CHAPTER 12

Administrative Processes and Controls

STUDY OBJECTIVES

This chapter will help you gain an understanding of the following concepts:

![]() An introduction to administrative processes

An introduction to administrative processes

![]() Source of capital processes

Source of capital processes

![]() Investment processes

Investment processes

![]() Risks and controls in capital and investment processes

Risks and controls in capital and investment processes

![]() General ledger processes

General ledger processes

![]() Risks and controls in general ledger processes

Risks and controls in general ledger processes

![]() Reporting as an output of the general ledger processes

Reporting as an output of the general ledger processes

![]() Ethical issues related to administrative processes and reporting

Ethical issues related to administrative processes and reporting

![]() Corporate governance in administrative processes and reporting

Corporate governance in administrative processes and reporting

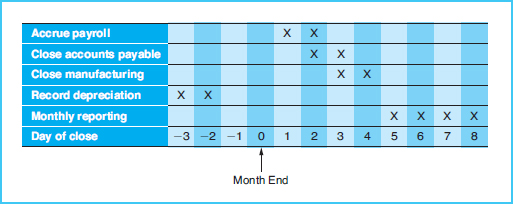

All but the smallest organizations do a monthly closing of the general ledger and provide feedback reports to management after the closing process. The closing process is necessary to ensure that all expenses are accrued and posted to the proper accounts prior to reports being prepared. The closing process entails posting all monthly transaction summaries and correcting any errors that are detected. This closing process can be very time-consuming, especially in situations where one department must wait on another department. For example, the general ledger cannot be closed until the payroll department receives and processes all month-end time cards. A typical timing of the closing process is shown in Exhibit 12-1.1

Notice that in example, the total time required is 12 working days and management receives financial reports eight days after month end. Many managers believe eight days is too long to wait to receive financial feedback reports. The modern, integrated IT systems in use today can help to drastically reduce the time of the monthly closing. In fact, many companies monitor the time required to carry out their closing process. Furthermore, some companies are striving to achieve a “fast close” or “virtual close,” whereby the timing of the monthly closing process is reduced to a few days or hours, respectively.

Despite these trends in improving the speed of the closing process, many companies still have long closing processes because of a lack of system integration and the time-consuming nature of the human steps in the process (such as error correction and re-keying of data). Even in the largest corporations with modern IT systems, there are still human processes in the general ledger closing because systems are not always integrated.

THE REAL WORLD

Alcoa, Inc., the world's leading producer of aluminum, is well known for its accomplishments in the areas of sustainability and innovation in the transportation, aerospace, construction, and electronics industries. In 2012, Alcoa was appointed to Fortune magazine's list of Most Admired Companies for the twenty-ninth consecutive year.

A lesser known fact about Alcoa is that it is often the first of the Dow Jones Industrial companies to report its quarterly earnings. Alcoa has worked hard to achieve a fast close, whereby it has fine-tuned its accounting processes and information systems to facilitate the completion of periodic transaction processing and closing of the general ledger within two days of the end of the period. Then, it can report its consolidated financial results externally within one week. In today's fast-paced business environment, companies can gain competitive advantage by closing their books quickly and delivering timely information to internal and external stakeholders.

The posting and closing process of the general ledger is one of the administrative processes described in this chapter. Also described here are source of capital processes, investing processes, and reporting. Therefore, the administrative processes described in this chapter include

- Source of capital processes

- Investment processes

- General ledger processes