Chapter 1. Making Sense of Innovation Fads and Fashions

"Innovate or die!"

—Various

Innovate and die. In evolutionary terms, that's usually what happens. Most mutations fail. Few truly new things survive, and even fewer of them thrive. This is just as true in the business world as it is in biology. The record of various innovation fads and fashions during the past few years certainly is consistent with this harsh fact.

For much of the past decade, however, management gurus, media, and markets preached a different doctrine. It was a "cult of innovation at all costs," an unquestioning, single-minded belief in the power of innovation above all else.[1] The risks of innovation seemed passé. The need for novelty took precedence. The real risk was not to innovate. Managers became mesmerized by the passionate but also threatening mantra of "Innovate or die!" Survival was a compelling enough reason to take heed of their urgent call to action. But beyond simple survival, the innovation enthusiasts promised much more.

It was a New Economy. The Old Rules did not apply. To the quick and bold pioneers of innovation would go faster and more fabulous riches than anything the traditional, tired ways of doing business could offer.

Innovation Excitement, Then Disillusionment

Swayed by this powerful mix of fear and fortune, many executives and entrepreneurs frantically rushed to innovate almost literally at any cost. A great number of companies seriously stumbled or even outright failed in the process. Their big, rushed bets on raw technologies and unproven business models did not pay off. Victims of this innovation obsession included enormous, globe-spanning, blue-chip corporations and new technology startups alike.

It's difficult to overstate how powerful and pervasive the innovation mania was during this time. It's useful to briefly reflect and recall the prevailing spirit. Something more than a bit of infectious zeal was going around. In retrospect, it all seems a bit surreal or unreal, even though we all experienced and participated in it just a short time ago. What were we thinking? How could all this possibly have happened? For many investors and employees, much of it probably does seem like a bad dream. In each case, the new theories and new models for innovation promised much, yet disappointed—or even worse.

The World's Most Innovative Company

Remember, for example, when Enron was the innovation exemplar, the exalted leader of a new breed of corporate innovator? From 1996 through 2001, Fortune magazine had proclaimed Enron the "Most Innovative" company among all its Fortune 500 peers. Each year, Enron placed far ahead of even hi-tech powerhouses such as Intel, Microsoft, and Cisco Systems. Fortune explained, "If any Old World company could thrive in the Internet era, it's this one."

Enron was also featured as the new model for corporate innovation in innumerable consultants' how-to books, academics' business-school case studies, and business-media cover stories. Enron was an old-line company that had become a master of corporate transformation and radical innovation. It was "leading the revolution." Management gurus noted Enron's "almost magical mix of entrepreneurship inside with the ability to leverage enormous scale and discipline to get things done." It was successfully pioneering new ventures and entirely new industries, from energy trading to broadband to weather derivatives. In just a few short years, Enron soared from a sleepy gas-pipeline company to one of the largest companies in the world, with a play on almost every new business imaginable. One book published in 2001 boasted that, "[T]he Enron model was New Economy before the New Economy got started."

How did Enron manage to innovate so much so quickly and successfully? Its internal "wars for talent" and powerful rewards and incentives (e.g., generous awarding of phantom stock and options to new venture leaders) fueled creativity and ignited its high-octane brainpower. These novel human resource practices let it attract and retain top innovative talent for the most promising new ventures. Enron's liberating organizational structures (e.g., autonomous corporate venturing units, novel partnerships and alliance structures, carve-outs and spinouts) also were featured as another key innovation enabler. These nimble and flexible structures freed new ventures from the corporate bureaucracy, giving them unprece dented entrepreneurialism. Likewise, Enron's cutting-edge financing, valuation, and risk management techniques (e.g., "real-options" approaches and "mark-to-market" accounting) were featured as powerful leverage for innovation. This sophisticated financial engineering let Enron more aggressively fund and better value and vet new ventures. All these tools and tactics were featured as templates for other would-be corporate innovators to follow—or else be left behind.

Of course, in retrospect, all these factors were subsequently cited as precisely the key contributors to Enron's rapid collapse and massive bankruptcy. Enron was innovation out of control. Any accounting gimmicks were little more than a sideshow to cover up the true underlying problem—its failed innovation strategies, structures, and processes.[2]

Not-So-Disruptive Technologies

The startup world offered other innumerable examples of innovation mania. Few paused to doubt that the Internet was a pervasive "disruptive technology." The web changed all the rules and threatened to transform and disrupt almost every aspect of commerce. But the imminent threats to incumbent retailers looked like fantastic and certain opportunities for e-commerce upstarts.

