RISKS AND CONTROLS IN CONVERSION PROCESSES (STUDY OBJECTIVE 4)

Because conversion processes involve the physical movement of inventory throughout the operating facility and may be spread among multiple locations, departments, and employees, it is important that sufficient internal controls be included in the related business processes. In terms of the five internal control activities introduced in Chapter 3, the following are some procedures to be considered for implementation in conversion processes.

AUTHORIZATION OF TRANSACTIONS

Designated employees in the company should be given responsibility for purchasing raw materials, including specifying the quality of the items needed, selecting of vendor, and determining the appropriate quantities to order.

The following activities in the conversion process require express authorization:

- Initiation of production orders

- Issuance of materials into the production process

- Transfer of finished goods to the warehouse or shipping areas

These responsibilities require continuous monitoring of the production activities, and should therefore be conducted by an experienced member of management.

SEGREGATION OF DUTIES

Custody of inventories and the accounting for inventories and cost of sales need to be separate in order for internal control objectives to be met. Adequate segregation of duties reduces the risk of errors or fraud by requiring separate processing by different employees at the various stages of the conversion process. This feature is enhanced by the performance of independent reviews and reconciliations, discussed later.

Ideally, those responsible for handling inventories in the materials storeroom and warehouse and issuing the movement of inventories into and out of these areas should be separate from the production stations and from the cost accounting function. Similarly, the inventory control functions should not be performed by those responsible for production or by those performing cost accounting functions. With respect to IT processing, companies should strive to separate the duties of systems development, computer operators, and users. The IT functions should also be separate from the accounting and custody functions.

ADEQUATE RECORDS AND DOCUMENTS

Complete, up-to-date, and accurate documentation on production orders, inventory and cost of sales records, and inventory status reporting is needed to support the conversion process. The practice of issuing documents on prenumbered forms is a control that helps to create clear records of the conversion transactions. When production orders and routing slips are issued numerically, a sequence can be accounted for to determine whether all conversion transactions have been recorded.

The creation and monitoring of variance reports is another control that is especially important in the conversion process. Its importance lies in the ongoing analysis of the information as it relates to production activities. The usefulness of variance data depends upon the integrity of the underlying system and the timeliness of its preparation. These variance reports are useful only if they contain reliable and accurate information. Likewise, they must be provided in a timely manner so that management can use them to make decisions in time to make a difference in the process.

SECURITY OF ASSETS AND DOCUMENTS

Physical controls should be in place in the company's storerooms, warehouses, and production facilities in order to safeguard the inventories held therein. These physical controls may include fences and alarm systems, security guards, or other, high-tech security tools such as retina scanners. In addition, water sprinkler systems, fire prevention devices, and adequate insurance coverage should be maintained in inventory storage areas. There should be policies in place to ensure that only authorized employees handle the inventories in each of these locations.

Likewise, only authorized employees should access the inventory records. In order to control this, companies should assign passwords to employees who access the files. These employees should be required to log all transactions in the logistics function. Timely backup of production files is also important in protecting the information and guaranteeing continued processing even in the event of destruction of the original files.

INDEPENDENT CHECKS AND RECONCILIATION

There are many recommended procedures for overseeing the conversion process through the performance of various supervision and review activities. Probably the most typical control is the requirement for conducting periodic physical inventory counts and comparing the results with recorded inventory quantities. A physical inventory count determines the quantity of inventory on hand by actually counting all items on the premises and in other areas of the company's responsibility. This should be performed for all three categories of inventory (raw materials, work-in-process, and finished goods), regardless of whether perpetual or periodic systems are in place. Companies using periodic inventory systems rely upon the physical inventory counts as a basis for determining the end-of-period inventory and cost of sales amounts. However, even companies that maintain perpetual records tend to conduct physical counts as a means of determining the accuracy of their records and the related general ledger control accounts. In perpetual systems, the quantity determined via the physical inventory count must be compared with the perpetual records. This activity is referred to as the physical inventory reconciliation.

In addition to the physical inventory reconciliation, someone independent of the record keeping and custody functions should review the materials, labor, and overhead reports that support the inventory amounts. Specifically, production orders should be reconciled with records of work-in-process and finished goods inventory. Labor reports should also be reconciled with employee time sheets. In addition, routing slips should be reconciled with records of inventories transferred to the warehouse or shipping areas.

The records and documentation section just presented describes the importance of the cost variance reports as control features. These reports need to be monitored and reconciled in order to determine the source of problems within the conversion process. These review procedures typically involve members of management who can overview the process and authorize improvements.

COST–BENEFIT CONSIDERATIONS

The more products a company has and the more complex its conversion process is, the more internal controls should be in place to monitor and safeguard its assets. There are other factors that influence the level of risk inherent in a business that may warrant the implementation of strong controls. Namely, if the goods are extremely valuable, they may be especially susceptible to theft. For instance, if a company's inventory consists of fine jewelry, its inventory storage facility is likely to be controlled much differently than the warehouses of a company whose inventory consists of construction materials such as lumber and cement mix. In addition, if a company's inventory items are difficult to differentiate or to inspect, strong controls may be needed in order to properly identify the items. Other conditions within the production facility may warrant the need for additional controls, such as inconsistent or high levels of inventory movement, which can make it difficult for supervisors to review the reasonableness of conversion transactions without additional information. Finally, there are factors about the organization of the company that affect the design of operation or its internal controls. If the inventory is held at various locations or the process of valuing inventories is particularly complex, additional controls may also be recommended.

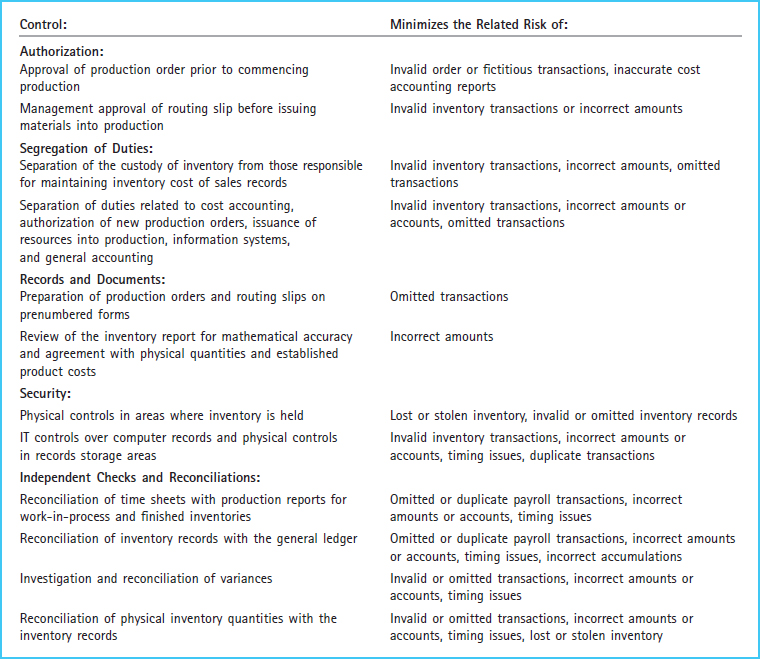

Exhibit 11-8 summarizes examples of internal controls in the conversion process and the related business risks that are minimized as a result of the implementation of these controls. This exhibit does not include all the possible controls and risks that may be encountered in the payroll process, but it does provide some common situations.