RISKS AND CONTROLS IN FIXED ASSETS PROCESSES (STUDY OBJECTIVE 6)

AUTHORIZATION OF TRANSACTIONS

Designated members of management should be assigned responsibility for authorizing the purchase of new fixed assets, as well as the disposal or transfer of existing fixed assets. In the case of high-dollar items, there should be a strict approval process requiring the authorization of top management or the initiation of the capital budgeting procedures. This strict process for purchasing fixed assets should include at least three formal steps:

- Investment analysis

- Comparison with the capital budget

- Review of the proposal and specific approval by the appropriate level of management

When a request is made to purchase fixed assets, there should be a formal investment analysis to justify that the expenditure will generate benefits that exceed the cost. This analysis could require two parts. The first part is financial justification with a model such as net present value, payback period, or internal rate of return. These models require that dollar estimates be determined for costs and benefits of the fixed asset. The second part would be a written narrative of the benefits, especially any benefits that are difficult to quantify in dollars. In many cases fixed asset purchases are important to consider even when financial costs exceed financial benefits. For example, if a direct competitor purchases a document imaging system to speed the processing of customer paperwork, a company may need to purchase similar technology just to stay competitive. A written narrative of the need for investment can help justify the expenditure when financial benefits do not immediately surpass costs.

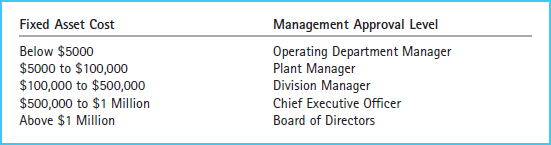

Secondly, management should establish a capital budget and compare all expenditures with the capital budget prior to approving any purchase of fixed assets. Finally, based on the investment analysis and the capital budget comparison, a manager at the appropriate level should approve or disapprove the purchase. Generally, management establishes a system that requires upper-level management approval for higher dollar amounts of fixed asset purchases, as in Exhibit 10-13.

This authorization process is much more formal and specific than the authorization of purchases of raw materials, inventory, and supplies. There should also be formal and specific approval for the disposal of fixed assets. Requests for these purchase and disposal transactions, and the related authorizations, should be documented and retained.

Exhibit 10-13 An Example of Fixed Asset Approval Levels

Companies should also require management approval for the selection of a depreciation method and assignment of useful lives and estimated salvage values. Likewise, a designated manager should handle asset quality specifications, vendor selection, and negotiation of payment terms for fixed asset purchases.

SEGREGATION OF DUTIES

Custody of fixed assets needs to be separate from the related record keeping. Adequate segregation of duties reduces the risk of undetected errors or fraud by requiring separate employees to handle the different transactions that occur in each phase of the asset's life. Ideally, those with custody of fixed assets should not perform any duties in the purchasing, receiving, or fixed asset accounting departments. In addition, key IT functions such as programming, operations, data input, and security should be segregated from each other and from the related accounting duties.

ADEQUATE RECORDS AND DOCUMENTS

Fixed asset subsidiary ledgers are used to control the physical custody, cost, and accumulated depreciation of the fixed assets. Just like the expenditures process for inventory purchases, fixed asset purchases should be supported by a purchase requisition, purchase order, receiving report, and vendor invoice. These documents need to be matched in order to establish the validity of the acquisition and to determine whether any items have been omitted from the records. Fixed asset tags may also be used to account for the numerical sequence of items acquired. In addition, management should prepare and follow a capital budget.

SECURITY OF ASSETS AND DOCUMENTS

Adequate supervision is an important control concerning the security of fixed assets, because fixed assets tend to be located throughout the company where many employees could have access to them. Supervisors need to make certain that the assets are being used for their intended purposes. Physical controls should also be in place to protect fixed assets from unauthorized use, and electronic controls are needed to control access to automated records. The appropriate security features depend on the nature and value of the property.

A company should also protect its investment in fixed assets by maintaining adequate insurance coverage and conducting regular preventative maintenance procedures such as tune-ups for machinery and vehicles.

INDEPENDENT CHECKS AND RECONCILIATION

Actual fixed asset expenditures should be compared with the capital budget, and additional approval should be required if budgets are exceeded. In addition, periodic counts of fixed assets should be made by someone not otherwise responsible for fixed-asset-related activities. Those physical counts should be reconciled with the accounting records. Also, performing independent verifications to match key purchasing documents and the related accounts payable reports may uncover errors or fraud within these records.

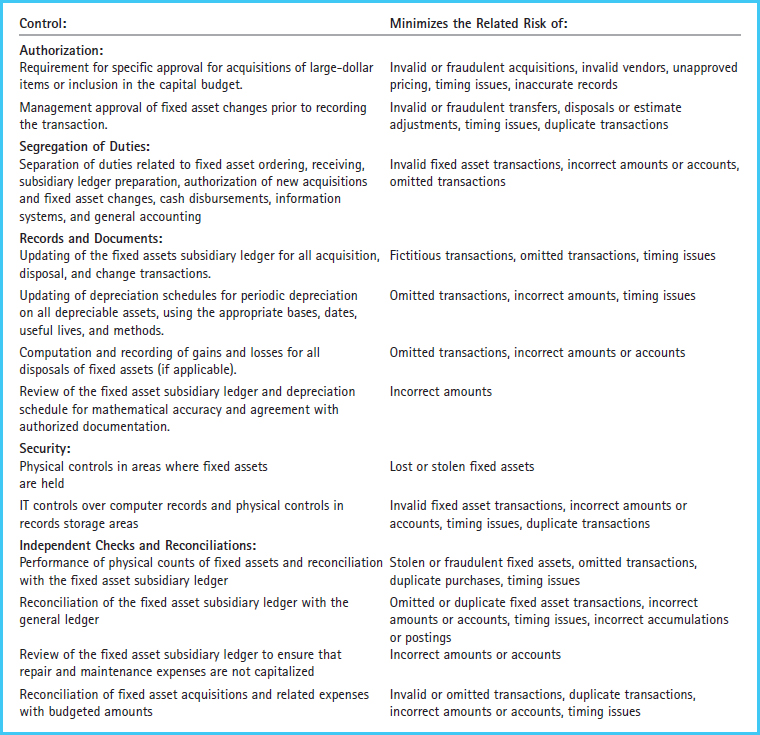

The value of fixed assets should be appraised periodically for insurance purposes. This procedure may also uncover the possibility of impairment issues on these assets. Exhibit 10-14 summarizes the fixed asset controls and risks.

Exhibit 10-14: Fixed Assets Controls and Risks

COST–BENEFIT CONSIDERATIONS

The general nature of fixed assets makes them susceptible to theft, since they are distributed throughout the business and are therefore in the hands of so many different employees. Some additional factors that indicate the need for internal controls over fixed asset processes include large quantities of fixed assets, large quantities of fixed asset changes (such as additions, transfers, and disposals), high likelihood of obsolescence due to technological changes, the existence of assets under capital leasing arrangements, and widely dispersed fixed asset locations.

Companies tend to implement internal controls when they can justify the expense in terms of increased benefits. Accordingly, companies should assess their risk from factors such as those mentioned previously, and decide on the appropriate mix of internal controls. The examples presented in Exhibit 10-14 identify internal controls used in the fixed assets processes and the related risks that are minimized through their implementation. Although this exhibit does not represent a comprehensive list, it includes many reasonable combinations of items that affect fixed asset processes. In addition, the purchasing process maps in Chapter 9 show some purchases and cash disbursements processes that are also relevant to fixed asset systems.