Online grocer Webvan was one of the best-funded and best-staffed new business ventures in history, for example, and was equipped with all the latest and greatest technology. Its management and technical talent came from some of the biggest and best global information-technology companies. It was funded and advised by some of the most successful venture capitalists (VCs). Even after burning through $1 billion in capital, however, Webvan still could not figure out how to deliver a gallon of milk to customers' doorsteps efficiently, effectively, and profitably. Webvan went bankrupt and liquidated just two years after its founding. The number of other failed e-commerce ventures, some of them also spectacular flameouts in their own right (from eToys to Pets.com), is too long to list. Disruption came not to the incumbents, but to the upstarts.

Incubating Half-Baked Ideas

The explosion of the much-heralded incubator concept was another cause and symptom of the innovation craze. Incubators were neither typical corporate innovators, nor typical startups, nor were they simply financial investment vehicles like a venture capital fund. Instead, the incubators were a unique, New Economy hybrid designed to offer both the scale and scope advantages of a larger parent company along with the best nimble, flexible, and entrepreneurial features that startups had to offer. The incubators were a new organizational form made especially for the Innovation Age.

Incubators typically offered their incubees a wide variety of different types of service and support (for example, office space, lab space, IT resources, internal consulting, and other types of shared services). Moreover, by being part of a larger parent that could raise capital and trade as a publicly held company (something a fresh young startup could never do on its own), each of the incubees could get more ready access to preferential funding and, thus, a powerful financial head start. The concept of the incubator was to be an innovation enhancer—bettering the odds of success—as well as an innovation accelerator—powering ideas to market faster in an era in which speed mattered most.

Idealab, CMGI, ICG, and U.S. Technologies were among some of the better-known incubator names. They raised billions in capital because the concept just seemed to make perfect common sense. Combine the best of big and small: public company and startup. Provide seed capital and follow-on funding. Share services, support, and expertise among the incubees and thereby realize powerful synergies.

The Economist succinctly captured the tremendous allure of the incubator model:

The very notion of a business incubator is intoxicating. Just imagine a floor or two of buzzing proto-companies, bursting with potential, sharing space, services, and ideas under the tutelage of well-connected industry experts. The time, too, is right: an explosion of Internet startups needing help meets a chronic office-space shortage. No wonder the past year has seen the launch of more than 300 Internet incubators, two-thirds of them in America—a rate of six a week.[3]

Despite its compelling intuitive appeal, in practice, the concept did not work so well. The ambitious and newfangled incubator model seemed to offer little advantage over the more well-established and well-defined venture-capital approach. What's more, the complexities of the incubator concept—being neither pure investment vehicle, pure startup, nor a real operating company—brought into play all sorts of heightened costs and tensions. Complicated legal, financial, and organizational issues soon followed. Rather than being advantaged, member startups became crippled by their incubator affiliations. Lawsuits from investors alleged conflicts of interest or worse (e.g., Idealab, U.S. Technologies). Numerous incubators went bankrupt or simply closed up shop.

Remnants of the grand incubator concept survived, but in much less ambitious forms. Non-profit and university incubators continued, and even increased, their modest operations. But most of the for-profit incubators survived only by morphing into more traditional VC firms and much simplified financial-holding companies, or by trying to morph into workable businesses that offered basic office space and services to startups.

Reconsidering Innovations in Innovation

In the morning-after retrospective, as everyone sobered and surveyed the post-innovation wreckage around them, the mantra of "Innovate or die!" seemed a worn and unwelcome cliché. At business conferences and board meetings, innovation—at least anything beyond incremental change—became a hushed topic. Instead, it was back to the real business of business: retrenching and restructuring, focus and efficiency, watching cash and waiting for clear signals from the marketplace. The deliberative, suit-and-tie Organization Man was back in vogue. The frenetic and disheveled Silicon Valley dream merchant was disdainfully out of style.

Of course, the innovation enthusiasts had been at least partly right with their cry of "Innovate or die!" Especially in fast and dramatically changing business environments, failure to adapt definitely might threaten a company's continued success or even survival. But these one-sided cries ignored the other half of the delicately balanced innovation equation. Both "innovate and die" and "innovate or die" are very real risks. Deftly managing this precarious balance is critical. This is the key dilemma—and the core challenge—of innovation.

The Rise of the Innovation Industry

Innovation is a gamble. It offers potentially huge rewards, but concomitantly high risks. It increasingly requires big, up-front, largely irreversible investments in the uncertain hopes of distant returns. It involves hard-to-corral creativity, beyond-our-control serendipity, more than a few diversions, leaps of faith, and outright mistakes on the road from conception to commercialization. Companies big and small find themselves struggling with the myriad strategic, organizational, and financial challenges of innovation.

