Which of the following statements concerning an operations list is true?

- It is an engineering document that describes the chain of events within a company's conversion process.

- It is an engineering document that specifies the descriptions and quantities of component parts within a product.

- It is a capital budgeting document that describes the chain of events within a company's conversion process.

- It is a capital budgeting document that specifies the descriptions and quantities of component parts within a product.

- Which of the following terms relates to the control of materials being held for future production?

- Routing

- Work-in-process

- Stores

- Warehousing

- Which of the following questions is most likely to be found on an internal control questionnaire concerning a company's conversion processes?

- Are vendor invoices for materials purchases approved for payment by someone who is independent of the cash disbursements function?

- Are signed checks for materials purchased mailed promptly without being returned to the department responsible for processing the disbursement?

- Are approved requisitions required when materials are released from the company's warehouse into production?

- Are details of payments for materials balanced to the total posted to the general ledger?

- When additional procedures are necessary to bring a defective product up to its required specifications, this is referred to as

- rework

- scrap

- work-in-process

- variance reporting

- A firm expects to sell 1000 units of its best-selling product in the coming year. Ordering costs for this product are $100 per order, and carrying costs are $2 per unit. Compute the optimum order size, using the EOQ model.

- 10 units

- 224 units

- 317 units

- 448 units

- Which of the following internal controls is typically associated with the maintenance of accurate inventory records?

- Performing regular comparisons of perpetual records with recent costs of inventory items

- Using a just-in-time system to keep inventory levels at a minimum

- Performing a match of the purchase request, receiving report, and purchase order before payment is approved

- Using physical inventory counts as a basis for adjusting the perpetual records

- If a manufacturing company's inventory of supplies consists of a large number of small items, which of the following would be considered a weakness in internal controls?

- Supplies of relatively low value are expensed when acquired.

- Supplies are physically counted on a cycle basis, whereby limited counts occur quarterly and each item is counted at least once annually.

- The stores function is responsible for updating perpetual records whenever inventory items are moved.

- Perpetual records are maintained for inventory items only if they are significant in value.

- The goal of a physical inventory reconciliation is to

- determine the quantity of inventory sold

- compare the physical count with the perpetual records

- compare the physical count with the periodic records

- determine the quantity of inventory in process

- Which of the following is not considered a benefit of using computerized conversion systems?

- Automatic computation of materials requirements

- Increased sales and cost of sales

- Increased efficiency and flexibility

- Early error detection and increased accuracy

- Which of the following represents a method of managing inventory designed to minimize a company's investment in inventories by scheduling materials to arrive at the time they are needed for production?

- The economic order quantity (EOQ)

- Material resource planning (MRP)

- First-in, first-out (FIFO)

- Just-in-time (JIT)

- For which of the following computerized conversion systems is Walmart well known?

- CAD/CAM

- MRP-II

- CIMs

- JIT

DISCUSSION QUESTIONS

- (SO 1) What are the three resources that an organization must have to conduct a conversion (or transformation) process?

- (SO 1) Do conversion processes occur in manufacturing companies only? Why, or why not?

- (SO 1) Why are conversion activities typically considered routine data processes?

- (SO 2) Differentiate between a bill of materials and an operations list.

- (SO 2) Differentiate between the roles of the engineering and the research and development departments.

- (SO 2) What are the two types of documents or reports are likely to trigger the conversion process?

- (SO 2) What are the three primary components of logistics?

- (SO 2) What types of information must be taken into consideration when scheduling production?

- (SO 2) Differentiate between a routing slip and an inventory status report.

- (SO 2) What are the conversion responsibilities of the maintenance and control, inventory control, inventory stores, and human resources departments?

- (SO 2) What is the purpose of an inventory status report?

- (SO 2) What is the overall goal of the inventory control department?

- (SO 2) What is the purpose of the quality control department?

- (SO 3) What is the purpose of determining standard costs?

- (SO 3) What should be done when unfavorable variances are discovered?

- (SO 3) Why would perpetual inventory records be preferable to periodic inventory records in a manufacturing company?

- (SO 4) Which three activities in the conversion process should require specific authorization before they are begun?

- (SO 4) Why is it important to separate the functions of inventory control and the production stations? What could go wrong if these functions were not separated?

- (SO 4) Why is it so important that variance reports be prepared in a timely manner?

- (SO 4) Explain how a physical inventory count would differ in a company using a perpetual inventory system versus one using a period inventory system.

- (SO 5) When IT systems are used in conversion processes, what are some of the resulting advantages to the organization?

- (SO 5) How can programmed controls within the IT system for conversion processes enhance internal controls?