In response to these challenges, an entire innovation industry bloomed in recent years. Many different players promised and promoted their own solutions for the dilemmas of innovation. Depending upon whom you were to believe, your problems could be successfully tackled if only you understood and applied the current, novel "best practice." Such simple appeals made for clear and emphatic marketing messages, if not deeper understanding. Cure-all and one-size-fits-all solutions proliferated.

The innovation industry peaked as New Economy enthusiasm grew to fantastic heights. Likewise, each innovation fad and fashion deflated along with the rest of the technology and market bubble. There is danger in these deflated expectations, however. Because managers are now understandably quite cynical after hearing far too much innovation hype for far too long, the danger is that an entire field of potentially valuable and practically useful ideas lies fallow.

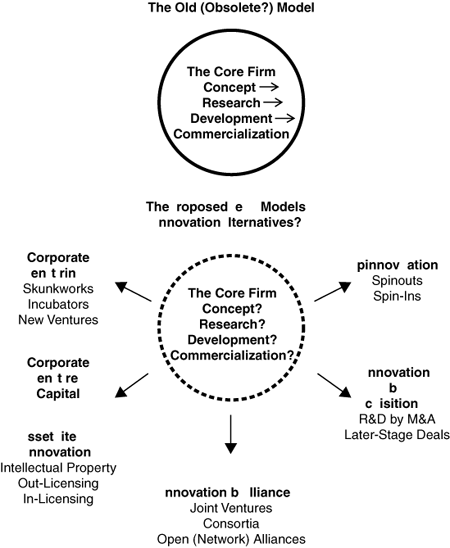

Innovations in Innovation

In our exploration of the innovation landscape, we focus less attention on those unstructured ideas that made pithy promises of supercharged creativity or profligate novelty. Whatever one thinks of these ideas and their promoters, they are difficult to analyze and critique because they offer anecdotes and affirmation more than balanced evidence and actionable recommendations. Instead, we focus on the more structured ideas that promised to power innovation to fruition, all the way from initial conception through full commercialization.

These innovative ideas include a large number and wide variety of different strategies and tactics. In this book, however, we focus on the most prevalent and important innovations in innovation. These strategic tools and organizational tactics include the following:

-

Corporate venturing, including corporate venture capital

-

Patenting and intellectual property licensing (asset-lite innovation)

-

Innovation by alliance

-

Innovation by acquisition

-

Spinouts and spin-ins (spinnovation)

As with all fads and fashions, something at the core of each of these "innovations in innovation" proved irresistibly appealing. As each of the latest and greatest innovation ideas splashed onto the scene, it was all too easy to get caught up in the excitement—whether it was to fund corporate venturing, aggressively patent or partner, to binge on acquisitions, or spin a spinout (see Figure 1-1). The market for management ideas is surely even less reasoned and objective than the fickle and gyrating financial markets themselves. As managers raced to adopt each new innovative idea that came in turn, the results most often were disappointing and disillusioning. In the aftermath, each idea lost its glow and the appeal of all the supposed innovations in innovation waned.

Figure 1-1. Seeking new innovation solutions.

Each of these approaches promised not abstractions, but rather more practical, tangible paths from invention to market: roadmaps for creating and capturing the value from innovation. Each approach offered a simple and appealing alternative model for innovation rather than a more complex menu of critical decisions and choices. In each case, one or two leading organizations were usually offered as exemplars for other companies to follow and imitate. Many managers did follow these examples and guidelines, often quite enthusiastically.

Bringing Silicon Valley Inside

With the rise of innovation enthusiasm, for example, corporate venturing quickly became an unqualified imperative. If your sclerotic, ossified Fortune 500 company were to have any hope of competing with young and aggressive entrepreneurial upstarts, corporate venturing was the answer. The idea was simple: Bring the youthful vigor of Silicon Valley inside your staid corporate bureaucracy—internalize the same excitement and energy, imagination and intellect, and motivation and incentives. Harness the power and principles of venture capital, the creative promise and possibilities of java-fueled skunkworks and incubators, and all the rest and best that intrapreneurship had to offer.

The goal was to stimulate the underutilized brainpower and capture the latent entrepreneurial energy of corporate employees who alternately had become too comfortable with, or too frustrated by, the old corporate bureaucracy and routines. Become a corporate venture capitalist, both figuratively and literally! Create autonomy and motivational rewards and set employees loose. Let them plant a bunch of real innovation options and watch as they grow. Then, prune the underperformers and nourish the healthy ones—just as in the hothouse, Darwinian world of venture capital–fueled entrepreneurship.

Many corporate venturing promoters went beyond recommending such simple intrapreneurship. They advocated stretching beyond the firm's own organizational and financial boundaries. Don't just act like a venture capitalist, literally be a venture capitalist. Use corporate cash to bankroll your own venture fund.

Especially by the late 1990s, more corporate executives began asking themselves, "Why should the Sand Hill Road VCs get all the glory and all the gains?" Instead, let's ourselves cast a wide net both inside and outside the company to capture new ideas with great strategic and financial promise—from whatever the source. Not Invented Here (NIH) became an asset, not a quandary. Let's fund them all, whether from inside or out, and manage the portfolio as would any sharp venture capitalist.

That was the theory, anyway. After a brief but intense splurge on such venture activities, even many of the more celebrated corporate venturing efforts were sharply curtailed or simply shut down after various dysfunctions, disappointments, and red ink ensued. Corporate venturing did not fulfill its promise; the venture imperative became the venture illusion. Even exemplars such as Lucent and Procter & Gamble either curbed or shut down their skunkworks and shut down or sold off most or all of their venture portfolios. The initial, uncritical enthusiasm for corporate venturing ignored the crucial fact that an established operating company is not—and probably should not try to be—either a venture capital firm or a de novo startup. It also became clear that successfully implementing corporate venturing activities requires careful balancing of numerous internal tensions and conflicts that venture capitalists and standalone startups simply do not have to deal with.

The mixed results of these corporate venturing experiments do not mean that there are no useful lessons for established companies to learn from the world of venture capital and startups. But whatever lessons might be gleaned from the VC mindset and a more general entrepreneurial perspective, successful and established operating companies must not abandon their strengths and, chasing after a dream, try to be something they are not designed for and can never be. Aggressive skunkworks and incubators often are not the right approaches for most companies; they do not offer innovation salvation and, in fact, tend to bring a host of new and serious challenges for a firm's core businesses. Corporate venturing would not be the establishment's innovation panacea, as many had hoped.

Spinnovation

Ironically, even as managers were urged to innovate internally far more aggressively, they were being advised by others that intrapreneurship was too limited an approach. Innovating outside the bounds of their existing organizations was an even quicker, more flexible, and richer innovation option. If there was a seeming contradiction in the concurrent popularity of these two ideas (internal venturing versus spinouts), it was lost in the excitement of the times. Spinouts became almost as hot a topic as corporate venturing.

As the Internet spawned proliferating dot-com startups in the late 1990s, for example, corporate executives were urgently advised that they could only hope to compete by taking radical action. They were advised to, literally, compete "outside the box," the "box" being their existing corporate structure. Established companies could spin out Internet versions of themselves and beat startups at their own game. The thinking was that the core established firms simply couldn't (or shouldn't) try to internalize the radically disruptive Internet. The old and new technologies, cultures, and business models were just too dissimilar. The entire hierarchy of the parent firm just didn't get it (whatever "it" was) and, therefore, was far too stodgy and slow to adapt.

Spin it out, however, and it was an entirely different ball game. This required setting up a new and separate organization, giving it a life and a label by attaching ".com" to the corporate moniker, and then (most importantly) spinning it out and setting it free. Only if it was loosed from the hierarchy and bureaucracy of its corporate parent, even as it leveraged the parent's brand and reputation, could a corporate dot-com be nimble enough to compete in the New Economy. The added bonus was that a spinout could tap into rich sources of new capital outside the corporate parent (including, perhaps, through a blockbuster IPO) to better fund expensive new ventures with less risk and yet greater upside.

With a spinout, the theory went, you could retain the advantages of corporate parenting even while giving the offspring increased freedom, focus, and funding of a truly independent entrepreneurial organization. Watch the spinout's value soar as its entrepreneurial energies are unleashed, and then capture your share of the value created through clever organizational, legal, and financial structuring. The list of corporate dot-com spinouts grew quickly as every old-line retailer pondered its future in the Internet age: Wal-Mart, Kmart, Toys R Us, Staples, and so on. Spinout excitement was not limited to cyberspace, either. In a variety of sectors, spinouts caught on quickly as a promising fast-track solution to innovation funding, organization, and commercialization.

Within a few years, however, the majority of technology boom spinouts clearly could not stand on their own terms. Many of them struggled to find their own workable business models and failed to gain traction in the marketplace. Most were spun back in or shut down, leaving a trail of less-than-stellar returns and legal and organizational messes in their wake. The problem was not just that they were dot-coms in a world where the Internet bubble had burst for everyone. Many of the non-Internet spinouts also met with disappointing fates. Again, exciting new innovation theory seemed to fizzle in practice.

The real explanation was more complex, of course. Spinouts can liberate and accelerate tremendous value creation from innovation. But they need to be done right, and for the right reasons. Spinouts are not the appropriate commercialization solution for every new patent, product, process, or channel. Choosing whether and when to spin out innovation, and mapping and executing exactly how, both require critical thinking.