- (SO 5) What is the difference between CAD, CAM, and CIM?

- (SO 5) What is the difference between MRP, MRP-II, and ERP?

- (SO 6) How can conversion processes be manipulated to show higher earnings?

BRIEF EXERCISES

- (SO 1) Consider a company that is in the business of producing canned fruits for grocery stores. (It is not in the business of growing the fruit.) List the items that would likely be included as this company's direct materials, direct labor, indirect materials, and other overhead.

- (SO 2) Give some examples of manufacturing processes that would fit into each of the three different types of production processes: continuous processing, batch processing, and custom made-to-order.

- (SO 2) List and describe each activity within the planning component of the logistics function.

- (SO 2) Some companies use the same facility for both inventory stores and warehousing. Describe the difference between these two inventory control activities, and how the respective areas might be distinguished within the facility.

- (SO 2) For the following activities within the conversion process, place them in sequence that indicates the order in which they would normally be performed:

- Inspection of goods

- Materials issuance

- Preparation of time sheets

- Preparation of a bill of materials

- Preparation of an inventory status report

- Preparation of a production schedule

- (SO 2, 3) Describe the purpose of each of the following cost accounting records or reports:

- Work-in-process and finished goods inventory accounts

- Bill of materials

- Variance reports

- Routing slips

- (SO 3) Describe how a cost accountant would cancel a production order upon completion of the related product. Why is this important?

- (SO 4) When taking a physical inventory count at a typical manufacturing facility, which category of inventory (raw materials, work-in-process, or finished goods) is likely to be the most time consuming to count and determine the relevant costs for? Why?

- (SO 4) Identify several factors that indicate the need for more extensive internal controls covering conversion processes.

- (SO 5) Match the IT systems on the left with their definitions on the right:

PROBLEMS

- (SO 2) Suppose a company has 1000 units of a raw material part on hand. If 750 of these units are routed into production, should the company place an order to stock up on more of these parts? In order to answer this question, determine the economic order quantity (EOQ) for this part, assuming that the following are true:

- The company plans to use 10,000 units during the coming year.

- The company orders this part in lots of 1000 units, and each order placed carries a processing cost of $2.50.

- Each unit of inventory carries an annual holding cost of $6.40.

- (SO 4) Suppose a company is experiencing problems with omitted transactions in the conversion process—i.e., inventory transactions are not always being recorded as they occur. Refer to Exhibit 7-7 to describe at least three internal controls that should be in place to help alleviate such problems.

- (SO 5) Using an Internet search engine, search for the terms “CAD” + “industrial robots.” Identify a company (name and location) that provides manufacturing automation by using robotics. Describe some of the robotic operations that are featured on the company's website.

- (SO 5) Using an Internet search engine, search for the terms “just in time” “automotive.” From the results you find, explain why just-in-time inventory systems are such an important factor in the competitive automotive industry.

- (SO 6) Explain how the over-production of inventories can be seen as unethical in an absorption costing environment.

- (SO 6) Price discounts are commonly used in the business world as incentives for customers. How may this practice (or its misuse) be deemed unethical?

- (SO 3) Texas Bar Supply manufactures equipment for bars and lounges. While the company manufactures several different products, one is a blender that bartenders use to make certain kinds of drinks. From the textbook website at http://www.wiley.com/college/turner, download the spreadsheet template named requisition.xls. Using information in the spreadsheet template, complete the requisition form to calculate the quantity and cost of the parts needed to manufacture a batch of 500 bar blenders. To look up the cost from the price list sheet, you will use a spreadsheet function called VLOOKUP. Be sure to design your formulas in a way that will incorporate changes in the batch size or changes to costs of individual parts.

- (SO 5) Using an Internet search engine, locate a publication called “RFID Journal.” Find a recent article that describes the use of RFID in manufacturing. Briefly describe the example(s) discussed in the article.

CASES

- Compton Falls Enterprises is a manufacturer of model trains that sell under the name CF Toy Trains in toy stores and hobby shops throughout the United States and Europe. The company employs 160 people in its home office and sole manufacturing and storage facility, which are both located in Compton Falls, Indiana.

The inventory storeroom is called the stores department, and it is managed by Henry Prayne. Both materials and finished goods are maintained in this area, as well as the supporting inventory records. Henry performs a daily review of the items on hand by monitoring the inventory subsidiary ledger and determining whether additional materials are needed. If they are, Henry prepares a materials requisition form to submit to the production planning department.