Virtual Reality: Patenting, IP, and "Asset-Lite"

The asset-lite approach to innovation offered a pitch different from that of either corporate venturing or spinnovation. The pitch went something like this: Don't do it (innovation commercialization) either inside or outside. Don't do it at all. Go virtual. Let someone else do the heavy lifting. In the New Economy, intellectual property (IP) is where the real value resides. Build your company around IP assets, set up smart and aggressive legal and financial structures (e.g., patent and licensing deals), and the checks roll in. The lure of the IP licensing, asset-lite model was its contention that you don't have to actually do much of anything tangible—just own and control the key intellectual assets and related intangibles. Create a virtual company that rakes in the cash from licensing while minimizing real cash investment in rusty property, plant, and equipment in order to maximize return on assets.

Even if you were on the other side of the licensing equation (i.e., the licensee), the IP licensing model still seemed to make sense. You could reap the benefits of others' discoveries by minimizing your own R&D at risk and simply in-license their IP as needed instead. The virtual, asset-lite, IP licensing model seemed like a win-win for both sides.

The reality is that almost no companies were able to radically transform themselves or otherwise build a core foundation around an IP licensing model. Few firms have been able to build a sustainable and scalable innovation strategy centered around IP alone. Most pure IP-based companies, even those that do it profitably, remain small niche players. If raw IP alone were such a mother lode, after all, U.S. research universities would be swimming in royalties. They're not. Even in the heart of the hi-tech economy, the technology licensing receipts of the most elite tech universities constitute less than 1–2 percent of their total revenues.

The pure IP, asset-lite model has considerable limitations. By itself, raw IP has limited value. Knowledge might be power, but it doesn't deliver profits. The bulk of revenues and profits in any industry come from "doing," not just "knowing." Customers pay richly for solutions, not abstractions. Moreover, over the long term, it's difficult to separate knowing from doing. Without actually getting intimately involved in the details of commercialization and competition, it's difficult for an IP-only company to stay in the game—to innovate the next generation of technology and ideas. The bottom line is that improved exploitation of IP offers significant but typically marginal benefits at best, however rich they might seem in the abstract. On the other side of the equation—i.e., as an IP licensee—depending mostly on in-licensing of key innovations from others can leave a company vulnerable to major, unforeseen costs, constraints, and uncertainties.

Both in-licensing and out-licensing therefore require careful strategic and financial consideration. An aggressive and structured IP plan is a necessary complement to, but not a substitute for, a more comprehensive innovation strategy. In the vast majority of cases, an asset-lite IP-based innovation strategy alone simply won't do the heavy lifting that's required to create and capture most of the potential profits of innovation.

Shared Creation

Some companies thought it would be best to simply share the costs and risks of innovation. The appeal of innovation collaboration led to a proliferation of R&D and commercialization alliances. The logic of innovation alliances was intuitively attractive: Two heads are better than one, and even more heads are better yet. Share the risks and investments while bringing together different sets of complementary knowledge, resources, and capabilities. In turn, reduce overall development expenses, speed time to market, and help more favorably influence and dominate the industry environment. Create a win-win for all the partners involved.

The advantages of innovation alliances often are illusory, however. Their record is weak in many areas. Remember Iridium? Iridium was the global, Motorola-led alliance designed to revolutionize global mobile telecommunications. The technology and investment consortium included high-profile partners and investors from every sphere of high-tech and from countries all around the world. But Iridium filed for bankruptcy in a spectacular, multibillion-dollar flameout in 1999, just a few months after launching service. Meanwhile, more nimble and focused competitors leapfrogged Iridium with simpler and cheaper solutions. The combined innovative power of many, even formidable organizations, is sometimes less than the power of one.

Even successful innovation alliances might not necessarily translate into profits. Most people would agree that Linux, for example, has been a successful software consortium. The catch is that Linux's great success as an innovation alliance is precisely a function of its relatively free and open nature. This, of course, is exactly the conundrum for those hoping to richly profit from it. Open alliances can be great for generating and commercializing innovation, but are not necessarily very profitable for many of the players involved.

Without a doubt, innovation alliances are often essential. But they carry with them many inherent tensions and challenges. Instead of speeding development, they are often slow and cumbersome. Instead of reducing the costs and risks of innovation, alliances can often increase costs, risks, and complexities. Innovation alliances sound ideal in concept. In reality, they inevitably introduce new issues that beg to be shrewdly planned for and smartly executed for the partnership to flourish rather than fail.

If You Can't Build It, Buy It

In the deal-driven climate of the late 1990s, a different and novel approach toward innovation gained great currency. Don't ally, buy! The basic idea: If you can't build it, buy it. Frothy financial markets fueled more technology deals than ever in terms of both total number and total value. Why waste all that time, money, and effort to do the dirty work of R&D yourself? Let others shed the blood, sweat, and tears, spend the cash, take the risks, and make the mistakes. Then, pick and choose and simply acquire one of the winners.

Cisco Systems was the model to emulate. As others tried to imitate Cisco, rushed and inflated bids for hot technology companies soon turned into record-setting, mind-numbing write-offs totaling hundreds of billions of dollars. JDS Uniphase alone wrote off more than $50 billion (as one observer noted, equivalent to the entire GDP of New Zealand). After acquirers spent huge sums, the technologies or markets frequently turned out to be much less feasible or attractive than advertised. Other companies found themselves holding expensive, hollow shells of companies as the targeted intellectual capital of the acquired firm simply walked out the door right after the deal closed. Entire acquisitions were liquidated for a single-percentage fraction of their purchase price or, in some cases, just completely shuttered.

Innovation by acquisition can pay off, but it's a bet that comes with a price. This price includes both the actual premium for the acquisition and all the difficulties and uncertainties of trying to successfully evaluate and integrate the target—its people, culture, technologies, customers, and more. Technology and markets can change rapidly, which can quickly outdate an expensive, big-move acquisition. Furthermore, there's no guarantee that the exact piece of R&D you need will be developed by another firm at all, that it will be on the market at the right time and at the right price, or that it won't already be snatched up by someone quicker and richer. Undue reliance on innovation by acquisition is a very risky bet.

Mixed Results: What Exactly Is It?

The saga of Andiamo Systems illustrates well the organizational twists and financial contortions that companies were willing to endure to the end of innovation. Silicon Valley–based Andiamo was founded in January 2001. The company developed intelligent data switches that enabled many disparate storage systems to communicate and unify as one. Most people had probably never even heard of Andiamo before Cisco Systems acquired it for $750 million in February 2004. This was not a typical Cisco acquisition.

It's complicated. The Andiamo transaction represented the culmination of a significant venture investment and ongoing alliance between Cisco Systems and Andiamo. Cisco already owned 44 percent of Andiamo at the time of the acquisition. Moreover, Cisco had been Andiamo's sole venture funder; Cisco initially had loaned the startup $42 million and subsequently agreed to provide additional funding of $142 million.

For these funds, Cisco had bought the rights to acquire the portion of Andiamo that it did not already own, at some future date. The purchase price might be as much as $2.5 billion in stock, depending on the success of Andiamo's technology and revenues. The acquisition agreement was also cleverly structured to vary along with Cisco's own market capitalization and revenue so as to minimize any potential impact on Cisco's financials.

Beyond the technology and cash, Cisco otherwise had strong connections with Andiamo. In an unusual arrangement, Andiamo and most of its 300-plus employees (many on leave from Cisco) worked in Cisco buildings on Cisco's main San Jose campus. Under various agreements with Andiamo, Cisco was the exclusive manufacturer and distributor of all Andiamo products. Cisco had even been expensing its cash investments in Andiamo as ongoing R&D costs since its original infusion in 2001.

It was a strong and close partnership. Many of the complexities of the relationship were revealed only after accounting rule changes in 2002 required Cisco to more fully disclose its various linkages with Andiamo. It was such a close partnership, in fact, that new SEC rules required Cisco to account for Andiamo as if it had consolidated the company since its initial investment in 2001.

A bit of background is useful to understand these novel arrangements. Prior to the founding of Andiamo in 2001, much of the start-up's top management, including CEO Buck Gee, had been Cisco executives. In fact, founding Andiamo was largely their idea, even while still working for Cisco. They also eventually ended up the primary holders of the 56 percent of Andiamo's equity that Cisco did not own. In fact, other than Cisco, Andiamo employees were the only other equity holders. In turn, many of them returned to roles as Cisco executives after the acquisition deal closed. By the time the acquisition was finalized, Cisco hinted that Andiamo's core market and revenues had both been disappointing. Nonetheless, in cashing out their equity stakes, many Andiamo employees effectively received a rich signing bonus for returning to their "former" employer. Of course, "returned" is also a curious term in this case; after all, they never left Cisco's main campus.

Cisco's Andiamo exercise is a fitting example of how far companies were willing to go in pursuit of innovation. Andiamo combined a bit of corporate venturing and corporate venture capital with the concept of the spinout—in spirit, anyway, even if it never actually left the premises. Cisco and Andiamo tied it all together with an ongoing, on-site R&D and manufacturing alliance. Finally, they finished it all with a spin-in acquisition. Companies were willing to try extraordinary things in order to foster and procure new ideas and new technologies.