The production planning department is led by Roberta “Berta” Aler. Upon receipt of a materials requisition form from Henry, Berta files the form. Berta's files contain not only the materials requisition forms received from Henry, but also sales forecasts received from the sales department. These files are monitored on a daily basis; if there is a match between the needs identified by both stores and sales, a bill of materials and a routing slip are prepared and forwarded to the production room. If inventory quantities for supporting materials are sufficient, a production schedule is prepared and forwarded to the production room. If materials are needed to support production of the items, a purchase requisition is prepared and forwarded to the purchasing and stores department.

Berta Aler is also the supervisor of the production room. Once new documents are obtained from the production planning department, the bill of materials and routing slip are sent to stores, where Henry retrieves the necessary materials. He makes a copy of the bill of materials and routing slips and then returns these documents to the production room, along with the requested materials. At the end of the day, Henry updates the inventory subsidiary ledger and prepares a journal voucher summarizing the day's use of materials.

In the production room, the leaders of each production line collect employee time cards at the end of each week and send them to the payroll and cost accounting departments. They also prepare weekly job cost reports for the cost accounting department, itemizing the various costs that have been incurred.

Dell Shay heads the cost accounting department. Dell uses the job cost reports and time cards to create journal vouchers that update the work-in-process and finished goods inventory accounts. As new cost data are obtained, the cost accountants are continually accumulating actual cost data to be compared with standard costs. Variances are calculated and compared, and the information is used to evaluate the line workers in the production room, as well as the managers and supervisors of each department.

Steve Stifer is responsible for updating the general ledger on a weekly basis. The information from the journal vouchers is entered in the general ledger program, which automatically updates the respective accounts. All journal vouchers are filed in Steve's office.

Required:

- Draw a process map of the conversion processes at Compton Falls Enterprises.

- Draw a document flowchart showing the records used in the conversion processes at Compton Falls Enterprises.

- List any strengths and weaknesses in the company's internal control procedures. For each weakness, suggest an improvement.

- Describe any benefits that Compton Falls Enterprises may receive by installing newer IT systems within its conversion processes. Be specific as to how IT systems could benefit each of the processes described, or how they could eliminate any weakness identified per item c.

- 60. Bokka Ski Line, Inc. is a manufacturer of equipment used for snow skiing and snow boarding. The company's products are sold under two brand names, one comprising its top-of-the-line equipment and the other comprising its line of moderately priced equipment and ski attire. Bokka's sole location near Rochester, New York, is home to both its offices and manufacturing facility. Bokka's products are sold worldwide, and current year sales are expected to reach $180 million.

Bokka's conversion process begins in the storekeeping department, where inventories and the related records are maintained. Ted Drescoll manages the storekeeping function by reviewing the files on a daily basis to determine the inventory needs. He prepares an inventory status report and forwards it to the production planning and control department.

Production planning and control is lead by Thom Ells. Every day Thom prepares bills of materials, routing slips, productions orders, and production schedules. Copies of each of these documents are forwarded to the production floor. Thom concurrently determines inventory needs by reviewing the following documents:

- Inventory status reports received from the storekeeping department

- Sales forecasts from the marketing division

If additional quantities of materials inventory are needed, Thom prepares a purchase requisition and forwards copies to the storekeeping and purchasing departments. If inventory quantities are adequate, no further action is taken.

Thom Ells also manages the production processes. Production supervisors on each of the company's six production lines report to Thom. When these supervisors receive production orders and supporting documentation from the production planning and control department, copies of the bill of materials and routing slips are forwarded to Ted Drescoll. In return, Ted sends the requested materials to the production line. Ted then updates the inventory ledger and sends the bill of materials and routing slips to the cost accounting department. He then prepares a journal voucher for the change in inventories and forwards it to Helena McPhea, who is responsible for the general ledger.

At the production lines, the supervisors prepare job tickets to accumulate costs associated with their activities; these tickets are forwarded to cost accounting. They also collect employee time sheets and send them to cost accounting on a weekly basis. The time sheets are prepared in duplicate, and the second copy is sent to the personnel department.

In Bokka's cost accounting department, Clive Hendersen collects all of the documents to determine the actual costs of the products. Actual costs are compared with standards, and variances are computed. Total variances are used to evaluate managers and supervisors. Next, Clive updates the work-in-process and finished goods inventory files; then he prepares a journal voucher and forwards it to Helena McPhea.

In the general ledger department, Helena updates the general ledger by entering the journal vouchers into the general ledger computer software program. Journal vouchers are filed by date.

Required:

- Draw a process map of the conversion processes at Bokka.

- Draw a document flowchart showing the records used in Bokka's conversion processes.

- List any strengths and weaknesses in Bokka's internal control procedures. For each weakness, suggest an improvement.