The Allure of Innovations in Innovation

The question remains: Why did so many good managers chase after what, at least in retrospect, seem to have been so many questionable ideas? Why did so many great companies pursue with abandon each of the latest and greatest innovation fads and fashions? Whatever their flaws in practice, there were at least three key reasons why all these "innovations in innovation" gained so much interest and momentum.

First, and most simply, innovation really had become more important than ever. It wasn't just a slogan or empty words. Heightened global competition meant that established industry leaders were pressured to generate new low-cost ways to compete or ever-more differentiated products and services to preserve their margins. Product lifecycles had accelerated, meaning "new and improved" had to come more often. Paradigm-shifting scientific breakthroughs in computing, communications, and life sciences, among other areas, started to transform the fundamental processes and products of invention in key industries. Radical new technologies threatened to upset existing business models and alter fundamental industry economics. The pressure for greater and faster innovation became a more central fact of business life. Each innovation fad and fashion, in turn, flourished as companies anxiously sought new and improved means to this end.

The second reason each idea proved so appealing is simply because the old model for innovation sputtered; it was no longer working. Everyone knew it. Everyone felt it. It was on the front page of the paper every day. The classic, brand-name, established success stories of yesteryear—truly original and enormously successful innovators in their own right and time—seriously stumbled. R&D labs that had been the envy of their global peers simply no longer produced. From IBM to GM, from AT&T to P&G, the products and services of former technology and market leaders appeared to grow ever-more stale and tired. It seemed like almost every blue-chip company was either reeling from slumping sales or was threatened by some new upstart. Established companies wanted to escape their musty legacies. They needed renewal. Corporations sought a new model for innovation, especially an alternative to their traditional and bureaucratic R&D approach.

The third reason all these innovation fads and fashions proved so alluring is because each really did offer some novel and valuable contribution. Unfortunately, the limitations and qualifications of each approach usually garnered a footnote at best. Executives and entrepreneurs consequently rushed to adopt each new tool or tactic with few inhibitions. Little thought was given to the critical details of application (when, why) or execution (exactly how). Despite these difficulties in application and execution, each concept did offer some fresh and useful new thinking. They were all useful additions to the innovation toolbox. As with any tools, however, their effectiveness depends on the judgment and skill with which they are used.

Mixing and Matching Tools and Tactics

Our intent, therefore, is not to debunk or discard any of these approaches to innovation. Indeed, our goal is to help rescue the good ideas from being needlessly discarded. Just as there are value stocks, there are value ideas. Value stocks get their value precisely because they are out of favor, yet they retain substantial, enduring intrinsic worth. Likewise, we believe all these innovation tools and tactics, despite having lost their initial luster, offer real, lasting, and essential advances in thinking about innovation.

However, none is the singular solution so often hoped for. No one approach can ever be a one-size-fits-all or cure-all solution for the variety of innovation problems confronting different firms in very different circumstances. Even a single given firm typically is a diverse portfolio of ventures, in different industries and at different stages of their respective lifecycles. Yet, what most often has been prescribed are universal templates extrapolated from a single anecdote or idiosyncratic exemplar company. Managing innovation frequently became driven by the pursuit of some superlative best practice, without considering the context and limitations of the particular approach. If everything could be reduced to a simple formula, innovation would be unremarkable and routine. It's clearly not.

Our practical approach is that context and contingencies matter. Antibiotics are great for fighting bacteria, but they won't do anything to kill the common cold virus. A glass or two of wine per day might improve your health and extend your life span, but binge drinking most certainly has the opposite effect. Innovation fads and fashions tended to ignore such judgment, selectivity, and balance.

What's more, each of these innovation prescriptions had a core problem. They tended to address superficial symptoms instead of underlying causes. The patient was left temporarily feeling better even as his fundamental health deteriorated. Future chapters discuss this critical core problem in greater depth and detail. It is a central issue for diagnosing what went wrong with the application and execution of each new idea, and for building and implementing a better model for innovation.

Innovation is a strategic and organizational problem as much as a technical or creative one. This is another key lesson of the past few years, and a central message of this book: The how matters as much as the what. Even Enron and Webvan had some good ideas. But their timing and execution certainly lacked. The message is that how a company chooses to pursue innovation has profound implications for its success. The choice of strategy and organization (e.g., venturing or spinout, alliance or acquisition, etc.), and its execution, determine whether a good idea flourishes or fails as much as the inherent worth of the idea itself. The how determines whether questionable ventures get terminated in good time and good order, or are instead allowed to swell to become enormous boondoggles. Quite simply, success or failure depends on exactly how a company chooses to pursue innovation as much as on the basic idea or invention itself.

Venturing, licensing, alliances, acquisitions, and spinouts therefore all have critical roles in the innovation mix. Knowing when and how each has its place in the mix and when and how to implement each is the critical knowledge. Learning from the ups and downs of each innovation idea requires more critical thinking about when and how these models apply and—just as importantly—when and how they do not. Applied for the right purposes, at the right time, and in the right ways, all of these tools and tactics can help build a more comprehensive innovation strategy and robust overall innovation portfolio. Rather than chasing the latest "magic bullet" or panacea, managers must understand all the different tools available in their innovation arsenal, when and how to use them, and how to combine all of them for maximum effect. The end game is to be able to assemble and juggle a more dynamically optimal mix of all these innovation options to create and capture value on an ongoing basis.

Much like assembling a good investment portfolio, superior performance does not come from any single innovation approach. Instead, the enduring worth—a successful, sustainable, value-creating company—comes from assembling and managing the complex and evolving mix of tools and tactics necessary to bring innovation to fruition. This is a critical feature of new and emerging models for innovation, a subject to which we return in the final chapter.

Background and Overview

A considerable amount of background research informs the examples, conclusions, and recommendations in each chapter. Cumulatively, we examined in detail the record of more than 100 corporate venturing and corporate venture capital programs, more than 100 innovation-driven acquisitions and alliances, and more than 50 licensing deals and spinouts each. We explored a diverse range of examples, of organizations of different sizes and from varied industries, during the 5-year period from the end of 1998 through the end of 2003. Innovation enthusiasm began to bubble by the beginning of this time frame. In many different media, new innovation models were being proposed and then implemented; innovation exemplars were featured and then imitated. Myriad experiments were launched. The choice of a 5-year window was necessary to examine these cases with sufficient richness: to examine their internal and external dynamics and their initial performance, their evolution and ultimate outcomes. A longitudinal examination was necessary to get a better sense of what worked, what did not, and why—i.e., what deeper lessons might be learned.

Except where otherwise cited, our data primarily comes from first-hand sources: conversations and interviews with company founders, executives and former executives, investors and partners, internal company memos and documents, press releases, formal filings, and so on. During the research process, we also reviewed the available innovation literature to better highlight and explore prevailing theories and examples. Where secondary sources are used for more in-depth support or detail, they are cited accordingly.

Here's the typical pattern: A new "innovation in innovation" was announced with great fanfare and introduced with great hopes and expectations. Exemplar companies were recommended as models and used as templates. Sooner rather than later, however, the results of these innovation experiments tended to be far less than satisfactory, and much less exemplary. Even when many of these innovations did succeed in a narrow, short-term sense, they often did surprisingly little for their parent companies from a broader, long-term perspective. The innovation initiatives then tended to be quietly "back-burnered," shut down, or sold off. Retrenchment followed and the cycle soon began again. Meanwhile, the parent organization's core innovation typically suffered and overall performance deteriorated. It's a fundamental and important question: Why do so many supposed "best practices" in innovation so often disappoint? Why does innovation "best practice" so often not work out well in practice?

Some of the individual cases we discuss could fill an entire book. In fact, a few of the examples have been the focus of one or more books. Although such in-depth case studies have obvious benefits, their limitations are also notable. Readers might be left wondering: Is this particular case, however rich and in-depth, the exception or the rule? How and why (or not) does any of this apply to my company and my industry? Were the outcomes simply the result of good (or bad) luck, or is there something more here? In fact, much of the problem with innovation fads and fashions was exactly that—idiosyncratic, exceptional cases were used to extrapolate rules and recommendations for a wide variety of firms, big and small, in myriad industries and situations. They were not designed to engender critical thinking.

This intentionally is not our approach. In covering so much territory, it is impossible to thoroughly delve into each example. In each chapter, therefore, we try to focus on the most important details, the critical variables and their effects, and major conclusions and recommendations. Our intent is to engage in critical analysis that helps lay a better foundation for managers' own strategic thinking and bottom-line approaches toward innovation. For the sake of brevity and clarity, each chapter especially focuses on analyzing in greater detail some of the most celebrated exemplars of each innovation idea. More critically revisiting these examples invariably generates interesting and useful postscripts and more complex but constructive lessons to learn. In most cases, the exemplars themselves were already struggling with their own novel approaches toward innovation, even as many other companies were only just beginning to be advised to mimic them.

Each chapter ends with a summary of key lessons learned based on our broad overview of each innovation in innovation. In the concluding chapter, we tie together all these lessons to help advance a new model for innovation—one that is more nuanced and complex, but also better-grounded and more durable.