- Brock's Footwear, Inc., is a manufacturer of a popular line of casual shoes and sandals that has experienced significant growth within the past 18 months. The unique design of its product line has always been the key to the company's success. It is currently still using a system consisting of manual job costing sheets and inventory cards. Although this system was satisfactory in the past, the company's recent growth has resulted in various problems with operations and inventory control. The biggest problem is with meeting the production and delivery schedules. Many products are delivered late because the products are not completed on time. In addition, some products are delayed in the production process because the required materials are out of stock; it sometimes takes a week or more to restock back-ordered materials. To make matters worse, the company has been unable to control waste of its raw materials. There are significant quantities of materials left over after the production runs. These excess materials are eventually written off because no known scrap market exists.

Job costing sheets and inventory cards are updated at the end of each week. It takes nearly a week for the production clerks to update the accounting records from these documents. When customers inquire about the status of their orders, the production clerks use the job costing sheets to estimate delivery dates. Because of the back-order problems, though, these estimates are often overly optimistic. This inability to provide accurate delivery dates has been a serious source of customer dissatisfaction.

The production and inventory managers have recognized the need for the company to improve its system of tracking customer orders and maintaining raw materials inventory. They have tried to convince top management of the need to improve the timeliness of information flow between the production, inventory, and accounting departments. However, top management believes that customers will be willing to wait for their orders because the products are in high demand. Furthermore, top management is reluctant to spend money on automation.

Recently, competitors have started to imitate Brock's footwear designs, and some customers have hinted that they are tempted to place future orders with these competitor companies. Brock's production and inventory managers are making another plea to top management for a new computerized inventory information system.

Required:

- List the problems with the existing system at Brock's Footwear.

- Identify the relevant information that the production and inventory managers need to accumulate in order to support the decision to automate the conversion process.

- List specific items that could be provided by an automated system, and describe how this could be essential to the company's continued success.

- (CMA Adapted) Arbol Dynamics, Inc., produces computer chips for personal electronic devices used to record music. The chips are sold primarily to large manufacturers; however, occasional production overruns may be discounted and sold to small manufacturers. Since Arbol's operating budget assigns all fixed production expenses to its predictable market—large manufacturers—there are no fixed expenses allocated to products sold to small manufacturers. This results in significant profits in the small manufacturer market segment, even though the products are discounted.

All of Arbol's products are tested for quality standards, and rejected chips are reworked to acceptable levels. The projected failure rate of reworked chips is determined to be 10 percent. Recently, however, customer feedback has suggested that the rework process is not always bringing the chips up to quality standards. Jamie Trogg, cost accountant, and Marty Cambiss, quality control engineer, have determined that a failure to maintain precise temperature levels during chip production results in a product defect that has a 50 percent failure rate. Unfortunately, current testing techniques do not detect this defect, so the company has no way to identify which chips will fail. Enhancements to the rework process would alleviate the defects problem; however, the additional cost is believed to be excessive, considering that half of the products would not benefit from the enhancement. Marty Cambiss and Jamie Trogg discussed this issue with Arbol's marketing manager, Ellis Wynn, who has indicated that the defect problem will have a significant negative impact on the company's reputation.

Jamie Trogg has documented the problem in her report, which will be presented at the meeting of the board of directors next week. She is convinced that the problem will have a serious impact on the company's profitability.

Upon reviewing the cost accounting report to be presented to the board of directors, the plant manager became enraged and stormed into the office of the controller, demanding that the report be revised to downplay the rework issue. The controller agreed that the report's current presentation would draw too much attention to the problem and would likely be alarming to the board members. He instructed Jamie Trogg to revise the report and tone down the issue so as to avoid upsetting the board members.

Jamie Trogg is convinced that the board members would be misinformed if the serious nature of this problem were not highlighted in her report. She went back to Marty Cambiss and Ellis Wynn to try to solicit their support in pressing this issue; however, both of them were unwilling to get further involved in a matter that appears controversial.

- What should Jamie do? Explain your answer and discuss the ethical considerations that she should recognize in this situation.

- What corporate governance functions are missing at Arbol? Be specific and describe the facts of the case and their relevance to corporate governance.

CONTINUING CASE: ROBATELLI'S PIZZERIA

Reread the continuing case on Robatelli's Pizzeria at the end of Chapter 1. Consider any issues related to Robatelli's conversion processes, and then answer the following questions:

- Briefly describe Robatelli's conversion processes—that is, what gets converted, how is it done, and where are the underlying processes performed [at which Robatelli's location(s)]?

- What procedures and internal controls would you recommend to Robatelli's to minimize the risk of lost sales due to stock-outs (i.e., running out of ingredients) and the resulting idle time that may be incurred while employees are awaiting delivery from the commissary?

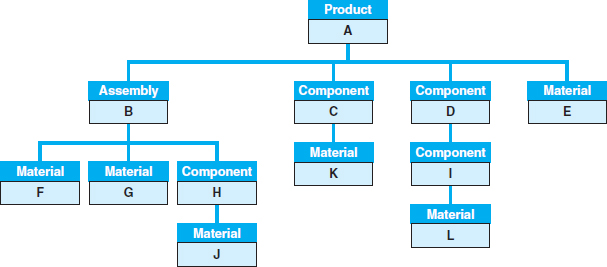

- Revise the accompanying example of the structure of a bill of materials to show specific details of the subassembly of the dough and the various components (sauce, toppings, and cheese) and underlying materials (ingredients) that would likely be included on Robatelli's bill of materials for a large deluxe pizza.

SOLUTIONS TO CONCEPT CHECK

- Manufacturing has changed in recent years as a result of each of the factors except d. lack of economic prosperity.

- (SO 2) The term conversion processes is used synonymously with d. all of the above. Operations, production, and manufacturing are all synonyms for the conversion process.

- (SO 2) c. Human Resource Management is part of the resource management component, not part of the planning component of the logistics function.

- (SO 2) c. Routing is an inventory control activity. Answer a. is part of the planning component; b. is part of the resource management component; d. is part of the operations component.

- (SO 2) The following statement concerning an operations list is true: a. It is an engineering document that describes the chain of events within a company's conversion process. Answer b. is incorrect because an operations list does not describe a product's components. Answers c. and d. are incorrect because an operations list is not a capital budgeting document.

- (SO 2) c. Stores relate to the control of materials being held for future production. Answers a. and b. relate to current production and answer d. relates to finished goods (past production).

- (CPA Adapted) (SO 2) The following question is most likely to be found on an internal control questionnaire concerning a company's conversion processes: c. Are approved requisitions required when materials are released from the company's warehouse into production? This is the only response that pertains specifically to the conversion process. Responses a. and b. concern the expenditures and cash disbursements functions, and response d. pertains to general accounting.

- (SO 2) When additional procedures are necessary to bring a defective product up to its required specifications, this is referred to as a. rework. Answer b. relates to defective products for which no additional procedures are deemed worthwhile; answer c. relates to the original production (rather than additional procedures); answer d. relates to quantification of production differences.

- (CIA Adapted) (SO 2) A firm expects to sell 1000 units of its best-selling product in the coming year. Ordering costs for this product are $100 per order, and carrying costs are $2 per unit. Compute the optimum order size, using the EOQ model. The answer is c. 317 units. This is the square root of (2 × 1,000 × $100) / $2, or the square root of 100,000. Answer a. is incorrect because total carrying costs are used rather than unit carrying costs. Answer b. is incorrect because it failed to multiply by the constant 2. Answer d. is incorrect because it failed to divide by carrying costs.

- (CPA Adapted) (SO 4) The following internal control is typically associated with the maintenance of accurate inventory records: d. using physical inventory counts as a basis for adjusting the perpetual records. Answer a. is incorrect because the most recent costs do not necessarily reflect the carrying cost of inventories. Answer b. is incorrect because it relates to cost savings rather than to an internal control improvement. Answer c. is incorrect because it relates to the existence of inventory rather than its accurate reporting.

- (CPA Adapted) (SO 4) If a manufacturing company's inventory of supplies consists of a large number of small items, the following would be considered a weakness in internal controls: c. The stores function is responsible for updating perpetual records whenever inventory items are moved. Since the stores function is responsible for movement of inventory (a custody function), a violation of the principles of segregation of duties exists if this function is also responsible for recordkeeping. Each of the other responses represents common practices that are not considered control weaknesses.

- (SO 4) The goal of a physical inventory reconciliation is to b. compare the physical count with the perpetual records.

- (SO 5) b. Increased sales and cost of sales is not considered a benefit of using computerized conversion systems. Each of the other answers relates to improvements in terms of cost savings, efficiencies, and/or improved controls.

- (CMA Adapted) (SO 5) d. JIT represents a method of managing inventory designed to minimize a company's investment in inventories by scheduling materials to arrive at the time they are needed for production. Answer a. relates to optimum order quantities. Answer b. relates to manufacturing systems. Answer c. is an inventory costing method.

- (SO 5) Walmart is well known for the computerized conversion system d. JIT. Each of the other answers relates to manufacturing systems and therefore would not likely be used by a retail business.

1G. Pascal Zachary, “Dream Factory.” Business 2.0, vol. 6, no. 5, June 2005, p. 99.